The Flair at Broker Fair

October 27, 2022

Times Square this weekend was filled with representatives of the alternative finance and fintech industry for this year’s Broker Fair.

Times Square this weekend was filled with representatives of the alternative finance and fintech industry for this year’s Broker Fair.

“There’s just lots of opportunities to network, I mean there’s certainly breakout sessions and things like that, I think many people are excited about those, but I think everybody’s here to network,” said Mike Mroszak, Vice President of Strategic Partnership at Dedicated Financial GBC. “…there’s ample opportunities to do that, the trade show room here is always packed with people, which is not always the case in every conference, so that’s a little bit unique to Broker Fair.”

Funder, brokers, and lenders flooded the sponsor showcase room to talk business and give out swag.

“The best tchotchke is the Lendini tchotchke. Okay, what it is, it’s just a little tool kit, very practical, very handy,” said Michael O’Hare, President at Cashyew Leads. “…the funniest one is actually from FinTap and basically, it’s a button and it says, funded, kind of based off of what Staples says, that was easy, instead it says funded.”

Speakers included Jay Shaw from OnDeck discussing what makes a successful sales team and Keynote speaker Kaplan Mobray inspiring attendees to be excellent. Mobray even surprised the audience with a quick clarinet show. Other sessions that took place include: Bad Deals, The Great Debate, Building America, Equipping the Dream Behind the Scenes, Successful Sales Team (Panel), The State of Real Estate, Truck and Equipment Financing 101, and legal panels surrounding litigation alternatives and the new disclosure laws.

Speakers included Jay Shaw from OnDeck discussing what makes a successful sales team and Keynote speaker Kaplan Mobray inspiring attendees to be excellent. Mobray even surprised the audience with a quick clarinet show. Other sessions that took place include: Bad Deals, The Great Debate, Building America, Equipping the Dream Behind the Scenes, Successful Sales Team (Panel), The State of Real Estate, Truck and Equipment Financing 101, and legal panels surrounding litigation alternatives and the new disclosure laws.

Platinum sponsors Lendini, Rapid Finance, and National Funding also took the stage in between sessions.

AltFinanceDaily CONNECT Miami was also announced for January 19th, 2023, at the Miami Beach Convention Center. With reoccurring faces at this year’s event, attendees, sponsors and speakers are very excited to reconvene once again in Miami.

“It’s been a good time, not my first actually, my second, but I’m looking to do a lot more and definitely the Miami one in January,” said Charles Wolff, VP of Loan Originations at Financial Lynx.

In The Wake of Hurricane Ian

October 21, 2022 The last week of September was pretty ugly for Floridians with Hurricane Ian hitting numerous cities like Fort Myers, Naples, and Tampa, to name a few. With 2.8 million small businesses making up the Sunshine state, many experienced power outages, flooding, and other physical damages. For the small business finance industry, natural disasters are always a possible challenge that they’ll have to contend with.

The last week of September was pretty ugly for Floridians with Hurricane Ian hitting numerous cities like Fort Myers, Naples, and Tampa, to name a few. With 2.8 million small businesses making up the Sunshine state, many experienced power outages, flooding, and other physical damages. For the small business finance industry, natural disasters are always a possible challenge that they’ll have to contend with.

Jordan Fein, CEO at Greenbox Capital, knows firsthand how to deal with natural disasters during hurricane season. The Miami-based funding provider has been in business since 2012 and has experience with funding businesses in tropical areas like Puerto Rico and the Virgin Islands.

“We’re now at a point where we feel that we do it among the best on how to handle these kinds of situations in terms of being able to meet our customers’ needs, especially during times of duress,” said Fein.

Flooding, wind damage, and trees fallen over on buildings and properties is what Tarneisha Peters, Regional Director of West Florida at Black Business Investment Fund (BBIF), has seen in her area of South Tampa. Many people have lost power for up to 4 days, affecting not only small businesses but staff members as well. And while the extent of the storm’s effects on some merchants are still unknown, Peters hopes the variety of program mentorship and training will help their clients remain resilient in the wake of the hurricane.

“Over 500,000 people experienced outages in the Tampa Bay area, as well as our staff in the Orlando area, including some of our clients,” said Peters. “Our goal is to support BIPOC business owner’s resiliency, so that they are prepared and able to navigate challenging circumstances that may come their way.”

Mark Kane, CEO at Sunwise Capital in Boca Raton, has seen a fair number of hurricanes since he started his business in 2010. His company has even had to relocate to Orlando before just to have internet in order to work. Businesses that are a true “brick and mortar,” as Kane described, may not have the luxury of moving elsewhere. But before immediately knowing which angle to help clients, Kane tries to look at it from a couple different angles. What was the impact of the damages? What exactly do they need? And how can they accommodate those needs?

Mark Kane, CEO at Sunwise Capital in Boca Raton, has seen a fair number of hurricanes since he started his business in 2010. His company has even had to relocate to Orlando before just to have internet in order to work. Businesses that are a true “brick and mortar,” as Kane described, may not have the luxury of moving elsewhere. But before immediately knowing which angle to help clients, Kane tries to look at it from a couple different angles. What was the impact of the damages? What exactly do they need? And how can they accommodate those needs?

“I think it has to be looked at from a number of different levels,” said Kane. “So, what was the total impact? Is it ‘hey, I’m done, I’m out of business?’ or ‘hey, I need a break, because our business is slow, or we haven’t reopened, and I’m not able to make the payments.’”

Meanwhile, impacted businesses may be eligible for Business Physical Disaster Loans as well as Home Disaster and Economic Injury Disaster Loans. For physical damage, the deadline to apply for a loan ends November 28th and economic injuries the deadline ends June 29, 2023.

“BBIF is an SBA lender,” said Tarneisha Peters, who added that the SBA was a great partner of theirs. “[The SBA provides] disaster related support, guidance and business assistance to help provide relief when it is needed most.”

Lavu Adds MCA Product Through Partnership With Parafin

October 7, 2022 It’s not just DoorDash that Parafin has partnered up with to provide MCA funding. Last week, the restaurant software company Lavu launched Lavu Capital to help restaurants owners access capital.

It’s not just DoorDash that Parafin has partnered up with to provide MCA funding. Last week, the restaurant software company Lavu launched Lavu Capital to help restaurants owners access capital.

“We are a restaurant software company that focuses on small and medium restaurants,” said Saleem S. Khatri, CEO of Lavu. “Think of your favorite restaurants that have one or two locations that are really really popular, that are ingrained in the community. We do everything from point of sale to online ordering, payment processing, and anything a restaurant would need to start and grow their business.”

Khatri said that one thing they noticed is that these restaurants have a fundamentally hard time getting loans and that led them to connect with Parafin. Parafin’s product is an advance on future sales, not a loan, and their offerings have been simply integrated into Lavu’s technology. Parafin automatically generates an offer for restaurant owners that they can see in their Lavu dashboard.

“…it’s just really beautifully designed,” said Khatri. “It basically says, ‘Hey, you have an offer to borrow up to $5,000. Do you want it yes or no?’ And you just click ‘yes’ and you’re good to go, the money deposits straight into your bank account, and then you have a repayment schedule. And it just pulls it directly from your bank account according to that repayment schedule.”

Khatri says they haven’t really begun to market the product yet and they’ve just started off with a limited base of customers but that the plan is to roll it out to all their customers around the US. They’d even do it with their customers outside of the US if they could, but the tech is not set up to do that just yet.

“This is going to be a feature and an offering that really really benefits our customers because it gets to the heart of what they need, which is they’re in constant need of liquidity, they’re in constant need of kind of tools to run their business better,” Khatri said. “And it just really fits our portfolio of products that we offer to these customers. So the reception has been awesome.”

Let’s Get Personal! (In Sales)

September 16, 2022 “Personalization is adding that human element to a buying process that can traditionally feel either very stressful or cold and clinical,” said Taylor Hicks, Creative Strategist at Elevate Funding. “It’s about recognizing that clients (and prospects) are humans with their own unique set of needs and goals.”

“Personalization is adding that human element to a buying process that can traditionally feel either very stressful or cold and clinical,” said Taylor Hicks, Creative Strategist at Elevate Funding. “It’s about recognizing that clients (and prospects) are humans with their own unique set of needs and goals.”

Working in this industry and communicating with clients is a given but being personable with each one encountered is a task within itself. No client wants to be victim to a boring sales call where the one pitching lacks a persuasive personality. And nobody wants to be on the other end of the call feeling like they are wasting their clients’ time with a dull sales pitch. Making the client-to-business communication an eventful experience for both parties comes with a great amount of pressure, and it also can make or break a deal.

“Be a human being. Don’t do the high-pressure sales things like some of these guys are doing,” said Alexander Gold, CFO at Future Funding. “I get compliments that my guys are not doing that, and I feel like it’s just timing. So, if your timing is good, people will give you the shot. If your timing is bad, you won’t get the shot…”

The client needs to know that they can fully put their trust into a company or product, and it will be worthwhile. Creating a mutual trust, especially when dealing with a person’s finances can be a very personal experience. The key to that can be very simple, as Gold says, to tell them who you are and how you can help with just a moment of their time.

“So first, you have to build credibility, I would say that’s the most important thing is building credibility,” said Gold. “That could be knowing something they don’t, showing them something or teaching them something that you can prove and then possibly show them as well. I would say products, being very knowledgeable in your products and your product base.”

“So first, you have to build credibility, I would say that’s the most important thing is building credibility,” said Gold. “That could be knowing something they don’t, showing them something or teaching them something that you can prove and then possibly show them as well. I would say products, being very knowledgeable in your products and your product base.”

“…[It’s] how do you provide them interesting insights into their finances or into their needs without coming across overbearing or selling them something that they don’t need?” said Greg Varnell, VP of Product and Development at Q2. “And that’s a real balance. And so, I think, for us, personalization isn’t just trying to sell somebody something, but it’s trying to tell them the information that they need when they need that information.”

“I think trust has to be earned,” said David Roitblat, Founder and CEO at Better Accounting Solutions. “Most of our clients are referral based from other clients. So I guess that speaks for itself. […] So that does give us a head start on that, but ultimately, people judge you based on your work.

“At Elevate, we take a custom-tailored approach for each client,” said Hicks of Elevate. “We send out newsletters to our clients biweekly to remind them of our various programs, like add-ons and renewals. We are proactive in reminding them of their Future Receivables Sales Agreement, and we’ll always work with them on reducing their payment amount if their revenue drops. We provide our clients a variety of ways to get ahold of us – whether that’s email, call, text.”

Regardless of your role in the finance industry, interactions can have long lasting impacts. From the initial meeting to developing trust, and eventually turning that journey into a meaningful working relationship. And who knows, that one great client interaction could lead to many referrals and recommendations in the future.

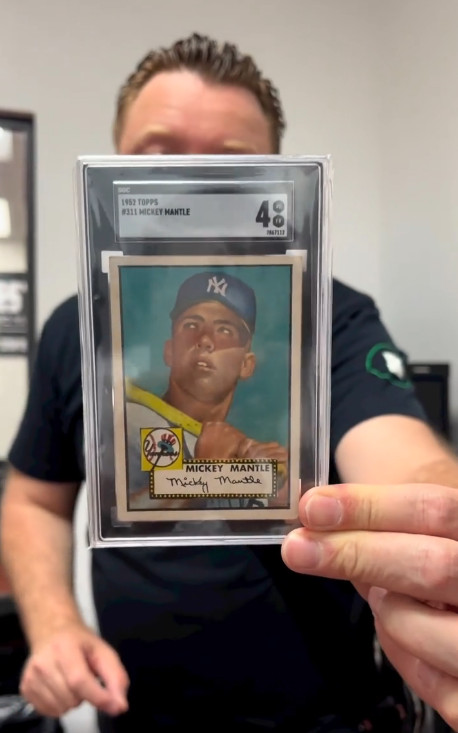

Got a Mantle, Bryant, or Mahomes Card? This Company Wants to Fund You

September 12, 2022 Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

The value of the Mantle sale came as no surprise to one budding entrepreneur in South Florida. On Instagram, he’d been talking about Mantle cards for weeks, even going so far as to hold up another ’52 Topps Mantle card to the camera to promote what his company can do, which is provide quick cash advances to owners of valuable sports cards.

The entrepreneur’s name is Edward Siegel, CEO of Card Fi. Siegel’s no stranger to the alternative finance space because he spent about a decade in the MCA industry, most recently as the founder of Bitty Advance, which he sold in 2020. Since then, Siegel returned to his roots and early passion of his youth.

“I had a background in sports cards as a collector, you know as a kid, but then in my early twenties, I was promoting card shows at malls,” Siegel said. “I was heavily into the hobby, setting up the card shows and promoting them and doing player appearances where players come in and do an autograph appearance.”

That was back in the late 80s, early 90s, according to Siegel.

When Covid hit and he exited his most recent company, he noticed a massive resurgence in the sports trading card market. His next business ultimately became Card Fi, a company that will evaluate the market value of a card and make an advance against it. There’s obviously risk involved so they take possession of the card for the duration.

“We have to get a hold of these cards and we’re responsible for them and then we vault them in our in-house bank vault,” Siegel said. The cards are stored in a highly secure climate controlled environment. Card Fi shows the vault off frequently in its Instagram videos.

Such a business requires large amounts of capital so Siegel went searching for investors, a pursuit that led him to a unique place, an Instagram Live pitch competition hosted by famed CEO and reality TV star Marcus Lemonis. Siegel entered himself in as a contestant, knowing full well that the odds of even being chosen to present his business to Lemonis were about a million-to-one.

Somehow, he was called up to pitch.

“So [businesses] went on there during the quarantine and you pitched your business,” Siegel explained. “I went on there and I pitched it […] And he understood it and he thought it made sense.”

The moment eventually led to a deal with Lemonis’ company and Card Fi was on its way.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

“If we look at it, there’s two different markets, you have the modern card market [where] I would say it’s basketball [that leads the pack],” he said. “For the vintage card market it’s baseball.”

Football is huge as well, he explained. A Patrick Mahomes rookie card, for example, an NFL Quarterback that’s still currently playing, recently fetched $861,000. There are only one of five like it in the world, the scarcity playing a major role in the value. Meanwhile, a Justin Herbert rookie card, an NFL Quarterback who’s only in his third year was already receiving bids above $1 million at the time this story was being written.

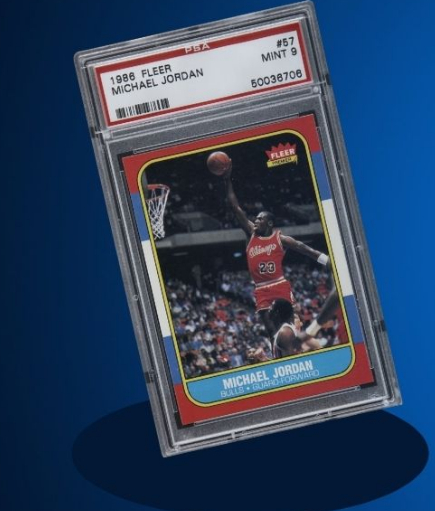

“It really depends on the card itself,” Siegel explained. “Some players might be known for having better careers but then you have cards that have more scarcity to them. Something that’s a one of one or maybe a very low populated card and a graded PSA 10 could very well be worth more than a [Michael] Jordan rookie because it has scarcity in it.”

PSA refers to cards that have been verified as authentic and graded on the condition of the card itself. Ten is the highest level a card can receive. Card Fi will only work with graded cards to avoid any funny business when it comes to advancing funds based upon the value.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

“This financing benefits the market as loans and cash advances have become an increasingly asked-for offering among trading card collectors,” said Chad Fister, PWCC’s CFO in a story that originally appeared on Sportico. “Enabling our clients to access liquidity through a menu of capital offerings is key as trading cards continue to prove themselves to be a valuable tangible asset class.”

For Card Fi, customers that take an advance can track everything through an online portal, including details about their cards, payments, and balance.

“We want to note that we built a full-service automated underwriting and collection platform to where, whether it’s the customer or the broker, they can log into our system and put the description of the card into the system and it’s going to automatically underwrite it and price it out,” Siegel said.

That description sounded like something straight out of the fintech industry of his past, especially the component about brokers.

“Just like the MCA space, we have a whole partnership side, a broker side, where brokers can refer us customers just as an affiliate where they just send the info over,” Siegel said. Similarly, they can earn a commission if a transaction is completed, he explained.

In this industry, brands like Topps, Upper Deck, and Panini have become the bread and butter for Card Fi. Even though it’s all business for Siegel these days, he couldn’t help but mention a particular card he had a personal attachment to.

“My personal favorite card in my collection is the 1965 Topps Joe Namath rookie card,” Siegel said. “Of course being a die hard New York Jets fan, that has to be my favorite card.”

Monday through Fund-day

September 8, 2022 Nothing screams excitement like a brand-new week filled with endless funding opportunities. Regardless of the type of funding, the ultimate goal is to find clients in need of capital and spring to action quickly.

Nothing screams excitement like a brand-new week filled with endless funding opportunities. Regardless of the type of funding, the ultimate goal is to find clients in need of capital and spring to action quickly.

“I would say Tuesday is like, a day that things get done,” said Michael Krepak, CEO of FlexCap Solutions. “People always talk about Friday’s a closing day. I’ve had a lot of success on Fridays as just like a funding day, like when the deals actually get done afterwards in all the underwriting and the back and forth and stipulations. So, Tuesdays and Fridays…”

Fridays may be hectic for some professionals in the business who are trying to close out a deal before the weekend is over. The pressure to close a deal can create competition within oneself to finish the week off strong or to make sure that nothing ruins it over the weekend.

“There’s always a push to get everyone funded right before the weekend, you don’t want deals rolling over,” said Brendan P. Lynch, CEO at Sharpe Capital. “Too many things can happen: negative days, they can go negative, and then the login, they have to redo it. And you know, the deal can die on Monday. So, you always want to get everything done before the weekend. That’s for sure.”

For equipment finance consultant Cheryl Tibbs, if she is able to finish funding by Thursday, she uses Fridays to either spend quality time with loved ones or to promote her business.

“I’m a bit different than most. I start off strong on Mondays and relax on Friday,” said Tibbs. “When I’m done Thursday, late Thursday evening, Friday is reserved for deals that will fund that day. If I don’t have anything booked for a Friday funding, I usually chill on Fridays and use that for marketing or family time.”

Sonia Alvelo of Latin Financial was non-committal to a day. “What gets us excited is the satisfaction of a job well done…” Alvelo said.

Krepak meanwhile, explained that if you’re working on commission, then there is an incentive to keep going strong every day. “Like every day, you want to do something every day,” he said. “It’s just a competitive face to begin with.”

Funders Weigh in on the New Disclosure Law in Virginia

August 10, 2022 “I think there are pros and cons on this law,” said Boris Kalendarev, CEO at Specialty Capital, in regards to the recently enacted sales-based financing disclosure law in Virginia. “I’m on the pro side and I think first and foremost it allows the good funders and the good brokers in the space to operate in the right manner.”

“I think there are pros and cons on this law,” said Boris Kalendarev, CEO at Specialty Capital, in regards to the recently enacted sales-based financing disclosure law in Virginia. “I’m on the pro side and I think first and foremost it allows the good funders and the good brokers in the space to operate in the right manner.”

The law technically went into effect on July 1st, shaking things up for funding providers and brokers alike, particularly through a set of uniform disclosures that are required every time a contract is put in front of a Virginia-based business.

“It holds a broker more responsible for the transaction that they’re going to complete,” said Sharmylla Siew, Senior Underwriter at Lending Valley. “It builds a deeper bond between the broker and the merchant. And it also creates a better bond between the broker and the funder.”

Echoing Siew’s perspective, Kalendarev also believes that being clear creates an honest business space for the broker, merchant, and funder.

“I think transparency is really the right way to run this business. Let’s try to make sure there’s even more transparency,” said Kalendarev.

One intent behind the law is to provide the business customer with all of the pertinent information in a digestible format. Notably, this includes the commission that a broker may be receiving from the funder.

“I do believe that it should be fully transparent on both sides to understand the transaction in full,” said Dylan J. Howell, CEO of Liquidibee. “The merchant should understand that the broker is getting compensated. And if he decides that the broker deserves an additional commission on top of what he’s getting paid from the funder, well, that’s an informed decision between the merchant and broker to come to an agreement with.”

“I do believe that it should be fully transparent on both sides to understand the transaction in full,” said Dylan J. Howell, CEO of Liquidibee. “The merchant should understand that the broker is getting compensated. And if he decides that the broker deserves an additional commission on top of what he’s getting paid from the funder, well, that’s an informed decision between the merchant and broker to come to an agreement with.”

Howell Suggested that some of what is required would be expected in other types of deals.

“If you would go out and buy a $500,000 house, you get to the closing table and you look at the bill, it says it’s $545,000, but the purchase price is 500,000, you would want a reconciliation page to show where that 45,000 of additional capital is going,” Howell said. “And it’s no different than in this transaction, in my opinion.”

Banks and credit unions were exempt from the law but some view targeted regulations like this one as a way to raise the bar and credibility of sales-based financing products in general.

“Merchants who wouldn’t have considered an MCA as a practical form of funding in the past may decide to explore this avenue knowing that the industry is being held to a higher standard of practice,” Howell said.

Siew, of Lending Valley, echoed same.

“I am actually very excited about the new regulations, and I feel that it would make a huge impact on the MCA industry,” she said.

Work With a Broker or Go Direct?

August 2, 2022“I believe that a merchant might be better off going to a broker so the broker can make available to the merchant several different offers,” said Pooja Nene, Broker Relations Manager at Balboa Capital. “And if they’re doing what they need to do correctly and if they’re really consulting the merchant correctly, I think that they would be providing the best offers to the merchant based on their needs.”

It’s the age-old question, are merchants better served by using a broker or going direct? Opinions vary and are usually colored by what role one has in the process.

It’s the age-old question, are merchants better served by using a broker or going direct? Opinions vary and are usually colored by what role one has in the process.

“The advantages of working with a broker is it saves the merchants a lot of time, and in some cases saves them money in fees,” said Randy Guerrier, Senior Funding Executive at Banana Exchange, a company that provides capital to MCA providers. Guerrier’s vantage point makes him less biased. “A lot of brokers do have a lot of preexisting relationships and wholesale rates that they could get with their relationships,” he said.

Matthew Washington, Founder & CEO of Moneywell GRP, says there’s a bit more nuance to the whole thing.

“The reality is that when the merchants go direct with lenders, they’re essentially dealing with the lender’s broker shop, right?” he explained. “Any lender that gets directly contacted by a merchant usually gives them off to their sales team, which [is also able] to send [them] off to other lenders.”

Washington, whose company is a funder, was an advocate for what brokers can accomplish for their clients especially since he relies entirely on them for business. He emphasized that his company is one that doesn’t have a direct sales team to handle any direct inquiries.

“All my business comes from my ISO channel,” he explained. “So when I approve a deal, it’s up to me and the broker to win it if there’s competition, but if I declined the deal, my brokers take that deal to another lender that has an appetite for that particular scenario.”

“[Lenders] may not have the staff available to form that relationship with a merchant,” said Pooja Nene of Balboa about the debate on broker vs. direct. She also cautioned that sidestepping a broker in the process might not translate into an increased likelihood of approval.

“[Lenders] may not have the staff available to form that relationship with a merchant,” said Pooja Nene of Balboa about the debate on broker vs. direct. She also cautioned that sidestepping a broker in the process might not translate into an increased likelihood of approval.

“If it’s the first round of funding, if it’s their first loan schedule, we don’t know who this merchant is, and we may feel a little bit more comfortable with that file coming through the broker and the broker discussing the terms with the merchant,” she said.

Guerrier of Banana Exchange said, “It always comes down to working with the right type of broker, right? It comes down to the person that answers the phone that’s working with you, whether it’s at a big company or small company, I like to look at things from the individual working with the right people.”

And finding the “right people” isn’t automatic because they still have to be found, and once they’re found the lender has to decide if the customer is also right for them. Speaking about that in relation to all the economic uncertainty, Washington of Moneywell GRP said that a funding company should stick to what they’re comfortable with and not “chase deals” that they wouldn’t normally fund.

“But, also [on being found], I would market the heck out of my company and make sure that everyone in the world knows what I do, my product line, my branding, my logo, and make sure that anyone that is looking for capital that they know ‘hey, this company is always popping up,’ and I’d make sure that I stand out,” Washington said.