Law Firm Sued for Tortious Interference With Loans and MCAs

January 31, 2018Rhode Island Superior Court has a tortious interference case on its hands. Small Business Term Loans, Inc., and BFS West, Inc. v Christopher M. Mulhearn, and Law Office of Christopher M. Mulhearn, Inc. is yet another front in the debt settlement war enveloping the alternative finance industry.

Here, the plaintiffs (known to many as BFS Capital), allege that Mulhearn and his law office attempt to persuade BFS Capital’s customers to breach their obligations to BFS Capital while routinely making misleading representations to their customers, including by promising to save them money by settling their obligations to BFS Capital for a discounted amount when they have no legitimate basis for being able to make such promises.

At least seven customers are alleged to have breached their agreements as a result of the defendants’ actions.

The defendants have not yet responded to the complaint. The suit is registered in Providence/Bristol County Superior Court of Rhode Island under case # PC-2018-0094.

Other such companies that have found themselves on the receiving end of a tortious interference lawsuit include MCA Helpline, Protection Legal Group, and Creditors Relief.

Originations Since Inception

December 8, 2017After several company announcements recently, we’ve compiled a milestone chart to plot where they rank. Originations may indicate business loans or MCAs funded on balance sheet, brokered, or placed through a marketplace. These rankings are a work in progress. This chart may not include companies for which public data is not available. If you’d like your figures to be listed here, e-mail sean@debanked.com.

| Company | Origination Volume Since Inception | Year Founded |

| OnDeck | $8 Billion | 2007 |

| Kabbage | $4 Billion | 2009 |

| Yellowstone Capital | $2 Billion | 2009 |

| BFS Capital | $1.7 Billion | 2002 |

| Funding Circle | $1 Billion (US only) | 2010 |

| IOU Financial | $500 Million | |

| Lending Club | $500 Million (SMB loans only) | 2006 |

| SmartBiz Loans | > $500 Million (SBA loans) | 2009 |

| Lendio | > $500 Milllion | |

| Forward Financing | $275 Million | 2012 |

| Blue Bridge Financial | $200 Million | 2009 |

Stacking Lawsuit Could Go to Trial

October 18, 2017 A lawsuit between RapidAdvance and Pearl Capital that has been making its way through the Maryland state court system for two years may be heading to trial.

A lawsuit between RapidAdvance and Pearl Capital that has been making its way through the Maryland state court system for two years may be heading to trial.

In this case, plaintiff Small Business Financial Solutions, LLC (SBFS AKA RapidAdvance) alleged that Pearl Beta Funding, LLC (AKA Pearl Capital) interfered with a loan agreement it had with a merchant when Pearl “stacked” financial obligations to Pearl on top of the obligations the customer owed to SBFS. Ultimately the merchant defaulted and SBFS wants to hold Pearl responsible for the damages it incurred.

Pearl originally moved to dismiss the suit but was unsuccessful. Later, Pearl filed a motion for summary judgment. On September 29th, that motion was denied, with the judge opining that issues of fact remained that were best left for a jury.

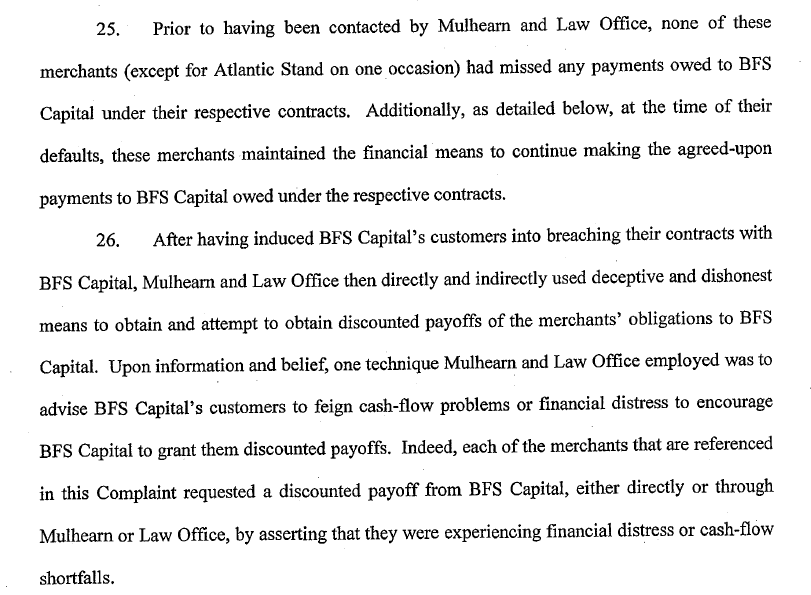

Unless Pearl appeals the decision or the parties settle, the case will go to a jury.

A representative for Pearl Capital declined to comment on the decision, citing ongoing litigation.

Patrick Siegfried, Assistant General Counsel for RapidAdvance, opted to tell AltFinanceDaily the following:

“The court’s decision from many months ago to reject Pearl’s motion to dismiss and its more recent decision to reject the motion for summary judgment and permit this case to go to trial confirms the anti-stacking position RapidAdvance has consistently taken. The court’s rulings make it clear that when a funding company funds a merchant knowing that doing so is a breach of the customer’s agreement with another funder and the stacker’s funding is a substantial cause of the merchant defaulting with the other funder, its actions constitute tortious interference. As a result, the company that stacked can be held liable for the losses the original funder incurs. While the outcome at trial is impossible to predict as the court will need [to] decide whether there are sufficient facts to satisfy each element, RapidAdvance is pleased that its legal reasoning on stacking has been confirmed in a written opinion and that we now have the roadmap for pursuing others that tortiously interfere with our contracts by stacking.”

Of note, is that RapidAdvance brought this case in The Circuit Court for Montgomery County, Maryland. Few other players in the industry may be able to designate Maryland as the proper venue. The standards for tortious interference may not be the same in other states. There are many circumstances in the case not discussed in this synopsis. Consult an attorney before drawing any conclusions. YOU CAN DOWNLOAD THE FULL DECISION HERE.

The case is Small Business Financial Solutions, LLC v. Pearl Beta Funding, LLC Case No. 411478-V in the Circuit Court for Montgomery County, Maryland.

Insurtech, the Alt Lending of 2017

October 17, 2017 A new asset class is emerging and it’s taking top talent away from the alternative lending space. Insurance technology, or insurtech, is a nascent market segment that presents a similar market opportunity that fintech did back in the day, sources say. And while there are parallels between the two niches, the market landscapes are unique in many ways, too.

A new asset class is emerging and it’s taking top talent away from the alternative lending space. Insurance technology, or insurtech, is a nascent market segment that presents a similar market opportunity that fintech did back in the day, sources say. And while there are parallels between the two niches, the market landscapes are unique in many ways, too.

Former OnDeck exec Paul Rosen recently decamped to insurtech startup CoverWallet where he’s been named COO. CoverWallet is an online marketplace for small- and medium-sized business insurance policies. Rosen left the alt lending space at a pivotal time for the industry and his former employer, both of which have experienced realignments to their approach in 2017.

So why would Rosen, the former chief sales officer at OnDeck, depart a proven market opportunity in alt lending for newer waters in a less mature segment in the insurance industry? In short, he’s not the only one.

Earlier this year, James Hobson, former COO of OnDeck, left to take the helm at insurance startup Attune. According to LinkedIn, OnDeck’s former SVP of operations Martha Dreiling made the same jump, joining Attune as head of analytics and corporate operations. Josh Wishnick, another OnDeck alum, is now spearheading business development at PolicyGenius.

One might question whether the trend is specific to OnDeck, given that the newly minted insurtech execs are originating from that company. The interest in insurtech, however, extends beyond the C-Suite and into the investor base, which is indicative of a broader trend unfolding.

OnDeck spokesperson Jim Larkin told AltFinanceDaily: “OnDeck was among the early pioneers of online lending going back to 2007. Since then, we have seen numerous other fintech initiatives take off. Insurtech is the latest. Several former OnDeck employees are providing their expertise to this new space and I’m confident they will help their new organizations to thrive in the same manner OnDeck has over the last decade. Growing talent and seeing some of them graduate and contribute to the vitality of FinTech ventures across the world is one of the things that we are most proud of here at OnDeck.”

Meanwhile CoverWallet in recent days announced a Series B-$18.5 million cash raise led by Foundation, a new investor in the startup that similarly backed Lending Club and OnDeck. This trend speaks to the comfort level among both alt lending industry execs and institutional investors for the emerging insurtech market.

“So, it’s interesting. A lot of the people that helped to grow and shape the fintech industry have now moved on to this industry. Insurtech today feels a lot like fintech did in 2011,” Rosen told AltFinanceDaily.

Industry Landscape

Industry Landscape

Insurtech stands to disrupt the insurance industry much the same way that alternative lenders did in that arena. The nascent market opportunity is also unique, with nuances that set insurtech apart not only from alternative lending but from the broader insurance industry as well.

“SMB insurance is very different from personal insurance. You can go online with Geico and switch insurance providers in 15 minutes. SMB insurance isn’t built that way right now,” said Rosen.

For instance, most SMBs go to brick-and-mortar insurance agencies to get whatever policies they need. But the process to getting a loan is slow and paper-work driven. They might have to fill out a 42-page application to get a $600 business owner policy.

The differences are even more pronounced between insurtech and alt lending, especially when it comes to compliance. “With this business, there are heavier regulations than there are in SMB lending. All our sales people must be licensed. There’s a heavier compliance component to it,” said Rosen.

As of today, CoverWallet markets to its customers directly. “If you look at the fintech industry, we’re kind of like an ISO. At this point we’re a distribution company going directly after our customers,” said Rosen, adding that they have put brokers using their technology on the back burner for now.

CoverWallet does some of the underwriting themselves. “We’re where insurance and technology meet,” he said. If a SMB went to a typical brick and mortar broker, they might fill out a 42-page application with 80 questions. Considering that CoverWallet is online, the product is extremely simple and intuitive so the SMB owner doesn’t have to answer tons of questions. “You go through the process a lot quicker. And a lot of the underwriting is done on the sales end by our sales team,” said Rosen.

CoverWallet acts like a marketplace in that they will go through the carrier that best meets the need of the SMB. “It’s very similar to a broker. We’re out there doing online marketing. We don’t do a lot of direct mail. A customer comes in and we examine the customer and based off the industry, location and some other things we determine where the best fit for that customer is. We send them to the carrier that’s the best fit based off carrier appetite,” he said.

That Was Then, This Is Now

So, what is it about insurtech that has some top-tier talent in the alt lending space running for the exit? Rosen pointed to a trio of parallels between insurtech today and alternative lending then (back in 2011), which perhaps is what’s compelling alt lending veterans to make a career change.

When Rosen joined OnDeck in 2011, one of the things they discussed was a $100 billion market opportunity in unmet demand in the small- and medium-sized business lending market. Six years later and the industry is probably lending $10 billion to $15 billion now, which suggests there’s still a lot of headway in the alt lending space today.

Meanwhile, Rosen points out that of the $100 billion in small- and medium-sized business insurance premiums that are written today in the United States, “virtually none of them are done online.” And that, he says, is the No. 1 reason why insurtech feels a lot like fintech did in 2011.

“If insurtech can get to $15 billion to $20 billion in premiums, that will be a huge opportunity for the right companies. We think we have a shot at it,” Rosen said, adding that it’s not a zero-sum game.

Secondly, insurtech is highly fragmented similar to how the online lending industry was before. “There aren’t a lot of brokers or distributors with a significant amount of market power, especially in the SMB market. When we started OnDeck, there wasn’t any one company from a lending SMB perspective with a whole lot of market power,” recalled Rosen.

Lastly, Rosen points to industry disruption. “The way SMBs were purchasing loans in 2010 was very similar to how they were purchasing loans 20 years prior. There was not a whole lot of innovation or disruption. Then OnDeck, BizFi, Lending Club, BFS Capital and CAN Capital came on the scene and started disrupting the space. On the SMB side, there has been no technology disruption till this point. Now a handful of companies like CoverWallet are looking to change that,” said Rosen.

More Fallout?

Rosen has been fielding inquiries from others in the alt lending space. “There’s definitely interest in the insurtech space from fintech team members,” he said. Meanwhile, even though he has left, Rosen remains “bullish” both on the alt lending space and his former employer, OnDeck. I have kept most of my equity at OnDeck,” he said.

All Companies Can Now Submit Draft IPO Registrations Confidentially

June 29, 2017 There’s a reason the public never got to view BFS Capital’s September 2015 IPO registration documents. Thanks to the JOBS Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.” They can then choose to abandon the offering altogether without having to suffer the fate of their financial statements being made public, which is what BFS Capital did. But if they ultimately had chosen to move forward, their documents would’ve been shared in the public domain.

There’s a reason the public never got to view BFS Capital’s September 2015 IPO registration documents. Thanks to the JOBS Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.” They can then choose to abandon the offering altogether without having to suffer the fate of their financial statements being made public, which is what BFS Capital did. But if they ultimately had chosen to move forward, their documents would’ve been shared in the public domain.

A new decision handed down by the SEC is now expanding that privilege beyond “emerging growth companies” to all companies. That means that any company can submit draft documents confidentially. It will take effect on July 10th.

“This is an important step in our efforts to foster capital formation, provide investment opportunities, and protect investors,” said Director of the Division of Corporation Finance, Bill Hinman. “This process makes it easier for more companies to enter and participate in our public company disclosure-based system.”

The only reason BFS Capital’s confidential filing is known, is because the company broadcasted that they had filed accordingly in a press release.

“By expanding a popular JOBS Act benefit to all companies, we hope that the next American success story will look to our public markets when they need access to affordable capital,” said Chairman Jay Clayton. “We are striving for efficiency in our processes to encourage more companies to consider going public, which can result in more choices for investors, job creation, and a stronger U.S. economy.”

It is possible that other companies in the industry have filed draft registration statements, got discouraging feedback from the SEC and then decided to withdraw without any of their competitors being the wiser.

The Top Small Business Funders of 2016

March 6, 2017The MCA and small business lending origination numbers for 2016 are in. In some cases, a company may have merely placed or facilitated an acquired customer with a partner or competitor (but still counted them in their annual volume) and thus the figures do not necessarily represent what actually went on balance sheet. The rankings omit some larger players for which no data could be confirmed and when a reasonable estimate could not be made.

| Company Name | 2016 Origination Volume | 2015 | 2014 |

| OnDeck | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 |

| PayPal Working Capital | $1,500,000,000* | $900,000,000* | $250,000,000* |

| Kabbage | $1,250,000,000 | $1,000,000,000 | $400,000,000 |

| CAN Capital | $1,100,000,000* | $1,500,000,000* | $1,000,000,000* |

| Square Capital | $798,000,000 | $400,000,000 | $100,000,000 |

| Bizfi | $550,000,000 | $480,000,000 | $277,000,000 |

| Yellowstone Capital | $460,000,000 | $422,000,000 | $290,000,000 |

| Strategic Funding | $375,000,000 | $375,000,000 | $280,000,000 |

| National Funding | $350,000,000 | $293,000,000 | |

| BFS Capital | $300,000,000 | ||

| BlueVine | $200,000,000* | ||

| Platinum Rapid Funding Group | $180,000,000 | $100,000,000 | |

| IOU Financial | $107,600,000* | $146,400,000 | $100,000,000 |

*Asterisks signify that the figure is an estimate

IT’S A BROKER’S WORLD

August 31, 2016

From east to west, small businesses are getting funded. But how they’re found and who they work with depends on where they are. In the US, where brokers tend to have a love/hate relationship with the funding companies they work with, they are no doubt a driving force in the market. In other countries, they might not even exist, are just starting to bloom or they add balance to a mature market. Is the world built for brokers? AltFinanceDaily traveled far and wide to find the answers.

Down under in Australia where American-based merchant cash advance and lending companies have expanded, the ISO (which stands for Independent Sales Office and is synonymous with broker) model has not really followed. David Goldin, CEO of Capify, an international company headquartered in New York, told AltFinanceDaily that there’s very few ISOs in Australia.

He believes that’s because there’s next to no payment processing ISO market there, a foundation that was a major precursor in the US towards the development of ISOs reselling merchant cash advances and business loans.

He believes that’s because there’s next to no payment processing ISO market there, a foundation that was a major precursor in the US towards the development of ISOs reselling merchant cash advances and business loans.

Luke Schmille, President of CapRock Services, echoed same. The Dallas-based company founded Sprout Funding in Australia earlier this summer as part of a joint venture with Sydney-based family office Huntwick Holdings. “Direct marketing is the primary method [of acquiring deal flow],” he said. “The credit card processing space is controlled by several large banks, so you don’t see ISO efforts in the acquiring space either.”

Big bank dominance was only one reason why another country’s emerging alternative small business funding market developed slowly. In Hong Kong, non-bank alternatives like merchant cash advances faced legal uncertainty for a long time. For example, Global Merchant Funding (GMF), once the only merchant cash advance company in the Chinese special administrative region, had been relentlessly pursued for years by the Secretary for Justice for conducting business as a money lender without a license. GMF fought it. And won.

In May of this year, the legality of merchant cash advances ultimately prevailed after the highest court ruled the agreements were not loans. Emboldened, several companies have stepped up their marketing of the product. But whether they’re doing daily debit loans or split-processing merchant cash advances (both of which exist there), marketing tends to be directed at merchants, not a middle market of brokers.

Gabriel Chung of Hong Kong-based Advanced Express Capital said that there are a handful of large brokers typically comprised of former bankers, but the rest of the broker market is highly fragmented, mostly made up of individual freelancers.

Gabriel Chung of Hong Kong-based Advanced Express Capital said that there are a handful of large brokers typically comprised of former bankers, but the rest of the broker market is highly fragmented, mostly made up of individual freelancers.

Adrian Cook, the Founder and CEO of Hong Kong-based Asia Capital Advance, agreed that marketing is usually aimed at merchants directly but that it’s changing. “Since the market is still very new and MCA is only beginning to gain popularity, brokers on the market are only starting to recognize MCA,” he said. “There is a lot of room for the brokerage market to grow.”

In the UK, where Capify also operates, CEO David Goldin explained that the UK doesn’t have a lot of credit card processing ISOs so there wasn’t a major migration from that business to MCA like there was in the US. But that doesn’t mean there is no middleman market at all.

Paul Mildenstein, executive director of London-based Liberis, said that brokers are an important channel, but not as dominant as they are in the US. “Our brokers are usually members of the NACFB, an organisation in the UK that actively supports and provides operating principles to the furtherance of the commercial finance broker community,” he wrote. The National Association of Commercial Finance Brokers claims to have 1600 members, one among them is Liberis.

Paul Mildenstein, executive director of London-based Liberis, said that brokers are an important channel, but not as dominant as they are in the US. “Our brokers are usually members of the NACFB, an organisation in the UK that actively supports and provides operating principles to the furtherance of the commercial finance broker community,” he wrote. The National Association of Commercial Finance Brokers claims to have 1600 members, one among them is Liberis.

“Many clients want the support of an experienced professional who can discuss the financial options available to them in their specific circumstances,” said Liberis’ CEO, Rob Straathof. “Given relatively low awareness of the Business Cash Advance product in the UK, this means that brokers have a key role to play in educating potential customers on when this is the right option for them,” he added.

Straathof stressed a robust criteria for the brokers they work with and explained that brokers are their eyes and ears in the market. “The relationships we have with them are not transactional, but transformational for our business,” he said.

The NACFB was also praised by Alexander Littner, Managing Director of Chelmsford, Essex-based Boost Capital. The company, which is actually a subsidiary of Coral Springs, FL-based BFS Capital in the US, sees a balance between their use of brokers and their efforts to acquire customers directly.

“As the alternative finance market is still relatively new here in the UK these brokers are important for this independent advice, and to help educate the market and establish trust,” Littner said. “At Boost Capital we work very closely with brokers across the UK, they are a critical part of our growth and fundamental to our ongoing success.”

In the US, brokers play such a dominant role in customer acquisition that some MCA funding companies rely on them to source the entirety of their business. Back in February, Jordan Feinstein of NY-based Nulook Capital told AltFinanceDaily, “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require.” Nulook markets its broker-only approach as a strength.

Others take a more blended approach, like Justin Bakes, CEO of Forward Financing, for example. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said earlier this year.

Notably, no such guiding authority like the UK’s NACFB exists for brokers in the US so it’s not easy to track exactly how many there are or how they operate, but their role in the industry cannot be understated. AltFinanceDaily actually labeled 2015 The Year Of The Broker, when it published an article in its March/April 2015 issue that tried to capture the essence of the industry at the time. Tom McGovern, who was then a VP at Cypress Associates LLC, said of brokers, “They’re like the missionaries of the industry going out to untapped areas of the market.”

But preaching the gospel of alternative funding exists at different stages across the world. And Goldin, whose company Capify operates in four countries including the US, thinks that many middlemen here at home may not ultimately survive. In an interview, he predicted that the stronger ones over time will be acquired by funding companies and that direct marketing will only increase. “I think more and more companies are going to start building their own internal sales forces,” he said.

Other brokers are not convinced that acquisition costs will lead to the death of their businesses, especially if they’ve already found ways to reduce overhead costs. Several brokers have discreetly mentioned running operations from Costa Rica, Nicaragua or elsewhere as a way to keep things profitable. Still more, like Excel Capital Management based in Manhattan, have found that offering a suite of products allows them to monetize more customers. Chad Otar, a managing partner for Excel, said that they recently brokered a $4.9 million SBA loan. MCA is just one of their options these days. “As long as there’s small businesses, there’s always going to be opportunity,” he said.

In the US, the brokers have certainly seized it, but that’s because most funding companies offer big bucks and quick payment to those that are capable of sourcing customers. In other countries, compensation for services rendered might be the responsibility of the broker to arrange with the merchant since it may not be customary for funding providers to pay commissions. That would mean more work and more risk for the broker.

In the US, the brokers have certainly seized it, but that’s because most funding companies offer big bucks and quick payment to those that are capable of sourcing customers. In other countries, compensation for services rendered might be the responsibility of the broker to arrange with the merchant since it may not be customary for funding providers to pay commissions. That would mean more work and more risk for the broker.

Ironically, some brokers in the US will tap into both sides, earning a commission from the funder and charging a fee to the merchant for services rendered. And if the broker has payment processing roots, they can go a step further and earn merchant account residuals as well.

Brokers can’t exist without funding companies willing to support their endeavors, of course. While their prevalence around the world varies, most of the funding companies AltFinanceDaily spoke to, appear eager to nurture the middleman’s role, so long as they act responsibly.

“Brokers in the UK are incredibly important as independent advisors to small businesses on the various sources of finance to suit their needs,” said Littner.

And as long as those customers, wherever they may be, are getting the value they want from a broker, that role, so long as it can continue to be done profitably, will likely have a place in the world for the foreseeable future.

Industry Trade Group Coming of Age: The SBFA is Becoming More Political

February 1, 2016By hiring an executive director, the Small Business Finance Association hopes to achieve at least two goals – taking a step toward becoming a full-service trade group and providing a public voice for the alternative finance industry.

Stephen Denis, formerly deputy staff director of the U.S. House Committee on Small Business, went to work in the new role in mid-December, setting up shop with his cell phone and laptop in a Washington, DC, area coffee emporium. He’s the SBFA’s first full-time employee.

Hiring Denis, who also has association experience, represents “the next evolution” of the trade group, according to David Goldin, SBFA president and Capify’s founder, president and CEO.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

“The goal is to start from scratch and take a look at everything the association is doing,” Denis told AltFinanceDaily, “and to really build this out to a robust group that represents the interests of small businesses.”

Denis appears optimistic about pursuing that goal. He’s a native of the Boston area and a Harvard University graduate whose first job out of school was as an aide to Republican Sen. John E. Sununu of New Hampshire. After three years in that position, he took a job for two years with a UK-based trade association, traveling frequently to London to inform the group of Congressional action in the United States.

From there, Denis went on to become director of government affairs and economic development for the Cincinnati Business Committee, a regional association that included Fortune 500 companies among its members. After two years in that role, Denis joined the staff of Rep. Steve Chabot, R-Ohio, moving back to Washington and serving as the congressman’s deputy chief of staff during a five-year stint that ended when he joined the SBFA.

While working for Chabot, Denis also became deputy staff director of the House Committee for Small Business, the No. 2 position there, and he has held that job for the last three years. The committee’s tasks include learning as much as they can about small business, including financing, and using the information to advise members of the House on policy initiatives.

The experience Denis has amassed in government should serve the association well because his duties include briefing federal legislators and regulators on how the alternative-finance business works. With Denis as spokesperson, the industry can speak to government with a single voice, Goldin asserted.

“We are going to be aggressive in our outreach to legislators and regulators as well as be active reaching out to local, state governments,” Denis said. The SBFA will “work with other trade groups and small business groups to promote our mission to ensure small businesses have alternative finance options available to them.”

Until now, too many players from the alternative finance industry have been vying for lawmakers’ attention, Goldin said. To make matters worse, some of those seeking to influence government in hearings on Capitol Hill are brokers instead of lenders and thus may not have a perfect understanding of risk and other aspects of the business, he maintained.

“We’re hearing that there are people trying to be the voice of small-business finance that either don’t have a lot of years of experience or they’re not telling the whole story,” Goldin said. “We want to make sure the industry’s represented properly.”

Denis can draw attention away from the “noise” created by unqualified voices and focus on information that Congress needs to make reasonable decisions about the alternative finance business, Goldin maintained.

Besides getting the word out in Washington, the SBFA hopes to convey its message to the general public on “the benefits of alternative financing,” Goldin said. At the same time the group can help make small business owners aware of the finance options, Denis added.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Meanwhile, updated “best practices” guidelines might be in the offing to help industry players navigate the business ethically and efficiently, Goldin said. A set of six best practices the association released in 2011 included clear disclosure of fees, clear disclosure of recourse, sensitivity to a merchants’ cash flow, making sure advances aren’t presented as loans and paying off outstanding balances on previous advances.

Addressing other possible steps in the association’s growth, Goldin said the group doesn’t plan to publish an industry trade magazine or newsletter. However, a trade show or conference might make sense, he noted.

Denis said he and the board had not discussed the possibility of a test, credential or accreditation to certify the expertise of qualified members of the industry. However, associations often establish and monitor such standards, so it would be reasonable for the SBFA to do so, he added.

The association might establish a Washington office, Goldin said. “We’ll look to Steve for his thoughts and guidance on that,” he observed. Denis seems amenable to the idea. “Down the road, we would love to open an office and hire more people,” he said.

In Goldin’s view, all of those moves might help the rest of the world comprehend the industry. Understanding the industry requires taking into account the cost of dealing with risk and business operations, he said.

Placing a $20,000 merchant cash advance, for example, requires a customer-acquisition effort that costs about $3,000 and a write-off of losses and overhead of about $4,000, Goldin said. That’s a total of $27,000 even without the cost of capital, he maintained.

“Most people don’t understand the economics of our business,” Goldin continued. The majority of placements are for less than $25,000, he said, characterizing them as “almost a loss leader when you factor in the acquisition costs.”

While spreading that type of information on the industry’s inner workings, Denis will also conduct the day-to-day for the not-for-profit’s affairs. The association’s board of directors will continue to set policy and objectives.

Members elect the board members to two-year terms. Current board members are Goldin; Jeremy Brown of Rapid Advance, who’s also serving as the group’s vice president; John D’Amico, GRP Funding; Stephen Sheinbaum, Bizfi; and John Snead, Merchants Capital Access.

Member companies include Bizfi, BFS Capital, Capify, Credibly, Elevate Funding, Fora Financial, GRP Funding, Merchant Capital Source, Merchants Capital Access (MCA), Nextwave Funding, NLYH Group LLC, North American Bancard, Principis Capital, Rapid Advance, Strategic Funding Source and Swift Capital.

Companies pay $3,000 in monthly dues, which Denis characterizes as inexpensive for a DC-based trade association.

Membership could spread to other types of businesses, Denis said. “I’d like to expand the tent to other industries,” he noted. “The association is trying to represent the interests of small business and make sure they have every finance option available to them.”

But a key purpose of the trade association is to provide a forum for members to come together as an industry, Denis said. “We’re thinking big,” he admitted. “We hope that all members of the marketplace will want to become a part of it.”