The Top Small Business Funders By Revenue

October 23, 2017The below chart ranks several companies in the non-bank small business financing space by revenue over the last 5 years. The data is primarily drawn from reports submitted to the Inc. 5000 list, public earnings statements, or published media reports. It is not comprehensive. Companies for which no data is publicly available are excluded.

| Company | 2016 | 2015 | 2014 | 2013 | 2012 |

| Square1 | $1,708,721,000 | $1,267,118,000 | $850,192,000 | $552,433,000 | $203,449,000 |

| OnDeck2 | $291,300,000 | $254,700,000 | $158,100,000 | $65,200,000 | $25,600,000 |

| Kabbage3 | $171,784,000 | $97,461,712 | $40,193,000 | ||

| Swift Capital4 | $88,600,000 | $51,400,000 | $27,540,900 | $11,703,500 | |

| National Funding | $75,693,096 | $59,075,878 | $39,048,959 | $26,707,000 | $18,643,813 |

| Reliant Funding5 | $51,946,472 | $11,294,044 | $9,723,924 | $5,968,009 | $2,096,324 |

| Fora Financial6 | $41,590,720 | $33,974,000 | $26,932,581 | $18,418,300 | |

| Forward Financing | $28,305,078 | ||||

| Gibraltar Business Capital | $15,984,688 | ||||

| Tax Guard | $9,886,365 | $8,197,755 | $5,142,739 | $4,354,787 | |

| United Capital Source | $8,465,260 | $3,917,193 | |||

| Blue Bridge Financial | $6,569,714 | $5,470,564 | |||

| Lighter Capital | $6,364,417 | $4,364,907 | |||

| Fast Capital 360 | $6,264,924 | ||||

| US Business Funding | $5,794,936 | ||||

| Cashbloom | $5,404,123 | $4,804,112 | $3,941,819 | $3,823,893 | $2,555,140 |

| Fund&Grow | $4,082,130 | ||||

| Nav | $2,663,344 | ||||

| Priority Funding Solutions | $2,599,931 | ||||

| StreetShares | $647,119 | $239,593 | |||

| CAN Capital7 | $213,402,616 | $269,852,762 | $215,503,978 | $151,606,959 | |

| Bizfi8 | $79,886,000 | $51,475,000 | $38,715,312 | ||

| Quick Bridge Funding | $48,856,909 | $44,603,626 | |||

| Funding Circle Holdings9 | $39,411,279 | $20,100,000 | $8,100,000 | ||

| Capify10 | $37,860,596 | $41,119,291 | |||

| Credibly11 | $26,265,198 | $14,603,213 | $7,013,359 | ||

| Envision Capital Group | $21,034,113 | $19,432,205 | $12,071,976 | $11,173,853 | |

| Capital Advance Solutions | $4,856,377 | ||||

| Channel Partners Capital | $2,207,927 | $4,013,608 | $3,673,990 | $2,208,488 | |

| Bankers Healthcare Group | $93,825,129 | $61,332,289 | |||

| Strada Capital | $8,765,600 | ||||

| Direct Capital | $432,780,164 | $329,350,716 | |||

| Snap Advances | $21,946,000 | ||||

| American Finance Solutions12 | $5,871,832 | $6,359,078 | |||

| The Business Backer13 | $19,593,171 | $11,205,755 | $9,615,062 |

1Square (SQ) went public in 2015

2OnDeck (ONDK) went public in 2014

3Kabbage received a $1.25B+ private market valuation in August 2017

4Swift Capital was acquired by PayPal (PYPL) in August 2017

5Reliant Funding was acquired by a PE firm in 2014

6Fora Financial was acquired by a PE firm in 2015

7CAN Capital ceased funding operations in December 2016 but resumed in July 2017

8Bizfi wound down in 2017. Credibly secured the servicing rights of their portfolio

9Funding Circle’s primary market is the UK

10Capify’s US operations were wound down in early 2017 and their operations were integrated with Strategic Funding Source. Capify’s international companies are still operating

11Credibly received a significant equity investment from a PE firm in 2015

12American Finance Solutions was acquired by Rapid Capital Funding in 2014, who was then immediately acquired by North American Bancard

13The Business Backer was acquired by Enova (ENVA) in 2015

The Top Small Business Funders By Revenue

September 14, 2017Thanks to the Inc 5000 list on private companies and earnings statements from public companies, we’ve been able to compile rankings of alternative small business financing companies by revenue. Companies that haven’t published their figures are not ranked.

| SMB Funding Company | 2016 Revenue | 2015 Revenue | Notes |

| Square | $1,700,000,000 | $1,267,000,000 | Went public November 2015 |

| OnDeck | $291,300,000 | $254,700,000 | Went public December 2014 |

| Kabbage | $171,800,000 | $97,500,000 | Received $1.25B+ valuation in Aug 2017 |

| Swift Capital | $88,600,000 | $51,400,000 | Acquired by PayPal in Aug 2017 |

| National Funding | $75,700,000 | $59,100,000 | |

| Reliant Funding | $51,900,000 | $11,300,000 | Acquired by PE firm in 2014 |

| Fora Financial | $41,600,000 | $34,000,000 | Acquired by PE firm in October 2015 |

| Forward Financing | $28,300,000 | ||

| IOU Financial | $17,400,000 | $12,000,000 | Went public through reverse merger in 2011 |

| Gibraltar Business Capital | $16,000,000 | ||

| United Capital Source | $8,500,000 | ||

| SnapCap | $7,700,000 | ||

| Lighter Capital | $6,400,000 | $4,400,000 | |

| Fast Capital 360 | $6,300,000 | ||

| US Business Funding | $5,800,000 | ||

| Cashbloom | $5,400,000 | $4,800,000 | |

| Fund&Grow | $4,100,000 | ||

| Priority Funding Solutions | $2,600,000 | ||

| StreetShares | $647,119 | $239,593 |

Companies who were published in the 2016 Inc 5000 list but not the 2017 list:

| Company | 2015 Revenue | Notes |

| CAN Capital | $213,400,000 | Ceased funding operations in December 2016, resumed July 2017 |

| Bizfi | $79,000,000 | Wound down |

| Quick Bridge Funding | $48,900,000 | |

| Capify | $37,900,000 | Wound down |

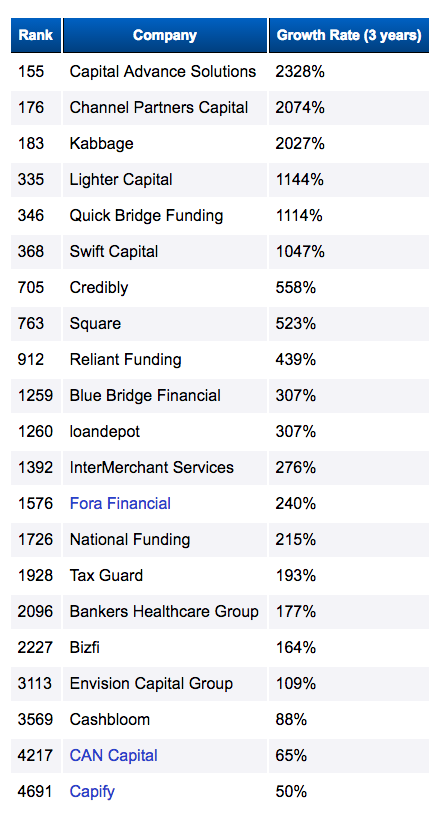

Where Alternative Finance Ranks on the Inc 5000 List

September 14, 2017Here’s where your peers rank on the Inc 5000 list for 2017:

| Ranking | Company Name | Growth | Revenue | Type |

| 15 | Forward Financing | 12,893.16% | $28.3M | MCA |

| 47 | Avant | 6,332.56% | $437.9M | Online Consumer Lender |

| 219 | OppLoans | 1,970.22% | $27.9M | Online Consumer Lender |

| 260 | US Business Funding | 1,657.42% | $5.8M | Business Lender |

| 361 | nCino | 1,217.53% | $2.4M | Software |

| 449 | Kabbage | 979.31% | $171.8M | Online Consumer Lender |

| 634 | Lighter Capital | 712.03% | $6.4M | Online Business Lender |

| 694 | Swift Capital | 652.08% | $88.6M | Business Lender |

| 789 | CloudMyBiz | 575.46% | $2.1M | IT Services |

| 1418 | loanDepot | 286.11% | $1.3B | Online Consumer Lender |

| 1439 | Nav | 281.98% | $2.7M | Online Lending Services |

| 1731 | United Capital Source | 224.85% | $8.5M | MCA |

| 1101 | ZestFinance | 165.99% | $77.4M | Online Lending Services |

| 2050 | National Funding | 184.74% | $75.7M | Online Business Lender |

| 2572 | Blue Bridge Financial | 136.73% | $6.6M | Online Business Lender |

| 2708 | Bankers Healthcare Group | 127.51% | $149.3M | Financial Services |

| 2714 | Tax Guard | 127.02% | $9.9M | Financial Services |

| 2728 | Fora Financial | 125.81% | $41.6M | Online Business Lender |

| 2890 | Reliant Funding | 121.61% | $51.9M | Online Business Lender |

| 4005 | Cashbloom | 70.47% | $5.4M | MCA |

| 4945 | Gibraltar Business Capital | 42.08% | $16M | MCA |

Compare that to last year’s list below:

Of the companies on the 2016 list, Capify and Bizfi were wound down while CAN Capital ceased operations but then later resumed them more than half a year later.

A Tale of “Debt Restructuring”?

April 19, 2017 Here’s a doozy for you: A merchant signed an agreement with a purported law firm on September 29, 2016 for assistance with restructuring their debts. As part of that agreement, the law firm, which goes by the name Protection Legal Group, LLC, also offers “Litigation Defense Services” in case the merchant gets sued for non-payment of debts. The basic “non-legal” services alone, however, required that this merchant pay approximately $100,000 to Protection Legal Group, according to court filings. That’s a pretty hefty service fee for a business that was only claiming $400,000 in debts, most of which it improperly classified as debt since they were actually sales of future receivables.

Here’s a doozy for you: A merchant signed an agreement with a purported law firm on September 29, 2016 for assistance with restructuring their debts. As part of that agreement, the law firm, which goes by the name Protection Legal Group, LLC, also offers “Litigation Defense Services” in case the merchant gets sued for non-payment of debts. The basic “non-legal” services alone, however, required that this merchant pay approximately $100,000 to Protection Legal Group, according to court filings. That’s a pretty hefty service fee for a business that was only claiming $400,000 in debts, most of which it improperly classified as debt since they were actually sales of future receivables.

The very next day, a merchant cash advance (MCA) company sued the merchant in New York for breach of contract, claiming that they were owed more than $300,000. And three months later, the merchant, represented by an attorney named Amos Weinberg, sued the first law firm that they hired. According to that complaint, filed on January 6, 2017, Protection Legal Group never even contacted the MCA company even though they were hired to negotiate with them specifically. Stranger yet, the merchant alleges that Protection Legal Group could not even have defended them in litigation because the MCA agreement’s jurisdiction was New York and Protection Legal Group has no lawyers that are licensed in that state. Naturally, the complaint further alleges that Protection Legal Group accepted payments anyway and has refused to return it.

The merchant’s new attorney, Amos Weinberg, is no friend to MCA companies, according to New York court records. Nevertheless, he offers harsh words for these new purported debt restructuring companies on his blog. “A growing industry that preys on people all over the country who are sued in New York is the debt resolution industry,” he wrote. “These companies promise to settle lawsuits for a portion of the sum sued by inducing the client to stop paying the creditor and instead pay sizeable weekly sums into an escrow account.” He then goes on to call out Protection Legal Group by name.

To summarize, a merchant hired a lawyer for an exorbitant fee to restructure their debts that weren’t debts, got sued and then had to hire a lawyer to sue their lawyer.

Protection Legal Group is also being sued by Forward Financing, an MCA company, for interfering with its contracts. That story has made the news in legal circles.

Court documents show that Protection Legal Group is fighting on another front as well since less than three weeks ago, a class action lawsuit (Case: 1:17-cv-02445) was filed against them for violating the TCPA. According to the complaint, they are allegedly marketing their services via pre-recorded voice messages to cell phones.

As an aside, most MCA contracts already permit merchants to have their payments lowered in the event that their revenues drop. Typically, they just need to send in their recent banking activity to demonstrate the drop and the MCA company will reimburse the merchant for anything collected above the specified percentage of sales. As this is a fundamental part of the agreement, the merchant shouldn’t require a debt negotiator or an expensive attorney to aid them with this.

IT’S A BROKER’S WORLD

August 31, 2016

From east to west, small businesses are getting funded. But how they’re found and who they work with depends on where they are. In the US, where brokers tend to have a love/hate relationship with the funding companies they work with, they are no doubt a driving force in the market. In other countries, they might not even exist, are just starting to bloom or they add balance to a mature market. Is the world built for brokers? AltFinanceDaily traveled far and wide to find the answers.

Down under in Australia where American-based merchant cash advance and lending companies have expanded, the ISO (which stands for Independent Sales Office and is synonymous with broker) model has not really followed. David Goldin, CEO of Capify, an international company headquartered in New York, told AltFinanceDaily that there’s very few ISOs in Australia.

He believes that’s because there’s next to no payment processing ISO market there, a foundation that was a major precursor in the US towards the development of ISOs reselling merchant cash advances and business loans.

He believes that’s because there’s next to no payment processing ISO market there, a foundation that was a major precursor in the US towards the development of ISOs reselling merchant cash advances and business loans.

Luke Schmille, President of CapRock Services, echoed same. The Dallas-based company founded Sprout Funding in Australia earlier this summer as part of a joint venture with Sydney-based family office Huntwick Holdings. “Direct marketing is the primary method [of acquiring deal flow],” he said. “The credit card processing space is controlled by several large banks, so you don’t see ISO efforts in the acquiring space either.”

Big bank dominance was only one reason why another country’s emerging alternative small business funding market developed slowly. In Hong Kong, non-bank alternatives like merchant cash advances faced legal uncertainty for a long time. For example, Global Merchant Funding (GMF), once the only merchant cash advance company in the Chinese special administrative region, had been relentlessly pursued for years by the Secretary for Justice for conducting business as a money lender without a license. GMF fought it. And won.

In May of this year, the legality of merchant cash advances ultimately prevailed after the highest court ruled the agreements were not loans. Emboldened, several companies have stepped up their marketing of the product. But whether they’re doing daily debit loans or split-processing merchant cash advances (both of which exist there), marketing tends to be directed at merchants, not a middle market of brokers.

Gabriel Chung of Hong Kong-based Advanced Express Capital said that there are a handful of large brokers typically comprised of former bankers, but the rest of the broker market is highly fragmented, mostly made up of individual freelancers.

Gabriel Chung of Hong Kong-based Advanced Express Capital said that there are a handful of large brokers typically comprised of former bankers, but the rest of the broker market is highly fragmented, mostly made up of individual freelancers.

Adrian Cook, the Founder and CEO of Hong Kong-based Asia Capital Advance, agreed that marketing is usually aimed at merchants directly but that it’s changing. “Since the market is still very new and MCA is only beginning to gain popularity, brokers on the market are only starting to recognize MCA,” he said. “There is a lot of room for the brokerage market to grow.”

In the UK, where Capify also operates, CEO David Goldin explained that the UK doesn’t have a lot of credit card processing ISOs so there wasn’t a major migration from that business to MCA like there was in the US. But that doesn’t mean there is no middleman market at all.

Paul Mildenstein, executive director of London-based Liberis, said that brokers are an important channel, but not as dominant as they are in the US. “Our brokers are usually members of the NACFB, an organisation in the UK that actively supports and provides operating principles to the furtherance of the commercial finance broker community,” he wrote. The National Association of Commercial Finance Brokers claims to have 1600 members, one among them is Liberis.

Paul Mildenstein, executive director of London-based Liberis, said that brokers are an important channel, but not as dominant as they are in the US. “Our brokers are usually members of the NACFB, an organisation in the UK that actively supports and provides operating principles to the furtherance of the commercial finance broker community,” he wrote. The National Association of Commercial Finance Brokers claims to have 1600 members, one among them is Liberis.

“Many clients want the support of an experienced professional who can discuss the financial options available to them in their specific circumstances,” said Liberis’ CEO, Rob Straathof. “Given relatively low awareness of the Business Cash Advance product in the UK, this means that brokers have a key role to play in educating potential customers on when this is the right option for them,” he added.

Straathof stressed a robust criteria for the brokers they work with and explained that brokers are their eyes and ears in the market. “The relationships we have with them are not transactional, but transformational for our business,” he said.

The NACFB was also praised by Alexander Littner, Managing Director of Chelmsford, Essex-based Boost Capital. The company, which is actually a subsidiary of Coral Springs, FL-based BFS Capital in the US, sees a balance between their use of brokers and their efforts to acquire customers directly.

“As the alternative finance market is still relatively new here in the UK these brokers are important for this independent advice, and to help educate the market and establish trust,” Littner said. “At Boost Capital we work very closely with brokers across the UK, they are a critical part of our growth and fundamental to our ongoing success.”

In the US, brokers play such a dominant role in customer acquisition that some MCA funding companies rely on them to source the entirety of their business. Back in February, Jordan Feinstein of NY-based Nulook Capital told AltFinanceDaily, “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require.” Nulook markets its broker-only approach as a strength.

Others take a more blended approach, like Justin Bakes, CEO of Forward Financing, for example. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said earlier this year.

Notably, no such guiding authority like the UK’s NACFB exists for brokers in the US so it’s not easy to track exactly how many there are or how they operate, but their role in the industry cannot be understated. AltFinanceDaily actually labeled 2015 The Year Of The Broker, when it published an article in its March/April 2015 issue that tried to capture the essence of the industry at the time. Tom McGovern, who was then a VP at Cypress Associates LLC, said of brokers, “They’re like the missionaries of the industry going out to untapped areas of the market.”

But preaching the gospel of alternative funding exists at different stages across the world. And Goldin, whose company Capify operates in four countries including the US, thinks that many middlemen here at home may not ultimately survive. In an interview, he predicted that the stronger ones over time will be acquired by funding companies and that direct marketing will only increase. “I think more and more companies are going to start building their own internal sales forces,” he said.

Other brokers are not convinced that acquisition costs will lead to the death of their businesses, especially if they’ve already found ways to reduce overhead costs. Several brokers have discreetly mentioned running operations from Costa Rica, Nicaragua or elsewhere as a way to keep things profitable. Still more, like Excel Capital Management based in Manhattan, have found that offering a suite of products allows them to monetize more customers. Chad Otar, a managing partner for Excel, said that they recently brokered a $4.9 million SBA loan. MCA is just one of their options these days. “As long as there’s small businesses, there’s always going to be opportunity,” he said.

In the US, the brokers have certainly seized it, but that’s because most funding companies offer big bucks and quick payment to those that are capable of sourcing customers. In other countries, compensation for services rendered might be the responsibility of the broker to arrange with the merchant since it may not be customary for funding providers to pay commissions. That would mean more work and more risk for the broker.

In the US, the brokers have certainly seized it, but that’s because most funding companies offer big bucks and quick payment to those that are capable of sourcing customers. In other countries, compensation for services rendered might be the responsibility of the broker to arrange with the merchant since it may not be customary for funding providers to pay commissions. That would mean more work and more risk for the broker.

Ironically, some brokers in the US will tap into both sides, earning a commission from the funder and charging a fee to the merchant for services rendered. And if the broker has payment processing roots, they can go a step further and earn merchant account residuals as well.

Brokers can’t exist without funding companies willing to support their endeavors, of course. While their prevalence around the world varies, most of the funding companies AltFinanceDaily spoke to, appear eager to nurture the middleman’s role, so long as they act responsibly.

“Brokers in the UK are incredibly important as independent advisors to small businesses on the various sources of finance to suit their needs,” said Littner.

And as long as those customers, wherever they may be, are getting the value they want from a broker, that role, so long as it can continue to be done profitably, will likely have a place in the world for the foreseeable future.

Can Technology Be More Than Automation?

August 19, 2016

In yet another Lending Club exposé, Bloomberg revealed the identity of the man who allegedly first discovered suspicious Lending Club loans that would later be confirmed connected to disgraced CEO Renaud Laplanche in a post-resignation audit. Brian Sims, a retail investor in Lending Club loans used a specially designed algorithm to spot patterns such as multiple loans made to a single borrower at different interest rates. No easy task considering Lending Club takes great strides to protect borrower identity.

And this truly is the argument both for and against technology. Irrespective of what side of the debate you’re on, it’s hard to argue its indispensability in day to day business. It’s the one thing CEOs think long and hard about and rightly so — automation makes or breaks the size and scale of a business, vastly improves productivity and narrows if not eliminates the margin for human error (up for debate).

So, at AltFinanceDaily we were curious to discover how small business financing companies use technology in their companies, what processes are automated and which side of the man vs machine debate they fall on.

Boston-based Forward Financing that makes merchant cash advances, working capital finance and small business loans up to $300,000 started investing in proprietary software right from the beginning, four years ago. It uses Salesforce for customer relations and basic reporting.

Its underwriting tool, channels leads and performs varying levels of automation to underwrite files quicker. The app pulls data from a number of different sources like credit bureaus, public record databases, social media and Google APIs before it goes to an underwriter. “Our goal over the next 3-4 months is to automate a percentage of all the deals that comes through the system,” said CEO Justin Bakes.

The company also has a banking application, a portal where customers log in with their bank details, with read-only access to their bank accounts to identify and analyze transactions which are then used to underwrite. Separately, it also has a portfolio management system that manages all the funding, transactions and all the collections.

While Bakes started investing in technology early on, it wasn’t until a year and a half ago that he tried automated underwriting. “Some hear the word automation and think they are going to lose their jobs,” said Patrick Hereford, Director of Technology at Forward Financing. “I can understand that automation can reduce jobs, but here, they found that they could underwrite more deals faster and with more accuracy.”

Hereford was hired in October last year from the TV show America’s Test Kitchen where he was working as a software engineer. Hereford makes a case for automated underwriting with proof — “We went from spending 20 minutes per file to six minutes per file,” he said. “We were expecting 50 percent efficiency in underwriting but we got more and increased productivity.”

The company hired full-time engineering staff last year to move all their tech support and development in house. “A majority of our new hires and investments have been in technology. The tech team has grown the most over the last year,” said Bakes. He noted that the company has spent over a million dollars in building proprietary software alone and 20 percent of its selling, general and administrative (SG&A) is allocated to technology development.

The company hired full-time engineering staff last year to move all their tech support and development in house. “A majority of our new hires and investments have been in technology. The tech team has grown the most over the last year,” said Bakes. He noted that the company has spent over a million dollars in building proprietary software alone and 20 percent of its selling, general and administrative (SG&A) is allocated to technology development.

“There is no doubt that we are a financing company but we are a tech-minded financing company. To be a true industry leader, you have to automate a certain amount. Our philosophy is we plan to keep improving our technology and the ability to approve faster than anyone else,” Bakes said.

Forward Financing is among other companies moving in that direction. California-based lender National Funding who has deployed $1.5 billion to small businesses over the last 17 years is also preparing for a technology overhaul, trying to get access to data pools to automate underwriting. “We need to be tech driven, as deals get smaller, we need to automate them to make it affordable,” National Funding CEO Dave Gilbert told AltFinanceDaily earlier.

And five-year-old Pearl Capital is on a similar journey. The company grew its tech team from two to twelve people over a year and a half ago including data analysts and statisticians and is making significant investments in scoring technology, portfolio management and risk assessment. “We had a human model running successfully for years and they produce good results but move to machine is additive and supplemental,” said CEO Sol Lax. “Data and tech add a lot more texture and nuance to the market, it’s like the weather radar, you have visibility and can price accordingly.”

But technology doesn’t have to necessarily mean automating underwriting. In fact, there is a strong bastion of people actively resisting it. Isaac Stern, CEO of New York-based Yellowstone Capital is one of them. “I am going to get my underwriters as much information as possible – background check, credit check to make good decisions but that does not mean I am going to let a computer decide whether to fund or not.”

That doesn’t mean Stern doesn’t care about efficiency. In fact, Yellowstone has invested over a million dollars over the last year in ramping up technology. It hired AIG’s chief data scientist and has improved data mining with access to over 140 data points including SIC codes, credit scores and loan history. The company uses an application called Clear®, a Thomson Reuters product, through which it can conduct background checks as well as review business history and public records.

No matter what camp you belong to, there are strong arguments to be made for each side and it really comes down to the philosophy of the matter. But in a crowded lending market, does it make sense to grab every opportunity to scale better?

“Different people have different thoughts on whether this is frankenstein going off the rails or not and whether that will blow up or not,” said Lax. “But the barrier to entry is low as a funder, and the spend on tech can be small yet profitable.”

There are many alternative finance companies who believe that staying in the game requires some change in incumbent models to boost efficiency and speed that’s driven by auto approvals and declines. But there are also some like Stern who treat technology as an aid rather than an aim.

Perhaps time will tell which system is better.

Loan Brokers or Self Origination? Here’s What Experts Say

February 22, 2016 Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

But a year on, as the dust has settled, we asked industry veterans what it means to remain successful in this business and what is the key to sustainability — is it in going for the ISO/broker channel to find deals or originating your own.

Here’s what they had to say

Don’t Break the Broker

Tom Abramov of MFS Global voted for the ISO/broker channel and said that that’s how the company strictly does deals, working with brokers who have a track record as a part of their recruitment system. The six year old company that started as an broker shop now focuses only on funding with products that are a mix of merchant cash advances and lines of credit.

“We don’t look at FICO scores or SIC codes, we only look at cash flows of businesses,” said Abramov. “I want to see if I give a someone a dollar whether they can turn it into two.”

Abramov added that his firm offers brokers 20 percent commission and their default rates are sub 5 percent.

The advantages of scoring deals through a broker channel can be alluring. It involves no overhead, no staff that needs compensation, motivation and incentives, and makes use of the existing broker-merchant relationships.

Jordan Feinstein of NuLook Capital said that his firm works with brokers exclusively and the model has helped them respond to merchants faster. “We do not have a sales team speaking to merchants directly, that’s in conflict with our model,” said Feinstein. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” he said.

Building a Hybrid Model

There are some others who want to make the best of both the models and work with brokers while originating and funding their own deals. Forward Financing which uses a hybrid model has strategic partnerships with some brokers while still originating their own deals. “We have a hybrid model because our goal is to have a program for any type of business and work with companies across the spectrum of risk,” said Justin Bakes, CEO of Forward Financing. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said.

The Original Origination

While the allure of a lean business is certainly attractive, there are some who are in the industry to build a bigger business and create value by making it robust — Jared Weitz of United Capital Source is one of them. “There is a big market for both analytical process as well as sales process. It’s important to go after your strength,” said Jared Weitz, founder and CEO of United Capital Source. “When you originate and fund your own deals, you’re in a rewarding position and in control of how merchants get treated.”

Industry Trends

Speaking of the industry in general, these experts agreed that the business was undergoing a change with new entrants coming in and experimenting with better services and technologies.

“Last year was the year of brokers but we are still missing the education with merchants. Some brokers are interested while some are not,” said Abramov.

“I notice a clear difference between the old and the new in terms of technology and pricing model,” said Bakes.

“New funders are coming in with different products and terms with increased competition in the ISO market,” said Feinstein.

“Marketing is getting more expensive and only the ones who can afford to pay can play,” said Weitz.

Dragin Technologies Unveils the Industry’s First AI Merchant Integrity Dashboard, Setting a New Standard for Underwriting Accountability

September 17, 2025New York, NY — September 17 2025 — Dragin Technologies, the automation engine powering some of the fastest-growing revenue-based financing companies, today announced the launch of its groundbreaking AI Merchant Integrity Dashboard, the first tool of its kind designed to ensure clean, accurate, and trustworthy underwriting decisions.

This new AI-powered feature combines every critical data source in the underwriting process — application forms, bank statements, credit reports, background checks, Dragin’s proprietary AI Web Report, and even the merchant’s interview — into a single, intelligent report. It then cross-references every data point to uncover discrepancies, validate claims, and flag potential risks before an offer is made.

How It Works

The AI Merchant Integrity Dashboard automatically reviews and cross-verifies all data points across multiple documents. It checks everything from business addresses to revenue patterns, ensuring consistency and truthfulness at every step.

For example:

- If a merchant claims their revenues are steadily increasing, the AI will verify this against actual bank statement data.

- If the merchant says they have “great credit,” Dragin will confirm that claim and flag missed payments or delinquencies.

- Business addresses are cross-checked between the application, background checks, and banking data to catch mismatches or fraudulent entries.

Every red flag identified by the AI must be manually reviewed and approved by an underwriter before a deal can move forward, creating a new layer of accountability and transparency in the underwriting process.

Why This Matters

For revenue-based financing companies, speed and accuracy are essential — but so is trust.

With the AI Merchant Integrity Dashboard, underwriters can no longer miss critical details or claim ignorance after a deal closes.

Key benefits include:

- Early fraud detection through cross-document analysis

- Cleaner, fully reconciled deal data for every file

- Reduced merchant default rates by catching inconsistencies up front

- Stronger underwriting accountability, protecting funders from costly mistakes

“This changes everything,” said Mark Ross, CEO of Dragin Technologies.

“For the first time, funders can hold their teams accountable for every detail in a deal. Our AI does the heavy lifting, surfacing risks that used to take hours — or never got caught at all. No more guessing. No more missed red flags.”

Part of Dragin’s Full Automation Suite

The AI Merchant Integrity Report is the latest innovation in Dragin’s end-to-end deal automation platform, which includes:

- Automated email parsing and document classification

- AI-powered application and bank statement reader

- Pre-qualification and pre-decline logic

- DraginForce CRM with built-in automation suite

- Real-time ISO portal for faster deal negotiations

- End-to-end deal tracking and syndication portal

About Dragin Technologies

Dragin Technologies builds the tools that power the future of revenue-based financing. With advanced AI, machine learning, and automation technology, Dragin enables funders to scale faster, reduce risk, and make smarter decisions. Its flagship CRM, DraginForce, and cutting-edge automation modules are trusted by some of the largest and fastest-growing funders in the industry.

Learn more at www.dragin.io