Funding Circle US Originated $800M in 2020, More than 90% of Borrowers Were Making Payments

March 26, 2021 Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle’s US loans generate low annual returns, its highest being a projected return of 4.1% to 4.9% for its 2016 cohort. Its 2020 cohort is projected to generate an annual return of between 1 – 3%.

Overall, Funding Circle reported a total net loss of £108.1M (approx $150M US) on just £103.7M in revenue, a massive loss that stemmed entirely from the first half of the year, attributed mostly to a write-down in “fair value.”

Funding Circle’s primary market is the UK. When comparing the market with the US, the company said that the US is in an earlier stage of development even though the market is 5x larger.

From Sales to Founder: Craig J. Lewis Talks Gig Wage’s $7.5 Million Funding Round

November 27, 2020 Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Lewis made $10 million in payroll tech sales before going on to lead a firm that has seen 30% month-to-month growth this year, during a pandemic no less.

“We help businesses pay independent contractors, but because we’re so tech-centric, it’s evolved beyond just payroll,” Lewis said. “What we ended up building was financial infrastructure for the modern workforce. We help businesses get money from their customers to their contractors as fast and as flexibly as possible.”

The way Gig Wage does this, Lewis said, is by offering an online platform for the hybridization of payroll, payments, and banking from a single login. Businesses can manage their payroll needs for 1099 workers, then shift to payment needs quickly, through direct to debit, all major cards, bank transfers, and accounts receivables.

“One of the only- the only platform in the world actually that has embedded banking into payroll and payments, which is what kind of allows for this speed and flexibility that we offer,” Lewis said. “We’re like B to B to C: We help the businesses with technology and operational excellence, and because independent contractors are separate from the workplace, we provide tools for them.”

Lewis has years of experience in the payroll space- starting as a salesman for ADP small business payroll products back in 2008. Realizing he had a passion for payroll tech and getting customers the best services possible, Lewis went on to learn anything he could about the industry. Selling $10 million in software while moving across the country, Lewis landed in Silicon Valley, where he studied what it took to start a company.

“I was just awed how they thought about technology and products and company building,” Lewis said. “And I vowed to bring that to the payroll industry.”

Lews joined a startup, learned the Silicon Valley way of creating a company through an African American tech acceleration program. In 2014, Lewis founded Gig Wage to do something disruptive in the payroll space.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

“With the maturation of Uber, Lyft, Postmates, Doordash, Grubhub, Upwork, all of these kinds of gig economy freelancer companies, we had great growth going into 2020,” Lewis said. “In Q1, we were set up to raise our series A, and then March happened, and the terms got pulled off the table.”

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

“The gig economy was right there waiting on the workforce to provide opportunities to earn, and we were positioned perfectly to help people compete for that talent and pay people in a modern way,” Lewis said. “The pandemic has been a huge growth accelerant for us, and we think those tailwinds will only continue.”

Those winds of success came during a time of protest. Amplified in the pandemic’s backdrop, the country was waking up to the unequal disenfranchisement black people faced. Only 1% of black founder entrepreneurs ever receive VC funding, and Lewis said he is proud to have raised a significant round, given that unfair stat.

“With so much controversy and negative energy around black people in general,” Lewis said. “I think putting this positive story out there and showing this black excellence, black tech, I think it’s super important, and it’s been something that I’ve embraced. We’ve been able to be a part of putting something extremely powerful and positive into the market.”

America is finally waking up to realize something Lewis said was obvious, that black people matter, even though it can be controversial to say so. He hopes his success can help others but affirms the funding round was no charity drive.

“This is a great opportunity for us to be clear about the fact that like hey, we’ve been working on this, we’ve built a good business and a good technology,” Lewis said. “This is a big business opportunity for our investors and us. It wasn’t charity, right: This isn’t like, oh he’s black, give him some money.”

The successful funding round shows confidence in the Gig Wage platform from Green Dot, which will allow Gig Wage to offer bank accounts and debit services to independent contractors. Green Dot is one of the only fintechs with a national banking license, Lewis said, and Gig Wage is joining the Banking-as-a-Service direction that the fintech industry is headed.

Beyond payroll, Lewis can’t wait to offer other financial products to businesses as the company grows.

“When you think about the gig economy, it’s important that people get paid fast and flexibly: You’ve got to have the cash to be able to do that,” Lewis said. “We see some unique opportunities to get involved in the lending space down the line as well as we continue to build out our technologies.”

Smarter Loans Co-Founder: Study shows Fintech in Canada Seeing Accelerated Growth

November 24, 2020 There has been fast-growing demand for digital finance products this year, according to the Smarter Loans Annual State of Canadian Fintech study. The report surveyed more than 2,500 users of the Smarter Loans site.

There has been fast-growing demand for digital finance products this year, according to the Smarter Loans Annual State of Canadian Fintech study. The report surveyed more than 2,500 users of the Smarter Loans site.

The findings show an accelerated shift to digital transactions, which Smarter loans co-founder Vlad Sherbatov attributed to a pandemic-acceleration of the tech-leaning trends that were already coming.

“One of the central insights from this year’s study is the overall increase of fintech adoption and lending,” Sherbatov said. “We’ve also noticed the fact that people are just much more likely to manage their finances online today than they were at this time 12 months ago or a year ago.”

Intending to gain insight into Canada’s fintech industry, Smarter Loans began sending questionnaires to their users starting in 2018.

“We survey some of the people that flow through our website that have used a fintech lending product in the past 12 months, we ask them questions about their experience,” Sherbatov said. “The purpose is to extract insights so that we can help push the industry forward and improve it.”

Even just two years ago the industry was a much smaller space but has ballooned since, and the Smarter Loans survey has become a one-of-a-kind focus on Canadian fintech markets. Featured with this year’s results is commentary from Canadian industry leaders like the Canadian Lenders Association, and AltFinanceDaily’s own Sean Murray.

“It’s become a bit of a staple in the lending industry,” Sherbatov said. “Because it’s the only piece of research in Canada that is laser-focused on fintech lending.”

With three years of data to compare, Sherbatov said he could see a significant increase in online activity. Part of this is just due to where the world is heading, as Sherbatov described the younger generations just stepping into the financial world.

“This is something that’s been happening for years; this is a trend that has started a long, long time ago,” Sherbatov said. “For younger generations, the way that they approach financial products and companies is very different from someone in my generation or older. Online is the standard of doing business, on-the-go, and mobile is the standard of managing your financial affairs.”

Fintech in Canada, Sherbatov said, tends to lag behind the growth of the fintech industry in other countries but is on the rise due to the Coronavirus. The digital adoption trend was pushed forward, as some customers that had been reluctant to bank online were forced to do so by necessity. Now, these changes to the way business is transacted are here to stay, Sherbatov said.

Like the surge in eCommerce activity, people are going online to make financial transactions.

“You go to Amazon to buy laundry detergent, and you go online to open up a checking account to pay some bills,” Sherbatov said. “Everybody needs financial services, just like everybody else needs household items; it’s how we’re going about obtaining them. This has changed and has accelerated due to Covid.”

PayPal Still Leads in Unsecured Small Business Lending

November 12, 2020PayPal recently disclosed the dollar amount of receivables it had “purchased” between its working capital and business loan program for the first 3 combined quarters of 2020. The figure was $1.5B, down by more than half from over the same period last year. That would seem to suggest that the actual origination figure is probably $1.3B, which is still larger than some of its closest competitors. Numbers from rivals like Kabbage (recently acquired by Amex) and Amazon were not readily available.

For a larger comparison chart, click here.

2020 YEAR TO DATE:

| Company | Q1 2020 | Q2 | Q3 | YTD TOTAL |

| PayPal | $1.3B | |||

| OnDeck | $592M | $66M | $144M | $806M |

| Square Capital | $548M | $0 | $155M | $703M |

| Shopify Capital | $162.4M | $153M | $252.1M | $567.5M |

Upstart Files for $100M IPO – Reveals Financials

November 6, 2020

Upstart, the online personal lender that uses non-traditional data like a college education, job history, and residency to evaluate borrowers, is moving forward with an IPO.

The company revealed its financial statements in an S-1 filed on Thursday. In 2019, Upstart generated $164.2M in revenue and had a net loss of $5M. For 2020 through Sept 30th, revenue was at $146.7M with a net income of $4.5M.

The company said that in 2020, 98% of its revenue was generated from platform, referral and servicing fees that it receives from its bank partners. Their bank partners “include Cross River Bank, Customers Bank, FinWise Bank, First Federal Bank of Kansas City, First National Bank of Omaha, KEMBA Financial Credit Union, TCF Bank, Apple Bank for Savings and Ridgewood Savings Bank.”

Upstart borrowers tend to have limited or no credit history, which is where its AI-driven models with 1,600 variables come into play.

“Our bank partners have generally increasingly retained loans for their own customer base and balance sheet,” the company wrote in its S-1. “In the third quarter of 2020, approximately 22% of Upstart-powered loans were retained by the originating bank, while about 76% of Upstart-powered loans were purchased by institutional investors through our loan funding programs.”

Upstart was valued at $750M during its 2019 Series D.

In 2017, AltFinanceDaily referred to Upstart as the Tesla of alternative lending.

“You hear so much about how Tesla cars will drive themselves, how Google or Amazon home assistants talk to you to as if you’re human,” said Dave Girouard, Upstart co-founder, in an interview back then. “In lending we are the first company to apply these types of technologies to lending.”

Girouard’s co-founder Paul Gu, who serves as SVP of Product and Data Science, was only 21 when Upstart launched in 2012. He’s now 29.

Anna M. Counselman, the third co-founder, is SVP of People and Operations.

Upstart is planning to raise $100M from its IPO.

Another Attorney Charged Criminally in 1 Global Capital Saga

September 29, 2020 Andrew Dale Ledbetter, a veteran securities attorney who once co-authored a book called How Wall Street Rips You Off – and what you can do to defend yourself, now stands accused of ripping investors off.

Andrew Dale Ledbetter, a veteran securities attorney who once co-authored a book called How Wall Street Rips You Off – and what you can do to defend yourself, now stands accused of ripping investors off.

Ledbetter was criminally charged on Tuesday by the US Attorney’s office in South Florida for his alleged role in the 1 Global Capital Securities fraud case. Ledbetter was formally accused of Conspiracy to Commit Wire Fraud and Securities Fraud. He was simultaneously hit with civil charges by the Securities and Exchange Commission.

Both agencies say that Ledbetter reaped nearly $3 million in referral fees from 1 Global Capital in exchange for raising nearly $100 million from investors, mostly retirees, all while making knowingly false statements and misrepresentations about the investments. For instance, they say that he knew the investments were securities but claimed they weren’t anyway. Similar circumstances brought down Florida attorney Jan Douglas Atlas last year. Ledbetter had been compensating Atlas on the side as part of the alleged scheme.

Ledbetter is the 4th individual to be criminally charged in connection with the 1 Global Capital case. The other three: Atlas, Alan G. Heide, and Steven Schwartz, have all already pled guilty.

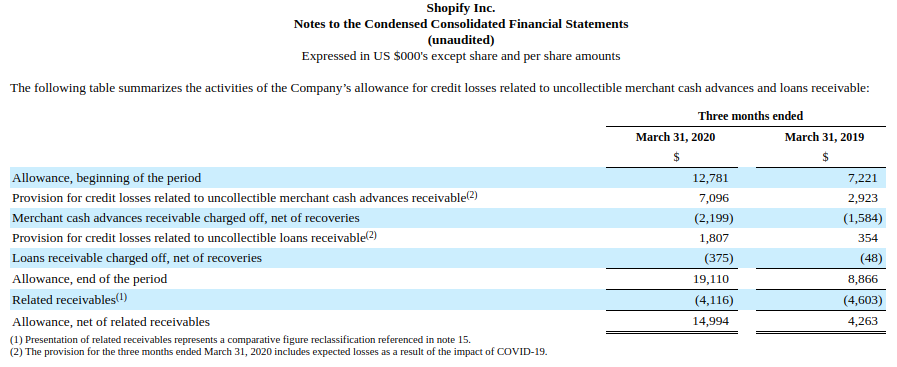

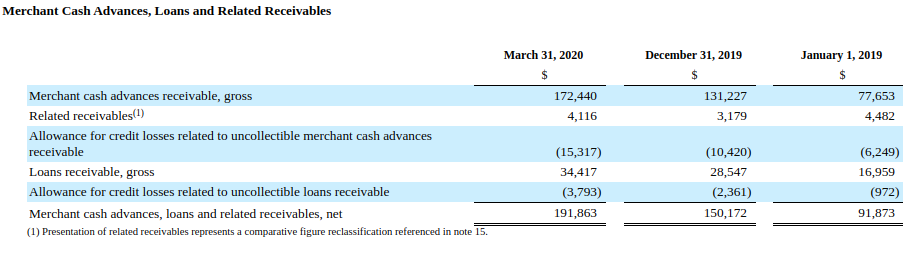

Shopify Shows Strength in Q1 Results, Issues $162.4M in MCAs and Loans

May 6, 2020eCommerce platform Shopify, 2nd only to Amazon in retail eCommerce sales, issued $162.4M in merchant cash advances and business loans in Q1, up from $115.9M in the previous quarter. The statistic pushed them past the $1 billion threshold of funds cumulatively issued since inception.

The company’s provision and allowance for loan losses ticked up from significantly from the same period the prior year but Shopify at that time was originating 50% less volume.

The company reported a GAAP net loss of $31.4M on $470M in revenue. Shopify also has approximately $2.36B in cash and cash equivalents on its balance sheet.

The company reported an increase of monthly recurring revenue, thanks to an increase in the number of merchants joining the platform, strong app growth, and Shopify Plus fee revenue growth.

Shares of Shopify (NYSE: Shop) jumped by more than 5% after the announcement.

Lists of States Where Non-Essential Businesses Have Been Ordered to Close

March 24, 2020Make sure you know about individual state orders that could affect a small business’s ability to operate. Below is a list of states and regions that have ordered some or all non-essential businesses to close. This list may be incomplete and the details of each state’s orders could change and may have changed since this was posted. Do you own due diligence:

- Alabama – Jefferson County

- California

- Colorado – Must reduce workforce by 50%

- Connecticut

- Delaware

- Florida – multiple counties

- Georgia – bars and restaurants

- Hawaii – Maui and Honolulu

- Idaho – Blaine County

- Illinois

- Indiana

- Kansas – multiple counties

- Kentucky

- Louisiana

- Maine – Bars and restaurants

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi – Certain cities

- Missouri – Certain areas in and around Kansas City

- Montana

- Nevada

- New Jersey

- New Mexico

- New York

- North Carolina

- Ohio

- Oregon

- Pennsylvania

- Rhode Island

- Tennessee – Multiple cities and counties

- Texas – Multiple cities and counties

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming – Multiple counties