Coming to the Rescue: Consolidation Can Save Merchants

June 24, 2015 In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

“Consolidations are a way to help merchants avoid defaulting,” said Chad Otar, managing partner at New York-based Excel Capital. Consolidation works if the buyout price is low enough and the terms allow enough room to handle the obligation.

“It can free up some cash and give the merchant some room to breathe, sustain the business and avoid taking on more debt,” he noted.

It’s helpful to think of consolidation as the equivalent of refinancing a house, according to Stephen Halasnik, managing partner at Payroll Financing Solutions, a Ridgewood N.J.-based direct lender. Payroll has been offering the service for about six months, he said.

Brokers and funders can benefit from consolidation because it puts a merchant back on track towards long-term sustainability, said a broker who requested anonymity. Moreover, the broker said that one in three of the potential deals he sees have multiple advances outstanding, which means companies could lose an alarming chunk of market share by declining too many potential funding candidates. “That’s what I believe the catalyst was to opening the doors to consolidation,” he contended.

SECRET TO SUCCESS

Success in consolidation lies in finding merchants worthy of another chance, said Otar. Clients who have taken two or three advances but stick to the new plan and stop stacking advances from other brokers have a reasonably good chance of succeeding, he said. His company can work with a merchant that has as many as three advances outstanding if they have sufficient revenue.

Otar provided the example of a merchant who’s diverting 20% of his gross revenue to three advances. Together, the advances have led to a total of $50,000 in future revenues sold. If the merchant generates enough monthly revenue to qualify for $100,000, Excel can buy out the three advances, provide the merchant with $50,000 in cash, and lower the payment to 8% to 12% of gross revenue. “All of a sudden they have all this cash flow to play with that really wasn’t there,” he said of merchants in that situation. “They tend to do really well.”

Halasnik of Payroll Financing Solutions offered the example of a trucking company that had taken three advances and was delivering a total of $1,138 a day on average to the funders. Payroll bought out the three funders and is charging the trucker $615 a day.

One of Payroll’s clients needed to repair a commercial vehicle but already had too many advances and couldn’t get another, Halasnik said. Payroll consolidated the positions and lowered the payment, enabling the merchant to save enough money in two weeks to have the vehicle fixed.

To qualify for a consolidation, the merchant has to meet the “50% Rule” by netting 50% of what Excel is offering, Otar said. Between 40% and 50% of the distressed merchants that the company considers for consolidation meet that criterion, he said. An additional 30% of the merchants can meet that standard in the near future, once they’re further along on their agreements.

Under the 50% Rule, a merchant that is still obliged to deliver $70,000 and qualifies for $100,000 would not be a candidate for consolidation, Otar said. In that situation, a merchant can wait until he has delivered more of the sold revenues to the funders and then get a consolidation, he said. “In the meantime, don’t take on any more debt,” Otar tells the merchants. That too could impact their ability to sell additional revenue streams in return for cash upfront down the road.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Brokers should also bear in mind that every deal’s different, cautioned Steven Kamhi, who handles business development and ISO relationships at Nulook Capital, a Massapequa, N.Y.-based direct funder. “It has to be the right deal,” he advises.

Brokers can identify distressed merchants within the first two minutes of a phone conversation when they say things like, “I need the money right now,” Otar said. Looking at the paperwork, the broker can see within 10 minutes whether the potential client is hard-pressed.

Asking the right questions helps reveal distress quickly, sources said. That can include asking how many advances the merchant has outstanding, how much in future sales they still have to deliver and how much revenue they’re grossing monthly. Asking what company advanced them cash can reveal a lot if they’re working with less-reputable companies.

Listening’s under-rated, too. Merchants sometimes explain that they’re coming up with more ways of making money and are, therefore, making themselves a better bet for sustainability, Otar said.

OTHER WAYS OF HELPING

Brokers can make deals more palatable to some distressed merchants by deducting payments weekly instead of daily, Otar said. “It’s something I’m seeing a big migration toward,” he noted. “It’s a big selling point.” Manufacturers and contractors don’t have customers swiping cards every day and especially appreciate the change. More widely spaced payments can also fit better with some clients’ seasonal cash flow.

Besides consolidation, brokers can help distressed merchants by providing traditional accounts-receivable financing, which can prove particularly helpful for manufacturers and construction companies, Otar said.

Suppose Customer A owes a contractor $100, Otar said by way of example. The contractor can get $90 from the factor, and the factor collects the $100 from Customer A. The client pays the cost of the financing upfront but reduces the waiting time to receive the cash and avoids daily or monthly payments.

Accounts-receivable financing costs merchants much less than a cash advance, Otar noted. But putting the deal together takes longer than approving an advance, and merchants in immediate need of cash might not be able to wait.

In another example of helping merchants, Payroll had a client who was a bicycle shop owner with good credit and equity in a home, so it granted him an advance that gave him time to go to a bank and get a home equity loan. “I counseled him to do that and then buy us out,” Halasnik said.

PREVENTING DISTRESS

On the sales side of the business, brokers can help distressed merchants by preventing stacking from occurring in the first place, sources said. Otar recommended, “listening to the customer, understanding the business and offering a product that is going to benefit the customer in the long run.” That way, the broker positions himself to work with the client for years, not two or three months. “At the end of the day, they appreciate that,” he said.

Halasnik relies on his experience as a small-business owner who has operated a printing company, staffing company and nurse registry to help him understand aspects of a client’s business that people from a purely financial background might not fathom.

Brokers seeking long-term relationships should know a client’s business well enough to advise against taking on more financial obligations when the time isn’t right, agreed Payroll’s Halasnik. However, after the broker urges caution, the decision rests with the business owner, he maintained. “We are on the same page as the client,” Halasnik said. “We are looking out for their best interest because, ultimately, we have to get paid back.”

THE CASE AGAINST CONSOLIDATION

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

When a merchant’s overextended, he should wait before taking another advance, Stern said. But when some merchants are denied another advance, they immediately seek out another funder, he maintained.

Yellowstone has put together a few consolidations but chooses not to create too many, Stern said. Some merchants find themselves a month or two away from going out of business unless they can find a source of cash, he observed. “They’ve been declined for that last credit card, and things are getting really rough,” he said.

Some members of the industry advocate coming together to improve standards and provide training. Wall Street’s testing and licensing could serve as an example, suggested one source. Background checks could also help root out unethical players, he noted.

But creating a training and certification infrastructure would prove a formidable task, according to Stern. The industry would have a hard time agreeing upon who should head a trade association to administer the standards, he said. He views the industry as a collection of Type A personalities – sometimes defined as ambitious, over-achieving workaholics – who would resist consensus. “It’s a nice idea, but I don’t see it working,” he said.

REASON TO BELIEVE

Though industry players are contending with some distressed merchants, Stern noted that the average credit score of his company’s clients is beginning to rise as the economy improves.

Though statistics on distressed merchants aren’t readily available, other industry veterans feel they’re not encountering as many now as a year ago. However, they said they may see fewer cases of distress because bigger players are beginning to offer consolidations.

“A year ago, nobody would consider doing it,” a broker said of consolidation. But as funders become more open to the product when they see competitors using it to gain market share. “It’s becoming more mainstream,” he said.

How brokers market their services can also determine how many distressed merchants they encounter, sources said. Using the same prospect lists that competitors use can lead to calling on overextended clients, they maintained.

Whatever the number of distressed merchants may be, stacking sometimes makes sense, said Halasnik. What if a client needs $30,000 to win a contract, and a funder is willing to provide only $15,000, he asked rhetorically. Perhaps another funder will put in $15,000, too.

Problems arise, however, if the two funders don’t know the merchant has made two deals because they happened the same day. It’s the kind of situation that sours some members of the alternative-funding community to consolidation. As Halasnik put it: “You’re dealing with somebody who’s in trouble. It’s the highest risk a lender could take.”

The Official Business Financing Leaderboard

June 20, 2015A handful of funders that were large enough to make this list preferred to keep their numbers private and thus were omitted.

| Funder | 2014 |

| SBA-guaranteed 7(a) loans < $150,000 | $1,860,000,000 |

| OnDeck* | $1,200,000,000 |

| CAN Capital | $1,000,000,000 |

| AMEX Merchant Financing | $1,000,000,000 |

| Funding Circle (including UK) | $600,000,000 |

| Kabbage | $400,000,000 |

| Yellowstone Capital | $290,000,000 |

| Strategic Funding Source | $280,000,000 |

| Merchant Cash and Capital | $277,000,000 |

| Square Capital | $100,000,000 |

| IOU Central | $100,000,000 |

*According to a recent Earnings Report, OnDeck had already funded $416 million in Q1 of 2015

| Funder | Lifetime |

| CAN Capital | $5,000,000,000 |

| OnDeck | $2,000,000,000 |

| Yellowstone Capital | $1,100,000,000 |

| Funding Circle (including UK) | $1,000,000,000 |

| Merchant Cash and Capital | $1,000,000,000 |

| Business Financial Services | $1,000,000,000 |

| RapidAdvance | $700,000,000 |

| Kabbage | $500,000,000 |

| PayPal Working Capital* | $500,000,000 |

| The Business Backer | $300,000,000 |

| Fora Financial | $300,000,000 |

| Capital For Merchants | $220,000,000 |

| IOU Central | $163,000,000 |

| Credibly | $140,000,000 |

| Expansion Capital Group | $50,000,000 |

*Many reputable sources had published PayPal’s Working Capital lifetime loan figures to be approximately $200 million in early 2015, but just a couple months later PayPal blogged that the number was more than twice that amount at $500 million since inception. The print version of AltFinanceDaily’s May/June magazine issue stated the smaller amount since it had already gone to print before PayPal’s announcement was made.

There’s No Room for More Competition

June 2, 2015 In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

There are basic facts that we can take from the “Broker Boom”

– Not enough beginning knowledge about this industry and how the Merchant Cash Advance process works.

– No time to make strong relationships: The concept of having “more” is usually more harmful than having a handful of trusting relationships.

– Overhead costs: the make-up costs from the spending on dead leads and the “start-up” costs of having an office, staff, draws – gave the wrong perception of what a “MCA” is when the rate mark ups pay for those expenses.

– Quick turnover when the top dog can’t fool the sales rep out of commissions any longer: Rep goes out into the world and starts their own company. This can lead to recycled bad practices or the few who want to do right.

– Co-Brokering: Everyone’s done it. I’ve done it. Edited agreements taken from other brokers/funders don’t always cover everything leading to many debacles that turn into “Jerry Springer” Forum threads. P.S. Don’t think merchants can’t see the forum either.

It’s absolutely exhausting to explain to someone from the mortgage industry or any industry that comes into the MCA space the “Rights” and “Wrongs” and the teachings. Most new Broker Company Owners and their sales come from those who don’t believe in “Best Practices” anyway.

Marketing and Leads in the Broker Space is affecting Brokers and Funders Alike – Are brokers ruining leads as well?

So, your questions about Marketing and Leads have the same answer- It does not matter what type of leads you get, it’s all about your presence, knowledge, and your “Handle”. These are the answers from actual merchants who get calls from UCCs. (This information came from old merchants that I had, I shortened the answers and stuck to the points).

- They don’t trust you because of your approach

- They tried before and was promised “X” and got a bunch of “Y” with excuses on how so many “Y’s” = “X”

- Backdoor calls- Sometimes the money isn’t the biggest savior- it’s the relationship that goes with it

- They don’t need it that bad to pay 30%. If they do need it- they want something structured to build their credit and keep their business afloat

When people think of getting money for their business- they used to think “Go to the Bank”. Professionalism, a structure that is always the same for each type of program, and knowledgeable staff they can rely on. They made the choice to come to your bank because of what is offered. Now, all but the “Capital” part is missing from this equation, but merchants still want to have that one consistent place to go to for their business needs.

I think we all lost sight of this Industry.

Brokers = Resellers and Marketers of Direct Funding programs. The Broker takes the programs from these Direct Funders and builds a portfolio of which each tier and industry and credit rating is satisfied by which funders he can qualify them to. The options are given to the merchant to satisfy their need for working capital.

You work for the Funder – Your Sales Target is the Merchant.

The Merchant has put everything into starting and maintaining their business. Most of them wanted the “American Dream” of owning a business since childhood. They have it now, and you come in and try to tell them what they need. Some believe you- some are money hungry and know the game. It’s all a numbers game no matter what kind or type of leads you buy.

All that am I saying is, the way this industry is looked at from a “Brokers” and “New-Age Funders” point of view vs. a “Veteran Broker” or “Veteran Funder” is two totally different aspects.

Unfortunately, there is no immediate solution for new “Brokers” and many solutions for the “New-Age Funders” to be on the path of “Best Practices” and less shenanigans.

There is no room for competition as we don’t know what we are competing for and rather than creating a solution so those leads can understand the growth and structure of what we are offering, we are too busy trying to find out how to get leads that won’t stick.

The Broker’s Future: Are The Good Times Over?

June 1, 2015 As we continue the Year Of The Broker discussion, we must take an honest look at The Future. Due to the low barrier to entry into our space, there isn’t a week that goes by that I don’t see another recruiting ad informing the reader that all they need is a heartbeat, a UCC list, and an industry list of SIC Codes to make big money in our space. But is everything really as rosey as promoted, or if you are a new broker, should you consider investing your capital (time, energy, money and mental health) in another industry?

As we continue the Year Of The Broker discussion, we must take an honest look at The Future. Due to the low barrier to entry into our space, there isn’t a week that goes by that I don’t see another recruiting ad informing the reader that all they need is a heartbeat, a UCC list, and an industry list of SIC Codes to make big money in our space. But is everything really as rosey as promoted, or if you are a new broker, should you consider investing your capital (time, energy, money and mental health) in another industry?

The Past

To understand The Future, sometimes we have to look at The Past. Instead of a year of the broker, there was instead an actual era of the Broker, and that was from 2000 to about 2013:

(( 2000 – 2007 ))

Few firms offered a “Merchant Cash Advance” as either a direct sell or value add, and very few merchants were receiving telephone solicitations in regards to the having “working capital” other than those involved in the Equipment Leasing or A/R Factoring sectors. While the market was wide open, most merchants wouldn’t entertain an advance for 6 months with a 1.25 – 1.30 factor rate when banks were lending pretty well at much lower borrowing costs.

(( 2008 to 2013 ))

When the economy and markets took a downturn in 2008 creating The Great Recession, and banks halted most of their lending to small business applicants, the Merchant Cash Advance product was more aggressively sold by the pioneers of the industry through their Merchant Processing ISO relationships, direct selling, online advertisements, and more. The pioneers also introduced risk based pricing and premium priced products, allowing them to appeal to the higher credit graded merchants who were finally entertaining the product due to banks not lending as efficiently as previously. The pioneers also introduced multiple formats of repayment including through ACH, which allowed them to service merchants that they couldn’t tie the repayment to their merchant processing volume due to the merchant’s inability to switch or the merchant’s low monthly processing volume.

Awareness of the Merchant Cash Advance skyrocketed, hundreds of millions in equity capital began pouring in, major media outlets such as CNBC gave the product coverage, and annually the industry was funding over $1 Billion to small business applicants.

This boom period also started the trend of new lenders and brokers popping into the industry overnight using mainly the same marketing strategies such as UCC Lists, SEO, PPC, Bankcard Portfolio Marketing, and Cold Calling Various SIC Codes. These strategies worked in a decent fashion until the flood of new direct lenders and brokers coming into the industry continued, with these new entrants using mainly the same strategies. Profits were being driven down, new client acquisitions were being driven down, and because a funder’s UCC filings were being called so much, they decided to begin filing them under fake names or only filing them on riskier merchants, or never filing a UCC at all. Also most of the Online Marketing methods became too expensive, pricing the little guy out of the market.

The Future

Now we are in 2015 and new broker entrants are mainly using the exact same strategies from 2008 – 2013, discovering that UCC lists and Cold Calling SIC Codes just will not work efficiently going forward. The Future of profitability and new client acquisition in our space is going to be through Strategic Partnerships. There are three sections of your Strategic Partnerships and they are your Professional Network, Mom and Pop Network, and Online Network.

• Professional Network – The creation of a professional network from referrals such as Banks, Credit Unions, Accountants, Business Brokers, Merchant Processing ISOs, etc., to bring in a high amount of consistent leads of small business applicants who are currently seeking capital.

• Mom and Pop Network – The creation of an external independent broker channel that includes hundreds of random brokers that you sign up to resell your services. You would use the same tongue and cheek, everything is rosey, recruiting ads that I see every week just to get a rush of people on the telephone making cold calls to SIC codes, trying to compete in online marketing, or calling the remains of UCC lists, all with the dream of making a lucrative payday. The volume produced on an individualized basis will be so small it’s irrelevant, but as a collective, they will make up a major chunk of volume. This why I call these sources Mom and Pop.

• Online Network – This is your SEO, PPC, High Traffic Website Ads, and other online advertising methods. These methods will become more expensive going forward and only those with large marketing budgets will be able to truly capitalize in this area with positioning, listings, etc.

Summary

Our space is changing and new broker entrants might want to reconsider investing their capital (time, energy, money and mental health) into this venture. Only direct lenders with team members that were pioneers of this space as well as with the right networks and equity sources, are capable of truly seizing The Future. Those just now trying to come in and ride the wave will soon discover that just like with the Stock Market, the real money has already been made and most of the future returns are already capitalized. As a new broker, you more than likely will fall into that dreaded Mom and Pop category, which isn’t a good position to be in for The Future.

OnDeck Gets Taste of its Own Medicine

May 24, 2015 You know those subtle and not so subtle knocks OnDeck has made about merchant cash advances over the years regarding costs and transparency? Well, the tables have turned.

You know those subtle and not so subtle knocks OnDeck has made about merchant cash advances over the years regarding costs and transparency? Well, the tables have turned.

A supposed unnamed merchant shared their capital raising adventure stories with Fundastic and apparently confused the OnDeck cost factor of 1.24 with an APR of 24%. “The interest rate was 24%, which we thought was excessive, as well as the daily $984 payments we got as part of the deal, but in the end we moved forward with the line,” the business owner reported. A Fundastic editor’s note explained the merchant’s APR was actually around 52% because of the closing fees.

The business owner continued to gripe about not receiving an amortization schedule, as well as the fact that they couldn’t pay off the loan early without incurring a penalty.

Apparently the simplified dollar for dollar cost that OnDeck outlined wasn’t forthcoming enough for them, and they were much more satisfied when they switched to Lending Club.

The merchant then went on to explain that their Lending Club business loan rate was only 9.9%, down from OnDeck’s 24%.

Transparency and full understanding at last?

Ironically, Fundastic had to add yet another note to show that the APR was actually 12.96%. 9.9% was not an APR. “LendingClub had a transparent loan — reasonable interest rate (we have 9.9% + 3% origination for a 2-year loan),” the business owner wrote, yet it seems he was unaware of the APR here either.

Fundastic ultimately concluded, “If you qualify for both LendingClub and OnDeck business loans, I can’t see any reason why you would go with OnDeck. LendingClub’s loans are cheaper in cost [and] more transparent.”

Lending Club might’ve been cheaper in this scenario but the merchant appears to have gotten similar information from both lenders. I’m not sure how much more transparent a lender can be when they spell out exactly how much you have to pay back, though an APR would be useful for certain comparative purposes.

Them’s fightin’ words

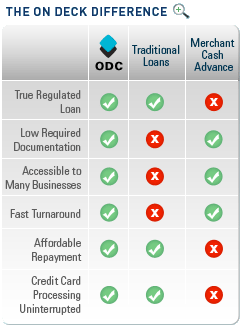

The jab at OnDeck though is reminiscent of the way OnDeck historically attacked merchant cash advances. In a 2008 press release, they wrote, “On Deck Capital fills the void between bank loans and alternative business financing products such as merchant cash advances which, similar to payday loans, charge excessive percentage rates for short term capital.”

The jab at OnDeck though is reminiscent of the way OnDeck historically attacked merchant cash advances. In a 2008 press release, they wrote, “On Deck Capital fills the void between bank loans and alternative business financing products such as merchant cash advances which, similar to payday loans, charge excessive percentage rates for short term capital.”

They even used to display this little chart to explain just how much merchant cash advance sucked compared to them.

Affordable repayment? NOPE!

Meanwhile, OnDeck is still not profitable after 8 years. That either just goes to show how hard it will be for them to compete with Lending Club’s pricing or it indicates that Lending Club is severely underpricing its business loans. It might be the latter.

Lending Club’s business loan program is still highly experimental and dozens of business lenders have entered the space with the belief that undercutting higher priced products right out of the gate will magically yield positive results.

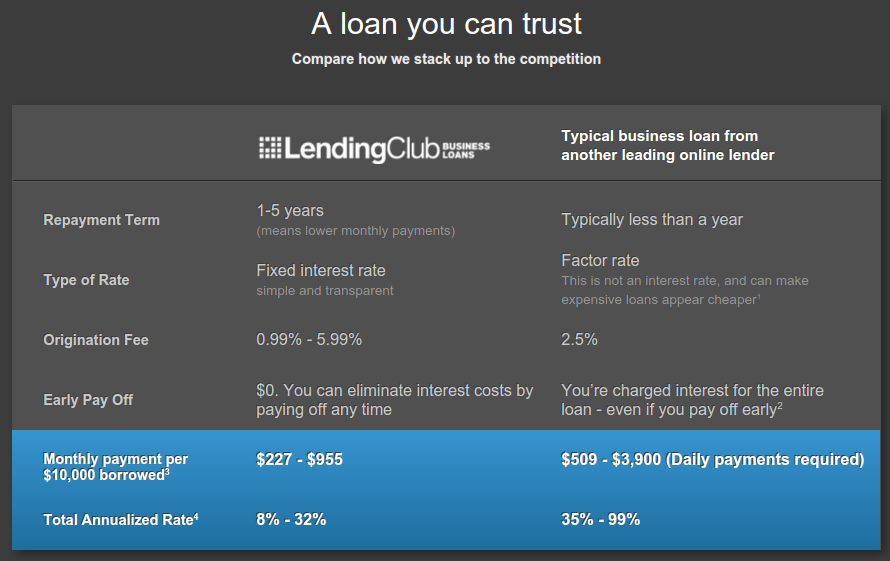

Does this look familiar? OnDeck is being attacked by Lending Club with its own playbook:

And in case you weren’t sure if they were comparing themselves to OnDeck specifically, the 2.5% origination fee is the number that appears right on OnDeck’s website. “We charge an origination fee of 2.5% of the loan amount for your first loan,” it states.

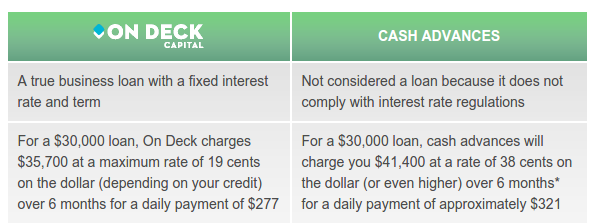

And here’s a snippet of a chart that used to appear on OnDeck’s website:

OnDeck has repeatedly stated that competitive pressure has not been the reason that their interest rates are dropping. It may actually be in anticipation of a brewing public relations war. Lending Club’s supporters are beginning to attack OnDeck in the same way that OnDeck attacked merchant cash advance companies.

Most merchant cash advance companies held firm on their terms over the years and it has paid off. Costs have come down where warranted, but few have been interested to actually underprice their product and risk bankruptcy just to appease criticism.

The circumstances are slightly different for OnDeck who has more to lose as a public company. If their model is dependent entirely on growth and Lending Club begins to snatch some of the lucrative partnerships away from them, their shareholders might suffer in a big way. They can’t have that, so they’re dropping their rates.

Perhaps they should take a page from the merchant cash advance playbook and hold firm, or given their current financials, even raise their rates. Let Lending Club do their thing. Whether the rate is 9.9% or 12.96% is great for a small business, but it’s unlikely to be sustainable or profitable for the lender.

How safe is small business lending really?

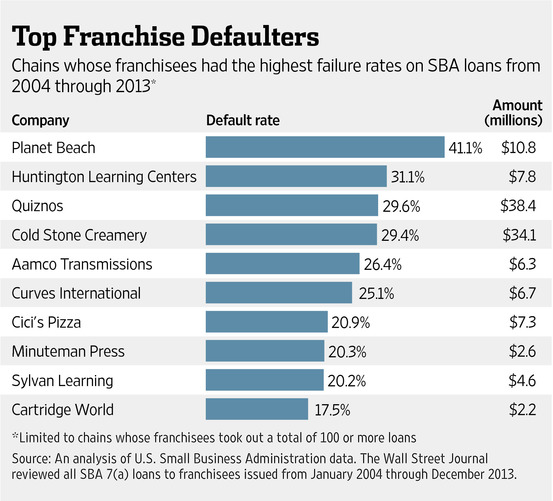

Did you know that 29.4% of all Cold Stone Creamerys that received an SBA 7(a) loan defaulted? 29.4% of all Quiznos have defaulted. 26.4% of all Aamco Transmissions have defaulted.

Scarier yet, the SBA’s special ARC loans that were put together in the wake of the recession had an anticipated 60% default rate across the board.

These figures should serve as a warning to any startup business lender, especially if they’re taking jabs at their higher priced competitors.

It’s a great time to get a loan as a merchant, but a politically tough environment for a lender to price that loan profitably. One day you’re the hot new low cost alternative serving up a public relations beating to the standard bearers of alternative finance, the next day someone’s using the exact same strategy on you.

Can OnDeck take the heat?

The Dumbest Guy in the Room

May 11, 2015 “This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“So what would need to be different in order for this to be a more viable idea? Like what would I need to change and come back with?” I asked.

“Come back?! COME BACK?! Don’t come back,” she shouted while taking my business plan and literally crumpling it into a ball and throwing it on the ground. She then got up and left. She was shaking from the rage. I was the dumbest person she ever encountered and it took effort for her not to kill me.

This experience happened to me three years ago when a NYC-based Venture Capital group sent out invitations to a free seminar and workshop. I liked the refreshing thought of hearing what VCs had to say, especially those not familiar with the merchant cash advance industry. Besides, I had a few concepts I wanted to get feedback on, and thought this would be a great opportunity to do it.

The seminar was more of a fireside chat, held by a zen-like VC I’ll refer to as Rain. He was in his mid-30s, wore a long flowy purple velvet shirt and sat indian style and barefoot in the front of the room. It was a stark contrast to the attendees in the audience, all of whom were wearing suits. Rain walked the crowd through his experience as a VC, most of which seemed to be an annoyance to him. Startups were full of personal drama of which he often got roped into. There was always a partner who was an idiot, a delusion the founder(s) couldn’t see past, or an insatiable need for additional funds.

And during the Q&A at the end, an attendee asked him if he would ever consider using a VC to raise money if he were not a VC himself. “Put the phones down guys, this stays here,” he said. “I wouldn’t.”

However confusing that might come across as, it didn’t change the energy in the room. Just about everyone who attended had an idea for a startup and desperately wanted VC funding.

Afterwards, you were allowed to schedule a one-on-one with one of their startup experts to develop your ideas further. It sounded cool and it was free, so I signed up.

I drafted up a concise business plan based upon a model that was just starting to take root in the merchant cash advance industry. It had its own little twist and I’m sure flaws too, but I believed this one-on-one would be a helpful conversation where I could get honest feedback without giving anything away to potential competitors.

Three minutes into the meeting, I was being scolded. “What do you mean it would break even for the first 2 years?!”

“Oh, well what I’m try –,” I attempted to respond. She talked over me. “You mean to tell me you would make no money in the first 2 years? Are you starting a charity?!”

“Well I was under the impress–,” I started, but she kept going. “This is the absolute dumbest thing I’ve ever seen.”

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

Not me though. I was the dumbest guy in the room, too dumb to even come back with something better. It was a humiliating moment considering I thought this was supposed to be an instructional meeting where the experts would essentially help you master a business plan.

As I walked out of the office towards the elevator, I noticed that even the cheery receptionist who had excitedly welcomed me in, ignored me with her head down as I walked out.

There goes the dumbest guy that ever existed, I imagined she was thinking.

My world spinning as the elevator descended, I tried to recount how it went wrong so quickly. I had showed her a pro-forma P&L that broke even for the first two years as I would reinvest 100% of the profits back into marketing to scale. I personally didn’t like it that way. I wanted to make money, but everyone around me was bleeding red and raising tens of millions along the way. I had started to believe that sacrificing any shred of profitability in exchange for growth is what got investors excited.

My expert didn’t share that view. A business that wasn’t profitable wasn’t a business. It was dumb, and not just regular dumb, but the dumbest thing that anyone ever thought of. EVER.

A couple of days later when I had shaken off the blow to my self esteem, I was thankful for the experience. She was a New Yorker to the core and so was I. I had no inner desire to start a business that didn’t make money (for the sake of disrupting or whatever), but I was being swept up in the craze of companies that were doing just that. She brought me back to reality, though she left a lasting imprint of a boot on my ass.

Three years later, companies with models similar to the one I had cooked up have raised hundreds of millions of dollars. They don’t break even. They lose money, lots of it. But they are looked upon and celebrated as some of the brightest guys in the room. Many of those guys are smarter than me and are probably executing their concepts way better than I ever could. But the lose-a-lot-of-money and grow model isn’t meant for everyone. It all depends on who you’re talking to.

In HBO’s Silicon Valley, a hit that many view as more of a reality show than a sitcom, they poke fun at a truth purveying the California startup scene. Forget profits, the show explains, just having revenues hurts your chances of raising money.

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

Two years ago, Bezos was worth $25 billion and was the 20th richest person in the world. Some experts might say a business model that loses money for 20 years would qualify as the new winner for dumbest thing that ever existed ever. It’s apparently just the opposite.

But once you find an investor that believes in the loss model, do you take the money and then go out and disrupt, hoping that somehow you’ll end up a billionaire?

Loan broker Ami Kassar is faced with that very dilemma. In his recent blog post, he wrote about the offer he has on the table from a VC, “While I could substantially grow my top line – the chances of making any profit are small and the chances of losing money are high.”

Fictional billionaire Russ Hanneman would surely approve, but over in realityville, Kassar is balking. “I can only speculate that they’re more interested in market share – than profits. Their investors want growth. They’re on the venture capital treadmill.”

Admittedly, I poked fun at Kassar, an entrepreneur I’ve often sparred with online. “Should I be worried that in their quest for growth they will build a train and run me over?” He asked in his blog.

Of course I linked to it in the following manner:

Kassar concludes that sustainable long term value is the only logical way forward. Is he wrong?

The current investment atmosphere where anybody with a model and a programmer is raising hundreds of millions of dollars to basically see how fast they can spend it all, is affecting those that have always believed in profits and longevity.

In another post by Kassar just a week earlier, he wrote, “Am I missing the boat and doing something wrong? That’s how I have felt lately as I’ve watched the emergence of the online small-business financing space. It seems every other week I wake up to another announcement about a company in the small-business financing space who has raised a lot of money from venture capitalists at a really high valuation.”

Just last week, consumer lending startup Affirm raised $275 million in a Series B round. Many people in the alternative lending community had never heard of Affirm but they are apparently so good that they can raise a quarter billion dollars.

Investors are scrambling. They don’t want to be left out. On multiple occasions, I have heard of investors skipping basic due diligence in a rush to capture a deal. Some of those deals blew up in a matter of weeks, others in months when they realized they didn’t even know who the owners were or what financial standing they were in.

Lending Club and OnDeck have received billion dollar valuations. That’s what everybody wants, though the market has temporarily cooled on OnDeck, a company that has lost money for almost eight straight years.

Even Shark Tank investor Kevin Harrington has gotten in on it, through his new business loan marketplace, Ventury Capital.

One thing looks certain three years after I met with that expert. The supposed dumbest thing that could ever be conceived of ever has made tons of people millionaires.

A year ago, Kevin Roose of New York Magazine wrote this of profitless startups, “They’re simply taking millions of dollars in venture capital with the hope of keeping prices low, pushing rivals out of the market, and eventually finding a way to turn a profit.” It can be predatory pricing, Roose argues. Basically large venture backed companies can sell below their cost using unlimited funds until the competition is out of business. Then with the entire market all to themselves, they can figure out a model towards profitability.

There seems to be a lot of this happening in the alternative lending space where the lenders backed by hundreds of millions of dollars are not only undercutting the competition at a loss, but they’re running lobbying campaigns that accuse their profitable brethren of being greedy and predatory. The media and general public eat this message up. There is no defense for a lender who has been accused of charging too much by one charging less even if the one charging less will need to declare bankruptcy if it does not raise a fresh round of new capital to sustain operations.

Only the rare observer can read between the lines as Forbes contributor Marc Prosser did. In his own research, he discovered that, “a company which loans money to small businesses at an interest rate of more than 50% was losing money.”

Though I won’t name names, there are a few players out there that believe the answer to their cycle of losses is to push regulatory agencies to attack profitable companies, or at least constrain them through penalties and new laws. Essentially, if it looks like they can’t win the war of attrition, then they might as well stick the government on them.

Speaking of the war of attrition, the race to bring costs to merchants down to zero doesn’t seem to be having the desired effect on the competition. In OnDeck’s Q4 earnings call for example, CEO Noah Breslow said the following:

Overall this market is still characterized by extreme fragmentation. The behavior that we see with our customers is that they might research other competitive options online but then when they actually apply to OnDeck and receive that offer, they kind of have this bird in hand dynamic, and there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they typically just take that offer that OnDeck has provided to them.

Translation: Once merchants have an offer from somewhere, they go with it. There is no price-competitive marketplace on the macro level.

OnDeck has been undercutting the entire merchant cash advance industry for years. None of their competitors have gone out of business, at least not because of a profit squeeze. Instead, everyone is growing, OnDeck included.

So why lose money?

In the case of OnDeck, they can argue that growth has allowed them to expand into Canada and Australia. They’ve forged partnerships with Prosper and Angie’s List. They’ve acquired more data because they’ve done more deals than most. And who is another billion dollar company likely to partner with in the lending space? Probably the one doing 10x the volume of everyone else, the one whose name is all over the place. They have the advantage to win the partnerships.

Five years from now, when the competition is trying to catch up in volume, all the lucrative partnerships might be snatched up already. Maybe it really is about who can spend the most the fastest. It’s a depressing thought.

Some startup vets will you tell that the most important aspect is actually the team. The CEO of 140 Proof for example has written, “You succeed or fail not on the strength of your idea or your product, but on the strength of your team. Venture capitalists fund teams, not business plans.”

With that in mind, I tried to imagine how that meeting three years ago would’ve turned out had I showed up with OnDeck’s CEO Noah Breslow and Lending Club’s CEO Renaud Laplanche in tow. “We’re going to disrupt lending,” I imagine the three of us tell the fierce startup expert.

The expert knew nothing about me. As far as she knew, I was just some random guy off the street holding a stack of papers with an incredulous plot to dominate the lending industry. I had never worked for a bank. I was young. I had no partner. I didn’t graduate from Harvard or MIT. It probably looked pretty ridiculous. “Duhhh so whaddya think?” I imagined I appeared to her.

With her guard down, she had no reason to hold back from saying what she really felt, that the plan was the absolute dumbest thing she’s ever seen.

Might the dumbest guy in the room only be that because he believed what she said? Or did she have it right all along?

Broker Business Planning – Selecting the Right Lenders

May 10, 2015Continuing The “Year of the Broker” Discussion

2015 is certainly the “Year of the Broker,” as the low barrier to entry into our space, in conjunction with various recruiting advertisements promising lucrative pastures, is attracting a variety of individuals with various levels of professional backgrounds. Some entrants have prior experience as a mortgage broker, insurance agent or banking specialist, while others are less familiar with professional sales and are under the belief that our space welcomes a lucrative introduction. Nevertheless, I believe that new broker entrants must be reminded that this is an entrepreneurial pursuit, rather than a get rich quick procedure, and efficient business planning will play a major part in the success or failure of your venture. A part of this efficient business planning, other than the basics of good resources for accounting, legal, marketing, market research, and financing, is the strategic selection of your lender partnerships. The right partnerships will grow, develop and sustain your business, but the wrong partnerships could add your entrepreneurial pursuit to the list of business startup failures.

2015 is certainly the “Year of the Broker,” as the low barrier to entry into our space, in conjunction with various recruiting advertisements promising lucrative pastures, is attracting a variety of individuals with various levels of professional backgrounds. Some entrants have prior experience as a mortgage broker, insurance agent or banking specialist, while others are less familiar with professional sales and are under the belief that our space welcomes a lucrative introduction. Nevertheless, I believe that new broker entrants must be reminded that this is an entrepreneurial pursuit, rather than a get rich quick procedure, and efficient business planning will play a major part in the success or failure of your venture. A part of this efficient business planning, other than the basics of good resources for accounting, legal, marketing, market research, and financing, is the strategic selection of your lender partnerships. The right partnerships will grow, develop and sustain your business, but the wrong partnerships could add your entrepreneurial pursuit to the list of business startup failures.

The selection of your lender partnerships will depend on your unique value proposition (UVP). No entrepreneur should begin a pursuit without a well-defined UVP, for your UVP is the foundation of all of your business planning and return on investment forecasts. Your UVP should answer this question:

Understanding my market segment, what is it specifically that I will bring to the segment that isn’t already being provided by the current crop of solution providers?

The question includes three main components that must be addressed:

- The identification of a market segment

- The characteristics of all services within your industry, being sold to that market

- The services that you will uniquely provide to said market and their unique characteristics

Once your UVP is set, now it’s time to look into the selection of your Lender Partnerships.

Once your UVP is set, now it’s time to look into the selection of your Lender Partnerships.

To begin, let’s say that you decide to come into the industry and target start-up retail/restaurant businesses, that is, those with less than 1 year in operation. Because you are selling working capital solutions, you would research all available working capital options to this market segment which include sources such as nonprofit loans, business credit cards, personal savings, loans from retirement accounts, friends and family, equipment leasing, and merchant cash advances. To serve this market segment efficiently, you would choose to offer merchant cash advances and equipment leasing.

Next, you would scroll through all of the direct lending sources in the country that provide the working capital solution you have decided to lead with, but who also specialize or at least “serve” the target market you are seeking. Many equipment leasing companies do not fund businesses with less than 2 years in business, and many cash advance companies do not fund companies with less than 1 year in business. Your goal would be to find these lenders and create that network, negotiate pricing, workout your commission schedules, and verify all aspects of said partnership to make sure that it’s beneficial for your clients and your office. It should be a win-win-win partnership, a win for your clients as they find a source for working capital that they didn’t know existed, a win for your partner as they obtain “feet on the street (or telephone)” reps without having to pay their overhead, and a win for your office as you are allowed to serve your market and be paid well in doing so.

Due Diligence Is Key

When finalizing your lender selections, make sure all forms of due diligence are completed on the lender(s) to verify their credibility and competency. These forms of research include all of the following:

(( Structure and Legality ))

- The lender should be a licensed direct lender (in states where necessary).

- The lender shouldn’t be a start-up, but instead a proven entity with at least 2 years of operation.

- The lender should have at least directly funded volume in the eight digits (over $10,000,000).

- The lender should have a full staff of employees rather than just one person.

- The lender’s customer service and support departments should be easy to reach.

- The lender should have some sort of press or news media releases on its establishment.

- The lender should specify if they are going to do advances or loans or both.

- The lender’s funding agreements should specify if the transaction will be an advance or loan.

(( Online Presence ))

- The lender should have a fully functional business website, registered for at least two years.

- The lender should have a business email from their business website domain.

- The lender should be BBB Accredited (www.BBB.org) with at least an A rating.

- The lender should be a part of business associations with logo(s) displayed on their website.

- The lender should be included on basic online business directory listings.

(( Broker Respect ))

- The lender should provide a comprehensive Broker Agreement full of legal provisions.

- The lender’s Broker Agreement should spell out all provisions of the relationship.

- The lender’s Broker Agreement should spell out any quotas.

- The lender’s Broker Agreement should spell out new/renewal deal commission structure.

This is a rough introduction and surely there are other criterion that are important in selecting your lender partnerships. However, these recommendations will surely give you a head start as you head into one of the most competitive industries in financial services.

The OnDeck Hedge

May 6, 2015 Days after OnDeck went public in December 2014, a handful of their competitors licked their lips and said, “Perfect. Now we can hedge ourselves.”

Days after OnDeck went public in December 2014, a handful of their competitors licked their lips and said, “Perfect. Now we can hedge ourselves.”

But can they really?

OnDeck isn’t quite merchant cash advance and not quite Lending Club. They might be heralded in news media as the poster child for the non-bank business financing movement but one could hardly say that they typify the average company in the industry. They do things their own way and always have. It’s the very reason they are often criticized by their competitors. OnDeck doesn’t represent an industry but rather an antithesis to an industry they were borne out of.

That’s not to say there aren’t many common denominators between their products and others such as merchant cash advances. There are. But as an outside investor who wanted to be long on the success of the merchant cash advance industry, OnDeck isn’t a perfect match. And if they wanted to be long on non-bank business lending, the daily payment short term system at the core of the company probably isn’t what an investor had in mind.

OnDeck presents only one investment opportunity, themselves.

But what if you short them? That’s the trade some funders and lenders talk giddily about over drinks as the answer (at least hypothetically) to an eventual economic downturn. How do you hedge your own portfolio’s losses? Just short OnDeck! or so the theory goes.

I don’t doubt that some folks have secretly placed the OnDeck hedge in their back pocket as a legitimate possibility, but I’m not sure anyone has really thought this through.

First, many funders rely on credit facilities from third parties to fund deals and scale operations. That means restrictions and covenants on how the money is allocated. I don’t think taking a multi-million dollar short position on a single stock was what the institutional lenders had in mind. Business lenders and merchant cash advance companies are not hedge funds. The immediate reaction to a downturn (whether miniscule or massive) should be to reduce the default rate, tighten underwriting, and cut costs, not take huge positions in the securities markets.

The logic behind this trade is almost like realizing that the restaurant you own is on fire and instead of running for water to put it out, you call an insurance company and take out a policy on the neighboring businesses instead. If those businesses burn down, you get paid, and the loss from your own restaurant burning down will be offset. Except now your business is gone.

The logic behind this trade is almost like realizing that the restaurant you own is on fire and instead of running for water to put it out, you call an insurance company and take out a policy on the neighboring businesses instead. If those businesses burn down, you get paid, and the loss from your own restaurant burning down will be offset. Except now your business is gone.

Second, OnDeck isn’t a perfect match for this trade. In Barroom small talk, the hypothetical circumstances surrounding a hedge are less often an economic downturn and more often about everything going to hell. If everything goes to hell, we can just short OnDeck!

Except there are many sane reasons why OnDeck would soar in such a scenario. If purchases of future sales were interpreted to be usurious loans, well then that might cause everything to go to hell for merchant cash advance companies but boost the value of OnDeck who has been cognizant of state usury laws and the complexities of being an actual lender for some time now.

And if business lenders issuing 5 year loans with monthly payments are all falling apart, it’s possible that OnDeck with their 1-year terms and daily payment schedules would be a refuge.

Just yesterday, OnDeck beat the street’s expectations and then for some reason immediately lost more than 15% of their market capitalization. Bloomberg’s Zeke Faux ran the following headline, OnDeck Tumbles as Competition Forces Online Lender to Cut Rates, despite OnDeck’s execs specifying TWICE in the earnings call that competition had no bearing in their decision to cut rates.

While beating the street and subsequently getting clobbered may lend credence to the phrase, “buy the rumor, sell the news,” there wasn’t anything particularly jarring in the report to warrant such a huge sell-off. OnDeck doubled year-over-year revenues and they funded an astounding $416 million in loans in a single quarter.

The 15+ day delinquency ratio increased from 7.2% to 8.4% year-over-year however. CEO Noah Breslow and CFO Howard Katzenberg defended this as normal Q1 seasonality but were non-committal to the direction this would move in future quarters. Maybe that’s what spooked investors? It’s tough to say.

Had CAN Capital been publicly traded too, should OnDeck have taken a short position on them when they saw their own 15+ day delinquency rate spike? And should OnDeck buy put contracts on competitors that also eventually go public, you know… just in case everything goes to hell?

Probably not.

The only investment OnDeck should focus on making is in themselves. Leave the trades to the hedge funds who may actually be in the business of buying insurance contracts on a burning restaurant’s next door neighbors.

The only hedge to a failing business is to create a business built to last. Shorting OnDeck makes for entertaining barroom chatter, but it cannot be a serious fallback for a funding company worried about their portfolio.