When The Music Stopped: How The Pandemic Threatened the History and Culture of Austin, Texas

November 15, 2020

In April of this year, Threadgill’s – a legendary Austin music venue and beer joint that, in the 1960s, famously launched the career of blues singer Janis Joplin — turned off the lights and pulled the plug on its sound stage.

A converted gasoline station, Threadgill’s had been a rollicking music scene since 1933 when musician and bootlegger Kenneth Threadgill secured the first liquor license in Texas after Prohibition. His juke box was crammed with Jimmie Rodgers songs and Threadgill himself famously sang and yodeled Rodgers’ tunes.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

“The first time I went to Threadgill’s was in the fall of 1968, when I was a freshman at UT,” recalls Perry Raybuck, a songwriter-folksinger and retired government worker who, as a member of the Southwest Regional Folk Alliance, played the stage in 2018. “It was the beginning of an education for me,” he adds. “I had been a Beatles and rock n’ roll kid and it opened me up to different music styles. I became a convert.”

In 1981, Threadgill’s was taken over by another acclaimed club owner, Eddie Wilson, who previously had been the proprietor of the Armadillo, a fabled music venue. Wilson began to actually pay musicians – Threadgill had compensated them mainly with free cold beer – and installed a circular stage.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

“Live music,” says Laura Huffman, chief executive at the Austin Chamber of Commerce, “is why people come here. It is a central component of Austin’s cultural and economic life.”

Omar Lozano, director of music marketing for Visit Austin, the city’s main tourism organization, says: “We have close to 250 places in the greater Austin region where you can hear live-music, although it’s closer to 50-70 on any given night. During South by Southwest, no stone is left unturned — everything becomes a stage: parking garages, grocery stores, housing co-ops. There are also four or five stages at the Airport, which helps liven up the mood.”

But that identity is being put to the test. So far this year, Austin has lost a raft of live music venues. Among those joining Threadgill’s in honky-tonk heaven since the pandemic struck are Barracuda, Plush, Scratchhouse, Shady Grove, and Botticelli, all of which provided niche audiences to both established musicians and up-and-coming acts.

The roller-coaster ride of government mandated shutdowns followed by a limited re-opening in the spring and another shutdown since July fourth is making life miserable and untenable for both club owners and already hardpressed musicians and artists, says Marcia Ball, a piano player and blues singer.

Ball, who was named by the Texas Legislature as “2018 Texas State Musician” and whose musical style was once described by the Boston Globe as “mixing Louisiana swamp rock and smoldering Texas blues,” told AltFinanceDaily: “There was already a limited amount of opportunity for musicians to perform and monetize their work in Austin, so it has always been necessary to travel to make a living. But we still depend on a thriving local scene, and we’re losing that when key venues like Threadgill’s disappear.”

Adds Graham Williams, a prominent Texas promoter of touring bands: “These venues and bars are vital to the music ecosystem. Local bands and cover bands need hangouts, even if people are not buying tickets. They’re places to play every night of week.”

While unheralded outside the Austin scene, the local music joints were often a port-of-call for out-of-town promoters and nightclub owners checking out Austin talent – “most notably Barracuda (which) had super-popular acts and was like a hipster garage venue,” says promoter Williams. “A lot of touring bands played there on their way up.”

A July study by the Hobby School of Public Affairs at the University of Houston found that the city’s live music industry is in desperate straits. Sixty-two percent of live music spots and 55% of the bar-and-restaurant businesses reported to researchers that that they can endure for no more than four months, making them the most vulnerable of 16 industries surveyed.

And the situation has become “even more ominous” since the report was published, explains Mark P. Jones, a political scientist at Rice University in Houston and a lead researcher on the Hobby study. “That survey finished polling two hours before all bars and restaurants closed back down,” he says. “Everything people were saying was when bars were at 50% capacity. That’s a best-case scenario.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

“He knocked down the rent a little bit,” Severin says of his landlord, but the situation is dire. “We just had a fifth venue, Re bar, close at the end of August,” he says. “It was a punch in the gut. This could be me.”

The Bitter End in Greenwich Village is also keeping its head above water despite not opening its doors since March. The nightclub has a storied past: owner Paul Rizzo recounts that it is where pop singer Neil Diamond got his start and where “everyone from Curtis Mayfield to Randy Newman” has performed since its opening in 1961. But the club is silent now since the pandemic overwhelmed the city’s hospitals and made New York the epicenter of sickness and suffering during the spring. So far the club is getting help from a landlord’s forbearance and loyal musicians.

Peter Yarrow (the “Peter” in the bygone trio Peter, Paul and Mary), donated a streamed concert to patrons who contributed to a fundraiser that raised more than $50,000. And grateful local musicians also put on a benefit directing people to a Go Fund Me page on the Internet that raised another $16,000. “We’re a major venue for local musicians,” Rizzo says. “We should pull through.”

It’s in their self-interest for artists to do whatever they can to keep the doors open at a club like The Bitter End. “These days because of the last two decades of declining record sales — live music is the bread and butter of a musician’s income,” says journalist Edna Gundersen, a recently retired, 28-year-veteran of USA Today. “That’s true whether it’s a local entertainer or an international superstar.” (Gundersen earned the reputation as Bob Dylan’s favorite journalist; it was she who scored his only interview after he won the Nobel Prize for literature in 2018, publishing his eccentric musings in the The Telegraph of London and breaking the news that he would indeed accept the prize.)

“Touring has been crushed,” Gundersen adds, “and festivals have been canceled. So people doing the circuit and clubs are gone for all intents and purposes. Streaming — while initially up — is down because people aren’t listening to music in the gym or in their cars. Physical record sales are also down because people aren’t going to stores. All of this is just killing musicians.”

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

Hoping to win attention and assistance for their plight from the federal government — “We’re the first to close and the last to reopen,” Severin says — live-music entrepreneurs like himself and Rizzo and more than 2,800 club-owners and promoters across the country have banded together to form the National Independent Venue Association.

Their membership includes independent proprietors (no corporate members allowed) of saloons, cabarets and concert halls as well as theaters, opera houses and auditoriums from every state plus the District of Columbia. To help plead their case with Congress, the organization hired powerhouse law firm Akin Gump Strauss Hauer & Feld, the largest Washington, D.C. lobbying firm by revenue.

NIVA also blanketed Congressional offices with two million letters, e mails and correspondence generated from hordes of fans and performers. Among the many scriveners are a slew of boldface names: Mavis Staples, Lady Gaga, Willie Nelson, Billy Joel, Earth Wind & Fire, and Leon Bridges. Comedians Jerry Seinfeld, Jay Leno and Jeff Foxworthy have also penned notes to lawmakers championing NIVA’s cause.

Their message: without federal funding, 90% of independent stages will go under over the next few months. “The heartbreak of watching venues close is that once a building is boarded up, it’s not going to be a music venue any more,” warns Audrey Fix Schaefer, communications director at NIVA. “They operate on thin business margins to begin with and they’re too hard to develop.” For touring acts, each city stage is “an integral part of the music ecosystem,” Schaefer explains. “When artists finally do get back on the tour bus, they might have to skip the next five cities and go on to the sixth.”

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

The legislation would provide grants up to $12 million for live entertainment venues to defray most business expenses incurred since March, including payroll and employees’ health insurance, rent, utilities, mortgage, personal protection equipment, and payments to independent contractors.

NIVA’s chief argument for the legislation is coldly economic rather than sentimentally cultural. The organization cites a 2008 study by the University of Chicago that spending by music patrons produces a “multiplier effect” for the broader economy. For every dollar spent by a concert-goer at a live performance, the Chicago study determined, $12 in downstream economic activity occurs.

Explains Scott Plusquellec, nightlife business advocate for the City of Seattle: “You buy a ticket to a show and the direct economic impact of that purchase is that it pays the artist, bartender and the club itself as well as the band, advertisers, and promoters. The indirect economic impact,” he adds, “is that after you bought the ticket, you went to a barber shop or a hair salon to look good that night. You might also have dinner, go to a bar for a drink and tip the bartender. That’s the whole the idea of a ‘multiplier.’”

In Austin, that economic logic is an article of faith with city burghers, asserts Lozano of Visit Austin, who reports that live music in the capital city is roughly a $2 billion industry. To promote live music, the tourism bureau sponsors such endeavors as “Hire an Austin Musician.” That program, Lozano says, “sends musicians around the U.S. to represent us during marketing season.” In another promotional campaign, Visit Austin arranged for singer-songwriter Julian Acosta to play a gig at travel agents’ offices in London when Norwegian Air inaugurated direct flights between London and Austin in 2018. “The U.K. is one of our best markets,” he reports.

Even so, efforts by the business community and the City of Austin have failed to stanch much of the industry’s bleeding. According to its website, the city has disbursed $23.7 million in loans and grants to small businesses and individuals, but slightly less than $1 million of that has gone to live-music and performance venues, entertainment and nightlife, and live-music production and studios.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

The Continental Club on South Congress – a key fixture in the hip “SoCo” strip just over the Colorado River from downtown – appeared to do best. It picked up $79,919 from two programs: $40,000 in the CARES-backed small business grants program, and $34,919 from the city’s Creative Space Disaster Relief Program. Other clubs receiving $40,000 in the small business grants program included Stubbs, The Belmont, Cheer Up Charlies and the White Horse. (For a full list go to: http://www.austintexas.gov/edims/document.cfm?id=347299)

Joe Ables, owner of the Saxon Pub, a major Austin venue for jazz – blues singer Ball hailed it as one of several important Austin clubs “that sustains creative endeavor, especially for songwriters” – was vexed that his grant application was denied by the city “with no explanation.” Ables also voiced dissatisfaction that the city paid the Better Business Bureau a 5% administration fee to handle $1.14 million in relief funds, including determining which applicants were approved. “What would they know about live music,” he says.

Even for clubs that received city largesse, it hasn’t been nearly enough to sustain them. The North Door, which got $15,240, closed for good on September 11 (an ominous day — the anniversary of the attacks on the World Trade Center and the Pentagon.)

Meanwhile, enough clubs and venues were left out in the cold that club owner Stephen Sternschein could tell AltFinanceDaily just before the slide show was released: “I’ve heard talk of a $21 million grant program but most people I know haven’t seen a dollar of that.”

Sternschein is managing partner of Heard Presents, an independent promoter and operator of a triad of downtown clubs that includes the spacious Empire Garage, which features hip hop and urban jazz, and has space for 1000 music-goers. A member of NIVA, Sternschein describes efforts by both the state and local governments as “woefully inadequate.” Says he: “People are looking to the federal government for answers.”

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

“You can go out to dinner in Waco,” he observes, referring to the mid sized Texas city between Austin and Dallas best known as home to Baylor University and its “Bears” football team, fervent Baptist religiosity, and unremarkable night life. “Music brings in revenue to Austin and to Texas that wouldn’t otherwise come here.”

In addition, Jones says, the large presence of “artists, creative types, and freelancers” helps make Austin a strong selling point for “brain industries” to attract talent from the East and West Coasts. “It supports the technology industry by making it easier to recruit employees to live there,” he says. “Austin is an alternative to Silicon Valley. People who are progressive might be hesitant to come to conservative, red-state Texas from California but they’ll come to Austin because it’s culturally cool.”

Austin, which embraces the slogan “Keep Austin Weird,” is on the verge of becoming just like every place else in Texas. Should it relinquish its flavor and charm, it could discourage many of the assorted business groups and professionals from keeping Austin on their dance card as a popular destination for meetings, conferences and get-away trips.

Howard Freidman, managing director at Bluechip Jets, a broker of private luxury aircraft, had an earlier career as a technology industry executive. Partly drawn by his previous experiences with the city, Freidman moved to Austin earlier this year. “It had the same coolness and weirdness of New Orleans — but also with the professionalism of a tech city,” he says.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

Many of the technology firms – including such needy companies as Samsung, Intel, Rackspace, Facebook, and Apple – have each received tax breaks, grants and subsidies worth tens of millions of dollars from a variety of local jurisdictions. Not only have the city of Austin and Travis Country been beneficent, but adjacent county governments and the state of Texas have provided abundant support. A 2014 study by the Workers Defense Project, in collaboration with UT’s Lyndon B. Johnson School of Public Affairs, reported that the state of Texas showers big business with $1.9 billion annually in state benefits. Most recently, officials with Travis County and a local school district granted Tesla more than $60 million in tax rebates to build a massive “gigafactory” southeast of town near Austin-Bergstrom International Airport.

To house the burgeoning cohort of “knowledge workers,” there are condominium conversions, tear-downs, high-rises and other forms of frenetic real estate development which, in their train, bring higher property taxes, steeper rents, and unaffordable housing.

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

The drop-off in live music and the belt-tightening by musicians is causing third-party pain for people like veteran Austin journalist and publicist Lynne Margolis, whose national credits include stories for Rolling Stone online, and radio spots for NPR. “The public relations aspect of my work has dropped away because artists can’t afford to pay,” she says, “and music journalism is falling by the wayside. It’s hard not to feel to like a double dinosaur.”

Led by bars, restaurants and music venues, on many days the solemn departure of small establishments has the business news sections of Austin newspapers reading more like the obituary page. One hardy survivor is Giddy Ups – a throwback honky-tonk on the town’s outskirts that advertises itself as “the biggest little stage in Austin” – promising “just about everything,” says owner Nancy Morgan, including “country, blues, rock, bluegrass, and soul.” For the past 20 years Giddy Ups has developed a devoted following of musicians and patrons while fending off hyper modernity.

“It has an untouched, back-to-the-seventies, cosmic cowboy vibe,” says local musician Ethan Ford, a guitarist and bass player whose trio, The Slyfoot Family, has graced its stage. “It’s a time capsule,” Ford adds.

Morgan declined to disclose her annual receipts but in 2019, she reports paying out $188,000 in wages to employees, $72,000 to musicians, and $185,000 in combined sales taxes to the city of Austin and to the state. Despite her status as a taxpayer, employer and entrepreneur, she has received no state aid and is disqualified from receiving city pandemic assistance programs, meager as they may be, because she’s located in an extra-territorial jurisdiction.“

Nancy still bartends most nights and does all of the booking,” says Ford. “Her knowledge of the Austin music scene could fill a couple of books. I know a decent fistful of Austin venue owners and she’s about the only one that hasn’t given up, been forced out, or just retired. She’s a dynamo.”

Unless the cavalry arrives for Morgan and other holdouts, though, their musical days may be numbered.

Editors Note: Threadgill’s didn’t make it. The venue “has closed for good, the property has sold, and the building will eventually be torn down,” according to information disseminated for its Last Call Music Series. Its November 1st grand finale show featured Gary P. Nunn, Dale Watson, Whitney Rose, William Beckman, and Jamie Lin Wilson.

The building will be replaced with apartments.

New Jersey Legalizes Recreational Marijuana

November 4, 2020One chill result from the 2020 election was the legalization of recreational marijuana in New Jersey for adult use. In a 2-1 victory, Option One on New Jersey ballots passed, paving the way for a regulated environment for recreational use, possession, and cultivation in the Garden State.

4:20 PM.

Time to legalize it. pic.twitter.com/157WC7qgof

— Governor Phil Murphy (@GovMurphy) October 28, 2020

Before the vote, Gov. Murphy showed support

We did it, New Jersey!

Public Question #1 to legalize adult-use marijuana passed overwhelmingly tonight, a huge step forward for racial and social justice and our economy. Thank you to @NJCAN2020 and all the advocates for standing on the right side of history.

— Phil Murphy (@PhilMurphyNJ) November 4, 2020

The amendment was billed as not only a chance to increase tax revenue but as civil rights reform. Advocates argued that prohibition laws disproportionately harmed minority communities.

The change was initially put before the legislature in 2017 but failed to pass by 2019. A bipartisan supermajority put the choice up to the public referendum. Appearing in Willingboro on Tuesday, long time advocate of legalization, Gov. Phil Murphy, spoke on voting day in last-minute support.

“I got to supporting it first and foremost due to social justice,” Murphy said. “We inherited when I became governor the largest white, nonwhite gap of persons incarcerated in America, and the biggest contributor to that was low-end drug offenses.”

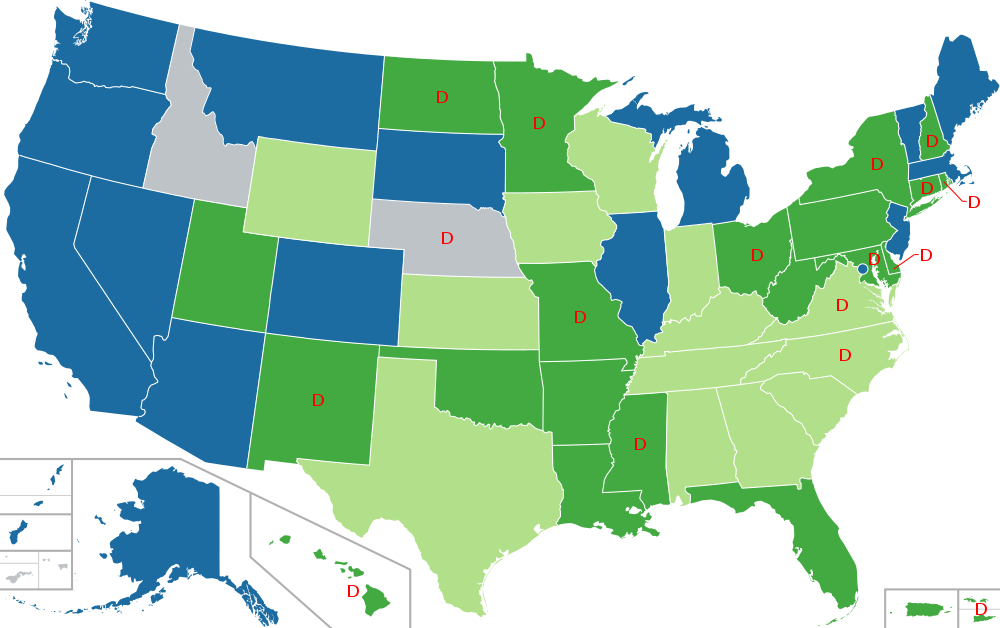

New Jersey was one of four states with legalization on the ballot, and all succeeded, bringing adult use to Arizona, Montana, and South Dakota as well. After Tuesday, more than 111 million Americans- a third of the country live in a state where recreational marijuana is legal.

Image SourceKEY

Blue = Legal

Dark Green = Legal for medical use

Light Green = Legal for medical use – limited THC content

Grey = Prohibited for any use

D = Decriminalized

Cannabis legalization advocates, like Doctors For Cannabis Regulation (DFCR), saw the day as a significant victory for industry and social progress. Dr. David Nathan founded DFCR in 2015, where he serves as president of the board. Dr. Nathan stood up and spoke out against the prohibition of marijuana 11 years ago and said he was one of the first accredited mainstream physicians to do so.

“I’m not a medical cannabis physician, I’m a psychiatrist who sees how much damage cannabis prohibition does compared to the drug itself,” Dr. Nathan said. “I’ve really been given the platform to speak up, but at the same time, it was hard to get colleagues to speak up on an issue.”

After working for NJ United for Marijuana Reform, Dr. Nathan founded DFCR to create an organization to facilitate physicians who wanted to get involved at a national level. The success of Tuesday’s vote demonstrates how far legal cannabis advocation has come, from a resounding no to a majority yes.

“A lot of doctors who understood cannabis prohibition as a tragedy and a mistake were concerned about what their peers would think about them if they spoke out,” Dr. Nathan said. “Now we’ve got a group of highly respected physicians organized and advocating strongly, not just for legalization but much more importantly for effective regulation.”

Dr. Nathan sees the NJ amendment as a significant chance for improvement in public health. Despite legalization, it is unclear how the new law will go into effect. Per the amendment, the state will create a regulatory framework and tax the sale of marijuana at 6.625%, but implementation is up for debate.

Legislators still have to agree on how a new Cannabis Regulatory Commission will function. The state will also have to choose how decriminalization, possession limits, growing limits work, and forgiveness of past marijuana crimes.

All of which will be figured out and are necessary to the fair implementation of the passage of the amendment, Dr. Nathan said.

But those changes may come fast. NJ, like many states, is hurting during the COVID recession. Last month New Jersey officials approved a budget that is set to borrow $4.5 billion from the Federal Reserve to plug pandemic-sized holes in state spending.

Basing estimates on Colorado’s experience after legalizing cannabis in 2014, the state legislature predicts NJ could see tax revenues of up to $126 million a year from recreational sales.

“According to the Colorado Department of Revenue, retail cannabis sales, excluding medical cannabis, totaled $1.2 billion in calendar year 2018,” The report said. “Assuming New Jersey experiences similar per capita sales of recreational cannabis as Colorado, total retail cannabis sales for New Jersey could reach $1.9 billion, yielding sales tax revenues of up to $125.6 million annually at the current 6.625 percent sales tax rate.”

With such high revenues, some suspect New Jersey to lead the way for other northeastern states; income will spur jealous neighboring Pennsylvania and New York to legalization in competition.

“If this gives both Pennsylvania and New York a push, that would be great,” Dr. Nathan said. “I do think it’s going to have an impact, now that there will be a state right in the middle of the Mid Atlantic that is going to have regulated sales.”

But even with tristate legalization, the cannabis industry faces a problem with funding.

Most firms in cannabis supply chains- from growers to dispensaries- are small businesses that suffer from a lack of access to bank funding. Because marijuana is an illegal Section 1 drug like Heroin on a federal level, banks and venture capitalists have their hands tied when it comes to credit. But with Tuesday’s victories for legalization, federal regulation is closure to changing.

“I think that each state that adopts, sends a stronger message to the federal government,” Dr. Nathan said. “The voters in those states are giving resounding victories to the notion that cannabis should be de-scheduled not rescheduled, and then regulated.”

deBanked has been following the SAFE Banking Act since it passed in the House last year, a piece of legislation that hopes to address cannabis banking problems by allowing legal pot firms to open banking deposit accounts.

The law was bundled into the HEROES act with the rest of business aid projects, stuck between the GOP-controlled Senate and the blue House since the summer. Depending on the Senate’s layout when ballots are fully counted, financial institutions that have left pot companies de-banked may be-danked.

University of Delaware, Other Universities Going Long on Fintech

September 15, 2020The University of Delaware recently received a $9 million tax incentive to construct a new Fintech Center on its premier Science, Technology, and Advanced Research (STAR) campus, with help from a community-building company Cinnaire. Slated for completion in 2021, the building marks yet another fintech-focused resource for higher education.

Financial technology programs have long been offered at prominent business schools such as Harvard, Stanford, and Columbia, international schools such as Oxford, and research institutions like MIT since the late 2000s.

Now that fintech has become a long term value creator in the financial world, other institutions such as the University of Michigan, Fordham, and Delaware are excited to implement fintech opportunities on campus for undergraduate and graduate students alike.

Discover Bank and Cinnaire jointly funded the building, a $39 million project. According to Delaware plans, it will create a space on the Delaware STAR campus to host a new Financial Services Incubator to encourage research and collaboration between students and industry leaders.

Discover Bank and Cinnaire jointly funded the building, a $39 million project. According to Delaware plans, it will create a space on the Delaware STAR campus to host a new Financial Services Incubator to encourage research and collaboration between students and industry leaders.

“The FinTech building will bring together computer science, engineering and business experts in cybersecurity, human-machine learning, data analysis, and other emerging financial technologies,” said Levi Thompson, Dean of the College of Engineering. “These collaborations will allow us to provide our students with a very unique experience that prepares them to excel in the workforce. Furthermore, our Fintech discoveries will benefit people throughout Delaware and the world.”

Cinnaire is a national nonprofit that focuses on improving communities’ financial health by creating capital solutions to revitalization projects: lending funds, managing, and building housing structures.

Funding communities is what Cinnaire does best: in this case, utilizing a New Markets Tax Credit to fund an addition to the Delaware campus.

The nearby University of Fordham at Lincoln Center has also been trending toward preparing students for a fintech world. Undergrad and graduate students pursuing an MBA through the Gabelli School have the option of a fintech concentration.

The nearby University of Fordham at Lincoln Center has also been trending toward preparing students for a fintech world. Undergrad and graduate students pursuing an MBA through the Gabelli School have the option of a fintech concentration.

The course work not only incorporates data science and machine learning skills into the worlds of credit lending and risk management but facilitates relationships between students and a wealth of industry partners.

Sudip Gupta, professor, and Director of the MS Quantitative Finance program, spoke about the courses’ popularity there. The program is ranked in the top 20 of its kind in the world by Risk Magazine.

He has seen a revolution in fintech in the past few years that has recently received a big push by pandemic forces, introducing the wholesale adoption of fintech techniques into traditional financial institutions.

“The fintech revolution in the industry- big data, machine learning techniques, storage capacity, and cloud computing has been going on for the last couple of years,” Gupta said. “The pandemic provided the big push to move toward that direction.”

Gupta has been following the development of alternative credit closely, recently publishing an award-winning paper studying machine learning to create alternative consumer credit scores using mobile phone and social media data.

“The idea of my research- let’s look at people who do not have a credit history or enough traditional credit you could get from a FICO score,” Gupta said. “Using this data, it turns out they are better predictors, and better to judge than FICO, and can reach out to more people.”

Gupta is excited for the adoption of big data techniques into alternative and traditional consumer loans because it offers a win-win for consumers and institutions alike, he said. Echoing the findings of many successful alternative finance companies, Gupta said his research showed that collected data could offer better insight for lending than “stale FICO scores.”

Up north at the Univerisity of Michigan, Professor Robert Dittmar at the Ross School of Business heads the Fintech Initiative. He is working on adding even more fintech classes. Recently, through a partnership with PEAK, a Chicago fintech lending company, Michigan launched a fintech initiative that incorporates undergrad and grad classes, faculty research, and a fintech entrepreneurial club that connects students to industry leaders.

Up north at the Univerisity of Michigan, Professor Robert Dittmar at the Ross School of Business heads the Fintech Initiative. He is working on adding even more fintech classes. Recently, through a partnership with PEAK, a Chicago fintech lending company, Michigan launched a fintech initiative that incorporates undergrad and grad classes, faculty research, and a fintech entrepreneurial club that connects students to industry leaders.

Michigan Ross is adding fintech classes for a variety of reasons.

“The simplest reason: students are interested in learning more about this kind of space,” Dittmar said. “And we’re seeing more demand from the industry side for students that know more.”

For years Dittmar said tech companies and startups in silicon valley were pioneering innovations in the industry. Through talking with alumni and contacts in the industry, Michigan found that fintech has gotten to the place where there is an excellent supply of data engineers. Still, there is a demand for professionals with the financial business expertise to implement these technologies.

“What we are trying to do at Ross is fill in that gap,” Dittmar said. “what we’d like is for [students] to know enough about the technology that they can provide the insights of finance and business to the people that are doing that technical work.”

At Ross, they are organizing what will one day be like a fellowship program. The program will feature a combined learning experience: students will learn data analytic finance, apply their computing skills in credit decision making classes, and then connect with the industry in experiential learning classes.

“In the last couple of years, I have been taking students to London to work at fintech startups in the UK,” Dittmar said. “And we are hoping to expand that program so that most or all graduate students have the opportunity to participate in something like that.”

Last year Ross hosted a “Fintech Challenge” competition to design a banking service to reach customers in a “banking desert” in rural Michigan. The program is hoping to host another challenge this year, despite complications of COVID-19.

Lists of States Where Non-Essential Businesses Have Been Ordered to Close

March 24, 2020Make sure you know about individual state orders that could affect a small business’s ability to operate. Below is a list of states and regions that have ordered some or all non-essential businesses to close. This list may be incomplete and the details of each state’s orders could change and may have changed since this was posted. Do you own due diligence:

- Alabama – Jefferson County

- California

- Colorado – Must reduce workforce by 50%

- Connecticut

- Delaware

- Florida – multiple counties

- Georgia – bars and restaurants

- Hawaii – Maui and Honolulu

- Idaho – Blaine County

- Illinois

- Indiana

- Kansas – multiple counties

- Kentucky

- Louisiana

- Maine – Bars and restaurants

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi – Certain cities

- Missouri – Certain areas in and around Kansas City

- Montana

- Nevada

- New Jersey

- New Mexico

- New York

- North Carolina

- Ohio

- Oregon

- Pennsylvania

- Rhode Island

- Tennessee – Multiple cities and counties

- Texas – Multiple cities and counties

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming – Multiple counties

How Hot Is The Legal Cannabis Industry?

February 24, 2020 One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

That’s some 30% more than the 1,000 vendors who packed into the Central Hall in 2018 and about double the 678 who were showing off their wares in the smaller North Hall two years ago, reports Chris Day, vice president for external relations at Denver-based Marijuana Business Daily, which follows the cannabis industry and sponsored the Las Vegas trade show.

“In December, 2019,” Day declares, “we did not have to turn people away because we expanded. We had enough room for exhibitors but we needed both halls.” Unable to resist a boast, he adds: “We’ve been the fastest-growing trade show in the country three years running.”

One face in the December crowd was seasoned financial broker Scott Jordan, the Denver-based managing director of the Alternative Finance Network. He was occupying a booth accompanied by two attractive female models in fetching T-shirts emblazoned with the message: “How much would you borrow at zero percent?”

The young ladies’ arresting appearance and the message worked to the extent that “it got people talking,” Jordan says. As for the zero-interest rate, it’s not exactly free money. “I’ve got a product that puts together a line of credit,” he explains, “and after they receive the line of credit, it charges them a fee.”

As a broker, Jordan does the spade work of poring through a cannabis business’s financial statements and business model before he tees up a deal—typically between $250,000 and $750,000—to “a cadre” of 35 lenders in 10 states. He’ll ascertain whether the best funding option should be structured as equipment leasing, a working-capital loan, a revolving line of credit, project financing, or a real estate loan.

One recent cannabis deal that Jordan midwifed involved a “post-revenue, pre-profitability” manufacturing and processing company headquartered in Colorado. The financing, which closed in April, 2019, involved a pair of four-year term loans: one for $400,000 to refinance existing machinery, and a second for an additional $500,000 to acquire new laboratory equipment. Both credits carried interest rates in the “mid-teens,” he says, and were secured by the equipment.

Once the debt financing was in place, the manufacturing operation was “fully functioning,” Jordan reports, paving the way for the company to raise $30 million in venture capital financing. Jordan argues that “even if they pay a 10-20 percent interest rate, it’s better to preserve equity and finance through a normal type of loan. If you need an extraction machine or packaging equipment,” he adds, “why give up equity if you can finance it through debt?”

Jordan’s reasoning appears to sit well with clients and funders alike. Since 2014, he has brokered 85 transactions worth $33 million. He reckons that two out of three deals that he takes to funders meet with success. “My best year was 2015 because there were only a few competitors and I was the only guy on the block,” he says.

As the country steadily decriminalizes and legalizes pot, however, early market entrants like Jordan no longer have the cannabis business all to themselves. Thirteen states have legalized recreational marijuana for adults. These include California, Colorado, Oregon, Washington and Nevada in the West; Illinois and Michigan in the Midwest; and Massachusetts, Vermont and Maine in the East. Hawaii and Alaska permit it and, if you’re over 21, you can legally grow, smoke or ingest weed in the District of Columbia, but it cannot be sold commercially.

An additional 24 states have approved medical marijuana. While research on cannabis’s medicinal properties remains thin—largely because of objections by federal law enforcement—it is being prescribed for a range of maladies, including cancer, glaucoma, epilepsy, Crohn’s Disease, multiple sclerosis, nausea, and pain. [“The marijuana plant contains more than 100 different chemicals called cannabinoids,” according to WebMD. “Each one has a different effect on the body. Delta-9- tetrahydrocannabinol (THC) and cannabidiol (CBD) are the main chemicals used in medicine. THC also produces the ‘high’ people feel when they smoke marijuana or eat foods containing it.”]

Industry data assembled by MJBizDaily reflects both the broad acceptance of legal cannabis use and its increasing commercial popularity. U.S. revenues from legal weed and its byproducts are expected to clear $16.4 billion this year, a 40% growth rate over the $11.75 billion in estimated revenues for 2019. The legal cannabis industry now employs about 200,000 persons in the U.S., about the same number as flight attendants (120,000) and veterinarians (80,00) combined.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

“We’re showing that sales were close to $3.2 million on the first day of 2020,” says MJBiz’s Day. “Illinois is the big story right now,” he adds. “Anytime a new state opens up in the market, you’re seeing enormous pent-up demand and enthusiasm.”

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

That designation has also made it hard for the cannabis industry to engage in simple financial transactions, much less obtain financing. “Despite the majority of states’ having adopted cannabis regimes of some kind, federal law prevents banks from banking cannabis businesses,” Joanne Sherwood, president and chief executive at Citywide Banks, a $2.3 billion-asset bank headquartered in Denver, testified to Congress last summer. “The Controlled Substances Act,” added Sherwood, who is chair of the Colorado Bankers Association, “classifies cannabis as an illegal drug and prohibits its use for any purpose. For banks, that means that any person or business that derives revenue from a cannabis firm is violating federal law and consequently putting their own access to banking services at risk.”

And despite the herculean efforts by the cannabis industry to soften its image, obtaining financing from traditional sources like pension funds, insurance companies and university endowments remains a daunting proposition as well, says David Traylor, senior managing director at Golden Eagle Partners. His four-person, boutique investment fund, which makes equity investments in up-and-coming cannabis companies, relies on wealthy individuals and family offices for the bulk of its funds.

“Capital is hard to come by for this industry,” Traylor says. “From day one, most venture capitalists have been staying out of it. It’s still illegal in many states and their limited partners are endowments like Harvard and Yale, which see marijuana as the antithesis of education.”

Sarah Sanger, chief financial officer at Oak Investment Funds, a real estate investment firm based in Oakland, says: “There’s a great deal of economic activity in California but it’s stymied by the lack of financing and difficulty with changing regulations. It provides an opportunity for really expensive debt from private investors willing to do due diligence.”

That absence of establishment financing has opened up a plethora of opportunities for alternative funders, and not just in agriculture and plant cultivation. While agriculture represents the bedrock of the industry there is no downstream product, of course, without the cannabis leaf— growing and harvesting cannabis is just one stage of the industry’s life cycle.

MJBiz’s Day notes, for example, that that the legal cannabis industry is regulated for safety, so growers must show that “the flower has no molds or contaminants.” That means that crops are subject to rigorous testing and decontamination, which requires both materials and expertise. To process the leaf and develop “infused products” by extracting cannabis-based oils entails the purchase and deployment of costly technology. Packaging and labeling along with tracking systems that, Day says, “are stricter than in other places” are also key components of the farm-to-market supply chain.

Meanwhile, in an ongoing effort to appeal to a fresh cohort of customers, Jordan notes, the cannabis industry continues to develop innovative uses for the plant. “There are so many applications and new products that keep appearing, like ice cream with marijuana, vaporizers, inhalers, and syrup,” he says. “Now, there are mints—something I hadn’t seen before—and different ways to ingest the product and get high and not look like a druggie.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Recent Greenbox Capital deals in 2019, Fein says, included one with merchant cash advances of $80,000 and $60,000 in growth capital to a Colorado dispensary. The operation put the money to work adding two retail outlets during the year, he says, bringing to four its total number of storefronts. In addition to cannabis flower, the dispensary sells “edibles, tinctures, lotions, and wax concentrates,” Fein reports. Both short term cash advances require regular ACH payments.

Greenbox Capital also made a $135,000 cash advance to a cannabis-testing laboratory in Southern California in August, 2019 for the purchase of sophisticated equipment. The company, he says, is doing $140,000-a-month in revenue and cashflow is strong and on the rise.

“Greenbox is always interested in higher risk deals,” Fein says, noting that banking services remain off limits to legal cannabis firms. “But we fund them for the same reason we fund lawyers and auto sales—things that most others will not do. There’s nothing wrong with risk,” he adds, “as long as you clearly assign a proper value to the deal and price to it.”

Steve Sheinbaum, a New York broker and chief executive at Circadian Funding, has unabashedly climbed aboard the cannabis bandwagon. “The market is exploding and it’s attractive to lenders because it’s a product people can put their hands on,” he says. “If I’m dealing with a grower, I can leverage real estate and usually there’s equipment. If they’re producing, there’s inventory and I can look at the income statement to see what kind of cash flow the business is generating.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

In another recent deal, Circadian arranged an unsecured merchant cash advance for $300,000 to a Pacific Northwest technology company developing specialty, point-of-sale software for the cannabis industry. The firm showed monthly revenues of $300,000.

“It’s not federally permitted for cannabis firms to take payments from Visa, Mastercard or American Express,” Sheinbaum explains. “But this technology company is using debit or credit cards to pay for cryptocurrency which is stored on a prepaid card which customers can then use to purchase cannabis.”

The tech company had been struggling to find money and Sheinbaum took satisfaction in a deal announcement that went out in an e-mail to the industry. “Funding complicated deals is what gets our blood flowing,” Sheinbaum wrote. “Anyone can get a restaurant or dentist funded. No one needs help with that.”

Manny Columbie, a Miami-based senior funding manager at H&J Capital Group, an Orlando firm, reports funding agricultural and dispensary businesses in California, Colorado and Washington State. In the Evergreen State, he says, he recently provided funding to a woman who owned a marijuana-themed café connected to a cannabis dispensary. The deal went through after examining her recent bank statements and two years of federal tax returns.

“The best thing about lending to people in this industry is their ability to repay,” Columbie says. “They’re never lacking in funds.”

He provided more detail on a deal currently in the works involving a physician in Irvine, California, with an 800-plus credit score from the rating agency Experian and personal tax returns showing $2 million in annual income. The doctor, Columbie says, has been making transdermal patches infused with THC in addition to his medical practice and needs specialized equipment to lower his manufacturing costs to 55 cents per patch. The patches sell for $40-$60 apiece, Columbie says, depending on the THC content.

If the deal goes through and is approved by H&J’s credit committee, the physician would likely be extended a $350,000 loan with a 10-year maturity secured by the Chinese-manufactured equipment. Factoring in the doctor’s excellent credit and other positives, the interest rate on the credit could be as low as 5%-7%.

While the environment for legal cannabis seems to grow more favorable by the day, market participants urge funders to remain circumspect. One remaining fly in the legal cannabis ointment has been the persistence of an illegal black market. Estimates are that as much as 60% to 80% of the marijuana market in California is illicit, says Craig Behnke, an equity analyst at MJBiz.

Law-abiding businesses must also contend with overbearing regulators and high taxation. The California Department of Fee and Tax Administration recently jacked up its excise tax on cannabis to 80%, effective on Jan. 1, 2020.

And the state’s constabulary isn’t helping matters either, notes Sanger of Oak Funds. “There are going to be a lot of operators that end up being losers because of the regulatory environment,” she says. “Law enforcement is using all of its resources to make sure legitimate businesses are following the rules instead of clamping down on black market activity. That makes it harder for legitimate retailers to make money because people are still shopping in the black market.”

The recent collapse of the shares of publicly traded Canadian cannabis companies, which some blame in part on the illicit competition from the black market, also stands as a cautionary sign. Last August, the Motley Fool listed ten “Pot Stocks”—including Canopy Growth and Aurora Cannabis, both of which are listed on the New York Stock Exchange—that together lost a stunning $20 billion in market capitalization.

The drubbing that heedless investors have taken in the Canadian stocks reminds analyst Behnke of the debacle in dotcom stocks back in 2001-2002, but with a big difference. “The dotcoms were a brand-new invention and people had no idea how big the Internet companies would be,” he told AltFinanceDaily. “But cannabis has been around for a thousand years. I feel like it was a shame on investors and the companies. This shouldn’t have happened.”

Big Money, Small Town: How SBA Loans Are Powering America

December 26, 2019

“The Mountains Are Calling” is the motto of Gatlinburg, an East Tennessee town of roughly 4,000 citizens known for its spectacular views of the Smoky Mountains and as a jumping-off spot for hikers, campers and winter skiers. The town also offers attractions such as Ripley’s Aquarium and arts-and-crafts festivals.

“The Mountains Are Calling” is the motto of Gatlinburg, an East Tennessee town of roughly 4,000 citizens known for its spectacular views of the Smoky Mountains and as a jumping-off spot for hikers, campers and winter skiers. The town also offers attractions such as Ripley’s Aquarium and arts-and-crafts festivals.

To get around, 800,000 tourists and locals alike hop aboard the 20-odd trolley buses operated by Gatlinburg Trolley, the private transit system. Few riders marveling at the picturesque scenery and enjoying the sprightly vehicles, which recall San Francisco’s cable cars, know that they’re riding a custom-made trolley-bus built by Hometown Trolley of Crandon, Wisconsin.

And even fewer would know that the chief executive and president of that company is Kristina Pence-Dunow, making it the only female-owned manufacturer of transit vehicles in the US. Bolstering the manufacturing enterprise—which Pence-Dunow acquired in 1997 from her ex-husband, who wanted to “liquidate” it, she says—have been multiple bank loans backed by the Small Business Administration.

And even fewer would know that the chief executive and president of that company is Kristina Pence-Dunow, making it the only female-owned manufacturer of transit vehicles in the US. Bolstering the manufacturing enterprise—which Pence-Dunow acquired in 1997 from her ex-husband, who wanted to “liquidate” it, she says—have been multiple bank loans backed by the Small Business Administration.

The most crucial SBA loan came in 2005, she says, just as she was nearly driven out of business in a price war. “We had to be innovative” to survive the cutthroat competition, Pence-Dunow told AltFinanceDaily in a telephone interview.

Using a $350,000, five-year SBA credit issued by River Valley Bank (now Incredible Bank of Wausau, Wis.), the transit company developed the prototype for a “lowfloor entry vehicle.” The design feature made her trolleys accessible to riders with walkers and wheelchairs and enabled the company to beat out its competitor for a key contract with Hampton Roads (Va.) Transit. That deal, in turn, generated sales to transit authorities in Miami Beach, Laguna Beach, and the University of Oklahoma.

Subsequent SBA loans, Pence-Dunow says, enabled the company to create its own dealer network and develop battery-powered, clean-energy vehicles. The financings also allowed her to buy out, in 2016, the rival trolley company that had tried to run her buses off the road.

Her grit and determination—for many years Pence-Dunow ran the company as a single mother raising two children—have also paid dividends for her Wisconsin community. With annual sales of $20 million and 65 employees receiving health and life insurance as well as pension benefits, Hometown Trolley has brought good-paying jobs to successive generations of families in the Northwoods.

In 2018, she earned the SBA’s “Small Business Person of the Year” award for the state of Wisconsin.

Hometown Trolley, meanwhile, is just one of 30 million small businesses that make up the backbone of the US economy. Small businesses—a small business is broadly defined as a commercial or professional enterprise with fewer than 500 employees—accounted for the employment of 58.9 million people in 2015, according to the US Census Bureau’s most recent figures. That’s just shy of 50% of the country’s total workforce. And it seems that the smaller the better: In 2018, firms employing fewer than 20 employees added 1.1 million net jobs to the US economy, the largest gains among the small business cohort.

By contrast, large manufacturing companies only employ about 11% of the total workforce, notes Karen G. Mills, former SBA administrator and member of President Barack Obama’s cabinet. The bottom line is that the contribution to the economy made by both small business and the SBA “is under-appreciated,” says Mills, now a senior fellow at Harvard Business School and author of Fintech, Small Business & the American Dream. “It’s a much more powerful job-creator than the manufacturing component of the US economy,” she adds.

By contrast, large manufacturing companies only employ about 11% of the total workforce, notes Karen G. Mills, former SBA administrator and member of President Barack Obama’s cabinet. The bottom line is that the contribution to the economy made by both small business and the SBA “is under-appreciated,” says Mills, now a senior fellow at Harvard Business School and author of Fintech, Small Business & the American Dream. “It’s a much more powerful job-creator than the manufacturing component of the US economy,” she adds.

During the Great Recession, which coincided with her tenure at the SBA, Mills reports that 60% of the country’s job losses were in the small business sector. As many as 1.8 million jobs disappeared in a single quarter in 2009. Mills credits the SBA’s lending as playing a key role in buffering the US economy against even more severe ravages.

To help reverse the economic free-fall, the SBA eliminated all SBA fees and temporarily upped the 75% government credit guarantee to 90%. The agency also persuaded a thousand commercial banks that had not issued an SBA-backed credit since 2000 to turn on the spigots. “Banks are the primary source of financing for small businesses,” she notes. “They (small businesses) can’t go to the credit markets like big business does.”

S.R. Rosati, Inc., an Italian ice manufacturer based in Clifton Heights, Pa., is one of those small businesses that nearly went belly-up. Headed by Richard Trotter, a West Point graduate, former US Army captain and company president, the Italian ice business is thriving today. It has just under 30 employees and reports annual sales of $10 million. But ten years ago it was in desperate straits. “Even though we’re a 100-year-old company,” Trotter says, “we could have been like a ton of businesses that went out of business every week. The SBA helped us get through tough economic times in 2007-2008 when a lot of businesses took a hit.”

The SBA’s flagship product is the 7(a) loan, which range up to $5 million. Almost 2,000 US banks, as well as a number of nonbanks, participate in the program. The loans are currently backed by a 75% government guarantee and are targeted to those entrepreneurs who, the SBA states, “otherwise would not have access to capital to start, grow, or expand their small businesses.”

An SBA loan, former Administrator Mills explains, “is designed to fill a market gap— to make loans to creditworthy borrowers that the market feels are too risky to make without some support.”

Currently bearing an interest rate of 7.75%-9%, according to financial technology firm Fundera, 7(a) loans are affordable and the terms are fairly generous: typically, the borrower has 10 years to repay the loan. The loans can be used for multiple purposes: as working capital, to purchase equipment and inventory, make a business acquisition, meet payroll, hire new employees, and (in some cases) refinance crushing debt.

If a borrower is eligible and able to secure a 7(a) loan, “it’s the gold standard,” remarks Levi King, chief executive and co-founder of Utah-based Nav, an online, credit-data aggregator and financial matchmaker for small businesses.

William McSweeney, chief operating officer in the business banking section at Citizens Bank in Boston, says that insufficient collateral is most often the reason that a small business fails to qualify for a conventional business loan. With an SBA loan, he says, the government guarantee serves as a bulwark “to cover the weakness of a collateral position.”

He cites the case of a dentist who’s attempting to acquire an existing dental practice for $1 million. Unless the practice owns a building, McSweeney says, there’s probably not enough collateral to support a $1 million borrowing. Yet the deal is attractive: Dentistry is a reliable industry (or “vertical” in lender jargon), the targeted practice has a solid client base, there’s strong cashflow, and the practice boasts a fully equipped armamentarium. “An SBA loan will guarantee the $1 million loan for 75 percent,” McSweeney says. “Now I can ask, ‘Is there $250,000 in collateral.’ That’s the way I look at it.”

He cites the case of a dentist who’s attempting to acquire an existing dental practice for $1 million. Unless the practice owns a building, McSweeney says, there’s probably not enough collateral to support a $1 million borrowing. Yet the deal is attractive: Dentistry is a reliable industry (or “vertical” in lender jargon), the targeted practice has a solid client base, there’s strong cashflow, and the practice boasts a fully equipped armamentarium. “An SBA loan will guarantee the $1 million loan for 75 percent,” McSweeney says. “Now I can ask, ‘Is there $250,000 in collateral.’ That’s the way I look at it.”

Adds Kirk Jacobson, an SBA lender at Northwest Bank branch in Independence, Ohio: “In my experience, the preponderance of SBA loans have a collateral shortfall. Even lending to hotels or something tangible can be risky. The collateral (the hotel) can lose value quickly. The challenge for banks like ours is to use the SBA as the tool where conventional lending doesn’t work.”

By at least one yardstick SBA lending appears to be at a crossroads. The SBA reports that the number of small businesses taking advantage of the 7(a) program fell by 13% in the most recent fiscal year, which ended September 30, 2019. The 52,000 small businesses securing 7(a) credits in 2019 was more than 8,000 fewer than the previous year. The dollar amount of credits acquired also dropped; the $23.7 billion in lending was a 6.5% drop.

This is being taken as a good sign by the agency. “A strong economy is powering America’s 30 million small businesses, and the SBA’s numbers bear that out,” Chris Pilkerton SBA’s acting administrator and general counsel, said in a recent statement. “When the economy is doing well, 7(a) lenders are more willing to provide capital without the need for a federal loan guarantee.”

But even small businesses that are outwardly healthy and experiencing growth often face hardship. Consider the case of Kyle McClelland, owner of Have Lights Will Travel, a Reno-based contractor that handles illumination for office buildings, stores, parking lots, and warehouses across northern Nevada. He got in over his head this year when he subcontracted lighting work for Macy’s and Target parking lots in a string of northern California cities.

There was no money advanced by the main contractor for materials, wages or expenses, he says. As a subcontractor, McClelland doesn’t get paid until the job is done. Yet, almost overnight, he doubled his workforce to 70 employees, footed the bill for a platoon of workers to lighting equipment, all of which exhausted his $100,000 line of credit with a Reno bank. His situation looked dire and it was taking an emotional toll. “The company was on life support.” he says. ”I realized that I needed extra funds to make payroll. I honestly didn’t sleep for months. I was lucky to get three hours of sleep a night.”

McClelland was bailed out in August when he secured a $350,000 line of credit through an SBA Express loan fronted by Five Star Bank, a Sacramento financial institution. SBA Express loans, which are part of the 7(a) program but carry only a 50% government guarantee, can be made in as few as 36 hours. But McClelland says that it took him four weeks to obtain the loan.

Trotter, the owner of the Italian ice company, says that his business too is in an expansion phase and that its financial situation was cramped. He had been saddled with a pricey, short-term note for $1.4 million that was weighing down business. With the intercession of Multifunding, a Philadelphia-area broker, Trotter took out a $2.5 million, 10-year loan with Celtic Bank in Utah at prime plus 2.75%, his third SBA loan in 20 years. The refinancing, which closed in late July, is saving him $30,000 in monthly cashflow, he says, more than $100,000 to date.

“Now we can play a little bit of offense,” he says. “We have the up-front money to go into convenience stores and supermarkets with our product.”

One common experience of the business-people who spoke to AltFinanceDaily is that assembling the required documents and applying for SBA loans can be a daunting and often discouraging task. “The whole thing with these loans is making sure the I’s are dotted and the T’s are crossed,” says Domenic Rinaldi, managing partner at Sun Acquisitions, a Chicago-based firm specializing in lower middle-market, merger-and-acquisition deals using SBA loans. “The government is demanding,” he adds, “and if everything is not in order, you won’t get your money.”

To cut through the inordinate amount of red tape, many businesses turn to brokers like Multifunding and other financial midwives, who receive a commission from the bank. “The fastest I’ve done an SBA loan is two weeks and the longest is 18 months,” says Ami Kassar, founder and chief executive of Multifunding. He says that the firm’s SBA credit business constitutes 70% of his work and that he relies on a network of 10 banks. “The average time it takes for an SBA loan is probably 90 days,” he adds.

“Grueling” is how Daniel Shemtob of Los Angeles describes his experience obtaining an SBA loan. “I had gone to 30 banks,” he says, “and I did qualify for a loan but I didn’t like the deal.”

Shemtob is the chief executive and—thanks to securing an SBA backed financing for an acquisition—the sole owner of The Lime Truck, which has bragging rights to winning the Food Network’s “Great Truck Race.”

In addition to the truck, his Southern California business also includes a couple of brick-and-mortar restaurants and a catering company. The operation, which will do $5.5 million in sales this year, employs 40 full-time workers plus part-time catering help.

Shemtob finally scored an SBA loan with assistance from Kassar’s Multifunding, which he found through Entrepreneurs’ Organization, where he’s a board member of the L.A. chapter. He was able to take out a pair of 10-year loans totaling $1.8 million with IncredibleBank at prime plus 2.75%. Even with a broker, he says, it took him three months to get the loan, which closed earlier this year. “The ten-year loans give you stability and an affordable payment,” he says. “If I hit my sales targets,” he adds, “the loans will allow me to grow the business.”

But what if he hadn’t obtained SBA-backed financing? “I don’t know if the company would be around today,” Shemtob says.

SBA loans used for acquisitions play a major role in extending the life of enterprises that likely would have disappeared upon the retirement or death of an entrepreneur, the unwillingness of succeeding generations to take control of a family business, or the break-up of a partnership, notes Rinaldi, the Chicago M&A specialist.

To arrange SBA acquisition loans for purchasers of small businesses, Rinaldi deals mainly with 18 banks, including Busey Bank (Champaign, Ill.), U.S. Bancorp (Minneapolis), Byline Bank (Chicago) and Canadian Imperial Bank of Commerce (Toronto). “Banks may say, ‘Bring us all your manufacturing deals’ and two years later there’s a management change and they’ll only make loans to distribution and service companies,” Rinaldi says. “Part of my job is understanding which sectors are handled by which banks.”

Meanwhile, an emerging debate is brewing within banking circles about the best use of SBA 7(a) loans, which were capped at $28 billion in the last fiscal year. While the overall U.S. economy has continued to prosper since the Great Recession, and the official unemployment rate has dipped below 4%, the lowest in 50 years, the bounty is being shared unevenly. While most large US cities and suburbs are generally adding jobs and experiencing good times, many rural areas and Rust Belt communities are dealing with stagnant wages, job losses and population outflows.

Meanwhile, an emerging debate is brewing within banking circles about the best use of SBA 7(a) loans, which were capped at $28 billion in the last fiscal year. While the overall U.S. economy has continued to prosper since the Great Recession, and the official unemployment rate has dipped below 4%, the lowest in 50 years, the bounty is being shared unevenly. While most large US cities and suburbs are generally adding jobs and experiencing good times, many rural areas and Rust Belt communities are dealing with stagnant wages, job losses and population outflows.

The question is: Should more banking resources be directed to distressed communities through SBA loans? Or should the banking industry lend as it sees fit, largely focused on profitability and shareholder value, albeit within the SBA’s guidelines, perhaps with a nod to businesses owned by women, minorities and veterans? Many banks incorporate both philosophies. But this dichotomy in operational goals can sometimes be seen in sharp relief.

The stark difference in SBA lending practices between Live Oak Bank of Wilmington, N.C. and Northwest Bank of Warren, Pa. is a case in point.

With $4.6 billion in assets, Live Oak Banking Company, which was founded in 2007, is just a dozen years old but it’s already become the No. 1 SBA lender in the US. In the most recent fiscal year, from just one branch on North Carolina’s seacoast, it made 913 SBA loans totaling $1.347 billion, an average of nearly $1.5 million per loan. To comprehend the magnitude of that accomplishment: Live Oak nearly lapped Wells Fargo Bank, the No. 2 lender with $786.4 million in loan totals, despite the latter’s making triple the number of SBA loans. It also out-lent such worthies as J.P. Morgan Chase and Bank of America, both of which lagged well behind Live Oak in the SBA lending tables.

With its adroit use of technology and its meteoric rise to become an SBA powerhouse, Live Oak has emerged as a Wall Street darling. Thomas Brown, a founder and chief executive at Second Curve Capital, a hedge fund that invests exclusively in financial services companies and manages $150 million in assets, calls Live Oak “a freak of nature.”

“For their veterinarian-lending practice,” Brown observes, “they hire a vet as their lending officer. They do this with all their verticals, whether it’s chicken farming or funeral homes. And when they’re dealing with a client, they have all this incredible expertise.”

Steve Smits, chief credit officer at Live Oak, told AltFinanceDaily that the bank now lends to 29 verticals across all 50 states. Its most recent additions were early childhood education centers and franchisees for aftermarket companies like Jiffy Lube and Meineke. Not only does Live Oak have experienced loan officers with deep knowledge of their sectors making the loans, but the bank is conscientious about keeping up with its clients. So much so that it maintains a stable of consultants, accountants and other professionals who are on call to add value.