Elevate Announces New Financing Facility for Non-Prime Credit Product

October 13, 2021

Elevate Credit, Inc., a top provider for credit solutions marketed for non-prime individuals, announced Wednesday a $50 million financing facility, which may increase to $100 million, according to a company press release. The funding is to grow the Today Card, a credit card designed to expand access to credit while promoting intelligent credit decisions for people with less than perfect credit scores.

Financing for the Today Card will come from Park Cities, an asset management and alternative investment company that provides flexible debt solutions to its customers. The partnership will help reduce the amount of capital required by Elevate for the project.

“The Today Card has seen outsized demand and has been the fastest growing brand over the last 12 months,” said Elevate CEO, Jason Harvison. “To continue that growth, we have announced a new lower cost credit facility. Park Cities has demonstrated a deep understanding of our space. I am pleased to both diversify our financing and promote our platform’s ability to serve non-prime consumers at even lower APRs.”

Backed by Mastercard, Today Card offers all the benefits of a regular credit card to individuals who may not qualify for the same perks through other creditors. Family share, fraud control, and flexible payment options are all packaged into the Today Card product. These options will familiarize cardholders with these types of benefits should their credit improve in the future and they qualify for other cards with different banks.

“Elevate is changing the game for non-prime Americans. We are proud to partner with a mission driven organization and help enable their growth,” said Park Cities Managing Partner, Alex Dunev.

Elevate has originated $9.2 billion in non-prime credit to more than 2.6 million non-prime consumers to date, and has saved its customers more than $8.5 billion versus the cost of payday loans, according to the report. They already offer borrower incentives like reduced interest rates over time, free credit monitoring, and free financial training.

What Makes a Great ISO?

October 13, 2021 Working and developing relationships with ISO’s can be some of the best and most difficult parts of working in the small business finance industry. The relationships between the merchants and these individuals can make or break the success of a funder, and a great ISO can take a funder and the merchant to the next level.

Working and developing relationships with ISO’s can be some of the best and most difficult parts of working in the small business finance industry. The relationships between the merchants and these individuals can make or break the success of a funder, and a great ISO can take a funder and the merchant to the next level.

Kristin Parisi, ISO Relations Manager for Park East Capital, shared with AltFinanceDaily what traits, characteristics, and commonalities separate the best reps from the rest of the pack.

“I think the top thing is someone that is super attentive,” said Parisi, when asked what is the biggest factor that makes a successful ISO. “Someone [who] is available to speak at all times, after sending something in an email or they send me something, I’ll call them and they’ll pick up, someone easy to reach out to, and someone who cares about the deal.”

Kindness also plays a big factor in making a great ISO according to Parisi, who said that sometimes the attitude of certain reps can impede business and make funding deals much more difficult. “I have come across some people who can be super rude,” she said. According to her, kindness and honesty can make or break not only an individual deal between a funder and a rep, but can be the foundation for the entire relationship between the two.

“It’s like a friendship type of thing,” she said, when describing the ideal relationship between both parties. “Someone who is trustworthy, loyal, someone who won’t screw you over behind your back, who won’t send your deals somewhere, someone who won’t screw you over for money. Honesty is the main thing.”

Parisi credits her success to these developed relationships. “The ISO’s I do work with are all my friends now, and I think we have a great thing going,” she said.

She noted the challenge of dealing with ISO’s from a female perspective, setting boundaries and being assertive while also trying to be kind and develop positive relationships. “Being a woman in this industry is a little different than being a male. I’m kind of approached differently, the girls on my team are approached differently. I’m one for being really kind and honest, but [only] to a certain extent because [ISO’s] will walk all over you.”

Apart from the personality that is projected on the funders themselves, another key trait is the professionalism of the ISO themselves, according to Parisi. She spoke about the younger, money-hungry mentality that can lead to ISO’s becoming disingenuous or difficult to work with. Rather than a hustle and bustle mentality, she credits understanding the terminology and how the industry functions as a desirable trait in a potential ISO.

“You don’t need ten plus years in the industry,” said Parisi. “You need a few months in the industry, you get it, and you’re good.”

Facebook is Buying Invoices, But is it Factoring?

October 8, 2021 After Facebook announced Facebook Invoice Fastrack, a program that would allow the company to enter the invoice factoring business effective October 1st, few knew what to expect.

After Facebook announced Facebook Invoice Fastrack, a program that would allow the company to enter the invoice factoring business effective October 1st, few knew what to expect.

“My gut tells me here that Facebook is not all of the sudden getting into the lending business,” said James Cretella, Partner at Ottoburg LLC and guest speaker at the IFA conference last Spring. “Big tech is seeing the information symmetries, especially in small business lending. It’s very fragmented, and [tech] is trying to exploit that to bring down the cost, and to consolidate that industry,” he said.

Cretella expressed a positive outlook on Facebook’s entrance into the factoring sphere. “I think it’ll be a very good thing for small businesses when big tech gets involved.”

Others believe that big tech is doing pseudo-funding in an effort to break into the space and improve their public image. “There’s always a question when big tech or similar big anything’s get into factoring,” said Robert Zadek, Of Counsel for Buchalter and CEO of Lender’s Funding. “They might call that factoring, but it’s not. It’s a fake factoring product. Fake in the sense that it’s only part of what factoring is,” Zadek said.

Since then Facebook has revealed its program partners, Supplier Success and Crowdz.

The major component here is whether or not Facebook is doing the standard operating procedures of a factoring company, or just purchasing invoices owed. “They’re probably not filing a financing statement a UCC-1, because that takes a long time, and [tech] likes fast,” Zadek said. “Filing is slow and almost manual.”

Without going through the processes of a factoring company, Facebook may just be banking on the good faith of borrowers to pay and eating the costs of those who don’t. “[Facebook] is left with an earned 1% fee with no work, which would be profitable if they get back. If they don’t it’s like a write off,” said Zadek.

According to a Facebook announcement, the company has already practiced factoring with a handful of small businesses, claiming that the program has successfully helped these select businesses grow, even giving some businesses opportunities to just keep their doors open.

We wanted to make a commitment to building tools that made information and inclusive funding partners easy to find and understand,” said Ronnie Cameron, Product Manager, Social Impact at Facebook. “We’ve been able to engage with some amazing [organizations]. The pandemic brought to light the gaps in access to funding that have always existed for underrepresented business owners.”

We wanted to make a commitment to building tools that made information and inclusive funding partners easy to find and understand,” said Ronnie Cameron, Product Manager, Social Impact at Facebook. “We’ve been able to engage with some amazing [organizations]. The pandemic brought to light the gaps in access to funding that have always existed for underrepresented business owners.”

Facebook is positioning itself in a way that appears that the company is providing an exclusive service to a community who had already been underserved prior to the pandemic, and now, according to them, needs help more than ever before. As the company has had a tough time maintaining a positive image to the public, this could also just be a slightly profitable way to fix their public perception.

Zadek compared tech’s entrance into funding to when MCAs began competing with Factoring Companies. “Instead of whining about MCAs, why don’t you give the client more money?,” he asked his predominately factoring audience when they would complain to him about MCAs. “The MCAs don’t have a death wish,” he told his audience. “They are giving money because they believe they are going to be paid back.”

Sticking to the notion that Facebook’s take on factoring is different from what his industry does, Zadek summed up his take on Facebook’s announcement.“They’re not doing factoring, they’re doing something that has little pieces of factoring in it.”

Miami is Now Making Money Off of Its Own Crypto Coin

October 7, 2021 Francis Suarez, the crypto-crazed mayor of Miami that has attempted to make his city the next center of innovation in the industry, has recently generated more than $7.1M in funding for Miami’s government via MiamiCoin. Arriving in the form of a crypto “donation” to the city, it was all made possible by CityCoins, a nonprofit that allows users to mine coins that the company claims can help the wallets of both coin holders and the cities with whom they look to invest in.

Francis Suarez, the crypto-crazed mayor of Miami that has attempted to make his city the next center of innovation in the industry, has recently generated more than $7.1M in funding for Miami’s government via MiamiCoin. Arriving in the form of a crypto “donation” to the city, it was all made possible by CityCoins, a nonprofit that allows users to mine coins that the company claims can help the wallets of both coin holders and the cities with whom they look to invest in.

According to CityCoins’ website, each time a city launches a new coin, users can mine coins themselves. They are an open-source network that allows developers to create smart contracts on top of the same layer used by Bitcoin, a feature normally reserved for blockchains like Ethereum or Cardano.

“Each time a new CityCoin such as MiamiCoin launches, 20+ unique wallets are needed to activate the token’s mining process,” the site reads. “Once this happens, a 150 block (~24 hour) countdown begins, signaling the start of the CityCoins’ mining process at the end of the countdown period. From there, anyone is eligible to participate in the CityCoins mining process within a given Stacks block and be rewarded for their contributions.”

The system creates a bidding process, sending Stack tokens to the chosen city’s smart contract for a specific block. The more Stack tokens that are sent to the contract, the more likely a user is to win rewards for that block. This creates a system where anyone can compete for the coins, as the process of mining a CityCoins product is completely free of any type of hardware.

Thirty percent of miners’ forwarded Stacks is directed into a crypto wallet for the respective city, and the remaining 70% can be used to earn Stacks or Bitcoin. Winners of the coins through CityCoins’ mining process, are chosen by a Verifiable Random Function (VRF) that takes into account the number of Stacks sent to specific contracts.

Anyone would be forgiven if the process and potential utility sounds convoluted. It becomes even more so after examining what exactly a “Stack token” is.

Stacks, a type of blockchain token originated into existence in 2019, were previously registered as securities with the SEC, a rarity in the crypto space. The company that issued them, however, has since changed course and has chosen to no longer register them. This was based upon the company’s own legal opinion, not the SEC’s.

Bottom line: However this CityCoins systems works and whatever the reasons why anyone would participate in it, it has somehow managed to yield more than $7 million for the city of Miami.

While everyone today likes to focus on the negative and want to create conflict and division…We made 1 million dollars on Miami Coin…TODAY…think about that! https://t.co/Ycbwre6Wss

— Mayor Francis Suarez (@FrancisSuarez) October 1, 2021

When speaking about the city’s involvement in becoming a fintech hub with The Floridian, Suarez credited timing to why his city is becoming the go-to spot for fintech businesses to flock. “We had an opportunity,” Suarez said. “You had cities across America, urban cities, pushing out innovators through taxation policies, sometimes elected officials saying “F” Elon Musk, or Amazon picks New York and they push them out.”

Suarez, a member of the Florida BlockChain Task Force, also credited his December 2020 viral tweet as a reason for tech’s attraction to Miami. Suarez answered a tweet with “how can I help?” after a user took to Twitter asking people if they believed Silicon Valley should move to Miami. “It was so counter-narrative to the way elected officials were dealing with technology and technologists,” he said, in reference to the Tweet.

According to Suarez, the city’s focus on crypto and fintech has made Miami a tech-trendsetter for other cities. Thanks to tech’s arrival, Miami is the first city to pursue paying workers in Bitcoin, the first to allow citizens to pay taxes in Bitcoin, and hitting huge numbers in the city’s job market. According to Suarez, the city added 8,000 jobs with an average annual salary of $120,000 in the past nine months.

“For the first time in [Miami’s] history, we are now creating high paying jobs,” Suarez said.

LOOP Brings Real Tech to Auto Insurance

October 6, 2021 LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

“We get rid of all the stuff that doesn’t matter in pricing [customers],” said John Henry, Co-CEO and Co-founder of LOOP, when explaining how the ways traditional insurance companies price their customer’s rates. This is where LOOP separates themselves from the pack. Things like credit scores, education, and income are not considered when pricing out their customer’s rates according to Henry, rather it’s how and where they are driving that determines the cost of insurance.

As an [Managing General Agent] MGA, LOOP underwrites its own risk and chooses the services they partner with to operate their claims. “This is not some digital brokerage or a quoting engine,” said Henry. “When you are insured by LOOP, it’s our actual product you’re insured by. We don’t sell any other products, we don’t sell leads, we are in the business of insuring people.”

LOOP will provide information to its customers that enables them to improve their driving and decrease their future rates. They will send customers tips on where and when to drive, and how to drive if they are driving erratically via a phone-based app. Their initial rate is based on population-level statistics from the respective area, and their personalized rate is a standard 6-month premium, meaning that the monthly rate won’t change month-to-month based upon how customers drive at certain times.

“We have millennials encumbered with student loan debt, we have immigrant populations with consumer loans, baby boomers selling their homes and losing their home and auto bundles, and the realities of the post-pandemic era means that we need more flexible and contemporary insurance solutions, and we are proud to be emerging as that,” Henry said.

![]() “We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

“We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

Henry boasted about how his company is the only one writing policies without traditional demographics in mind. “Today, I’m really proud to say that LOOP is the only insurance product that is a standard auto product that doesn’t have any of those demographic factors, it’s completely technology driven,” Henry said.

According to Henry, LOOP’s status as a public-benefit corporation, or B-Corp, will give his company the moral obligation it needs to fulfill its mission of being a fair, non-biased, and non-discriminatory auto insurance provider. The B-Corp status creates a “double bottom line” as Henry put it, creating a legal obligation for the company to hold the values in its mission statement for its customers, as well as the traditional corporate obligation to what’s best for its shareholders.

“From a business perspective, it’s kind of a risky thing,” Henry stressed when talking about the obligation to their customers as part of the public-benefit agreement. “The public can sue us if they ever feel like we are straying away from our mission.”

Customers are saving an average of 35% on their auto insurance premiums when quoted by LOOP, according to Henry. The company name directly correlates with the envisioned series of events that a LOOP customer will experience while holding a policy. A LOOP customer signs up, gets a good rate, utilizes the information given by LOOP, their driving is tracked and the data is analyzed, and the rate drops upon renewal after the policy expires. By repeating this, the customer “loops” around a cycle of better information leading to better rates.

“This is a mass market product. There is mass consumer demand. Our waitlist has grown to over 30,000 people across all fifty states, with different age groups and backgrounds,” Henry said. “I think people are excited to have an insurance company they can love again.”

Fintech Déjà Vu: Wait, Has This All Happened Before?

October 6, 2021 All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

Touted as the “5-minute online business loan,” the ad for LoanWise ran in newspapers starting in 1999. That was 22 years ago. Back then, LoanWise was described as a marketplace that connected small businesses with lenders where borrowers could comparison shop for loans.

Provident Bank was the first to join the platform, where it would approve between $5,000 – $50,000 in as little as five minutes. At the time, the Los Angeles Times said that there were only 2,160 matches on Google for the phrase “small business finance.”

“2,160 is a big number no matter how you look at it,” the Times reported.

There’s over 6 million today by comparison.

LoanWise had set up 10 lenders on the platform by the end of 1999, with names that included American Express, Compass Bank, and PNC Bank. There was competition as well. Business Finance Mart and America’s Business Funding Directory also connected interested borrowers with lenders, according to the Times.

Today, all 3 websites no longer exist, forgotten vestiges from the land before fintech.

Or has this all happened before?

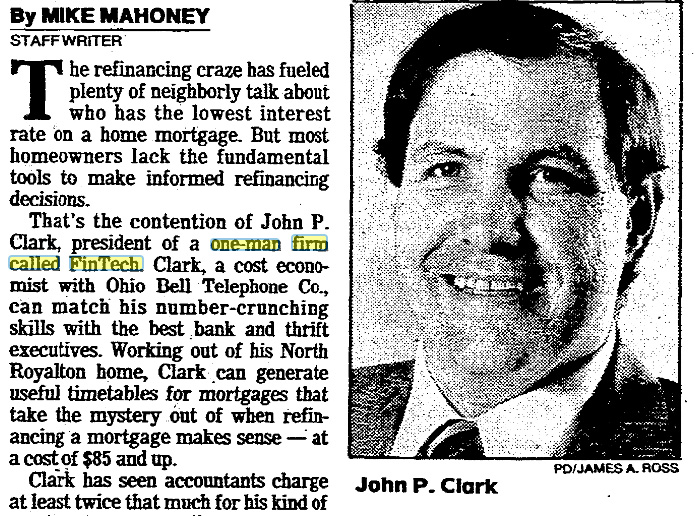

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

“Clark can generate useful timetables for mortgages that take the mystery out of when refinancing a mortgage makes sense,” wrote The Plain Dealer. Had it been 2021, Clark sounds like it would have been a billion dollar fintech app.

It was not a one-off.

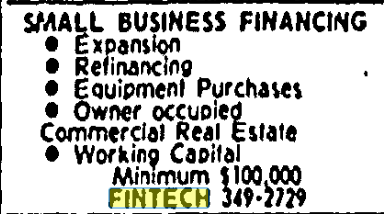

Fintech was the place to call if you wanted a working capital small business loan in San Antonio, TX starting in 1989. Ads for Small Business Financing advised people to call Fintech to get their business funded.

You could also just subscribe to the newletters. The Financial Times had four “FinTech Newsletters” in 1989 that were dedicated to covering electronic office, advanced manufacturing, telecom markets, and mobile communications. The price was £344 to £395 per year to receive them bi-weekly.

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

But hey, it’s all just a coincidence that ideas were roughly the same thirty years ago. Out in say, Des Moines, Iowa in the 1960s, for example, none of these things would’ve occurred to anyone.

Or would they have?

Sidney Feintech, a supermarket owner, expanded his store in 1963 to sell appliances, car batteries, clothing, and televisions. He got the idea that selling on credit would boost sales so he formed his own in-house credit company so that customers could Buy Now, Pay Later. Innocent enough, except the newspapers mispelled his last name.

“Fintech,” the papers said, had gotten into the credit business.

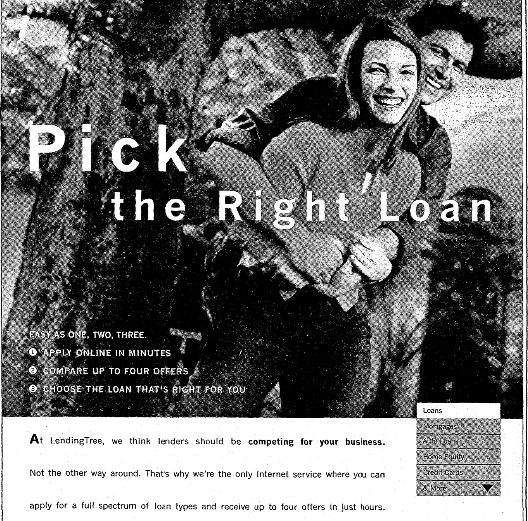

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

“I thought, ‘why can’t I put my information somewhere and let the banks compete for my business,” Lebda said. Launching a website, his company went on to generate $460 million worth of loans in just the fourth quarter of 1999 alone.

“There are other sites on the internet where you can apply for a loan, but those sites are operated by the lenders themselves,” Lebda said at the time. “We don’t lend money; that’s what makes us unique.”

That website was LendingTree, a company that today still has over 900 employees and a market cap of $1.8B. And Lebda is still the CEO.

In 1999, the hardest part was educating consumers to shop for loans online.

“Consumers have always done this one way, and this requires a behavioral change,” said consultant James Punishill in 1999. “In the old world, you’d pick up the newspaper and see a bunch of rates.”

“I knew from the start this would work because consumers really hate getting loans,” Lebda said at the time. “The market is huge and it’s perfect for e-commerce.”

Canada is Looking Forward to Open Banking

October 4, 2021 “It’s a fairly big deal,” said Tal Schwartz, Senior Advisor to the Canadian Lenders Association, when discussing the Canadian government’s renewed interest in alternative lenders after the recent Canadian election. As potential government officials from both parties discussed ideas about open banking in their election campaigns, such a conversation had been quelled by the “Big Five” Canadian banks— until now.

“It’s a fairly big deal,” said Tal Schwartz, Senior Advisor to the Canadian Lenders Association, when discussing the Canadian government’s renewed interest in alternative lenders after the recent Canadian election. As potential government officials from both parties discussed ideas about open banking in their election campaigns, such a conversation had been quelled by the “Big Five” Canadian banks— until now.

“The closer we get to some kind of entrenched regulatory framework, the better positions fintechs will be in to actually compete, get access to financial data, and raise money in an environment where there is regulatory certainty,” said Schwartz.

In August, the Canadian department of Finance welcomed a Final Report from the Advisory Committee on Open Banking that showcased a plan to modernize the Canadian financial regulatory system, with open banking and fintech in mind.

“Consumer-driven finance, or open banking, is already part of Canadians’ lives,” said Chrystia Freeland, Canada’s Deputy Prime Minister and Minister of Finance, in the report.

“Many use digital services every day to manage their money, to budget for expenses, and to make investments. Working towards a regulated, made-in-Canada system will make sure that we continue to enjoy a strong, stable, and innovative financial sector that is globally competitive, promotes consumer choice, prioritizes data privacy, and contributes to economic growth,” Freeland continued.

Schwartz said that the traditional oligopolistic structure of Canadian banking can offer advantages in times of financial crisis, but not when the government is shelling out money to help businesses during pandemic-related shutdowns.

“The reality was, if you’re a small business, you don’t have a credit relationship with a big bank, the only credit relationship you have is with an alternate lender,” said Schwartz. “By distributing money through big banks, in one sense, you’re not servicing customers the way they want to be served, and you’re cutting oxygen to a flourishing part of the innovation economy in Canada.”

“The reality was, if you’re a small business, you don’t have a credit relationship with a big bank, the only credit relationship you have is with an alternate lender,” said Schwartz. “By distributing money through big banks, in one sense, you’re not servicing customers the way they want to be served, and you’re cutting oxygen to a flourishing part of the innovation economy in Canada.”

Unlike in the United States, the Canadian government gave exclusive access of allocation to pandemic-induced federal assistance loans to the Big Five banks, leaving small business lenders relatively out to dry during that time. When asked about what issues he would like to see the new administration tackle first when it comes to alternative lenders, Schwartz mentioned the allocation of this type of money moving forward.

Other institutions outside of big banking in Canada are making strides in their effort to compete. Fintech giant Stripe announced hiring sprees for their new Toronto office last Thursday. Then there’s Nuula, a startup that aims to build a user-centric financial super app, announcing $120M in funding in early September.

To reach its full potential, Canadian fintech companies need the access to more data. The report recognizes the acknowledgement of the necessity this data is to fintech companies. “The scope of Canada’s open banking system in its initial phase should include data that is currently available to consumers and small business through their online banking applications,” it says. “Financial institutions should be allowed to exclude derived data – described as data enhanced by financial institutions to provide additional value to their consumers, such as internal credit risk assessments” the report reads.

“Historically, there hasn’t been very tech friendly or [Big Bank] challenger friendly regulations,” Schwartz said. “This is really the first time we’ve seen the political parties even mention issues of open banking and saying this will be a priority for our next government.”

“This has given the industry a lot of hope,” said Schwartz.

Would You Invest Your IRA Funds into MCAs?

September 22, 2021 A partnership between Supervest and Alto Solutions will bring in an unprecedented opportunity for investors, as the two groups will come together to allow IRA investors a chance to put their money in MCA funding. Account holders with Alto will be able to divide their money on a fractional basis to a diverse set of investments on the Supervest interface.

A partnership between Supervest and Alto Solutions will bring in an unprecedented opportunity for investors, as the two groups will come together to allow IRA investors a chance to put their money in MCA funding. Account holders with Alto will be able to divide their money on a fractional basis to a diverse set of investments on the Supervest interface.

“We expect these alternative investments to be very popular given the meaningful diversification they can provide to individual retirement portfolios in addition to being yield-generating and short-duration products,” Alto’s Chief Revenue Officer Tara Fung told AltFinanceDaily on Tuesday. “We will continue adding to our platform so that clients have more options to invest in alternative assets that further diversify and grow their retirement portfolios.”

Alto has made a business model out of using IRA funds for unique alternative investments. Crypto investments are another option listed on their website.

Supervest is no stranger to incorporating new business ideas, either. Their business model is based on connecting investors to inaccessible classes of assets, like MCAs for example.

John Donahue, the Chief Investment Officer with Supervest, spoke with AltFinanceDaily on Wednesday about the opportunity it gives IRA account holders. “It’s the opportunity for any accredited investor to now be able to access the Supervest platform of fractionalized participation in MCA deals through their self-directed IRA,” Donahue said.

MCAs can be inherently riskier than a typical lukewarm investment portfolio, but the IRA concept is basically detached from the selected risk profile therein.

“The IRA is strictly a structure,” said Donahue, when asked about the inherent risks of MCA investments with IRA money. “It really doesn’t have a connotation of conservative or aggressive nature. You can have aggressive mutual funds [in an IRA], you can have your entire investment of your IRA in the ARK New Technology fund, and while that has gone up considerably in the past few years, there’s a massive amount of volatility, it’s extremely risky, and arguably much riskier than an MCA investment.”

Donahue reiterated that only “accredited investors” would have access to these types of investments through the Supervest platform.

As the partnership between the two companies kicks off, it’ll be interesting to see if individuals are willing to put their retirement money on the line to invest in small businesses.