Lightspeed Accelerates Growth of its MCA Business

February 9, 2025Lightspeed Capital accelerated the growth of its principal issued for its merchant cash advance program, the company shared in its latest quarterly earnings report. Normally the company has more to say about this division but its attention was focused on an “executing a full transformation plan.”

As part of its previously-announced strategic review, the Company conducted an in-depth evaluation of its portfolio, including market attractiveness, competitive dynamics, and its right-to-win as well as evaluating the best ownership structure to navigate Lightspeed through a transformation. The Company has already set its transformation plan in motion, focusing on growth in retail in North America and hospitality in Europe, both leading growth engines, with a strategic focus on expanding locations and increasing software and payments ARPU, with the other business areas optimized for efficiency and aimed at driving a maximum profitability for the whole business.

The Company-wide transformation to deliver on the new strategy will focus on:

- Go-to-market: enhancing Lightspeed’s go-to-market strategy with targeted outbound efforts, field sales and local marketing expansion, and verticalized execution to maximize efficiency and improve win rates, including deepening supplier integration in focus verticals and deploying AI-driven customer acquisition across retail in North America;

- Product & Technology: investments focused on key growth areas—enhancing inventory management, forecasting, and supplier integration for retail in North America, while optimizing operations, guest experience, and analytics for hospitality in Europe;

- Capital Allocation: transformation initiatives to free up capital for investment in growth areas; and

- Share Repurchase: a share repurchase program to return up to $400 million in cash to shareholders, including the immediate execution of approximately $100 million3 under our current authorization, plus an additional $300 million, in each case subject to market conditions.

American Fintech Council (AFC) Welcomes Acting Director of the CFPB Scott Bessent and Doubles Down on its Commitment to Champion Earned Wage Access (EWA) Through Federal and State Advocacy

February 3, 2025Washington, D.C. (February 3, 2025) – The American Fintech Council (AFC), the premier industry association representing responsible fintech companies, innovative banks, and the largest number of responsible Earned Wage Access (EWA) providers, is intensifying its efforts to ensure responsible EWA services remain accessible to American workers. Through federal engagement and testimony before eight state legislatures so far across the country, with two upcoming hearings in Nebraska and Utah, AFC is committed to supporting clear, pragmatic regulation for EWA to empower consumers and foster responsible innovation.

“Earned Wage Access is an essential financial tool for millions of American families, offering a safe and responsible alternative to the predatory credit products of the past,” said Phil Goldfeder, CEO of the American Fintech Council. “For generations, workers have been captive to an arbitrary pay period system that separates their work from their wages. EWA restores this connection, providing greater financial flexibility and stability for those who need it. AFC and responsible EWA providers are committed to establishing a regulatory framework that protects consumers and preserves access to EWA by recognizing that this product is not a loan, and should not be regulated as such.”

In a letter to Treasury Secretary Scott Bessent, who also serves as Acting Director of the Consumer Financial Protection Bureau (CFPB), AFC urged the pursuit of a formal rulemaking process that would allow consumers and industry participants to convey the nuances and benefits of responsible EWA products. AFC emphasized that responsible EWA providers offer a non-recourse, fee-transparent alternative to traditional credit products that helps workers access their earnings when needed, without late fees or penalties. AFC also highlighted the need for consistent federal regulation to address the patchwork of state laws that risk undermining the stability and availability of EWA services.

In a previous letter to the CFPB in February 2024, AFC asked for formal legislative rulemaking process, but the request went unheeded by then-Director Chopra. Instead, the CFPB issued a proposed informal interpretive rule, which discussed a novel and inaccurate interpretation of EWA and was never finalized. In addition, the CFPB rescinded its 2020 Advisory Opinion–the Bureau’s only official position on EWA–in the final moments of the previous administration, leaving industry participants without a clear understanding of the CFPB’s position.

In addition to federal advocacy, AFC representatives recently testified at hearings on EWA in Colorado, Indiana, New Mexico, North Dakota, Oregon, and Vermont, as well as two hearings in Washington state, with upcoming testimony in Nebraska and Utah, to speak about the consumer benefits of these offerings and the need to support responsible EWA practices. AFC will continue to monitor legislative and regulatory developments around EWA at the state level, and is prepared to engage collaboratively with any state considering guidance around this technology.

“A regulatory framework for Earned Wage Access must be grounded in a clear understanding of its role as an empowering tool for financial stability—not mischaracterized as traditional credit,” said Ian P. Moloney, SVP and Head of Policy and Regulatory Affairs at AFC. “EWA provides workers with immediate access to their hard-earned wages, helping them avoid the cycle of high-interest debt and predatory financial products. Misguided regulation risks sidelining this critical innovation, leaving millions of Americans without a safe, transparent alternative to address their financial needs. AFC is committed to ensuring that regulatory decisions are informed by facts and protect the unique consumer benefits EWA provides.”

A standards-based organization, AFC is the premier trade association representing the largest financial technology (Fintech) companies and innovative banks offering embedded finance solutions. AFC’s mission is to promote a transparent, inclusive, and customer-centric financial system by supporting responsible innovation in financial services and encouraging sound public policy. AFC members foster competition in consumer finance and pioneer products to better serve underserved consumer segments and geographies.

###

B2B Finance at AltFinanceDaily

July 5, 2024 When Broker Fair first debuted in 2018, the keynote speaker was none other than Ryan Serhant, then a fast rising New York City real estate broker and star of Bravo’s Million Dollar Listing. Today he’s got his own Netflix Series called Owning Manhattan.

When Broker Fair first debuted in 2018, the keynote speaker was none other than Ryan Serhant, then a fast rising New York City real estate broker and star of Bravo’s Million Dollar Listing. Today he’s got his own Netflix Series called Owning Manhattan.

“After selling real estate for 12 years, I decided to start my own company,” Serhant says in the trailer for the first episode, “and if you can’t sell, you can’t be here.”

That New York hustle attitude was the connecting link for why Broker Fair chose him despite the broker audience being largely engaged in small business financial services at the time. But since then the small business finance broker community has become increasingly diversified in its product offerings and real estate is frequently one of the assets on the menu.

“People will be surprised how many clients have real estate, not just a [primary home], but they own just a small multifamily down the road that they never touched or tapped into,” said Julio Sencion, Principal at Alta Financial, in a recent interview with AltFinanceDaily.

Companies like World Business Lenders figured that out a long time ago while still more discovered the business during the covid recovery, leading AltFinanceDaily to produce a video miniseries about real estate investing in the summer of 2021. The guests ranged from real estate influencer Ralph DiBugnara to NestSeekers International’s Chief Economist Erin Sykes to a couple of old fashioned guys named Danny and Bruce who started investing in real estate across New Jersey long ago.

AltFinanceDaily also interviewed house-flipper turned real estate tech CEO Andrew Luong of Doorvest, did a deep dive as to why real estate was becoming the side hustle of choice in the industry, and even bought real land using the blockchain for the purpose of a story.

Equipment financing has also taken off, leading AltFinanceDaily to produce the first ever sales reality series named Equipping The Dream in 2022.

That’s been complemented by regular coverage and even sitdown interviews from Andrew Carman, Steve Geller, and George A. Parker.

AltFinanceDaily’s Sean Murray has previously presented at the International Factoring Association’s (IFA) Fintech educational event, been a guest on the Coleman Report run by renowned SBA expert Bob Coleman, and moderated panels separately for the New York Institute of Credit and the Alternative Finance Bar Association.

Murray was also the host and producer of the industry’s first ever Broker Battle which took placed in Miami Beach this past January.

AltFinanceDaily is also affiliated with the largest online small business finance community in the US, DailyFunder, and has produced nearly two dozen events since 2017.

“Back in 2018, there was a question that Serhant posed on stage to the Broker Fair audience to make sure he understood where they were coming from,” Murray said. “‘You guys are all B2B right?’ he said, and I think his characterization was spot on, because B2B is pretty much what we’ve been all along.”

AltFinanceDaily is collaborating with the Small Business Finance Association on the B2B Finance Expo that’s taking place in Las Vegas on September 23-24. For info, visit: https://www.b2bfinexpo.com

Forget the Metaverse, I Bought Real Land

February 20, 2024 In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

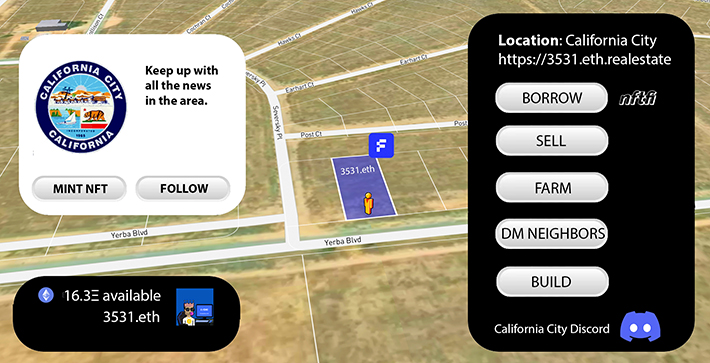

All of this history was something I breezed through right before I impulsively clicked a button on my screen asking me to confirm my purchase for a lot there. One click. That’s apparently all it took to become the newest member of a potential future neighborhood in California City, one that might not ever come to fruition. But how I found it in the first place is the real story. It appears that in the modern era this sleepy desert outpost has become a bit of an experimental laboratory for something relatively new in the real estate world, converting properties into NFTs.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Founded in 2018 and backed by investors like Mark Cuban and Zain Jaffer, properties tokenized by Fabrica “can be traded instantly, used as collateral and are compatible with all NFT platforms,” the company states. “The product automates sales transactions, facilitating title transfer, payments and regulatory compliance.” Fabrica facilitates the on-ramping of your land into an NFT and even provides its own marketplace for buyers and sellers. That’s where I got mine. Interested parties can read up on a property’s on-chain history and even check the title. There’s also a cool little Google Earth-like animation that flies the user to their specific plot of land. The experience feels a lot like buying a plot of virtual land in a video game or the metaverse except this land is real. That means that sleek little NFT in your digital wallet comes with real responsibilities like property taxes, which Fabrica works to keep the owner informed about. It also means any and all liabilities of property ownership. The upside is that you can go and visit it in real life and even develop it. You can’t do that in a video game.

Although I’ve counted six properties in California City that are immediately identifiable as NFTs, it’s hardly the only place in the United States where this is being done. Properties available for sale as NFTs as of this writing include locations across Colorado, Arizona, New Mexico, San Bernardino-CA, and even Orange, New York. Some are very remote and speculative, while others are a part of normal civilization and priced accordingly. Buyer beware of course given the serious nature of these assets.

Perhaps one of the biggest obstacles to understanding how this is all possible is the widespread misconception of what NFTs are. Most of the American population lives under the mistaken impression that NFTs are cartoon art pictures like Bored Apes or CryptoPunks that were all the rage in 2021 and to some extent are still popular in niche circles, but almost anything can be tokenized. More recently, for example, domain names are being converted into NFTs to facilitate faster sales and quicker payouts. The same is true now here with land. Not only can land ownership change hands in the blink of an eye by transferring the NFT but one can also easily tap into the value by pledging it on a peer-to-peer NFT loan marketplace like NFTfi. Fabrica officially announced a partnership with NFTfi this past December, for example. The possibilities are endless

For the perpetual skeptics of all things blockchain that are convinced real business will only ever be done in the real world, a visualization of an NFT on a crypto wallet app might not be all that convincing, especially if the icon for it is situated right next to one of those expensive monkey pictures that kids wouldn’t shut up about years ago. The proof then is in the adventure. With a drive of less than two hours from Downtown Los Angeles, there’s a little plot of land on a quiet street known as Yerba Boulevard. It’s covered in weeds and reddish soil. Empty plains make up most of the backdrop but the suburbs are very slowly creeping their way there. In fact, I’ve since learned who my neighbor is across the street. It’s a 26,000 square foot cannabis facility that was just built in 2022. I bet the owners would be into NFTs (😂). Since that facility is up for sale, numerous 3D surrounding views exist of my plot. Turns out I can even walk to the airport. It’s not much but it’s home to me and all I could afford for the purpose of this story and learning what it was all about. Maybe those 400,000 planned residents will eventually want my land and it’ll make me a millionaire. Ah the allure of California City.

A Fun QSR Chain or “Big Sandwich”?

November 27, 2023 As the small business financing space contemplates competition from merchant-integrated platforms like Square, Shopify, and Intuit, one behemoth is taking over the franchises themselves. The company is Roark Capital, an Atlanta-based PE firm with $37B in assets under management, and they taste delicious.

As the small business financing space contemplates competition from merchant-integrated platforms like Square, Shopify, and Intuit, one behemoth is taking over the franchises themselves. The company is Roark Capital, an Atlanta-based PE firm with $37B in assets under management, and they taste delicious.

Roark Capital already owns Arby’s, Auntie Anne’s, Baskin-Robbins, Buffalo Wild Wings, Carvel, Cinnabon, Carl’s Jr., Hardees, Culver’s, Dunkin Donuts, Jamba, McAlister’s, Moe’s Southwest Grill, Schlotzky’s, Seattle’s Best Coffee, Jimmy John’s, SONIC, Jim’n Nick’s Bar-B-Q, Miller’s Ale House, North Italia, Nothing Bundt Cakes, and the Cheesecake Factory. Three of those are among the top fast-food sandwich chains in America (Arby’s, Jimmy John’s, and McAlister’s Deli). Roark is also presently in the process of acquiring Subway, the leading company in that category by nationwide sales. The deal was announced in August.

But now the FTC is saying not so fast on the basis that it might create a monopoly. According to Politico, “the government is focused in part on whether the addition of Subway gives Roark too much control of a lucrative segment of the fast food industry.”

“We don’t need another private equity deal that could lead to higher food prices for consumers,” railed Senator Elizabeth Warren on social media. “The FTC is right to investigate whether the purchase of Subway by the same firm that owns Jimmy Johns and McAlister’s Deli creates a sandwich shop monopoly.”

While many comments on social media made fun of this regulatory effort, perhaps such consolidation is a wakeup call for the small business finance industry. Once upon a time the textbook definition of a non-bank funding merchant was a restaurant or QSR sandwich shop. Although the target customer has broadened considerably since then, it may be worth keeping in mind that a large diversified portfolio of QSR funding customers might not be so diversified at all. Behind the scenes, it may actually all be a single counterparty. A small business might not be so small. You could be dealing with Big Sandwich.

Summer Dealmaking

July 18, 2023The summer of 2023 has not disappointed. The industry is making moves! In case you missed what moves we’re talking about, here’s a list of the most notable:

7/17/23 – Nav Acquires Tillful

7/14/23 – IOU Financial announces it is being acquired

7/12/23 – Loanspark expands to Canada

7/10/23 – Owners Bank launches SMB loans

6/29/23 – Blue Bridge Financial extends and upsizes corporate note to $20M

6/15/23 – CFG Merchant Solutions surpassed $1B in MCA originations

6/13/23 – Merchant Growth acquires small business loan rights from Loop

eCapital names Todd Zarin as Chief Legal Officer

January 17, 2023MIAMI – January 17, 2023 – eCapital Corp. (“eCapital” or “the company”), a leading finance provider for businesses across North America and the U.K., today announced the appointment of Todd Zarin as chief legal officer. As part of the executive leadership team, Zarin will oversee eCapital’s in-house legal team and be responsible for all legal operations for the company.

“Todd’s proven aptitude and demonstrated ability to skillfully navigate complex legal scenarios make him a valuable addition to our executive leadership team,” said Marius Silvasan, chief executive officer of eCapital. “I am confident his expertise will prove instrumental as we continue to enhance our service offerings and expand into new markets to meet the financial needs of even more organizations.”

Zarin’s legal and corporate career spans more than 20 years, with strategic roles helping public and privately held clients in financial services and other industries succeed while navigating critical moments. Throughout his career, Todd has been instrumental in driving business objectives such as strategic mergers and acquisitions, securing funding through various transactions, and guiding companies through initial public offerings. He also provided guidance and direction on corporate governance and securities law compliance matters.

As a seasoned lawyer and board member, he has served clients in multiple capacities, including as general counsel to a South Florida financial services company and as outside counsel with premier law firms such as Weil, Gotshal & Manges and, most recently, as a shareholder at Miami-based Stearns Weaver Miller. Zarin has also helped clients as a strategic and transactional advisor through his own consultancy.

“eCapital’s unique approach to strategic growth while changing the shape of the alternative finance and lending landscape is exciting,” said Zarin. “The leadership team has a well-defined and ambitious vision for the future, and I look forward helping achieve the company’s long-term goals and continue driving the company’s dynamic growth trajectory.”

Zarin is a member of the Florida and New York bars and earned his Juris Doctor from Brooklyn Law School. He also holds a Master of Business Administration from the Kellogg School of Management at Northwestern University.

About eCapital Corp.

eCapital is committed to accelerating access to capital for companies in the United States, Canada, and the U.K. By leveraging a team of over 800 experts and proprietary, industry-leading technology, eCapital is creating the future of business funding. With a full suite of products such as freight factoring, invoice factoring, lines of credit, asset-based lending, payroll funding, and equipment refinancing, eCapital ensures businesses have the funds they need to do more. Through its Transportation, Staffing, Wellness, Healthcare, Factoring and ABL divisions, eCapital delivers customized funding solutions for over 80 industries. To learn more about eCapital, visit eCapital.com.

# # #

This New Small Business Lending Tech Started in New Zealand

October 3, 2022 Dave Lewis, CEO at Ranqx, co-founded his company in 2015 in New Zealand. With a plan to help small businesses, accountants, and bankers all understand the financial performance of a business, the company eventually realized that such information could be used to improve the archaic small business lending process with banks.

Dave Lewis, CEO at Ranqx, co-founded his company in 2015 in New Zealand. With a plan to help small businesses, accountants, and bankers all understand the financial performance of a business, the company eventually realized that such information could be used to improve the archaic small business lending process with banks.

“The long story short is we pivoted into small business lending because we saw that banks and credit unions were broken and couldn’t efficiently lend to small businesses,” said Lewis, “and we think there’s a huge opportunity to change that going forward.”

At the time, Ranqx was focused on its own domestic market, a nation with approximately 5 million people. It was when Covid started that the company’s technology was finally understood. In 2020, for example, Lewis received a call from the CEO of Kiwibank, saying, “Look Dave I think every CEO of every bank in the world has just figured out that it’s not a good idea to have small businesses visit a branch to fill out forms for a loan because we’re in a pandemic.”

Suddenly, Ranqx became the technology behind Kiwibank’s Fast Capital product, opening the door to a lightning fast online loan application process.

“A small business can apply for working capital in under two minutes. And they’ve got a decision within three minutes of that application,” said Lewis. “Within five minutes they know whether they’re going to be funded by Kiwibank or not.”

More recently, Ranqx is expanding into North America where it sees similar opportunities to improve the loan application process. Though the target customer is still banks, the company is open to working with online lenders, which Lewis thinks can benefit from the tech as well.

“We see a lot of portals that happen in the online lending space, but we don’t see a great use of real time data of APIs, of auto decisioning,” said Lewis, “which we’ll see there are a lot of manual processes that go in there, a lot of document uploading, and a lot of, still people-time required to underwrite and manually spread the financials to be able to get a yes or no decision.”

Ranqx has also recently appointed Ex-JPMorgan Chase CIO and Treasurer John Horner as its new chairman and formed a new partnership with Visa.

“I think the key thing that I would want [the] audience to be aware of is just the alternative data sets that are now available that can be automatedly analyzed and calculated and used within an underwriting decision,” said Lewis. “And the ability to ingest that data from companies like us in an orchestrated way, is something that we can really help accelerate. At the end of the day, it doesn’t matter whether you’re a bank or an online lender, the key fundamentals are, ‘who am I listening to and how likely am I going to get repaid?’”