The Unsung Disruption in Online Lending – Stacking, Litigation and Questionable Debt Negotiators

June 22, 2016

Give a small business two options, a low APR 3-year business loan and a short term loan with a high factor rate, and you’ll find advocates for each product arguing over which is better and why. We’ve been led to believe that it’s one versus the other, that one is good and one is bad, and that’s all there is to the story. Entire business models have been developed along the lines of this thinking, algorithms deployed and merchants funded, along with narratives framed in the mainstream media about why one system is superior to others.

But to hear the men and women in the phone rooms tell it, when given a choice between one funding option or the other, small businesses are often choosing both at the same time. Reuters said that stacking is the latest threat to online lenders, and in many ways they’re right. The practice isn’t new of course, the tendency for merchants to take on multiple layers of capital (often times in breach of other contracts) has been a central cause of tension between funding companies for the last few years. But the reason the story is bubbling over into traditional news media now as the latest threat, is because opponents of stacking assumed that the practice would be eradicated by now. There was this false sense of hope that government agents in black suits would show up one day unannounced after hearing that a merchant had taken a third advance or loan despite having not yet satisfied the obligations of the previous two. And when that didn’t happen, some of the models heralded as better for the merchant started to show cracks. What happens to the forecasts when the merchants priced ever so perfectly for a low rate long term loan go and take three or four short term loans almost immediately after? Back in October, Capify CEO David Goldin argued that long dated receivables were already dangerous to a lender regardless because the economy could turn south. “You’re done. You’re dead. You can’t save those boats. They are too far out to sea,” he told AltFinanceDaily.

Sue everyone?

When it comes to disruption, nothing has changed the game as much as stacking, and companies must prepare for the likelihood that it could be around forever. That means forming a long-term business model that is equipped to deal with this practice. Several lawsuits have been waged in an attempt to generate case law to deter it, including one filed last year in Delaware by RapidAdvance against a rival. Patrick Siegfried, assistant general counsel of RapidAdvance told the Wall Street Journal last fall, “we’re doing it to establish the precedent,” he said. “This kind of thing is happening more and more.” At the time, a motion to dismiss the case entirely was pending. RapidAdvance since won that motion but only by a hair and with a judge that was very reluctant to move the case forward.

Last October, MyBusinessLoan.com, LLC, also known as Dealstruck, sued five companies at once, a mix of lenders and merchant cash advance companies after one of their borrowers defaulted, allegedly because of actions carried out by the co-defendants. They were greeted with several motions to dismiss for failure to state a claim.

Even if these funding companies don’t win, simply letting the world know that they’ll sue rivals for stacking can act as a deterrent. But it’s an expensive tactic, especially when some defendants are more than happy to litigate the claims. Litigation is definitely an underrated cost of doing business for online lenders and merchant cash advance companies. In one recent case, a merchant challenged the legitimacy of a contract with Platinum Rapid Funding Group, a company whom they sold a portion of their future receivables to. The merchant asked the judge to recharacterize the contract to a loan so that they could try to use a criminal usury defense. The judge refused in a well-written decision that called the merchant’s attempt to do that “unwarranted speculation.” But even with the precedent of a favorable ruling, countless merchants have attempted to come up with strategies to wriggle their way out of their agreements, sometimes with ample legal counsel at their side.

Debt negotiators and questionable characters

Stacking has become a cost of doing business, but something else is creeping in as well. An entire cottage industry of “debt negotiators” has set their sights on online lenders and merchant cash advance companies, and at times these self-professed business experts don’t even realize there’s a difference between the two. One MCA funder told altfinancedaily earlier this week that a merchant in default claimed to be represented by Second Wind Consultants, a debt restructuring firm that lists one Don Todrin as the CEO on their website. Not mentioned among Todrin’s accolades is that he is a disbarred attorney who pled guilty to federal bank fraud charges in 1994, according to an old report by the Boston Globe, after he filed at least nine false financial statements to acquire $1.4 million in loans.

Another purported debt negotiation firm, who has the irked the ire of merchant cash advance companies, is apparently trying to assert affiliation to a native American tribe and invoke tribal immunity in response to lawsuits against them, according to court filings in New York State.

And only three weeks ago, an attempted class action against a merchant cash advance company failed because each named class representative had waived its right to participate in a class action in exchange for business financing. The initial action, before being moved to federal court, was brought by a merchant represented by an attorney who had just been reinstated to practice law, following a long suspension for pleading guilty to identity theft.

On top of it all, there are merchants themselves that act in bad faith, with some preying on the perceived vulnerabilities of an online-only experience. In the November/December 2015 issue of AltFinanceDaily Magazine, attorney Jamie Polon said some applicants don’t even own businesses at all, they just pretend to. “They’re not just fudging numbers – they’re fudging contact information,” he told AltFinanceDaily. “It’s a pure bait and switch. There wasn’t even a company. It’s a scheme and it’s stealing money.”

Weeding out bad merchants is a job for the underwriting department but for the good merchants seemingly deserving of those 3-5 year loan programs, the future is not as easy to predict as it once was. They might stack regardless, no matter how favorable the terms are. And given that government agent ninjas aren’t likely to drop down from the sky to stop them any time soon, many funding companies are faced with hard choices. Are the initial forecasts still valid? Is it economically feasible to turn the client away for additional funds because they breached their original agreement, all while the cost to acquire that customer in the first place was really high? Do you sue your rivals, make them look bad in the press, or lobby for regulations that will hurt them? How do you handle the new breed of debt negotiators who use the same UCC lead lists as lenders and brokers?

Sure, things like marketing costs are going up and the capital markets are less inviting than they used to be. But once loans and deals are funded, making sure those agreements are lived up to can take time, resources, and undoubtedly a lot of lawyers. And realistically, these issues aren’t likely to change any time soon. Help, in whatever relief form some are hoping for, is not on the way. How’s that for disruption?

BRIEF: OnDeck Expands in Denver, Invests $5 million in Office Space

June 16, 2016

OnDeck is expanding its Denver hub.

The online lender inaugurated a new office space worth $5 million, that can accommodate 550 people as it plans to add more to its existing staff there of 170. This is OnDeck’s second biggest hub after New York where it employs 300 people.

The state of Colorado and the Denver Office of Economic Development each gave the company $500,000 in 2012. And in August 2015, OnDeck won an additional $10.4 million in job growth incentive tax credits for creating an additional 400 jobs.

“Our goal is to steadily grow the office and invest more in Denver,” said Noah Breslow, the company’s CEO was quoted as saying in the Denver Post. “Denver is a natural fit for OnDeck.”

States like Colorado and New Jersey are wooing new fintech companies to build and expand their bases in the region. Thanks to the Grow New Jersey Assistance Program, merchant cash advance companies including World Business Lenders and Yellowstone Capital relocated from New York City over across the Hudson to Jersey City in exchange for tax credits. Yellowstone, for instance will earn $3.3 million over ten years in tax credits.

BRIEF: Legend Funding Secures $3 million Debt Facility

June 14, 2016New York City-based merchant cash advance company Legend Funding secured a $3 million debt facility from Houston-based investment investment banking firm Ango Worldwide.

Legend provides working capital financing to businesses in the USA and Canada and the company plans to use the funds for expansion. The deal gets Ango some equity and a seat on the board.

“The merchant cash advance industry is experiencing exciting growth and we felt that the legend management team are strongly positioned to take advance of this opportunity,” said Ango CEO John Carson in a news release.

Industry Goes Par for the Course

June 13, 2016Two companies in the industry are sponsoring golfers in this year’s U.S. Open, Mike Van Sickle via Expansion Capital Group (ECG) and Billy Horschel via Lenders Marketing.

Back in February, ECG SVP Steve Beveridge said, “we are excited to announce our partnership with Mike as a member of the ECG team. His motivation, drive, and dedication represent the same core values that ECG admires in our business clients who are pursuing their own individual dreams.” (Below: Van Sickle in an Expansion Capital Group shirt)

Van Sickle is ranked 1,297th in the world.

Horschel by contrast is ranked 55th in the world. Lenders Marketing, a lead generation company, also sponsored Michael McCabe last year during the PGA Tour Barracuda Championship in Reno, Nevada. (Below: McCabe in the green hat and Justin Benton of Lenders Marketing behind him to the left with the glasses over a white hat)

Transparent Pricing Creates a Level Playing Field, says Kabbage’s Kathryn Petralia

June 7, 2016 Loan matchmaking site Lending Tree has joined the Innovative Lending Platform Association (ILPA) to participate in developing a universal small business lending disclosure system to raise transparency with lenders. It will work closely with the association over a 90-day “national engagement period” to create and implement the SMART Box (Straightforward Metrics Around Rate and Total Cost).

Loan matchmaking site Lending Tree has joined the Innovative Lending Platform Association (ILPA) to participate in developing a universal small business lending disclosure system to raise transparency with lenders. It will work closely with the association over a 90-day “national engagement period” to create and implement the SMART Box (Straightforward Metrics Around Rate and Total Cost).

AltFinanceDaily spoke to Kathryn Petralia, cofounder of Kabbage Loans, which is spearheading the association with OnDeck and CAN Capital. Below are the edited excerpts from the interview:

Tell us about how the ILPA came about?

We (OnDeck, CAN Capital and Kabbage) represent the largest non bank lenders. We have collectively lent $12 billion through the course of our businesses and so we thought it will be great for us to make a statement through ILPA. We came from a perspective that there are a lot of different products for small businesses on the market like merchant cash advance, equipment financing, invoice factoring and lines of credit. All of these serve different needs and are ambiguously priced. So we wanted to find some methodology which is transparent to borrowers so they can know the exact price and total cost of borrowing.

We want to keep it open and hope that everyone participates in the disclosure methodology so borrowers can have a clear understanding of the fees they are paying.

What is SMART Box. How does it work?

Different loan products have different fees — some have maintenance fees, some have broker fees, usage fees and so on and they are all structured very differently. It can get very confusing and so we came up with all the products to understand what disclosures would be necessary to know the total cost of borrowing. We’re working with OnDeck and CAN Capital to gather comments and disclose a series of methodologies that will create the ‘Straightforward Metrics Around Rate’ and Total Cost or SMART Box. Those who want to participate will have to disclose it on loan agreements to their customers.

What about disclosures by companies? Would you say the industry needs more regulation on that front?

Kabbage and other companies in the industry are all regulated and go through FDIC audits. We all follow KYC, CIP, FFIEC guidelines that refer to lenders. We all follow these regulations and I would argue vociferously that we are regulated businesses already. All companies are very different and there are a bunch of things happening — states like California, Illinois and New York and CFPB are all taking interest in small business lending and it’s a positive that they recognize the partnership between banks and tech companies. On the general lending side, we have Dodd-Frank and Madden vs Midland which look at lending issues. Some of the regulation is around how loans are sold and some of it is around how they are limited. And on the small business lending side, there is push for more transparency which is the reason we launched ILPA. We wanted to set the standard for what that would look like. And having it done comprehensively is beneficial for us as it gives us a level playing field.

On the consumer lending side, there is transparency but it’s still lacking a comprehensive system that encapsulates the total cost of borrowing. APR is a great metric but the total cost of borrowing must be included.

Give us a snapshot of what the industry looks like to you

All businesses serve different markets, are different in the way they fund their loans and operate in different geographies, so it’s hard to say but in general those who have done a good job at incorporating data and tech and streamlined operative process will have an advantage and will make it through economic turbulence.

What’s your short-term prediction?

Companies that are not well capitalized will have a tough time raising capital in 2016 and we have already been approached by a number of businesses that are looking to sell or find a partnership because they aren’t well capitalized.

Tell us what’s happening at Kabbage?

We have two businesses – the direct lending business which we are trying to grow and the second is the platform business where we have seen sustained growth, with existing partnerships with ING in Europe, Santander in the UK and Scotia Bank in Canada. More partnerships are in the offing – both domestically and in Latin America.

New Funder Doing 12-Month Deals With Weekly Payments (Guess Who)

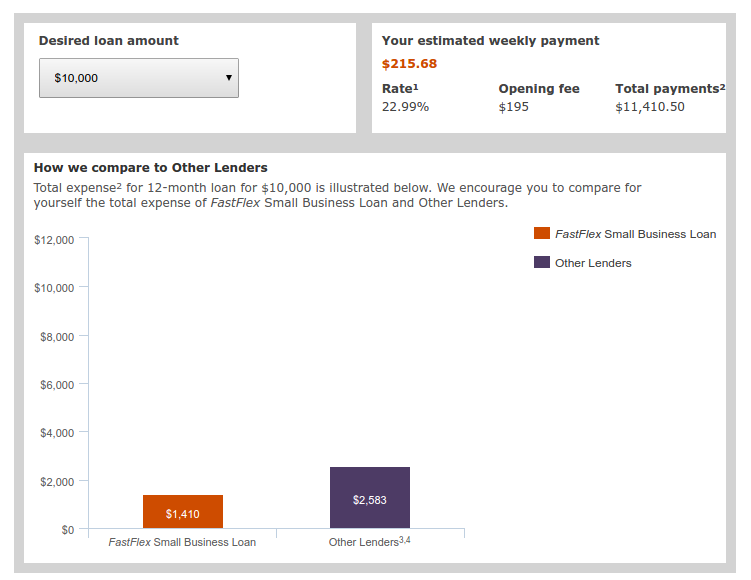

June 3, 2016 Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

The name of the funder? Wells Fargo Bank.

The caveat is that applicants must have banked with Wells Fargo for at least 1 year to be eligible. The upside is that little documentation is required to apply outside of the application. The loan is unsecured and the closing fee is only $195. Dubbed FastFlex, the product is clearly meant to compete against online business lenders because well, they mention CAN Capital, OnDeck, and Kabbage in the footnotes on their loan calculator page.

Using their loan calculator, Wells Fargo estimated a 10k loan on a 1.14 over twelve months with weekly ACH payments.

Wells Fargo’s marketing message sounds awfully familiar:

Next day funding, not just your credit score, weekly payments…

Wells Fargo is not alone in their attempts to attack online lenders. Discover Bank for example, is targeting Lending Club directly. By going after the same borrower profile and offering better terms, Discover hopes to cut into Lending Club’s newfound market share.

Unsurprisingly, it is the non-bank prime lenders that will feel the growing bank threat the most. Companies offering small business loans or merchant cash advances to small businesses with damaged credit or complex situations are unlikely to find their target customer pool become bankable any time soon.

It’s Time to End the Phrase ‘Marketplace Lending’ – Because it’s Insane

May 19, 2016

Nobody knows what “marketplace lending” means, including me. That’s kind of ironic considering AltFinanceDaily is for the most part a publication dedicated to it. In fact, the cover of the March/April issue featured a big yellow robot sporting a name tag that actually said, “Hello, my name is Marketplace Lending.” Even the letter I penned that introduced readers to the issue used the phrase not once, not twice, but FIVE TIMES.

The FDIC basically defined it as encompassing all types of financing that include the practice of pairing borrowers over an online platform. Eager to be hip to the industry’s newest lingo, I got on board, and unfortunately perpetuated something that makes almost no sense.

Many companies operating under the marketplace lending umbrella don’t even know that they’ve been lumped into it. It’s become a media buzzword, something to help the simple masses understand so that they will click on a news headline without worrying if the content will only be geared toward the financially savvy.

Imagine shopping for a loan at a supermarket, but ONLINE, and voilà, marketplace lending!

But there are virtually no online platforms that work like that. The simplest explanation to describe a dizzyingly diverse industry is the most incorrect one. Lenders set rates and terms, borrowers don’t choose exactly what they want from a virtual shelf and put them in an imaginary shopping cart. There are however, portals where prospective borrowers can review different offers from different lenders in an Expedia-like environment, but this is really just Online Lead Aggregation 2.0, not a new-age system of lending.

Of course, some adopters of the phrase will point out that the marketplace was supposed to refer to the investor side, not the borrower side. It is investors that can shop for loans or notes that they want to invest in. Indeed, on platforms like Lending Club and Prosper, investors can select individual notes with terms befitting their desires and place them in an online shopping cart for purchase. Behold, the marketplace!

But what if you didn’t deal with retail investors hand-selecting $25 notes at a time? Notably, some online platforms that sell their loans to institutions in giant pools by the thousands or millions believe that such activity constitutes a marketplace because somebody is buying what they’re selling. And so long as somebody is selling something to somebody else at some point, the whole thing might as well be a marketplace. And even if it’s not, referring to it as such anyway will garner more press, attract more investors, and boost valuations.

I mean, would a site like TechCrunch be more likely to write about a FinTech Marketplace Lender or a generic financial company that sold a batch of loans to a bank?

I can tell you firsthand that if a press release submitted to us used the term “marketplace lender” instead of “finance company,” we’d at least check it out, or at least we used to. These days, we are becoming numb to its overuse.

Peer-to-Peer lending was an awesome term and it was descriptive too. Everybody could understand it. But then those platforms had to go and start selling their loans to Wall Street instead of peers and come up with something else to still sound trendy, techie, and disruptive. There’s nothing trendy of course about selling loans to financial institutions. It is a quintessential boring business activity of Wall Street. It is the opposite of disruptive, except in the events where all the loans go bad and the entire economy collapses like in 2008.

Peer-to-Peer lending was an awesome term and it was descriptive too. Everybody could understand it. But then those platforms had to go and start selling their loans to Wall Street instead of peers and come up with something else to still sound trendy, techie, and disruptive. There’s nothing trendy of course about selling loans to financial institutions. It is a quintessential boring business activity of Wall Street. It is the opposite of disruptive, except in the events where all the loans go bad and the entire economy collapses like in 2008.

The FDIC specifically said that marketplace lending can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, real estate loans, merchant cash advance, medical patient financing, and small business loans. This wildly diverse list, which even includes a non-loan product, will obviously have platforms in every category where people or businesses can get paired with a source of funds via the Internet. It’s 2016. It’d be weird if you couldn’t search for financing online. You can do everything else on the Internet. Just because a search happens online shouldn’t mean that the resulting options should be thrown together in some special broad category of lending and then be judged according to what all the other sectors do.

None of this is said to diminish the technological feats that many platforms have achieved. People and businesses can access capital in much faster and more convenient ways than ever before. Their growth and success is America’s economic gain. Jobs have been created and borrowing costs reduced. Hooray, perhaps, for marketplace lending.

The problem is merely the characterization that anyone lending to anyone else these days must also be a marketplace. That makes no sense.

Who will be the first to stop the madness?

Defrauding Fintech Lenders Leads to Conviction

May 8, 2016 It’s not just collection firms and attorney demand letters that deceptive borrowers need to be wary of. In the Western District of Tennessee, Preston E. Byrd was convicted on six counts after defrauding RapidAdvance and Windset Capital out of more than $100,000 collectively.

It’s not just collection firms and attorney demand letters that deceptive borrowers need to be wary of. In the Western District of Tennessee, Preston E. Byrd was convicted on six counts after defrauding RapidAdvance and Windset Capital out of more than $100,000 collectively.

According to the original indictment filed in August of last year, “Byrd did knowingly devise and intend to devise a scheme and artifice to defraud Windset Capital and RapidAdvance by means of false and fraudulent pretenses, representations and promises.” As part of that, Byrd submitted fake bank statements, a fake lease agreement and other misleading documents. He faked his own name, calling himself Jason Hester, and pretended to be the landlord of the property in question, confirming falsely to underwriters that a lease existed and was in good standing.

In reality, he had no business location.

Once Byrd received the funds from each company, he wired portions of the ill-gotten proceeds to other accounts.

The jury convicted him on three counts of wire fraud and three counts of engaging in monetary transactions in criminally derived property. The trial concluded on March 24th of this year and Byrd is expected to be sentenced on June 16th.

The case is unique because the sole victims were fintech lenders and the criminal charges were brought by United States Attorney Edward L. Stanton III.

On his twitter account, Byrd describes himself as a “multifamily housing developer, entrepreneur, business consultant, public speaker, mentor, yogi, and (some might say) a cool dude.” Not mentioned there however is that Byrd was previously convicted of wire fraud in 2003 and that he also lost a lawsuit brought by Arvest Bank for fraud.

The criminal case # concerning Byrd with Rapid and Windset is 2:15-cr-20025-JPM