Broker Business Planning – Selecting the Right Lenders

May 10, 2015Continuing The “Year of the Broker” Discussion

2015 is certainly the “Year of the Broker,” as the low barrier to entry into our space, in conjunction with various recruiting advertisements promising lucrative pastures, is attracting a variety of individuals with various levels of professional backgrounds. Some entrants have prior experience as a mortgage broker, insurance agent or banking specialist, while others are less familiar with professional sales and are under the belief that our space welcomes a lucrative introduction. Nevertheless, I believe that new broker entrants must be reminded that this is an entrepreneurial pursuit, rather than a get rich quick procedure, and efficient business planning will play a major part in the success or failure of your venture. A part of this efficient business planning, other than the basics of good resources for accounting, legal, marketing, market research, and financing, is the strategic selection of your lender partnerships. The right partnerships will grow, develop and sustain your business, but the wrong partnerships could add your entrepreneurial pursuit to the list of business startup failures.

2015 is certainly the “Year of the Broker,” as the low barrier to entry into our space, in conjunction with various recruiting advertisements promising lucrative pastures, is attracting a variety of individuals with various levels of professional backgrounds. Some entrants have prior experience as a mortgage broker, insurance agent or banking specialist, while others are less familiar with professional sales and are under the belief that our space welcomes a lucrative introduction. Nevertheless, I believe that new broker entrants must be reminded that this is an entrepreneurial pursuit, rather than a get rich quick procedure, and efficient business planning will play a major part in the success or failure of your venture. A part of this efficient business planning, other than the basics of good resources for accounting, legal, marketing, market research, and financing, is the strategic selection of your lender partnerships. The right partnerships will grow, develop and sustain your business, but the wrong partnerships could add your entrepreneurial pursuit to the list of business startup failures.

The selection of your lender partnerships will depend on your unique value proposition (UVP). No entrepreneur should begin a pursuit without a well-defined UVP, for your UVP is the foundation of all of your business planning and return on investment forecasts. Your UVP should answer this question:

Understanding my market segment, what is it specifically that I will bring to the segment that isn’t already being provided by the current crop of solution providers?

The question includes three main components that must be addressed:

- The identification of a market segment

- The characteristics of all services within your industry, being sold to that market

- The services that you will uniquely provide to said market and their unique characteristics

Once your UVP is set, now it’s time to look into the selection of your Lender Partnerships.

Once your UVP is set, now it’s time to look into the selection of your Lender Partnerships.

To begin, let’s say that you decide to come into the industry and target start-up retail/restaurant businesses, that is, those with less than 1 year in operation. Because you are selling working capital solutions, you would research all available working capital options to this market segment which include sources such as nonprofit loans, business credit cards, personal savings, loans from retirement accounts, friends and family, equipment leasing, and merchant cash advances. To serve this market segment efficiently, you would choose to offer merchant cash advances and equipment leasing.

Next, you would scroll through all of the direct lending sources in the country that provide the working capital solution you have decided to lead with, but who also specialize or at least “serve” the target market you are seeking. Many equipment leasing companies do not fund businesses with less than 2 years in business, and many cash advance companies do not fund companies with less than 1 year in business. Your goal would be to find these lenders and create that network, negotiate pricing, workout your commission schedules, and verify all aspects of said partnership to make sure that it’s beneficial for your clients and your office. It should be a win-win-win partnership, a win for your clients as they find a source for working capital that they didn’t know existed, a win for your partner as they obtain “feet on the street (or telephone)” reps without having to pay their overhead, and a win for your office as you are allowed to serve your market and be paid well in doing so.

Due Diligence Is Key

When finalizing your lender selections, make sure all forms of due diligence are completed on the lender(s) to verify their credibility and competency. These forms of research include all of the following:

(( Structure and Legality ))

- The lender should be a licensed direct lender (in states where necessary).

- The lender shouldn’t be a start-up, but instead a proven entity with at least 2 years of operation.

- The lender should have at least directly funded volume in the eight digits (over $10,000,000).

- The lender should have a full staff of employees rather than just one person.

- The lender’s customer service and support departments should be easy to reach.

- The lender should have some sort of press or news media releases on its establishment.

- The lender should specify if they are going to do advances or loans or both.

- The lender’s funding agreements should specify if the transaction will be an advance or loan.

(( Online Presence ))

- The lender should have a fully functional business website, registered for at least two years.

- The lender should have a business email from their business website domain.

- The lender should be BBB Accredited (www.BBB.org) with at least an A rating.

- The lender should be a part of business associations with logo(s) displayed on their website.

- The lender should be included on basic online business directory listings.

(( Broker Respect ))

- The lender should provide a comprehensive Broker Agreement full of legal provisions.

- The lender’s Broker Agreement should spell out all provisions of the relationship.

- The lender’s Broker Agreement should spell out any quotas.

- The lender’s Broker Agreement should spell out new/renewal deal commission structure.

This is a rough introduction and surely there are other criterion that are important in selecting your lender partnerships. However, these recommendations will surely give you a head start as you head into one of the most competitive industries in financial services.

Is Alternative Lending An Illusion? (LendIt 2015 Summary)

April 18, 2015More than 2,400 people packed into the LendIt conference last week in New York City and everywhere you turned, startups were boasting of their ability to lend billions of dollars to underserved consumers and businesses. Companies not even old enough to have attended last year’s LendIt conference had reportedly lent tens of millions or hundreds of millions of dollars already. Is it all an illusion?

Investors circled like hawks to try and grab an opportunity into this exploding market. Alternative lenders were practically being tackled by VCs, Private Equity firms, and specialty finance lenders:

Technological innovation is disrupting the status quo, attendees echoed. Surely banks can afford to develop new technology to compete, so why haven’t they? Lendio’s Brock Blake wasn’t afraid to challenge the Short Term Business Lending Panel on this. “Is there real innovation happening or is there regulatory arbitrage?” he asked.

The panelists mostly agreed that it was a combination of both. Stephen Sheinbaum, founder of Merchant Cash and Capital (MCC) and BizFi, said “regulation is not something that scares us in any way.” That’s not surprising considering MCC has survived more than ten years in business and fellow panelist CAN Capital has survived more than seventeen.

But for the newer players entirely reliant on third party brokers or dependent on a Reg D exemption to issue securities, their success may indeed be regulatory arbitrage. And time is on their side.

Karen Mills, the former head of the Small Business Administration asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

It’s the brokers that worry some folks most, an issue that PayPal and Square Capital do not have to contend with at all. OnDeck CEO Noah Breslow stated, “there is always going to be a set of customers that want to shop and want to have help.”

Kabbage’s Kathryn Petralia explained that only 2% of their business comes from brokers and their fees are capped at 4%. CAN Capital’s Jason Rockman argued that it’s about working with brokers that share their values. MCC’s Sheinbaum said, “you have to be willing to not do business with some of the unscrupulous players out there.”

But while these industry captains minimized the role that brokers play, 2015 is already being dubbed the Year of the Broker.

The regulatory environment isn’t the only issue to be worried about, skeptics argued. There was cautious alarm about the market’s viability when interest rates rise or the economy takes a turn for the worse.

“I think there’s going to be a shakeout,” said Steve Allocca of PayPal. MCC’s Sheinbaum explained that when he sees other funders doing deals that don’t appear to make sense, to not feel pressured to do them as well. “Stick to your disciplines. Stick to your guns,” he preached.

Fundation CEO Sam Graziano argued that small business lending is already very risky. The lifetime default rate on 7(a) SBA Loans is 20%, he said. Graziano, who hates the term alternative lending prefers to refer to the industry as digitally enabled lending.

And digitally enabling is something that OnDeck has focused on. In Breslow’s presentation, he said that applying offline for a loan takes 33 hours of work on average. Banks are shuttering branches at a record rate, he added.

Banks are dead, said many in attendance. Kathryn Petralia of Kabbage disagreed. “The death of banks has been greatly exaggerated,” she argued on a panel.

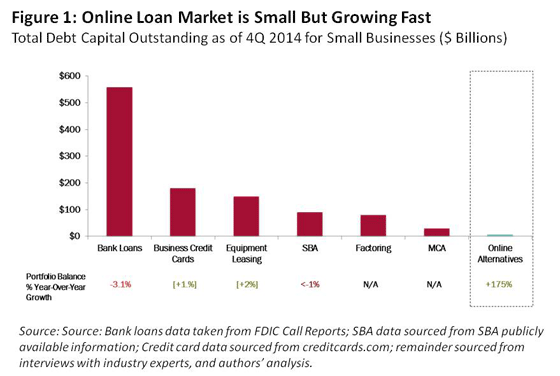

Indeed, Mills’ report shows that total outstanding debt on business loans by banks dwarfs the alternatives by more than 50 to 1.

But former U.S. Treasury Secretary Larry Summers is convinced the tide is turning.”The conventional financial sector has, in important respects, let all of its main constituents down over the last generation, and technology-based businesses have the opportunity to transform finance over the next generation,” he said during the keynote speech.

With conference sessions looking and feeling like a cramped NYC subway during rush hour, the popularity of alternative lending is no illusion.

But healthy skepticism is at least creeping in while the industry marches forward. Changes in regulations, interest rates, and economic activity will separate those simply riding a wave from those that have created something real. Expect companies that exhibited at this year’s conference to be gone by 2016 or 2017, said several panelists.

The final count of LendIt attendees was 2,493 people. 150 people who tried to register at the last minute were turned away. More are expected to attend next year.

Objectively, alternative lending appears to be very real.

Good Recordkeeping Plays Important Role in Funding Success

April 17, 2015CPA Yoel Wagschal recently started working with a syndicator who relied on Excel spreadsheets to track all his deals. The syndicator thought he had everything in tip-top shape, but it turns out that his system was hard for an outsider to understand and the data didn’t reconcile with his bank statements.

Wagschal, who heads an accounting firm in Monroe, New York, comes across this problem frequently these days. It’s been exacerbated by the exponential growth of the alternative funding industry in recent years. There are a sizeable number of alternative funders that started out small and have grown by leaps and bounds, yet they are still using rudimentary systems to keep track of their business dealings. In most cases, funders want to do the right thing, but they don’t always know how or the extent of what’s involved. Unknowingly these funders may be setting themselves up for financial or legal troubles.

“Sooner rather than later you are going to find yourself swimming in the Atlantic Ocean without any plan on how to get out of there,” Wagschal says.

“Sooner rather than later you are going to find yourself swimming in the Atlantic Ocean without any plan on how to get out of there,” Wagschal says.

Although newbie funders may be able to get by with simple tools and minimal staff, more sophisticated efforts are required once they are doing multiple transactions a month. It’s one thing when you are tracking a few daily deals on a spreadsheet. It’s quite another when you’re trying to keep track of all the moving parts for hundreds of deals.

What’s more, there’s a lot of slicing and dicing of data that goes into properly understanding your existing business and growth possibilities. If you don’t use the right tools to help you keep precise records, it’s nearly impossible to understand the fundamentals of your business in order to grow. Excel, while a useful tool, has its limits, and funders who rely exclusively on spreadsheets don’t get the benefits of other more sophisticated options that have become available to them in the past few years. Manually entering data also increases the possibility of human error, which can lead to thousands upon thousands of lost revenue for a funder’s business.

The Pitfalls of Not Keeping Good Data

Keeping good data is especially important to funders who want to take on additional investors or who are considering a sale at some point. Kim Anderson, chief executive of Longitude Partners Inc., a strategic advisory firm in Tampa, Florida, works with a number of funders that are looking to facilitate additional growth by bringing on outside investors. Many of these companies find themselves scrambling because they don’t readily have access to the kind of information potential investors want.

Not keeping good books can also inhibit a funder’s ability to expand into additional markets. Say a funder wants to introduce a new product or migrate a product offering to a different vertical. Companies that don’t analyze their data effectively may have a hard time understanding what part of their existing portfolio would be the most appropriate or profitable segment to introduce the product to, Anderson says.

Potentially impeding growth is bad enough, but funders that don’t keep proper books can also find themselves embroiled in legal or tax troubles. Some MCA providers, for instance, have faced stiff penalties for treating transactions as loans on their books instead of the purchase and sale of future income.

“If they are showing the revenue recognition in the exact same way that loan industry companies are doing, then they are setting themselves up to be judged in the same way that a loan company would,” says Christina Joy Tharp, a staff accountant in Wagschal’s office. If you’re using the same accounting methods as lenders, you could be deemed a predatory lender by multiple enforcement agencies, even if that’s not your intent, she says.

The strength of your business can also be significantly impacted by how you classify performing and nonperforming loans or receivables. “There are thousands of pages of rules on how banks have to classify performing and non-performing loans. None of that exists for this industry, which is completely unregulated,” says Alex Gemici, managing director and head of M&A at World Business Lenders, an alternative lending company in Manhattan.

As a result, funders don’t have a universal way of keeping their books. Many funders believe that as long as they are collecting sporadic payments, a loan or receivable should be classified as performing. Gemici strongly disagrees, saying this approach sets up a funder for potential failure given that the default rate for loans/receivables is about one in five. “It’s one thing to show on your books that loans or receivables are performing, it’s another when you run out of cash,” Gemici says.

Choosing an Outside Provider

Recognizing that Excel spreadsheets can only carry a funder so far and that out-of-the-box software probably won’t be a complete solution for alternative funders, a small number of companies have stepped up to provide customized solutions for the industry. MCA funders—where the perceived need is greatest—are a particular focus for these providers.

Benchmark Merchant Solutions, a processor in Amherst, New York, is one such company honing in on the MCA funder space. In 2014 the company launched MCA Track, software that’s designed to help MCA funders with their recordkeeping needs. It also helps them keep track of their income for tax purposes.

Benchmark Merchant Solutions, a processor in Amherst, New York, is one such company honing in on the MCA funder space. In 2014 the company launched MCA Track, software that’s designed to help MCA funders with their recordkeeping needs. It also helps them keep track of their income for tax purposes.

Among other things, MCA Track allows funders to view their performance at a glance. It shows them, for example, how merchants are performing, how the funds are allocated according to syndicator, the status of a deal, open cash advances, closed cash advances and defaulted cash advances. Funders can also get profitability data and other types of big picture information about their business as well. The software costs about $2,000 a month depending on the user’s size.

Benny Silberstein, chief operating officer of Benchmark, says the software was created because the processing company found that funders were often asking Benchmark to get data for them, especially when there were discrepancies. It can be real headache for funders to wade through inconsistencies with merchants, syndicators and ISOs, Silberstein says. “I can’t begin to tell you how many times funders asked us for a list of all the payments they’d received.”

PSC of Port Washington, New York, is another company trying to help MCA funders keep better records and manage their business more effectively. For a monthly membership fee, the company offers a front-end to back-end relationship management solution that allows funders to track all their contacts, documents, deals and commissions. Daily reports provide detailed data and summary information about an MCA’s funding business. The data includes the actual advance amount, the right to receive amount, the factor rate, processing fees, daily debits and credits, commissions paid to outside brokers or their own people, other management fees, ACH fees, wiring fees, payments, missing payments, collections information and participation with other syndicates.

The product has been on the market for about two years and the monthly fee varies according to a funder’s size, says Tom Nix, director of sales for PSC. He declined to be more specific about cost.

“The companies that are small and just starting out—if they are just doing a few transactions a month—they could probably get by using a spreadsheet. But that’s only feasible if you have a few transactions that you’re doing per month. Once you’re growing, when you get up to 10, 20, 30, 100 deals, the management of data becomes truly uncontrollable,” says Nix, who has seen a number of funders struggling to stay afloat or exit the business entirely because of their inability to keep good records.

“If you don’t have the right information and understand it, you’re going to give money to someone and you won’t [necessarily] get it back,” Nix says.

It’s possible for funders to set up their own infrastructure, but it can be costly and some feel it detracts from their ability to generate new business. That’s why Anthony Mannino, president of Nulook Capital in Massapequa, New York, chose to work with PSC. He researched the idea of doing all the back office and data collection on his own, but he decided not to reinvent the wheel since it would have meant hiring additional staff and would divert the company’s attention away from its primary focus—bringing in new business.

“A service provider like PSC gives us the ability to grow our company controlled and in a much quicker manner than we ever could than if we had to build our back end on our own,” Mannino says. “It takes most of the responsibility off of my company so we are able to focus on just growing the business and growing the sales.”

CloudMyBiz Inc. in Los Angeles is another company trying to service the alternative funder market, providing customized CRM systems for both lenders and MCA providers.

The CloudMyBiz system relies on a platform called Salesforce and is customized to the funding industry. It helps funders with the various facets of origination, underwriting and loan servicing. It helps them generate and track leads, automate funding workflow, understand and manage their deal pipeline and daily funding activities, collect and schedule recurring ACH payments and track syndication partners.

You could buy the Salesforce software and use it out of the box, but it provides only the basic functionality that funders need to run their business properly, says Henry Abenaim, principal consultant at CloudMyBiz. That’s where CloudMyBiz comes in by customizing the software for a funder’s specific business requirements. The fee varies widely, depending on the funder’s specifications, he says, declining to be more specific.

About two and a half years ago, Creative Vision Studio LLC in Long Beach, Calif., which had focused on the merchant credit card processing industry for more than a decade, also started offering a CRM system to MCA providers. The software is called Bankcard Pros CRM and customers can use it for merchant credit card processing, MCA or both. The software automates the data entry, underwriting, approval, funding and payback process from start to finish, says Robert Hendrix, the company’s chief executive. Funders also have access to 17 different management reports so they can track the performance and profitability of their entire portfolio per month.

The company charges an upfront fee of $4,000 to $5,000 to use the software, which is customized to a particular client’s business. There’s a $399 monthly fee after that. While it may seem costly to some funders, Hendrix says the software pays for itself within a month because of the efficiencies created. Importantly, the software eliminates the possibility of costly human mistakes that can occur in manually updating daily payments on a spreadsheet. “One little mistake can cost funders $2,000 to $3,000, even up to $10,000. They can be very costly mistakes,” he says.

It is, of course, possible for funders to keep good books and records using homegrown systems and personnel, and funders need to carefully weigh their options, taking into account that doing it right will probably require a meaningful investment in infrastructure and personnel. Whether they do it alone or hire an outside vendor, the important thing for funders is to collect the data and be able to evaluate it and display it in a way that makes sense to them, their customers, tax preparers, potential investors and others who need access.

Funders also need to remember that being successful in the business over the long term requires them to do more than simply capture accurate data. Beyond that, funders need to be able to manipulate the information in a way that helps them understand the nuts and bolts of their specific business, says Anderson of Longitude Partners.

“They may be able to produce enough financial information to complete an accurate tax return, but when it comes to understanding their operating metrics, they may not have collected or evaluated all of the right information to answer questions about what really drives the growth or sustainable profitability of the business,” he says.

From Lowes to Loans: Meet William Ramos

April 12, 2015Non-bank financing changed William Ramos’ life. Not as a borrower, but as a mover and shaker in the competitive world of financial deal-making. As an ambitious 20-year old, Ramos was working at both Lowes and ShopRite to try and put himself through Staten Island Community College. These were stepping stones, he told himself. He was dedicated to bettering himself, or more aptly to be the best at whatever he did.

Already on a path to success, he found himself growing impatient. The life of two jobs and school was a slow grind. Ramos wanted to do something big. He wasn’t sure what it would be, but he was confident that his attitude combined with his strong work ethic would eventually lead him to great success.

And so one day, he made a promise to himself to go out and find that big thing rather than wait for it to find him. It’s a bit of an American Cliché to say that his lucky break coincided with a sudden bout of adversity, but that’s exactly how it played out. Raised in the tough neighborhood of Brownsville in eastern Brooklyn, he didn’t have the connections to step right into the business world. Instead, Ramos had to start his search on the ground floor with millions of others on Craigslist.

His luck began with an interview for a job in telemarketing, a role that meant being connected to an autodialer nine hours a day as an opener. Undeterred by the challenge, Ramos had a feeling that this is where it would all begin. “I’ll do it,” he said.

There was only one problem, they didn’t want to hire him. The firm, which sold mostly financing products to small business owners, was very selective, even with cold callers. His interviewer at the time, who later became his boss, confirmed to me that he didn’t think Ramos was the right fit after they first met. But Ramos was determined to change his mind.

After calling the firm repeatedly over the next week to convince them that he was up to the task, they finally acquiesced. It didn’t mean he was in. It just meant it was time to put up or shut up. “They gave me a three-day trial period,” Ramos said.

After calling the firm repeatedly over the next week to convince them that he was up to the task, they finally acquiesced. It didn’t mean he was in. It just meant it was time to put up or shut up. “They gave me a three-day trial period,” Ramos said.

His former boss confirmed this relentless persistence.

39 working hours, 3,000 calls, and 3 days later, Ramos brought in two deals, one for $100,000 and another for $35,000. They both went through.

It was more than good enough to survive the trial and he was offered a job to work full time.

With a starting compensation of only $250 a week + commission, he still had a long way to go. “I would be the first one in and last one out,” Ramos shared with me. “I kept my head down and I wouldn’t leave my seat unless I needed to use the bathroom or eat. All I would do is make my calls.”

His former boss explained to me that Ramos had a knack for bringing in the firm’s larger deals even from the very beginning. He was too junior early on to be making a lot of money, but they were very focused on developing his skills. The firm saw his potential and was committed to nurturing him.

Within the first three months he managed to save $700 and he used it to buy a Mercedes-Benz C240 from a co-worker. After a life of taking the bus to work, Ramos had reached his first milestone of success.

While it was obvious that he still harbors pride in that first car, it sadly became all that stood in the way of homelessness. He had sacrificed everything for this job including college. Unfortunately there would be just one more thing to lose.

Adversity struck when a series of unfortunate events suddenly left him without a place to live. Ramos’ car was now both his ride and his home, though with the long hours he was putting in at the office, he might as well of lived at his desk. His boss took a special interest in his life and soon discovered just how much his young protégé was struggling.

“He was literally sleeping in his car,” his former boss told me. “I offered to let him sleep on my couch or at the very least let him stay in the office,” he added. Ramos took him up on the latter and began sleeping at the office. At the same time his commission percentage was bumped up, which sweetened the potential and only encouraged him to keep going.

Always looking for an edge, he sometimes pretended to be a customer himself. “I would call up lenders as a merchant to hear what pitches their sales teams were using,” he said. “I would then take that pitch, tweak it and make it my own.”

Always looking for an edge, he sometimes pretended to be a customer himself. “I would call up lenders as a merchant to hear what pitches their sales teams were using,” he said. “I would then take that pitch, tweak it and make it my own.”

Soon he was regularly closing more than $500,000 a month in deal flow and his financial situation and lifestyle began to improve significantly. A little more than a year later, Ramos had risen up to become a sales manager and was overseeing a team of five members.

Now some people in his shoes might’ve decided not to press their luck. He had taken a major gamble and it had paid off, so why do anything to jeopardize it?

But Ramos didn’t leave everything behind to settle for pretty good and a middle class lifestyle. After two years, he gave his boss and mentor some bad news.

“I’m going off on my own,” he explained. They parted on amicable terms and to this day still do business with each other. Ramos’ last commission check there was for $15,000, an amount he had never imagined back in his Lowes days.

In 2013 he founded Supreme Capital Group, a firm that primarily brokers merchant cash advances but will fund A paper deals on its own. With only two years in business, they are already on pace to generate more than $1.5 million in revenue over the next 12 months. He excitedly recalled a recent deal that generated $66,000 in commission. And that was just one deal!

He attributes part of his success to strong organizational skills. “I don’t think brokers realize how important keeping track of all their data is,” he said. He went on to explain that he can email the list of all his old leads and turn that into six to ten closed deals easily. He doesn’t have to work as much as he used to, but he still does.

With 10 callers working for him now, he’s not content with just being the boss. “I am still currently pounding the phones, doing email marketing, and sending out mailers,” he said. “We use the mailers to follow up with merchants, and we get a great response from it,” he added.

After working incredibly hard for several years, Ramos has at least found the time to play hard too. In the summer of 2014, he had made enough money to buy a white Maserati GranTurismo MC Sport Line, of which he shared several photos with me. He’s since upgraded to a 2013 Ferrari California in a color he described as Pepsi blue. And while that might be the kind of car some people would dream of sleeping in, Ramos has said those days are long over.

After working incredibly hard for several years, Ramos has at least found the time to play hard too. In the summer of 2014, he had made enough money to buy a white Maserati GranTurismo MC Sport Line, of which he shared several photos with me. He’s since upgraded to a 2013 Ferrari California in a color he described as Pepsi blue. And while that might be the kind of car some people would dream of sleeping in, Ramos has said those days are long over.

He just bought a house in Mesa, Arizona where his fiancée grew up and he plans to relocate his office there. “It’s already in the process of being built,” he said.

Ramos is now just 25 years old. He said he regrets not finishing school and he plans to go back. But he wouldn’t change everything that happened to him. He stressed more than once that asking questions is something he considers to be very important to success, especially in the business he’s in. “For all the newcomers in the industry, my advice would be to work hard and ask a lot of questions,” he said.

He was certain he had found the right opportunity almost from the beginning. “I knew that if I made those commissions the first week that I could make more,” he said.

It wasn’t easy.

William Ramos is the President of Staten Island, New York-based Supreme Capital Group.

Search Engine Lead Generation Is Probably Rigged

March 21, 2015 Hoping to do some nifty SEO to boost your site to the top of search results for valuable keywords? Don’t bother. In August, 2014, I presented six signs that alternative lending is rigged, at least as far as search was concerned.

Hoping to do some nifty SEO to boost your site to the top of search results for valuable keywords? Don’t bother. In August, 2014, I presented six signs that alternative lending is rigged, at least as far as search was concerned.

Two days ago, the Wall Street Journal ran a story that exposed a confidential FTC report on Google. The article opens with, “Officials at the Federal Trade Commission concluded in 2012 that Google Inc. used anticompetitive tactics and abused its monopoly power in ways that harmed Internet users and rivals, a far harsher analysis of Google’s business than was previously known.”

The conclusion? Google indeed skewed search results to favor its own services.

The 160 page report that the WSJ draws its analysis from was not supposed to be made public. Only a handful of pages are presented on the WSJ’s website in their entirety. Below are two of them:

Though I cannot find the specific comment anymore on LinkedIn, one of the responses I received on my August post regarding Google’s search results came from a former Google employee. They informed me that my suspicion was preposterous and that Google would never ever manipulate results.

While I made no effort to assert my evidence as anything more than circumstantial, the outright dominance of Google-owned lending companies for high value lending keywords was impossible to ignore. The WSJ story adds fuel to this fire.

Admittedly, the WSJ story doesn’t mention lending, nor do I think lending keywords were a subject of the FTC report (There are 156 pages the WSJ didn’t share). What I think is compelling here is a conclusion that Google did indeed manipulate results and penalized competitors to favor its own financial goals.

Despite the findings, the FTC ultimately did not bring any action against Google.

Is the game rigged? I feel a little bit better about saying, yes. Don’t put all your eggs in the SEO basket.

Merchant Cash and Capital Hits a Billion Dollars

March 18, 2015I was there. In August 2006, a little startup in College Point, Queens hired its third and fourth employees. One of them was me. The company’s CEO Steve Sheinbaum hired us to be underwriters of a financial product that at that point didn’t really have a name. It would later become referred to as a merchant cash advance.

The company grew fast, almost too fast. By December of 2006, half of the company was working out of temporary offices in the Empire State Building. And when that no longer made sense, we leased a floor at 450 Park Avenue South in mid-2007 where Merchant Cash and Capital still has its headquarters today.

Fast forward to 2008, I was the most senior risk manager of the firm. As the Director of Underwriting, my direct reports were two underwriting managers. Below them were three or four team leaders. And below them were entry-level underwriters and their administrative assistants. I oversaw what was arguably the most important department leading up to the financial crisis. I really believe the hard work of all the underwriters and the seriousness of which they took their job is a huge contributing factor to why MCC survived when many of their competitors did not.

It is great to see them hit the milestone of $1 billion in funding. Congratulations.

Advice to New Loan Brokers, ISOs, and Funders

February 24, 2015 Some words of wisdom to avoid having a bad experience in this industry:

Some words of wisdom to avoid having a bad experience in this industry:

1. If you can’t afford a lawyer, don’t be a funder. This is a litigious business and despite the myth that commercial financing is unregulated, there are plenty of ancillary laws to adhere to. States, FTC, OCC, IRS, etc.

2. Have a lawyer review your contracts (merchant agreements, ISO agreements, syndication agreements, etc.) If you can’t afford one or don’t want to take the time to do it, this business might not be for you.

3. Don’t send your deal to someone with a free email address (yahoo, gmail, hotmail, etc.).

4. Don’t send your deal to some random company just because they posted something on a forum, LinkedIn, or somewhere else. Check them out on Google, ask other forum members to vouch for them. Be extremely smart and overly diligent about it.

5. This is not a get rich quick business or industry. You can lose money funding and syndicating. You can technically also lose money brokering on commission clawbacks for deals that go bad right away.

6. Leads are expensive. Do not launch an ISO with only 2 grand in the bank.

7. Learn to generate your own leads and you will save yourself a lot of stress down the road.

8. A wise man once told me it is better to build a book of business and a long lasting passive income than to grind it out for a quick buck month after month. What’s your strategy?

9. You will lose deals, commissions, arguments, and occasionally your mind. Accept your losses when they happen and focus on the next deal.

10. Use appropriate language. A company that buys future revenues is not a lender and their financial transactions are not loans. Loans have noticeable things like interest rates and fixed terms. Make sure you know which one you’re talking about at any given time.

It’s Okay For a Business to Act Like a Business

February 10, 2015 A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

McCarthy wrote that achieving a transformation, “will depend in part on facilitating greater transparency, accountability, and fairness across our sector, and reining in predatory actors.” He cuts right to the chase by attacking lenders all while ignoring the reality that businesses are regularly preying on financial companies too, especially in the technology age.

It’s an epidemic. There is actually an entire industry association that is dedicated to preventing repeat merchant fraud. Respecting that small business is the backbone of this country though, it probably wouldn’t be appropriate to draft a Lenders’ Bill of Rights, whereby merchants promise not to deceive, lie, or commit fraud against them. Instead the industry deals with it quietly, investing in new risk infrastructure and ultimately passing the costs on to the good borrowers.

Merchants aren’t inherently bad, but neither are the companies that provide them with financial services. Let’s agree that the world is good but that bad actors exist.

McCarthy’s argument for a Small Business Borrowers’ Bill of Rights is premised on the assumption that in every commercial financing transaction, one side is painfully unaware and uneducated about what’s going on around them despite being an owner, president, or CEO of a company.

I think a dose of self-deprecating reflection is healthy and 2014 definitely brought out many discussions about how to increase transparency and better serve small business. But there’s a line between self-improvement and self-loathing that nobody should lose sight of.

It’s okay to make a profit

It’s okay to make a profit

Imagine that the CEO of a widget retailer grossing $2 million a year is looking for a new widget wholesaler to buy product from. The CEO sits down with a prospective wholesaler and asks for a quote. The wholesaler says they have deals with domestic widget manufacturers and Chinese exporters and based upon these relationships and the circumstances they can sell them in bulk at a price of $2 per widget. Unbeknownst to the retailer, the wholesaler quoted a competing retailer a price of only $1.80 per widget earlier that day. But this is business and if the wholesaler can charge more to this company, he will.

Unsure if he should accept the terms, the retailer pulls out a Widget Retailers’ Bill of Rights and demands the wholesaler charge not a penny more than what would adequately compensate the wholesaler for his work in the name of fairness. He also demands to be presented with unbiased facts on costs, benefits, and risks of every widget manufacturer, so that they can compare products on an apples-to-apples basis without pressure. And if they don’t do this, they will get Washington involved.

If you think this is supposed to be silly, it’s not. It’s McCarthy’s worldview applied. What’s missing from this scenario is that the wholesaler has a widget cost basis of about $1 and is selling them for $1.80 to $2.00, a nice margin. The retailer will sell these widgets for $10 a piece in their stores for an even better margin.

Maybe it’s the consumer that ends up getting screwed on price but even that seems unlikely since widgets are selling off the shelves at lightning speed. So what would be fair and adequate compensation for every party involved? What if the manufacturers are producing widgets for 7 cents each? Is there another layer of possible unfairness here?

Everybody has some kind of incentive and that’s how a marketplace works. If the price is too high, customers won’t buy, they’ll negotiate the price down or they’ll shop elsewhere.

In McCarthy’s Bill of Rights, he rejects the very notion of self-interest. “Some lenders charge higher interest rates just because they can,” he writes. This is how capitalism works. Find your customers price point and sell for a profit. Don’t forget we’re talking about commercial transactions only here!

You ever wonder why they’re called deals?

I’m reminded of someone from the peer-to-peer lending world that once asked me why folks refer to merchant cash advances as deals. They’re not loans, they’re not units, they’re deals!

And true to their deal making roots, terms on them are almost always negotiable. Two companies come together to make a deal… get it? Traditional merchant cash advances are also not loans. They’re literally contracts negotiated by businesses to sell future revenues at a discount in return for upfront cash flow. The concept couldn’t be any more commercial.

And over on the lending side, McCarthy might have you believe that the average small business CEO is unsophisticated shark bait in this unfair world so I pulled up the stats on the industry’s most famous small business lender. According to the S-1 filing, 90% of OnDeck Capital’s borrowers gross between $150,000 and $3.2 million a year in revenue and have been in business for an average of 7.5 years. These are bright companies.

Curiously there’s a group of financiers that are unabashedly capitalist. They will charge whatever they can get away with, take half a business if they want and even call their customers shark bait to their faces. Hopefully they clean up their act before Washington steps in! Thankfully the regulators have not yet put an end to ABC’s Shark Tank though I’m sure McCarthy will propose they do so.

That means you too Marcus Lemonis… Rumor has it you do things to make money all while applying high pressure sales tactics on TV to get people to agree and without telling the business owners the unbiased facts about every other financing option in the entire marketplace.

If it’s okay on TV, it has to be okay in real life.

Business on a deeper level

Business on a deeper level

I didn’t mean to take a stab at Brayden McCarthy personally but his message reflected a culmination of emotions that some people feel in this industry when they’re struggling to keep up. They can’t believe that a client would take something more expensive when they had an offer for something less expensive. Almost 7 years ago I competed against another salesman for a client to whom we both made almost the exact same offer; Same advance amount, same holdback %, same closing fees, but a different receivable purchase amount. The ONLY difference was that the other guy’s price was $2,000 more expensive. Everything else was the exact same and he knew it. And you know what happened? He went with the more expensive offer…

I remember confronting that salesman about it a few days later after I had let my anger cool down. A lot of thoughts had gone through my mind, that perhaps the other guy had lied, coerced him, or conducted some kind of shady trick. Why else could this have happened?! It seemed completely illogical. Of course it was none of those things. The other salesman developed a strong rapport with the customer and they spent most of their time talking about football on the phone.

“He freaking loved me,” the salesman said.

“That can’t be it,” I thought. Still hurt and determined to get the truth, I sent the lost prospect a very long email complete with mathematical formulas (I even used exponents, square roots, and fancy squigglies for good measure) to show how much he would’ve been better off with my offer. He responded almost immediately. “You see, this is exactly why I didn’t go with you,” he wrote.

While I was busy trying to open the customer’s eyes to the magic of the Black-Scholes model, the other salesman was talking to him about whether or not Eli Manning was really franchise quarterback material.

Still a very inexperienced salesman at the time, I had learned a new truth. Business went deeper than just prices, market efficiencies, and a desire to make money, it was also about relationships. Treating one side like an uneducated idiot has become a cornerstone of regulations to protect consumers, and perhaps even rightfully so but imagine the widget retailer grossing $2 million a year walks into a business negotiation and is immediately told that he is too dumb and too unaware to not only understand how to assess a deal but to foresee the consequences of his own decisions if he makes a deal.

Transparency is good, relationships are greater. There’s no need to codify sour emotions into an awkward Bill of Rights. Let two businesses make a deal. It doesn’t have to be the smartest, the fairest, or the best, just something both ultimately agree to. I can’t imagine it any other way.