Reactions to the Treasury RFI: Business Lenders and Merchant Cash Advance Companies Share Their Thoughts

August 13, 2015 The Treasury Department could get an earful from the alternative funding industry during a 45-day public comment period on online marketplace lending that began July 17.

The Treasury Department could get an earful from the alternative funding industry during a 45-day public comment period on online marketplace lending that began July 17.

Treasury emphasizes that it isn’t a regulator and its Request for Information, or RFI, isn’t a regulatory action. The department just wants to hear success stories and opinions on potential public policy issues, a Treasury spokesman said.

“There isn’t a lot of data available on this industry,” the spokesman noted. “The RFI allows us to gather information from the public.”

One portion of the public – alternative funding executives – may have a lot to say on the subject. At least some of the industry’s top players favor regulation or legislation that could clean up the industry and clarify conflicting directives.

“Personally, I’d be glad to see it on the federal level,” Stephen Sheinbaum, president and CEO of Merchant Cash and Capital, said of regulation. “We won’t have to deal with 50 individual states, which is more unruly.”

Others would prefer to see the industry regulate itself instead of having federal agencies issue dictates or having Congress pass laws.

“I would like to put in my two cents,” said Asaf Mengelgrein, owner and president of Fusion Capital, indicating he intended to respond to the RFI. “I see a need for better practices, but regulation should come internally.”

Whoever makes the rules, restrictions seem inevitable because of alternative funding’s prodigious growth, executives agreed. “Regulatory attention is a sign of an emerging industry,” said Marc Glazer, president and CEO of Business Financial Services.

Regulation should curb the practice of stacking loans or advances, which can burden merchants with more financial obligations than they can meet, Sheinbaum said. Stacking has proliferated even though ethical members of the industry avoid it, he said.

At the same time, disclosure statements should become more transparent so that merchants can easily identify how much they’re paying in fees and expenses, Sheinbaum maintained. Merchants should also be able to see how much they’re paying the different entities involved in the deal, he said.

“I’m not suggesting someone should make more or less, but transparency is a healthy thing and this industry could use a little more of it,” Sheinbaum said.

The alternative-funding industry could follow the example of the mortgage business, where more-standardized forms help consumers compare competing offers, Sheinbaum said. “That’s not the case in this industry, so that might help,” he maintained.

The alternative-funding industry could follow the example of the mortgage business, where more-standardized forms help consumers compare competing offers, Sheinbaum said. “That’s not the case in this industry, so that might help,” he maintained.

The industry should not emulate the credit card processing business, which uses complicated and dissimilar contracts to keep customers uniformed, Sheinbaum said. “It’s not so easy for a merchant to understand the effective cost of a transaction – and that’s by design,” he said.

Reviewing those issues could confuse among regulators who don’t understand the industry, Mengelgrein warned. Someone “on the outside looking in” might consider the industry’s fees and factor rates outrageously high, but that’s because they fail to understand the financial risk involved with lending to small businesses, he said.

Before imposing rules, regulators should also bear in mind that many small businesses could not survive without alternative funding, Mengelgrein continued. In recent years banks have failed to step up and help merchants in need of cash, and the alternative lending community has filled the gap.

Sheinbaum agreed. “I hope the regulators and legislators will make an earnest effort to understand all the good that folks in the alternative finance space provide for people,” he maintained. “It’s a critical role we play in keeping small businesses going, and small business is important to this country.”

The Small Business Finance Association could play a critical role in helping government understand the industry, Sheinbaum suggested. He noted that the trade group changed its name from the North American Merchant Advance Association because the industry is adding loans to its initial offering of merchant cash advances.

Whatever shape regulation takes, the industry should keep up with the new rules, Glazer cautioned. “As this industry evolves, we will work closely with our partners and our customers to ensure that everyone is informed about any new regulations and the potential impact that they may have on our business,” he said.

Meanwhile, Treasury’s efforts to comprehend the business are continuing. Its RFI contains 14 detailed questions that respondents could address.

The department held a forum on Aug. 5 called “Expanding Access to Credit through Online Marketplace Lenders.” The event included two panel discussions and roundtable discussions with Treasury staff.

Attendees numbered about 80 and included consumer advocates, representatives of nonprofit public policy organizations and members of the financial services industry, the department said.

Merchant Cash Advance: Do You Know What You’re Selling?

June 22, 2015 Continuing on with the Year of The Broker discussion, I want to now shift focus to the continued wave of new broker entrants that are not receiving sufficient training. I don’t believe that it’s so much the fault of the brokers, as it’s the fault of the companies they are reselling for. Those companies usually fail to provide a structured training regime. Training provided to new broker entrants is typically centered around the memorization of sales scripts, the practice of outdated rebuttals, and the repetition of lines that can end up sounding very canned and robotic.

Continuing on with the Year of The Broker discussion, I want to now shift focus to the continued wave of new broker entrants that are not receiving sufficient training. I don’t believe that it’s so much the fault of the brokers, as it’s the fault of the companies they are reselling for. Those companies usually fail to provide a structured training regime. Training provided to new broker entrants is typically centered around the memorization of sales scripts, the practice of outdated rebuttals, and the repetition of lines that can end up sounding very canned and robotic.

If I had to recommend new age sales training, I’d have to go with my favorite, which is Diagnostic Selling, promoted by the likes of Jeff Thull from Prime Resource Group (www.primeresource.com). Thull explains that as the sales consultant, you should be a valued source of business advantage for your client, rather than just a person that goes through a series of sales material regurgitation. You should have access to products, services, platforms, big data, knowledge, key players, new solutions, forecasts, trends, etc., that the merchant does not have access to, which allows them to see you as a “valued extension” of their organization. This leads to not just new client acquisition, but the real key to making money in our space, and that’s client longevity.

In order to truly achieve this level of sales consultancy, it’s important that you truly understand the products being sold because, firstly, you want to be able to distinguish between the products you are selling so that you can provide a valued consultation. You might find yourself selling one product when you should be referring another. Secondly, understanding these products is important from a regulatory standpoint as the legal connotations of the products must be disclosed properly or mistakes in disclosure, marketing, or funding agreements could become costly.

If you are an independent broker in the alternative commercial lending space, you are usually going to be selling one or multiple of the following products:

- The Merchant Cash Advance

- The Alternative Business Loan

- Equipment Leasing

- Accounts Receivable Factoring

- Accounts Receivable Financing

- Purchase Order Financing

To begin, let’s discuss the Merchant Cash Advance…

Product Value Points

Don’t Let The Critics Win

Critics of the product focus mainly on its high cost and it can be very expensive, but when used properly the product is a great leveraging tool.

Critics fail to shed light on the value of the product in terms of the merchant’s usage. Going back to that Growth Investment example, if the product had not been available, then what were the other sources available for the merchant to take advantage of the growth opportunity? In actuality, there were no other credible sources. Had the Merchant Cash Advance not been available, that investment would not have been made, and a ton of national, state and local economic activity would not have taken place, such as:

- The Equipment Manufacturer’s sale of the equipment

- The Merchant’s generation of $300,000 in revenue based on having the equipment

- The Purchaser’s revenue from borrowing costs incurred from the client using the advance

- My individual commission

- Then all of the federal, state and local taxes that would have been paid as a result

All of that economic activity vanishes if said transaction does not take place. Despite the high cost of the product, the fact is that this transaction would have been a win across the board for all parties involved including the Manufacturer, the Client, the Purchaser, Myself, as well as the Federal/State/Local Government. The true value of business capital, no matter if it’s conventional or alternative, is that the capital should produce enough new revenues so that it truly pays for itself.

The Co-brokering Phenomenon: In Business Loans & Merchant Cash Advance

May 25, 2015 Meet the broker’s broker, the middleman serving the middleman. Some call this co-brokering since both parties will typically share in the commission.

Meet the broker’s broker, the middleman serving the middleman. Some call this co-brokering since both parties will typically share in the commission.

Wait, what?

The broker’s broker might have relationships that the little broker does not. They could have leverage over their funding partners because of the amount of volume they can produce or the amount of professionalism they bring to the table. And they likely have a canny ability to close deals that otherwise would get tossed by the wayside.

Disintermediation is the war cry of today’s famous tech-based lenders but in the Year of the Broker, reintermediation has been the unforeseen byproduct. Big lenders such as OnDeck are shedding third party funding advisors but those advisors aren’t magically going away.

A number of them are still getting their deals funded at OnDeck, just indirectly. They have to go through a broker whom OnDeck has not cut off, a handful of salespeople have told me. Many brokers acknowledge that OnDeck’s rates and terms are not easily attainable elsewhere so they’d rather share a commission with an OnDeck approved broker than risk a dead deal with no commission.

And CAN Capital is known to offer comparable pricing to OnDeck but it’s been reported that new brokers must go through a rigorous audit before CAN will accept their business. It’s not something everybody wants to go through.

With the two largest funders in the industry imposing real barriers to doing business with them, sanctioned brokers play toll booth operator for the swarm of shops that can’t get their deals submitted without them.

Perhaps as a direct result of that, there is now an entire niche of brokers whose only business is brokering deals for other brokers. They have little to no interaction with merchants. They have no marketing budget. They might not even have a website. And they play an almost mystical role of gatekeeper and power broker.

Onesy-twosy woes

A strong focus within the industry has been growth. There’s a lot of time, resources, and salesmanship that goes into courting the lucrative partnerships. Large funders, especially those with VC backing, are typically not interested in mom and pop broker shops. “If they’re only going to send one or two deals per month, we don’t want them,” I’ve heard time and time again.

Even five to ten deals a month can draw yawns. It’s nothing particularly against the mom and pop brokers, but experience has apparently shown them that the same amount of resources are spent on the onesy-twosy brokers as the ones doing a hundred deals a month. The cost benefit analysis has to make sense, they say.

That’s left hundreds or perhaps even thousands of mom and pop brokers to fend for themselves. What outsiders might not seem to realize is that the commission on a $50,000 loan or advance can be $5,000. That’s potentially enough for a stay-at-home parent to pay for the rent, groceries, and all the other bills. A onesy-twosy broker might be completely insignificant to a funder doing a billion dollars worth of deals a year, but to a mom and pop broker, it only takes one deal to pay their bills and only a handful to make them rich, especially if they live in middle America where the cost of living is cheaper.

In From Lowes to Loans, superstar broker William Ramos said he made $66,000 on just one deal alone. While his shop produces more than a million dollars in deal flow a month, it’s easy to see what’s drawing the hoards of newbies in. A $66,000 commission might be the only commission someone needs for an entire year.

There is no licensing required so becoming a broker is as easy as imagining that you are one. And as the space invites the less knowledgeable, a more sinister element has found opportunity as well.

Shady

“There is no president/ruler of the MCA world that can help you with your commission debacles,” wrote PSC’s Amanda Kingsley on an industry forum. That was part of her reply to a thread titled, co-brokering scumbags. The thread might be new, but the circumstances aren’t. A broker sent their deal to another broker who got the deal closed with a funder. The original broker supposedly got screwed out of the commission.

“There is no president/ruler of the MCA world that can help you with your commission debacles,” wrote PSC’s Amanda Kingsley on an industry forum. That was part of her reply to a thread titled, co-brokering scumbags. The thread might be new, but the circumstances aren’t. A broker sent their deal to another broker who got the deal closed with a funder. The original broker supposedly got screwed out of the commission.

It’s a case of stolen deals. “You just have to find the right people to work with. There are a lot of shady characters in this industry,” wrote another user.

1st Capital Loans Managing Member John Tucker, who recently authored, Broker Business Planning, wrote in reply to the thread, “Get everything in writing and research your lender/partner heavily before contracting with them. Talk to other brokers and ask them about their experience with said lender/partner in terms of paying on new deals, renewals and residuals. Get a ‘feel’ for them.”

Several faulted the aggrieved party for not taking the time to hammer out a contract that would allow them to rectify the situation easily through a lawsuit. But even with a contract, pursuing the offender legally could cost more than the commission lost. A stolen deal might cost a broker a few hundred or a few thousand dollars, figures worthy of small claims court.

“Under no circumstances would I ever co-broker a deal,” wrote Tucker. “There’s just no reason to unless you are a newbie and getting trained by said broker.”

But another user wrote, “Sometimes you don’t even know you are co-brokering until after the fact.”

Unscrupulous brokers will be purposely deceitful but for others walking the thin line between broker and funder, it’s difficult to judge what constitutes direct. There are brokers that wholeheartedly believe that if any portion of their own funds are invested in a deal, then they too are a direct funder. That means a broker that syndicates with a variety of funders could be so inclined to identify themselves as a direct funder by extension.

Kingsley wrote, “You have to understand what a ‘broker’ is in this space and understand that it is A LOT different than brokering in another industry.”

She also pointed out that it’s not always the little guy that’s susceptible to becoming a victim, as could be the case if an early deal default leads to a commission chargeback. When that happens, the funder will take back the full commission on the deal from the broker of record. It’s the responsibility of that broker to claw back whatever split of the commission they shared with the sub-broker.

“The broker you sub-brokered for, can vanish,” Kingsley wrote.

Ban the bad guys?

Several industry veterans have suggested creating an ISO/funder blacklist for those that steal commissions or deals. The challenge is that a stolen deal is not always a black and white situation. Often times there are expiration dates built into contracts that allow funders to claim deals if they have not been closed by the submitting broker within a specified period of time. Other times it’s a case of miscommunication, or the victim conveniently left out key details that would certainly add a degree of color to the situation.

Calling out an offender online can quickly devolve into a he said/she said schoolyard brawl. Unfortunately, this might be the only remedy a victim has, especially if they have limited financial resources to pursue legally, or the only evidence of their deal is a handshake or an email.

The bad guys, if they’re engaged in trickery on a large scale, tend to get identified rather quickly. There’s always a few that come in, burn a lot of bridges, and then find themselves completely ostracized from the industry. When the damage is done, they might never be heard from again or they might try to repeat the process by using a different name. Blacklisting a broker or funder wouldn’t be foolproof, especially if the company owner legally changes their name, which has actually happened before.

Trust

Through it all, Tucker offered this advice, “In a nutshell, the only true thing protecting your compensation is a very good relationship with an honest, credible and ethical lender.”

And if you have to go through a broker, make sure you choose the right one. Don’t blindly send your deal to somebody you met on a message board. An unscrupulous player will tell you exactly what you want to hear. Ask around for references. If nobody’s ever heard of them, chances are you’re talking to the wrong shop.

Even the author of that thread conceded that co-brokering offers benefits. “I’m all for co-brokering deals, especially if someone has a solution that may suit the client better than a traditional MCA or when an MCA wont work,” he wrote.

So there just may be a place for the broker’s broker, whether as a gatekeeper, power broker, or toll booth operator. And like it or not, reintermediation has ironically become a byproduct of disintermediation. There are sadly no algorithms that exist to vet how a broker might treat another broker. Co-brokering is a trade that relies on the most basic of basics, trust.

Nothing’s more valuable.

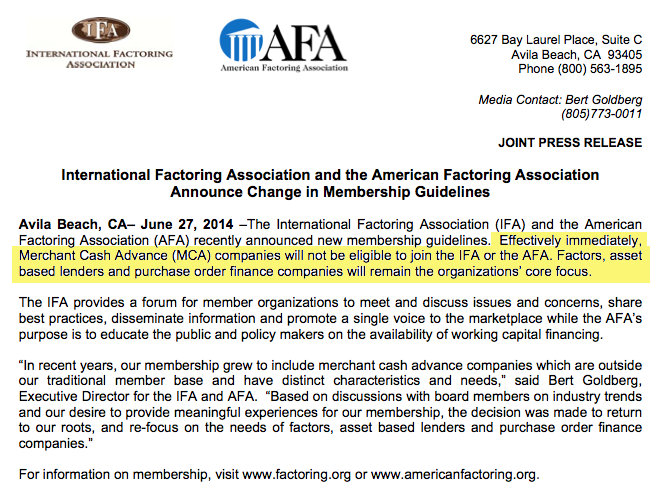

IFA Tells Merchant Cash Advance Companies to Get Lost

August 22, 2014On June 27, 2014, the International Factoring Association (IFA) and the American Factoring Association (AMA) publicly announced their decision to ban merchant cash advance companies from obtaining memberships. The nature of just how public that announcement was is questionable since nobody in the industry seemed to be aware of it, including a dozen plus merchant cash advance companies who have been longtime members of the IFA.

The timing of the ban is leaving a few companies unsettled since it was announced immediately following the IFA’s annual factoring conference in which merchant cash advance companies not only exhibited but were also amongst some of the event’s featured speakers.

To illustrate just how awkward the timing was, the IFA had just begun to thank everyone for attending the conference in the May/June issue of their magazine and in practically the same breath revealed that all merchant cash advance companies were banned going forward:

The IFA annual conference has grown to become the number one industry event for the factoring and receivable finance industry. The IFA convention is now the largest and most relevant event of the year, and as the attendees of San Francisco conference can attest to, it has become the must attend event of the year. Thank you to everyone that attended and helped the IFA achieve this unprecedented growth.

… … …

Due to the number of complaints that have been received, both the IFA and the AFA have voted to bar Merchant Cash Advance companies from membership in each organization. The boards of both associations felt that the model for this type of financing has changed and that there are a number of MCA companies that are not operating in an upfront manner. Given that the goal of both organizations is to assist the factoring community, we found it best to dissociate ourselves from this type of financing.

It is unclear if the IFA’s current merchant cash advance members were immediately terminated or if the rule only applies to new applications going forward. This is especially confusing since the feedback we’ve gotten from their members so far is that nobody knew this had even taken place.

Hopes for a peaceful breakup between the two industries has possibly weakened after a story was spotted in the July/August issue of the IFA’s Commercial Factor magazine aimed at attacking and discrediting merchant cash advance companies.

Hopes for a peaceful breakup between the two industries has possibly weakened after a story was spotted in the July/August issue of the IFA’s Commercial Factor magazine aimed at attacking and discrediting merchant cash advance companies.

The article by factoring attorney Steven N. Kurtz alleged that tortious interference, regulatory scrutiny, and rampant disorder were reasons to steer clear of merchant cash advance companies. A more detailed breakdown of his arguments can be found on dailyfunder, but it fails to mention the way he concludes the story:

At the moment, there seems to be too many new players in the merchant cash advance industry, with no experience and loose underwriting standards. There is likely going to be a shakeout because the industry segment has a high default rate and investors who lose money will lose their appetite for the deals. Before the market corrects itself, the factoring industry will have to ride out the storm by adjusting their business practices to effectively compete.

Did you catch his last sentence about riding out the storm? He’s saying to adjust, hold on, wait for a shakeout, and hopefully business for factoring companies will go back to normal. The reason it’s not normal now is because merchant cash advance companies are killing them competitively.

I guess if you can’t beat ’em, ban ’em? They should’ve just said that was the reason from the beginning…

How to Value a Merchant Cash Advance Company (or Alternative Lender)

February 9, 2014If you’re at all interested in the future of the merchant cash advance industry, you need to read Wall Street Evaluates Merchant Cash Advance in the first issue of DailyFunder. It offers a fresh perspective through the eyes of financiers outside the industry looking in.

Names include:

- Jason Gurandiano, Managing Director in Deutsche Bank’s Financial Technology Group

- David Cox, Managing Director at Evercore Partners

- Thomas McGovern, Vice President at Cypress Associates

- Steven Mandis, adjunct professor at Columbia Business School.

The article is relatively broad but it communicates some very important points:

1. Some players in the space exist as lifestyle businesses. They’re not scalable, their success is largely attributed to what the owner does for it, and company’s long term vision is to basically make sure the owner takes home a nice paycheck.

2. Some of the big players in the space are on similar growth trajectories. Nothing differentiates each of them from the pack, and none of them really have an advantage over the other.

3. EBITDA is a bad valuation measure and growth is a good one.

3. EBITDA is a bad valuation measure and growth is a good one.

On point #1, a lifestyle business is no good to a professional investor in this space. Aside from the success usually being owner-dependent, one question an investor is certain to ask a prospect is, “If I gave you $100 million today, what would you do with it?” There are many wrong answers to that question. If you said solicit more ISOs, buy more leads, or hire more sales people, they’re going to wonder why you haven’t done those things already.

On the same token, those answers would communicate that you’re going to do the exact same thing you’re already doing. It’s a mistake to think that scaling in such a manner will keep the original margins intact. It also does nothing to protect the company against change or enable it to grow exponentially.

On point #2, it’s great to be big, established, and growing at a moderate pace, but what good is that to an investor looking to double, triple, or quadruple their money? And who’s to say that a moderate growth strategy will continue as it has in the past?

Many many many (did I say many yet?) people have come into this space with visions of grandeur, to be bigger than CAN Capital in less than 24 months. What do their plans usually consist of? Pay higher than average commissions and fund deals they shouldn’t be funding. To date, none of those companies are bigger than CAN Capital and some of them are out of business. A growth plan can’t consist of funding deals you don’t want to and paying commissions you can’t afford. That’s called a suicide mission and it’s very effective.

Some big funding companies may appear sustainable on the outside but they’re woefully fragile on the inside. Jason Gurandiano said it best with this quote, “The general knock on merchant cash advance has been that they are an ISO-centric model.” I’m not discounting the value of ISOs in this business. To some extent they rule the roost, and that’s the problem in the eyes of investors. Many merchant cash advance companies rely on a handful of symbiotic relationships. The ISO relies on the funding company for commissions and the funding company relies on the ISO for deals. But what happens if:

- The ISO is enticed with higher commissions or better service with somebody else

- The ISO’s deal flow slumps

- The ISO goes out of business

- The ISO uses unscrupulous sales practices when selling the funding company’s product

- The ISO uses their relationship as leverage on the funding company to make bad decisions

- The funding company needs to reduce commissions but the ISO can’t sustain it

An ISO-dependent merchant cash advance company doesn’t have much control over growth. Believe me, I’ve been on those phone calls where the ISO is asked to send more business. But what happens if they have no more to send? Or what if they would just rather do most of their business elsewhere?

Again, there is absolutely nothing wrong with a purely ISO-centric model in general, but it is much less attractive to investors looking to do a deal in this industry and that’s the theme of this post.

Point #3 is unique because it addresses the how to value a company once you’ve found one worth investing in. Earnings Before Interest Taxes Depreciation and Amortization (EBITDA) is not a viable valuation formula here as it doesn’t make sense to measure the worth of a company dependent on expensive debt by stripping away the cost of that debt.

Point #3 is unique because it addresses the how to value a company once you’ve found one worth investing in. Earnings Before Interest Taxes Depreciation and Amortization (EBITDA) is not a viable valuation formula here as it doesn’t make sense to measure the worth of a company dependent on expensive debt by stripping away the cost of that debt.

According to Aswath Damodaran, debt to a financial service company should be treated like a raw material. In his 2009 paper, Valuing Financial Services Firms, he states, “debt is to a bank what steel is to a manufacturing company, something to be molded into other products which can then be sold at a higher price and yield a profit.” It is a perfect analogy for a merchant cash advance company.

Damodaran’s analysis covers a range of situations but I find an Asset Based Valuation intriguing. It states, “How would you value the loan portfolio of a bank? One approach would be to estimate the price at which the loan portfolio can be sold to another financial service firm,” There isn’t a lot of precedent for that in this industry unfortunately. Damodaran continues though with, “but the better approach is to value it based upon the expected cash flows.” For certain, one would have to take into account the renewal rate, renewal commissions, the average recovery timeframe, and the default rate.

If you bought $100 million in RTR today, how much would you get back 1 year from now or 2 years from now? This number is going to differ from company to company.

An Asset Based Valuation might be in order for a funding company that is winding down and shedding its existing portfolio, but it’s not appropriate for one with growth. One should assume that they’re buying a growing business when investing in a merchant cash advance company, not a packaged portfolio.

One question an investor might ask is, “what am I buying?” The average merchant cash advance company can be perceived as nothing more than a vehicle to maximize the spread between revenue and borrowing costs. They’re not really businesses in the traditional sense, more like arbitrageurs. They buy leads and/or they pay commissions, there are some fixed costs, but there’s not a whole lot more to it. There are virtually no barriers to entry and anybody can replicate the model. So you invest in the people who are doing it currently and their system (assuming it’s working so far). The value of that might only be equivalent to 1x – 4x annual profit. Why pay more when competition can drag margins down, regulations could disrupt the space in the future, or the investor could just as easily start their own company with the funds they have instead?

With that said, the average merchant cash advance company is more attractive to a lender than an equity investor. Additionally, they can also offer a nice monetary return by allowing people to participate in the funding of individual deals. Both are indeed what many investors choose to do, either lend money to these companies or syndicate. Why buy the cow when you can get the milk for free?

Merchant Cash Advance companies that make the headlines with big equity investments are not average. They create value, rather than just engage in arbitrage. They’re building something, changing something, disrupting something. They don’t profit off spreads in the market, they create the market and dominate it. Today this typically happens through technology, and not just any technology, but technology that leads to substantial future earnings. There’s a difference between spending a million dollars on a platform to make things more efficient and spending a million dollars on a platform that causes earnings to increase by 1,000%. Too many companies view technological investments in the former sense, a cost that eats into the spread instead of one that can blow the roof off of it.

Investors are looking for companies that plan to soar from Point A to Z, not ones that are moseying along from A to B.

RapidAdvance was said to have gotten an Enterprise Valuation in excess of $100 million when being acquired by Rockbridge Growth Equity. For the most part that number reflects Total Debt + Total Equity – Cash. When you buy a company, you’re buying their debts as well. 90% of their enterprise value could potentially have been the value of their outstanding debts. Of course I doubt it was, but it should put their eye opening valuation into perspective.

Contrast the RapidAdvance deal with the most recent valuation of Lending Club at $2.3 billion. Lending Club earns substantially lower returns per deal but they have an engine for growth that is virtually unmatched. In the month of August 2012, they booked $70 million in loans. In January of 2014, they booked $258 million. That’s 3.7x the monthly volume they were doing less than 18 months ago. That’s what an investor calls an opportunity.

How do you value a merchant cash advance company? There’s no easy way to do it and it largely depends on whether or not they’re an arbitrage shop chugging along or one creating substantial value.

There’s plenty of free milk out there. Why would someone pay top dollar for your cow?

– Merchant Processing Resource

Merchant Cash Advance Hits Shark Tank

October 26, 2013 If you missed Friday night’s episode of Shark Tank, you absolutely must catch a rerun of it. Jason Reddish and Val Pinkhasov came on the show to pitch their merchant cash advance company, Total Merchant Resources. It was one of the best few minutes in merchant cash advance history for several reasons:

If you missed Friday night’s episode of Shark Tank, you absolutely must catch a rerun of it. Jason Reddish and Val Pinkhasov came on the show to pitch their merchant cash advance company, Total Merchant Resources. It was one of the best few minutes in merchant cash advance history for several reasons:

- Mark Cuban, the 213th richest man in the U.S. feared the growing popularity of expensive short term financing would invite tough government regulation.

- Kevin O’Leary understood that there were no barriers to entry and thus anyone with money can get into the industry.

- Robert Herjavec thought the capital was too expensive for small businesses.

- Kevin O’Leary said that non-bank alternative lenders like Total Merchant Resources were necessary to keep businesses afloat.

- Jason Reddish went at the Sharks like a Shark himself.

TMR walked away with a rather small 400k valuation through the deal they made with Kevin O’Leary that gave them 200k for 50% equity. It was O’Leary’s claim that his connections and capital would blow the lid off their business that was too good to pass up.

O’Leary had a compelling argument for why his terms were non-negotiable. Anyone can be in this business. The valuation itself was moot because two guys with a relatively small operation just became partners with a famous venture capitalist worth $300 million. Had I been in their circumstances, I would’ve taken the deal as well.

O’Leary’s name in the space makes TMR relevant and a company to watch out for, but they are by no means guaranteed success. They are up against much deeper pockets. Dan Gilbert, the 126th richest man in the U.S. owns RapidAdvance (through Rockbridge Growth Equity), a firm that got an enterprise valuation of over $100 million. Google and Peter Thiel have their hand in On Deck Capital. Google also has a stake in Lending Club, a peer-to-peer lender worth $1.55 billion that threatens to disrupt the alternative business loan market with their new loan product come early 2014. Capital Access Network funds nearly three quarters of a billion dollars a year. Every day another power player swoops in and raises the stakes, putting O’Leary in a position he’s probably not used to being in himself, in the shark tank.

At the end of the day, there are a lot of profitable ISOs and small funders. Pinkhasov and Reddish did what no one else to date has done, gone on TV and pitched Mark Cuban on merchant cash advance. And for that, they will go down in history. We’ll follow their story as it develops and I invite them to e-mail me if they’d like to comment.

You can follow the thread about their appearance on the show and find the link to the video on DailyFunder.

Merchant Cash Advance Industry is Busy at Work

May 16, 2013 After what was one of the wildest two weeks in Merchant (MCA) history, the game-changing news finally subsided, but no one is taking a deep breath. Instead, everyone is busy working their butts off trying to help small businesses grow.

After what was one of the wildest two weeks in Merchant (MCA) history, the game-changing news finally subsided, but no one is taking a deep breath. Instead, everyone is busy working their butts off trying to help small businesses grow.

UPDATE 5/16: RapidAdvance has acquired the operating assets of ProMAC. First Instance of consolidation that we’ve been predicting would happen this year. See news release detailing the acquisition HERE.

There is just loads of capital available right now and the technology is catching up quick to support the mass deployment of it. A writer for the American Banker believes that the MCA industry is even beginning to threaten community banks.

Many community bankers would be open to using online applications and other technological tools to make faster loan decisions, says Trey Maust, co-president and chief executive at the $121 million-asset Lewis & Clark Bank in Oregon City, Ore. But most community banks use a business model that requires more hands-on interaction with borrowers, he says.

Hands-on is another term for driving back and forth to the bank for appointments, having the bankers visit your business, all the while they try to sign you up for other bank products, like checking accounts that incur a monthly fee.

Who’s at Work

We know some of the major industry players but it’s interesting to see who else is doing significantly large volume. Pearl Capital recently reported funding $7 million in a single month and United Capital source came in at a tad shy of $4 million in just this past April. These are firms you may have heard of already, but they’re now sitting at the big kids table.

What the Generals are Saying

If you haven’t been paying attention to the DailyFunder.com forum, 4 Chief Executives have contributed to the site in a very meaningful way by sharing their thoughts on the MCA industry at large. This is the kind of wisdom you would normally get in bits and pieces through occasional citation in the Green Sheet or other publications, but the full monty has materialized in the very exclusive CEO Corner. Some key highlights from what they’ve shared so far:

Excerpts from Jeremy Brown, CEO of RapidAdvance:

Those of us that have been in this business for 5 years or more – Rapid started in 2005 – are excited at the positive press we get today vs. several years ago and how we are becoming embraced and accepted as a mainstream product. More PE firms, banks, and others want to invest in or lend to the industry. Those groups have always been intrigued by the returns in this industry but the conversations are different today.One thing I think will be different next year are fewer deals offered over 12 months in payback period. When you look at the data over an extended period of time, 18 month term loans don’t make sense for the merchants that are funded. It’s not the most efficient use of funds, limits the ability for the merchant to renew and the longer term deals are far riskier. (See: Year in Review and What Next Year May Bring)

Isn’t that the point of a 6 month MCA – to meet a current need and have the merchant be able to draw again in 4-6 months for the next capital need? That is the problem with the 15 – 24 month deals that are being offered to merchants today. Our industry is based on providing working capital to merchants. By its very definition, working capital is less than 12 months. Longer term deals are permanent capital, even when they are repaid over 15-24 months.it was no surprise when the economy tanked in late 2008 that the merchants in our portfolios at that time took a major hit to sales and therefore the funding companies losses increased by 50% or more on their outstanding portfolios. So what happens when the next recession – big or small – hits and funders have portfolios out to 24 months? It doesn’t take an MBA from Harvard to figure out that answer. (See: Working Capital or Permanent Capital

Haven’t gotten into the industry myself in 2006, I can totally validate the complete 180 in press coverage. I’ve put all my energy into MCA and it’s gratifying to finally hear the praises so many years later.

Excerpts from Steve Sheinbaum, CEO of Merchant Cash and Capital:

The industry already services hundreds of thousands of small business merchants with cash advances for growth and other purposes based upon monthly credit card receipts. For years this has been the basic model of operation. But, what about the substantial number of businesses that require quick and easy access to capital who don’t accept credit cards or don’t produce enough in monthly credit card receipts to qualify under the normal MCA guidelines? Tens of thousands of businesses could use the capital infusions the industry provides daily but either don’t think they’ll qualify or, because of our lack of creativity, the industry hasn’t produced a means of addressing their needs. These businesses would make great customers but because of the rigid requirements we have in place to protect our livelihoods we’ve left money on the proverbial table.That’s not the case anymore. (See: Creativity in the C-Suite…Another way to Fund!)

In regards to advances on gross revenue instead of just credit card payments, he’s absolutely right.

Excerpts from Andy Reiser, CEO of Strategic Funding Source:

the most important part of any deal is the people. We rely heavily on the relationships we have with the client and most importantly with our ISO partners and ISO syndicate partners who invest side by side with us. Valuing these relationships is far more important than relying solely on the numbers and how sophisticated our technology is.Over our 8 year history, we have noticed that the performance of a deal has more to do with the relationship we have with our ISO partner and ISO syndicate partner, then with the deal itself. We have all kinds of tools available to help us analyze the potential success of a deal – FICO scores, due diligence checklists, signed affidavits, warranties and representations, scoring models, algorithms, etc. And yet, some of the ugliest deals on paper have been some of our best performers, while some of the most attractive deals on paper have been nothing but trouble. (See: Business and Baseball Fantasies)

During my time as a head underwriter, I witnessed the exact same thing. Solid referral partners had solid performing clients even if they didn’t look so good on paper. Likewise, the shakier resellers had clients that underperformed across the board, including the deals that looked cleanest.

Excerpts from Craig Hecker, CEO of Rapid Capital Funding

As each MCA company grows and creates a positive reputation, we all grow as an industry…together. But as our popularity grows, however, so does our competition. We already know that Amazon, eBay, and Google are stepping into the market, and AMEX is looking to expand their short term financing portfolio. These big business industry leaders will help build our brand of finance and benefit our portfolios, but I also think it is fundamental that we market ourselves as the alternative to big business finance and identify ourselves with the small business owner. (See: Small Business and How MCA Can Bridge the Gap to Success

We’ve got some big names in the industry now, whether they are financing the merchants directly or backing the funders that do the financing. I agree that you need not be intimidated by competing against these established brand names. Positioning yourself as the funder next door, people that have walked a mile in the merchant’s shoes (literally) can actually be a strong advantage.

What’s Next?

We’re pretty confident there will be more big headlines in the near future but for now we can’t confirm or say anything. DailyFunder.com is also lining up additional industry captains to participate in the CEO Corner and I’m sure there will be plenty of nuggets for us all to dissect. They’re probably the best source of MCA information that you can possibly get.

Stay tuned.

– Merchant Processing Resource

../../

MPR.mobi on iPhone, iPad, and Android

Soul Mates: Merchant Cash Advance and Silicon Valley VCs

May 1, 2013 Almost 1 year ago to the day, I wrote a piece titled How the Facebook IPO Affects the Merchant Cash Advance Industry. In a most fitting way to commemorate this anniversary, it was reported early this morning that Google Ventures and Peter Thiel are investing in On Deck Capital (“ODC”) through additional Series D Financing. Thiel is especially symbolic in this case as he was the first outside investor in Facebook back in 2004.

Almost 1 year ago to the day, I wrote a piece titled How the Facebook IPO Affects the Merchant Cash Advance Industry. In a most fitting way to commemorate this anniversary, it was reported early this morning that Google Ventures and Peter Thiel are investing in On Deck Capital (“ODC”) through additional Series D Financing. Thiel is especially symbolic in this case as he was the first outside investor in Facebook back in 2004.

But don’t expect Jesse Eisenberg to be called upon to play Noah Breslow or Mitch Jacobs in a movie about small business lending just yet, as the ODC story is a tad less revolutionary than facebook. Or maybe it’s not. Google Ventures is not one of the usual backing suspects in the MCA industry, but their involvement in this case is a perfect validation of my prediction 1 year ago.

Merchant Cash Advance financing turns 15 this year and split-funding goes back more than two decades, but the best of times are just beginning. On September 19, 2012 I bid farewell to an era and made my case for the one I foresaw on the horizon. Facebook wasn’t the first social network on the Internet, nor was their concept original, but they changed how we interact with strangers, friends, and family members online forever. There is a familiar trend with ODC and even Kabbage, two names that every journalist appears obligated to mention these days when writing about Main Street. Perhaps their technology based approaches send a tingle up the leg of the mainstream media or maybe they’re just really changing the game. They definitely appeal to the Silicon Valley crowd in a way that the old guard of Merchant Cash Advance companies apparently do not.

“Old guard, did you just say old guard?!”

Contrary to urban myth, On Deck Capital and Kabbage are not taking on small businesses all by themselves. They are but a fraction of the overall alternative business lending market with the leaders being anything but old guard. Debt and Equity are pouring into these firms and there are no signs of it letting up any time soon. I can’t go a day without a fund, lender, or investor reaching out to me in some way with the hope that I can steer them to a funding provider in need of a capital raise. Their options to get in now are running low and my advice to them is to set your sights lower on ISOs. The big funders have got capital covered and the ISO market is the next gold rush.

The industry can’t grow without originations and most funders depend on some level of ISO business (a few entirely) to hit their benchmarks month after month. So the funders do their job well, but the lead generators are driving a large percentage of the growth.

The industry can’t grow without originations and most funders depend on some level of ISO business (a few entirely) to hit their benchmarks month after month. So the funders do their job well, but the lead generators are driving a large percentage of the growth.

In March, I attended the Search Marketing Expo in Silicon Valley. In a sheer twist of fate, at the same time a Merchant Cash Advance guy like myself was touring the campuses of Facebook and Google, it appears that Facebook and Google were busy touring the campuses of a Merchant Cash Advance company.

The connection between Silicon Valley and alternative business lending is beginning to run deep, very deep. I think we’re soulmates. Only time will tell.