Google’s Payday Loan Ad Ban Smells Like Government Intimidation

May 12, 2016 CFPB Director Richard Cordray

CFPB Director Richard CordrayGoogle loved payday lending and products like it, until something happened.

Google Ventures is one of the most notable investors in LendUp, a personal lender that charges up to 333% APR over the period of 14 days. The famous creator of Gmail, Paul Buchheit, is also listed as one of LendUp’s investors. Four months ago, Google Ventures even went so far as to double down on their love for the concept by participating in LendUp’s $150 Million Series B round.

This week, Google Inc. has apparently found Jesus after “reviewing their policies” and determined that personal loans over 36% APR or under 60 days will be forever BANNED from advertising on their systems. “This change is designed to protect our users from deceptive or harmful financial products,” they wrote in a public message. Ironically of course, Google is tacitly admitting that it must protect users from its own products that it has invested tens of millions of dollars in because they are deceptive or harmful.

LendUp is not the only company that Google Ventures has invested in that charges more than 36% APR. A business lender they previously invested in charged up to 99% APR. That investment was for $17 million as part of a Series D round. At the time, they called the management team’s vision “game changing.”

The only thing game-changing now is their about-face after their supposed policy and research review. It’s hard to imagine that in 2016, Google is just finally reading research about payday lending, especially considering that payday loan spam has for so long been a part of their organic search results. It cannot be understated that they’ve even created entire algorithms over the years dedicated to payday search queries and results. And “loans” as a general category is their 2nd most profitable. Yes, surely they know about payday.

Predatory middleman

Google has good reason lately to be afraid of sending a user to a website to get a payday loan however, even if they’re just an innocent middleman in all of this.

Last month, the Consumer Financial Protection Bureau filed a lawsuit against Davit (David) Gasparyan for violating the Consumer Financial Protection Act of 2010 through his previous payday loan lead company T3Leads. In the complaint, the CFPB acknowledges that T3Leads was the middleman but argues that its failure to properly vet the final lender customer experience is unfair and abusive. At its core, T3Leads is being held responsible for the supposed damage caused to individuals because they may not have ended up getting the best possible loan terms.

One has to wonder if Google could be subject to the same fate. Could they too be accused of not auditing every single lender they send prospective borrowers off to?

Four months before being sued by the CFPB personally, the CFPB sued T3Leads as a company.

Gasparyan however, is already running a new company with a similar concept, Zero Parallel. That company is indeed advertising on Google’s system.

Chokepoint

For the CFPB, coming fresh off of having made the allegations that even a middleman sending a prospective borrower off to an unaudited lender is culpable for damages, the most bold way to achieve their goals of total payday lending destruction going forward would be to threaten the Internet itself, or in more certain terms, Google.

It’s quite possible that Google has been strong-armed into this new policy of banning short term expensive loans by a federal agency like the CFPB. Not giving in to such a threat would likely put them at risk of dangerous lawsuits, especially now that there are some chilling precedents. By forcing Google to carry out its agenda under intimidation, the CFPB wouldn’t have to do any of its day-to-day work of penalizing lenders individually that break the rules. Google essentially becomes a “chokepoint” and that’s quite literally something right out of the federal regulator playbook.

In 2013, the Department of Justice and the FDIC hatched a scheme to kill payday lenders by intimidating banks to stop working with them even though there was nothing illegal about the businesses or their relationships. That plan, which caused a massive public outcry, had been secretly codenamed “Operation Chokepoint” by the DOJ. A Wall Street Journal article uncovered this and a Congressional investigation finally put an end to the scheme after two years, but not before some companies went out of business from the pressure.

Given this history, it’s highly plausible that Google has been pressured in such a way that it’s too afraid to reveal it.

Google has long known all about payday lending. Their recent decision smells like government and they just might very well be the chokepoint.

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True?

April 28, 2016

The alternative small-business finance industry has exploded into a $10 billion business and may not stop growing until it reaches $50 billion or even $100 billion in annual financing, depending upon who’s making the projection. Along the way, it’s provided a vehicle for ambitious, hard-working and talented entrepreneurs to lift themselves to affluence.

Consider the saga of William Ramos, whose persistence as a cold caller helped him overcome homelessness and earn the cash to buy a Ferrari. Then there’s the journey of Jared Weitz, once a 20 something plumber and now CEO of a company with more than $100 million a year in deal flow.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

Alternative funding can provide a second chance, too. When Isaac Stern’s bakery went out of business, he took a job telemarketing merchant cash advances and went on to launch a firm that now places more than $1 billion in funding annually.

All of those industry players are leaving their marks on a business that got its start at the dawn of the new century. Long-time participants in the market credit Barbara Johnson with hatching the idea of the merchant cash advance in 1998 when she needed to raise capital for a daycare center. She and her husband, Gary Johnson, started the company that became CAN Capital. The firm also reportedly developed the first platform to split credit card receipts between merchants and funders.

BIRTH OF AN INDUSTRY

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Many of the early entrants came from the world of finance or from the credit card processing business, said Stephen Sheinbaum, founder of Bizfi. Virtually all of the early business came from splitting card receipts, a practice that now accounts for just 10 percent of volume, he noted.

At first, brokers, funders and their channel partners spent a lot of time explaining advances to merchants who had never heard of them, Goldin said. Competition wasn’t that tough because of the uncrowded “greenfield” nature of the business, industry veterans agreed.

Some of the initial funding came from the funders’ own pockets or from the savings accounts of their elderly uncles. “I’ve met more than a few who had $2 million to $5 million worth of loans from friends and family in order to fund the advances to the merchants,” observed Joel Magerman, CEO of Bryant Park Capital, which places capital in the industry. “It was a small, entrepreneurial effort,” Andrea Petro, executive vice president and division manager of lender finance for Wells Fargo Capital Finance, said of the early days. “A number of these companies started with maybe $100,000 that they would experiment with. They would make 10 loans of $10,000 and collect them in 90 days.”

That business model was working, but merchant cash advances suffered from a bad reputation in the early days, Goldin said. Some players were charging hefty fees and pushing merchants into financial jeopardy by providing more funding than they could pay back comfortably. The public even took a dim view of reputable funders because most consumers didn’t understand that the risk of offering advances justified charging more for them than other types of financing, according to Goldin.

Then the dam broke. The economy crashed as the Great Recession pushed much of the world to the brink of financial disaster. “Everybody lost their credit line and default rates spiked,” noted Isaac Stern, CEO of Fundry, Yellowstone Capital and Green Capital. “There was almost nobody left in the business.”

RAVAGED BY RECESSION

Perhaps 80 percent of the nation’s alternative funding companies went out of business in the downturn, said Magerman. Those firms probably represented about 50 percent of the alternative funding industry’s dollar volume, he added. “There was a culling of the herd,” he said of the companies that failed.

Life became tough for the survivors, too. Among companies that stayed afloat, credit losses typically tripled, according to Petro. That’s severe but much better than companies that failed because their credit losses quintupled, she said.

Who kept the doors open? The firms that survived tended to share some characteristics, said Robert Cook, a partner at Hudson Cook LLP, a law office that specializes in alternative funding. “Some of the companies were self-funding at that time,” he said of those days. “Some had lines of credit that were established prior to the recession, and because their business stayed healthy they were able to retain those lines of credit.”

The survivors also understood risk and had strong, automated reporting systems to track daily repayment, Petro said. For the most part, those companies emerged stronger, wiser and more prosperous when the crisis wound down, she noted. “The legacy of the Great Recession was that survivors became even more knowledgeable through what I would call that ‘high-stress testing period of losses,’” she said.

ROAD TO RECOVERY

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

They included making good use of the quick churn that characterizes the merchant cash advance business, Petro noted. The industry’s better operators had been able to amass voluminous data on the industry because of its short cycles. While a provider of auto loans might have to wait five years to study company results, she said, alternative funders could compile intelligence from four advances within the space of a year.

That data found a home in the industry around the time the recession was ending because funders were beginning to purchase or develop the algorithms that are continuing to increase the automation of the underwriting process, said Jared Weitz, CEO of United Capital Source LLC. As early as 2006, OnDeck became one of the first to rely on digital underwriting, and the practice became mainstream by 2009 or so, he said.

Just as the technology was becoming widespread, capital began returning to the market. Wealthy investors were pulling their funds out of real estate and needed somewhere to invest it, accounting for part of the influx of capital, Weitz said.

At the same time, Wall Street began to take notice of the industry as a place to position capital for growth, and companies that had been focused on consumer lending came to see alternative finance as a good investment, Cook said.

For a long while, banks had shied away from the market because the individual deals seem small to them. A merchant cash advance offers funders a hundredth of the size and profits of a bank’s typical small-business loan but requires a tenth of the underwriting effort, said David O’Connell, a senior analyst on Aite Group’s Wholesale Banking team.

The prospect of providing funds became even less attractive for banks. The recession had spawned the Dodd-Frank Financial Regulatory Reform Bill and Basel III, which had the unintended effect of keeping banks out of the market by barring them from endeavors where they’re inexperienced, Magerman said. With most banks more distant from the business than ever, brokers and funders can keep the industry to themselves, sources acknowledged.

At about the same time, the SBFA succeeded in burnishing the industry’s image by explaining the economic realities to the press, in Goldin’s view.The idea that higher risk requires bigger fees was beginning to sink in to the public’s psyche, he maintained.

Meanwhile, loans started to join merchant cash advances in the product mix. Many players began to offer loans after they received California finance lenders licenses, Cook recalled. They had obtained the licenses to ward off class-action lawsuits, he said and were switching from sharing card receipts to scheduled direct debits of merchants’ bank accounts.

As those advantages – including algorithms, ready cash, a better image and the option of offering loans – became apparent, responsible funders used them to help change the face of the industry. They began to make deals with more credit-worthy merchants by offering lower fees, more time to repay and improved customer service. “The recession wound up differentiating us in the best possible way,” Bizfi’s Sheinbaum said of the changes.

His company found more-upscale customers by concentrating on industries that weren’t hit too hard by the recession. “With real estate crashing, people were not refurbishing their homes or putting in new flooring,” he noted.

Today, the booming alternative finance industry is engendering success stories and attracting the nation’s attention. The increased awareness is prompting more companies to wade into the fray, and could bring some change.

WHAT LIES AHEAD

One variety of change that might lie ahead could come with the purchase of a major funding company by a big bank in the next couple of years, Bryant Park Capital’s Magerman predicted. A bank could sidestep regulation, he suggested, by maintaining that the credit card business and small business loans made through bank branches had provided the banks with the experience necessary to succeed.

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Some of today’s alternative lenders don’t have the skill and technology to ward off bad deals and could thus find themselves in trouble if recession strikes, warned Aite Group’s O’Connell. “Let’s be careful of falling into the trap of ‘This time is different,’” he said. “I see a lot of sub-prime debt there.”

Don’t expect miracles, cautioned Petro. “I believe there will be another recession, and I believe that there will be a winnowing of (alternative finance) businesses,” she said. “There will be far fewer after the next recession than exist today.”

A recession would spell trouble, Magerman agreed, even though demand for loans and advances would increase in an atmosphere of financial hardship. Asked about industry optimists who view the business as nearly recession-proof, he didn’t hold back. “Don’t believe them,” he warned. “Just because somebody needs capital doesn’t mean they should get capital.”

Further complicating matters, increased regulatory scrutiny could be lurking just beyond the horizon, Petro predicted. She provided histories of what regulation has done to other industries as an indication of the differing outcomes of regulation – one good, one debatable and one bad.

Good: The timeshare business benefitted from regulation because the rules boosted the public’s trust.

Debatable: The cost of complying with regulations changed the rent-to-own business from an entrepreneurial endeavor to an environment where only big corporations could prosper.

Bad: Regulation appears likely to alter the payday lending business drastically and could even bring it to an end, she said.

Still, regulation’s good side seems likely to prevail in the alternative finance business, eliminating the players who charge high fees or collect bloated commissions, according to Weitz. “I think it could only benefit the industry,” he said. “It’ll knock out the bad guys.”

Lending Club Looks to Do First Major Securitization Deal

April 26, 2016

As marketplace lenders look to reduce their dependence on traditional capital sources, Lending Club appears to be ready to finally give in and do a securitization.

Lending Club is reportedly in talks with Goldman Sachs and Jefferies Group to put together its first big bond offering, according to the WSJ. The news is significant because the company has previously shunned them.

Earlier this year, Lending Club CEO Renaud Laplanche told the Financial Times, “We are showing that we can scale without the securitization market.” That was after saying they weren’t “willing to take more risk to do a securitization than we would through the normal operation of the platform.”

Since then, the market and the mood has changed. Citigroup for example, announced that they would stop securitizing loans for Lending Club rival Prosper Marketplace only two weeks ago due to looming fears of increasing losses. Prosper is also reported to be talking to Goldman Sachs about future securitizations.

Having Problems With Leads? Don’t Feel Alone

April 24, 2016

Having problems with leads? Don’t feel alone. Funders and lead providers say response rates to offline marketing have been cut in half while the price of pay-per-click campaigns has skyrocketed. They blame intense competition in an increasingly crowded field of funders, market saturation by lead generation companies, better email spam filters and comparison shopping by small-business owners who are becoming more savvy about how much they need to pay for merchant cash advances and loans.

Clicks that cost $5 each seven years ago now command a price of nearly $125, says Isaac Stern, CEO of Yellowstone Capital LLC, Green Capital and Fundry. “Pay-per-click marketing has gotten out of control,” he laments. “So you need a hefty, hefty budget to compete in that world.” He reports spending $600,000 to $700,000 a month on internet marketing, compared to $100,000 monthly on direct mail.

Even when the price of individual clicks isn’t measured in hundreds of dollars, the cost of the multiple clicks required to create a lead can mount up, according to Michael O’Hare, CEO of Blindbid, a Colorado Springs, Colo.- based provider of leads. If it takes 15 clicks that cost $25 each to obtain a lead, that comes to $375, he notes. Still, some companies manage to use key words that cost $8 or so per click to get decent leads for less than $100, he says.

While the cost of pay per click is exploding, the response to direct mail marketing is declining precipitously, says Bob Squiers, who owns the Deerfield, Fla.-based Meridian Leads. The percentage of small-business owners who respond to advertising they receive in the mail has fallen from 2 percent just a few years ago to 1 percent now, partly because they receive so many mailings from so many more lead-generation companies, he says. “There weren’t too many people doing direct mail into this space five years ago,” he notes. His company’s leads range in price from pennies to $60, he says.

While Blindbid and Meridian both specialize in finding leads by sending out direct mail pieces and then qualifying the respondents in phone conversations, one of their competitors, Lenders Marketing, takes a different approach, according to Justin Benton, sales director for the Camarillo, Calif.-based company. Benton’s data-driven method combines his company’s databases with the databases of financial institutions. He cultivates relationships with the banking industry’s executives to facilitate that process, he says, and his company does not make phone calls to qualify leads.

But placing too high a value on data gives rise to two problems, the way O’Hare views the search for leads. First, analyzing the data creates plenty of challenges, he says. Second, human beings just aren’t rational enough in their decision-making to fit data-driven profiles or cohorts, he maintains. “The holy grail is to find some algorithm that will predict that a merchant needs funding, and they can then find these people through massive data,” he says with skepticism.

Whatever path a company takes to finding and verifying leads, it pays to establish three elements before classifying them, O’Hare says. First, prospects should qualify financially for credit or advances. Second, prospects should demonstrate a genuine interest in obtaining funding, as opposed to less-than-serious “tire kicking.” With both of those characteristics in place, O’Hare informs prospects they can expect to hear from funders.

Blindbid also wants to guide the expectations of the funders who are calling the leads, O’Hare says. To that end, the vendor invites funders to listen to recordings of the phone calls it makes to qualify leads. Just the same, funders should bear in mind that they may not receive the same reception when they contact the lead, he cautions. “We see it all the time, he says. “We speak to the merchant in the morning and they’re pleasant. Then in the afternoon when they speak to the funder or the broker, the merchant is grumpy.”

Retailers’ mood swings aside, funders can soon gauge the quality of the leads they’re buying. “You can’t judge a lead on cost, Squiers admonishes. “Judge them by performance.” However, performance fluctuates according to the funder’s sales skills, product offering and product knowledge, he maintains.

Meanwhile, the problems plaguing the lead business should prompt funders to become creative in their approach to finding prospects. That’s why even vendors who make their living selling leads encourage funders to search for prospects on their own. “We always advise generating your own leads,” says Benton. “The only leads you can truly count on are the ones you generate yourself.”

Meanwhile, the problems plaguing the lead business should prompt funders to become creative in their approach to finding prospects. That’s why even vendors who make their living selling leads encourage funders to search for prospects on their own. “We always advise generating your own leads,” says Benton. “The only leads you can truly count on are the ones you generate yourself.”

Knowing where to look for leads can require a thorough grasp of what’s happening in a particular market. “You can look at what industries are hot,” O’hare suggests. The trucking business is heating up, for example, because so many truckers need funding to buy expensive equipment to meet new requirements for electronic logs, he says. Meanwhile, the recession has wracked the martial arts industry, so dojos might require funding for marketing to help them recover, he notes.

Understanding every industry in that much detail isn’t practical, so lead generation companies urge funders to specialize in just a few niches. Building a network of customers who know each other can result in referrals, Benton observes. It also soothes skeptical prospects, he notes. “Once you say I’ve worked with Fred down at Tony Roma’s – they can feel more comfortable, especially if you’ve done it in the same city,” he maintains.

Whether leads arise internally or come from a vendor, funders have to work them properly to succeed in closing deals, lead-generating companies agree. “The real key is being consistent and persistent,” Benton says. “Research has shown the average lead is called 1.3 times, so once you make that second call you are ahead of the curve.” He advocates that funders use their CRM system by taking copious notes on their calls, setting up nurture campaigns and following up with leads in an organized manner.

And don’t forget that at least some prospects are getting pummeled with calls. “A lot of brokers are carpet bombing – they’re on the phone all day,” says O’Hare. “I talked to one guy who said he makes 400 or 500 calls a day on a manual dial. I’d like to do a video of that.

SCORCHED EARTH – Controversial Bill Could Eliminate Marketplace Lending, Merchant Cash Advance and Nonbank Business Loans in Illinois (and starve small businesses in the process)

April 9, 2016

The State of Illinois wants to make it a Class A misdemeanor for providing small businesses with quick, easy working capital.

The world’s strangest bill, dubbed the Small Business Lending Act, could send marketplace lenders, nonbanks, and merchant cash advance companies to prison for up to 1 year if applicants don’t submit at the very least, their most recent six months bank statements, the previous year’s tax return, a current P&L, a current balance sheet, and an accounts receivable aging.

Loans in which the monthly payments exceed at least 50% of the business’s monthly net income would be illegal, which implies that any business that is either breaking even or running at a loss would be banned from obtaining a loan from alternative sources.

This is not an April Fools’ prank. Not even preemption granted under the National Bank Act or Federal Deposit Insurance Act is safe.

Introduced into the State Senate under the pretense that it would squash predatory lenders, the bill’s licensing and compliance proposal would also effectively outlaw marketplace lending and securitizations by making the sale of loans illegal unless it’s to a bank or another state-licensed party. Even merchant cash advances are referenced specifically but almost as an afterthought and defined in such a way that even traditional factoring companies may be in jeopardy.

No licensee or other person shall pledge, assign, hypothecate, or sell a small business loan entered into under this Act by a borrower except to another licensee under this Act, a licensee under the Sales Finance Agency Act, a bank, savings bank, community development financial institution, savings and loan association, or credit union created under the laws of this State or the United States, or to other persons or entities authorized by the Secretary in writing. Sales of such small business loans by licensees under this Act or other persons shall be made by agreement in writing and shall authorize the Secretary to examine the loan documents so hypothecated, pledged, or sold.

At a time when most fintech lenders are advocating for smart regulation, the State of Illinois apparently wants to end all nonbank commercial finance under $250,000 completely, with the exception of one organization (which we’ll get to shortly).

At a time when most fintech lenders are advocating for smart regulation, the State of Illinois apparently wants to end all nonbank commercial finance under $250,000 completely, with the exception of one organization (which we’ll get to shortly).

There are some exemptions granted under this proposal of course. Loans over $250,000 aren’t subject to it, nor are any loans made by Illinois-based banks or credit unions, that is unless they are acting as the agent for another party like say perhaps a marketplace lender.

Hidden inside is also an exemption for nonprofit lenders, a loophole left open for Accion Chicago, the nonprofit masterminds behind the bill who seem to want the entire state’s lending market all for themselves.

Illinois State Senator Jacqueline Collins Introduced This Bill

Senator Collins introduced the legislation as an amendment to Senate Bill 2865 on April 6th. A former journalist, she’s now the chairwoman of the Illinois Senate Financial Institutions Committee. Among her self-professed accolades is that she “has played a key role in addressing predatory lending and high foreclosure rates in Chicago through legislation that protects homebuyers and homeowners with subprime mortgages.” She lists the Mortgage Rescue Fraud Act, the landmark Sudan Divestment Act and the Payday Loan Reform Act among her major legislative accomplishments.

It’s no surprise then that sections of the bill are borrowed straight out of the Payday Loan Reform Act. Collins isn’t acting on her own however…

Chicago City Treasurer Kurt Summers

In January, Senator Collins joined Chicago City Treasurer Kurt Summers in a call for “new legislation to protect small business owners from misleading and dishonest predatory lenders.” In a closed-door hearing, the committee supposedly heard from business owners, advocates and elected officials on predatory lending.

“Chicago’s small business community deserves protection from the unchecked greed of predatory lenders,” Treasurer Summers said. “While access to capital is the number one concern of small business owners across the state, bank and commercial loans continue to decline, steering them to underhanded lenders. As we continue to urge banking partners to increase their local investment, this new, common-sense legislation would ensure transparency in lending that so often puts our entrepreneurs at risk.”

Of note is his use of the phrase “banking partners” since this bill has bankers all over it, as we’ll get into shortly. Summers represents the Chicago Mayor’s office and the Mayor’s office says they’ve launched this campaign thanks to partners like Accion Chicago.

Hon. Kurt Summers, Treasurer, City of Chicago from City Club of Chicago on Vimeo.

Accion Chicago and the Mayor’s Office

Last year, Mayor Rahm Emanuel announced a joint campaign with Accion Chicago to help small businesses avoid predatory lending.

Accion Chicago, ironically makes business loans themselves, having originated 535 loans totaling $4.8 million in 2014 with a maximum loan size of $100,000.

Who is Accion Chicago really?

The Small Business Lending Act virtually ensures that small business loans under $250,000 only be facilitated by banks and nonprofits. Isn’t it convenient then that Accion Chicago is not only a nonprofit, but also funded and staffed by banks?

According to their 2014 annual report, Citibank and JPMorgan Chase were two of their three largest supporters (the third was the US Treasury!). Below are some of the figures:

$100,000+

- Citibank

- JPMorgan Chase

$50,000 – $99,999

- Bank of America

$20,000 – $49,999

- Fifth Third Bank

- PNC Bank

- U.S. Bank

$5,000 – $19,999

- American Chartered Bank

- Alliant Credit Union

- BMO Harris Bank

- First Bank of Highland Park

- First Eagle Bank

- First Midwest Bank

- Ridgestone Bank

- State Bank of India

- The PrivateBank

- Wells Fargo Bank

About a dozen more banks gave less than $5,000.

JPMorgan Chase has also been a partner of the annual Taste of Accion fundraising event, and was the lead sponsor in 2014, a spot that costs $30,000. Benefactor sponsorships which cost $20,000 each were comprised of American Chartered Bank, Capital One, Northern Trust Company, and Wintrust Bank. And the lesser sponsorships? Again, mostly banks.

JPMorgan Chase has also been a partner of the annual Taste of Accion fundraising event, and was the lead sponsor in 2014, a spot that costs $30,000. Benefactor sponsorships which cost $20,000 each were comprised of American Chartered Bank, Capital One, Northern Trust Company, and Wintrust Bank. And the lesser sponsorships? Again, mostly banks.

You know who hasn’t donated to Accion Chicago? Marketplace lenders and merchant cash advance companies.

Accion Chicago raised only $1.4 million in 2014 from public support, the bulk of which came from banks or related traditional financial institutions. So is it just a coincidence that this predatory lending bill they’re supporting grants exemptions to all the banks from compliance?

Accion Chicago’s 2014 Board of Directors includes executives from:

- American Chartered Bank (chairman)

- First Eagle Bank

- JPMorgan Chase

- Ridgestone Bank

- MB Financial Bank

- Talmer Bank & trust

- Citibank

- First Midwest Bank

The 2014 committees were made up almost entirely of bank executives from:

- First Eagle Bank

- The PrivateBank

- Ridgestone Bank

- U.S. Bank

- JPMorgan Chase

- Forest Park National Bank & Trust Co.

- MB Financial Bank

- FirstMerit Bank

- Wintrust Bank

- Standard Bank & Trust Co.

- First Midwest Bank

- Wells Fargo Bank

- Seaway Bank & Trust Co.

- Metropolitan Capital Bank

- Evergreen Bank Group

- First Financial Bank

- PNC Bank

Thanks to the impartial work of these good citizens, they have discovered that small businesses should only be working with banks or nonprofits funded and staffed by banks and have craftily devised a bill to legislate all the alternatives out of existence.

If this was really about predatory lending, then they screwed up big time

All coincidences aside, some of the bill’s rules have nothing to do with protecting borrowers, like the required $500,000 surety bond to become licensed for example. Compare that to California’s $25,000 licensed lender surety bond. And the restriction on being able to sell or securitize a loan, how does that help small businesses?

These requirements and others suggest that it’s about preventing all alternatives from existing in the marketplace, rather than predatory alternatives. The losers would undoubtedly be small businesses and the Illinois job market. Senator Collins and Treasurer Summers, both of whom have a strong track record of empowering their constituents financially, may have underestimated or overlooked the likely negative consequences of this bill.

The nonbanks

Several nonbank trade groups are reportedly in the process of formulating a response.

The Commercial Finance Coalition for example, a nonprofit coalition of financial technology companies, told AltFinanceDaily that they are concerned about the impact this will have on the Illinois job market and will indeed have representatives on the ground in Illinois.

They also wanted to make known that they welcome support from marketplace lenders, nonbanks and merchant cash advance companies in these efforts and that interested parties should email Mary Donahue at mdonohue@commercialfinancecoalition.com

To contact Senator Jacqueline Collins who introduced the bill, call her at 217-782-1607.

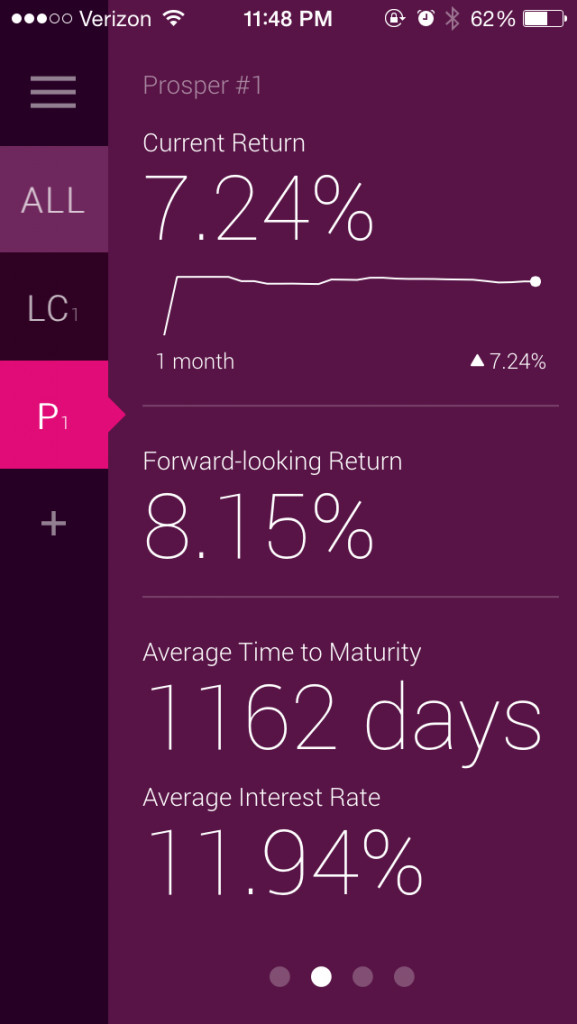

LendingRobot is Now Your On-The-Go Marketplace Lending Robo-Advisor

April 8, 2016

Checking your marketplace lending portfolio is now as easy as checking a stock quote

Marketplace Lending just became a little bit more friendly for investors thanks to LendingRobot’s new mobile app. The app allows investors to track the daily performance of their Lending Club, Prosper and Funding Circle portfolios all in one place. Its utility valued is bolstered by the fact that none of the three integrated platforms have published their own investor-oriented mobile apps, which came as a surprise even to LendingRobot CEO Emmanuel Marot.

The app complements the existing web service where investors can set custom filters to automatically buy notes that meet their criteria from the platforms whenever they become available. To date, more than 5,000 investors have signed up to use LendingRobot and more than $80 million of their collective investments are being measured by the service. Most of those users have only integrated their Lending Club or Prosper portfolios as of now, and not just because Funding Circle is a new addition, but also because their model is slightly different. “You have to be an accredited investor,” Marot said of using Funding Circle. There is no such requirement for the other two platforms.

The app complements the existing web service where investors can set custom filters to automatically buy notes that meet their criteria from the platforms whenever they become available. To date, more than 5,000 investors have signed up to use LendingRobot and more than $80 million of their collective investments are being measured by the service. Most of those users have only integrated their Lending Club or Prosper portfolios as of now, and not just because Funding Circle is a new addition, but also because their model is slightly different. “You have to be an accredited investor,” Marot said of using Funding Circle. There is no such requirement for the other two platforms.

The app is unique because it makes your aggregate marketplace lending portfolio data as handy as the latest stock quote. “It was kind of surprising actually for us to see that we have about 30% of our clients coming several times per week just to check it,” Marot said.

But perhaps as adoption of marketplace lending continues to catch on as part of a normal everyday diversified investment strategy, this will become more of a trend. For investors with large portfolios for example, the robo-advisor is likely acquiring notes for them multiple times per day every day, increasing the likelihood an investor will want to check in regularly to see how they’re doing.

Along with calculating the aggregate and individualized returns based on formulas that LendingRobot devised themselves, users can quickly refer to a baseline value known as their “portfolio health.” This number is not based on some proprietary advanced formula, Marot explained, but is rather the straightforward percentage of notes that are in good standing relative to all “live” notes. Charged-off notes are no longer considered live, Marot said.

Along with calculating the aggregate and individualized returns based on formulas that LendingRobot devised themselves, users can quickly refer to a baseline value known as their “portfolio health.” This number is not based on some proprietary advanced formula, Marot explained, but is rather the straightforward percentage of notes that are in good standing relative to all “live” notes. Charged-off notes are no longer considered live, Marot said.

Users can also check their portfolio composition, the average time to maturity and the average interest rate being assessed, in addition to being able to review raw figures such as how many notes became late in the last week or paid in full, for example.

Lending Club, Prosper and Funding Circle are just the beginning, Marot said, while expressing optimism about adding other platforms in the future. They saw the original three platforms they’re integrated with now as being a good fit because they are “safe.” “We are very cautious,” he said. Notably, those companies are also the three founders of the newly formed Marketplace Lending Association, of which he voiced support for.

Michael Raneri, a PwC Managing Director and Fintech Advisory Lead, wrote on Forbes that millennials will serve as early adopters for robo-advisors. “The next generation of investors has been quick to embrace new technologies and experiences, and this should apply to robo-advisors,” he wrote. “Furthermore, millennials have a general mistrust of large financial institutions, particularly in the wake of the financial crisis of 2008. Unlike their parents, who forged close relationships with advisors—even using their phones to have conversations with them, as primitive as that sounds—millennials are equally comfortable with making digital connections. They’ve been conditioned to accept that technology can match the performance of its human predecessors, while offering reduced fees and providing greater convenience.”

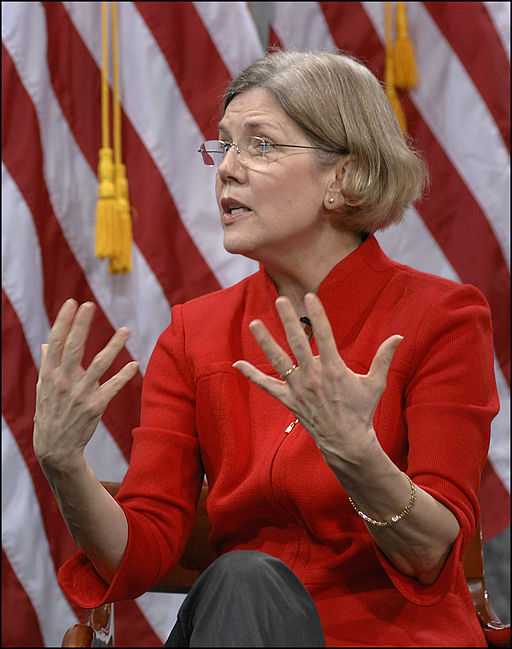

Senator Elizabeth Warren Rips Former Protégé in CFPB Debate

April 6, 2016 Massachusetts Senator Elizabeth Warren was forced to confront an unexpected witness yesterday in a Senate hearing over consumer finance regulations, former protégé Leonard Chanin. Chanin, who was there to testify about why he believed the Consumer Financial Protection Bureau (CFPB) was acting outside its intended scope, was accused by Warren of being the person responsible for not catching the entire 2008 financial crisis.

Massachusetts Senator Elizabeth Warren was forced to confront an unexpected witness yesterday in a Senate hearing over consumer finance regulations, former protégé Leonard Chanin. Chanin, who was there to testify about why he believed the Consumer Financial Protection Bureau (CFPB) was acting outside its intended scope, was accused by Warren of being the person responsible for not catching the entire 2008 financial crisis.

“Of all the people who might be called on to advise Congress about how to weigh the costs and benefits of consumer regulations, I am surprised that my Republican colleagues would choose a witness who might have one of the worst track records in history on this issue,” Warren said.

Of note however, is that after the financial crisis, she herself hired Chanin to be the CFPB’s rule-writer after he came highly recommended for his service as the deputy director of the Federal Reserve’s Division of Consumer and Community Affairs. “I’m also pleased to have Leonard Chanin playing a key role in building an effective and efficient rule writing team,” she said back in December 2010.

Chanin spent nearly 20 years at the Fed and received a Federal Reserve Board Special Achievement Award for his work on the Truth in Savings Act.

“So my question is, given your track record at the Fed, why should anyone take you seriously now?” she asked Chanin, even while acknowledging that she had hired him previously based upon that same track record.

Chanin is now an attorney at Morrison & Foerster LLP.

The CFPB is often attributed as being Warren’s brainchild and she is believed to be a contender for Vice President on the Democratic ticket.

Watch the exchange between Warren and Chanin below:

The APR Enigma Confuses Everyone – Even Lenders

April 3, 2016

A study published by Lendio last week confirmed the results found in recent government studies, that small businesses are confused by Annual Percentage Rates. But they’re not alone…

It might be time to reconsider the calls for APR standards in small business lending. In a recent survey of 1,000 small business owners, only 17.4% of respondents chose APR as the easiest method to understand the cost. The vast majority selected the total net dollar cost of the loan as being the easiest.

The data matches the results found in a study conducted by the Federal Reserve Bank of Cleveland last year, in which small business owners generally responded that there was nothing confusing about a loan when cost was presented as a total dollar value. It was interest rates that tripped them up, the Fed determined.

When attempting to answer questions about the total amount owed and interest rates, participants became notably less confident in their ability to make an informed borrowing decision, with many qualifying their answers or indicating they were “not sure.”

– Federal Reserve Conclusion from Alternative Lending through the Eyes of “Mom-and-Pop” Small-Business Owners 8/25/15

Additionally in the Fed study, small business owners guessed the interest rate of a presented hypothetical loan to be anywhere from 5% to 50%, with some saying they just didn’t know. All of them were wrong. An analyst for the Federal Reserve Bank later acknowledged that it was a trick question. “The correct answer is that ‘it depends on how long it takes to pay back,'” said Ellyn Terry, an economic policy analysis specialist. The Fed report itself had to be amended more than a month later because this question and the answers produced in the study were confusing to even the sophisticated parties trying to make sense of it. That amendment reads as follows:

*Note: In practice, for a credit product structured like Product A, the effective interest rate varies depending on how long it takes a borrower to repay which, in turn, depends on the volume and timing of credit card sales receipts. Simply put, the interest owed on Product A is 30% of the principal value, but assuming consistent monthly sales and daily payments, the effective interest rate is on the order of 60%, and higher if funds are repaid sooner than one year. (Added 9.29.2015)

Does that clear it up for you??? Even the added note intended to make the interest rate question more clear is confusing. Small business owners never stood a chance…

But it seems those on the lending side of things are confused too.

Lendio CEO Brock Blake followed up his study with a blog post on LendAcademy to try and articulate the implications of the findings. Titled, Communicating the Cost of Capital in Alternative Lending, Blake was roasted in the comments for comparing a 6-month loan to a 5-year loan by those presumably involved in lending themselves.

Apparently, math is very subjective

In an example Blake used to illustrate a point, he gave a 6-month loan an Effective APR of 83% and a 5-year loan an Effective APR of 19%. Critics eager to point out holes in his argument challenged the fundamental numbers used to construct it.

“By the way, I tried to verify the APR of that #1 loan, and I get 137.03%, not 83%. Has anyone else tried to verify this calculation?”

“I ran the numbers on #1 but came up with a different number altogether. I think the error is in total cost of capital, which should be $4,500 vs. $4,016. With 22% simple interest, interest paid would be $3,960 plus the $540 origination fee.”

One set of facts, 4 different opinions on APR. How can this be?

In sparking this debate, Blake may not have fully convinced readers that a 6-month high-APR loan can be better than a 5-year low-APR loan, but he did unintentionally demonstrate support for his study’s findings, that APR as a universal measurement is flawed since even those that believe they understand it came up with different percentages than their peers.

Consider that the Federal Reserve study referenced above implied to business owners that APR is simply an abbreviation for interest rate, which isn’t true. “When it comes to borrowing for the short term, are you more comfortable knowing the interest rate (APR) or total cost of repayment?” it asked those polled.

Bad form

Bad form

The Truth in Lending Act (TILA) makes a clear distinction between an APR and an interest rate. “Since an APR measures the total cost of credit, including costs such as transaction charges or premiums for credit guarantee insurance, it is not an ‘interest’ rate, as that term is generally used.” Well then why are they presented as the same thing in a Fed study measuring comprehension of loan costs?

Note also that only one of the Fed study’s mock products mentioned an APR and only in the context of an Effective APR, something that the Fed has long known to be confusing. In April 2006, Macro International (now ICF International) was hired by the Fed to examine the comprehensibility of these very formulas.

One of the most consistent findings was that very few participants understood the meaning of an Effective APR (At that time known as the Fee-Inclusive APR). “Participants had a wide variety of incorrect interpretation of these percentages, including that they were the interest rates that would be paid on fees, penalty rates that would be charged if late payments were made, or the percentages of total transactions that were made of each type.”

It got worse though, because “in addition to a general lack of understanding of the [Effective APR], qualitative testing also found several instances when participants confused this term with their nominal APR for a given transaction.”

But it’s gotten better right?

For all of the studies conducted and regulations implemented, one might expect that banks, which bear the brunt of disclosure requirements in the financial world, would receive the highest marks on transparency. But that’s not the case. Another study, one jointly published by seven Federal Reserve banks, found that dissatisfied business borrowers were slightly more likely to encounter transparency issues with large banks than they were with online lenders.

Bankers probably aren’t surprised by that

Last Fall, B. Doyle Mitchell Jr, who spoke on behalf of the Independent Community Bankers of America during a House subcommittee hearing, said that new loan disclosures [required by Dodd-Frank] was not making it easier for borrowers to understand, to the point that they don’t even know what they are signing anymore. “In fact it is even more cumbersome for them now,” he said.

Non-bank lending critic Ami Kassar has publicly claimed that lenders are simply afraid of disclosing APRs because they don’t want their borrowers to know the real cost.

The data indicates however that borrowers don’t know what to make of APRs. Worse, the issue seems to be a universal one, one that confounds consumers, business owners, government surveyors and those within the lending industry itself.

APRs also struggle to remain relevant as a measure for short term loans. For example, OnDeck CEO Noah Breslow has said that a six month loan with a 60% APR may actually only cost 15 cents on the dollar. “The APR overstates the actual cost of the loan to the borrower,” he previously told Forbes.

“Asked which method was easiest to understand, two-thirds of respondents chose total payback amount,” Lendio’s survey concluded.

That seems to be the trend indeed.

{kind=link}