At Least One Firm is Leaving New York before Disclosure Law Lands

April 29, 2021 New York MCA firms are in the dark. In January, the governor delayed implementation of the APR disclosure bill until 2022. But the bill leaves it to the Department of Financial Services (DFS) to finalize how it will all work and not everyone is confident the outcome will be positive for business in New York State.

New York MCA firms are in the dark. In January, the governor delayed implementation of the APR disclosure bill until 2022. But the bill leaves it to the Department of Financial Services (DFS) to finalize how it will all work and not everyone is confident the outcome will be positive for business in New York State.

For example, Greenwich Capital, a small business funding company, has decided to move from Manhattan to Hoboken, NJ in preparation for the law. They anticipate that the cost of compliance will be high enough to warrant a trip on the PATH starting now rather than when it may be too late to contemplate later.

“There’s a lot of ambiguity, and our five-year lease was up,” Rich Gipstein, General Counsel at Greenwich Capital, said. “We’ll be moving to Hoboken for the time being and see what’s going on with this law. But in the meantime, it’s a lot cheaper for us.”

Based on vague wording language like double-dipping, Gipstein said there is no clear way to tell who or what the law aims to regulate. At least for his firm, it’s better to sit this one out.

“I think there’s quite a lot left open, and it’s intended to be broad,” Gipstein said. “There won’t necessarily be much time to know what the law means until it’s effective. I think there will probably be some lead time, but likely not quite enough for most businesses in the industry to adapt.”

For example: when does a deal become a “specific offer” and come under the purview of the law? In an industry where deals are won through cold calling, social media blitzes, and emails, when would it become necessary to disclose an APR? In a DM on LinkedIn? Rich said it is unclear what a “provider” is, whether it be funders, brokers, or ISOs. In the bill, a provider is required to make commercial financing disclosure clear and let a recipient know at the time of the “specific offer” the all-inclusive rates of a product. Without clarity, it’s hard to predict what the cost of compliance will be.

For example: when does a deal become a “specific offer” and come under the purview of the law? In an industry where deals are won through cold calling, social media blitzes, and emails, when would it become necessary to disclose an APR? In a DM on LinkedIn? Rich said it is unclear what a “provider” is, whether it be funders, brokers, or ISOs. In the bill, a provider is required to make commercial financing disclosure clear and let a recipient know at the time of the “specific offer” the all-inclusive rates of a product. Without clarity, it’s hard to predict what the cost of compliance will be.

“I think, from my reading of it and from my understanding of New York’s position, it would seem that they are trying to regulate both funders and brokers under the same regulation,” Gipstein said. “I think it’s possible that the legislature intentionally left some things vague for DFS to fill in. The law basically says, ‘there’ll be regulations that will make this make sense.'”

Gipstein said it’s common for politicians to leave it to the regulators to finish the job, after all, the DFS has its nose to the grindstone in the day-to-day. But when a law affects an entire industry like this, Gipstein said it is uncommon for changes to be left until the last moment.

“It’s more than just disclosure requirements; this is not similar to what California did,” Gipstein said. “The law also dictates how to calculate the projected sales volume. You’re required to either use the historical method, in which you must always use the same number of months leading up to the deal, or you can opt-out and use your own projection. But if you use your own projection, that opens you up to disclose the results of all your deals to the government… It’s almost like an annual audit.”

The historic method doesn’t really work, Rich said when the industry comprises atypical merchants who wouldn’t be looking for funding if traditional methods could predict their sales volume. When it comes to self-declaring and letting the government poke around: Gipstein said the way a funder evaluates deals is proprietary. It’s what sets them apart; it’s the value proposition.

Greenwich Capital isn’t alone in their assessment. The Small Business Finance Association (SBFA), a trade group comprised of similar financial companies, has also been vocal about the law’s perceived shortcomings.

Greenwich Capital isn’t alone in their assessment. The Small Business Finance Association (SBFA), a trade group comprised of similar financial companies, has also been vocal about the law’s perceived shortcomings.

“You have a group of companies that are pushing these types of disclosures, for no reason other than their own self-interest,” said Steve Denis, executive director of the SBFA, back in October. “We’re fine with disclosure, we are all for transparency, but it needs to be done in a way that we believe is meaningful to small business owners.”

Denis had further said that those firms taking credit for writing the laws are the same companies that will end up suffering under the strict tolerance of an APR rule.

“The companies pushing this, the trade associations pushing it, they like to take credit for writing the bill in California and writing the bill in New York: I don’t even think they’ve read it,” Denis said at the time. “It’s going to subject their own members to potentially millions if not hundreds of millions of dollars in potential liability [fines.]”

When the DFS finalizes the terms, it will likely make dealing with disclosure too costly to remain in New York State, Gipstein said.

Gipstein said we’ll have to wait and see if NY-based brokers will have to go through extra compliance even if their funders or merchants are out of state. The worst-fear scenario is a possibility that after New Years’ 2022, out-of-state funders will stop working with NY brokers entirely, just because they live in NY. Merchants in the state, subject to the law, may find commercial finance a barren marketplace.

“We’ve got a lot of different things to manage as we grow, and one of the things we don’t want to do is create is a large compliance department,” Gipstein said. “It’s just cheaper for us, after doing a cost-benefit analysis, to move to a different state. We’re probably not going to be a New York funder by 2022.”

Move Over PPP, There’s a New Gov Grant in Town

April 23, 2021 We’ve heard rumblings of funding slowdowns because of competition from Uncle Sams’s emergency stimulus programs. But a soon-to-launch grant specifically targeting restaurants, food, and alcohol services may put PPP to shame.

We’ve heard rumblings of funding slowdowns because of competition from Uncle Sams’s emergency stimulus programs. But a soon-to-launch grant specifically targeting restaurants, food, and alcohol services may put PPP to shame.

The $1.9 trillion American Rescue plan signed last month set aside $28.6 billion toward the Restaurant Revitalization Fund. Just like PPP, the fund will dole out refundable grants up to $10 million to the most hard-hit food-related businesses.

Since PPP funds tend to run out quickly, the SBA apportioned $500 million just for merchants with less than $50,000 gross receipts in 2019. $4 billion will be set aside for the $50k- $500k bracket and $4 billion toward the $500k- $1 million bracket.

During the first 21 days of the program, the SBA will also focus efforts on disadvantaged businesses controlled by veterans, women, or those that suffer bias due to race or ethnic prejudice.

Just as in the PPP program, eligible businesses will have to devote the grant toward business expenses. That means payroll, loan financing, utilities, supplier, and equipment costs. Only companies that have survived the pandemic thus far with a physical location are eligible. The stipulations forbid a recipient to use funds to open a new venue.

Recipients will have to spend the money before the SBA end date, possibly December 2021 or later, or they will have to return the funds. The program is not live yet, but rumor has it will be opening in late April.

Can’t Wait For An Inheritance? Someone Will Fund You

April 19, 2021 Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

For some, the aftermath of losing a loved one can turn into a long drawn out legal process and delay the transfer of rightfully owed inheritance in the process. Probate funders fix the problem, paying cash upfront, purchasing the future receivable of a will. The small industry is remarkably similar to the merchant cash advance world and uses the same terminology. “Inheritance Cash Advances are not loans,” one website says, “with an Inheritance Cash Advance, we send immediate cash to heirs in exchange for an assignment of a fixed dollar amount of their eventual inheritance.”

David Horton, a University of California-Davis law professor who delved into 1,119 probate agreements in the San Francisco area as part of a UPenn Study, said of the product “in almost all cases, with rare exceptions, the lender not only gets their advance back but also gets a huge markup.”

Interestingly, this type of funding is most popular in California, where some of the most complicated estate laws in the country make inheriting a hassle. But a less than flattering industry profile in Consumer Reports says that such companies “earn millions offering cash advances to heirs, with effective interest rates as high as 490 percent.”

And yet, industry advocates say that they are providing a needed service. “We are proud of the service we provide and the highest ethical way we conduct our business at IFC,” said Doug Lloyd, CEO of Inheritance Funding Company to Consumer Reports. “It is easy to understand why banks and other financial institutions are not in this business.”

His company has already advanced more than $200 million to customers. The following video is featured on their website:

Selling Finance Door-to-Door During Covid

April 9, 2021 This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

This week, lockdown returned to Ontario, Canada, due to the third wave of Covid cases. On April 3rd, the Premier issued a stay-at-home order, putting 14 million Canadians back behind closed doors. Based in Ontario, Canadian Financial is a one-stop alternative and traditional funding shop that still champions door-to-door sales and the lockdown has sidelined them for the third time.

“We just went back into lockdown. The whole province, everything just shut down,” CEO Patrick Labreche said. “We were getting 20 to 30 new cases a day, and then it jumped to like 200 a day.”

Meanwhile, 110 miles down south at AltFinanceDaily, de Blasio announced NYC public beaches would be opening up by Memorial Day. Because of the wide range of government shutdowns this past year, Labreche said it is hard to admit to some that his business is booming.

“I was having a conversation with a guy who does payment processing, he makes residuals on his customers, and so his book of business was not making any money right now; he’s hurting,” Labreche said. “So it’s kind of hard to tell a guy like that that we’re flourishing, and maybe you should come work with us.”

Labreche said that the processor was actually going to work with Canadian Financial. Success this past year came from leveraging the interpersonal skills that make an excellent door-to-door salesperson thrive, Labreche said.

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

“I started in the door-to-door and b2b at 19 years old, completely broke. I dropped out of school, and I started knocking on doors, and you know, that business model has changed my entire life,” Labreche said. “When you get into door-to-door sales, you understand how to sell yourself first. You get a sense of how to communicate with people, how to understand their needs, their pain points: How to leverage the service or product that you have.”

With a team of salespeople connected through weekly department meetings and messaging groups to keep the energy up, the deals kept rolling in throughout covid. Labreche said his firm is set apart from a good portion of Canadian alt finance: they offer a smorgasbord of financial products directly to the borrower instead of using lead generators.

While most fintechs think all business owners want a one-button final product, Labreche attests to the opposite- his firm sends out salespeople to make sure businesses know they have a rep to rely on.

“I have nothing bad to say about aggregators; that’s their business model, not ours,” Labreche said. “Our business model is going into a business that didn’t even know that the solution was available. When you’re looking online, you’re looking for a solution that you already know is available.”

Labreche favors traditional finance. His firm offers MCAs and other alternative forms of funding but said those are mostly band-aid solutions and he regularly sees MCA deals taking advantage of merchants. For example, Labreche said he walked into an ESCO gas station last month, and through talking to the owner, discovered an opportunity. The owner had taken an MCA from a big Canadian firm but was confused about the cost of capital- he thought he was paying 17%, but Labreche read a recent statement and discovered the rate was really 50%.

“Right there and then he was like, ‘oh my God, that’s crazy I didn’t know,’ he was misled, and it’s like that across the board. So I ended up getting him a quarter-million dollars at four and a half percent on a term loan,” Labreche said. “Nobody’s ever walked into his business or called him, offering him traditional money. We feel like there’s a huge underserved, undereducated market.”

This week, walk-ins have become less of a possibility, with a lockdown banning all non-essential travel. Still, business development manager Julian Hulan looked forward to when things would open back up. He had masked up and gone out on sales calls throughout the year when the government wasn’t in shutdown mode. Recently he traveled to 20 car dealerships to offer financing in a two-day period and said he found merchants excited to see him in person instead of over email.

“They were like ‘oh, I can actually sit down and talk to this guy?’ and that’s when they eat it up,” Hulan said. “They know because they’ve already made that connection face to face, they can call me directly. We don’t do this whole 1-800 Number. You’re going to call me directly and if I don’t answer, you leave me a voicemail, I call you back, it’s that personal relationship between me and that client.”

IOU Financial Funded $12.1M in March

April 8, 2021 IOU Financial originated $12.1M in funding to small businesses last month, the company revealed. It was IOU’s biggest loan volume month since the beginning of the pandemic.

IOU Financial originated $12.1M in funding to small businesses last month, the company revealed. It was IOU’s biggest loan volume month since the beginning of the pandemic.

The figure was included in an announcement regarding the company’s intention to repurchase up to $2M of Convertible Debentures.

“The move to repurchase corporate debt comes after a year of strategic initiatives as part of IOU’s Pandemic Resilience Plan that focused on reducing corporate expenses while reaffirming commitments from its diverse portfolio of funding sources and capitalizing on new opportunities to continue to support small businesses in 2020,” IOU said.

“IOU’s response to the COVID-19 pandemic in 2020 (‘Pandemic Resilience Plan’) put the Company in a position of strength to consolidate its stake in developing the opportunities ahead,” said Phil Marleau, CEO. “We are proud to be able to stand with our network of brokers and small business owners as we prepare for the economic recovery with great optimism.”

Before the pandemic, IOU originated $154M in funding for all of 2019.

PPP Deadline Extended, Jobs Act Proposed

April 1, 2021 President Biden signed a law extending PPP lending until May 31st. The PPP Extension Act passed through Congress on March 25th and will allow businesses to access emergency loans past the original March 31st deadline.

President Biden signed a law extending PPP lending until May 31st. The PPP Extension Act passed through Congress on March 25th and will allow businesses to access emergency loans past the original March 31st deadline.

According to the PPP loans tracker, as of 3/21 the SBA has disbursed $718 billion of the $806 billion available, leaving $88 Billion left for funding. Businesses will be able to apply until the new deadline, and the SBA will be able to process applications until the end of June. The new filing deadline gives the SBA some breathing room to review the 234,000 applications currently in the queue.

Biden signed it a day after unavailing a $2 trillion American jobs and infrastructure plan, aimed at revitalizing roads, bridges, and protecting the environment. The money is split into a cross-section of infrastructure, subsidies, like $100 billion toward bringing broadband internet to 30 million Americans, $50 billion toward semiconductor research, and $174 billion toward electric car manufacturing.

Not every spending point is for future tech. There are lump sums for healthcare, like $400 billion for long-term elderly care, and $30 billion for pandemic preparedness.

Biden has said he plans to pay for the expenses through the Made In America corporate tax plan raising the corporate tax rate from 21% to 28% after President Trump leveled the tax from 35%.

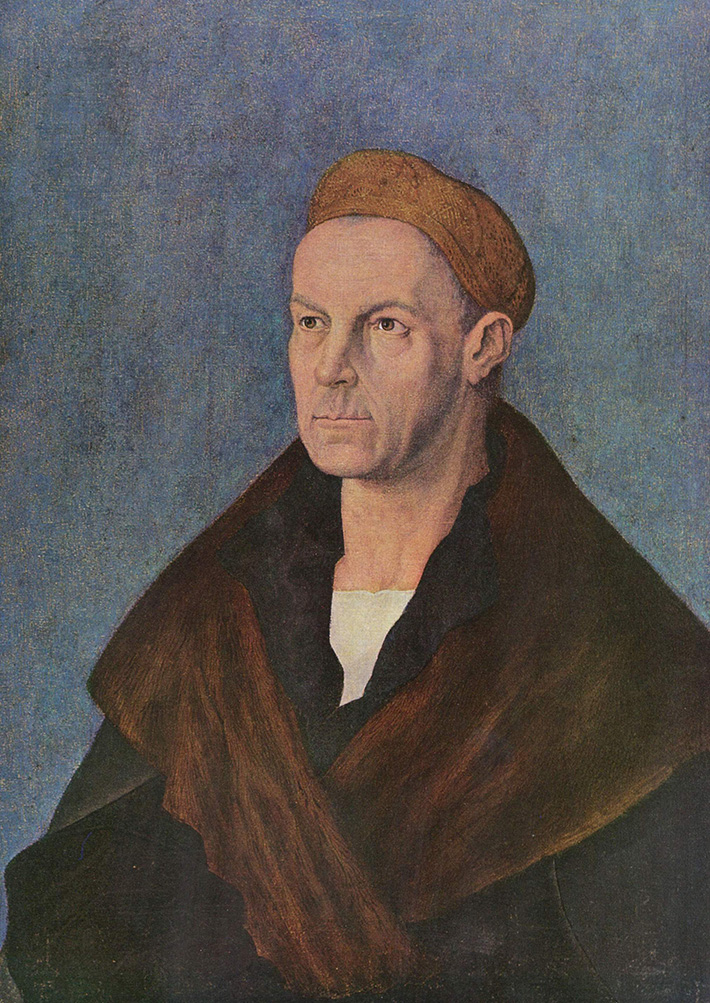

Merchant Cash Advance is as Old as The Renaissance

March 21, 2021 The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

In Jakob Fugger the Rich, historian Jakob Strieder writes the Fugger enterprise began as one of the upstart merchant families of the Renaissance. The Fuggers were traders and cloth merchants from Augsburg, Germany. They created a network of aristocratic clients, furnishing weddings and parties through trading warehouses in modern-day Venice, Florence, and Austria. Jakob Fugger I lent some money around, but when Jakob Fugger II joined the family shipping warehouse in Venice, he looked for a better return on capital.

According to International Business History: A Contextual and Case Approach, Fugger entered an agreement to supply some cash- 23,627 Florins to a silver mine owned by Archduke Siegmund in 1487.

Siegmund had plenty of silver laying around for collateral; he just needed cash for the day-to-day. It was a collateral-backed loan, common today: if he couldn’t pay it back, the Fuggers would get paid in silver. The transaction worked so well that a year later, Siegmund reapplied, this time in a revolutionary way. Siegmund would get 150,000 florins, and the Fuggers would get paid the future receivables of the silver mine: unrefined and cheap future silver for cash now.

The problem, written by historian Greg Steinmetz in The Richest Man Who Ever Lived, was the Church. Any interest-based transaction was specifically outlawed, though there were hundreds of lenders during this era. The line from Luke 6:35, “Lend and expect nothing in return,” was taken by the Church to mean an outright ban on usury, defined as the demand for any interest at all.

Even savings accounts were considered sinful, but Venetians ignored these rules as they preferred making money to pleasing God, entombed in the motto “First Venetians, then Christians.” Fugger began accepting deposits like a bank to his clients, with a 5% return to investors.

But convicted usurers could be excommunicated and denied a Christian burial, a nightmare for a capitalist who relied on a Christian network. Fugger did not worry about punishment or the apparent sin of money lending, but as he became a fixture in European society, his reputation became increasingly vulnerable.

Fugger needed the laws to be changed, or at least relaxed, or his lending business was in trouble. In 1515, he wrote a letter to Pope Leo X and funded a debate in the St. Petronius Basilica in Bologna. The debate ran for five hours, a back and forth of philosophy, scripture, and rampant crowd heckling. In the end, it was declared a tie, but Pope Leo X that year signed a papal “bull” reforming the concept of usury.

Originally, the Church pointed to the philosopher Aristotle’s model for determining what was okay to charge for and what wasn’t. Aristotle had said that charging someone for a cow because it produced milk was fine, but money was a dead thing and unfair to profit from.

A silver mine produced silver and as such paying cash for the future proceeds of the mine had allowed Fugger to more or less carry on his business. It wasn’t called merchant cash advance back then but he applied that model wherever he could. Not everyone in need of money had a business, however, and it was critical that he be allowed to charge interest when circumstances called for it.

More than a millennium after Aristotle, Pope Leo X found that risk and labor involved with safeguarding capital made money lending a living thing. As long as a loan involved labor, cost, or risk, it was in the clear. This opened a flood of church-legal lending: Fugger’s lobbying paid off with a fortune.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

McCarthy wrote: That was one of the problems with the Fugger model- “how does one take possession of Austria or France or Spain when its rulers default or lag behind debt repayment schedules?”

After gaining the good faith to lend in the Church’s eyes, the papacy itself became a Fugger customer. Positions in the Church were inseparable from social and political power, and the only way to get a place on the totem pole was by paying for a title. Just as the richest silver mine owners didn’t have the cash to pay for lunch- so did wealthy aristocrats need capital to afford positions in the cloth.

By the time Martin Luther “nailed” his 95 theses to the door of a church in 1517, he was rallying against the Fugger funding family and its stranglehold on the Roman Catholic Church.

It all came down to an in-house promotion. Albert Brandenburg brought a whole new meaning to the concept of “moneychangers in the temple.” A German Archbishop of Magdeburg, Brandenburg was promoted to Elector of Mainz: the second in command of the Holy Roman Empire. Unfortunately, he had to pony up 21,000 ducats to pay the Roman Curia (the Church’s admin)- for the title. Naturally, he didn’t have the cash, and the Fuggers stepped in.

Brandenburg got a loan on interest. To pay it back, he also paid Pope Leo X for the right to sell indulgences. Indulgences were contracts the church sold to forgive sins, allowing believers to purchase their way out of purgatory and into heaven. A fresh round of indulgences was printed to fund the construction of St. Peter’s Basilica, and Brandenburg was entrusted to sell them in 1517. (Their sale was later banned by the Church in 1567).

The sale of indulgences  interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

“I’m saying that there are some specific parts of modern life that derive directly from the Protestant Reformation. We couldn’t have these features if it hadn’t happened.” Ryrie said. “That combination of free inquiry, democracy, and limited government is pretty much what makes up liberal, market democracies. It runs the modern world.”

To this day, no one is sure of the extent of the Fugger fortune. Historian Mark Häberlein found that Fugger struck a deal with Augsburg Tax authorities in 1516: he agreed to pay an annual lump sum on the condition that his family’s true wealth would never be revealed. He died in 1525.

To get an idea of the extent of his wealth, we can base calculations on the cost of butchering a pig in 1522 (yes, that’s a real metric.) It cost one Gulden, a new coin minted in 1500 to butcher a hog. The German coin contained about the same amount of gold as a Florin.

Based on those ham prices, Jim Ulvog from Ancient Finances estimated that in 2017 a single florin would be worth ~$900, and other writers have put the florin in the same range. Though the true wealth of the Fuggers may never be known, when Charles V aimed to take control of the Holy Roman Empire in 1519, the Fuggers were lending Charles 543,000 guldens to buy votes: approximately $448 million. That’s just in a single deal.

It’s been said that merchant cash advances or sales-based financing is relatively new, but it could be argued that such transactions are so old that life as we know it in the modern world only exists because a guy 500 years ago was engaged in non-loan transactions to fund businesses in a manner that was Church-compliant and wanted to expand.

Maryland’s Latest Merchant Cash Advance Prohibition Bill Failed to Advance

March 18, 2021 Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

“I don’t want to snatch defeat from the jaws of victory,” he maintained.

There were several amendments up for consideration, including the inclusion or removal of a 24% APR rate cap on MCA transactions. The subject of APR dominated the light Q&A that took place, but one delegate voiced concern that creating restrictions on capital providers to businesses that might not be able to obtain funding elsewhere would probably be counterproductive. And when a roll call of votes was taken to determine if the Bill should advance to the Floor, he voted no, as did nineteen of his colleagues. Only three voted yes, so the bill did not advance, ending its prospects for the 2021 legislative session. However, it could be reintroduced again in 2022.

Committee Vice-Chair Kathleen Dumais (D) said that she thought the bill “was not ready” despite Delegate Howard “having worked hard on it.” This was Howard’s second try in two years to move it forward. His first attempt, introduced on February 7, 2020, was called the Merchant Cash Advance Prohibition Bill. The more recent one dropped the “prohibition” label but used language that would have effectively prohibited them in the state of Maryland.