Everlasting Capital Releases EverHub, a Front-End Online Portal That Delivers Enhanced Online Capability for Partners and Equipment Vendors

January 17, 2017Rochester, NH, January 17, 2017 – a trusted lender of short term working capital, equipment finance & leasing, and consolidations, today announced the general launch of the EverHub front-end solution. Everlasting Capital’s dedicated front-end proposition for Independent Sales Offices and Equipment Vendors provides an improved online service offering for building stronger relationships with our partners and clients.

The solution comprises two distinct portals, Partner Portal & Vendor Portal, each offering a user experience tailored specifically for the intended target product. The Vendor portal is intuitive and delivers convenient, time-saving access to account data, approval, underwriting, and funding information. The Partner portal delivers the same functionality but with a significantly more powerful, task and MI oriented interface for the efficiency and transparency of each file.

Josh Feinberg, Chief Executive Officer at Everlasting Capital, said “The pressure is on to retain and boost assets under management. As such, web-delivered services – which meet partner demand for convenient, time-saving access to client account data – are increasingly important. Whether a Partner or Vendor, EverHub provides the exact data they need whenever they need it, while also offering both the ability to better track applications, underwriting/funding activity, and deliver needed product messages.” He added, “We are seeing a new wave of digitalization within the financial services market and with EverHub we are enabling ISOs, equipment vendors and their personnel to really get ahead of the competition.”

The portals are delivered and deployed as a single application package and introduce significant efficiency savings from close integration with back-office administration systems and analytics. They offer real-time, web and mobile delivered access to key functionality, with simple deployment and light implementation effort. Support for multiple brands enables different, customer propositions to be developed for both ISOs and vendors.

The EverHub solution is data agnostic, using its service oriented architecture to consolidate and present information from multiple systems. Core capabilities include single sign-on, 24×7 availability and reactive design techniques. The solution is backed by a comprehensive and proven service proposition, covering support and maintenance, as well as consulting and development services.

Everlasting Capital’s Chief Executive Officer, Josh Feinberg was quoted in this press release. To ask Everlasting Capital a question regarding the release or to discuss it in more detail, email EverHub@everlastingcapital.com.

Source: Everlasting Capital

Fintech Startup BlueVine Raises $49 Million in Series D Funding

December 14, 2016- The company has provided more than $200M in financing to thousands of businesses

- In response to customer demand BlueVine is increasing credit lines to $2 million for invoice factoring and $100,000 for business lines of credit

- Company is expanding strategic relationships with partners like Intuit

REDWOOD CITY, Calif. (December 14, 2016) BlueVine, a leading online provider of everyday financing to small businesses, announced today it has closed $49 million in funding. The Series D funding round was led by existing investors, including Lightspeed Venture Partners, Menlo Ventures, 83North, Citi Ventures, Rakuten FinTech Fund and Silicon Valley Bank.

Since launching in March 2014, BlueVine’s cloud-based financing solutions have helped thousands of small businesses obtain quick, easy access to the funds they need to purchase inventory, cover expenses and expand operations.

We are very proud of all we’ve accomplished in 2016 and excited to continue on our incredible growth trajectory, said Eyal Lifshitz, CEO and founder of BlueVine. BlueVine is delivering unprecedented ease and convenience to meet SMB owners¹ financing needs and help them achieve their goals.

This financing will support BlueVine’s rapid growth as it expands its team and range of offerings. BlueVine has already funded more than $200 million in working capital for SMBs and is on track to fund more than $500 million in working capital during 2017.

This team continues to push the pace of innovation to deliver best-in-class everyday financing products, said Yoni Cheifetz of Lightspeed Venture Partners. We are delighted to have supported BlueVine’s journey to date and thrilled to enable them to bring their vision to thousands more SMBs across the country.

BlueVine’s business line of credit has proven to be very popular with QuickBooks users, said Rania Succar, business leader of QuickBooks Financing. It fills a critical part of the QuickBooks Financing portfolio and allows us to extend credit to younger businesses. We are excited about expanding our partnership to serve even more QuickBooks SMBs with BlueVine’s business line of credit.

BlueVine also announced it has once again increased its maximum credit lines based on client demand:

- For invoice factoring the maximum credit limit has been increased from $250,000 to $2,000,000

- For the business line of credit the maximum credit limit has been increased from $50,000 to $100,000

BlueVine offers credit lines starting at $5,000 for a business line of credit and $20,000 for invoice factoring.

About BlueVine

BlueVine offers small businesses financing solutions to access the funds they need to purchase inventory, cover expenses or expand operations. BlueVine was the first factoring company to develop a fully online, cloud-based platform for invoice factoring, enabling rapid advances on outstanding invoices due in 7-90 days and bringing a 4,000-year-old industry into the digital age. BlueVine also offers Flex Credit, an on-demand, revolving line of credit through the same online platform. With BlueVine, business owners can focus on growing their business instead of worrying about their bank account. BlueVine is funded by Lightspeed Venture Partners, Citi Ventures, 83North, Correlation Ventures, Menlo Ventures, Rakuten Fintech Fund and other private investors.

About Lightspeed Venture Partners

Lightspeed Venture Partners is an early stage venture capital firm focused on accelerating disruptive innovations and trends in the Enterprise and Consumer sectors. Over the past two decades, the Lightspeed team has backed hundreds of entrepreneurs and helped build more than 300 companies globally. The Firm currently manages over $4 billion of committed capital and invests in the U.S. and internationally, with investment professionals and advisors in Silicon Valley, Israel, India and China. www.lsvp.com

Press Contact

Amberly Asay

BlueVine Public Relations

801-461-9776

bluevine@methodcommunications.com

Motivating Your Sales Force – Tips From the Floor

August 30, 2016

Fancy steak dinners, electronic devices and cold hard cash are just some of the ways ISOs and funders these days are motivating sales reps to bring in business.

Although it’s largely a field for self-starters, many companies find that even small tokens of appreciation do wonders to increase rep productivity. “Waving a carrot in front of your reps can make a massive difference,” says Zachary Ramirez, branch manager of the Costa Mesa, California branch of World Business Lenders, an ISO and a lender.

When it comes to motivating sales reps, every company does things slightly differently. Some have more established incentive programs, while others are more ad hoc, depending on how the day, week or month is shaping up. The common goal of all the programs, however, is to give a little something to get something greater in return.

Ramirez remembers one sales rep who won a trip to Las Vegas and then continued to be the top rep for three months running. “Those types of rewards can keep a sales team motivated, hungry and excited,” he says.

From time to time, Ramirez offers rewards such as a small cash bonus if a rep meets certain metrics like getting three submissions in a day or multiple fundings in a week. In addition, whenever his reps, who are all hourly employees, hit key performance indicators, Ramirez rewards them with a poker chip. After they accumulate enough, they can trade in their chips for various prizes. Twenty-five poker chips might be worth a flat-screen TV and 50 chips could be an expense-paid trip to Las Vegas, for example.

When it comes to motivation, it’s important to incentivize the correct behavior, Ramirez says, noting that in his earlier years running an ISO, he used to reward reps based on the number of calls they made in a day rather than applications, approvals or fundings.

The latter represent a much more serious commitment and are worth motivating for as opposed to simply making a phone call, where the outcome is uncertain. “Even if they make as many as 500 phone calls in a day, it’s irrelevant if they are not moving the transactions forward by getting applications and bank statements,” he says.

It’s also very important to have clear-cut expectations; reps need to know the consequences of not performing, Ramirez says. Most top salespeople won’t need the stick. But it’s still necessary for them to know the policies, he says.

THE POWER OF SELF-ORIGINATION

One major way United Capital Source incentivizes its 15-person sales force is by self-originating leads. It provides its reps—who are all W2 employees—with merchants that are actively expecting phone calls as opposed to handing them a laundry list of names to pitch which may or may not pan out. It costs more for United Capital to do this, but it works well for the company and for its sales force, says Jared Weitz, chief executive of the New York-based alternative-finance brokerage.

“It enables us to put our guys in a position where they are growing with the company and the company is growing as well,” he says.

In addition, United Capital has an aggressive pay structure that allows salespeople to grow with the company. For instance, the pay plans are all based on how the company is doing overall, as opposed to an individual salesperson’s performance. In this way, it encourages the sales force to work together, as opposed to each person being out for himself. Weitz says its sales team understands that if the company hits x, the sales team gets y. United Capital also offers competitive healthcare and 401(k) plans and there’s no vesting period for employees to receive their 401(k) employer match. Additionally, the company does small things like Friday lunches on the company’s dime as a thank you for time spent. It’s another way to keep the sales team happy, Weitz says.

Fundzio, an alternative funder in Fort Lauderdale, Florida, also works very hard to make sure it keeps up its pipeline of fresh leads so that reps don’t have to do that on their own. Indeed, Fundzio provides them with between seven and ten fresh and promising revenue-earning opportunities each day. This helps tie the reps to Fundzio because they have a continuous stream of business and don’t have to find it on their own.

“It guarantees them at bats every day,” says Edward Siegel, founder and chief executive of Fundzio. It also helps tie the reps to Fundzio because they have constant business. “The key thing is having new leads,” he says.

Additionally, anyone who funds a deal gets to spin a wheel in the office at the end of the business day and earn cash or special prizes like concert tickets or a fancy dinner or a $200 gift certificate. Reps really appreciate getting those prizes, which is evident when they come back to work after enjoying their steak dinner at a Fort Lauderdale waterfront restaurant. “I think it creates a fun and relaxed atmosphere feeling. A little bit goes a long way,” Siegel says.

Additionally, anyone who funds a deal gets to spin a wheel in the office at the end of the business day and earn cash or special prizes like concert tickets or a fancy dinner or a $200 gift certificate. Reps really appreciate getting those prizes, which is evident when they come back to work after enjoying their steak dinner at a Fort Lauderdale waterfront restaurant. “I think it creates a fun and relaxed atmosphere feeling. A little bit goes a long way,” Siegel says.

One way Fundzio motivates reps from the get-go is to bring them on initially as independent contractors. If they prove themselves over a 90-day period, they have the opportunity to become an employee. At any given time, the company has about 20 to 25 sales reps, representing a combination of contractors and W2 employees.

Another way Fundzio helps motivate reps is by allowing them to earn residuals from repeat business for the life of the account as long as they are still employed by the funder. Many funders have renewal departments and reps don’t directly benefit when a customer does repeat business, but that’s not the case at Fundzio, Siegel says.

REVVING UP SALES WITH CONTESTS

Certainly, to succeed in the alternative finance industry, sales reps have to be self-starters. It’s a key requirement to do the job well, in part because so many shops are purely commission-based. Nonetheless, many companies find it helps to grease the wheel a bit—regardless of whether reps are independent or W2 employees.

Fast and Easy Funds, for instance, holds weekly contests to encourage its internal sales force of 15 independent contractors. One week the contest may be for the rep with the most dials, another week it’s for the most submissions and another week for the highest number of deals funded. Each contest pays in the vicinity of $150 to $250 cash. “Every week I change it up. They don’t know what the contest is going to be until the last day of the week,” says David Avidon, president of Fast and Easy Funds, a broker and alternative funder in Boca Raton, Florida.

iAdvanceNow, a brokerage firm in Uniondale, New York, runs daily, weekly and monthly bonuses for its 38-person sales force. For instance, if a rep submits two completed deals for approval in a day he or she might get $100 cash; for three completed deals, the cash bonus might be $250, says Eddie Hamid, president of iAdvanceNow.

On a weekly basis, for submitting six complete files, reps get one spin on a big Wheel of Fortune-like apparatus in the office. Everybody is a winner; the prize depends on where the arrow lands. It may be a cash prize of $20, $50, $100 or a physical prize like a 40 inch-Samsung TV, an Apple Watch or iPad, Hamid explains.

On a monthly basis, meanwhile, each team of five to seven sales reps has a goal. If as a team they reach their goal, they get $1,500. Additionally, the top producer of the month—provided he or she has achieved a minimum of three merchants being funded—receives the top producer bonus of $1,500. The runner-up receives a $1,000 bonus and the third place sales rep receives $500. The top team in the office also gets a steak dinner at a local establishment, Hamid says.

The system works because it gives them a drive to obtain a goal while also encouraging friendly competition, says Hamid, noting that he once overheard reps talking about how much they value being named the top producer. “With sales people, they are more concerned with the recognition than the prize or the money they are receiving,” he says.

iAdvance has been in business for about two years. The current motivational system has been in place for about a year-and-a-half and it seems to work very well to motivate the sales force, Hamid says. In addition, if they are having a down sales month, Hamid ups the ante for the daily goals, adding not only cash, but also prizes.

These techniques all help to light a fire under the sales force, he says.

STRATEGIES FOR SLOW DAYS

STRATEGIES FOR SLOW DAYS

Sometimes around 3 p.m., if he feels like the room is starting to quiet, Jordan Lindenbaum, director of sales at Excel Capital Management in New York, a business financing ISO, might offer $20 or $30 cash for the next submission. Or he might offer $40 to $50 for two or three submissions by the end

of the day.

“All it takes is one slow day to kill the energy of a sales rep,” he says.

Lindenbaum finds that motivation checkpoints seem to work well. For instance, at the end of the month, the firm commonly gives a $200 bonus to the sales rep with the most submissions. For actual deals funded, Excel Capital is also working to implement a more concrete revenue-based bonus system as well, Lindenbaum says.

Excel Capital works with independent ISOs in addition to its in-house staff to bring in business. To encourage independent ISOs to refer business, the funding company offers higher payouts to those who consistently bring in high quality deals than to ISOs who bring in deals sporadically.

Chad Otar, co-founder and managing partner at Excel Capital, says a key piece of motivating sales reps is to make sure the sales manager feels motivated as well. Accordingly, the firm also makes sure to motivate Lindenbaum with larger payments for doing an outstanding job of motivating the sales force to bring in deals. “We need to motivate the sales manager so the sales manager motivates the people on the phone. It’s a chain effect. You motivate one and it motivates the others,” he says.

Excel Capital also believes in the power of team rewards. Recently, for instance, company executives treated all staffers to a steak dinner at Delmonico’s in New York City. “We’ve done it many times so our team knows they are appreciated and that our goals were met because everyone worked together,” Otar says.

THE SALARY VS COMMISSION CONUNDRUM

Paying reps a base salary in addition to commissions is another strategy some ISOs use to motivate sales reps. A salary is especially meaningful to reps just starting out, notes Ramirez of World Business Lenders.

He says he has worked with a lot of ISOs and many of them don’t want to pay reps a base salary because they feel it’s a mistake to give them a cushion. Because by doing so, reps get comfortable and when they get comfortable, they don’t push deals—or so the thinking goes. But Ramirez believes this is counterproductive to the rep’s career and the ISO’s sales.

He believes reps should be given a big enough base while they are learning the industry—say for 90 days. Giving them $2,500 a month or so, motivates them and it doesn’t choke their possibility for survival. “You have to give every salesperson the opportunity to succeed. Give them some coaching, give them some guidance, give them a little time. But if there’s no possibility of that rep succeeding or being an asset to your team, it’s important to remove them as efficiently as possible,” he says.

It may seem counter-intuitive, but removing dead weight is also motivating for reps who are really working hard to sell, Ramirez says. To keep that person is demoralizing for the other reps—who may feel they don’t have to work as hard either or who feel they have job security even without doing their best. “It fosters complacency,” he says.

National Funding Deploys $1.5B, Beefs up Automated Underwriting

July 26, 2016California-based small business lender National Funding said that it has deployed $1.5 billion in capital, funding small businesses with short-term working capital loans.

The 17-year-old company funded $152 million in loans in the half of 2016, up 45 percent from the same period last year. The company’s customers include general contractors, medical services and trucking companies that average about $1 million in sales annually.

While 80 percent of the loans are for working capital, the company has seen demand for equipment leasing slowly resurge after the financial crisis. “After 2008, the market turned negative in LA and we had to shrink our company,” said CEO Dave Gilbert.

The company is also preparing for a technology overhaul, trying to get access to data pools to automate underwriting. “We need to be tech driven,” he said. “As deals get smaller, we need to automate them to make it affordable.”

National Funding generates 25 percent of its loan volume through brokers. “Given everything that’s happening in the industry, a lot of lenders will be forced to become balance sheet lenders,” he said.

The company hired Geoff Howard from Intuit to lead its technology efforts and aims to automate underwriting for 40 percent of its deals, doubling up from its present rate of 20 percent.

The average size of its loans is $50,000 and the company also plans to launch its first long-term loan product later this year.

Direct Mail Still Very Effective, Says National Funding President Torrie Inouye

April 16, 2016 When I met with San Diego-based National Funding President Torrie Inouye at Lendit, I was surprised to learn that the company had quietly funded $293 million to small businesses in 2015, enough to earn them a spot on AltFinanceDaily’s top 10 alternative business funder list. The company isn’t new. They were founded in 1999, which puts them in the same category as CAN Capital, a 90s era relic that has not only survived but has continued to evolve and quite literally be a leader of the pack.

When I met with San Diego-based National Funding President Torrie Inouye at Lendit, I was surprised to learn that the company had quietly funded $293 million to small businesses in 2015, enough to earn them a spot on AltFinanceDaily’s top 10 alternative business funder list. The company isn’t new. They were founded in 1999, which puts them in the same category as CAN Capital, a 90s era relic that has not only survived but has continued to evolve and quite literally be a leader of the pack.

Inouye graduated from Stanford University in 2001 with a BA in Economics and started at National in 2004 where she worked as a Corporate Strategy Analyst. After 3 and a half years, she went on to play key roles at Union Bank and Intuit before returning back to National in the Fall of 2014. With a strong background in data analytics, Inouye took over as the company’s president just last week. Dave Gilbert, the company’s founder, has been the CEO since the beginning.

“Dave has always understood that data is valuable,” Inouye said, adding that she had been tasked with harvesting it.

“One of the trends that we’re seeing in our data is our direct mail response rates being much higher than what other people might expect,” she said. “We’re still surprising really good at direct mail.”

Others within the alternative lending space have made similar assertions, which ironically kind of undermines the concept of online lending itself. For Inouye, she says the online part is “the product.”

“You can control the message and you can control who you’re talking to with direct mail,” she explained. Though in a way the offline tactic is driving people to engage online. “A lot of our direct mail response comes through our website,” she said.

An expanded version of our interview will appear in AltFinanceDaily’s May/June 2016 edition scheduled to come out in early June. Subscribe FREE here.

Lending Club TurboTax Integration Attempts to Solve Marketplace Lending’s Tax Problem

February 15, 2016 Lending Club’s retail investors scored big on February 12th when they announced an integration with TurboTax software. The complexity of marketplace lending from a tax perspective has historically been one of the most prohibitive cost barriers for retail investors. Unlike savings accounts which issue a standard 1099-INT, Lending Club (and Prosper) issue both a 1099-OID and a 1099-B.

Lending Club’s retail investors scored big on February 12th when they announced an integration with TurboTax software. The complexity of marketplace lending from a tax perspective has historically been one of the most prohibitive cost barriers for retail investors. Unlike savings accounts which issue a standard 1099-INT, Lending Club (and Prosper) issue both a 1099-OID and a 1099-B.

According to the IRS, the 1099-OID should “state the excess of an obligation’s stated redemption price at maturity over its issue price. Original Issue Discount (OID) on a taxable obligation is taxable as interest over the life of the obligation. If you are the holder of a taxable OID obligation, generally you must include an amount of OID in your gross income each year you hold the obligation.”

For the average person, explanations like these are enough to warrant the help of an accountant. But that’s a problem for people that are investing a small amount. For example, if $10,000 invested in Lending Club notes generated $700 in income for the year, it wouldn’t be practical to pay an accountant $500 to help you figure it all out. Between that and the actual taxes owed, an investor could easily end up losing money.

For the average person, explanations like these are enough to warrant the help of an accountant. But that’s a problem for people that are investing a small amount. For example, if $10,000 invested in Lending Club notes generated $700 in income for the year, it wouldn’t be practical to pay an accountant $500 to help you figure it all out. Between that and the actual taxes owed, an investor could easily end up losing money.

Lending Club tries to make it all as easy as possible for investors with their step-by-step tax guide, but it can still feel a little confusing. One problem to consider is that investors can only deduct up to $3,000 of their losses if they don’t have any other capital gains.

While an integration with TurboTax is a win for retail investors, marketplace lending had long been a thorn in the side for TurboTax. Complaints about the software not being “peer-to-peer friendly” have haunted Intuit’s help pages for years.

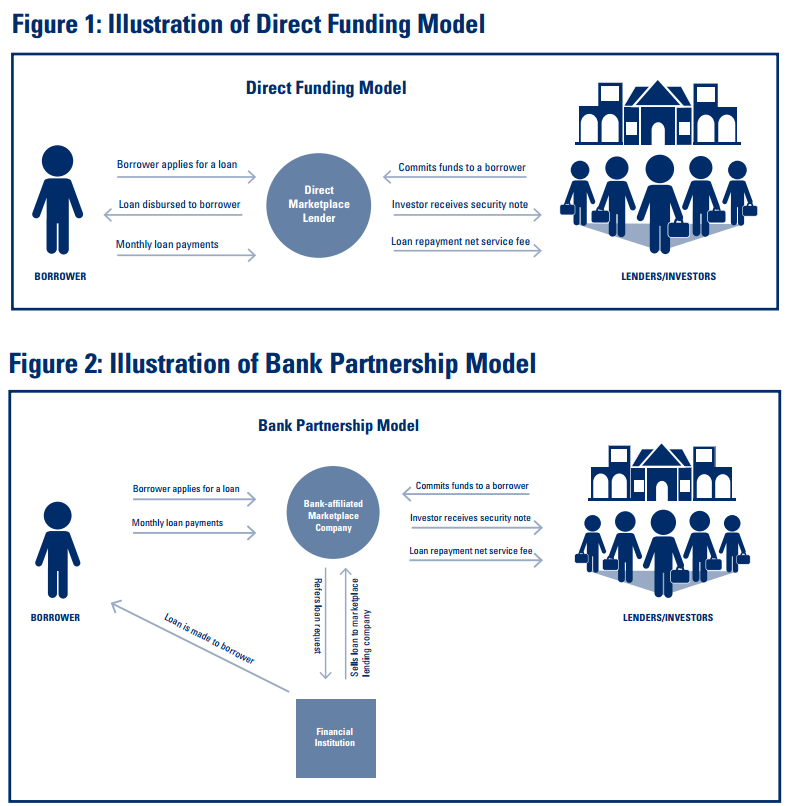

How the FDIC Defines Marketplace Lending

February 5, 2016Marketplace lending is one of this year’s hottest buzzwords but its meaning is not very intuitive. According to a recent Federal Deposit Insurance Corporation (FDIC) report, “marketplace lending is broadly defined to include any practice of pairing borrowers and lenders through the use of an online platform without a traditional bank intermediary.” This might sound similar to peer-to-peer lending and that’s because it’s the same thing, the FDIC explains. “Although the model, originally started as a ‘peer-to-peer’ concept for individuals to lend to one another, the market has evolved as more institutional investors have become interested in funding the activity. As such, the term ‘peer-to-peer lending’ has become less descriptive of the business model and current references to the activity generally use the term ‘marketplace lending.'”

Voilà, marketplace lending is what you get when peers are replaced by private equity firms, pension funds, and hedge funds. Additionally, there is a general assumption that the intermediary platform is also underwriting and grading the loans.

The FDIC separates marketplace lenders into two categories, the “direct funding model” and “bank partnership model,” both of which are illustrated below:

In both circumstances, investors are actually buying securities, rather than participating in the loans themselves.

The FDIC says that marketplace lending can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, education financing, real estate loans, merchant cash advance, medical patient financing, and small business loans.

For even more information, read the official report.

Credibly Secures $70 Million Credit Facility Led by Suntrust Bank

February 2, 2016NEW YORK—February 2, 2016—Credibly, a tech and data-inspired lending platform that makes access to capital for small businesses simple and intuitive, announces the closing of a $70 million credit facility with SunTrust Bank, one of the nation’s largest financial services firms, and Alostar Bank of Commerce, a specialty provider of asset-based loans. SunTrust served as the structuring and administrative agent, committing $50 million, with Alostar coming in as the first participant with a $20 million commitment. The terms of the deal allow for flexibility to increase the committed amount by another $30 million, bringing the total facility potential to $100 million.

An online lending platform that delivers a broad range of short- and long-term capital to satisfy the entire SMB credit spectrum, Credibly has provided access to capital for more than 4,500 businesses in over 300 industries. In the past year, the company has increased revenue 100%, was recognized by Crain’s as one of the 50 fastest growing companies in New York, and made its second consecutive appearance on the Inc. 500 list of the fastest growing private companies in America.

The new credit facility is consistent with Credibly’s three-prong financing strategy: on-balance sheet, whole loan sales, and securitization. The facility more than doubles Credibly’s onbalance sheet funding capacity, accelerating their ability to provide more small businesses with access to affordable capital, regardless of credit profile or life cycle stage.

“Being vetted and validated by a bank partner of SunTrust’s stature is one of our greatest milestones to date, and provides us with one of the lowest costs of capital in the industry,” said Glenn Goldman, CEO of Credibly. “The continued participation from Alostar – our first credit facility lender going back to 2014 – gives us increased flexibility in our product suite, which in turn provides better terms for borrowers and helps us execute on our core philosophy that all small businesses deserve access to right-sized capital.”

“SunTrust is pleased to work with Credibly to assist them in achieving their mission to fuel American entrepreneurship through access to capital,” said Tarun Mehta, Group Head, Financial Institutions Investment Banking at SunTrust Robinson Humphrey.

“The new SunTrust facility is a validation of the strength of the platform and team that Credibly has built. We remain extremely excited about our partnership with Glenn and his team” said Steve Begleiter, Managing Director at Flexpoint Ford, LLC, a private equity firm that added Credibly to its portfolio in 2014.

About Credibly

Founded in 2010 and with offices in Michigan, Arizona, Massachusetts, and New York, Credibly is a best-in-class Fintech platform that leverages data science and analytics to improve the speed, cost, and choice of capital available to small businesses in the United States. Credibly is dedicated to creating a superior borrowing experience that meets the needs of all small businesses, regardless of product need or credit profile. All loans obtained through Credibly are made by WebBank, a Utah-chartered industrial bank and member of the FDIC. Learn more at www.credibly.com.

About SunTrust Banks, Inc.

SunTrust Banks, Inc., one of the nation’s largest financial services organizations, is dedicated to Lighting the Way to Financial Well-Being for its clients and communities. Headquartered in Atlanta, the company serves a broad range of consumer, commercial, corporate and institutional clients. As of September 30, 2015, SunTrust had total assets of $187 billion and total deposits of $146 billion. Through its flagship subsidiary, SunTrust Bank, the company operates an extensive branch and ATM network throughout the high-growth Southeast and Mid-Atlantic States and a full array of technology-based, 24-hour delivery channels. The company also serves clients in selected markets nationally. Its primary businesses include deposit, credit, trust and investment services. Through its various subsidiaries, the company provides mortgage banking, asset management, securities brokerage, and capital market services. Learn more at www.suntrust.com.

About AloStar Bank of Commerce

AloStar Bank of Commerce, with $900 million in assets, is a specialty lender with extensive experience in providing Asset Based Loans to middle market companies. In addition, the bank provides value for depositors, small-to-medium-sized companies and community banks across the country through on-line customer service, and unique lending products and services. Learn more at www.alostarbank.com.