Yellowstone Capital, FTC Lawsuit Results in Settlement

April 22, 2021 The lawsuit filed by the FTC against Yellowstone Capital et al has resulted in a settlement. The defendants agreed to pay $9,837,000 for the matter to be resolved.

The lawsuit filed by the FTC against Yellowstone Capital et al has resulted in a settlement. The defendants agreed to pay $9,837,000 for the matter to be resolved.

As part of it, the defendants did not admit or deny the allegations of the complaint. They also agreed to have the FTC monitor their compliance with the agreement for varying but long periods of time.

Aside from the cost, the FTC made its point in two areas, the requirement that the defendants comply with a specific system of customer disclosure and that they not debit or cause withdrawals to be made from any customer’s bank account without the customer’s express informed consent. On the former, they must (roughly speaking) disclose clearly and conspicuously the amount and timing of any fees, the specific amount a customer will receive at the time of funding, and the total amount customers will repay.

The announcement coincides with the Supreme Court decision that revoked the agency’s presumed authority to obtain restitution or disgorgement under Section 13(b), the basis that the FTC brought against Yellowstone Capital in August 2020.

The FTC signed and filed the agreement less than 24 hours before the SCOTUS decision.

North Mill Restructures Working Capital Solution and Expands Customer Benefits

April 12, 2021NORWALK, CT – North Mill Equipment Finance LLC (“North Mill”), a leading independent commercial equipment lessor providing small-ticket financing through its network of referral agents, announced today that it has restructured its working capital solution to make it more competitive with other, less cost-effective options on the market.

The financing arrangement, called “Cash Out,” allows a customer to borrow the equity of paid-up business equipment and channel the proceeds back into the company. Although similar in concept to a sale leaseback, Cash Out is structured as a loan. It delivers a well-deserved reprieve for borrowers looking for a less expensive alternative to finance day-to-day operating expenses.

“There are many ways a company can obtain working capital,” explained Paul Cheslock, VP of Customer Relations, North Mill. “Some of the more common include a merchant cash advance (MCA), a revolving line of credit and accounts receivable factoring. And while they all fill the same need, they are not created equal. Cash Out in particular offers a long list of customer benefits including better rates, monthly vs. weekly payments, and terms up to 60 months. It’s a powerful tool for our referral agent partners looking to grow their customer base.”

According to Cheslock, the product’s loan-to-value ratio was restructured to enable customers to borrow a larger percentage of equity from an unencumbered asset. One of the most significant advantages of Cash Out is that it includes an early pay-off feature. Customers can pay off the loan without premium or penalty after 18 consecutive, on-time payments — a benefit that other products simply do not offer.

“The product is simple and straightforward. There are no fees tied to accounts receivable, invoices, or credit card sales,” said Cheslock. “What’s more, the equipment that’s used for the loan stays put on site, so business operations remain uninterrupted. And if that were not enough, the borrower retains title.”

For more on Cash Out and other financial solutions from North Mill, register for the company’s upcoming webinar “Meet North Mill and Its Financial Solutions” on Tuesday, April 27, 2021 at 3:00 pm EST.

About North Mill Equipment Finance

Headquartered in Norwalk, Connecticut, North Mill Equipment Finance originates and services small-ticket equipment leases and loans, ranging from $15,000 to $300,000 in value. A broker-centric private lender, the company handles A – C credit qualities and finances transactions for numerous asset categories including, but not limited to, construction, transportation, vocational, healthcare, manufacturing, printing, franchise opportunities and material handling equipment. North Mill is majority owned by an affiliate of Wafra Capital Partners, Inc. (WCP). For more information, visit NMEF.com.

###

CONTACT: Don Cosenza, SVP, Chief Marketing Officer

PHONE: (203) 354-1710

EMAIL: dcosenza@nmef.com

Merchant Cash Advance is as Old as The Renaissance

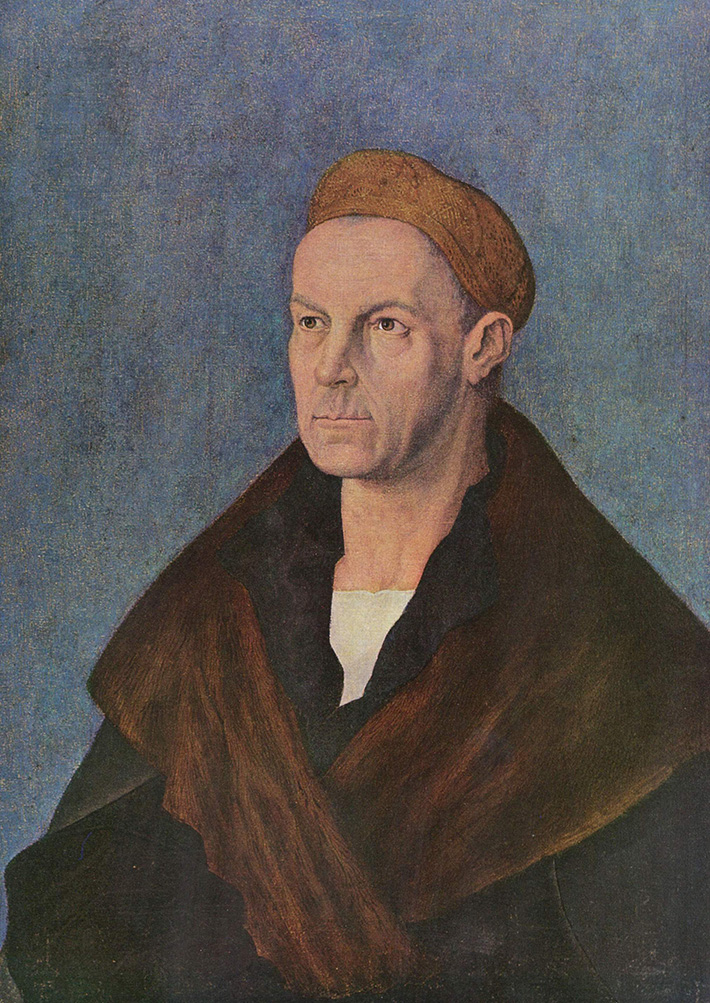

March 21, 2021 The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

In Jakob Fugger the Rich, historian Jakob Strieder writes the Fugger enterprise began as one of the upstart merchant families of the Renaissance. The Fuggers were traders and cloth merchants from Augsburg, Germany. They created a network of aristocratic clients, furnishing weddings and parties through trading warehouses in modern-day Venice, Florence, and Austria. Jakob Fugger I lent some money around, but when Jakob Fugger II joined the family shipping warehouse in Venice, he looked for a better return on capital.

According to International Business History: A Contextual and Case Approach, Fugger entered an agreement to supply some cash- 23,627 Florins to a silver mine owned by Archduke Siegmund in 1487.

Siegmund had plenty of silver laying around for collateral; he just needed cash for the day-to-day. It was a collateral-backed loan, common today: if he couldn’t pay it back, the Fuggers would get paid in silver. The transaction worked so well that a year later, Siegmund reapplied, this time in a revolutionary way. Siegmund would get 150,000 florins, and the Fuggers would get paid the future receivables of the silver mine: unrefined and cheap future silver for cash now.

The problem, written by historian Greg Steinmetz in The Richest Man Who Ever Lived, was the Church. Any interest-based transaction was specifically outlawed, though there were hundreds of lenders during this era. The line from Luke 6:35, “Lend and expect nothing in return,” was taken by the Church to mean an outright ban on usury, defined as the demand for any interest at all.

Even savings accounts were considered sinful, but Venetians ignored these rules as they preferred making money to pleasing God, entombed in the motto “First Venetians, then Christians.” Fugger began accepting deposits like a bank to his clients, with a 5% return to investors.

But convicted usurers could be excommunicated and denied a Christian burial, a nightmare for a capitalist who relied on a Christian network. Fugger did not worry about punishment or the apparent sin of money lending, but as he became a fixture in European society, his reputation became increasingly vulnerable.

Fugger needed the laws to be changed, or at least relaxed, or his lending business was in trouble. In 1515, he wrote a letter to Pope Leo X and funded a debate in the St. Petronius Basilica in Bologna. The debate ran for five hours, a back and forth of philosophy, scripture, and rampant crowd heckling. In the end, it was declared a tie, but Pope Leo X that year signed a papal “bull” reforming the concept of usury.

Originally, the Church pointed to the philosopher Aristotle’s model for determining what was okay to charge for and what wasn’t. Aristotle had said that charging someone for a cow because it produced milk was fine, but money was a dead thing and unfair to profit from.

A silver mine produced silver and as such paying cash for the future proceeds of the mine had allowed Fugger to more or less carry on his business. It wasn’t called merchant cash advance back then but he applied that model wherever he could. Not everyone in need of money had a business, however, and it was critical that he be allowed to charge interest when circumstances called for it.

More than a millennium after Aristotle, Pope Leo X found that risk and labor involved with safeguarding capital made money lending a living thing. As long as a loan involved labor, cost, or risk, it was in the clear. This opened a flood of church-legal lending: Fugger’s lobbying paid off with a fortune.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

McCarthy wrote: That was one of the problems with the Fugger model- “how does one take possession of Austria or France or Spain when its rulers default or lag behind debt repayment schedules?”

After gaining the good faith to lend in the Church’s eyes, the papacy itself became a Fugger customer. Positions in the Church were inseparable from social and political power, and the only way to get a place on the totem pole was by paying for a title. Just as the richest silver mine owners didn’t have the cash to pay for lunch- so did wealthy aristocrats need capital to afford positions in the cloth.

By the time Martin Luther “nailed” his 95 theses to the door of a church in 1517, he was rallying against the Fugger funding family and its stranglehold on the Roman Catholic Church.

It all came down to an in-house promotion. Albert Brandenburg brought a whole new meaning to the concept of “moneychangers in the temple.” A German Archbishop of Magdeburg, Brandenburg was promoted to Elector of Mainz: the second in command of the Holy Roman Empire. Unfortunately, he had to pony up 21,000 ducats to pay the Roman Curia (the Church’s admin)- for the title. Naturally, he didn’t have the cash, and the Fuggers stepped in.

Brandenburg got a loan on interest. To pay it back, he also paid Pope Leo X for the right to sell indulgences. Indulgences were contracts the church sold to forgive sins, allowing believers to purchase their way out of purgatory and into heaven. A fresh round of indulgences was printed to fund the construction of St. Peter’s Basilica, and Brandenburg was entrusted to sell them in 1517. (Their sale was later banned by the Church in 1567).

The sale of indulgences  interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

“I’m saying that there are some specific parts of modern life that derive directly from the Protestant Reformation. We couldn’t have these features if it hadn’t happened.” Ryrie said. “That combination of free inquiry, democracy, and limited government is pretty much what makes up liberal, market democracies. It runs the modern world.”

To this day, no one is sure of the extent of the Fugger fortune. Historian Mark Häberlein found that Fugger struck a deal with Augsburg Tax authorities in 1516: he agreed to pay an annual lump sum on the condition that his family’s true wealth would never be revealed. He died in 1525.

To get an idea of the extent of his wealth, we can base calculations on the cost of butchering a pig in 1522 (yes, that’s a real metric.) It cost one Gulden, a new coin minted in 1500 to butcher a hog. The German coin contained about the same amount of gold as a Florin.

Based on those ham prices, Jim Ulvog from Ancient Finances estimated that in 2017 a single florin would be worth ~$900, and other writers have put the florin in the same range. Though the true wealth of the Fuggers may never be known, when Charles V aimed to take control of the Holy Roman Empire in 1519, the Fuggers were lending Charles 543,000 guldens to buy votes: approximately $448 million. That’s just in a single deal.

It’s been said that merchant cash advances or sales-based financing is relatively new, but it could be argued that such transactions are so old that life as we know it in the modern world only exists because a guy 500 years ago was engaged in non-loan transactions to fund businesses in a manner that was Church-compliant and wanted to expand.

Maryland’s Latest Merchant Cash Advance Prohibition Bill Failed to Advance

March 18, 2021 Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

“I don’t want to snatch defeat from the jaws of victory,” he maintained.

There were several amendments up for consideration, including the inclusion or removal of a 24% APR rate cap on MCA transactions. The subject of APR dominated the light Q&A that took place, but one delegate voiced concern that creating restrictions on capital providers to businesses that might not be able to obtain funding elsewhere would probably be counterproductive. And when a roll call of votes was taken to determine if the Bill should advance to the Floor, he voted no, as did nineteen of his colleagues. Only three voted yes, so the bill did not advance, ending its prospects for the 2021 legislative session. However, it could be reintroduced again in 2022.

Committee Vice-Chair Kathleen Dumais (D) said that she thought the bill “was not ready” despite Delegate Howard “having worked hard on it.” This was Howard’s second try in two years to move it forward. His first attempt, introduced on February 7, 2020, was called the Merchant Cash Advance Prohibition Bill. The more recent one dropped the “prohibition” label but used language that would have effectively prohibited them in the state of Maryland.

Greenbox Capital Comments on Landmark Florida Legal Victory

January 7, 2021 Greenbox Capital was the victor of a major lawsuit argued before Florida’s Third District Court of Appeal that conclusively established the legality of merchant cash advances in the state.

Greenbox Capital was the victor of a major lawsuit argued before Florida’s Third District Court of Appeal that conclusively established the legality of merchant cash advances in the state.

When asked for comment, Greenbox Capital® CEO Jordan Fein said:

“It’s been a long, arduous, and expensive battle over the last few years proving in a court of law that a Merchant Cash Advance is not a loan. Today, we celebrate a win for all Merchant Cash Advance companies in Florida and the entire United States who are dedicated to funding small businesses through ethical practices. Our hard work and commitment to helping small businesses grow was validated and we are thrilled with the final decision of the District Court of Appeal.”

The decision in Florida echoes a similiar opinion reached in New York in 2018.

It’s Official, Merchant Cash Advances Not Usurious in Florida

January 6, 2021 Big news in the State of Florida. The Third District Court of Appeal entered its order on January 6th to decide the fate of Craton Entertainment, LLC, et al., v Merchant Capital Group, LLC, et al..

Big news in the State of Florida. The Third District Court of Appeal entered its order on January 6th to decide the fate of Craton Entertainment, LLC, et al., v Merchant Capital Group, LLC, et al..

Merchant Capital Group, LLC dba Greenbox Capital sued Craton in December 2016 over a default in a Purchase and Sale of Future Receivables transaction. In turn, Craton responded with various defenses and counterclaims that asserted the underlying transaction was really an unenforceable usurious loan.

The Circuit Court for Miami-Dade County sided with Greenbox in August 2019. The defendants appealed.

The District Court of Appeal decided the matter conclusively on January 6, holding that the original ruling was affirmed on the basis that:

- The transaction is not indicative of a loan where repayment obligation is not absolute but rather contingent or dependent upon the success of the underlying venture

- that the transactions in which a portion of the investment is at speculative risk are excluded from the usury statutes

- when the principal sum lent or any part of it is placed in hazard, the lender may lawfully require, in return for the risk, as large a sum as may be reasonable, provided it is done in good faith.

The decision can be viewed here.

The lawyers representing Appellee Greenbox Capital were Henderson, Franklin, Starnes & Holt, P.A., William Boltrek III, Shannon M. Puopolo and Douglas B. Szabo.

You should contact an attorney to discuss the implications of this ruling. Merchant Cash Advance contracts are not all the same.

This ruling is similar to a ruling in New York that was made in 2018.

Halcyon Capital Announces Launch

January 4, 2021A trusted Midwest Business Cash Advance, LOCs and Commercial Loan Broker with a portfolio Targeting $100K to $20MM Opportunities

Kansas City Metro Area / November 21st, 2020 – The Halcyon Group LLC (“Halcyon Capital”) announced today the launch of its Broker and ISO lending platform. Halcyon’s mission is to provide a white-gloved service and consultation to match underserved small-to-medium sized businesses (SMBs). Halcyon is here to help them unlock capital to grow and create jobs. Its financing solutions work for businesses nationwide, and in most industries.

Kansas City Metro Area / November 21st, 2020 – The Halcyon Group LLC (“Halcyon Capital”) announced today the launch of its Broker and ISO lending platform. Halcyon’s mission is to provide a white-gloved service and consultation to match underserved small-to-medium sized businesses (SMBs). Halcyon is here to help them unlock capital to grow and create jobs. Its financing solutions work for businesses nationwide, and in most industries.

About Halcyon Capital LLC

Provide fast and easy MCA, Term, LOC and Commercial Loan financing to small-to-medium sized businesses in the United States seeking $100,000 to $20 million to grow and scale their companies.

Halcyon is here to help SMBs navigate the challenges that all business owners face. They have over 30 years of experience at their side. Through a holistic approach they will review all possible funding solutions that match your business needs.

By utilizing Halcyon’s extensive lending partner platform, SMBs can dramatically increase their profitability, and ability to scale their businesses with credit facilities that can grow and become more flexible. Side by side as a compliment to their business.

PPP funding options are available as well to help ease the path associated with the nearly $300 billion in additional funding set to arrive in days. We have partnered with Lendver and Loan Source to give a streamlined tech platform. With this process it will allow business owners to take the burden off of them and remained focused on growing their business and keeping employees stable.

SMBs that need $100,000 to $20 million of asset backed or Commercial RE are often overlooked by traditional and alternative financing because the large, fixed costs of underwriting make economies of larger deal sizes important—creating a wall for smaller opportunities. Halcyon’s lender platform streamlines the application and approval process for these clients. Business owners will be able to utilize Halcyon’s lending platform to obtain financing in a fast, efficient and transparent way.

Alex Wigginton, who has significant experience in Merchant Cash Advances, Term Loans and Lines of Credit lending, will serve as Managing Partner and CEO of Halcyon. Alex Trigg, who has vast amount of experience in Commercial Real Estate, Equipment, SBA Loans and AR/Factoring, will serve as managing partner and COO of Halcyon.

For more information about Halcyon Capital go to www.halcyonlending.com or contact Alex Wigginton or Alex Trigg at underwriting@halcyonlending.com to learn more about its financing solutions.

Related Links

www.halcyonlending.com

www.linkedin.com/in/alex-wigginton-015b5036/

www.linkedin.com/in/alex-trigg/

SRS Capital Enters Chapter 7 Bankruptcy

January 4, 2021SRS Capital, a merchant cash advance company based in Long Island, NY, has entered Chapter 7 bankruptcy, according to court documents obtained by AltFinanceDaily. In September, several of the company’s creditors petitioned for involuntary bankruptcy. Although it was contested by SRS, the Court granted relief under the Code and appointed a trustee.

The primary entity is listed as SRS Capital Funds, Inc.

The company had revenues of $1.5 million in 2020.

The proceedings are ongoing. SRS Capital’s website is presently offline.