Not All Marketplace Lenders Are Created Equal – The State of Fintech Lending

March 30, 2016 It’s kind of a problematic term, said CommonBond CEO David Klein about “marketplace lending.” Klein was one of four industry experts on the State of Fintech Lending panel hosted at their office on Tuesday morning. “Not all marketplace lenders are created equal,” he said. There are different asset classes, different credit spectrums and even different investor responses, he explained.

It’s kind of a problematic term, said CommonBond CEO David Klein about “marketplace lending.” Klein was one of four industry experts on the State of Fintech Lending panel hosted at their office on Tuesday morning. “Not all marketplace lenders are created equal,” he said. There are different asset classes, different credit spectrums and even different investor responses, he explained.

CommonBond for example, focuses on student lending and more specifically, the very upper end of the credit spectrum. As proof, Klein said the company has not even experienced a 30-day delinquency or default. Compare that asset with some of the products offered by Fundera, which range from merchant cash advances to SBA loans and it’s easy to see why marketplace lending as a category can be overly broad. Fundera CEO Jared Hecht was another panelist alongside PeerIQ CEO Ram Ahluwalia and Macquarie Group Managing Director Brian Foley. WSJ reporter Telis Demos served as the moderator.

Klein’s company deals with institutional investors, which loosely qualifies it as a marketplace in the sense that there are buyers for their loans. Hecht’s company is a marketplace too but for small business owners seeking loans. Fundera is not a lender. “We don’t have to run around and deal with the capital markets,” Hecht said.

Despite the incredible diversity of asset and credit classes, PeerIQ’s Ahluwalia described the quality of the securitizations taking place throughout the industry as very good. “This is going to be a very different movie than The Big Short,” he said. As of the end of 2015, PeerIQ ranked total cumulative securitizations at $8.4 Billion, with 41 deals issued to date (25 Consumer, 9 Student, and 7 Small Business).

Pension funds and insurance funds who are attracted to this space are focused on AAA rated bonds, said Macquarie’s Foley. “They want scale, performance and track record,” he said, adding that they’re happy to trade away return for a reduction of risk so that they can sleep at night.

There’s over 200 marketplace lenders in the US, Klein stated. Only 12 or 13 have reached a certain level of scale though, he added. “2016 will be the year that marketplace lenders go from the mainstream to maturity,” he said.

Perhaps as part of that, however, the marketplace lending term will have to mature with it. “Each category is very different,” said Klein.

Commercial Finance Coalition Emerges – An All Inclusive MCA Industry Trade Group

March 16, 2016 A new trade association hopes to bring together every type of company in the alternative-finance industry to form a united front capable of managing state and federal regulation.

A new trade association hopes to bring together every type of company in the alternative-finance industry to form a united front capable of managing state and federal regulation.

The fledgling Commercial Finance Coalition (CFC) welcomes potential members that include funders, brokers, payments processors, data providers and collection agencies, said Matt Patterson, CEO of Sioux Falls, SD-based Expansion Capital Group LLC and a board member and organizer of the new trade group.

Patterson began thinking about forming an association early last year when he learned that the established Small Business Finance Association (SBFA), formerly the North American Merchant Advance Association, wasn’t communicating with legislators and regulators on behalf of the industry. “When I talked to them six or nine months ago, they had no road map for affecting legislation or regulation,” he said.

Since then, the SBFA has hired an executive director with legislative and association experience to tell the industry’s story on Capitol Hill. (See here.) So, two industry groups now plan to begin contacting government officials to educate them on the cause of small-business alternative finance.

The decision to create the CFC came at a dinner meeting convened Dec. 3 in New York. That gathering came together after several months of conference calls and videoconferences, Patterson said.

The CFC is working with two well-established lobbying groups, Patterson noted. Both organizations advised the CFC during its formation, he said.

The CFC is working with two well-established lobbying groups, Patterson noted. Both organizations advised the CFC during its formation, he said.

Law firm WilmerHale was selected to represent the CFC. The combination of Polaris and WilmerHale will give the association an immediate Washington presence, he noted.

The group intends to write best practices for its members but doesn’t contemplate starting a trade show, trade publication or merchant watch list, Patterson said.

The CFC is beginning its journey with nearly 20 member companies, according to Patterson. Recruitment of additional members is scheduled to intensify after the association has been operating for a while.

Inviting members from all facets of the industry indicates a philosophy that differs from that of the SBFA, which includes only funders on its roster, Patterson said. “We want to be inclusive,” he said. “We’re interested in building a broad base of constituents that all have an incentive to see that the industry survives and thrives.”

The coalition’s trusted service providers include:

- Arena Strategies

- Catalyst Group

- Polaris Consulting

- Wilmer Cutler Pickering Hale and Dorr

Google Culls Online Lenders – Pay or Else?

March 15, 2016Can you become one of the biggest or most successful online lenders without Google? A search layout update may be inadvertently culling the herd.

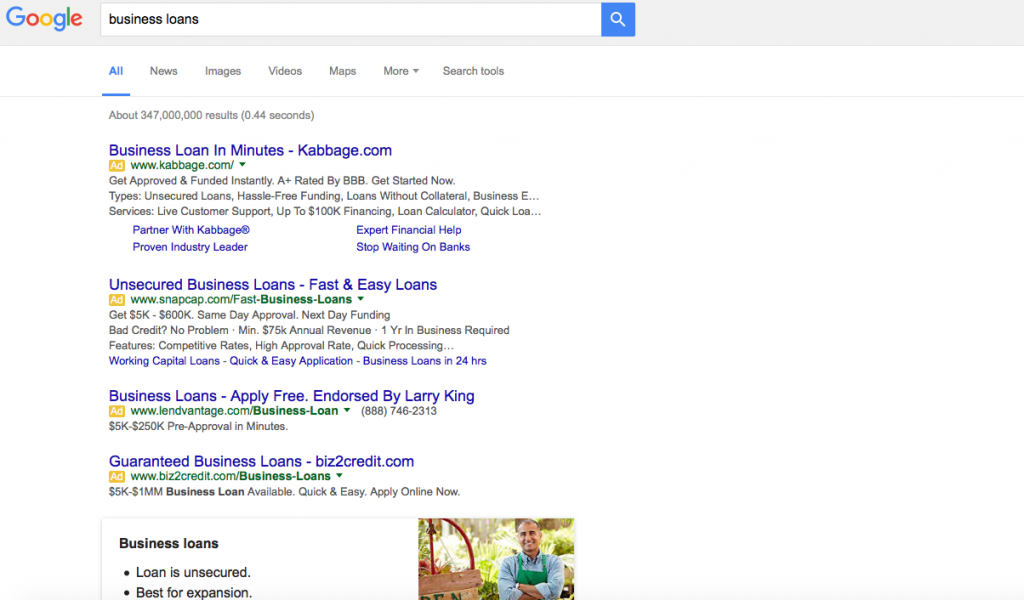

In late February, Google eliminated ads from the right side of the page while adding another layer to the top and bottom. When factoring in features like site links, the effects on organic search has been devastating. Non-paid links are now entirely below the fold for many commercial keywords, which means users may limit their selections entirely to ads. Here’s an example of a full screen browser window on a Macbook Air when searching for Business Loans:

Brad Geddes, a Google Adwords marketing author, expert and consultant, has said the Click-through rate (CTR) on this new 4th ad placement is skyrocketing. “Depending on the keyword, position 4 is going to have a 400%-1000% CTR increase,” he said on Webmaster world. And while side links and bottom links were never a huge factor anyway (less than 15% of click-throughs), Geddes believes a consequence of this change is that fewer ad slots means higher cost bids to rank on the 1st page. “Companies with thin margins are going to have a lot of words fall to page 2,” he wrote.

In summary: Fewer ad placements, higher costs per click, decreased likelihood of organic click-throughs.

And the online lending industry is already feeling the burn. Several funders and ISOs on the commercial side have told AltFinanceDaily in confidence that the online lead gen battle has been lost or that they have been temporarily sidelined by the increase in costs. At least one funder is refocusing their efforts entirely on the ISO channel after a horrible experience with Pay-Per-Click.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

On one industry forum, ISOs have reported that the cost of acquiring a merchant cash advance or business loan deal from Pay-Per-Click is ranging from $700 to $1,200. “PPC for premium keywords as high as $40 at times. Ugly. Real ugly,” one user wrote. Another user wrote, “It’s not just Adwords that is saturated. The whole market is saturated. Lenders and the onslaught of new brokers are making it tough. Lenders with programs like Funding Circle and Kabbage, and with all the advertising money in the world to burn and get direct traffic.” And still another believes that online ads are simply inviting the lowest hanging fruit. “Internet leads have the highest level of fraud,” said one sales manager.

Notably, many of the top 8 funders are only competing for a limited number of competitive keywords or may not even be running Adwords at all. PayPal and Square for example, focus only on their existing payment processing customers despite being “online lenders.”

It’s too early to tell what effects Google’s ad changes will have on the online lending industry, though a couple of companies who were paying just enough to extract clicks from side ads have indicated the change is for the worse and they have suspended their campaigns.

The natural alternative to paid search, organic search, is seldom discussed anymore as a realistic strategy these days, in part because the rankings might be rigged anyway.

One irony that’s pervasive in the online lending industry is that borrowers are being targeted offline where it’s potentially more affordable. In a discussion thread that garnered 76 posts last fall, ISOs and funders suggested that direct mail, referrals, UCCs, cold calling, radio and even going out and shaking hands, were pegged as “what’s next” for marketing. Pay-Per-Click was only mentioned once and only in the context of it being something that had long ago been made too expensive for small and mid-size companies.

The cost of making these things work might be why so many funders are hoping that brokers can figure it out. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” said Nulook Capital’s Jordan Feinstein in an interview with AltFinanceDaily last month.

With Google becoming even more competitive now though, perhaps United Capital Source’s Jared Weitz summed it up best. “Marketing is getting more expensive and only the ones who can afford to pay can play,” Weitz said.

Is OnDeck Back On Deck? – Industry Veterans Weigh In

March 8, 2016 After an unpleasant seesaw ride, Ondeck’s stock bounced back to its pre-earnings levels hovering around $8. The lender’s stock crashed 20 percent following its financial earnings on February 22nd due to a soft forward guidance.

After an unpleasant seesaw ride, Ondeck’s stock bounced back to its pre-earnings levels hovering around $8. The lender’s stock crashed 20 percent following its financial earnings on February 22nd due to a soft forward guidance.

The online lender funded a record $557 million in loans in Q4 2015 and generated $68 million in revenue but it wasn’t enough to make up for the $4.6 million in loss. As AltFinanceDaily commented earlier, the markets can be unforgiving and irrational in its speculation of a downturn. And while OnDeck prides itself for being a company built for downturns because of its short-term repayment cycle, its stock has slumped over 65 percent since its December 2014 debut.

AltFinanceDaily spoke to experts to ask how reflective this was of the industry and if this portends a larger economic gloom. Here’s what they had to say:

Downturn Survival? Not So Sure

David Obstfeld and Eric Cavalli of merchant cash advance provider S.O.S Capital, think that the market reaction to OnDeck is too strong, even unwarranted. “This is a fairly new industry and many don’t understand it yet,” said Cavalli. “Everybody is expecting an economic downturn and since this is an unproven business, one cannot really comment on whether MCA and the small business lending industry will actually survive.”

While OnDeck’s big data-led algorithmic lending has brought about a major shift in the industry, Obstfeld and Cavalli suspected that it might be why the company lost touch with the ISO base they relied on when it started.

OnDeck, Not On Deck

OnDeck, Not On Deck

Heather Francis of Elevate Funding does not consider OnDeck a part of the alternative finance industry given its business model and its fintech brand identity. “OnDeck has a brand issue, they want to be a software company on one hand and an alternative bank on the other,” Francis said. “The marketplace does not know what to do with them and no one sees what OnDeck sees in the mirror.”

Francis also commented that the hype around algorithmic lending is driven less by success and more for investor appeal in fintech. “OnDeck and Lending Club have a lot of capital behind them but there will be a lot of segregation between these companies and the traditional alternative finance companies. OnDeck cannot handle any kind of downturn.”

Just Process, Not Alarm

Corey Cicero at Platinum Rapid Funding considered the market reaction to be harsh and said that this is a normal trajectory for any company. “They are a market leader as far as brand names go. They have a lot to validate their leadership and they are on everybody’s bank statement who has a merchant cash advance,” Cicero said. “I don’t think the stock will be affected further. Congress is figuring out what to do with the industry, everyone else is figuring it out. This is a process.”

Industry Trends

Obstfeld at S.O.S Capital expects a major shakeout in the lending industry. “The market is saturated and in the next six months, the reputable companies will slash rates and when rates cannot be lowered further, companies will get creative with products and pricing.”

And Francis thinks that shakeout could come in the form of consolidation. “The market will shrink and people will spend more to get more origination and the most eye-catching product appealing to millennial entrepreneurs will take off.”

Meanwhile, Cicero at Platinum Rapid Funding said he thinks that there will be a purge of people writing bad loans. “This industry has a low barrier to entry leading to too much competition. People who write bad loans will be weeded out and the industry will correct itself.”

Cost of Online Lenders Takes Back Seat to Cost of Government Regulations

March 8, 2016 Study indicates that regulation and taxes are the chief problems, not borrowing costs.

Study indicates that regulation and taxes are the chief problems, not borrowing costs.

Small businesses are being smothered in the age of marketplace lending… by the government. According to the National Small Business Association’s (NSBA) most recent year-end annual report, regulatory burdens and federal taxes ranked among the most significant challenges to business survival.

The NSBA is a non-partisan small business organization with 65,000 members. In the survey they used to prepare their report, 33% of respondents said regulatory burdens were one of the most significant challenges to their future growth and survival. 24% cited federal taxes. The cost of health insurance benefits beat both of those with 36% of respondents choosing it.

Only 3% of those surveyed reported using an online lender or non-bank lender within the last 12 months. 43% used a bank loan, half of which came from a large bank. In another study, dissatisfied borrowers were slightly more likely to have transparency problems with big banks than online lenders.

Regulators might want to take notice of these statistics when considering future regulations for the commercial side of the marketplace lending industry. That’s because the cost of complying with any such regulations would likely increase the cost to borrowers, not reduce it.

Such was the case with Dodd-Frank and its impact on community banks. Speaking on behalf of the Independent Community Bankers of America last fall during a House Committee hearing, B. Doyle Mitchell Jr., the CEO of Industrial Bank, said that “Dodd Frank has only increased our costs.”

For bank loans in particular, 11% of respondents to the NSBA study that had taken a bank loan within the past 12 months said that the terms have become less favorable to their business. Only 4% reported the terms becoming more favorable.

When it came to the number one issue that small businesses believe that Congress and President Obama should address first, 15% said simplify the tax system, 9% said reduce the tax burden, 9% said rein-in the cost of health care reform, 8% said reduce the regulatory burden on businesses, and only 5% said increase small business access to capital.

Regulators mulling more regulation might want to consider what their constituents are actually saying, and that’s to roll back regulations, not come up with new ones. Online lenders might be expensive, but when asked what’s challenging their growth and survival, they barely even register, if they even register at all.

In a recent story by The Atlanta Journal-Constitution, Holly Wade, a representative of the National Federation of Independent Business, said “Our fear is that they will over-regulate [online lenders] out of existence or to the point that it’s no longer a benefit.”

Loan Brokers or Self Origination? Here’s What Experts Say

February 22, 2016 Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

But a year on, as the dust has settled, we asked industry veterans what it means to remain successful in this business and what is the key to sustainability — is it in going for the ISO/broker channel to find deals or originating your own.

Here’s what they had to say

Don’t Break the Broker

Tom Abramov of MFS Global voted for the ISO/broker channel and said that that’s how the company strictly does deals, working with brokers who have a track record as a part of their recruitment system. The six year old company that started as an broker shop now focuses only on funding with products that are a mix of merchant cash advances and lines of credit.

“We don’t look at FICO scores or SIC codes, we only look at cash flows of businesses,” said Abramov. “I want to see if I give a someone a dollar whether they can turn it into two.”

Abramov added that his firm offers brokers 20 percent commission and their default rates are sub 5 percent.

The advantages of scoring deals through a broker channel can be alluring. It involves no overhead, no staff that needs compensation, motivation and incentives, and makes use of the existing broker-merchant relationships.

Jordan Feinstein of NuLook Capital said that his firm works with brokers exclusively and the model has helped them respond to merchants faster. “We do not have a sales team speaking to merchants directly, that’s in conflict with our model,” said Feinstein. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” he said.

Building a Hybrid Model

There are some others who want to make the best of both the models and work with brokers while originating and funding their own deals. Forward Financing which uses a hybrid model has strategic partnerships with some brokers while still originating their own deals. “We have a hybrid model because our goal is to have a program for any type of business and work with companies across the spectrum of risk,” said Justin Bakes, CEO of Forward Financing. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said.

The Original Origination

While the allure of a lean business is certainly attractive, there are some who are in the industry to build a bigger business and create value by making it robust — Jared Weitz of United Capital Source is one of them. “There is a big market for both analytical process as well as sales process. It’s important to go after your strength,” said Jared Weitz, founder and CEO of United Capital Source. “When you originate and fund your own deals, you’re in a rewarding position and in control of how merchants get treated.”

Industry Trends

Speaking of the industry in general, these experts agreed that the business was undergoing a change with new entrants coming in and experimenting with better services and technologies.

“Last year was the year of brokers but we are still missing the education with merchants. Some brokers are interested while some are not,” said Abramov.

“I notice a clear difference between the old and the new in terms of technology and pricing model,” said Bakes.

“New funders are coming in with different products and terms with increased competition in the ISO market,” said Feinstein.

“Marketing is getting more expensive and only the ones who can afford to pay can play,” said Weitz.

Without Scalia, Media Outlets Reporting Marketplace Lenders Supposedly Doomed With Supreme Court Case (They’re Wrong)

February 18, 2016 Without Antonin Scalia, marketplace lending is apparently doomed, according to news outlets reporting on the matter. A high profile case (in the banking world anyway) known as Madden v Midland, is pending before the U.S. Supreme Court. Midland Funding seeks to reverse an appellate court ruling that said that interest rate preemption under the National Bank Act did not apply to them and thus they were subject to New York State’s usury laws.

Without Antonin Scalia, marketplace lending is apparently doomed, according to news outlets reporting on the matter. A high profile case (in the banking world anyway) known as Madden v Midland, is pending before the U.S. Supreme Court. Midland Funding seeks to reverse an appellate court ruling that said that interest rate preemption under the National Bank Act did not apply to them and thus they were subject to New York State’s usury laws.

According to BankRate.com’s reporting on the Scalia angle, “The U.S. Supreme Court has been asked to review a lower court decision that prevents marketplace lenders from getting around state usury laws by hooking up with banks headquartered in states that don’t have those rules.” But that’s not true at all. The case isn’t about marketplace lenders and the appellate court’s ruling isn’t currently preventing marketplace lenders from doing anything.

Midland Funding is a debt collector. Saliha Madden, a New York resident, obtained a bank issued credit card with an interest rate of 27% APR, racked up charges and didn’t pay them. The debt got written off and the bank sold the debt to Midland Funding. Midland continued to assess interest on the credit card debt while it attempted to collect. Saliha Madden sued on the basis that Midland was violating New York State usury laws. Midland Funding won and Madden appealed. Then a weird thing happened. The United States Court of Appeals for the Second Circuit held that in order “[t]o apply NBA preemption to an action taken by a non-national bank entity, application of state law to that action must significantly interfere with a national bank’s ability to exercise its power under the NBA.”

And from there began the somewhat justifiable panic in the marketplace lending industry. If a collector buying a charged-off debt from a bank can’t continue to enforce the terms as originally contracted, then could you make the same argument for loan platforms that buy newly issued loans? The answer is simply that you could make the argument. It’s not definitive. It’s one of those things that would likely have to be challenged in court by a borrower confident that a case involving a debt collector and a bank issued credit card somehow related to the matter between a marketplace lender and a borrower.

But there’s another problem in trying to make that link.

The Madden v Midland case involved a national bank and preemption under the National Bank Act. Many marketplace lenders such as Lending Club are not even conducting their business with national banks but with state-chartered banks. Their preemption ability falls under the Federal Deposit Insurance Act.

Lending Club did not shut their business down after the appellate court ruling and they didn’t stop lending in the states in which the Second Circuit has jurisdiction (New York, Connecticut and Vermont). Lending Club’s CEO Renaud Laplanche even expressed little worry about how it would impact their business when asked about it during their 2015 Q2 earnings call.

American Banker reported that “Scalia’s Death Is a Setback for Online Lenders in Key Court Fight.” But it’s really only a setback in the sense that a loss would peel away just one layer of the onion. Marketplace lenders weren’t going to suspend their operations regardless of whether or not the Supreme Court heard the case and regardless of whether or not Scalia was there to dissent.

Consider also that exporting home state interest rates using national and state chartered banks is only one system available to marketplace lenders. Square’s working capital program for example, is actually structured as a purchase of future receivables. There is no bank, no loan, and no preemption. An unfavorable Madden v Midland ruling would have no impact on that model or the dozens of merchant cash advance companies that offer similar products.

There’s also state by state licensing, which while costly and time consuming to set up, would at least allow marketplace lenders to lend in many states without relying on a bank or preemption. “I think the stronger business model is the state licensing model, as opposed to partnering up with a bank,” said Richard Eckman, a lawyer at Pepper Hamilton, to American Banker.

Even further distanced from this case are commercial marketplace lenders since state lending laws are generally less burdensome for business-to-business transactions.

And even if all else failed, a choice-of-law provision in a loan agreement can potentially decide which state’s law applies. Lending Club’s Laplanche said as much last year. “We continue to operate in the Second Circuit district where that decision was rendered, exactly as we did before and are relying on our choice of law provisions,” he said during an earnings call.

Scalia’s absence is at most a bummer for marketplace lenders. A win would only serve to tie up loose ends and finally put an end to bank charter model naysayers. Madden v Midland became so famous because the ruling was just so shocking. It practically begged the industry to take a look and wonder, what if? If this, then why not that? And if that, then who’s to say not this then? Even on AltFinanceDaily, we’ve explored the nightmare scenario in which a well established system totally unravels and the world ends. The real world holds much more promise.

The real losers in an unfavorable Supreme Court ruling would be national banks and credit card companies. And that’s because if debt collectors can’t enforce their loan agreements, then they’re not going to buy that debt to begin with. And if debt collectors won’t buy that debt, then banks are going to have to figure out a better way to collect on their own, else they make even less risky lending decisions.

Something tells me though that banks would find a creative work-around for that anyway. Because if they didn’t, Madden v Midland would end up being a massive boon for marketplace lenders.

Imagine that.

The Dual Aura of Fora – How Two College Friends Built Fora Financial and Became the “Marketplace” of Marketplace Lending

February 16, 2016A recent Bloomberg article documented the hard-partying lifestyle of two young entrepreneurs who struck it rich when they sold their alternative funding business. The story of their beer-soaked early retirement in a Puerto Rico tax haven came complete with photos of the duo astride horses on the beach and perched atop a circular bed.

But two other members of the alternative-finance community have chosen a different path despite somewhat similar circumstances. Jared Feldman and Dan B. Smith, the founders of New York-based Fora Financial, are about the same age as the pair in that Bloomberg article and they, too, recently sold an equity stake in their company. Yet Smith and Feldman have no intention of cutting back on the hours they dedicate to their business or the time they devote to their families.

They retained a share of Fora Financial that they characterized as “significant” and will remain at the head of the company after selling part of it to Palladium Equity Partners LLC in October for an undisclosed sum. Palladium bought into a company that has placed more than $400 million in funding through 14,000 deals with 8,500 small businesses. It expects revenue and staff size to grow by 25 percent to 35 percent this year.

The deal marks Palladium’s first foray into alternative finance, although it has invested in the specialty-finance industry since 2007, said Justin R. Green, a principal at the firm. His company is appointing two members to the Fora Financial board.

Palladium, which describes itself as a middle-market investment firm, decided to make the deal partly because it was impressed by Smith and Feldman, according to Green. “Jared and Dan have a passion for supporting small businesses and built the company from the ground up with that mission,” he said. “We place great importance on the company’s management team.”

Negotiations got underway after Raymond James & Associates, a St. Petersburg, Fla.-based investment banking advisor, approached Palladium on behalf of Fora Financial, Green said. RJ&A made the overture based on other Palladium investments, he said.

The potential partnership looked good from the other point of view, too. “We wanted to make sure it was the right partner,” Feldman said of the process. “We wanted someone who shared the same vision and knew how to maximize growth and shareholder value over time and help us execute on our plans.”

It took about a year to work out the details of the deal Feldman said. “It was a grueling process, to say the least,” he admitted, “but we wanted to make sure we were capitalized for the future.”

It took about a year to work out the details of the deal Feldman said. “It was a grueling process, to say the least,” he admitted, “but we wanted to make sure we were capitalized for the future.”

The Palladium deal marked a milestone in the development of Fora Financial, a company with roots that date back to when Smith and Feldman met while studying business management at Indiana University.

After graduation, Feldman landed a job in alternative funding in New York at Merchant Cash & Capital (today named Bizfi), and he recruited Smith to join him there. “That was basically our first job out of college,” Feldman said.

It struck Smith as a great place to start. “It was the easiest way for me to get to New York out of college,” he said. “I saw a lot of opportunity there.”

The pair stayed with the company a year and a half before striking out on their own to start a funding company in April 2008. “We were young and ambitious,” Feldman said. “We thought it was the right time in our lives to take that chance.”

They had enough confidence in the future of alternative funding that they didn’t worry unduly about the rocky state of the economy at the time. Still, the timing proved scary.

Lehman Brothers crashed just as Smith and Feldman were opening the doors to their business, and all around them they saw competitors losing their credit facilities, Smith said. It taught them frugality and the importance of being well-capitalized instead of boot-strapped.

Their first office, a 150-square-foot space in Midtown Manhattan, could have used a few more windows, but there was no shortage of heavy metal doors crisscrossed with ominous-looking interlocking steel bars. The space seemed cramped and sparse at the same time, with hand-me-down furniture, outdated landline phones and a dearth of computers. Job seekers wondered if they were applying to a real company.

“It was Dan and I sitting in a small room, pounding the phones,” Feldman recalled. “That’s how we started the business.”

At first, Smith and Feldman paid the rent and kept the lights on with their own money. Nearly every penny they earned went right back into the business, Feldman said. The company functioned as a brokerage, placing deals with other funders. From the beginning, they concentrated on building relationships in the industry, Smith said. “Those were the hands that fed us,” he noted.

By early 2009, Smith and Feldman started raising capital from friends and family members so that they could fund deals themselves. About that time, they developed a computer platform to track the payments they received from funding companies where they placed deals.

Smith and Feldman’s first credit facility came from Entrepreneur Growth Capital. The stake enabled them to begin handling deals on their own instead of passing them along to funders. At the same time, they expanded their computing platform to handle entire deals.

From there, Smith and Feldman expanded their computing capability to help with accounting, underwriting and other functions. A combination of staff and outside developers guided the platform’s evolution. Today, three full-time in-house tech people handle programming.

Smith and Feldman emphasize that they don’t consider Fora Financial a tech company, but Green said the company’s platform helped cinch the deal. “We view Fora Financial as a technology-enabled financial services company,” he maintained.

While building the platform and expanding the business, Fora Financial secured mezzanine financing from Hamilton Investment Partners LLC, a company that bases its investments on the strength of management teams. “I am industry-agnostic,” said Douglas Hamilton, managing partner and and cofounder. “Dan and Jared are one of the best young teams I have encountered in my 35 years of doing private investing.”

Meanwhile, Fora Financial moved six times to larger accommodations. The company’s 116 employees now occupy 26,000 square feet in Midtown, with half of the staff working in direct sales and the other half devoted to back office, underwriting, finance, IT, customer service, collections and legal duties.

Meanwhile, Fora Financial moved six times to larger accommodations. The company’s 116 employees now occupy 26,000 square feet in Midtown, with half of the staff working in direct sales and the other half devoted to back office, underwriting, finance, IT, customer service, collections and legal duties.

Seventy percent of the company’s business flows from its inside sales staff and the rest comes from ISOs, brokers and strategic partners, Feldman said. “Most of the industry is the opposite,” he noted.

Finding salespeople presents a challenge in New York, where they’re in great demand. “We’ve invested a lot of money in finding the right salespeople,” Feldman said. “We also have to make sure that we’re right for them.” The sales staff includes recent graduates and experienced people from other sectors of financial-services or other businesses, Feldman noted.

“We don’t hire from within the industry,” Smith added. “From Day One, we’ve been training our staff our way and not bringing in tainted brokers.” That way, the company can make sure salespeople hew to the company’s ethical approach to business, he maintained. It’s part of creating a company culture, he said.

The Fora Financial culture also includes strict compliance with state and federal regulation because until recently Smith and Feldman owned the entire company, Feldman said. “Regulatory compliance is a core value with us and has been for some time,” he noted, adding that it’s also resulted in conservatism and due diligence.

Those traits have not gone unnoticed, according to Robert Cook, a partner at Hudson Cook, LLC, a Hanover, Md.-based financial-services law firm that has worked extensively with the company. “Fora was one of the first clients in this small-business funding area that took compliance to heart,” Cook said. “As time has gone on, we’re seeing more and more companies make compliance part of their culture, but Fora was one of the early adapters in this area.”

Those traits have not gone unnoticed, according to Robert Cook, a partner at Hudson Cook, LLC, a Hanover, Md.-based financial-services law firm that has worked extensively with the company. “Fora was one of the first clients in this small-business funding area that took compliance to heart,” Cook said. “As time has gone on, we’re seeing more and more companies make compliance part of their culture, but Fora was one of the early adapters in this area.”

Top management at alternative finance companies often talk about compliance, and the discussion too often ends there and doesn’t filter down through the ranks, Cook said. But that’s not the case at Fora Financial, he maintained. “It’s throughout the organization,” he said of the company Smith and Feldman founded. “From a compliance attorney’s standpoint, that’s always a great sign.”

Nurturing a penchant for compliance and dedicating a company legal and compliance department to pursuing it became a factor in Palladium’s decision to become involved with the company, Feldman said.

The focus on compliance also spread to the way Fora Financial brings brokers on board, Smith said. The company scrutinizes potential partners carefully before taking them on, he maintained.

“We probably missed out on some business as the industry grew because we were more cognizant of doing things the right way, but that paid off in the long run and some of our competitors have followed suit,” Smith said.

Compliance first became particularly important when Fora Financial added small-business loans to their initial business of providing merchant cash advances. They began making loans because lots of businesses don’t accept cards, which serve as the basis for cash advances.

On a cash basis, the current portfolio is 75 percent to 80 percent small-business loans. Loans started to surpass advances during the fourth quarter of 2014. The shift gained momentum after the company began funding through its bank sponsor, Bank of Lake Mills, in the third quarter of 2014.

Growth of loans will continue to outstrip growth of cash advances because manufacturers, construction companies and other businesses usually don’t accept cards, Smith said. If a customer qualifies for both, Fora Financial helps decide which makes the most sense in a specific case, Feldman added.

“We don’t sell our loans – we carry everything on the balance sheet and assume the risk,” Feldman said. “If it’s not good for the customer, it’s going to come back and hurt the performance of our portfolio over time,” he noted.

That thinking helped the company recognize the importance of adding loans to the mix. “We were one of the first companies (in the alternative-finance industry) to get our California lending license,” Feldman said. The company obtained the license in 2011 and got to work on lending. Offering loans required some retooling because the underwriting criteria differ so much from those in the cash advance business, Feldman said.

With the help of several law firms, they made sense of regulation from state to state and began offering the loans one state at a time, Smith said. “We wanted to make sure we rolled it out the right way,” Feldman noted.

As the company was changing, Smith and Feldman saw a need to rebrand. Initially, they called their company Paramount Merchant Funding to reflect their merchant cash advance offerings. When they added small-business loans to the mix, they used several additional names. Now, they’ve brought both functions and all of the names together under the Fora Financial brand. Fora means marketplace in Latin and seems broad enough to cover products the company might add in the future, Feldman said.

Smith and Feldman are contemplating what form those future products might take, but they declined to mention specifics. “We’re constantly getting feedback from customers on what they need that we’re not currently delivering,” Feldman said. “We have ideas in the pipeline.”

Despite changes in the business, Smith and Feldman have managed to remain true to timeless values in their personal lives. Smith grew up near Philadelphia in Fort Washington, Pa., and Feldman is a native of Roslyn, N.Y. Both now reside in Livingston, N.J. and occasionally ride the train together to work in New York. Smith is married and has two children, while Feldman and his wife recently had their first child.

“We’re at it everyday,” Feldman said of their work-oriented lifestyle. “When we’re out of the office, we’re traveling for work. So is the rest of the team. We’re only going to go as far as our people.”

And what about that other pair luxuriating in the Caribbean? As Feldman put it: “New Jersey is a long way from Puerto Rico.”

—

Learn more about Fora Financial at www.forafinancial.com