Alternative Funding: Over The Top Down Under

September 2, 2015 San Francisco had its gold rush, Oklahoma had its land rush and now Australia is experiencing a rush of alternative funding. After a slow start a few years ago, foreign and domestic companies have been flocking to the market down under in the last 18 months.

San Francisco had its gold rush, Oklahoma had its land rush and now Australia is experiencing a rush of alternative funding. After a slow start a few years ago, foreign and domestic companies have been flocking to the market down under in the last 18 months.

As many as 20 new alt-funders are doing business in Australia, but that number could swell to a hundred, said Beau Bertoli, joint CEO of Prospa, a Sydney-based alternative funder. “The market in Australia has been very ripe for alternative finance,” Bertoli, said. “We see an opportunity for the alternative finance segment to be more dominant in Australia than it is in America.”

Recent entrants to the embryotic Australian market include Spotcap, a Berlin-based company partly funded by Germany’s Rocket Internet; Australia’s Kikka Capital, which gets tech backing from U.S.-based Kabbage; America’s Ondeck, which is working with MYOB, a software company; Moula, which began offering funding this year but considers itself ahead of the curve because it formed two years ago; and PayPal, the giant American payments company.

The new entrants are joining ‘pioneers’ that have been around a few years, like Prospa, which has been working for three years with New York-based Strategic Funding Source, and Capify (formerly AUSvance until it was consolidated into the international brand Capify), which came to market in 2008 with merchant cash advances and started offering small-business loans in 2012.

Some don’t take the newcomers that seriously. “There are small players I’ve never heard of,” said John de Bree, managing director of Capify’s Sydney-based office, in a reference to local Australian funders. “The big ones like OnDeck and Kabbage don’t have the local experience.”

But many players view the influx as a good sign. “I think it’s an endorsement of the market,” Bertoli said. “There’s more publicity and more credibility for what we’re doing here in terms of alternative finance.” It’s like the merchant who gets more business when a competing store opens across the street.

Besides, the market remains far from crowded. “I’m not concerned about the arrival of OnDeck and Kabbage because it really does validate our model,” maintained Aris Allegos, who serves as Moula CEO and cofounded the company with Andrew Watt.

The market’s relatively small size – at least compared to the U.S. – doesn’t seem to bother players accustomed to the heavily populated U.S., a development some observers didn’t expect. “I’m very surprised,” de Bree said of the American interest in Australia. “The American market’s 15 times the size of ours.”

Others see nothing but potential in Australia. “This is a market that will evolve over time, and we think the opportunity is enormous,” said Lachlan Heussler, managing director of Spotcap Australia.

Some view the Australian rush to alternative finance not so much as a solitary phenomenon but instead as part of a worldwide explosion of interest in the segment, driven by banks’ reluctance to provide loans since the financial crisis, de Bree said.

Viewed independently or in a larger context, the flurry of activity in Australia is new. “The boom is probably only getting started,” Bertoli maintained in a reference to the Australian market. “Right now, it’s about getting the foundation of the market established.”

To get the business underway in Australia, alternative funders are alerting small-business owners and the media to the fact that alternative funding is becoming available and teaching them how it works, de Bree said. “Half of our job is educating the market,” noted Heussler.

New players are building the track record they need to bring down the cost of funds, according to Allegos. “Our base rate is 2 percent or 3 percent higher than yours,” he said, adding that the cost of funds is more challenging than gearing up the tech side of the business.

Although the alternative-lending business started later in Australia than in the United States and lags behind America in in exposure, it’s maturing rapidly, said de Bree. Aussie funders are benefitting from the lessons their counterparts have learned in the U.S., he said.

But the exchange of information flows both ways. Kabbage, for example, chose to enter the Australian market with a local partner, Kikka. Kabbage learned from its earlier foray into the United Kingdom that it makes sense to work with colleagues who understand the local regulatory system and culture, said Pete Steger, head of business development for Atlanta-based Kabbage.

But the exchange of information flows both ways. Kabbage, for example, chose to enter the Australian market with a local partner, Kikka. Kabbage learned from its earlier foray into the United Kingdom that it makes sense to work with colleagues who understand the local regulatory system and culture, said Pete Steger, head of business development for Atlanta-based Kabbage.

Such differences mean that risk-assessment platforms that work in the United States or Europe require localization before they can perform effectively in Australia, sources said.

Sydney-based Prospa, for example, got its start three years ago and has been working ever since with New York-based Strategic Funding Source to localize the SFS American risk-assessment platform for Australia, said Bertoli, who shares the company CEO title with Greg Moshal.

Moula, which has headquarters in Melbourne, sees so many differences among markets that it decided to build its own local platform from scratch, according to Allegos.

One key difference between the two markets is that Australia does not have positive credit reporting. “We have nothing that even comes close to a FICO score,” said Allegos. The only credit reporting centers on negative events, he said.

Without credit scores from credit bureaus, funders base their assessments of credit worthiness largely on transaction history. “It’s cash-flow analytics,” said Allegos. “It’s no different from the analysis you’re doing in your part of the world, but it becomes more significant” in the absence of positive credit reporting, he said.

Australia lacks credit scores at least partly because the country’s four main banks control most of the financial sector and choose not to release credit information, sources said. The banks have warded off attacks from all over the world because the regulatory environment supports them and because their management understands how to communicate with and sell to Australian customers, sources said.

The big banks – Commonwealth Bank, Westpac, Australia and New Zealand Banking Group, and National Australia Bank – set their own rules and have kept money tight by requiring secured loans and long waiting periods, Bertoli said. It’s difficult for merchants who don’t fit into a “particular box” to procure funding, he maintained. “It’s almost like an oligarchy,” Allegos said of the banks’ grip on the financial system.

Eventually, the banks may form partnerships with alternative lenders, but that day won’t come soon, in Allegos’ estimation. It could be 12 months or more away, he said.

Even as the financial system evolves, deep-seated differences will remain between Australia and the U.S. Most Americans and Australians speak English and share many views and values, but the cultures of the two countries differ greatly in ways that affect marketing, Bertoli said. “In your face” advertising that can work well with “loud, confident” Americans can offend the more “laid-back” Australian consumers and business owners, he said.

Australians have become tech-savvy and comfortable with online banking, but they guard their privacy and often hesitate to reveal their banking information to a funding company, Allegos said. The entrance of OnDeck and Kabbage should help familiarize potential customers with the practice of sharing data, he predicted.

Cost structures for businesses differ in Australia from the U.S., Bertoli noted. Australian companies pay higher rent and have to pay minimum wages set much higher than in the United States, he said. Published reports set the Australian minimum wage at $13.66 U.S. dollars. The higher costs down under can take a toll on cash flow. “Take an American scorecard and apply it to Australia?” Bertoli asked rhetorically. “You just can’t.”

Distribution’s not the same for commercial enterprises in the two countries, Bertoli maintained. Despite having about the same geographic area as America’s 48 contiguous states, Australia has a population of 23 million, compared with America’s 322 million.

Distribution’s not the same for commercial enterprises in the two countries, Bertoli maintained. Despite having about the same geographic area as America’s 48 contiguous states, Australia has a population of 23 million, compared with America’s 322 million.

No matter how many people are involved, changing their habits takes time. Australian merchants prefer fixed-term loans or lines of credits instead of merchant cash advances, Bertoli said. In many cases Australian merchants simply aren’t as familiar as Americans are with advances, Allegos said.

Besides, the four big banks in Australia tend to solicit merchants for credit and debit card transactions without the help of the independent sales organizations and sales agents. In the U.S., ISOs and agents play an important role in explaining and promoting advances to merchants, Bertoli said. Advances make sense for merchants because advances adjust to cash flow, and they help funders control risk, but just haven’t caught on in Australia, Bertoli said. Australians resist advances if too many fees are attached, said Allegos.

Pledging a portion of daily card receipts might seem too frequent, too, he said. Besides, advances are limited to merchants who accept debit and credit cards, while any business could conceivably choose to take out a loan, said de Bree.

Advances have to compete with inventory factoring, which has become a massive business in Australia, according to Heussler. The business can become intrusive because funders may have to examine balance sheets and talk to customers, he said.

Australia’s reluctance to turn to advances, leaves most alternative funders promoting loans and lines of credit. Prospa, for example, uses some brokers to that end but also relies on online connections, direct contact with customers, and referrals from companies that buy and sell with small and medium-sized businesses.

“Anyone that touches a small business is a potential partner,” said Heussler, including finance brokers, accountants, lawyers and even credit unions, which have the distribution but not the product.

Moula finds that most of its business comes from well-established companies and that loans average just over $27,000 in U.S. currency and they offer loans of up to more than $77,000 U.S. The company offers straight-line, six- to 12-month amortizing loans.

Using a model that differs from what’s common in the U.S., Moula charges 1 percent every two weeks, collects payments every two weeks and charges no additional fees, Allegos said. A $10,000 (Australian) loan for six months would accrue $714 (Australian) in interest, he noted.

Spotcap Australia offers a three-month unsecured line of credit and doesn’t charge customers for setting it up, Heussler said. If the business owner decided to draw down, it turns into a six-month amortizing business loan for up to $100,000 Australian. Rates vary according to risk, starting at half a percent per month but averaging 1.5% per month.

Spotcap Australia offers a three-month unsecured line of credit and doesn’t charge customers for setting it up, Heussler said. If the business owner decided to draw down, it turns into a six-month amortizing business loan for up to $100,000 Australian. Rates vary according to risk, starting at half a percent per month but averaging 1.5% per month.

If companies have all of the necessary information at hand, they can complete an application in 10 minutes, Allegos said. Moula has to research some applications offline if the company’s structure deviates too greatly from the usual examples – much the same as in the U.S., he maintained. The latter requires strong customer-service departments, he said.

Kikka uses a platform based on the Kabbage model, which gives 95 percent of customers a 100-percent automated experience, Steger said. “It goes to show the power of our automation, our algorithms and our platform,” he maintained.

Spotcap prefers to deal with businesses that have been operating for at least six months, Heusler said. The funder examines records for Australia’s value-added tax and other financials, and it likes to connect with the merchant’s bank account. Spotcap can usually gain access to the account information through cloud-based accounting systems and thus doesn’t require most companies to download a lot of financial documents, he noted.

Despite the differences between the two countries, banking regulations bear similarities in Australia and the United States, sources said. In both nations the government tries harder to protect consumers than businesses because they assume business owners are more financially savvy. For consumers, regulators scrutinize length of term and pricing, sources said, and on the commercial side the government is concerned about money laundering and privacy.

Regulation of commercial funding will probably intensify, however, to ward off predatory lending, Bertoli said. Government will consult with businesses before imposing rules, he said. A couple of alternative business funders aren’t transparent with their pricing and they charge several fees – that sort of behavior will encourage regulation, Allegos said.

“I know they’re watching us – and watching us very closely,” he added.

In general, however, the Australian government supports alternative finance, Bertoli said, because they want there to be options other than the four big banks and wants small business to have access to capital. Small businesses account for 46 percent of economic activity in Australia and employ 70 percent of the workforce, he noted, saying that “if small businesses are doing badly, the economy is doing badly.”

Hence the need, many in the industry would say, for more alternative funding options in Australia.

Stock Slump Makes Marketplace Lending Look Like Safe Haven

September 2, 2015 The premium might be gone in peer-to-peer lending, but a step forward is definitely still better than three steps back. Probably the most frustrating thing for long term investors in the stock market is the day-to-day volatility. Some of it’s rational, and some of it’s just, well, who knows…. it’s the stock market.

The premium might be gone in peer-to-peer lending, but a step forward is definitely still better than three steps back. Probably the most frustrating thing for long term investors in the stock market is the day-to-day volatility. Some of it’s rational, and some of it’s just, well, who knows…. it’s the stock market.

It’s a hopeless feeling to see your stock portfolio balance drop substantially all because something is happening in China. But if you’ve diversified your overall investment portfolio beyond just stocks, it’s not all bad right now. It’s actually a bit of a golden era.

On Lending Club, my portfolio’s Adjusted Net Annualized Return is 8%. On Prosper, my Annualized Return is 11%, though that portfolio is younger and smaller. And then there’s my merchant cash advance portfolio which is beating both of those by a long shot.

These investments are a wonderful balance to the stock market because they don’t care what’s happening in China either. It’s times like these though when you need to be patient and not overreact. The easy mistake to make right now is to substantially reallocate your portfolio so that the majority of your capital is in marketplace loans.

LendingMemo’s Simon Cunningham believes that having 20% of your portfolio in peer-to-peer lending investments is reasonable.

And Lend Academy founder Peter Renton told Equities.com last year that, “The official word from the platforms is that you should not invest more than 10 percent of your net worth.” He also went on to say that some people are putting half their life savings into this and that it’s probably not a good idea.

And he’s right. As volatile as stocks can be, your steep loss today can be erased by a rally tomorrow. With notes backed by the performance of loans, a loss today can’t just rally back tomorrow. When the loans go bad, the money is gone and thus the risk of loss is a little bit more permanent since you can’t just ride it out.

In that same interview, Renton said, “If there were another 2008 or 2009 now, I feel very confident that my returns would remain positive. I’m earning close to 12 percent right now. If there were another 2008-9 right now, I might go down to 6 percent.”

I think that’s probably a best case scenario in a worst case scenario. Everyone should plan for events or contingencies that will lead to losses. If there were no possible outcomes that could lead to losses, then the market has obviously mispriced the loans and I don’t believe that has happened.

One nightmare scenario to consider for example, is if the loans are invalidated by a court. Oddly enough, this very possibility is being discussed after the outcome of the Madden v. Midland ruling which hurt the reliance on chartered banks to originate loans. Lending Club’s CEO answered concerns over that by saying they were protected by their choice of law provision, a safeguard that just recently proved to be imperfect.

As Patrick Siegfried, Esq, wrote, “Last Thursday, the Attorney General of North Carolina was granted an injunction against Western Sky Financial and CashCall prohibiting them from offering any loans to North Carolina consumers or collecting on any outstanding accounts in that state.” The companies pointed to their choice of law provisions that supposedly made the rates permissible. This practice is actually commonplace for alternative lenders. But Siegfried said, “Because the Attorney General was not a party to the agreements, the court found that the Attorney General was not bound by the agreements’ choice of law. Therefore it could enforce North Carolina’s usury laws against the defendants.”

Now however remote the possibility of judicial or regulatory invalidation of loans, it is sobering possibilities like these that should prevent anyone from putting half their life savings into marketplace lending. It is a nice complement to a portfolio of stocks, but not a replacement for one.

Over the last week, my marketplace lending portfolios have been a bright spot and a source of optimism in a news cycle and market that has suddenly turned bearish. I’m tempted to reallocate my investments accordingly, but I’m not going to.

Hopefully you won’t make any impulsive maneuvers either…

Regulator Disregards Choice of Law Provision in Usury Enforcement Action

September 1, 2015 Last Thursday, the Attorney General of North Carolina was granted an injunction against Western Sky Financial and CashCall prohibiting them from offering any loans to North Carolina consumers or collecting on any outstanding accounts in that state. The Attorney General argued that the payday loans offered by the defendants violated North Carolina’s usury laws.

Last Thursday, the Attorney General of North Carolina was granted an injunction against Western Sky Financial and CashCall prohibiting them from offering any loans to North Carolina consumers or collecting on any outstanding accounts in that state. The Attorney General argued that the payday loans offered by the defendants violated North Carolina’s usury laws.

The defendants countered that the loan agreements at issue included choice of law provisions that made the law of the Cheyenne River Sioux Tribe the governing law. The defendants argued that the rates charged were permissible under tribal law.

The Superior Court rejected the defendants’ arguments and granted the Attorney General’s request for the injunction. The court reasoned that the Attorney General “was not a party to the Loan Agreements, but instead [wa]s acting as an enforcement arm of the State of North Carolina.” Because the Attorney General was not a party to the agreements, the court found that the Attorney General was not bound by the agreements’ choice of law. Therefore it could enforce North Carolina’s usury laws against the defendants.

In support of its ruling, the court cited BankWest, Inc. v. Oxendine. In that case, the Georgia Court of Appeals held that “[t]he parties to a private contract who admittedly make loans to Georgia residents cannot, by virtue of a choice of law provision, exempt themselves from investigation for potential violations of Georgia’s usury laws.” 462 Mass. 164, 172 (2012).

These cases are concerning for lenders that engage in interstate lending activities because they undermine the use of choice of law provisions as a method of usury law compliance. Choice of law provisions serve dual purposes. By selecting the governing law beforehand, a lender can be more confident that the terms of its loan agreement will be enforceable against a debtor. Additionally, a choice of law provision narrows the number of states that could potentially have an interest in the transaction. This limits the number of laws the lender must comply with.

These decisions, however, cast doubt on a lender’s ability to rely on a choice of law clause when faced with a regulatory enforcement action. This could result in the paradoxical situation where a court permits a lender to enforce a choice of law clause to collect interest on a contract but at the same time allows a state regulator to bring a usury action against the lender based on the exact same contract.

Federal Reserve Publishes Results of Alternative Lending Focus Groups

August 26, 2015 Alternative lenders have a lot of work to do!

Alternative lenders have a lot of work to do!

In a study conducted by the Federal Reserve which included focus groups moderated by the Nielsen Company, small business owners that had not heard of online lenders or had not used them, expressed extreme skepticism about their legitimacy. Among the negative responses were words such as shady, scam, identity theft, high APRs, ridiculous, wild west and unregulated, among others.

The focus groups, while small, had to meet a minimum criteria to be eligible:

- Have 2 to 20 employees

- Have annual revenues between $200,000 and $2 million

- Be the financial decision maker

- Not be a new business

Only 44 people participated.

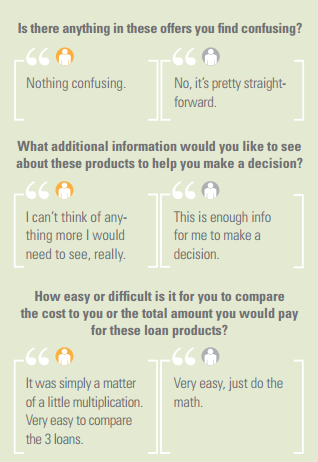

There were both bright and dark spots in the findings, with one of the bright spots being that people’s attitudes became more positive about online lenders once they started to actually navigate the websites of several big industry players.

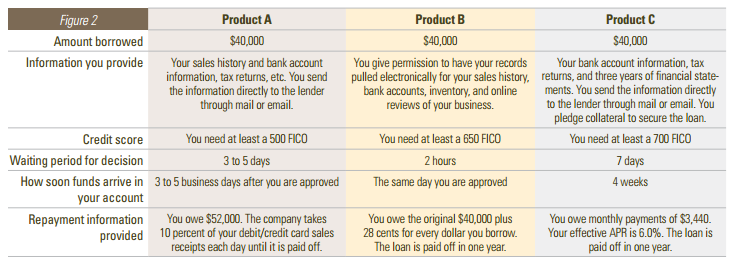

While the extent of the research is significant for any lender trying to get into the mind of a small business owner, there was a section in particular that warrants closer attention. In a mock comparison, participants were asked to compare three unnamed financial products, with one supposedly representing the characteristics of a merchant cash advance based on future credit card sales, another on a daily debit business loan, and the last a traditional bank loan.

Respondents generally reported that they understood these offers and were not confused by them.

Unfortunately, the researchers assigned some gut-wrenching characteristics to the structure of the product alleged to represent merchant cash advances (Product A).

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

Since the researchers presented the theoretical product as a loan, not a sale, they have potentially tainted the inferred conclusions about the transparency of future receivable transactions. Given the strong authority associated with the Federal Reserve and Nielsen, there is a troubling implication that the findings about a hypothetical loan could be used as a basis to make future regulatory decisions about unrelated products like receivable purchases.

Ironically, the diversity of wrong answers to the interest rate question could lead one to this conclusion though, that APRs wouldn’t necessarily be a transparency cure.

If business owners don’t understand what Annual Percentage Rates represent, then it might not be a very good medium to make comparisons. This argument is actually reinforced by the study’s own research since two of the three products were presented without the confusion of interest rates and “participants initially reported the three were easy to compare and that they had all the information they needed to make a borrowing decision.”

In regards to the traditional bank loan, one business owner is actually quoted as saying, “I am not sure what they mean by my ‘effective APR.'”

While value can be gleaned from the results of such a small sample size of 44 business owners, it’s obvious that the researchers influenced the participants answers on how they assessed the cost of merchant cash advances in particular.

- A transaction typically structured as a sale was presented to participants as a loan.

- A predetermined time frame of 1 year was provided to participants when they were asked about interest rates even though purchase transactions have no time frame.

The merchant cash advance product presented in the focus groups has just about no similarities to the purchase transactions that exist in real life.

What are your thoughts on this report and particularly the way merchant cash advance is framed in it? You can download the full report, including the focus group questionnaire here.

Alternative Lending Becoming Less Alternative

August 23, 2015 Alternative funders are looking a little more like bankers these days, but that’s not to say they’re developing a taste for pinstriped three-piece suits and pocket watches on gold chains. They’re promoting bank loans, applying for California lending licenses and contemplating the unlikely possibility that one day they’ll obtain their own bank charters.

Alternative funders are looking a little more like bankers these days, but that’s not to say they’re developing a taste for pinstriped three-piece suits and pocket watches on gold chains. They’re promoting bank loans, applying for California lending licenses and contemplating the unlikely possibility that one day they’ll obtain their own bank charters.

“It’s what everybody’s talking about,” said Isaac Stern, CEO of Yellowstone Capital LLC, a New York- based funder. “If it’s not in their current plans, it’s in their longer-term plans over the next three to five years.”

Funders promote bank loans to drive down the cost of capital, sell a wider variety of products, offer longer terms and bask in the prestige of a bank’s approval, said Jared Weitz, CEO of United Capital Source.

Loans allow for much more customization than is possible with merchant cash advances, noted Glenn Goldman, CEO of Credibly, which was called RetailCapital until a little less than a year ago. The name changed as the company began offering loans in addition to it original advance business. It’s now working with three banks.

While the terms don’t vary much with advances, borrowers can pay back loans daily, weekly, semi-monthly or monthly, Goldman said. Loans can also include lines of credit that borrowers draw down only when they choose. Interest rates on loans can vary, too, he said, and loans can come due after differing periods of time.

Besides that flexibility, loans also offer familiarity among merchants and sales partners – unlike the sometimes baffling advances, Goldman said, adding that “everybody knows what a loan is, right?”

Loans have so many advantages over advances that Credibly expects its loan business to grow more quickly than its advance business, said Goldman, who was formerly CEO of CAN Capital.

Those advantages are also encouraging other advance companies to form partnerships with banks to provide merchants with loans that aren’t subject to state commercial usury laws, said Robert Cook, a partner at Hudson Cook LLC, a Hanover, Md.-based financial services law firm.

The advance company markets the loan to the customer, the bank makes the loan, and the advance company buys it back and services it at the rate the bank is allowed under federal law, Cook said. The bank doesn’t lose any capital, it takes on virtually no risk and it profits by collecting a few days’ interest or a fee, he noted.

Where the bank’s located can make a big difference. A bank based in New York, for example, can charge only 25 percent interest no matter where the customer resides, while New Jersey allows banks to collect unlimited interest anywhere in the country, Cook said.

But the partnerships funders are forming with banks could face a threat. The United States Court of Appeals for the Second Circuit ruled in May in Madden v. Midland Funding LLC that a non-bank that buys a loan cannot charge interest set where the bank is located but must instead charge interest according to the laws of the state where the consumer is located, Cook noted. That could mean a lower rate.

In Cook’s view the case was poorly argued, the decision was wrong and the ruling may be reversed, “but it has to trouble someone who is thinking about starting up a bank partnership,” he said.

The court was asked whether the rules that apply to a national bank also apply to the non-bank that bought the loan, Cook maintained. That’s not the question, he asserted. The argument should have been that the idea of “valid when made” should take precedence. It states that a transaction that’s not usurious when it’s made doesn’t become usurious if a party takes action later – like reassigning the note, Cook said.

Meanwhile, offering bank loans isn’t the only way alternative funders are coming to resemble banks. Some are obtaining what’s formally called a California Finance Lenders License that enables them to make loans in that state.

California began requiring the license in response to lawsuits over the cost of advances. The state has published a licensee rulebook that’s about the size of an old-school New York phone book – the kind kids sat on to reach the dining room table, according to Yellowstone’s Stern, who completed the licensing process three years ago.

Getting the license took 15 or 16 months and required lots of help from the legal team at Hudson Cook, Stern said. The state investigated his back- ground and fingerprinted him. The cost, including lawyers’ fees came to about $60,000, he recalled.

“Man, it was like pulling teeth to get that license,” Stern said. Keeping it’s not easy, either. “We guard that thing fiercely,” he maintained. “They’ll take away your license if you even sneeze the wrong way.”

The hassles have paid off, though, because Yellowstone now deals directly with California customers instead of sharing the profits with other companies licensed to operate there. What’s more, companies that don’t have licenses are sending business Yellowstone’s way.

The hassles have paid off, though, because Yellowstone now deals directly with California customers instead of sharing the profits with other companies licensed to operate there. What’s more, companies that don’t have licenses are sending business Yellowstone’s way.

Retaining the profits from loans is also prompting some funders to contemplate applying for their own bank charters. But Cook, the attorney from Hudson Cook, sees little or no chance of that happening.

Federal bank regulators are reluctant to grant charters to mono-line banks – institutions that perform only one financial-services function, Cook said. “It’s risky to put all your eggs into one basket,” he maintained.

Regulations make forming or acquiring a bank so difficult for businesses that want to make small loans at high rates, Cook said. “If that’s going to be their business plan, they’re not going to get a bank.” A state charter requires the approval of the Federal Deposit Insurance Corp., which isn’t likely, he noted.

Utah industrial banks and Utah industrial loan companies are insured by the Federal Deposit Insurance Corp. but aren’t considered bank holding companies, Cook said. However, that’s a regulatory loophole that may have closed and thus may no longer offer a way of becoming a bank, he noted.

Clearly, the complications surrounding bank loans, lending licenses and bank charters mean that becoming more bank-like requires more than a pinstriped suit.

Second Guessing Alternative Lending

August 21, 2015The best case scenario for the alternative lending industry is that every startup’s model is pure genius and all the founders’ assumptions are correct. To an extent, it kind of feels that way right now, that everyone’s riding this unstoppable growth train. I can barely go a half hour without getting an email alert telling me that yet another fintech player has raised millions to disrupt lending. The steady drumbeat of news validates ideas, concepts, and investments, and puts pressure on others to jump on board and join the party.

Meanwhile, industry conferences become self-reinforcing loops of assurance. They’re great places to hear what you already thought.

No, you’re brilliant!

No, you’re the brilliant one!

It’s incredibly easy to get caught up in it all. I am guilty of it myself sometimes. I know this because my pedestrian friends outside the industry have reacted to the investment opportunities in it with extreme skepticism.

“But isn’t this brilliant?!,” I ask them. Most are amused, but I’ve never convinced a pedestrian to invest in marketplace loans. They see flaws and risk all over it, and sometimes for reasons I hadn’t even considered. I compared these responses in my head with responses I’ve heard from industry professionals. Was the contrast in feelings reflective of differing philosophies? And do industry professionals just have more knowledge to think the way they do?

I had an epiphany when a colleague sent me a link to a short puzzle published on the NY Times website to see if I would arrive at the same conclusion that she did. I didn’t.

For the sake of fun and knowing what I’m talking about, you can take it here.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

According to a sample, a mere 9 percent heard at least three nos — even though there is no penalty or cost for being told no. 78 percent never even got one no before they guessed the answer. “It’s a lot more pleasant to hear ‘yes’,” the research claims. “This disappointment is a version of what psychologists and economists call confirmation bias. Not only are people more likely to believe information that fits their pre-existing beliefs, but they’re also more likely to go looking for such information.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The sobering viewpoint was immediately met with criticism, most notably by Mike Cagney, the CEO of SoFi. Cagney issued a direct response to Baker in own American Banker piece. Of Baker, he wrote, “While his intentions are good, his rationale is flawed.”

But whether or not you agree or disagree with what Baker wrote, he’s done the industry an enormous favor. He looked at it all and said “no.” According to the Times, “We’re much more likely to think about positive situations than negative ones, about why something might go right than wrong and about questions to which the answer is yes, not no.”

Keep that in mind when Baker wrote, “If an [Marketplace Lender] MPL can’t issue new loans — which will happen any time investors refuse to buy loans in the MPL marketplace — the transaction fees that are the MPLs’ main source of revenue and cash will instantly disappear, while expenses continue to mount. An MPL has to keep issuing loans to survive.”

Few people like to think about what would happen when or if investors refuse to buy loans. And when Cagney responds directly to this by saying, “The scenario he describes can’t happen,” one has to wonder if his rationale might be subject to confirmation bias. “If there is no buyer, MPLs simply stop lending,” he explained.

Rather than rebut Baker’s argument, he seems to confirm it. Without being able to issue loans, an MPL’s revenue will disappear, and therefore an MPL indeed has to keep issuing loans to survive. How else does an MPL stay in business if it stops lending?

Baker reminds us all that we have been here before. “When sentiment changes, the MPL investors’ rush to the exits will be no less swift than it was for traditional finance companies in 2007-8 or in the Russian and Asian debt crises of the late 1990s,” he writes. He alludes that large swaths of industry professionals have convinced themselves that things will be different this time even though history continues to repeat itself.

“There is too much money to be made before the inevitable blow-up,” he laments.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Nos are healthy and should be considered a welcome concept in this industry. Those working on credit models should remember that it’s not just about confirming your theories, but also about disproving them. Build your model and then try to destroy it. Test things that you think won’t work in addition to the things you think will work. Go out there and break things. Run worst case scenarios. Fund money to a deal that you think will go bad. See what happens.

“Often, people never even think about asking questions that would produce a negative answer when trying to solve a problem — like this one. They instead restrict the universe of possible questions to those that might potentially yield a ‘yes’,” says the Times. This flawed approach could lead to catastrophe.

In The Quants: How a New Breed of Math Whizzes Conquered Wall Street and Nearly Destroyed It, odd scenarios not accounted for in computerized trading models led to disastrous losses. At times, the quants’ computers refused to acknowledge events that were actually happening because the built-in models believed they were too statistically impossible.

So when SoFi’s Cagney says, “the scenario [Baker] describes can’t happen,” in regards to the potential of an MPL failing because there are too few loan buyers, it should be taken with a grain of salt. Of course it can happen.

But it should also be mentioned that SoFi is now worth about $4 billion. That means that in a room full of alleged geniuses, Cagney is a certifiable genius. But there’s no way someone in his position would raise a fresh billion dollar round of capital and then concede to American Banker that the whole system could be torn to shreds at any moment.

The danger is that others will point to Cagney as validation that their own lending aspirations are viable even when their own models and market positioning are substantially weaker. Not every new lending startup CEO is Mike Cagney. And there is plenty of truth in Baker’s opening line, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

A lot of arguments have been put forth about why everything is different this time, that it is impossible to fail, but we may find out just as we have countless times before that this isn’t the case.

It’s refreshing to hear someone second guess the whole industry. Hopefully if you’re a player in this space, you’ve thought of reasons why your business might be flawed. If you’re like 78% of the population that’s too scared to even get one no before committing to an answer, you’re probably in big trouble…

Reactions to the Treasury RFI: Business Lenders and Merchant Cash Advance Companies Share Their Thoughts

August 13, 2015 The Treasury Department could get an earful from the alternative funding industry during a 45-day public comment period on online marketplace lending that began July 17.

The Treasury Department could get an earful from the alternative funding industry during a 45-day public comment period on online marketplace lending that began July 17.

Treasury emphasizes that it isn’t a regulator and its Request for Information, or RFI, isn’t a regulatory action. The department just wants to hear success stories and opinions on potential public policy issues, a Treasury spokesman said.

“There isn’t a lot of data available on this industry,” the spokesman noted. “The RFI allows us to gather information from the public.”

One portion of the public – alternative funding executives – may have a lot to say on the subject. At least some of the industry’s top players favor regulation or legislation that could clean up the industry and clarify conflicting directives.

“Personally, I’d be glad to see it on the federal level,” Stephen Sheinbaum, president and CEO of Merchant Cash and Capital, said of regulation. “We won’t have to deal with 50 individual states, which is more unruly.”

Others would prefer to see the industry regulate itself instead of having federal agencies issue dictates or having Congress pass laws.

“I would like to put in my two cents,” said Asaf Mengelgrein, owner and president of Fusion Capital, indicating he intended to respond to the RFI. “I see a need for better practices, but regulation should come internally.”

Whoever makes the rules, restrictions seem inevitable because of alternative funding’s prodigious growth, executives agreed. “Regulatory attention is a sign of an emerging industry,” said Marc Glazer, president and CEO of Business Financial Services.

Regulation should curb the practice of stacking loans or advances, which can burden merchants with more financial obligations than they can meet, Sheinbaum said. Stacking has proliferated even though ethical members of the industry avoid it, he said.

At the same time, disclosure statements should become more transparent so that merchants can easily identify how much they’re paying in fees and expenses, Sheinbaum maintained. Merchants should also be able to see how much they’re paying the different entities involved in the deal, he said.

“I’m not suggesting someone should make more or less, but transparency is a healthy thing and this industry could use a little more of it,” Sheinbaum said.

The alternative-funding industry could follow the example of the mortgage business, where more-standardized forms help consumers compare competing offers, Sheinbaum said. “That’s not the case in this industry, so that might help,” he maintained.

The alternative-funding industry could follow the example of the mortgage business, where more-standardized forms help consumers compare competing offers, Sheinbaum said. “That’s not the case in this industry, so that might help,” he maintained.

The industry should not emulate the credit card processing business, which uses complicated and dissimilar contracts to keep customers uniformed, Sheinbaum said. “It’s not so easy for a merchant to understand the effective cost of a transaction – and that’s by design,” he said.

Reviewing those issues could confuse among regulators who don’t understand the industry, Mengelgrein warned. Someone “on the outside looking in” might consider the industry’s fees and factor rates outrageously high, but that’s because they fail to understand the financial risk involved with lending to small businesses, he said.

Before imposing rules, regulators should also bear in mind that many small businesses could not survive without alternative funding, Mengelgrein continued. In recent years banks have failed to step up and help merchants in need of cash, and the alternative lending community has filled the gap.

Sheinbaum agreed. “I hope the regulators and legislators will make an earnest effort to understand all the good that folks in the alternative finance space provide for people,” he maintained. “It’s a critical role we play in keeping small businesses going, and small business is important to this country.”

The Small Business Finance Association could play a critical role in helping government understand the industry, Sheinbaum suggested. He noted that the trade group changed its name from the North American Merchant Advance Association because the industry is adding loans to its initial offering of merchant cash advances.

Whatever shape regulation takes, the industry should keep up with the new rules, Glazer cautioned. “As this industry evolves, we will work closely with our partners and our customers to ensure that everyone is informed about any new regulations and the potential impact that they may have on our business,” he said.

Meanwhile, Treasury’s efforts to comprehend the business are continuing. Its RFI contains 14 detailed questions that respondents could address.

The department held a forum on Aug. 5 called “Expanding Access to Credit through Online Marketplace Lenders.” The event included two panel discussions and roundtable discussions with Treasury staff.

Attendees numbered about 80 and included consumer advocates, representatives of nonprofit public policy organizations and members of the financial services industry, the department said.

Ignoring Cease and Desist Letters – Just Don’t Do It

August 12, 2015 Usury law is complex. It is an area of law heavily burdened with obscure exceptions and antiquated nuances. Yet, one point is clear.

Usury law is complex. It is an area of law heavily burdened with obscure exceptions and antiquated nuances. Yet, one point is clear.

No matter how clear the case law, sophisticated the compliance program or lax the regulator, when a business receives a cease and desist letter from a state or federal authority it must be addressed. To do nothing risks litigation and worse. Case in point is the recent complaint filed by the CFPB against payday lender NDG Financial Corp. and its affiliates.

According to the complaint, NDG received cease and desist letters regarding its lending practices from Michigan (2014), California (2012, 2013, and 2014), Virginia (2013), New Hampshire (2011), Maine (2011), Oregon (2011), and Pennsylvania (2010). And though NDG stopped lending in some of these jurisdictions, it apparently felt confident enough to continue its operations in a number of these states even after receiving the letters. Partly as a result, the Bureau filed suit.

Now, I am in no way suggesting that CFPB will prevail in its claims against NDG or that merely receiving a cease and desist letter is evidence of wrongdoing. As a recent post of mine shows, regulators are often incorrect in their interpretation of usury law. That being said, the number of previous warnings NDG received from state regulators prior to being sued is stunning. So it seems to me that NDG is somewhat responsible for the targeting it has received from the CFPB.

If a lender has received 8 cease and desist letters within a 4 year period, there is a problem. It doesn’t mean it must immediately stop all lending. But it would be wise to undertake a greater review of its operations and, hopefully, generate a plan to address the regulators’ concerns.

Placing one’s head in the sand just won’t cut it.