Addressing Stress and Depression Over Declined Deals

July 29, 2015 I wanted to add to my series discussion by touching on a topic that isn’t often discussed in our space, and it pertains to dealing with depression, stress and other mental health related conditions over the loss of a deal.

I wanted to add to my series discussion by touching on a topic that isn’t often discussed in our space, and it pertains to dealing with depression, stress and other mental health related conditions over the loss of a deal.

Let’s Be Honest

Let’s face it, most of us (as brokers) work on a 100% commission structure, or derive a significant portion of our income from commission, this means that our compensation is based on performance. This performance is directly correlated to the amount of new/renewal business that we fund. The word fund is the keyword here, as your performance in terms of selling might be excellent with the continued production of new leads, new applicants and new interested parties to our industry’s working capital selections. However, if those new leads and applicants don’t fund, then in terms of your performance, they don’t count. An applicant can be declined for a variety of reasons and all of them are usually totally out of your control. However, your compensation is dependent upon your merchant’s approval as well as the offering of terms/conditions that they deem acceptable. This high level of stress can lead to mild bouts of depression, and that depression could lead to a variety of other issues such as overeating, not eating, over sleeping, not sleeping enough, emotional breakdowns, paranoia, personal relationship issues, along with a variety of other inefficiencies.

The Loss Of Hope

Google says that the definition of depression is related to “the feelings of severe despondency and dejection.” Despondency and dejection refers to a state of low spirits caused by the loss of hope, and hope is sometimes all we have as Brokers. All we have going for us is an internal “hope” that our sales abilities will produce the commissions needed to not just cover our business/tax expenses, but cover our personal expenses, insurance, etc., and leave some left-overs to allow us to save for retirement. If you put your soul into this (like I do), then with every funded deal you will rejoice internally, and with every deal declined or approved with terms that are unacceptable to your client, you might feel sudden emotions of panic, fear and uncertainty. As a one man show, I have funded hundreds of deals while also building up a side merchant processing portfolio that processes tens of millions in volume every year. But I have also lost a ton of potential deals on both the funding side and the merchant processing side through declines or approvals that were unacceptable to my client. If left unchecked, still to this day I feel emotions of sickness and depression over declined and lost deals, so much so that sometimes I just have to go home and lay down in the bed for a minute.

Tackling The Stress Through Other Means Of Management

So how do I handle depression and stress over declined and lost deals for the most part? Here are some tips on how I handle the stress and depression of this industry, and perhaps they too can provide some assistance for you in those critical, nerve-racking situations of receiving emails from your Funder with “Declined” or “Application Ineligible” typed out in the Subject Line:

Diversify, Diversify, Diversify

This isn’t just true in Stocks, but it’s also true in being an Independent Agent/Broker. You are a 1099 Independent Sales Office and there’s just no reason why you ought to only be selling one product. Remember as I touched on in prior AltFinanceDaily articles, as a Broker your job is to be as Jeff Thull from Prime Resource Group explains, which is to be a valued source of business advantage for your prospective and current clientele. You should have access to knowledge, resources, networks, products and platforms that your prospective and current clientele lacks access to, allowing them to see you as a “valued extension” of their organization in terms of the value of your expertise and network.

So there’s no reason that you should just be selling Merchant Cash Advances or Alternative Business Loans, you should be selling a variety of other products in various different segments such as POS Systems, Merchant Processing, Equipment Leasing, Insurance, Big Data, Marketing Programs, Cost Reduction Programs, etc., just to name a few.

Do This Because It’s Your Purpose, Not Just For The Money

Listen, I’m not here to convert anybody to any particular Religion, but I believe that if you are going to be an entrepreneur (which is what you are as a 1099 Broker/Agent) then you need to have a very strong internal spirit or soulful foundation. Your motivation, joy, peace and confidence should extend beyond your earthly circumstances. You should see this industry as something you do as a Purpose that aligns with your spirit or soulful foundation, rather than just seeing it solely as a means to make an income.

Continued Learning and Development

The Merchant Services related industry continues to evolve and you should be following all of the trends and updates. The best places to do this for the Merchant Services related industry, is to make sure to follow AltFinanceDaily as well as other sources such as The Green Sheet, Payment Source’s ISO/Agent, The ETA, The SBFA, as well as various industry trade conferences such as LendIt and The AltLend Summit.

Focus On Total Financial Management

Focus On Total Financial Management

Financial management is not just about bringing in decent income, it’s about managing the six pillars of finance which are Income, Investments, Insurance, Credit, Expenses and Taxes.

For example, you might be bringing in $100,000 a year in commissions from your Home Office, but you might be living in a high cost of living area, have horrible spending habits, have inefficient tax reduction strategies, and you have four children from four different women paying very high child support claims. This means that your expenses are too high and your financial efficiency is going to be off.

On the other hand, you might be making $50,000 a year in commissions from your Home Office, with no children, living in a low cost of living area, with efficient budgeting and tax reduction strategies, putting away let’s say $7,500 a year into your retirement accounts. If you do this for 40 years from 25 – 65 for example, with just a conservative 5% per year return, you will have over $1 million at age 65. You will have made yourself a self-made millionaire and you didn’t need a six figure annual commission compensation to do it. All you needed was Total Financial Management.

To Wrap

So in a nutshell, I manage the stress and depression of our industry through having a totally efficiently managed financial system in place, not selling just one product, always learning, and making sure that everything I do is grounded in Purpose. I believe that if you too were to adapt some of these techniques, the loss of that deal you worked so hard on, might not “sting” as bad after all.

A Square IPO Would Be Alternative Lending’s Third

July 26, 2015 First Lending Club, then OnDeck, and now… Square? The news media was flooded with stories late last week that payments company Square had filed their S-1 in secret. The move can be done under a JOBS Act provision that allows companies that grossed less than $1 Billion in revenue in the most recent fiscal year.

First Lending Club, then OnDeck, and now… Square? The news media was flooded with stories late last week that payments company Square had filed their S-1 in secret. The move can be done under a JOBS Act provision that allows companies that grossed less than $1 Billion in revenue in the most recent fiscal year.

Square’s merchant cash advance arm, Square Capital, reportedly funded $100 million to small businesses in 2014, a figure large enough to earn them a spot on the AltFinanceDaily leaderboard.

While often reported as a lending program, Square’s own website describes their working capital transactions as sales of future credit card receivables. At face value, and aside from what their contracts might actually say, it’s a textbook merchant cash advance.

While some publicly traded companies have dabbled in merchant cash advances, the financial product is one of Square’s two major products, the first obviously being payments.

And while OnDeck offers loans that are very similar to merchant cash advances, Square could potentially be the first true merchant cash advance IPO.

Also on the IPO watch list is CAN Capital, a company that offers both loans and merchant cash advances. In November of last year, Bloomberg and WSJ claimed the company was already working on it. While it has been eight months since that news came out, word on the street is that a CAN Capital IPO is still very much a possibility.

Unfortunately, because of the same JOBS Act provision that allowed Square to file an S-1 (if they actually did) also applies to CAN Capital. There is no way to know what’s going on behind the scenes until the filing is made public or leaked to the media.

Either way, the end of 2015 will likely end in at least one more IPO for the commercial side of alternative lending.

Could Jack Dorsey and his wacky beard be the future face of the merchant cash advance industry?

BREAKING: JACK DORSEY’S BEARD pic.twitter.com/Quv8nVG9PZ

— Nicholas Carlson (@nichcarlson) June 12, 2015

Federal Government Wants Your Thoughts About Online Lending

July 19, 2015 Whether you’re a funder, lender, broker, or platform, the U.S. Treasury Department deserves to hear your input.

Whether you’re a funder, lender, broker, or platform, the U.S. Treasury Department deserves to hear your input.

Only July 16th, the Treasury announced that it was seeking public comment on various business models and products offered by online marketplace lenders to small businesses and consumers. One stated purpose of this is to study “how the financial regulatory framework should evolve to support the safe growth of the industry.”

The comment period is only open for six weeks.

Over the last year, many funders and brokers have voiced their opinions on best practices, ethics, and standards. Some want regulation to curb what they believe to be immoral behavior and others just want clarity where the laws are obscure, illogical, or even in conflict with themselves.

In at least one recent case, a merchant cash advance company CEO wrote about the complexity of dealing with an endless amount of state laws. In Lift the Fog, Give us Regulation, Merchant Cash and Capital CEO Stephen Sheinbaum wrote, “It is also better, at least for the financial services industry, if the central government is the one to craft the regulation instead of getting one rule from each of the 50 state governments.”

Meanwhile the Consumer Financial Protection Bureau (CFPB) will eventually start to enforce the amendments to the Equal Credit Opportunity Act, which technically already became the law under Section 1071 of the Dodd Frank Act. As part of that, underwriters of business loans and merchant cash advance alike may no longer be allowed to meet applicants, speak with them on the phone, examine their driver’s licenses, review their social media profiles, or even ask what their business model is or how they market themselves.

One has to look at any opportunity afforded by a government agency to share input before future regulations are implemented then as a duty. It might not matter, but you should do it anyway, just like voting.

Below are the questions, the Treasury wants you to answer (or Click to view on Treasury.gov):

1. There are many different models for online marketplace lending including platform lenders (also referred to as “peer-to-peer”), balance sheet lenders, and bank-affiliated lenders. In what ways should policymakers be thinking about market segmentation; and in what ways do different models raise different policy or regulatory concerns?

2. What role are electronic data sources playing in enabling marketplace lending? For instance, how do they affect traditionally manual processes or evaluation of identity, fraud, and credit risk for lenders? Are there new opportunities or risks arising from these data-based processes relative to those used in traditional lending?

3. How are online marketplace lenders designing their business models and products for different borrower segments, such as:

• Small business and consumer borrowers;

• Subprime borrowers;

• Borrowers who are “unscoreable” or have no or thin files;

Depending on borrower needs (e.g., new small businesses, mature small businesses, consumers seeking to consolidate existing debt, consumers seeking to take out new credit) and other segmentations?

4. Is marketplace lending expanding access to credit to historically underserved market segments?

5. Describe the customer acquisition process for online marketplace lenders. What kinds of marketing channels are used to reach new customers? What kinds of partnerships do online marketplace lenders have with traditional financial institutions, community development financial institutions (CDFIs), or other types of businesses to reach new customers?

6. How are borrowers assessed for their creditworthiness and repayment ability? How accurate are these models in predicting credit risk? How does the assessment of small 10 business borrowers differ from consumer borrowers? Does the borrower’s stated use of proceeds affect underwriting for the loan?

7. Describe whether and how marketplace lending relies on services or relationships provided by traditional lending institutions or insured depository institutions. What steps have been taken toward regulatory compliance with the new lending model by the various industry participants throughout the lending process? What issues are raised with online marketplace lending across state lines?

8. Describe how marketplace lenders manage operational practices such as loan servicing, fraud detection, credit reporting, and collections. How are these practices handled differently than by traditional lending institutions? What, if anything, do marketplace lenders outsource to third party service providers? Are there provisions for back-up services?

9. What roles, if any, can the federal government play to facilitate positive innovation in lending, such as making it easier for borrowers to share their own government-held data with lenders? What are the competitive advantages and, if any, disadvantages for nonbanks and banks to participate in and grow in this market segment? How can policymakers address any disadvantages for each? How might changes in the credit environment affect online marketplace lenders?

10. Under the different models of marketplace lending, to what extent, if any, should platform or “peer-to-peer” lenders be required to have “skin in the game” for the loans they originate or underwrite in order to align interests with investors who have acquired debt of the marketplace lenders through the platforms? Under the different models, is there pooling of loans that raise issues of alignment with investors in the lenders’ debt obligations? How would the concept of risk retention apply in a non securitization context for the different entities in the distribution chain, including those in which there is no pooling of loans? Should this concept of “risk retention” be the same for other types of syndicated or participated loans?

11. Marketplace lending potentially offers significant benefits and value to borrowers, but what harms might online marketplace lending also present to consumers and small businesses? What privacy considerations, cybersecurity threats, consumer protection concerns, and other related risks might arise out of online marketplace lending? Do existing statutory and regulatory regimes adequately address these issues in the context of online marketplace lending?

12. What factors do investors consider when: (i) investing in notes funding loans being made through online marketplace lenders, (ii) doing business with particular entities, or (iii) determining the characteristics of the notes investors are willing to purchase? What are the operational arrangements? What are the various methods through which investors may finance online platform assets, including purchase of securities, and what are the advantages and disadvantages of using them? Who are the end investors? How prevalent is the use of financial leverage for investors? How is leverage typically obtained and deployed?

13. What is the current availability of secondary liquidity for loan assets originated in this manner? What are the advantages and disadvantages of an active secondary market? Describe the efforts to develop such a market, including any hurdles (regulatory or otherwise). Is this market likely to grow and what advantages and disadvantages might a larger securitization market, including derivatives and benchmarks, present?

14. What are other key trends and issues that policymakers should be monitoring as this market continues to develop?

The Treasury asks that you include your name, company name, address, job title, email address, and phone #. You can submit your responses on http://www.regulations.gov/. Just click on the tab that says “Are you new to the site?”

You can also submit by mail:

To: Laura Temel,

Attention: Marketplace Lending RFI,

U.S. Department of the Treasury, 1500

Pennsylvania Avenue NW., Room 1325

Washington, DC 20220

If you have questions, email marketplace_lending@treasury.gov or call 202-622-1083.

Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree

July 16, 2015Bank statements. Those in consumer lending argue they’re all but irrelevant because FICO and credit reports do the job of predicting risk just fine, but over in today’s small business lending environment, there’s an entirely different sentiment; Reveal your recent banking history or be declined.

After having bought nearly $60,000 worth of consumer notes on Lending Club and Prosper combined, there’s something I’ve seen a lot of, bounced ACHs.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

For all the fanfare surrounding online marketplace consumer lending, access to borrower banking history is oddly absent.

“Welcome to consumer lending, where the rules are different because the game is too,” replied a user to my comment on a peer-to-peer lending forum.

Veteran consumer lenders assumed I was a lost newbie who knew nothing about lending. “I have a feeling if you ask to crawl someone’s bank account, they’ll just go elsewhere,” one user said. “Seems that’d only work on subprime borrowers who have limited bargaining power.”

“I’m assuming you may be new to lending,” he continued. “Making a loan based on deposit balances is rarely a good idea.”

My initial question to them was that without bank statements, how could they ascertain if a borrower’s finances were actually in order at least at the time the loan was issued? It’s really easy to access someone’s banking history for the last 90 days by using common tools like Yodlee or Microbilt, I argued.

Some people sympathized with my logic but others believed requesting bank data would be suicide in today’s competitive environment. And still more wondered if there might be consumer protection laws that prevented lenders from seeing a loan applicant’s banking records (which sounded ridiculous).

A Credit Card Issuer’s Take

Those questions led me to interview an underwriting manager at one of the nation’s largest credit card issuers who would only speak on the condition of total anonymity, including the bank’s name. There, he oversees a department of people that manually assess credit card applicants. There is no algorithmic approval process. In his department, humans underwrite each application, conduct phone interviews with the prospective borrowers, and request additional documents if they feel it’s warranted.

Requesting bank statements is a regular part of the job, explained the manager. “We require proof of income for any line over 25k,” he added. “It’s the main thing we ask for along with proof of address.”

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

“The Adverse Action reason [for that] would be ‘sufficiently obligated’,” he stated. “That’s when their bank account shows they can not take on any additional financial obligations.”

The manager shared however that he believed there is a very strong correlation between what’s on the credit report and what to expect in the bank statements. Generally speaking, good credit will show a healthy banking situation, he explained. They’re rarely taken by surprise. Overall, the credit reports and phone interviews are enough for them to feel comfortable and the bank statements are really just there to check off a compliance box.

Meanwhile, those that speculated requesting bank data would be a death knell competitively might want to talk to Kabbage’s sister company, Karrot. Karrot already crawls bank accounts as part of their consumer loan application program and competes with Lending Club, Prosper, and Avant. Considering Kabbage has funded more than half a billion dollars worth of business loans using this very methodology, it’s safe to say that applicants aren’t flocking to competitors in droves over the perceived injustice or inconvenience of filling out three additional fields on a web application to share their transaction history.

Bounced Payments

Kabbage CEO Rob Frohwein offered these comments last year about their underwriting, “A critical aspect of consumer lending is determining the appropriate amount of a payment to collect so that an account doesn’t become overdrawn. Our intelligence accurately predicts how much of a payment to request via ACH so consumers avoid the cost and headache associated with non-sufficient funds.”

I thought about those statements when I noticed that thirty-six of my Lending Club notes carried a Grace Period status the other day. These are borrowers whose payments just recently bounced. Some are only three or four months into a five-year loan. Worse, there are those that are saying they have no money whatsoever to make a payment. How can this be when they just practically got approved?

To the consumer crowd it’s business as usual. “If you got their bank account, you still wouldn’t be able to predict who will default. You can’t predict defaults on any individual borrower,” argued one veteran on a forum.

But it’s not all about the lender’s tolerance for risk. ACH rejects can have consequences that affect a lender’s ability to debit accounts in the future.

“Ultimately, regulatory thresholds set by NACHA will continue to become more and more critical of returns,” said Moe Abusaad of ACH Processing Co, an ACH processor based in Plano, TX. “I think it’s safe to say that there is a positive correlation in considering statements as a component of the underwriting process to the rate of returns incurred,” he added.

And while it’s true that bank data can’t make predictions perfectly on its own, nobody in small business lending or merchant cash advance would consider an approval without it.

Bank Statements or Bust

“There is no substitute for banking information when reviewing a client for approval,” said Andrew Hernandez, a co-founder of Central Diligence Group, a risk management firm that allows business lenders and merchant cash advance companies to outsource their underwriting.

“Money moves fast through these businesses and every business is unique, so a lot more variables come into play than just having to account for the timely monthly payments of credit cards, cars, and mortgages as you find in the consumer world,” he added. “A FICO score along with other information presented in a credit report provide a detailed, historical snapshot of a client’s creditworthiness in consumer lending, and while these are great complementary tools for us to use in our underwriting process, I believe that banking data paints us a picture of its own which is absolutely essential in assessing the risk of a B2B transaction in our space.”

Those underwriting business loan deals have reported seeing applicants with open personal loans from Lending Club, which shows that the exact same borrowers are being underwritten in two different ways.

But Julio Izaguirre, another co-founder of Central Diligence Group added that, “banking transactions are essential in gauging the cash flow of the business by looking at recent and up-to-date bank volume, but it is even more important with businesses that lack historical data and cannot provide financials or other documentation to show and prove their track record.”

Translation: A lack of credit history and formal financial statements can be overcome thanks to in-depth analysis of bank account data.

“When our underwriters look at a bank statement you can get a better understanding of the business cash flow, operational cost and how the owner manages his business,” said Heather Francis, CEO of Gainesville, FL-based Elevate Funding. “The credit score is like a person’s blood pressure reading,” she continued. “It indicates there may be an issue but until lab work is pulled and analyzed you don’t know what that issue is. The bank statement is that lab work and it can tell you more about the issues behind the scenes than a credit score can.”

Greg DeMinco, a Managing Partner of Americas Business Capital based in Cherry Hill, NJ would probably agree. “FICO isn’t everything,” he shared. “Bank statements can tell a great story especially if there is upward momentum month after month, and more importantly a high ratio of deposits to requests for the advance.”

Meanwhile, the manager of the credit card issuer was surprised to hear about the high value placed on bank statements in business lending. I offered him the example of an applicant with good credit that was consistently negative in the bank because of a reliance on overdraft protection as a way to make sure all the bills were being paid. “That’s the craziest thing I ever heard,” he commented.

But over in the peer-to-peer lending forum it didn’t sound so crazy at all. “Plenty of Americans are ‘broke’, in the sense that they have negative net worth, yet they’ll continue servicing their debts for… a long time… no matter what it takes,” shared one user.

The argument seems to come full circle, that business lending and consumer lending are just different.

But to Isaac Stern, the CEO of New York-based Yellowstone Capital, the bank statements are not just about financial health. “We are literally underwriting against fraud,” said Stern, who said his office regularly receives applications with doctored statements. “Logging in [to the banks] and verifying those statements are probably the most important part of the process,” he noted.

His logic goes that a consumer that is paid a salary has a predictable stream of income and so that information along with a credit report might be enough for a consumer lender, but business revenue is less predictable and can vary practically day-to-day.

“You can’t just look at a FICO score and say, ‘this is a good a business’,” Stern explained. “The story is in the bank statements.”

A Decade of Funding

July 7, 2015Next month is my 9 year anniversary in the merchant cash advance industry, which means I’ll be starting my 10th year. A decade of merchant cash advance… holy shit. I’ve had the opportunity to view it from many different angles and have accrued my fair share of adventures, plenty of which I’ve written about and others I’ll have to take to my grave.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

Looking back now, there weren’t many people keeping a live diary of events as the industry dove headfirst into the financial crisis. Who would’ve bothered to report on an industry that was arguably made up of only a thousand people?

In April 2009, even before AltFinanceDaily launched, I submitted a story to the only merchant cash advance magazine of its kind. It didn’t have a very clever name, just Merchant Cash Advance Publication. My story, titled, An Underwriter in Salesman’s Clothing, rambled on about the end of the industry’s glory days, the wave of declined deals in the recession, and how funders should be more appreciative of ISOs.

Here’s a summary of what I wrote more than six years ago:

Here’s a summary of what I wrote more than six years ago:

I was complaining about stacking as far back as 2007 apparently. I addressed it as a merchant problem. Merchants were taking advantage of funders, not the other way around like some frame the argument in 2015.

I left my post as Director of Underwriting in late 2008 because “I wanted the ringing phones, the commotion, the markerboards with stats, the glory, the $20,000 [monthly] checks.”

Funding companies became super conservative during the financial crisis and all my deals were being killed (25 deals declined in a row at one point.)

I had recently charged my first closing fee, felt bad about it, and got in trouble for it.

I said 1.40 factor rates wouldn’t last (I was wrong about this!)

I bitched about algorithmic declines (I apparently thought computers underwriting files was a good way to upset ISOs.)

I acknowledged my own hypocrisy when I realized how hard it was to be a sales rep after thinking sales reps were overpaid and overrated in my previous years as an underwriter.

I continued on as a sales rep for another two and a half years after I wrote that. That means that in 2010 when I started AltFinanceDaily, I was still calling UCCs, closing deals and boarding merchant accounts while sitting in a windowless room rented by a startup ISO.

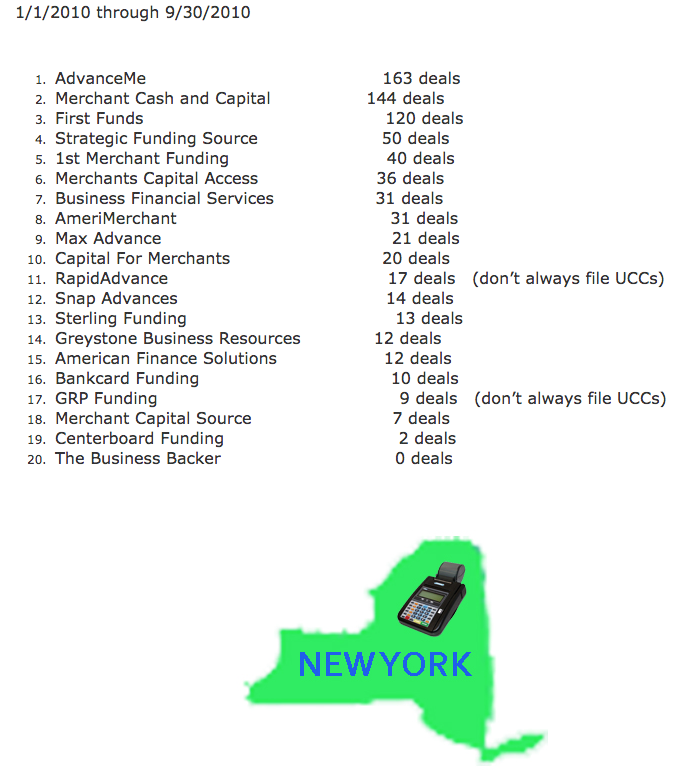

But what was there to blog about in 2010? Oh little stuff like who the biggest funding companies were at the time by checking UCC filings since almost everyone filed UCCs back then. Notably, the third largest merchant cash advance company of 2010, First Funds, is no longer in business.

I also wrote about shopping deals around and the impact that might have on a merchant’s credit report. That was the day-to-day stuff though, information I was just putting out there hoping someone on the Internet might see it. What got everyone excited was the 2010 New York State leaderboard which eventually prompted me to spend my nights and weekends investigating the industry on a wider level.

I began talking to people at other funding companies about their monthly numbers. It wasn’t that hard to get information as an industry insider, especially if you had deals to send somebody’s way. I also spent money to acquire secured party lists to count the number of UCC filings by funders in all 50 states rather than just look at one free state like I did with New York originally. I think I was the only person in the industry at the time running up their personal credit card bill to conduct such research. I had also been in the industry for four years at that point and had a great network of contacts who could clue me in on their volume.

While I said that I also looked at census records and department of labor records, I’ll admit that data wasn’t extremely useful. The end result was a best guess estimate that in 2010, there were approximately 21,000 merchant cash advances transacted for $524 million.

My data would go on to be republished in ISO&Agent Magazine, The Scotsman Guide, and Leasing News, and also end up in many other places I didn’t expect, like in the business plans of merchant cash advance companies that were looking to raise capital. In fact, in a private meeting I had with an MCA company months later in South Florida, the CEO let me take a peek at the docs they had just submitted to a bank for a credit facility. Included was a printout of these numbers with my name on it and all. Apparently there was something to this writing thing…

My last day as a sales rep was in the Fall of 2011. I left the commission-only life (oh what, you 2015 pansy closers actually get a base salary?) for something even more risky, an entrepreneurial life. For a couple years, I played underwriting consultant to a handful of merchant cash advance companies and industry expert to institutional investors interested in the space. I learned how to code in my spare time and spent more than a year in online lead generation.

I never stopped writing.

Along the way I’ve visited the offices of dozens of ISOs and funders, syndicated in deals, and test-drove new technology.

None of this makes me particularly special, especially when I hear about how much some of my old sales buddies are making these days on deals. “Are you SURE you don’t want to come back?” they ask. It’s enticing no doubt. A part of me wants to grab the phone out of their hand and attempt to shatter their record on the markerboard this month even though I’m pretty sure I’m rusty as hell.

One thing noticeable between now and 9-years ago is that my hair turned grey. This industry will do that to you (or at least it did to me.) And I still get a kick out of meeting folks who got into the industry years before I did. The 90s/early 2000s AdvanceMe crowd likes to tell me that they were funding merchants while I was still in diapers. They are practically right.

As I enter my own tenth year in the biz however, it’s exciting to think that the industry is just now getting started. OnDeck was the first IPO in the space and the general public is learning about short term business funding for the first time. There’s no shortage of news to report and that keeps me plenty busy these days.

And so even after a decade of MCA, it’s never too late to put on your Funded pants. Opportunity awaits and I hope you’ll continue to ride the wave with me. Thanks for reading since 2010!

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after AltFinanceDaily sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on AltFinanceDaily’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as AltFinanceDaily’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

Still Reviewing Paper Bank Statements? Stop

June 26, 2015 Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Technology has made it easier to create authentic looking documents and the rise in online lending seems to be bringing out the worst in people. Somebody in a desperate situation might not have the guts to look a banker in the eye and hand him a stack of fraudulent documents but they might roll the dice with somebody over the Internet they’ll never have to meet.

The fakes aren’t obvious anymore. Anyone can go online and buy doctored documents from professionals. The business is booming on Craigslist for example where fraudulent documents can be made to order in under an hour.

In the Miami area, fraud hucksters are even beginning to offer deals such as buy 2 fake documents, get 1 free.

Industry-wide, funding companies are complaining that attempted fraud is out of control. One broker recently took to the dailyfunder forum to share her frustration. “I can spot them a mile away!!! 2 different deals submitted this week with fraudulent statements!!!,” she vented.

Other brokers chimed in, sharing their stories such as a merchant whose doctored statements were only noticed because ATM withdrawals were listed with odd amounts like $90.83.

Oddly, nobody seems to be reporting this fraud to the authorities. It all seems to get swept under the rug as business as usual. Orchard co-founder David Snitkoff for example, was asked just last month about the rate of marketplace lending fraud and he apparently said, “No worries, none to date.” He seemed to be implying that fraudulent applicants are getting screened out. But that doesn’t mean people aren’t trying.

Seven months ago, merchant cash advance underwriter Pierre Mena wrote in detail about the challenges he faces in detecting fraud. He said:

Some of the more well hidden fraud can usually be found by comparing the summary page and last page of the bank statement to other statements. Typically, most banks and some credit unions offer you a snapshot of the starting balance, which should generally match up with the ending balance of the previous month. If it doesn’t, you should look for any transactions from the previous month that did not settle until the current month. If there is none, this is usually a red flag indicating that the merchant forgot that statements are continual time series financial data whose totals carry on to the following month.

-Pierre Mena, Rapid Capital Funding

A lot of these issues can be easily overcome by simply disregarding paper statements altogether. Microbilt’s instant bank verification tool for example, will allow you to pull the most recent 90 days worth of transaction data directly from the banks themselves. Funders using these automated checks swear by their effectiveness and the capability is essential for any company that wants to scale.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

Cultural differences play a role in this according to Gil Zapata, the founder of Florida-based Lendinero. Zapata recently wrote that latino business owners over the age of 45 are not accustomed to doing business over the Internet, email, fax, or phone. “This group has a high level of distrust in doing business via the Internet,” he said.

So is there a middle ground? On the dailyfunder forum, Chad Otar, a managing partner of Excel Capital Management said that he tells merchants they can change their online banking passwords after a verification. And Andy McDonald of Yellowstone Capital wrote that verifying the bank data is beneficial for the merchants too. “It protects the merchant by allowing us to check their account to make sure our pulls aren’t going to bounce,” he wrote in a thread back in April. He also added that he comes across 2-3 applications PER DAY with altered statements.

Humans can only do so much. Pierre Mena actually wrote, “Some of these statements are doctored so well that you may have to zoom in upwards of 300% to find a comma that should actually be a period to separate dollars from cents.” At this point, an instant bank verification would probably work wonders.

Online business lender Kabbage might have the best model. On their website, applicants are instructed to enter their email address followed by their bank account username and password. Their system will analyze their bank transactions and if eligible, will then ask the applicant for their first and last name. It flies in the face of all the pushback that funders claim merchants give them over data privacy and security.

Four months ago Kabbage announced they were already up to funding $3 million per day. Obviously there is an entire segment of small business owners that are sucking up whatever concerns they had about bank verifications in order to get the capital they need.

The majority of the small business financing industry is still relying on paper statements and probably shouldn’t be. If you have to zoom in upwards of 300% to find a comma that should actually be a period and if con artists are offering discounts for bulk orders of fraudulent statements, it may be time to throw in the towel and join the rest of the world in using the Internet…

Dear Brokers, Investors Love You Too

June 25, 2015Hedge funds, private equity, and family offices have been all hot and bothered by lending marketplaces and direct funders for a while now, but there’s a new sexy stud that everybody wants to take to the dance, the brokers that originate the deals. An entire segment of the industry still calls them ISOs (Independent Sales Organizations) and in 2015, nobody can seem to shut up about them.

One minute brokers are being fingered as the source of the industry’s moral decline and the next minute they’re the lifeblood of it all.

Ever since World Business Lenders began acquiring broker shops and converting them into franchisees, the institutional investors suddenly woke up.

They’re Buying Brokers? BUT WHY?!

Over the years, dozens of funders have opened for business and then realized they don’t know how to get deals or where to get them from.

It’s not a build-it-and-they-will-come industry anymore. As much as certain people try to berate brokers, it’s widely believed that they still control up to 50% of the industry’s deal flow. Institutional investors examining portfolios have taken notice that some funders are successful only because they have a loyal group of broker shops. So if the brokers make the funder, then why not court the brokers?

And so they’re doing just that…

If you’re brokering less than a million a month though, you’re not really investment material yet. There’s thresholds. The more volume you produce, the more options at your disposal.

At this size, you’re really just a couple of dudes (or dudettes) sitting in a room with phones. There’s not enough action to get anyone excited. There may be some potential to get an investor to co-syndicate with you, but that’s it.

$1 Million/month to $4 Million/month

Congratulations, you’re not just a bunch of dudes anymore. If you’re using decent software, hopefully you can print out the necessary reports to woo investors. At this level you’re eligible for co-syndication, an advance rate to fund your own deals, or to be rolled up as a franchisee. If you’ve got a criminal record or have been banned by the SEC, then forget it though.

$4 Million+

If you’re not already funding your own deals at this point, you’re going to be encouraged to by an investor. They’ll want to set you up on a platform that they trust and participate in the funding in some way. You can get a credit facility. You’re also acquisition material. Funders and investors have little interest in acquiring a couple of dudes sitting in a room because there’s no actual assets to value. At $4 million a month and more, there may potentially be something beyond just the dudes running the company and therefore something to consider. If you can’t pass a criminal background check though, then forget it. And if you’re running scrappy like a $200k/month shop, then they’re not really going to be able to help you. It doesn’t help if you’re stack-heavy either.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

Last year, every banker I sat down with told me they were looking to invest in the next OnDeck or CAN Capital. And what happened was, you had 200 bankers competing for the same handful of deals. This year, the conversations are all about brokers.

“Who wants to become a funder?”

“Who needs money to syndicate?”

“Who is serious about growing their broker shop?”

Did someone say Year of the Broker?

It damn sure is. If you’re funding more than a million a month, don’t rely on stacking, don’t have a criminal record, have actual reporting systems (not Excel), and want to be a funder or participate in more deals, then there’s a group of investors that are ready and willing to swipe right.

You might not be the next OnDeck and that’s okay. If you’ve got the flow, you can get the dough. <3 😉