Recent Merchant Cash Advance News

April 14, 2013 In case you missed some of the big headlines in this last week, below is a summary:

In case you missed some of the big headlines in this last week, below is a summary:

Forbes changed its tune on MCA after five years

It took only a handful of journalists to set the Merchant Cash Advance industry’s momentum back YEARS. One of those journalists was Maureen Farrell, a previous writer for Forbes. Her story on January 31, 2008, titled Look Who’s Making Coin Off The Credit Crisis mercilessly labeled Merchant Cash Advance providers as blood sucking vampires borne out of the Great Recession. Sensational headlines attract attention and Farrell did her job well. But for someone whose background is Art History, English, and Journalism, she may not have been in the best position to make a qualified assessment of such a unique method of alternative finance. It’s unfortunate then that Forbes ran the story since it no doubt impacted public opinion in a negative manner for years.

That’s why it was so refreshing to see ‘Money, Money’ — How Alternative Lending Could Increase Your Company’s Revenue in 2013. Published by Cheryl Conner, she wastes no time in pointing out Farrell’s prior coverage as one of personal opinion and skepticism. Merchant Cash and Capital’s CEO, Stephen Sheinbaum was instrumental in Conner’s fresh assessment of the industry.

Read the new article on Forbes…

Deals being stretched out over 15 to 24 months may not be a step in the right direction

At least that’s the take of RapidAdvance’s CEO Jeremy Brown. In his latest post on DailyFunder Brown argued permanent capital solutions do not fit working capital needs.

Read his post…

Major executive shake-up occurs at Capital Access Network

Capital Access Network, the parent company of AdvanceMe, CapTap, and NewLogic recently let go of several top executives. Before official announcements were made, word had already leaked out and was being discussed on DailyFunder.

Read the discussion…

Merchant Cash Group announced the winner of their NCAA March Madness contest

NCAA basketball took us for a wild ride this year, but Merchant Cash Group is still awarding all their participants with bobble heads. The first place winner got cold hard cash.

His name is….

On Deck Capital embraces startup culture

Video games and ping pong tables adorn On Deck’s new office. Is the culture changing in alternative lending?

Read the story…

The ETA Expo is fast approaching. Are you going? Plan meetups

ETA expo thread on DailyFunder…

Kabbage Closed on a $75 million credit line

Read the story…

The Inefficient Merchant Lending Market Theory

March 5, 2013There are 4 major factors used to determine approvals in the merchant lending market:

• FICO Score / Credit Report history of owners

• Monthly Gross Revenue

• Time in Business

• Average Daily Bank Balance

Only 1 of these factors considers the applicant’s reputation, and that’s credit reports. Credit reports reveal past payment history with other creditors. They show lawsuits, unpaid taxes, and bankruptcies. Knowing whether an applicant pays on time or not is valuable to lenders but it fails to reveal an even more important metric, the business’s ability to generate future profits. If you’re shaking your head and saying “credit reports aren’t for that purpose,” I would respond by asking which of the 4 factors then is?

The amount of money deposited in someone’s bank account in the past reveals how much they took in, but it doesn’t indicate what will happen in the future. Similarly, a substantial daily ending bank balance may show responsibility to maintain a cash cushion, but it says nothing about how likely customers are to buy from that business in the future.

Could time in business then tell us? Is it safe to assume that a business that has been operational for a year, two years, or five years will be there for many more years to come? The local auto mechanic that’s been around for 5 years may only have lasted because no one else has gotten around to opening up a rival auto shop. Would it be safe to give the most hated mechanic in town a three year loan when their success is simply the result of being the only auto mechanic in the community? There may be somewhat of a correlation between time in business and customer satisfaction but it is by no means strong enough to predict future success.

In effect, the major metrics used to judge small businesses for financing today take no consideration of the number one thing that matters to a business for survival, customers. Without customers, the amount deposited historically means nothing. Without customers, a 700 FICO score cannot produce sales, profits, or money to repay a loan. Without customers, a 50 year old restaurant can’t continue to stay open just because it’s been there for 50 years. And without customers you better hope that $1 million in sales last year made you really rich, since without customers, you’re going to need to start a new business… preferably one WITH customers.

This doesn’t mean that these 4 factors are irrelevant, they’re not. But I believe these factors combined are but a tiny sliver of data to predict how well a business will do in the future and at the same time repay a loan. Relying on weak indicators forces lenders to charge higher rates since they must compensate for the risk of unknowns. It also decreases the length of time that lenders can trust their borrowers to hold their money for.

It is no surprise then that loan terms in the merchant lending industry only range from 3 to 12 months. None of the lenders are able to predict how their borrowers are going to do far into the future, so they bank on the odds that sales and deposits in the next few months will mimic sales and deposits in the last few months. That’s also the reason why there are a lot of test/starter/trial funding rounds that are short to witness how a merchant “does” before funding additional capital on a longer term. Underwriters are flying blind. They have to see how you do because they have no data to suggest what will happen.

The big firms do have SOME data by now, but they’re broad statistics that say a certain industry in a certain region is likely to perform X with a Y margin of error. Or FICO scores below 600 are likely to have a Z rate of default. Yet this data also ignores a business’s reputation and relationship with its customers. It applies a blanket assumption of performance over the period of 3 to 12 months. These statistics are highly important to a lender because they can use them to predict defaults and delinquencies as a whole and enable them to set rates that will cover all of it and then some.

The big firms do have SOME data by now, but they’re broad statistics that say a certain industry in a certain region is likely to perform X with a Y margin of error. Or FICO scores below 600 are likely to have a Z rate of default. Yet this data also ignores a business’s reputation and relationship with its customers. It applies a blanket assumption of performance over the period of 3 to 12 months. These statistics are highly important to a lender because they can use them to predict defaults and delinquencies as a whole and enable them to set rates that will cover all of it and then some.

The owner of an ISO once asked me, “Wouldn’t it be great if we got to the point where we were funding every business in America?” My answer was “No.” If 10, 20, or 30% of those businesses failed to repay or eventually went out of business (and they would if you funded everyone) and the lender STILL made money, then the ones in good standing had to of gotten charged way too much. It would also mean that there had to be a portion of performing loans that were actually distressing the borrower, causing the capital they obtained to work against them, rather than for them. The goal shouldn’t be to fund EVERYONE, but rather to fund the few that could truly benefit.

A great example of doing it wrong is Wonga, a UK based lender that accepted a 41% rate of bad debt in 2011 while still managing to reap £62.4 million in profit. If Wonga had a few hundred bucks, a few thousand bucks, or heck only a million, they’d probably be very careful about who they approved and why they approved them. But venture capital changes the game and not always in a positive way. Putting a few hundred million dollars in the hands of Wonga has caused them to become incredibly inefficient.

Why should they only fund 5,000 people through a highly comprehensive underwriting process when they can fund 30,000 people with a one-size fits all rate, ask no questions, and accept that they will burn a lot of their customers along the way? This is the question they must have asked themselves years ago. (You can read the founder’s interview HERE)

At some point when they were developing their business model they had to admit that they really didn’t care what the outcome would be for their borrowers, so long as the business made money. And so they created an algorithm that would statistically predict the rate of default based on weak indicators like demographics, how they answered a few questions, and credit score and the resulting delinquencies were just necessary casualties to make the system work. In essence, Wonga knows they will devastate a portion of their customers and accepts this. They’re like a restaurant that only sells sugar frosted donut cheese ice cream to obese people and accepts that 41% of their revenues will be lost due to their customers dying. Can a lender truly be helping a community or economy where it intentionally hurts a percentage of borrowers because it’s still profitable at the end of the day? Do their contests, soccer sponsorships, and positive messaging on social media make up for their disruption to the economy?

Wonga’s mission is to grab market share, a strategy to make holy their blanket performance statistics and the rate that has to be charged to make money. Every single individual in the country becomes a candidate for their loans even though the lender will never know anything about the individual borrowers, their long term prospects, or what they can afford. The math says it doesn’t matter because an acceptable amount of the loans will perform and applicants can either accept the high rate or get nothing.

How I portray Wonga is not what I think of the merchant lending market in the US but rather I believe they’re a good example of the trap that merchant lenders COULD fall into if they come into too much money. When I first began to hear lenders fresh off a capital raise saying they wanted to fund the sh*t out of small business and would do anything in their power to fund as many deals as possible, I fear they could end up disrupting communities more than they could help them.

You know that thing called the Internet?

You know that thing called the Internet?

So I’ve talked a lot about what lenders don’t know but nothing about what they can learn. There is an unbelievable amount of free data available on the web that can collectively be used as a strong indicator of future business performance. You know those all important customers I spoke about earlier? The ones that make a business a business? Well lucky for us, they seem to go online and offer feedback about their experiences. Yelp, Zagat, and Facebook come to mind.

How is a business REALLY doing? Reviews will tell you a lot so long as there are enough of them, and not just the star meter, but the actual written reviews. I assure you that it will help a lender if they see that the last 10 reviews say that the owner is a no good lying crook that stopped paying his employees and punched a customer just the other night. A business’s whole reputation can’t be assessed from paperwork and credit scores, but it can be by hearing from people in the local community. That community is online.

That brings me to another point here. If a small business isn’t online, then no faith should be put in that small business in 2013. I don’t know why there are still so many small businesses out there that don’t use e-mail, don’t have a website, and don’t participate on social networks. Unless their shtick is that they are an Amish style operation striving for authenticity, then not being online should be an indicator that they do not care much about their long-term success. I would go so far as to say that any business that does not have at least a website, business fan page on Facebook, twitter account, or a reasonable substitute should be automatically declined for financing. Yeah, I said it!

In 2013, ignoring the Internet is like opening a store with no sign, boarding up the windows, and surrounding the front door with barbed wire. Sure, the locals might know you’re there and be smart enough to come in the back door, and maybe they’re enough to keep your business stable but no one else will find you and the ones that do, will see that you have no interest in being something more. You don’t have to be on every social network but if you’re not on any, you’re doing something wrong. Ideally, you should be somewhat active with your customers online too. This doesn’t mean sending each person that dined at a restaurant a Thank-You e-mail, but it does mean addressing complaints if there are any, posting announcements so customers can see them, and taking steps to improve your reputation.

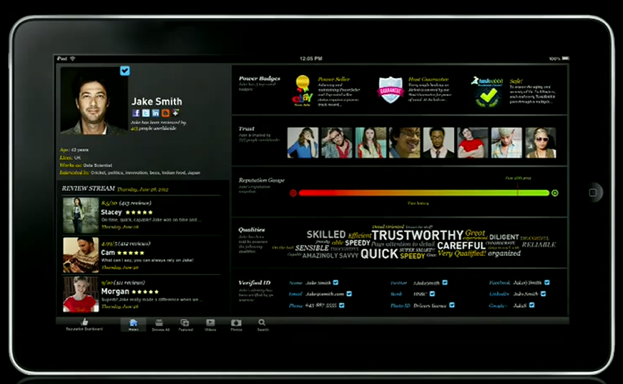

There are many, many trust and reputation signals online. At the most recent TED Conference, Rachel Botsman talked about collaborative consumption, trust, and reputation. She believes that trust is the most vital currency in our economy, not the money in your bank account, but trust. I highly recommend you watch it below. You should definitely take notice of what may eventually become a reality, an individual’s reputation scorecard, a report that aggregates reviews from everyone you’ve ever had an exchange with, and one that has the ability to evaluate the transactions which have the most meaning. My stellar e-bay seller record going back to 1999 might be on there (72 rave reviews baby!) but they won’t be as important if you’re looking to determine how credible I am as a business lending analyst. Still, in the grand scheme of reputation, they could have their place if someone wanted to gauge how trustworthy I am to deliver on something I agreed to.

Release the darn data

You want to know who is holding out on making the merchant lending industry and American economy a better place? The North American Merchant Advance Association (NAMAA) is. NAMAA possesses a database of every merchant that has defaulted or gone delinquent with a funding member in the last 4 years. There’s thousands of names in it. Not a member of NAMAA? You won’t get to know if a merchant has tried some funny stuff with another funder or gone out of business while having an advance.

But you want to know who this private bank of data hurts most? It hurts every business and wholesaler these merchants work with in the future. A month after a retail store fraudulently skips out on a $100,000 advance, that same retailer could apply for 60 day terms with a supplier and sign a 5 year lease for a new business location. Don’t that supplier and landlord deserve to know that their “awesome” new client has a reputation for committing theft and fraud as recent as 30 days ago? I think it’s our duty to let them know. NAMAA is withholding information that could prevent a lot of unreputable people from doing further harm in local economies. Make this data public and we’ll allow suppliers, landlords, and other lenders to make more informed decisions.

But you want to know who this private bank of data hurts most? It hurts every business and wholesaler these merchants work with in the future. A month after a retail store fraudulently skips out on a $100,000 advance, that same retailer could apply for 60 day terms with a supplier and sign a 5 year lease for a new business location. Don’t that supplier and landlord deserve to know that their “awesome” new client has a reputation for committing theft and fraud as recent as 30 days ago? I think it’s our duty to let them know. NAMAA is withholding information that could prevent a lot of unreputable people from doing further harm in local economies. Make this data public and we’ll allow suppliers, landlords, and other lenders to make more informed decisions.

I’ve heard the argument that privacy can be a big selling point to borrowers. They don’t necessarily want outsiders to know that they borrowed money or to suffer the shame if they don’t pay it back. I can understand the benefits of privacy from a competitive standpoint for a borrower but it defies all logic and reason for a lender to keep a default under tight wraps. Public record of a default discourages borrowers from defaulting in the first place and is helpful to everyone that may interact with that borrower in some way in the future. How many merchants would reconsider signing on the dotted line for $50,000 if they knew a default meant the lender would personally message all of their fans on Facebook to tell them about it? Is this wrong? Is this any of the customers business? What if their customers were paying for services 12 weeks in advance? Would their customers have the same confidence that their service would be rendered knowing this new information? It is likely that some customers would view a default as a sign that the business cannot deliver on their promises and reconsider using them. By not letting them know, you are putting them all at risk of paying for services they might not get.

Even though everyone hates me, I project 300% growth!

Show an underwriter a chart of sales projections for the next two years and they’ll have no idea if it’s just wishful thinking. All the demographic research in the world won’t convince the bank that people will trust your product. Show an underwriter that 50, 100, or a thousand people are saying positive things about their experience with you online, and they might believe you’re on to something. Time in business, cash flow, profitability, and positive credit history show what someone did and what they have, but reputation and trust reveal what someone’s success in the future will be like.

It’s not just what they say about you

Your reputation goes beyond just what people are saying about you. At some point, you’ll talk back and what you say can clue lenders into who you are and what you are doing. I’ve caught a few business announcements on Facebook that went something like “To our loyal customers, we are making a last ditch effort to get a merchant cash advance to pay off our landlord by Friday and keep the business open. If it does not happen, then we want to thank you all for your support over the years as we will close for good.” Yeah, it’s interesting to see things like this after you just had a 15 minute conversation with that same person that claimed the funds would be used for a marketing campaign.

With hundreds of millions of dollars burning a hole in their pocket, a lender may be tempted to take the Wonga approach. I guarantee Wonga would say I wasted my time by examining a business owner’s social interactions. They’d say there were statistics and data that show they should fund that business anyway because the FICO score and sales volume are within their parameters, that defaults were acceptable and built into the numbers, and that funding as many businesses as fast as you can above a certain interest rate, is better than funding fewer businesses with more appropriate terms.

This is the premise of my inefficient merchant lending hypothesis for lenders that get real sloppy when they have too much money. Would you rather be a lender that charges more, funds more, and knows less about your borrowers or would you rather charge less, fund more intelligently, and know more about who you’re funding? The first road accepts that you will outright devastate a percentage of your customers, disrupt local economies, and leave a bad taste in the mouth of a handful of people. It might be profitable, but could you really claim to be a helper of small business?

When you fund EVERYONE, businesses with bad reputations can knock out competitors with good reputations, the cost of debt can harm more than it helps, or lenders can get skinned alive by defaults they never saw coming. We need to be aware that there are consequences to backing a business with a bad reputation because it can allow them to squeeze out the guys that would’ve actually had the most positive impact on a community. The counter argument may be the theory by the philosopher Adam Smith, a gentleman famous for promoting economic principles such that the pursuit of self-interest promotes the good of society. By this standard, if it’s good for the lender, then ultimately it must be good for the economy. However, allowing yourself to devastate a percentage of your customers isn’t good for the lender’s reputation even if it’s profitable. In a sense, pursuing immediate profit doesn’t mean pursuing ones self-interest. It may be months or years before enough unsatisfied borrowers begin to affect your reputation as a whole. Eventually, public opinion will sway. It’s happening to Wonga right now. If a lender’s business practices today could force them out of business in 5 years, then they are not pursuing their self-interest.

When you fund EVERYONE, businesses with bad reputations can knock out competitors with good reputations, the cost of debt can harm more than it helps, or lenders can get skinned alive by defaults they never saw coming. We need to be aware that there are consequences to backing a business with a bad reputation because it can allow them to squeeze out the guys that would’ve actually had the most positive impact on a community. The counter argument may be the theory by the philosopher Adam Smith, a gentleman famous for promoting economic principles such that the pursuit of self-interest promotes the good of society. By this standard, if it’s good for the lender, then ultimately it must be good for the economy. However, allowing yourself to devastate a percentage of your customers isn’t good for the lender’s reputation even if it’s profitable. In a sense, pursuing immediate profit doesn’t mean pursuing ones self-interest. It may be months or years before enough unsatisfied borrowers begin to affect your reputation as a whole. Eventually, public opinion will sway. It’s happening to Wonga right now. If a lender’s business practices today could force them out of business in 5 years, then they are not pursuing their self-interest.

Real predictions, not just hoping tomorrow’s financial standing will be the same as it was yesterday

I look forward to the day when a merchant lender announces a 3, 5, or 7 year program. Their underwriting analysis would have to be incredibly well thought out, but that’s not a bad thing. Borrowers shouldn’t be forced to choose between an 8 month loan and a 9 month loan because so few lenders are willing to make real long-term projections. A business might make good use of short term financing to pay for an aggressive marketing campaign, but the likelihood that they could “open a 2nd store” and pay back all of the money with interest in 4 months isn’t very good.

My advice to the merchant lenders that are flexing their hundred million dollar muscles right now? Don’t carpet bomb the entire country with loans and hope that a one-size fits all rate and term will have a positive impact on the economy. It won’t. Writing off a portion of your customers today as collateral damage will hurt your reputation in the long run. Some businesses shouldn’t be getting funded even if they have money in the bank and a history of revenue. Others can’t sustain such short term repayments. These things should matter not just in the context of how much it will impact profits, but how much it will impact communities.

Incorporating factors like trust and reputation don’t have to slow the application process down. There are technologies to help aggregate, sort, and make sense of these signals online. Automation and speed are good but the day that lenders stop caring about who they’re funding and why they’re funding them is the day that lending becomes inefficient. When it becomes purely a numbers game, we’ll be in bubble territory. Can you think of any other industries where lenders stopped considering whether or not the loans were good for their borrowers and played the numbers? I’m sure you can 😉

Incorporating factors like trust and reputation don’t have to slow the application process down. There are technologies to help aggregate, sort, and make sense of these signals online. Automation and speed are good but the day that lenders stop caring about who they’re funding and why they’re funding them is the day that lending becomes inefficient. When it becomes purely a numbers game, we’ll be in bubble territory. Can you think of any other industries where lenders stopped considering whether or not the loans were good for their borrowers and played the numbers? I’m sure you can 😉

Lend efficiently, be a good citizen, and don’t be afraid to place a value on what customers are saying about your applicants.

– Merchant Processing Resource

../../

MPR.mobi on iPhone, iPad, and Android

How The Facebook IPO Affects the Merchant Cash Advance Industry

May 18, 2012 Facebook went live on the Nasdaq earlier today, causing many people to become instant millionaires or billionaires. Yea…soo… how is this in any way relevant to Merchant Cash Advance (MCA)? you might ask. Well, because MCA is the next BIG thing. One of the major winners of the Facebook IPO is Accel Partners, a venture capital (VC) firm that invested $12.7 million in Mark Zuckerberg’s college networking website in 2005. Today, they’re cashing in on billions from that bet. Since then, Accel has repeatedly struck gold by backing wildly successful businesses such as Groupon and Etsy. Many hungry and jealous VCs are looking to jump into any industry Accel likes, to either compete for marketshare or to piggyback on the success.

Facebook went live on the Nasdaq earlier today, causing many people to become instant millionaires or billionaires. Yea…soo… how is this in any way relevant to Merchant Cash Advance (MCA)? you might ask. Well, because MCA is the next BIG thing. One of the major winners of the Facebook IPO is Accel Partners, a venture capital (VC) firm that invested $12.7 million in Mark Zuckerberg’s college networking website in 2005. Today, they’re cashing in on billions from that bet. Since then, Accel has repeatedly struck gold by backing wildly successful businesses such as Groupon and Etsy. Many hungry and jealous VCs are looking to jump into any industry Accel likes, to either compete for marketshare or to piggyback on the success.

And that’s how Facebook and MCA are related…

On February 7, 2012 Accel Partners invested $30 million into Capital Access Network (CAN), the holding company of AdvanceMe and NewLogic Business loans. There was some buzz about it in February, but it faded fast. It seems like every day there is a new press release from some MCA firm bragging about how they secured a mult-million dollar credit line. So it’s no surprise that industry insiders didn’t immediately poo themselves in hysterical awe of this announcement.

CAN is also on pace to fund $600 million this year, an astounding figure that makes $30 million sound like a mere drop in the bucket. It’s as if Accel gave them a Starter Advance. 😉

On a more serious note, the rest of the VC and Growth Capital world waited about 3 seconds before pouncing on all things MCA. The frequency in which we’re receiving random calls and e-mails from “investors” about putting money into MCA providers has increased dramatically. A few other funders and large ISOs have shared that they are experiencing the same thing. Right now there is a great chance that there are back room negotiations going on all over the industry between funders that already have millions and investors that have billions.

Raising capital has never been a real problem in the industry, as the Wall Street establishment has been funneling millions into the New York, California, and Florida MCA powerhouse providers for years. Do we really need Silicon Valley to jump into bed with us? Maybe. Although MCA has been around since the late 1990s, there’s been this lingering acknowledgment that most of the small business market that could benefit from financing still doesn’t know that MCA exists. Way too many business owners respond to an explanation of the MCA program with shock, “Wow, I never knew you could do something like that.” That’s a problem and it’s real.

Sean Murray, the founder of Merchant Processing Resource, recently did a presentation through the Manhattan Chamber of Commerce last month to 30 small business owners about MCA financing. The first question asked by one of the attendees after it was over was, “did you come up with this whole concept yourself?” He certainly did not, and it epitomizes that there is still room for exponential growth in a billion dollar industry that is more than a decade old.

Naysayers predicted that the MCA concept would fail years ago, and yet it has grown, mutated, and evolved. Some folks got into this business in their early twenties right out of college, and have literally made a career out of it. It’s quite a picture to see that they’ve grown up, gotten married, and had a few kids only to learn that Silicon Valley is picturing this entire industry as something still in startup phase. But hey, it took Pinterest years before anyone really noticed it.

In 2012, you can apparently still get in early on MCA. If you have stock in an ISO or funding provider, don’t be quick to sell it. It could be worth millions or billions in the future.

At some point in 2014, the Winklevoss twins will probably claim they invented Merchant Cash Advance, a challenge they will lose badly. Not even CAN, the company that did invent it, was able to prove in court that they did. But they did manage to continue their dominance of the industry and they are the ones that caught Accel Partners’ fancy. But the rest of the MCA players aren’t exactly going to wither away and die like MySpace. So the battle is on and there is money to be made.

Target valuation: $100 Billion. Who’s going to get there first?

– AltFinanceDaily

../../

Read how Merchant Cash Advance could be molded to be more like Silicon Valley: Just Call it a Coupon!

Merchant Cash Advance On Huffington Post / Just Call it a Coupon!

March 16, 2012An article was published by the Huffington Post today that explained the need for Merchant Cash Advance providers. Though some of it was described in an unflattering light, it conveyed some important messages.

- Real business owners explain that banks both big and small are not interested in lending to them

- One woman is quoted as saying: “If I ever write a book on how to open a restaurant, the first chapter is going to be ‘Banks Are Not Your Friends.'”

- A direct funding provider revealed that demand for merchant cash advances increased by 15 percent to 20 percent in 2011 and that 70% of businesses use more than 1 advance.

Our favorite line and perhaps the most important thing you can take away from this article is the quote by the CEO of AmeriMerchant. “[Merchant Cash Advance] is less expensive than [offering] a Groupon for 50 percent off or putting inventory on sale for 30 percent off.” Isn’t it ironic that the Groupon/e-coupon/social coupon concept is today’s business as usual and is at the same time significantly more costly than what the media considers to be expensive financing?

Our favorite line and perhaps the most important thing you can take away from this article is the quote by the CEO of AmeriMerchant. “[Merchant Cash Advance] is less expensive than [offering] a Groupon for 50 percent off or putting inventory on sale for 30 percent off.” Isn’t it ironic that the Groupon/e-coupon/social coupon concept is today’s business as usual and is at the same time significantly more costly than what the media considers to be expensive financing?

LivingSocial has 60 million members worldwide and they operate much in the same way that Groupon does. Let’s discuss this. According to wikipedia, Groupon’s business model works as follows:

For example, an $80 massage could be purchased by the consumer for $40 through Groupon, and then Groupon and the retailer would split the $40. That is, the retailer gives a massage valued at $80 and gets approximately $20 from Groupon for it (under a 50%/50% split).

So the 50% discount to the consumer is actually a 75% loss of revenue for the business owner. This practice is publicly accepted as fair, practical, and a way to increase your sales. If that’s the case, should’t financing that costs $2,800 to receive $10,000 be considered a bargain? We think so. Expensive is in the eye of the beholder. The media has a funny way of convincing people that a 75% discount is a great deal but financing costs of 28% are astronomical. Not to say that 28% is cheap, but there is only one reason that low rate bank loans even existed in the first place. The SBA is willing to cover up to 90% of the defaults and charge it to the taxpayers. That’s an advantage the rest of the private sector doesn’t get.

We can’t help but think what would be if the Merchant Cash Advance concept was rebranded as a powerful social marketing tool to drive sales. What if a Merchant Cash Advance provider purchased $12,800 of a store’s future sales in exchange for $10,000 today and then mass marketed that business to local consumers through mailing lists, iphone apps, and website ads to drive customers to the store. That would allow the Merchant Cash Advance provider to recoup their purchase as fast as possible and at the same time create viral growth for the business. The technology already exists and businesses are already willing to accept 75% losses. Isn’t it time they all started getting a lot more bang for their buck?

It’s not expensive when it’s spun that way is it? Sayonara Groupon and LivingSocial! Merchant Cash Advance is the sleeping giant at your doorstep.

– AltFinanceDaily

../../

The SEO War for ‘Merchant Cash Advance’

February 12, 2012 Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

In 2007, back when the industry hadn’t put much thought into the Internet, the #1 search result for Merchant Cash Advance was the blog by David Goldin, the CEO of Amerimerchant. It made sense because it was a self proclaimed “online resource dedicated to the merchant cash advance industry.” There, small business owners and competitors could read about the trials and tribulations of an industry on the verge of explosive growth. It was interesting, it was informative, and best of all, he ranked first without trying.

Nowadays, it’s all commercial. Merchant Cash Advance companies with fat advertising budgets are spending thousands to rank for their favorite keywords, with Merchant Cash Advance still high on that list. The friendly information resource has been replaced by a website that not only crushed the competition in search positioning but seems to publicly brag about it too.

As we write this article, the top 10 Google search results for Merchant Cash Advance are:

1. Merchant Cash in Advance

2. YellowStone Capital

3. Entrust Cash Advance

4. Merchants Capital Access

5. Merchant Resources International

6. American Finance Solutions

7. Nations Advance

8. Bankcard Funding

9. Rapid Capital Funding

10. Paramount Merchant Funding

Do keep in mind that your results may differ slightly depending on your region. Google geographically targets searchers to bring them the most relevant matches.

How much is the #1 spot worth? The market priced it at $75,000 three months ago when MerchantCashinAdvance.com was sold in an online auction for that amount (saved in pdf). So which powerful Merchant Cash Advance company unloaded their precious website? None. The owner of the site was actually an SEO guru looking to make a quick buck. He studied the industry a bit and then within two months ranked a site at the top of Google.

75k might even be considered a steal, as we were actually approached to purchase that website ourselves in August 2011. The exchange was a bit contentious, with them being unwilling to accept less than $200,000 and us making an insulting offer of $100. Perhaps it was jealousy or perhaps it was because we didn’t realize how a Merchant Cash Advance website could be worth so much, but the discussion quickly degraded into name calling and we never spoke again.

How many small businesses are searching for Merchant Cash Advance anyway? According to Google, there are 14,800 searches for it a month. We assume that at least 75% of those are from the companies offering it. You probably Google the phrases several times a day yourself. Admit it!

The real money is in the long tail keywords, since merchants are more likely to personalize their search. Being first for merchant loan for bad credit might be more potent than Merchant Cash Advance. It’s tough to say since AltFinanceDaily doesn’t really rank for either of those. Then again, we’re an information destination, much like David Goldin’s Blog was/is.

We’re not SEO experts, but we do quite alright with Google ourselves. Without giving away all of them, this is our current placement for just the following keywords:

- Merchant Cash Advance directory: 1, 2

- Largest Merchant Cash Advance companies: 1

- Merchant Cash Advance UCC: 1, 2, 3

- Merchant Cash Advance statistics: 1

- Merchant Cash Advance stats: 1, 2

- Merchant Cash Advance default: 1, 2

- Merchant Cash Advance UCCs: 2, 3, 4, 5

- Merchant Cash Advance laws: 2

- Merchant Cash Advance forums: 2

- Merchant Cash Advance articles: 3

- Merchant Processing: 3

- Merchant Cash Advance Jobs: 8

- Sell your mom for cash: 1 (don’t ask)

MerchantCashinAdvance.com was no different and they claimed to be #1 for over 300 business lending related keywords. A spreadsheet of the analysis they put up during the auction can be found here.

With nothing more than an organic search presence, they claimed to have had the following results:

Month of July for 2011: Received 647 calls & 148 online business lending applications: Funded 81 deals, $26,000.00 profit.

Month of August for 2011: Received 731 calls & 234 online business lending applications: Funded 113 deals, $29,500.00 profit.

Month of September 2011: Received 1026 calls & 276 online business lending applications: Funded 147 deals, $41,750.00 profit.

If that’s the case, then $75,000 was a bargain. That no doubt led to the auction of a similar site just a month later. MerchantCashAdvances.org is currently ranking 51st for Merchant Cash Advance. They claimed to earn $12,500 annually in ad revenue and $200,000 in commissions. The starting bid was $10,000 and although there were many inquiries, it didn’t sell.

That doesn’t mean it wasn’t worth the price. Most Merchant Cash Advance companies are secretly or not-so-secretly investing thousands into SEO campaigns. Black hat SEO is rampant and even the most reputable companies have engaged in it at some point. The underwriting room is the one they show their clients. The sales floor is the one they show their new recruits. But ask where the internet marketing room is, and they’ll claim it doesn’t exist. But it does of course. They’re usually small quarters with no windows that are filled with computers armed with software like ScrapeBox, Article Marketing Robot (AMR), XRumer, and a list of working proxies.

Even the white hats are building backlinks manually and creating endless articles for use on their own company blogs or for services like BuildMyRank. One moderately sized Merchant Cash Advance company in New York City has just as many SEO employees as they do sales representatives. For some, this is just the beginning. It’s not unusual to spend $10,000 – $20,000 a month on pay-per-click campaigns.

The Internet has become a place where the person with the most to spend wins. Because of competition, a paid Google campaign for Merchant Cash Advance keywords can cost $20 per click! We did a phone call with Google and were told that less than 10% of clickthroughs convert into a sale or completed form. If only 1 out of every 10 visitors calls or inquires through the site, that amounts to $200 for a single lead. If only 1 out of every 5 of those leads turn into a closed deal, the acquisition cost is effectively $1,000. That number is awful especially considering commissions and factor rates have been rapidly declining over the last year. And merchants wonder why this financing is more expensive than a bank loan…

It also explains why the practice of closing costs and service fees have survived internal industry scrutiny. Some resellers would be operating in the red without them. Organic traffic is in essence free, that is if you don’t consider the salary or fees you pay your SEO team. Hopefully they don’t overdo it and place your site in the Google sandbox. Until then, the rewards outweigh the risks and every day the industry pushes the envelope a little further in the quest to rank on page 1.

If you can earn $200,000 a year from a website or sell one for $75,000 after two months of work, then there is plenty of room for growth. If the industry was saturated, it wouldn’t be that easy. If your mother is getting into the Merchant Cash Advance business, make sure she knows how to market her website. It’s a war out there.

– AltFinanceDaily

../../

Does Your Mom Sell Merchant Cash Advance?

February 4, 2012Five years ago, everyone seemed to add the phrase, “but I also do mortgages on the side” in response to questions about their career.

“I’m a stockbroker, but I also do mortgages on the side.”

“I’m a school teacher, but I also do mortgages on the side.”

“I’m a stay at home mom and a loving wife, but I also do mortgages on the side.”

Times have changed and today the new side gig is reselling Merchant Cash Advance (MCA), at least in the New York metropolitan area. The Independent Sales Office (ISO) model is dissipating into a few thousand sole proprietors, all of whom are competing for the same prospects. Most of them started at one of the larger ISOs or funding sources and have over time traded it for the opportunity to work for themselves. Others have pushed it aside as a part time gig while earning a living in another line of work.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

And yet, I haven’t heard many complaints from independent agents, which may mean the MCA industry is far from over-saturated. Sixteen of my former co-workers have gone on to start their own MCA ISOs. I even know a pair of twin brothers that run ISOs independent of each other. Some of these newly formed mini-ISOs (less than five people) break apart and each member seems to go on and repeat the cycle.

The Derailing of the Shakeout

In early 2008, it was predicted that low budget marketing would cause a massive shakeout of MCA resellers. David Goldin, the CEO of AmeriMerchant published the following in his blog:

There is another train of thought that is inevitable to fail – those that thought they can sell business cash advances with minimal capital expenditure, meaning hiring unqualified salespeople using inexpensive marketing techniques such as voice broadcasting (with these providers giving the same data to 100s of phone rooms) to dial hundreds of thousands of businessses an hour with a prerecorded message. (Merchants around the country are getting 3 – 5 prerecorded calls a day). The challenge is the quality of anyone that is going to press ‘2’ on their phone for money tends to be “lower hanging fruit” and lower quality deals. With the recent credit crunch and many merchant cash advance funding companies tightening up, some merchant cash advance agents were seeing approval rates as low as 15%-20%. There is no way they can survive and stay in business with that kind of approval rate.

Back then, it was quite popular to have a hundred sales agents in a single room making phone calls. Overhead was the biggest part of the budget, which in places like New York City, could consist of tens of thousands of dollars in rent alone. Add that to all the money that was spent on technology, payroll, dialers, and commissions, and it became really easy to generate a net loss.

With the emergence of mini-ISOs, many are foregoing traditional overhead expenditures such as the renting of a centralized office. Technology costs are also being eliminated since most people already own a personal computer and a cell phone, the only two tools really necessary to interact with prospects. As for state of the art auto dialers? Well, many agents are completely fine using inexpensive resources such as phone books or public UCC filings. Ask around in the MCA industry and you’ll learn just how prevalent this practice is.

There are so few barriers to entry in the MCA industry, that it catches a lot of folks from other financial fields off guard. We receive a dozen e-mails a month from mortgage brokers, stockbrokers, and insurance agents asking what licensing requirements they will need to sell MCA. There are none of course, but they more are shocked to learn that there are no regulations to abide by either. Take your cell phone, throw in your e-mail, spend twenty bucks on a website and you’re an official MCA reseller! It’s just that easy. Thousands of people are getting in on it.

Who is Who?

The flood of resellers and fly-by-night agents is making it increasingly difficult to know where all the MCA money is actually coming from. Here on the Merchant Processing Resource’s website, we’ve created transparency by listing the largest direct funding providers. Need to know if that UCC filing is MCA related? We can help you with that too.

We’re also working on creating an official directory of resellers, for which there will be some requirements for inclusion. That means if you’ve e-mailed us on this topic already and you haven’t heard from us yet, be patient. You will be contacted soon with instructions on how to become an approved MCA reseller.

Consolidation

In the meantime, the increasing fragmentation also presents an incredible buying opportunity. Large ISOs that are looking to add to their portfolios and leverage the brand names that mini-ISOs have created should be able to buy them out at very affordable prices. When this practice starts to happen, it’ll be interesting to see what the market value of mini-ISOs are. Could a business owned by two individuals with a pool of two hundred clients be worth $50,000? $100,000? $300,000? Once someone sets the bar, we should prepare for a year of consolidation, and the little guys will get gobbled up by the big ones. A lot of folks could end up walking away very rich or disappointed. Perhaps now is a good time for your Mother to go into the MCA business for herself and flip the value created for a nice profit a year from now.

ISOs on Steroids

The popularity of co-funding or syndication is also allowing the remaining large ISOs to really flex their muscles in a way they weren’t able to in 2008. Syndication is where an ISO is able to invest their own capital in the MCA deals they close. For instance, on an advance of $20,000, $15,000 of it might come from the MCA funding source, and the remaining $5,000 from the ISO themselves. As long as these accounts perform well, syndicating can create a supernatural rate of growth. This further whets the appetite for opportunities to expand.

So why are mini-ISOs a buying opportunity? Customer loyalty is something big companies can’t always shake, no matter how much is spent courting them. Furthermore, these mini-ISOs tend to have historical performance records on their clients, data that is incredibly valuable. Should a Super ISO invest $20,000 in a small business that has never used MCA before or should they invest it in a business that has responsibly used MCA for two years with no issues, exhibits fierce loyalty, and has a proven record of success? The opportunity to participate in funding that business now and repeated times in the future should be worth a lot.

The Unknown

There are other forces at work that may reshape the industry in a way we can’t predict. The incredible rise of micro-lending is cannibalizing the MCA market, but is also allowing ISOs to offer a variety of financial products to a larger pool of businesses. One New York City MCA funding source privately revealed that micro-loans now make up 80% of their monthly funding volume, a stunning shift from their MCA-only portfolio of 2010.

The growing popularity has also caught the attention of regulators and in some states, the purchase of future credit card receivables is being governed by existing lending laws. The day may come when every agent needs a license to sell, but until then, thousands of people are playing the biggest game in town, helping small businesses get funding to grow. Are you a part of it?

– AltFinanceDaily

../../