Commission Chargebacks: The Good, the Bad and the Ugly

August 10, 2015 Imagine you’re a 20-something-year-old broker who’s just, in good faith, referred a merchant to a funder. You walk away with a few thousand dollars in your pocket, and you promptly spend it on rent and a celebratory steak dinner. Then all of a sudden…BAM! Just like that the merchant goes belly up and the funder’s knocking on your door to clawback your hard-earned commission money, which, of course, you’ve already spent.

Imagine you’re a 20-something-year-old broker who’s just, in good faith, referred a merchant to a funder. You walk away with a few thousand dollars in your pocket, and you promptly spend it on rent and a celebratory steak dinner. Then all of a sudden…BAM! Just like that the merchant goes belly up and the funder’s knocking on your door to clawback your hard-earned commission money, which, of course, you’ve already spent.

For many brokers, it’s a familiar-sounding story—with an ending they’d like to rewrite. Their thinking goes like this: underwriters, not brokers, are the ones who are supposed to dig into a company’s finances before approving a deal. Underwriters, not brokers, are the ones who make the financial decisions about whether or not a deal can go forward. Therefore, underwriters, not brokers, should be responsible when deals implode.

“There are a lot of people who think there should not be commission clawbacks—that they’re unfair,” says Archie Bengzon, who runs the New York sales office for Miami-based Rapid Capital Funding, a direct funder. Bengzon was previously the president of Merchant Cash Network, an ISO in New York.

While there’s a fair amount of closed-door grousing by brokers, most funders are standing their ground—with only a select few companies kicking these controversial policies to the curb. More commonly, funders claim clawbacks, despite being hated by brokers, are a necessary evil. These funders say that without them, they’d stand to lose too much on bad deals and that they need a way to protect themselves from rogue brokers.

“There is a group of people out there who are trying to game the system,” says industry attorney Paul Rianda, who heads a law firm in Irvine, California.

The Case for Scrapping Clawbacks

Brokers in favor of changing the status quo understand the need to prevent bad apples from smelling up the entire industry. But even so they believe that chargebacks are patently unfair to the honest majority of brokers who often make just enough to scrape by. In most cases, the brokers are typically young—18-to-26-year-olds trying to make money and learn the industry. They don’t have the financial resources that the funders do and the onus shouldn’t be on them if the deal they brought in—with good intentions—goes bust in a short time, according to the owner of a top-tier ISO/Hybrid in Staten Island, New York, who requested his name not be used.

This is especially true in cases where the underwriter took risks they shouldn’t have or decided to fund merchants in cases where they shouldn’t have. “It’s the underwriter’s job to protect the money that their company is lending out,” he says. “[Chargebacks] shouldn’t be going on in this industry.”

One solution might be for more ISOs to stand up to funders and refuse to send them future deals. That’s exactly what the Staten Island executive did a few years ago when a funder he repeatedly worked with tried to claw back his commission on a particular deal. He made a big stink and told them he’d never send them business again. It was enough of a threat to convince the funder to back off. “If more ISOs start saying that…then the funders will start sweating and change their contracts. Because it really isn’t fair,” he says.

For some brokers, however, taking such a strong position with funders is a risky strategy in a cottage industry where all the major players know each other and there’s no shortage of hungry young brokers willing to do business. So while these brokers don’t like losing money, they aren’t necessarily loudly crying foul either.

Matthew Ross, managing member of Go Ahead Funding, a broker and funder in Basalt, Colorado, has been in the business for nine years. He’s only had one commission clawed back once in this time period—it was a commission for $1,500 on a $25,000 deal that went sour within a month, he recalls. He was upset at the time and felt the underwriter should have done more to vet the merchant who went belly up. “Why didn’t the underwriters catch this?” he remembers asking at the time.

Matthew Ross, managing member of Go Ahead Funding, a broker and funder in Basalt, Colorado, has been in the business for nine years. He’s only had one commission clawed back once in this time period—it was a commission for $1,500 on a $25,000 deal that went sour within a month, he recalls. He was upset at the time and felt the underwriter should have done more to vet the merchant who went belly up. “Why didn’t the underwriters catch this?” he remembers asking at the time.

Nonetheless, Ross was a lot calmer than some brokers might have been under the circumstances. For instance, he says he never threatened to stop sending the funder business as many brokers might have done. “I don’t necessary like it, but I understand it. I’m not going to fight it,” he says.

Some brokers are making their displeasure with the practice known by declining to sign contracts that contain clawback clauses. Nathan Abadi, founder and president of Excel Capital Management, a New York-based funder and ISO, says he either refuses to do business outright or he comes to a verbal agreement with a funder that he’ll wait two weeks for payment to make sure the deal has legs. “I meet them in the middle,” he says.

The reason he likes this approach is that it’s more palpable for brokers to lose paper commissions versus actual money that they’ve already been given and possibly spent. Otherwise, as a business owner working with numerous agents, it’s bad for business. “It causes an internal conflict because now you have to penalize the person who’s working for you,” Abadi says.

The Flip Side of the Chargeback Coin

Meanwhile, there’s a whole other camp within alternative funding—including some brokers—who feel chargebacks are important as a fraud-deterrent. Given the fact that the industry is still largely unregulated, many believe that funders need some type of fire retardant to prevent being burned by unscrupulous brokers.

“We think that they serve an important role,” says Stephen Sheinbaum, founder of Merchant Cash and Capital, a New York-based funder. “Most of our stronger referral partners do not object to it. It’s a way of aligning our interests with the sales force.”

About 60 percent of the company’s funding business comes from third-parties including ISOs; its direct sales force accounts for the other 40 percent.

Even some brokers concede that clawbacks can serve a valuable purpose. Sure, it’s aggravating to lose money, but they feel that without clawbacks the industry would be even more of a free-for-all than it already is.

“I can see both sides,” says Bengzon, the funder and broker. Wearing his broker hat, Bengzon has felt the sting of losing a commission once or twice in the 100 or so deals he’s done. But he still understands why funders—who take a big monetary hit when deals go sour—would want to protect themselves and require brokers to have some skin in the game.

“If we’re going to reap the rewards of a nice commission, we should also understand that it can still be taken away if a deal goes bad,” he says.

When he sends leads to funders, Ross of Go Ahead Funding says he does his best to make sure he’s sending only high quality merchants. He tries to vet them upfront—to the limited extent he can—in order to avoid problems later on. Clawback provisions serve as “an incentive for [brokers] to keep their eyes open,” he says.

Know What You’re Signing

About 80 percent of the agreements that come across the desk of Rianda, the industry attorney, have a 30-day clawback provision. But he’s seen some agreements that have longer time frames—60, 90 or even 120 days. Those types of contracts aren’t as common, but they’re out there.

It’s important for brokers to carefully read the fine print of a contract before signing on the dotted line. “It sounds obvious, but a lot of people don’t do that,” says Bengzon.

The shorter the clawback time frame, the less brokers tend to balk. “People don’t want to be paid on a deal and three months later they lose that commission, which they’ve already spent,” he says.

Bengzon believes a clawback that extends any more than a month is excessive. “I would never sign something greater than 30 days,” he says.

According to Sheinbaum of Merchant Cash and Capital, 30 days is an appropriate time frame to help weed out fraud without putting unnecessary burden on brokers who are sending legitimate business. “The purpose of the provision is to try and stop people from committing fraud at the outset,” he says.

According to Sheinbaum of Merchant Cash and Capital, 30 days is an appropriate time frame to help weed out fraud without putting unnecessary burden on brokers who are sending legitimate business. “The purpose of the provision is to try and stop people from committing fraud at the outset,” he says.

David Sederholt, executive vice president and chief operating officer at Strategic Funding Source Inc. in New York, says clawback provisions in the contracts Strategic uses range from 30 to 45 days depending on the contract. He says he understands brokers don’t like them, but that it’s nonetheless important to have the provision in order to protect the funders. “There’s got to be some partnership involved here,” he says.

Clawbacks Not A Free-For-All

Many funders recognize that there’s a fine line between protecting their business and cutting off potential revenue sources.

“You start clawing back commissions on every default, a broker will stop sending business,” says Ross of Go Ahead Funding.

Sheinbaum of Merchant Cash and Capital notes that clawbacks aren’t used as often as some brokers might think. He says out of 800 deals in a 30- or 31-day period, his company enforces its clawback policy only a handful of times each month.

He also points out that while the clawback policy is on the books, Merchant Cash and Capital looks at each situation individually. If it’s clear that the broker tried to defraud the funder, that’s one thing, he says. But, if for instance, a merchant has a heart attack and dies 20 days into a deal and can’t pay back the funds, Merchant Cash and Capital wouldn’t try to clawback the broker’s commission in that situation, he says.

Strategic Funding has only clawed back commissions once or twice in the past nine years, says Sederholt, the EVP.

The company works with a variety of brokers. Some have less than a 1 percent default rate and others have 12 percent to 14 percent default rates. As extra protection with brokers who have bad track records, Strategic Funding either declines to work with them at times, or has in place a stronger underwriting procedure with these deals.

Being more careful upfront is a better tactic than trying to go after commissions, which is extremely hard, Sederholt says.

Changing the Modus Operandi

While it’s not the industry norm, there are a few funders who have stopped using clawbacks, or are considering doing so, given all the headaches they can cause. Isaac D. Stern, chief executive of Yellowstone Capital LLC, a New York-based funder, says his company no longer tries to clawback commissions when deals go bust. The few times they tried to clawback commissions several years back, the brokers they went after were upset and threatened not to do business with them anymore. Yellowstone decided this approach was bad for business and that it would be more prudent to try something else.

“There’s too much competition, and if we were going to do clawbacks it would decimate our business,” he says. “It’s the broker’s job to bring in the deals. It’s our job to underwrite it. If something goes wrong on the deal, that’s on us. It’s not the broker’s fault.”

As protection, the contracts Yellowstone uses with brokers contain a provision allowing it to seek damages when fraud’s alleged. But in cases where brokers send what seems to be a legitimate deal that goes bad for something other than fraud, Yellowstone turns the other cheek. Yellowstone can afford to eat the $5,000 or $6,000 commission to ensure ongoing—and hopefully more positive leads—or so the thinking goes, according to Stern.

Overtime—if peer pressure continues to mount—it’s possible that more even more funders will decide chargebacks just aren’t worth the trouble. “I think the reason why some funders are moving away from [clawbacks] is because people are afraid of losing volume. Once one funder acquiesces, others will follow suit,” says Sheinbaum of Merchant Cash and Capital.

What’s in the SoFi AAA Rated Bonds?

July 30, 2015 Should you buy student loan debt from a startup tech-based lender? DBRS is signaling yes with a AAA grade to $387 million of the notes in a $418 million offering. To put that into perspective, the U.S. Dollar was given the same grade just months before. Bonds issued by Goldman Sachs however were rated two levels lower at A on July 6th.

Should you buy student loan debt from a startup tech-based lender? DBRS is signaling yes with a AAA grade to $387 million of the notes in a $418 million offering. To put that into perspective, the U.S. Dollar was given the same grade just months before. Bonds issued by Goldman Sachs however were rated two levels lower at A on July 6th.

As Safe as the U.S. Dollar?

Founded just four years ago in 2011, SoFi has already made more than $2.3 billion in student loans. The company CEO Mike Cagney is a regular fixture at FinTech trade shows and I myself admittedly often wear a SoFi t-shirt on hot summer days around the city.

Of all the loans to invest in though, I would’ve put student loans at the very bottom of my list. Everywhere I turn, recent college grads and the elderly alike are lobbying against what they perceive as an unfair system.

In a bombshell article in the New York Times last month titled, Why I Defaulted on My Student Loans, author Lee Siegel argued that repaying student loans will lead to “self-disgust and lifelong unhappiness, destroying a precious young life.”

The story ignited a political firestorm across social networks. But Siegel was unapologetic and encouraged others to follow his example of defaulting.

“I chose life,” he wrote. “That is to say, I defaulted on my student loans. As difficult as it has been, I’ve never looked back. The millions of young people today, who collectively owe over $1 trillion in loans, may want to consider my example.”

He’s found sympathy from millennials who came of age right during or after the financial crisis, since many of them have struggled to find jobs or move out of their parent’s homes.

And it’s not just them, “Over 16% of the $1.2 trillion in outstanding student loan debt belongs to individuals over 50 years old.” According to Forbes, the epidemic of student loan debt is even affecting seniors in retirement, some of whom are facing garnishment of their social security checks.

The outlook isn’t good either. According to the Wall Street Journal, the Class of 2014 is the most indebted ever, that is unless the Class of 2015 steals the title.

And there’s another statistic to consider. “The problem developing is that earnings and debt aren’t moving in the same direction,” reports the WSJ. “From 2005 to 2012, average student loan debt has jumped 35%, adjusting for inflation, while the median salary has actually dropped by 2.2%.”

And there’s another statistic to consider. “The problem developing is that earnings and debt aren’t moving in the same direction,” reports the WSJ. “From 2005 to 2012, average student loan debt has jumped 35%, adjusting for inflation, while the median salary has actually dropped by 2.2%.”

But the SoFi rating is based on data, not on emotionally charged arguments over social networks regarding the morality of paying for college. Obviously the numbers must indicate something to give them a creditworthiness equal to U.S. Dollar, at least for the pool of notes that earned the grade.

Across the entire offering, dubbed 2015-C, there are also notes with a BBB grade. Altogether, the portfolio contains a weighted-average credit score of 777 and a weighted-average borrower income of $143,132. This isn’t exactly a group of poor struggling borrowers.

100% of the loans were refinanced from another lender so they had a prior track record of making payments.

“Refinancing Loan borrowers have already graduated, have proven well-documented incomes and have stronger credit profiles as compared with typical newly originated student loans,” the DBRS report states. “Further, such borrowers have demonstrated an ability to gain employment and repay their student loan debt.”

And yet a large portion of borrowers have a variable rate loan, with the average balance on those being $74,315. It’s a recipe that could shake the system years down the road.

A AAA rating is an eye-opening assessment even with the quality of borrowers. The final maturity dates for those notes are in August, 2035, a full two decades from now. SoFi has only been in business for four years.

Technologists and scientists say to trust in the data, but there’s got to be credibility afforded to the noise coming from millennials over the last few years. That message, at least the one that I’ve heard, has been that student loans are ruining lives.

Breaking news stories about predatory colleges feed into this narrative. Just last month, the NYT alluded that as many as 350,000 students were scammed by Corinthian Colleges. “Corinthian was a longtime target for federal and state regulators, with a host of investigations and lawsuits charging falsified placement rates, deceptive marketing and predatory recruiting, targeting the most vulnerable low-income students,” the NYT stated.

A Corinthian College graduate would probably not qualify to be a SoFi borrower. 3.5% of borrowers in 2015-C graduated from NYU and 2.5% from Columbia. 59% have an MBA, law, or medical degree.

If the DBRS report makes anything absolutely clear, it’s that these are the types of borrowers you’d bring home to meet your parents.

The irony is not lost however that Lee Siegel, the NYT author that encouraged kids to default on student loans like he did, is a graduate of Columbia.

Perhaps for that reason, competing ratings agency Moody’s graded the senior notes only AA2, two notches below what they consider perfect.

Yesterday I would’ve told you that I would never consider student loans as an investment, but now I’m not so sure.

The data and the review by the ratings agencies definitely conflict with what I hear from real life borrowers and their attitudes about student loan debt.

What are your thoughts?

Addressing Stress and Depression Over Declined Deals

July 29, 2015 I wanted to add to my series discussion by touching on a topic that isn’t often discussed in our space, and it pertains to dealing with depression, stress and other mental health related conditions over the loss of a deal.

I wanted to add to my series discussion by touching on a topic that isn’t often discussed in our space, and it pertains to dealing with depression, stress and other mental health related conditions over the loss of a deal.

Let’s Be Honest

Let’s face it, most of us (as brokers) work on a 100% commission structure, or derive a significant portion of our income from commission, this means that our compensation is based on performance. This performance is directly correlated to the amount of new/renewal business that we fund. The word fund is the keyword here, as your performance in terms of selling might be excellent with the continued production of new leads, new applicants and new interested parties to our industry’s working capital selections. However, if those new leads and applicants don’t fund, then in terms of your performance, they don’t count. An applicant can be declined for a variety of reasons and all of them are usually totally out of your control. However, your compensation is dependent upon your merchant’s approval as well as the offering of terms/conditions that they deem acceptable. This high level of stress can lead to mild bouts of depression, and that depression could lead to a variety of other issues such as overeating, not eating, over sleeping, not sleeping enough, emotional breakdowns, paranoia, personal relationship issues, along with a variety of other inefficiencies.

The Loss Of Hope

Google says that the definition of depression is related to “the feelings of severe despondency and dejection.” Despondency and dejection refers to a state of low spirits caused by the loss of hope, and hope is sometimes all we have as Brokers. All we have going for us is an internal “hope” that our sales abilities will produce the commissions needed to not just cover our business/tax expenses, but cover our personal expenses, insurance, etc., and leave some left-overs to allow us to save for retirement. If you put your soul into this (like I do), then with every funded deal you will rejoice internally, and with every deal declined or approved with terms that are unacceptable to your client, you might feel sudden emotions of panic, fear and uncertainty. As a one man show, I have funded hundreds of deals while also building up a side merchant processing portfolio that processes tens of millions in volume every year. But I have also lost a ton of potential deals on both the funding side and the merchant processing side through declines or approvals that were unacceptable to my client. If left unchecked, still to this day I feel emotions of sickness and depression over declined and lost deals, so much so that sometimes I just have to go home and lay down in the bed for a minute.

Tackling The Stress Through Other Means Of Management

So how do I handle depression and stress over declined and lost deals for the most part? Here are some tips on how I handle the stress and depression of this industry, and perhaps they too can provide some assistance for you in those critical, nerve-racking situations of receiving emails from your Funder with “Declined” or “Application Ineligible” typed out in the Subject Line:

Diversify, Diversify, Diversify

This isn’t just true in Stocks, but it’s also true in being an Independent Agent/Broker. You are a 1099 Independent Sales Office and there’s just no reason why you ought to only be selling one product. Remember as I touched on in prior AltFinanceDaily articles, as a Broker your job is to be as Jeff Thull from Prime Resource Group explains, which is to be a valued source of business advantage for your prospective and current clientele. You should have access to knowledge, resources, networks, products and platforms that your prospective and current clientele lacks access to, allowing them to see you as a “valued extension” of their organization in terms of the value of your expertise and network.

So there’s no reason that you should just be selling Merchant Cash Advances or Alternative Business Loans, you should be selling a variety of other products in various different segments such as POS Systems, Merchant Processing, Equipment Leasing, Insurance, Big Data, Marketing Programs, Cost Reduction Programs, etc., just to name a few.

Do This Because It’s Your Purpose, Not Just For The Money

Listen, I’m not here to convert anybody to any particular Religion, but I believe that if you are going to be an entrepreneur (which is what you are as a 1099 Broker/Agent) then you need to have a very strong internal spirit or soulful foundation. Your motivation, joy, peace and confidence should extend beyond your earthly circumstances. You should see this industry as something you do as a Purpose that aligns with your spirit or soulful foundation, rather than just seeing it solely as a means to make an income.

Continued Learning and Development

The Merchant Services related industry continues to evolve and you should be following all of the trends and updates. The best places to do this for the Merchant Services related industry, is to make sure to follow AltFinanceDaily as well as other sources such as The Green Sheet, Payment Source’s ISO/Agent, The ETA, The SBFA, as well as various industry trade conferences such as LendIt and The AltLend Summit.

Focus On Total Financial Management

Focus On Total Financial Management

Financial management is not just about bringing in decent income, it’s about managing the six pillars of finance which are Income, Investments, Insurance, Credit, Expenses and Taxes.

For example, you might be bringing in $100,000 a year in commissions from your Home Office, but you might be living in a high cost of living area, have horrible spending habits, have inefficient tax reduction strategies, and you have four children from four different women paying very high child support claims. This means that your expenses are too high and your financial efficiency is going to be off.

On the other hand, you might be making $50,000 a year in commissions from your Home Office, with no children, living in a low cost of living area, with efficient budgeting and tax reduction strategies, putting away let’s say $7,500 a year into your retirement accounts. If you do this for 40 years from 25 – 65 for example, with just a conservative 5% per year return, you will have over $1 million at age 65. You will have made yourself a self-made millionaire and you didn’t need a six figure annual commission compensation to do it. All you needed was Total Financial Management.

To Wrap

So in a nutshell, I manage the stress and depression of our industry through having a totally efficiently managed financial system in place, not selling just one product, always learning, and making sure that everything I do is grounded in Purpose. I believe that if you too were to adapt some of these techniques, the loss of that deal you worked so hard on, might not “sting” as bad after all.

A Square IPO Would Be Alternative Lending’s Third

July 26, 2015 First Lending Club, then OnDeck, and now… Square? The news media was flooded with stories late last week that payments company Square had filed their S-1 in secret. The move can be done under a JOBS Act provision that allows companies that grossed less than $1 Billion in revenue in the most recent fiscal year.

First Lending Club, then OnDeck, and now… Square? The news media was flooded with stories late last week that payments company Square had filed their S-1 in secret. The move can be done under a JOBS Act provision that allows companies that grossed less than $1 Billion in revenue in the most recent fiscal year.

Square’s merchant cash advance arm, Square Capital, reportedly funded $100 million to small businesses in 2014, a figure large enough to earn them a spot on the AltFinanceDaily leaderboard.

While often reported as a lending program, Square’s own website describes their working capital transactions as sales of future credit card receivables. At face value, and aside from what their contracts might actually say, it’s a textbook merchant cash advance.

While some publicly traded companies have dabbled in merchant cash advances, the financial product is one of Square’s two major products, the first obviously being payments.

And while OnDeck offers loans that are very similar to merchant cash advances, Square could potentially be the first true merchant cash advance IPO.

Also on the IPO watch list is CAN Capital, a company that offers both loans and merchant cash advances. In November of last year, Bloomberg and WSJ claimed the company was already working on it. While it has been eight months since that news came out, word on the street is that a CAN Capital IPO is still very much a possibility.

Unfortunately, because of the same JOBS Act provision that allowed Square to file an S-1 (if they actually did) also applies to CAN Capital. There is no way to know what’s going on behind the scenes until the filing is made public or leaked to the media.

Either way, the end of 2015 will likely end in at least one more IPO for the commercial side of alternative lending.

Could Jack Dorsey and his wacky beard be the future face of the merchant cash advance industry?

BREAKING: JACK DORSEY’S BEARD pic.twitter.com/Quv8nVG9PZ

— Nicholas Carlson (@nichcarlson) June 12, 2015

Federal Government Wants Your Thoughts About Online Lending

July 19, 2015 Whether you’re a funder, lender, broker, or platform, the U.S. Treasury Department deserves to hear your input.

Whether you’re a funder, lender, broker, or platform, the U.S. Treasury Department deserves to hear your input.

Only July 16th, the Treasury announced that it was seeking public comment on various business models and products offered by online marketplace lenders to small businesses and consumers. One stated purpose of this is to study “how the financial regulatory framework should evolve to support the safe growth of the industry.”

The comment period is only open for six weeks.

Over the last year, many funders and brokers have voiced their opinions on best practices, ethics, and standards. Some want regulation to curb what they believe to be immoral behavior and others just want clarity where the laws are obscure, illogical, or even in conflict with themselves.

In at least one recent case, a merchant cash advance company CEO wrote about the complexity of dealing with an endless amount of state laws. In Lift the Fog, Give us Regulation, Merchant Cash and Capital CEO Stephen Sheinbaum wrote, “It is also better, at least for the financial services industry, if the central government is the one to craft the regulation instead of getting one rule from each of the 50 state governments.”

Meanwhile the Consumer Financial Protection Bureau (CFPB) will eventually start to enforce the amendments to the Equal Credit Opportunity Act, which technically already became the law under Section 1071 of the Dodd Frank Act. As part of that, underwriters of business loans and merchant cash advance alike may no longer be allowed to meet applicants, speak with them on the phone, examine their driver’s licenses, review their social media profiles, or even ask what their business model is or how they market themselves.

One has to look at any opportunity afforded by a government agency to share input before future regulations are implemented then as a duty. It might not matter, but you should do it anyway, just like voting.

Below are the questions, the Treasury wants you to answer (or Click to view on Treasury.gov):

1. There are many different models for online marketplace lending including platform lenders (also referred to as “peer-to-peer”), balance sheet lenders, and bank-affiliated lenders. In what ways should policymakers be thinking about market segmentation; and in what ways do different models raise different policy or regulatory concerns?

2. What role are electronic data sources playing in enabling marketplace lending? For instance, how do they affect traditionally manual processes or evaluation of identity, fraud, and credit risk for lenders? Are there new opportunities or risks arising from these data-based processes relative to those used in traditional lending?

3. How are online marketplace lenders designing their business models and products for different borrower segments, such as:

• Small business and consumer borrowers;

• Subprime borrowers;

• Borrowers who are “unscoreable” or have no or thin files;

Depending on borrower needs (e.g., new small businesses, mature small businesses, consumers seeking to consolidate existing debt, consumers seeking to take out new credit) and other segmentations?

4. Is marketplace lending expanding access to credit to historically underserved market segments?

5. Describe the customer acquisition process for online marketplace lenders. What kinds of marketing channels are used to reach new customers? What kinds of partnerships do online marketplace lenders have with traditional financial institutions, community development financial institutions (CDFIs), or other types of businesses to reach new customers?

6. How are borrowers assessed for their creditworthiness and repayment ability? How accurate are these models in predicting credit risk? How does the assessment of small 10 business borrowers differ from consumer borrowers? Does the borrower’s stated use of proceeds affect underwriting for the loan?

7. Describe whether and how marketplace lending relies on services or relationships provided by traditional lending institutions or insured depository institutions. What steps have been taken toward regulatory compliance with the new lending model by the various industry participants throughout the lending process? What issues are raised with online marketplace lending across state lines?

8. Describe how marketplace lenders manage operational practices such as loan servicing, fraud detection, credit reporting, and collections. How are these practices handled differently than by traditional lending institutions? What, if anything, do marketplace lenders outsource to third party service providers? Are there provisions for back-up services?

9. What roles, if any, can the federal government play to facilitate positive innovation in lending, such as making it easier for borrowers to share their own government-held data with lenders? What are the competitive advantages and, if any, disadvantages for nonbanks and banks to participate in and grow in this market segment? How can policymakers address any disadvantages for each? How might changes in the credit environment affect online marketplace lenders?

10. Under the different models of marketplace lending, to what extent, if any, should platform or “peer-to-peer” lenders be required to have “skin in the game” for the loans they originate or underwrite in order to align interests with investors who have acquired debt of the marketplace lenders through the platforms? Under the different models, is there pooling of loans that raise issues of alignment with investors in the lenders’ debt obligations? How would the concept of risk retention apply in a non securitization context for the different entities in the distribution chain, including those in which there is no pooling of loans? Should this concept of “risk retention” be the same for other types of syndicated or participated loans?

11. Marketplace lending potentially offers significant benefits and value to borrowers, but what harms might online marketplace lending also present to consumers and small businesses? What privacy considerations, cybersecurity threats, consumer protection concerns, and other related risks might arise out of online marketplace lending? Do existing statutory and regulatory regimes adequately address these issues in the context of online marketplace lending?

12. What factors do investors consider when: (i) investing in notes funding loans being made through online marketplace lenders, (ii) doing business with particular entities, or (iii) determining the characteristics of the notes investors are willing to purchase? What are the operational arrangements? What are the various methods through which investors may finance online platform assets, including purchase of securities, and what are the advantages and disadvantages of using them? Who are the end investors? How prevalent is the use of financial leverage for investors? How is leverage typically obtained and deployed?

13. What is the current availability of secondary liquidity for loan assets originated in this manner? What are the advantages and disadvantages of an active secondary market? Describe the efforts to develop such a market, including any hurdles (regulatory or otherwise). Is this market likely to grow and what advantages and disadvantages might a larger securitization market, including derivatives and benchmarks, present?

14. What are other key trends and issues that policymakers should be monitoring as this market continues to develop?

The Treasury asks that you include your name, company name, address, job title, email address, and phone #. You can submit your responses on http://www.regulations.gov/. Just click on the tab that says “Are you new to the site?”

You can also submit by mail:

To: Laura Temel,

Attention: Marketplace Lending RFI,

U.S. Department of the Treasury, 1500

Pennsylvania Avenue NW., Room 1325

Washington, DC 20220

If you have questions, email marketplace_lending@treasury.gov or call 202-622-1083.

MCA Brokers: Constructing Your Funder Network

July 18, 2015 Progressing forward into the 3rd Quarter of The Year Of The Broker, I wanted to continue our focus on the vital issue of inefficient training that new broker entrants are receiving within our space. In the previous article for AltFinanceDaily on 6/22/2015, I inquired about if you knew what you were selling in terms of the Merchant Cash Advance product? Within the article, I discussed value points and overcoming the product’s criticism. In this article, I wanted to add to this discussion by deliberating over how to create a quality Funder Network for the Merchant Cash Advance Product.

Progressing forward into the 3rd Quarter of The Year Of The Broker, I wanted to continue our focus on the vital issue of inefficient training that new broker entrants are receiving within our space. In the previous article for AltFinanceDaily on 6/22/2015, I inquired about if you knew what you were selling in terms of the Merchant Cash Advance product? Within the article, I discussed value points and overcoming the product’s criticism. In this article, I wanted to add to this discussion by deliberating over how to create a quality Funder Network for the Merchant Cash Advance Product.

As a Broker, I believe your job is to be as Jeff Thull from Prime Resource Group explains, which is to be a valued source of business advantage for your prospective and current clientele. In terms of the Merchant Cash Advance Product, you should have access to knowledge, resources, networks, and underwriting criteria that your prospective and current clientele lacks access to, allowing them to see you as a “valued extension” of their organization in terms of the value of your expertise and network. However, too many Brokers are not taking the time to truly be this source of business advantage for their prospective and current clientele, which involves not just continued knowledge, analysis and study over the industry from a “Macro” perspective, but also rounding up the quality relationships to properly serve their clientele on a “Micro” level, such as the creation of a high quality Funder Network. In this article, I wanted to provide some information to assist new Brokers in creating a high quality Funder Network for the Merchant Cash Advance product.

Keeping Things In Perspective

In my first article for AltFinanceDaily from 5/10/2015, I discussed the importance of Selecting The Right Funders, if you haven’t already done so, please review this article to keep things in perspective going forward. After you have reviewed that article, now you should focus on carefully crafting your Funder Network so that you can fulfill your job as being a source of business advantage to your prospective and current clientele. This creation will be based on understanding industry paper grades, which represent the various situations of your clientele during the underwriting process that determine their approval, risk based pricing, terms and conditions.

Paper Grades

The Paper Grades across the board are pretty much the same, but your job is to make sure you have 1-2 reliable, credible and quality lenders for each of the Paper Grades so that you can properly serve your clientele with tailored pricing, terms and conditions based on their risk based profile.

- A Paper: These are merchants that usually have a 650 plus FICO score, clean bank statements with low NSFs/Overdrafts/Negative Days, healthy bank balances (ending and average), no tax liens, no judgment liens, no recent bankruptcies, and no landlord/mortgage issues. In terms of pricing, this merchant should qualify for premium pricing or what I define as Tier I Pricing.

- B Paper: These are merchants that usually have a 600 – 640 FICO, with a variety of potential profile weaknesses on top of the lower credit scoring. Some of those potential weaknesses include having somewhat clean bank statements, somewhat healthy bank balances, they might have a tax lien or judgment lien on a payment plan (and the judgment is not from a prior MCA Company or based on fraud), they might have had a dismissed/discharged bankruptcy, and/or they might have landlord issues but can be resolved at closing. Note that in terms of these weaknesses, this merchant should really have no more than two of these weaknesses, such as they might have somewhat clean bank statements along with a tax lien on a payment plan. In terms of pricing, this merchant should qualify for Tier II Pricing.

- C Paper: These are merchants that usually have a 540 – 580 FICO, with a variety of actual profile weaknesses that push them into this lower credit grade. Some of these weaknesses include having bank statements with 5 – 10 NSFs/Overdrafts/Negative Days, along with not so healthy bank balances. In addition, they might have a tax lien or judgment lien on a payment plan (and the judgment is not from a prior MCA Company or based on fraud), they might have had a dismissed/discharged bankruptcy, and/or they might have landlord issues but can be resolved at closing. Note that this merchant should really have no more than three of these weaknesses, such as they might have bank statements averaging 10 NSFs a month, a tax lien on a payment plan, and they might be one month behind with their landlord which can be made “whole” at closing. In terms of pricing, this merchant should qualify for Tier III Pricing.

- D/E Paper: These are merchants that are considered high risk and might not even get an approval completed. They usually would have as high as a 520 FICO score, but their FICO score could actually come in lower than 500. In addition, expect a variety of actual profile weaknesses that make their approval difficult, such as over 10 NSFs/Overdrafts/Negative Days a month on their bank statements, along with not so healthy bank balances. Furthermore, they might have a tax lien that’s not on a payment plan, or they could have a judgment lien that’s not on a payment plan or a judgment that included a prior MCA Company. Finally, they might have landlord issues that can’t be resolved at closing. Usually the weaknesses are severe to the point where an approval cannot be generated, however, if an approval is generated it’s usually a very high costing advance along the levels of what I define as Tier IV and Tier V Pricing. This level of pricing is very expensive and it might just be in the best interest of the client to not provide him any funding at the moment, opting to instead allow him time to improve his credit standing so he can at least qualify for C Paper status.

Final Word

Note that many industries are on generic restricted lists of Funders, and while they might be A Paper in terms of general credit standings and profile status, their restricted industry status might lead to an auto-decline or a decrease in their Paper Grade.

When you construct your Lender Network, your job is to get 1 – 2 lenders for each Paper Grade so that you can serve your clients efficiently based on their risk based profile. This process involves researching your prospective lenders, understanding their criteria, underwriting their pricing/terms, and testing out the relationship by sending a couple of deals to see how it goes from a first-hand basis.

Doing this level of work upfront gives you a higher probability of surviving in one of the most competitive landscapes in financial services. Not doing this level of work upfront makes your chances of survival, office profitability and career sustainability (as a broker) less probable.

Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree

July 16, 2015Bank statements. Those in consumer lending argue they’re all but irrelevant because FICO and credit reports do the job of predicting risk just fine, but over in today’s small business lending environment, there’s an entirely different sentiment; Reveal your recent banking history or be declined.

After having bought nearly $60,000 worth of consumer notes on Lending Club and Prosper combined, there’s something I’ve seen a lot of, bounced ACHs.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

For all the fanfare surrounding online marketplace consumer lending, access to borrower banking history is oddly absent.

“Welcome to consumer lending, where the rules are different because the game is too,” replied a user to my comment on a peer-to-peer lending forum.

Veteran consumer lenders assumed I was a lost newbie who knew nothing about lending. “I have a feeling if you ask to crawl someone’s bank account, they’ll just go elsewhere,” one user said. “Seems that’d only work on subprime borrowers who have limited bargaining power.”

“I’m assuming you may be new to lending,” he continued. “Making a loan based on deposit balances is rarely a good idea.”

My initial question to them was that without bank statements, how could they ascertain if a borrower’s finances were actually in order at least at the time the loan was issued? It’s really easy to access someone’s banking history for the last 90 days by using common tools like Yodlee or Microbilt, I argued.

Some people sympathized with my logic but others believed requesting bank data would be suicide in today’s competitive environment. And still more wondered if there might be consumer protection laws that prevented lenders from seeing a loan applicant’s banking records (which sounded ridiculous).

A Credit Card Issuer’s Take

Those questions led me to interview an underwriting manager at one of the nation’s largest credit card issuers who would only speak on the condition of total anonymity, including the bank’s name. There, he oversees a department of people that manually assess credit card applicants. There is no algorithmic approval process. In his department, humans underwrite each application, conduct phone interviews with the prospective borrowers, and request additional documents if they feel it’s warranted.

Requesting bank statements is a regular part of the job, explained the manager. “We require proof of income for any line over 25k,” he added. “It’s the main thing we ask for along with proof of address.”

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

“The Adverse Action reason [for that] would be ‘sufficiently obligated’,” he stated. “That’s when their bank account shows they can not take on any additional financial obligations.”

The manager shared however that he believed there is a very strong correlation between what’s on the credit report and what to expect in the bank statements. Generally speaking, good credit will show a healthy banking situation, he explained. They’re rarely taken by surprise. Overall, the credit reports and phone interviews are enough for them to feel comfortable and the bank statements are really just there to check off a compliance box.

Meanwhile, those that speculated requesting bank data would be a death knell competitively might want to talk to Kabbage’s sister company, Karrot. Karrot already crawls bank accounts as part of their consumer loan application program and competes with Lending Club, Prosper, and Avant. Considering Kabbage has funded more than half a billion dollars worth of business loans using this very methodology, it’s safe to say that applicants aren’t flocking to competitors in droves over the perceived injustice or inconvenience of filling out three additional fields on a web application to share their transaction history.

Bounced Payments

Kabbage CEO Rob Frohwein offered these comments last year about their underwriting, “A critical aspect of consumer lending is determining the appropriate amount of a payment to collect so that an account doesn’t become overdrawn. Our intelligence accurately predicts how much of a payment to request via ACH so consumers avoid the cost and headache associated with non-sufficient funds.”

I thought about those statements when I noticed that thirty-six of my Lending Club notes carried a Grace Period status the other day. These are borrowers whose payments just recently bounced. Some are only three or four months into a five-year loan. Worse, there are those that are saying they have no money whatsoever to make a payment. How can this be when they just practically got approved?

To the consumer crowd it’s business as usual. “If you got their bank account, you still wouldn’t be able to predict who will default. You can’t predict defaults on any individual borrower,” argued one veteran on a forum.

But it’s not all about the lender’s tolerance for risk. ACH rejects can have consequences that affect a lender’s ability to debit accounts in the future.

“Ultimately, regulatory thresholds set by NACHA will continue to become more and more critical of returns,” said Moe Abusaad of ACH Processing Co, an ACH processor based in Plano, TX. “I think it’s safe to say that there is a positive correlation in considering statements as a component of the underwriting process to the rate of returns incurred,” he added.

And while it’s true that bank data can’t make predictions perfectly on its own, nobody in small business lending or merchant cash advance would consider an approval without it.

Bank Statements or Bust

“There is no substitute for banking information when reviewing a client for approval,” said Andrew Hernandez, a co-founder of Central Diligence Group, a risk management firm that allows business lenders and merchant cash advance companies to outsource their underwriting.

“Money moves fast through these businesses and every business is unique, so a lot more variables come into play than just having to account for the timely monthly payments of credit cards, cars, and mortgages as you find in the consumer world,” he added. “A FICO score along with other information presented in a credit report provide a detailed, historical snapshot of a client’s creditworthiness in consumer lending, and while these are great complementary tools for us to use in our underwriting process, I believe that banking data paints us a picture of its own which is absolutely essential in assessing the risk of a B2B transaction in our space.”

Those underwriting business loan deals have reported seeing applicants with open personal loans from Lending Club, which shows that the exact same borrowers are being underwritten in two different ways.

But Julio Izaguirre, another co-founder of Central Diligence Group added that, “banking transactions are essential in gauging the cash flow of the business by looking at recent and up-to-date bank volume, but it is even more important with businesses that lack historical data and cannot provide financials or other documentation to show and prove their track record.”

Translation: A lack of credit history and formal financial statements can be overcome thanks to in-depth analysis of bank account data.

“When our underwriters look at a bank statement you can get a better understanding of the business cash flow, operational cost and how the owner manages his business,” said Heather Francis, CEO of Gainesville, FL-based Elevate Funding. “The credit score is like a person’s blood pressure reading,” she continued. “It indicates there may be an issue but until lab work is pulled and analyzed you don’t know what that issue is. The bank statement is that lab work and it can tell you more about the issues behind the scenes than a credit score can.”

Greg DeMinco, a Managing Partner of Americas Business Capital based in Cherry Hill, NJ would probably agree. “FICO isn’t everything,” he shared. “Bank statements can tell a great story especially if there is upward momentum month after month, and more importantly a high ratio of deposits to requests for the advance.”

Meanwhile, the manager of the credit card issuer was surprised to hear about the high value placed on bank statements in business lending. I offered him the example of an applicant with good credit that was consistently negative in the bank because of a reliance on overdraft protection as a way to make sure all the bills were being paid. “That’s the craziest thing I ever heard,” he commented.

But over in the peer-to-peer lending forum it didn’t sound so crazy at all. “Plenty of Americans are ‘broke’, in the sense that they have negative net worth, yet they’ll continue servicing their debts for… a long time… no matter what it takes,” shared one user.

The argument seems to come full circle, that business lending and consumer lending are just different.

But to Isaac Stern, the CEO of New York-based Yellowstone Capital, the bank statements are not just about financial health. “We are literally underwriting against fraud,” said Stern, who said his office regularly receives applications with doctored statements. “Logging in [to the banks] and verifying those statements are probably the most important part of the process,” he noted.

His logic goes that a consumer that is paid a salary has a predictable stream of income and so that information along with a credit report might be enough for a consumer lender, but business revenue is less predictable and can vary practically day-to-day.

“You can’t just look at a FICO score and say, ‘this is a good a business’,” Stern explained. “The story is in the bank statements.”

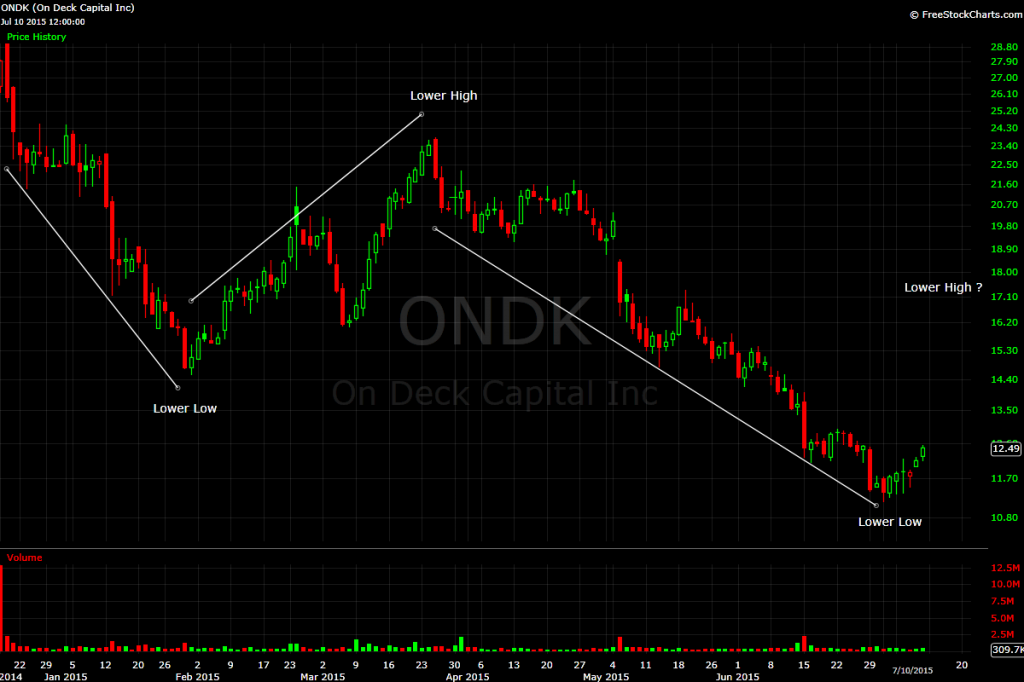

An OnDeck (ONDK) Technical Analysis

July 12, 2015For some of us working in the merchant cash advance industry, we saw the IPO of OnDeck (ONDK) as a major stepping stone in getting recognized by main street and receiving overall exposure. Unfortunately it has not been the best representative of us in the stock market. I started monitoring ONDK on the first day it started to trade and after 7 months, it clearly hasn’t looked positive.

I am a student in technical analysis. In layman’s terms, it is the study of price action of a traded financial instrument to make an informed investment decision. The following is my view.

The first thing that pops out when viewing the chart is that the single biggest day of volume (number of shares traded) was the IPO day. The stock has yet to trade in that kind of volume since then.

The other obvious thing that pops out is that the stock has been in downtrend, a series of lower lows and lower highs. As the old Wall Street adage says, “The trend is your friend.” Trying to call a bottom in this stock has been useless as it seems like those that have, are catching a falling knife.

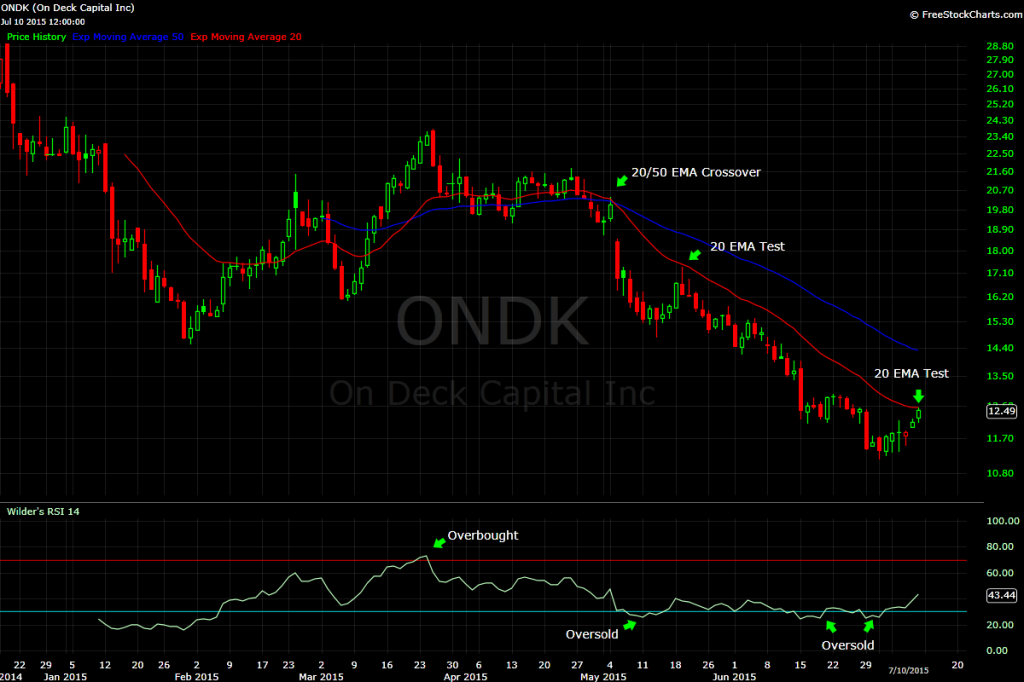

Moving averages are used to determine whether the stock is trending or not. With very few trading days the longer term averages are not able to be rendered. In May the stock met resistance at the 20/50 EMA crossover. Coincidentally this was also the beginning of the latest down leg. It is also worth noting that the stock has not closed above the 20 day EMA since it was breached. There was one failed attempt that resulted in the continuation of the down trend in the middle of May. The stock is currently at the 20 EMA and is testing this level again. A close above this could be an indication of a possible change in trend.

The bottom of the chart has the RSI. This is a measurement of Overbought and Oversold conditions, which is telling us that the stock has been oversold for a couple of months. It recently started moving upward from the oversold condition.

The MACD is another technical indicator used. It measures the momentum of the stock. I like to think of momentum as the thrust/force of the move in a stock. This indicator points two things to me. As the stock has been going lower there hasn’t been a lower low in the indicator. It actually seems there is a slight uptrend in the indicator, which tells me as the stock has gone lower, there hasn’t been the same force/thrust to the move. This is a classic example of divergence, meaning the stock is doing one thing while the momentum indicator is doing another.

The information above points to two possibilities. The first is that the stock is currently taking a breather from its downtrend. This is normal in a stock cycle; after all, stocks do not go up or down in straight lines. The other is that the stock could be in the beginning stages of stabilizing. Stabilizing does not mean that the stock will begin a new uptrend. It means the stock could be range bound for a couple of months.