Credibly Secures $70 Million Credit Facility Led by Suntrust Bank

February 2, 2016NEW YORK—February 2, 2016—Credibly, a tech and data-inspired lending platform that makes access to capital for small businesses simple and intuitive, announces the closing of a $70 million credit facility with SunTrust Bank, one of the nation’s largest financial services firms, and Alostar Bank of Commerce, a specialty provider of asset-based loans. SunTrust served as the structuring and administrative agent, committing $50 million, with Alostar coming in as the first participant with a $20 million commitment. The terms of the deal allow for flexibility to increase the committed amount by another $30 million, bringing the total facility potential to $100 million.

An online lending platform that delivers a broad range of short- and long-term capital to satisfy the entire SMB credit spectrum, Credibly has provided access to capital for more than 4,500 businesses in over 300 industries. In the past year, the company has increased revenue 100%, was recognized by Crain’s as one of the 50 fastest growing companies in New York, and made its second consecutive appearance on the Inc. 500 list of the fastest growing private companies in America.

The new credit facility is consistent with Credibly’s three-prong financing strategy: on-balance sheet, whole loan sales, and securitization. The facility more than doubles Credibly’s onbalance sheet funding capacity, accelerating their ability to provide more small businesses with access to affordable capital, regardless of credit profile or life cycle stage.

“Being vetted and validated by a bank partner of SunTrust’s stature is one of our greatest milestones to date, and provides us with one of the lowest costs of capital in the industry,” said Glenn Goldman, CEO of Credibly. “The continued participation from Alostar – our first credit facility lender going back to 2014 – gives us increased flexibility in our product suite, which in turn provides better terms for borrowers and helps us execute on our core philosophy that all small businesses deserve access to right-sized capital.”

“SunTrust is pleased to work with Credibly to assist them in achieving their mission to fuel American entrepreneurship through access to capital,” said Tarun Mehta, Group Head, Financial Institutions Investment Banking at SunTrust Robinson Humphrey.

“The new SunTrust facility is a validation of the strength of the platform and team that Credibly has built. We remain extremely excited about our partnership with Glenn and his team” said Steve Begleiter, Managing Director at Flexpoint Ford, LLC, a private equity firm that added Credibly to its portfolio in 2014.

About Credibly

Founded in 2010 and with offices in Michigan, Arizona, Massachusetts, and New York, Credibly is a best-in-class Fintech platform that leverages data science and analytics to improve the speed, cost, and choice of capital available to small businesses in the United States. Credibly is dedicated to creating a superior borrowing experience that meets the needs of all small businesses, regardless of product need or credit profile. All loans obtained through Credibly are made by WebBank, a Utah-chartered industrial bank and member of the FDIC. Learn more at www.credibly.com.

About SunTrust Banks, Inc.

SunTrust Banks, Inc., one of the nation’s largest financial services organizations, is dedicated to Lighting the Way to Financial Well-Being for its clients and communities. Headquartered in Atlanta, the company serves a broad range of consumer, commercial, corporate and institutional clients. As of September 30, 2015, SunTrust had total assets of $187 billion and total deposits of $146 billion. Through its flagship subsidiary, SunTrust Bank, the company operates an extensive branch and ATM network throughout the high-growth Southeast and Mid-Atlantic States and a full array of technology-based, 24-hour delivery channels. The company also serves clients in selected markets nationally. Its primary businesses include deposit, credit, trust and investment services. Through its various subsidiaries, the company provides mortgage banking, asset management, securities brokerage, and capital market services. Learn more at www.suntrust.com.

About AloStar Bank of Commerce

AloStar Bank of Commerce, with $900 million in assets, is a specialty lender with extensive experience in providing Asset Based Loans to middle market companies. In addition, the bank provides value for depositors, small-to-medium-sized companies and community banks across the country through on-line customer service, and unique lending products and services. Learn more at www.alostarbank.com.

Industry Trade Group Coming of Age: The SBFA is Becoming More Political

February 1, 2016By hiring an executive director, the Small Business Finance Association hopes to achieve at least two goals – taking a step toward becoming a full-service trade group and providing a public voice for the alternative finance industry.

Stephen Denis, formerly deputy staff director of the U.S. House Committee on Small Business, went to work in the new role in mid-December, setting up shop with his cell phone and laptop in a Washington, DC, area coffee emporium. He’s the SBFA’s first full-time employee.

Hiring Denis, who also has association experience, represents “the next evolution” of the trade group, according to David Goldin, SBFA president and Capify’s founder, president and CEO.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

“The goal is to start from scratch and take a look at everything the association is doing,” Denis told AltFinanceDaily, “and to really build this out to a robust group that represents the interests of small businesses.”

Denis appears optimistic about pursuing that goal. He’s a native of the Boston area and a Harvard University graduate whose first job out of school was as an aide to Republican Sen. John E. Sununu of New Hampshire. After three years in that position, he took a job for two years with a UK-based trade association, traveling frequently to London to inform the group of Congressional action in the United States.

From there, Denis went on to become director of government affairs and economic development for the Cincinnati Business Committee, a regional association that included Fortune 500 companies among its members. After two years in that role, Denis joined the staff of Rep. Steve Chabot, R-Ohio, moving back to Washington and serving as the congressman’s deputy chief of staff during a five-year stint that ended when he joined the SBFA.

While working for Chabot, Denis also became deputy staff director of the House Committee for Small Business, the No. 2 position there, and he has held that job for the last three years. The committee’s tasks include learning as much as they can about small business, including financing, and using the information to advise members of the House on policy initiatives.

The experience Denis has amassed in government should serve the association well because his duties include briefing federal legislators and regulators on how the alternative-finance business works. With Denis as spokesperson, the industry can speak to government with a single voice, Goldin asserted.

“We are going to be aggressive in our outreach to legislators and regulators as well as be active reaching out to local, state governments,” Denis said. The SBFA will “work with other trade groups and small business groups to promote our mission to ensure small businesses have alternative finance options available to them.”

Until now, too many players from the alternative finance industry have been vying for lawmakers’ attention, Goldin said. To make matters worse, some of those seeking to influence government in hearings on Capitol Hill are brokers instead of lenders and thus may not have a perfect understanding of risk and other aspects of the business, he maintained.

“We’re hearing that there are people trying to be the voice of small-business finance that either don’t have a lot of years of experience or they’re not telling the whole story,” Goldin said. “We want to make sure the industry’s represented properly.”

Denis can draw attention away from the “noise” created by unqualified voices and focus on information that Congress needs to make reasonable decisions about the alternative finance business, Goldin maintained.

Besides getting the word out in Washington, the SBFA hopes to convey its message to the general public on “the benefits of alternative financing,” Goldin said. At the same time the group can help make small business owners aware of the finance options, Denis added.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Meanwhile, updated “best practices” guidelines might be in the offing to help industry players navigate the business ethically and efficiently, Goldin said. A set of six best practices the association released in 2011 included clear disclosure of fees, clear disclosure of recourse, sensitivity to a merchants’ cash flow, making sure advances aren’t presented as loans and paying off outstanding balances on previous advances.

Addressing other possible steps in the association’s growth, Goldin said the group doesn’t plan to publish an industry trade magazine or newsletter. However, a trade show or conference might make sense, he noted.

Denis said he and the board had not discussed the possibility of a test, credential or accreditation to certify the expertise of qualified members of the industry. However, associations often establish and monitor such standards, so it would be reasonable for the SBFA to do so, he added.

The association might establish a Washington office, Goldin said. “We’ll look to Steve for his thoughts and guidance on that,” he observed. Denis seems amenable to the idea. “Down the road, we would love to open an office and hire more people,” he said.

In Goldin’s view, all of those moves might help the rest of the world comprehend the industry. Understanding the industry requires taking into account the cost of dealing with risk and business operations, he said.

Placing a $20,000 merchant cash advance, for example, requires a customer-acquisition effort that costs about $3,000 and a write-off of losses and overhead of about $4,000, Goldin said. That’s a total of $27,000 even without the cost of capital, he maintained.

“Most people don’t understand the economics of our business,” Goldin continued. The majority of placements are for less than $25,000, he said, characterizing them as “almost a loss leader when you factor in the acquisition costs.”

While spreading that type of information on the industry’s inner workings, Denis will also conduct the day-to-day for the not-for-profit’s affairs. The association’s board of directors will continue to set policy and objectives.

Members elect the board members to two-year terms. Current board members are Goldin; Jeremy Brown of Rapid Advance, who’s also serving as the group’s vice president; John D’Amico, GRP Funding; Stephen Sheinbaum, Bizfi; and John Snead, Merchants Capital Access.

Member companies include Bizfi, BFS Capital, Capify, Credibly, Elevate Funding, Fora Financial, GRP Funding, Merchant Capital Source, Merchants Capital Access (MCA), Nextwave Funding, NLYH Group LLC, North American Bancard, Principis Capital, Rapid Advance, Strategic Funding Source and Swift Capital.

Companies pay $3,000 in monthly dues, which Denis characterizes as inexpensive for a DC-based trade association.

Membership could spread to other types of businesses, Denis said. “I’d like to expand the tent to other industries,” he noted. “The association is trying to represent the interests of small business and make sure they have every finance option available to them.”

But a key purpose of the trade association is to provide a forum for members to come together as an industry, Denis said. “We’re thinking big,” he admitted. “We hope that all members of the marketplace will want to become a part of it.”

NetSuite Stakes Claim in Alternative Lending Industry

January 28, 2016NetSuite (NYSE: N), a San Mateo, CA based software company that employs thousands of people, has been planting their flag throughout the alternative lending industry. Earlier today, they announced that Avant, an online marketplace for consumer loans, has gone live on NetSuite OneWorld to manage their “mission-critical business processes.”

In September, Avant had received a private market valuation of nearly $2 billion after completing a Series E round, with one of the investors being JPMorgan Chase.

“Our previous system just couldn’t keep pace with the rapid growth we’ve seen in our industry and our business,” Avant CEO Al Goldstein is quoted as saying in the release. So they turned to a NetSuite product.

NetSuite has a public valuation of over $5 billion and is a popular choice in the alternative lending industry for companies who require scalability. For example, NetSuite OneWorld can support 190 currencies, 20 languages, and automate the tax compliance for over 100 countries. Avant already operates in 3 countries, The US, UK and Canada. More than 24,000 companies and subsidiaries use NetSuite.

“Avant is among a growing number of financial services companies innovating in a market that’s ripe for disruption and are relying on NetSuite’s cloud platform,” NetSuite President Jim McGreever is quoted as saying in their release. “We’re excited to see Avant’s success and look forward to helping them grow.

To date, Avant has issued more than 400,000 loans worldwide.

Several business lenders and merchant cash advance companies also use NetSuite.

Meet the Lending Platform With 0% Interest (Kiva)

January 6, 2016 Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Meet Kiva Zip, the anti-Lending Club because the borrowers are far from anonymous and the yield delivered to investors is negative due to inflation.

Angela’s Boutique, which is a real prospect on the Kiva Zip platform, includes a picture of the owner, her bio, endorsements, and comments from supporters.

According to Jessica Feingold, Kiva’s East Coast Manager of Development, “Kiva is the world’s first and largest crowdfunding platform for social good with a mission to connect people through lending to alleviate poverty and expand economic opportunity.”

And just like Lending Club, contributions as small as $25 are accepted. Obviously structured as a non-profit, “Kiva and its growing global community of 1.2 million lenders has crowdfunded more than $775 million in microloans to over 1.7 million entrepreneurs in 83 countries, all the while maintaining a 98% repayment rate,” according to Feingold.

Normally thought of as an overseas endeavor, Feingold said that “in 2011, Kiva launched Kiva Zip, a pilot program in the US that provides 0% interest crowdfunded loans to small business entrepreneurs.” Their underlying purpose and target market sounds very much like those being served by for-profit alternative lenders. “Kiva doesn’t require a minimum FICO score, collateral, or a minimum operations period for the business,” Feingold said.

Since inception they’ve made loans to over 1,800 borrowers in 47 days states, Peru, and Guam.

Notably, Lending Club promises borrowers that their “identity will at all times remain confidential and not be disclosed to anyone,” according to their website. Kiva by contrast is looking to “instill empathy” in their lenders. “We want to show that whether in East New York or Uganda, underserved entrepreneurs are credit-worthy, and will pay you back,” Feingold said. “All of these features on the Kiva websites enhance our ability to do so.”

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

According to the law, no loan underwriter or other officer or employee of a financial institution, or any affiliate of a financial institution, involved in making any determination concerning an application for credit shall have access to any information provided by the applicant about whether or not the business is women-owned or minority owned.

As small businesses often celebrate the heritage of their founders, and at times that can be the entire reason customers buy from them in the first place, the law has presumably put the small business lending world in an awkward position (and that’s why the law should be repealed). Non-profits like Kiva have embraced the very things that make a small business bankable outside of a credit score, like the owner, their background, and their story.

Borrowers on the Kiva Zip platform don’t raise all the money from strangers though. Their credit-worthiness is based on their ability to recruit friends and family to fund a small portion of their loan. The other lenders though of course may make their decisions based on the numbers or entirely on the perceived cultural, racial, or gender values of the borrower, all of the things that the CFPB is attempting to eradicate in the for-profit arena.

I didn’t ask Kiva any questions about Dodd Frank or Section 1071, but many people might empathize with their empathy approach as a way to fund small businesses that otherwise don’t qualify for bank loans. Its reminiscent of the subjective underwriting that a lot of alternative lenders and merchant cash advance companies employ to get deals done that banks won’t touch.

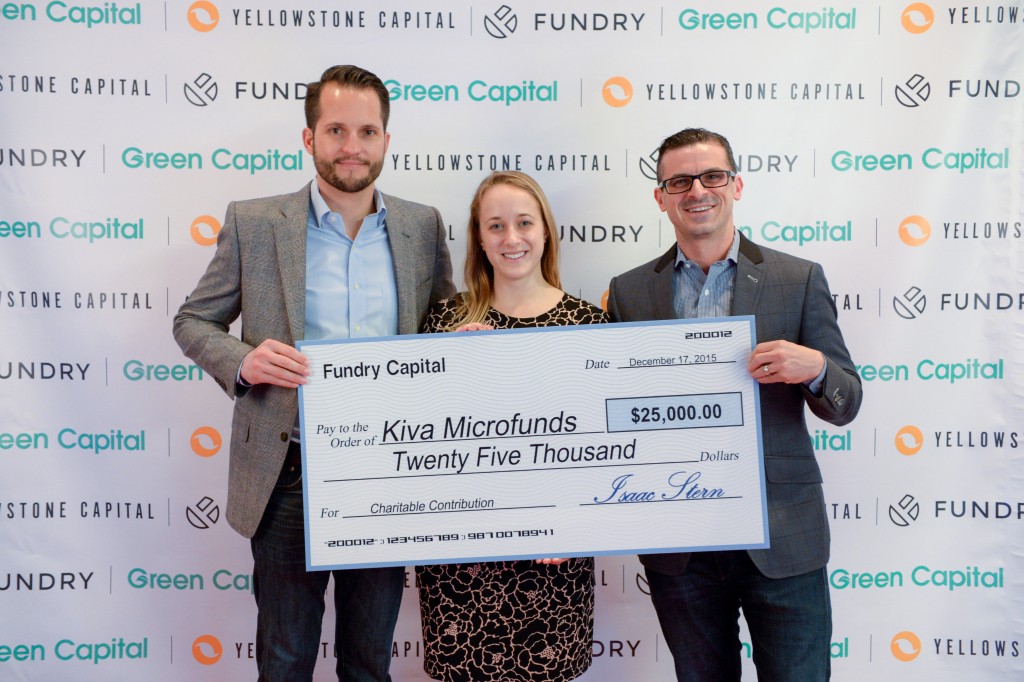

Not so coincidentally, Fundry, Yellowstone Capital’s parent company, donated $25,000 to Kiva just last month to support their cause.

Kiva’s Feingold (pictured at center above) said in regards to that, “Kiva is thrilled to receive a grant from Fundry to further our work to make credit more affordable.”

All in The Family (The MCA Kin)

December 20, 2015 FAMILY TIES

FAMILY TIES

During the holidays we get together with our family to reminisce on the good times, celebrate achievements, and be thankful for life’s fortunate moments. Most of the brokers within our space have families of their own to tend to during the holidays, which might include a large family gathering with relatives flying in from outside of the area, or it might just include a peaceful dinner with a small assembly.

But this has surely been the Year of the Broker, and what many of these new entrants might not realize is that the product we sell all year round (the merchant cash advance) has a family as well. While the MCA doesn’t exchange “gifts” with its kin, it sure does have a lineage that dates back to the 1600s, which makes the product something born out of a family of products, rather than something that seemingly just sprung up out of nowhere one day in 1998, by a company formerly known as AdvanceMe.

ALTERNATIVE FINANCE AND PURCHASING REVENUES HAVE BEEN AROUND A LONG TIME

- (The 1600s): The product is nothing but a purchase of future revenues or receivables, where a merchant is going to sell their receivables or future revenues to a purchaser, with a particular factor rate or “discount rate” applied to the transaction. This act is nothing new at all, as it has been around since the 1600s but didn’t become more common practice until around the 1800s in terms of the United States.

- (The Middle Of The 20th Century): The MCA is an alternative finance option from more boutique/niche firms, compared to the traditional products of terms loans and lines of credit from retail banks and credit unions. Alternative finance as a “comprehensive term” has been used in a mainstream fashion since the middle of the 20TH century, so this “act” is nothing new.

- (The Newborn): In other words, the merchant cash advance product is just the most recent “birth child” from a long and storied “family dynasty” of alternative financial services and revenue purchasers.

FAMILY GATHERING

The “family members” of the merchant cash advance include a variety of alternative financing vehicles that are popular and not as popular as others. For this article in particular, I wanted to discuss some of the more popular “family members” which include A/R Factoring, A/R Financing, P/O Financing, Equipment Leasing, Asset Based Lending and the Alternative Business Loan. This article will provide a general overview of each “family member”, which will serve as an introduction to a future article where I will go into specific sales strategies for many of the listings.

ACCOUNTS RECEIVABLE FACTORING

This product is based on a merchant having outstanding commercial receivables that are aged less than 60 – 90 days. With Factoring, the factor (buyer) is going to purchase the outstanding receivables from the merchant (seller), taking them off of the merchant’s balance sheet as an asset and onto the balance sheet of the factor. During the purchase, the factor advances about 80% of the amount purchased upfront to the merchant, with the remaining 20% coming after the merchant’s client base completes payment within 30 – 90 days, minus a discount fee of anywhere from 1% – 5%. Non-recourse factoring transfers the risk of the clients not paying the balances in full to the factor, while recourse factoring keeps the risk contained to the merchant.

ACCOUNTS RECEIVABLE FINANCING

This product is also based on a merchant having outstanding commercial receivables similar to Factoring, however unlike Factoring, there will be no purchase of the outstanding receivables but instead they will just be used as security/collateral for a financing arrangement.

PURCHASE ORDER FINANCING

This product is based on a merchant having outstanding purchase orders where a lender provides funds so a merchant can order materials to fulfill orders. Then once the orders are fulfilled, the lender collects a fee for service. This can also be done in the form of a vendor line of credit, where the lender opens a credit line with the vendor to allow the business to get materials needed to fulfill upcoming orders.

EQUIPMENT LEASING

This product basically allows a merchant in need of commercial equipment, technology, machinery, vehicles, tools, and furniture, to lease it rather than buying, as certain pieces go obsolete rather quickly and wouldn’t make sense for purchasing. The merchants are provided lease factor rates based on A-D credit grades, with options at the end of the lease to buy the unit(s) for $1.00, give them back, or start another lease period.

ASSET BASED LENDING

This product is based on a merchant having a particular type of pre-owned asset of appraised value, that could be used as security/collateral for a financing arrangement. The aforementioned Accounts Receivable Financing product can also be considered an asset based lending product, but also included are pre-owned pieces of equipment which could be used for sale-leasebacks or other items such as luxury vehicles, real estate, precious antiques and jewelry.

ALTERNATIVE BUSINESS LOAN

This product is similar to the merchant cash advance, as it’s based on a merchant having a particular consistent amount of monthly revenue, and approved as a percentage of annual gross revenue. The product can come from lenders that also offer merchant cash advance products or lenders who solely specialize in this alone.

AS A FINAL NOTE, MAKE SURE TO REMEMBER THE MCA’S VALUE

While the MCA is the baby in the family, don’t let its “youth” undermine its value. An MCA could potentially cost more than a loan, but a merchant might not be eligible for a loan or a loan might not be available fast enough to take advantage of a market opportunity. Merchants might not have assets available for collateral, eligible accounts receivable, and they might not issue invoices to customers on terms. That means merchants might have better luck with some family members than others just based on their business model or circumstances.

Happy Holidays.

Getting a California Lender’s License

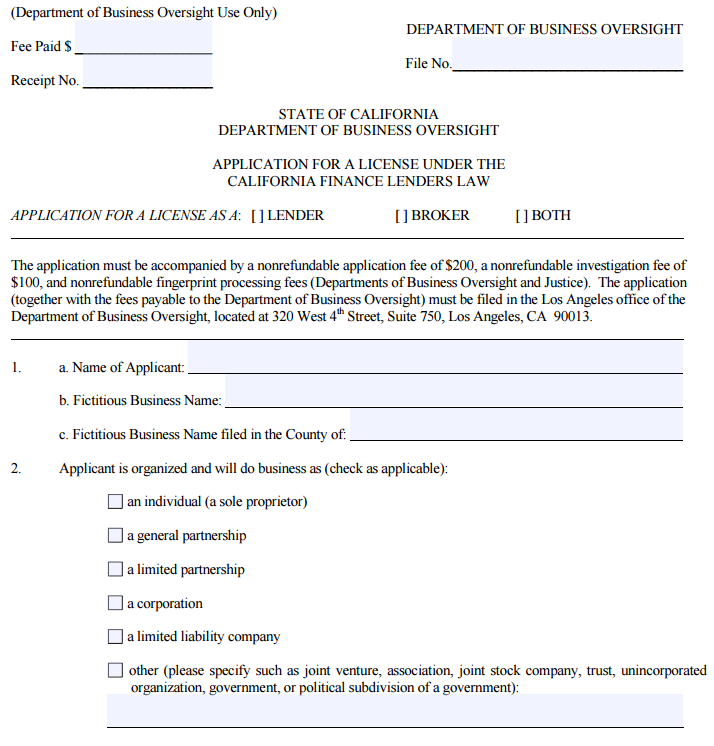

December 17, 2015Given the fact there have been a number of successful lawsuits against cash advance companies in California, many cash advance companies have decided to take a different route and get a lending license to provide loans to merchants in the state. If done correctly, this can allow companies to provide loans to merchants in California at roughly the same profit margins one could expect from a cash advance. Below I will discuss the process for obtaining a California lender’s license and some tips for making that process less painful.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

The first part of the application requests basic information about your company and its officers. In filling out this and other parts of the application, it is essential to respond to all the questions. If you fail to miss just one response the application will be rejected. To that end, even if a question does not apply to you I find it better to respond “N/A” or “not applicable” rather than just leaving a blank. By doing that you force yourself to fill in every blank and therefore reduce the chances for missing a response resulting in a rejection of your application.

Also, you need to be very precise in your responses. I have experienced a situation where the examiner rejected an application because the name of the company was incorrectly spelled on the application. The name of the company was submitted on the application with “Inc” instead of the complete “Inc.” at the end of the company’s name. The examiners are very good at what they do and very thorough. You need to make sure the packet you submit is perfect and also that there are no inconsistencies in the document.

Another important point to remember is that the application requires you to name the person that will be responsible for running the location where the lending is occurring. The main requirement is that the person running the location must be physically present at the location. As a result, you could not manage a California office remotely from New York for instance. In another twist, if your principal location is out of state, you will need to get the license and fill out the main application for that out of state address. For the California location, you will need to fill out the short form application in addition to the main application and submit the short form application as part of the packet to allow the license to apply to the location in the state of California.

There are a number of exhibits you also have to provide as part of the process. Some of them are simple like a balance sheet for the company. It is acceptable that the company is new and has little in the way of assets. You just have to make sure you attach a balance sheet and that it is prepared in compliance with generally accepted accounting principles. I have seen times when the balance sheet was rejected because there was no line items for liabilities for instance, even though the company was new and therefore had none. It is probably wise to engage your accountant to make sure you submit a balance sheet that complies with those guidelines.

You also have to get a surety bond in the amount of $25,000. There are readily available bonding companies that specialize in providing these bonds. In addition, you need some other exhibits like a statement of good standing for your company, authorization for financial disclosure, social security number (on a separate exhibit), organizational chart and a few other documents. As with the rest of the application the key is to make sure you include everything they are asking for exactly as requested.

The most involved exhibit is the “Statement of Identity and Questionnaire.” That exhibit has to be filled out for each owner, officer and manager listed on the application. It requests detailed information going back 10 years for each person for items like residence address and work history.

In addition, there are a series of questions on topics such as whether the person has been involved in lawsuits, had any licenses revoked or declared bankruptcy. Fingerprints are also taken as part of the process. This part of the application is trying to vet the various people working for the company to make sure they are suitable to be in the lending business.

Once you have all the documents prepared, you need to put them together in a packet to send off to the Department of Business Oversight to be reviewed. Again, I cannot overemphasize how important it is to completely and accurately answer the questions and put the packet together. You need to make sure things are in the proper order and complete. Triple check the application for errors and to make sure that packet is presented in the best manner possible. You also need to determine the amount of fees to submit with the application. Then, send the package by overnight delivery to make sure you have proof of delivery.

So what happens next? Well there is usually a bit of a wait. Typically it takes 3 months or more to get a reply. If you have done your homework, you might get lucky and successfully get your license on the first try. If there are any deficiencies, you will get a response letter from the State detailing the items that need to be corrected in the application and a time frame in which you have to respond or the application is abandoned.

On the first go round, you are usually given at least 2 months so you should have plenty of time. Digest the things they want and provide the required information. The deficiency letters are very detailed so it should be easy to make the requested changes. Resubmit the requested items and wait for the next response. It could be in the form of another deficiency letter but it could be an approval of the license. Just keep on trying until you are finally successful.

That’s it, you are finally a licensed lender in California! But that is where the fun begins. You are subject to many laws in California and audits by the State. To get the right to operate as a licensed lender, you need to make sure you prepare your application correctly. Once you have done that, you need to get all your loan documents drafted in compliance with California law. Make sure you have adequate experience and professional help to take on those tasks.

CAN Capital: Beyond Hyperbole

December 11, 2015 It’s usually risky to say “first,” “largest” or “best,” but CAN Capital invites those superlatives and more.

It’s usually risky to say “first,” “largest” or “best,” but CAN Capital invites those superlatives and more.

Asked whether the company’s the biggest in the alternative funding business, CEO Dan DeMeo hedges only a little with qualifiers like “might” or “probably” before proudly announcing that the company has provided access to more than $5.5 billion in working capital through 163,000 fundings to merchants operating in over 540 different kinds of businesses.

Glenn Goldman, the company’s CEO from 2001 to 2013 and now Credibly’s chief executive, doesn’t mince words about his former employer when he calls CAN Capital the biggest and most profitable small business alternative finance company in the U.S.

Cofounder and Chairman Gary Johnson proclaims without hesitation that CAN Capital was the first alternative small business finance company. His wife and cofounder, Barbara Johnson, came up with the idea of the Merchant Cash Advance in 1998 when she had trouble raising funds to promote her business, he said.

CAN Capital developed the first platform to split card receipts between the merchant and funder, and it gave birth to the idea of daily remittances, Johnson continued. Within a few years of its founding the company was turning a profit, another first in alternative finance, he claimed.

The innovation continued from there, according to Andrea L. Petro, executive vice president and division manager of Lender Finance, a division of Wells Fargo Capital Finance. She cited a couple of possible firsts she’s witnessed in her dealings with CAN Capital.

When CAN Capital received a loan from Wells Fargo in 2003, it may have been the first sizeable placement in the alternative finance industry by a major traditional financial institution, Petro said. In 2010, CAN Capital was among the first alternative funders to offer direct loans, she noted.

Petro stopped short of characterizing CAN Capital as the best in the alternative finance business, but she praised the company’s management and lauded its systems for underwriting and monitoring funding. “They continually upgrade their systems, upgrade their software, upgrade their people,” she said.

Calling CAN Capital one of the best comes naturally to Kevin Efrusy, a partner at Accel Partners and a CAN Capital board member. Accel saw opportunity in alternative finance because banks were reluctant to lend at the same time that an explosion of data on small businesses was informing the underwriting process. When Accel sought a position in the industry, it contacted CAN Capital, he said.

“Frankly, CAN Capital didn’t need or want our money,” Efrusy said. “We approached them.” Five years ago, Accel convinced CAN Capital that additional resources could help the company grow, and it bought a stake in the company.

With so many extolling the virtues of CAN Capital, AltFinanceDaily asked DeMeo for a look at the thinking that underlies the success.

PLOTTING STRATEGY

CAN Capital pursues a strategy that DeMeo visualizes as a honeycomb. In the center cell, he places the objective of “helping small businesses succeed.” The compartmental element above that provides a place for the goal of serving as “the preferred provider of financial solutions to small business,” he said. The company’s cultural values, summarized as “Care, Dare and Deliver,” reside in the compartment below the center cell as table stake underpinnings, he added.

DeMeo also describes the company as driven by four strategic planks: “1) Expand the market, 2) broaden the product set, 3) deepen relationships with customers, and 4) achieve operating excellence,” he said.

What does success look like to the company? To DeMeo, it’s dramatic growth in the number of customers, resulting in increased revenue, a more valuable company and better career opportunities. “Digital automation and customer experience are at the center of those efforts,” he said.

CAN Capital operates with a “huge appetite for ‘test and learn,’” according to DeMeo. “That’s how we keep innovation alive,” he said.

And the result of all that? The company has increased fundings by 29 percent (CAGR) and revenue by 24 percent (CAGR), with corresponding growth in earnings, DeMeo said. It has also grown its digital business by 600 percent since 2014, he noted.

AT THE WHEEL

AT THE WHEEL

DeMeo, the man at the top of CAN Capital, joined the company in 2010 as chief financial officer and became CEO early in 2013. He was previously CFO at 1st Financial Bank, and also served as CFO for JP Morgan Chase’s consumer and small business unit. DeMeo also was chief marketing officer and ran business development head for GE Capital’s consumer card unit. His career began at Citibank, where he held senior roles in marketing and customer analytics.

“I was very fortunate to work for some pedigree companies earlier in my career,” DeMeo said. “Those companies emphasized market based training and development, and I worked with very smart and hardworking people. I also had great experience in unsecured lending.” His formative years left him with great appreciation for “behavioral analytics and the quantitative, information-based approach to business finance.”

Experience convinced him, as a CEO, the importance of attention to the balance sheet and income statement. It’s vital to combine that with innovation and growth orientation, DeMeo said. He seeks to lead, inspire and motivate employees, he emphasized.

DeMeo grew up in Atlantic City, NJ, with parents who valued hard work, education and maximizing opportunity. His wife and three children have supported him in his career despite the long hours and dedication necessary for success.

At CAN Capital DeMeo has faced the challenge of managing the business through internal and external cycles. Running the company often comes down to balancing what customers want with what makes economic sense, he said. “Pigs eat, and hogs get slaughtered,” he maintained. “You can’t get too greedy.”

DeMeo runs the company without the help of a President or Chief Operating Officer. While DeMeo serves as the public face of the company, he also devotes himself to every aspect of operations, he said.

WHAT’S IN A NAME?

Although CAN Capital’s drive for technological innovation and its measured approach to fundings have remained constant, the company has renamed itself several times to fit changing times.

In November 2013, it rebranded itself publicly as CAN Capital, and the company now provides access to business loans through CAN Capital Asset Servicing Inc, and Merchant Cash Advances through CAN Capital Merchant Services.

With the CAN Capital rebranding, it dropped the umbrella name of Capital Access Network. At the same time, it retired the AdvanceMe, New Logic Business Loans and CapTap names.

Most of the company’s old names applied to products or distribution channels, DeMeo said. The company had added them when it presented a new product, such as loans, or introduced a way of going to market, like end-to-end digital technology.

Consolidating the names reflected the company’s decision to put its direct marketing efforts on equal footing with business generated by partner companies, DeMeo said. Having just one name would result in a more efficient approach to building a stronger brand, he noted.

“The opportunity is to create one brand, multiple products and omni channel distribution under one company,” he said. “For a company our size, it would be hard to create brand awareness if you had to put significant promotional support behind every one of those sub brands.”

CAN Connect is a sub-brand that has survived. “That’s not a product name or distribution channel name,” DeMeo said. “It’s the technology suite we use to connect with partners so that we can exchange information in real time.”

CAN Connect is a way to speed up the process and eliminate friction for customers and partners. For example, a partner is able to link their CRM directly into CAN Capital’s decision engine, eliminating manual steps in submitting and generating offers. For partners with a customer-facing portal, CAN Connect enables an offer to be made available in real time to a small business owner, taking advantage of data sharing APIs to tailor the marketing message to fit the prospective customer’s needs.

Attention to detail pays off in repeat business for CAN Capital, in DeMeo’s view. “Almost 70% of our merchants return for another contract,” he said

THE GENESIS

By all accounts, CAN Capital is a company born of necessity. Barbara Johnson, who had the brainstorm that became CAN Capital, was running four Gymboree playgroup franchises in Connecticut and needed funds to finance summertime direct marketing efforts for fall enrollment.

But her company didn’t have much in the way of assets to pledge, so banks weren’t interested in providing funds. Why, she reasoned, couldn’t she just borrow or receive an advance against the credit card receipts she knew would flow in when the kids came back in the autumn? Thus, she gave birth to an industry.

Barbara Johnson and her husband, direct marketing executive Gary Johnson, cofounded the company as Countrywide Business Alliance and put up their own money to build a computerized platform to split card revenue, Gary Johnson said.

Then they persuaded a card processor to partner with them. Once they were operating and had signed their first customer, venture capital began flowing their way to grow the business. These days, the Johnsons remain major shareholders.

“What made it an interesting concept was how huge the market potential was,” Gary Johnson said. “That’s what the attraction still is today.” Although Merchant Cash Advances may now seem commonplace, they were startling at first, he said. “When we first went out in the marketplace, everybody thought it was a crazy idea,” he noted.

The company earned patents on processing related to Merchant Cash Advances and daily remittances, Gary Johnson said. At first, the patents deterred potential competitors from entering the business, but the company was unable to defend the patents successfully in court. Rivals then entered the fray.

Just the same, the company became profitable early on through “deliberate decision-making, having the right people in place and being bigger than everybody else,” he said.

Much of the company’s early business came through firms that provide merchants with transaction services, and that remains the case today, DeMeo said. Many were placing point of sale terminals in stores and restaurants to accept credit cards, and working capital became an upsell or cross-sell, he noted.

The large base of business CAN Capital built with merchant services companies means it will always be an important channel for the company. Recently, new merchant sign-ups have come from more diverse channels, including cobranded and referral partners, and the fast-growing direct marketing channels.

From the beginning, the merchants receiving capital used it to grow their businesses, DeMeo said. “That feeds the whole economic system and creates jobs,” he said.

TODAY’S NUTS AND BOLTS

TODAY’S NUTS AND BOLTS

Daily remittances give CAN Capital nearly constant insight into how well customers are performing, which enables the company to discover potential issues quickly and take action. Such close monitoring also provides the company with enough information to enable funding opportunities that competitors might pass up, DeMeo said.

“The basis for our decisions is how the business performs and business-specific indicators, such as capacity and consistency, versus looking at the personal credit history of the business owner,” DeMeo noted.

Having that data also helps the company create models it can use to serve other businesses in the same classification, DeMeo said. “It’s poured into machine learning for future decisioning,” he maintained. “It’s a cool concept, right?”

The company’s 450 or so employees work in several locations. Three hundred of the total are attached to the office in Kennesaw, GA, the region where the company first set up operations. To this day, that’s where the company conducts most of its business, DeMeo said.

About 25 employees work in technology and operating support in offices in Salt Lake City because the area offers a strong talent pool and provides the company with additional time zone coverage, DeMeo said.

Some of the company’s former executives came from Western Union, which had a presence in Costa Rica. About a hundred employees are now stationed there, working on technology, maintenance and development. That location also houses back-office redundancy for the company, too.

On Manhattan’s 14th Street, the company has 30 or so employees, who include digital engineers, marketing and business development teams, the human resources lead, the chief financial officer, the chief legal officer, and the chief executive officer. The company moved its executive office there from Scarsdale, NY to take advantage of the digital boom, he said, adding that, “Google’s right around the corner.”

On Manhattan’s 14th Street, the company has 30 or so employees, who include digital engineers, marketing and business development teams, the human resources lead, the chief financial officer, the chief legal officer, and the chief executive officer. The company moved its executive office there from Scarsdale, NY to take advantage of the digital boom, he said, adding that, “Google’s right around the corner.”

Compared with most companies in alternative finance, CAN Capital has little venture capital as part of its ownership structure, DeMeo said. “It’s a self-sustaining business. We’re not forced to approach the capital market to cover our burn rate. We’re cash-flow positive.” Competitors have to borrow to fund their growth, he noted.

The company has taken on infusions of debt financing, not equity financing. In the latter, a company is selling part of itself, DeMeo said. “We raised $650 million from a syndicate with five new banks and 10 banks in total.” The company completed a securitization of $200 million the year before, he said.

CAN Capital recently introduced the new TrakLoan product that has no fixed maturity date, with daily payments that are based on a fixed percentage of card receipts. This way, payments ebb and flow with the merchant’s card sales. CAN Capital is also testing “bank-like” installment loans of as much as $500,000 with a payback period of up to four years.

And there’s nowhere to go but up, in the view of CAN Capital executives. With a market of 28 million small American merchants and penetration of between 5 and 10 percent, they see plenty of potential to keep earning superlatives.

National Security Could Prove to be Alternative Lending’s Achilles Heel

December 11, 2015 While alternative lenders debate disclosure policies, stacking, and the cost of bad merchants, there’s a new regulatory threat taking root that no one seems to be able to slow down, national security. Ever since it was revealed that one of the two terrorists in the San Bernardino attack received a $28,500 loan from the Prosper Marketplace, government officials and the public at large are pointing fingers at online lenders.

While alternative lenders debate disclosure policies, stacking, and the cost of bad merchants, there’s a new regulatory threat taking root that no one seems to be able to slow down, national security. Ever since it was revealed that one of the two terrorists in the San Bernardino attack received a $28,500 loan from the Prosper Marketplace, government officials and the public at large are pointing fingers at online lenders.

House Financial Services Chair Jeb Hensarling said on Thursday that, “clearly the financing link to terrorism is a critical one.” As quoted by Politico, “everything’s on the table,” he said when asked about further scrutiny of online lenders.

His sentiment echoes other responses, some of which are clearly emotionally charged and accusatory. LendAcademy’s Peter Renton for example wrote, “I have had to answer such ridiculous questions as, is P2P lending going to become the new way for terrorists to get funding?”

With so much misinformation now floating around out there about online lenders, conspiracy theorists are even claiming that it would be impossible for someone earning $53,000 a year (As Syed Farook did) to get an unsecured loan for $28,000, the implication being that there is something more sinister going on. Of course those that work in the alternative lending industry, including myself personally as someone who invests on the Prosper Marketplace, know that’s not true.

But before the experts can be called on to answer the questions, those motivated to protect this country at all costs (with noble intentions) are rallying around swift and immediate consequences for online lenders such as Prosper.

“The issue may end up being whether marketplace lenders are too easy of a source of cash to finance terrorist attacks,” said Guggenheim Partners analyst Jaret Seiberg in a research letter.

In an article published by The Street, writer Ross Kenneth Urken basically likened Prosper Marketplace to Silk Road where bitcoins were used to buy drugs, weapons, and killers for hire.

Breitbart News, a right-wing news website, led in with an even bigger headline, San Bernardino: Has Islamic State Hijacked Consumer Loans?. It quickly sums up the story by insinuating that online lenders will become the funding tool of choice for ISIS. “The San Bernardino terrorists, Syed Rizwan Farook and his wife Tashfeen Malik, funded their killing spree with a debt consolidation loan, raising questions about whether terrorists might use popular consumer loans to fund their activities,” Breitbart wrote.

And the International Business Times argued that Utah industrial banks are aiding terrorism. “Meanwhile, industrial banks in Utah are taking full advantage of the lack of regulation in the peer-to-peer lending market while they still can, aiding potential terrorists along the way,” author Erin Banco concluded.

According to the WSJ, the House Financial Services Committee will examine whether new legislation is needed in online lending. They’ve also made inquiries to the Treasury Department about existing online lending regulations. Treasury Counselor Antonio Weiss’s previous remarks hinted that the Treasury up until recently was concerned about discriminatory lending practices more than anything else, but stressed that they were not a regulator in this area. Terror financing was not something they even addressed.

According to many sources, lawmakers are drafting up legislation on terrorism financing and expect to have something ready early next year. As for how that will impact online lenders is unknown. Right now, everyone’s still trying to figure out what just happened. Hopefully whatever is ultimately done is done intelligently.