Skintech? Fintech Lenders in China Accept Nude Photos As Collateral

June 14, 2016 Some online lenders in China are taking an invasive application process to a whole new level, according to People’s Daily, a Chinese state-owned newspaper. To increase the likelihood of repayment, applicants may be required to upload a nude photo of themselves while holding an ID card, along with contact information for their friends and family members. And if they don’t pay, they’ll threaten to distribute it to all of them accordingly.

Some online lenders in China are taking an invasive application process to a whole new level, according to People’s Daily, a Chinese state-owned newspaper. To increase the likelihood of repayment, applicants may be required to upload a nude photo of themselves while holding an ID card, along with contact information for their friends and family members. And if they don’t pay, they’ll threaten to distribute it to all of them accordingly.

People’s Daily wrote that the borrowers tend to be educated university students and they are willing participants to these harsh terms if it means they can get the loan they seek. After all, they actually have to take the photos and upload them to the lender in the first place. Insiders reportedly said that naked IOUs have been a practice for a long time.

A reporter for Sixth Tone, a hip media company overseen by the Chinese government, was able to find a student lender online during their journalistic investigation that indeed requested a nude photo and family contact information. The ability to actually repay the loan was not assessed by the lender.

Fu Jian, a lawyer at Yulong Law Firm based in Zhengzhou that was interviewed by Sixth Tone said that the use of a naked photo as collateral is not forbidden by law, even if it does raise ethical questions. Were the photo to be leaked, only then would the law have been broken. “The online lending industry is like a food chain with some huge financial groups on the top, followed by the platforms, then the middlemen,” Fu said to Sixth Tone. “Students, sadly, are just the prey.”

The highly predatory practice is obviously carried out by unscrupulous players and is not representative of the fintech industry in China.

‘We Serve a Fragmented Market That is Ripe for Disruption,’ says Patch of Land CEO

June 3, 2016$484 million: That’s how much real estate crowdfunding platforms attracted in 2015, which was three times of that the previous year. There are an estimated 125 such portals and the new SEC rule which allows non accredited investors some leniency to invest in these projects. To demystify real estate crowdfunding, AltFinanceDaily spoke to Patch of Land’s CEO Paul Deitch to unravel the concept, measure the momentum of investor interest and the regulatory environment. Here are excerpts from the interview.

What’s on the horizon for Patch of Land this year?

Now that Patch of Land’s model is proven, we will be adding complimentary products for the real estate entrepreneur and investor, accompanied by a broadening of funding strategies. For example, we recently launched the new midterm loan product that addresses the opportunity in the $4 trillion single-family rental space.

How is the investment momentum different from that in ‘08-’09?

One of the biggest changes between then and now has been the enactment of the JOBS Act, which actually came about as a result of investment conditions in ‘08-’09. Peer-to-peer lending came into existence during the 2008 Recession when consumers and small businesses could not rely on banks for their funding needs. In 2012, President Obama signed a historic bill called the JOBS Act (Jumpstart Our Business Startups Act), allowing companies to raise working capital in the form of debt and equity via a crowdfunding model. When the SEC implemented Title II of the JOBS Act in 2013 it allowed companies to publicly solicit, via Internet marketing, their equity and debt offerings; private placements could now be advertised. Marketplace lending is an evolution of peer-to-peer lending, defined by the participation of traditional financial institutions purchasing the loans being issued by P2P lenders.

Whom do you consider your competition in the industry and how do you differentiate yourself from them?

We approach the competition question from a different perspective. One would think that other online lenders or real estate crowdfunding companies are our competition but they are not. We are all working towards creating more efficiency, transparency and access to real estate and investments. The market that Patch of Land is serving is fragmented, locally delivered, and highly manual — it is ripe for disruption. Banks are exiting the space due to capital and liquidity constraints and hard money lenders are limited by a single source of capital and local footprint. Unlike these offline incumbents, Patch of Land has a national footprint, and uses proprietary software to quickly and reliably make first lien position loans, pre-fund those loans, and then crowdfund the financing from thousands of investors (both individuals and institutions) on a fractional or whole loan basis.

Who regulates P2RE? And what are the challenges there?

P2RE and the real estate crowdfunding sector is regulated by the SEC. Patch of Land operates under Title II, Regulation D, Rule 506(c) whereby we can only accept investments from accredited investors, as defined by the SEC. This is a strict regulation that requires thorough diligence and vetting of the accredited status of the investor. The biggest challenge we face is that we have many retail investors who want to invest with us and we cannot accommodate them.

How are the ripples in the capital markets affected or will affect business?

Capital markets volatility has not had an adverse effect on our business. Our capital sources are very diversified and are not dependent on large capital market players. Over 90 percent of our loan volume has been, and continues to be, funded by crowd capital. We have on-boarded multiple institutions of various sizes that buy loans on a fractional basis, in addition to the whole-loan forward flow agreements in place.

How is crowdfunding for real estate different from marketplace lending specifically?

Crowdfunding for real estate, specifically when referencing debt, is a subset of marketplace lending. Patch of Land is a ‘real estate marketplace lender’ because we focus specifically and exclusively on debt and do not offer any equity projects for funding. Equity deals are crowdfunding deals, not marketplace lending deals. Therefore, a real estate marketplace lender that transacts with individual investors can be considered a crowdfunding platform, and a crowdfunding platform that does not transact in debt is not a marketplace lender. Two other elements that differentiate crowdfunding from marketplace lending are: 1) prefunding, where the platform fully funds the loans upfront and therefore is not engaging in crowdfunding that usually involves raising capital first, before disbursing it to the sponsor/borrower; 2) marketplace lending includes institutional and individual investors who participate in loan purchases, whereas a crowdfunding model is focused exclusively on individual investors.

How is crowdfunding poised to change real estate investing?

Traditional real estate (debt or equity) can be highly time consuming. We offer an alternative to have real estate debt as part of a portfolio, bringing both new and experienced investors all the data they need to make a decision. Most would never have the time to aggregate this much data on their own, through traditional methods. Crowdfunding allows capital to flow more easily to across the nation, rather than locally, to places and projects that might have been shut out or simply left behind because they were too difficult to assess, evaluate and understand, or were the purview only of local investors and gatekeepers “in the know”. Crowdfunding puts investors in the driver’s seat, giving them the power to pick and choose investments that meet their personal risk/return needs. It allows for investment strategies that are both more “bespoke,” and yet more diversified -both in the way of product type and geographies, all through fractional investments across a technology enabled, online platform. Investors not only have broader choices of where to invest, but they can do it from their mobile phones in seconds.

Merchant Cash Advance Accounting Q&A

May 25, 2016

As a successful and knowledgeable Merchant Cash Advance accountant I often receive questions from MCA business owners and syndicators. In the last tax season, my accounting firm recognized that many of the questions we receive are distinctly similar. In the following article I address the most common questions my accounting office receives.

Question #1: When I am accounting for my Merchant Cash Advance company isn’t a cash advance accounted for in the same way as a loan? It looks the same on a spreadsheet so isn’t the interest calculated in the same way as a normal loan?

Yoel Wagschal CPA: No. Merchant Cash Advance companies do not have interest. If you have interest then what you have is a loan business, not a Merchant Cash Advance business. Loans use an entirely different method of accounting. If you are still accounting for your Merchant Cash Advances as loans with interest then you will have regulatory issues. If you tell an IRS agent that you are not a loan company but they see your books are exactly like a loan company, how do you think that will end for you? Loans and interest are in a different world. You are the last person who wants to combine those two worlds. You need to see how they do their books at an accounts receivable factoring company and model yourself after them. They do it the way my accounting firm presents it.

Question #2: Your article mentions two ways in which Merchant Cash Advance Companies can account for transactions (cash basis and accrual). Are those the only two ways in which my accounting can be processed?

Yoel Wagschal CPA: I guarantee you would have a big argument if you brought 100 accountants together and asked them all this question: How do I recognize revenue in an accrual basis (from a GAAP standpoint) if I am allowed to take the entire income this year? You would have all kinds of voices and differences of opinions because there is no guidance for this industry. I have done the research and structured an accounting methodology. I’ve spoken with the biggest firms and dealt with the biggest names in this industry. I do have a passion for MCAs. When it comes to a tax standpoint, if you file a cash basis and you want to minimize your exposure, there is really only one way to do it. Those two ways (cash and accrual) can be kept so that they are converted from one to the other at the end of the year. Hence, if you want to prorate the income portion of your receivable (cash basis) I would still keep the books on accrual then convert it at the end of the year. You could do this with a single journal entry because it simplifies the bookkeeping process. You end up with an accrual basis financial statement and a cash basis tax return.

Question #3: I keep being told that my tax liability is based on the difference between what I spend (including funding merchants) and what I receive. For example, if we fund 100K and collect 140K in 140 days how should we keep our books? Right now we don’t recognize any income until we get back the initial funding, even if we renew the merchant over and over. Please elaborate on how revenue should be accounted for. I want to minimize my tax liability but I also want to be sure that this is the correct way to go about it.

Yoel Wagschal CPA: I have a very simple quiz:

YWCPA: Do you trust your accountant?

MCA: Yes. Yes, I do.

YWCPA: You should not. Even if you were my own client I would tell you the same thing. Why do you trust your accountant?

MCA: Because they are a professional. This is what they went to school for. This is what they do for a living.

YWCPA: Do you consider yourself a smart person?

MCA: Yes, I do.

YWCPA: Is it possible that you are smarter than your accountant? Is it possible that they simply learned a different trade than you?

MCA: Yes, that is possible.

YWCPA: Ok, then you should use your own IQ to see if what your accountant says makes sense. If your accountant tells you something that doesn’t make sense about your own business, and you believe your accountant because this is their job then you are not using your high IQ. This is especially true if you have strong negative feeling towards what you are being told. I am not telling you to jump to conclusions. I am saying you should ask questions. Think about this for as long as it takes. Your accounting should be clear and understandable to you.

I am a college professor. When I teach the principals of accounting I always start with debits and credits. I start here because students must know this concept through and through in order to be good accountants. It is the basis of all accounting. New students struggle with the logic behind this principle and I always respond that there are two options: The first option is simply to trust me. They can memorize the information and never know what it means. The second option is to completely understand. This is the option that both my students and Merchant Cash Advance business owners must choose. You, as the business owner, must understand where your own numbers come from. You must understand the foundation of your own accounting. You are entitled and responsible to understand it because of what you must sign on your company’s tax returns.

YWCPA: Do you know what you are signing on the tax return?

MCA: Do I know…?

YWCPA: Do you know what the fine print says directly above where you sign? It says:“Under penalty of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.” That is what you sign. Now, do you know what the preparer has to sign?

MCA: The same thing…?

YWCPA: The preparer signs an acknowledgement that they got paid! What I am saying is that you, the business owner, is ultimately responsible for the numbers that are on your tax return. It is you, not the preparer, who certifies that the numbers are legitimate. Of course, accountants are bound by Circular 230 and code of ethics but the level of responsibility is much higher proportionately to the tax payer than to the tax preparer.

Recognizing income only when a deal pays off is clearly, in my humble opinion, “Fraud and Tax Evasion”. I would not sign off on such a tax return. It goes even further that a lot of people who are saying this type of stuff will add that a renewal is an extension of payment and you don’t have to recognize this until the renewal is completely paid off. In this theory you can be in business for 50 years making billions of dollars and pay zero tax. If you were an IRS agent, would you accept that position?

MCA: Mmmm… What’s your point?

YWCPA: Just answer the question. If you were the IRS agent, would it help if the taxpayer told you “my accountant said it was fine”?

MCA: NNNnno.

YWCPA: That’s my point.

Question #4: When my company advances funds to a merchant how do I account for this? Also, how do I account for my company’s income with cash basis (tax return)?

Yoel Wagschal CPA: Ok, we know that in cash basis accounting we don’t recognize revenue before it is actually received. For instance, a grocery store that lets a customer take an order on credit doesn’t recognize revenue at that point. Income is recognized when funds come in.

Now we will think about the Merchant Cash Advance industry. Let’s start with when you advance funds to a merchant. For this example you advance 100k to a merchant and the payback is 140k. The 100k you send to that merchant should not be expensed. That 100k should stay on your balance sheet. You don’t recognize any income because you haven’t collected any income yet.

At the end of the year we have collected half of the advance. It started with 100k funded and 140k to collect. Now we have collected 70k. The most rational way to decide which part of the 70k goes down on the balance sheet and which part should be recognized as income is to prorate it. You should show that half has been collected which means that half of your income should be recognized now. We show it now because you have, in fact, collected revenue.

Question #5: For cash basis (tax return) purposes, when do we realize a loss? How do you show and what do you call the write off of uncollectible merchant cash advances?

Yoel Wagschal CPA: This is a very good question. There are some weird things going on in this industry because normally in a business you don’t exchange money to make money. On a cash basis tax return you would not see a receivable on the cash basis balance sheet. Concurrently, you would not see any bad debt.

Bad debt is usually not something that you see on a cash basis tax return. However, if you really look at the IRS regulations they do understand that even in a cash basis business there are bad debt expenses. Why wouldn’t you usually see bad debt expense? It is because you never recognize any income from the money you didn’t receive. Even with a cash basis tax payment, when a taxpayer lends money to a vendor (in a ‘normal business situation’) and that vendor doesn’t pay the taxpayer back, we know the taxpayer is entitled to take a bad debt expense.

In the Merchant Cash Advance situation, where we exchange money to make money, what could be more of a ‘normal business situation’? This is how your business works so if a merchant does not pay you back then you are entitled to a bad debt expense (of course, the actual realizable cash loss). This bad debt expense gets realized when the Merchant Cash Advance company is certain they are not going to get paid. In the rare situations where you have already written off a bad deal and the merchant does end up paying, you will need to reduce your bad debt expense for the following year or you can add it to your income for the following year.

As far as labeling, I believe the IRS wouldn’t care what you call it. I understand why you want to label it differently. The truth is that this comes only out of the fear that an amateur might look at it. A real trained knowledgeable professional will understand it. Bottom line is, it is perfect (although not normal) for a cash basis taxpayer to have a bad debt expense. But, you can see nothing here is the norm. So do we care for the amateur or for the expert?

Question #6: (This is for “syndicators” which we define here as entities who provide funds to MCA companies before those funds are sent to merchants). Should I do my books whenever I get a payment, week to week, or in one lump sum? From a GAAP or accounting perspective do we use immediate revenue recognition or the deferred method?

Yoel Wagschal CPA: If you want to simplify your bookkeeping I suggest after the fact accounting. Just be sure to maintain absolute consistency. At the end of the year your accountant should be able to take your information, adjust it to a proper trial balance, and create your year end reports. However, if you do not maintain the highest degree of accuracy and consistency then your accounting work will be much more time consuming and potentially flawed.

In my office we have all different types of clients. We have clients who want their books maintained on a live basis. This means we are responsible for taking the information off their MCA platforms and processing it in the accounting system.

We also have clients who want weekly reports. This is a more tempered measurement of the MCA activity. It paints the MCA picture in broader strokes while still maintaining absolute control where tax liability is concerned.

Finally we have clients who only want monthly or yearly reports. This almost completely separates the deal-to-deal MCA activity from the accounting activity. It leaves my accounting firm with the responsibility of tax liability and accounting while the MCA company does their own MCA deal tracking. Whichever approach works best for the individual companies is what you should choose.

In all of these cases there is one fundamental accounting rule and that is 100% consistency. I teach all of my clients to be very disciplined. We recommend having one bank account that is strictly used for funding and receiving money and a completely separate account for operations. For the larger clients we recommend they fund from one account and receive in another account. There is no problem shifting money between these accounts because when an accountant looks at your books it is very easy to follow your transactions.

After you have separated the accounts we can do the actual accounting work for you. However, as we are about to explain the basic journal entries for MCA accounting we caution you to remember this ‘Breaking Bad’ example. In the TV Show Breaking Bad the show’s star (Walter White) explains why he is irreplaceable. Someone else cannot simply step in and recreate his product. His argument is that he is a chemist with multiple advanced degrees as well as years of experience and research. He cannot simply impart all of the knowledge he has to someone in a matter of days. No one can match his intellect simply by watching his actions. His explanation is that a less experienced person would not be able to know if something was off. How would a less experienced person know if one of the ingredients was the wrong type? How would they know if the temperature was slightly off or the cooling phase took too long?

The same practical concept must be applied here, when you are doing the accounting for your MCA transactions. If there was an error in the journal entries, if a procedure was misunderstood and then applied over and over again, if a large transaction was classified incorrectly – how would you know? Only a highly skilled accountant with knowledge of the MCA industry will be able to look over your work and make sure that all of the procedures have been followed correctly. We are about to provide the most basic journal entries for MCA accounting. However we insist you use caution in implementing these entries. We stress that you should consult with a trained accountant who can understand the procedures and recognize mistakes.

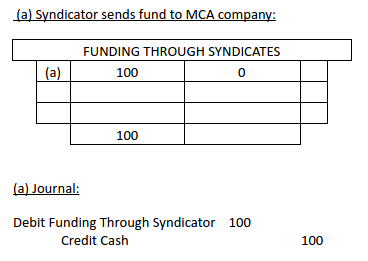

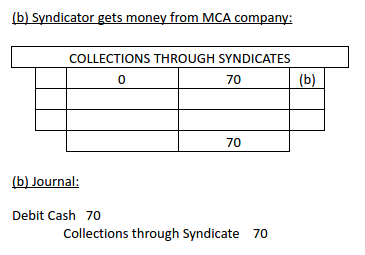

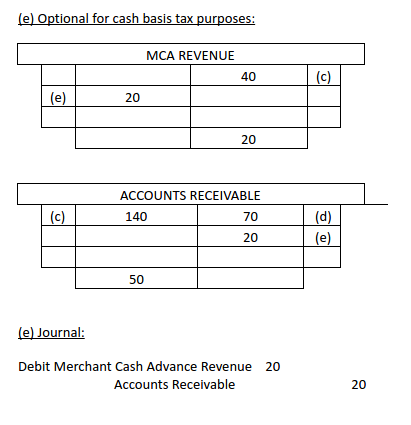

First, we start by looking at an entity who sends funds to an MCA company. As this is where the money trail starts, this is where we will start as well. When a syndicator sends funds to an MCA company they should set up a temporary ledger account. We usually call this “funded thru syndicates”. Every time they send money to the MCA company this entry will show a credit to cash and a debit to this temp account. It won’t have any meaning now but it will have a lot of meaning at the end of the year when they need to produce their financial statements. When this syndicator receives back their money they should debit cash and credit a different account. We usually call this different account ‘collections through syndicates’.

Now, the number of this type of transaction is going to depend entirely on how many deals the syndicator gets involved with and how often they receive cash back from the MCA company. Let’s say there are an accumulation of small transactions that happen over the year. Their outcome is going to be that their ‘funding through syndicate’ account is going to have a debit balance. For the sake of this example, we will make that debit balance 100k. Their ‘collections thru syndicate’ account is going to have a collective credit balance. For this example we will say the credit balance is 70k. As we said, these transactions will not have much meaning when you are processing them individually, but now they will show the bigger picture to your accountant (and hopefully to you!).

The ‘funded through syndicate’ account is at 100k because the syndicator provided the MCA company with 100k (which then went to merchants). Of course, they are not only getting 100k back. In this business the syndicators must make money on the funds they provide. For the sake of this example, the syndicator will look to get back 140k. Now you see that balance outstanding is 70k.

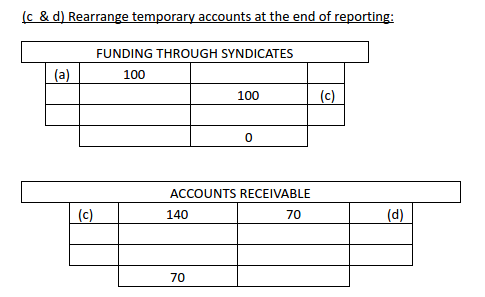

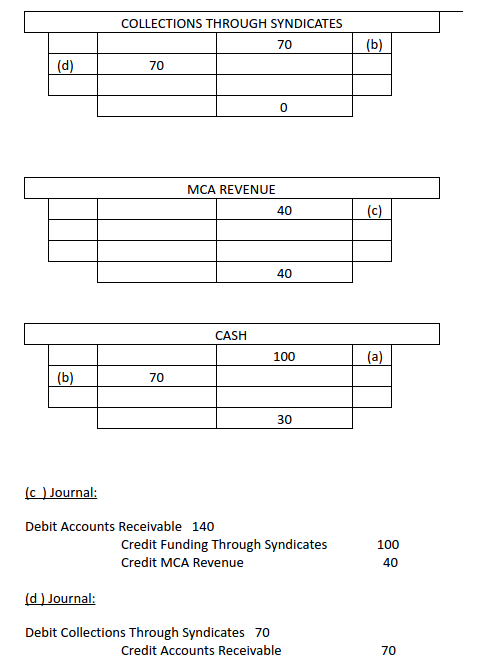

The MCA receivable has a debit balance of 70k, which is what they owe and their revenue is 40k. That’s the difference between the 140k and the 100k.

Now the temp accounts are down to zero. The next step looks at the 70k receivable. We know that 20k of it is uncollected revenue. Based on what we have before, which is used for cash basis purposes, I will add another journal entry crediting merchant cash receivable 20k. This will bring down my receivable to 50k which represents the principal portion of the 100k. This shows the syndicator gave the MCA company 100k and half of it is collected. Now we debit MCA revenue and that brings down the syndicator’s revenue from 40k to 20k for cash basis.

As far as GAAP is concerned we don’t have special guidance for this industry. The industry is very unique. We do have the principal of industry practices constraint. I have been very involved in this industry for years. I had a lot of talks with dozens of people all over the country. Investors, funders, creditors, ISO’s, professionals, etc, basically all walks of life connected to this industry. I do feel and believe that the way everyone wants and expects to see the reporting is the way I explained it. As far as MCA companies are concerned they do recognize revenue when your performance obligation has been completed; that is funding. Everything the funder does in the future is collecting their money. There is no performance that this merchant wants from the funder. As a matter of fact the merchant (customer) would be very happy if the funder ceases his activity which is strictly collections. In all other cases where we see revenue being deferred the company still has an obligation to perform. For example, prepaid phone service or insurance both provide services after the bill has been paid. Regarding uncertainty, I feel that this is no different than uncollected receivables. This is why we have a bad debt provision. The bad debt is based on historical performance of each one’s experience. As a side note, I do see a pretty consistent ratio across the line. Uncertainty leads you to the subject of derivatives. Derivatives are uncertain and unknown. Everything is underlined by a future event in the market value of a later date. This is different, as I explained. For instance, a grocery store’s AR is not certain in regards to how much they are going to collect. That is why we always work with fair estimates.

Question #7: How does this journal entry affect my tax returns? Won’t the IRS want it explained? Do they need to see it on each merchant cash advance or all in one entry?

Yoel Wagschal CPA: The IRS is not in the habit of asking to see your internal accounting unless they are performing an audit. They want to see the final result which is your tax return. This is the final report you provide to them. If you are audited then you have to substantiate your numbers and they ask for your ledger. If this happens they will see one journal entry (the one we just discussed) and they will ask how you got to those numbers. Here you will need to provide all the necessary backup, which you will undoubtedly have in your excel sheets, platforms, and correspondence. My accounting firm keeps a detailed record of all financial information we receive. When we do the final journal entry we keep and file all of the source documents that were used to calculate those numbers. We suggest you do the same not simply because the IRS may ask for them but because your investors may ask, your partners may ask, or you may need to present this information in order to diversify your business portfolio. The most important reason to have accurate and reliable financial information is, of course, that it will be used by the business owner – YOU!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

It’s Time to End the Phrase ‘Marketplace Lending’ – Because it’s Insane

May 19, 2016

Nobody knows what “marketplace lending” means, including me. That’s kind of ironic considering AltFinanceDaily is for the most part a publication dedicated to it. In fact, the cover of the March/April issue featured a big yellow robot sporting a name tag that actually said, “Hello, my name is Marketplace Lending.” Even the letter I penned that introduced readers to the issue used the phrase not once, not twice, but FIVE TIMES.

The FDIC basically defined it as encompassing all types of financing that include the practice of pairing borrowers over an online platform. Eager to be hip to the industry’s newest lingo, I got on board, and unfortunately perpetuated something that makes almost no sense.

Many companies operating under the marketplace lending umbrella don’t even know that they’ve been lumped into it. It’s become a media buzzword, something to help the simple masses understand so that they will click on a news headline without worrying if the content will only be geared toward the financially savvy.

Imagine shopping for a loan at a supermarket, but ONLINE, and voilà, marketplace lending!

But there are virtually no online platforms that work like that. The simplest explanation to describe a dizzyingly diverse industry is the most incorrect one. Lenders set rates and terms, borrowers don’t choose exactly what they want from a virtual shelf and put them in an imaginary shopping cart. There are however, portals where prospective borrowers can review different offers from different lenders in an Expedia-like environment, but this is really just Online Lead Aggregation 2.0, not a new-age system of lending.

Of course, some adopters of the phrase will point out that the marketplace was supposed to refer to the investor side, not the borrower side. It is investors that can shop for loans or notes that they want to invest in. Indeed, on platforms like Lending Club and Prosper, investors can select individual notes with terms befitting their desires and place them in an online shopping cart for purchase. Behold, the marketplace!

But what if you didn’t deal with retail investors hand-selecting $25 notes at a time? Notably, some online platforms that sell their loans to institutions in giant pools by the thousands or millions believe that such activity constitutes a marketplace because somebody is buying what they’re selling. And so long as somebody is selling something to somebody else at some point, the whole thing might as well be a marketplace. And even if it’s not, referring to it as such anyway will garner more press, attract more investors, and boost valuations.

I mean, would a site like TechCrunch be more likely to write about a FinTech Marketplace Lender or a generic financial company that sold a batch of loans to a bank?

I can tell you firsthand that if a press release submitted to us used the term “marketplace lender” instead of “finance company,” we’d at least check it out, or at least we used to. These days, we are becoming numb to its overuse.

Peer-to-Peer lending was an awesome term and it was descriptive too. Everybody could understand it. But then those platforms had to go and start selling their loans to Wall Street instead of peers and come up with something else to still sound trendy, techie, and disruptive. There’s nothing trendy of course about selling loans to financial institutions. It is a quintessential boring business activity of Wall Street. It is the opposite of disruptive, except in the events where all the loans go bad and the entire economy collapses like in 2008.

Peer-to-Peer lending was an awesome term and it was descriptive too. Everybody could understand it. But then those platforms had to go and start selling their loans to Wall Street instead of peers and come up with something else to still sound trendy, techie, and disruptive. There’s nothing trendy of course about selling loans to financial institutions. It is a quintessential boring business activity of Wall Street. It is the opposite of disruptive, except in the events where all the loans go bad and the entire economy collapses like in 2008.

The FDIC specifically said that marketplace lending can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, real estate loans, merchant cash advance, medical patient financing, and small business loans. This wildly diverse list, which even includes a non-loan product, will obviously have platforms in every category where people or businesses can get paired with a source of funds via the Internet. It’s 2016. It’d be weird if you couldn’t search for financing online. You can do everything else on the Internet. Just because a search happens online shouldn’t mean that the resulting options should be thrown together in some special broad category of lending and then be judged according to what all the other sectors do.

None of this is said to diminish the technological feats that many platforms have achieved. People and businesses can access capital in much faster and more convenient ways than ever before. Their growth and success is America’s economic gain. Jobs have been created and borrowing costs reduced. Hooray, perhaps, for marketplace lending.

The problem is merely the characterization that anyone lending to anyone else these days must also be a marketplace. That makes no sense.

Who will be the first to stop the madness?

Lending Club Faces Another Subpoena, This Time It’s NY Regulators

May 18, 2016

Adding to its list of woes, New York financial regulators have subpoenaed the lender on its interest rates charged to borrowers in New York. CNBC reports that this matter is unrelated to Laplanche’s exit.

From its CEO resigning on May 9th to being slapped with a Justice department notice the same week, the lender’s reputation has been through a lot of trauma. Its stock tanked more than 8 percent on Tuesday and opened under $4 on Wednesday.

And to add to the heap of bad news, the company evaluated its staffing needs and cancelled its 10-week summer internship program.

Lending Club received a Department of Justice grand jury subpoena on May 9th, according to the company’s quarterly earnings report, the same day that the resignation of their iconic CEO was announced. Grand juries are selected to decide if a criminal indictment should be brought against a party. The timing of the subpoena is suspicious because it leads one to suppose that a federal prosecutor had listened in on the May 9th earnings call, read news reports, decided there might be criminal activity, summoned jurors and issued a subpoena all within hours of the original announcement.

The WSJ, which did a great job reporting the details of the events leading up to Laplanche’s ouster, was not able to pin down the smoking gun that “convinced directors that more drastic action was needed,” just that the board had been “presented with evidence” that Laplanche knew many details of the $22 million loan sale.

A highly likely possibility (and this is just my theory) is that someone at Jefferies, the investment bank that Lending Club fudged the numbers on and ultimately bought $22 million worth of loans back from, tipped off federal authorities as to what took place with the loan sale.

Contrary to what people think about Wall Street, many bankers are scared to death about having knowledge of something that could lead to investors being harmed. Someone at Jefferies (and again just my theory) very well could have been so bothered by what Lending Club did, that they made sure the authorities knew what transpired. In doing so, they would probably have been viewed positively for blowing the whistle on bad behavior.

Cue a prosecutor’s interest, a grand jury, and likely a subpoena to individuals who would’ve had direct knowledge of the transaction. In my opinion, nothing would convince a board of directors more to give their famous CEO 24 hours to resign or be fired than having acquired knowledge of a grand jury investigation.

Cue a prosecutor’s interest, a grand jury, and likely a subpoena to individuals who would’ve had direct knowledge of the transaction. In my opinion, nothing would convince a board of directors more to give their famous CEO 24 hours to resign or be fired than having acquired knowledge of a grand jury investigation.

According to the WSJ, by Thursday, May 5th, Laplanche was removed as board chairman. On May 6th, he resigned. Over the weekend, he emailed friends from a new personal address, and on May 9th it was announced that he had resigned. That same day, Lending Club (the company), received a grand jury subpoena, of what I theorize was probably part of an investigation that was already in progress.

We may never know the full truth, but a seemingly innocent chain of events has clearly spiraled out of control to the point where over the course of a single week, Lending Club’s business model is seemingly coming undone. If nobody wants to buy loans or notes from their marketplace, then they are essentially out of business.

The dearth of interest in buying the loans they originate given the recent news has forced the company to disclose that it might actually have to use its own money to fund loans. No buyers, no business. So what else can they do? For one, they admit that they may need to reduce the volume of loans they originate, and that in doing so, it would likely have material adverse impact on their business.

These consequences have been predicted for years. What happens when investors just don’t want to buy the loans? How could a company where 90% of the income comes from loan origination fees provide continuous value to shareholders in an environment where there are no longer buyers?

Notably, veteran banker Todd Baker has been one of the most vocal on this issue. Six months ago, he publicly challenged SoFi CEO Mike Cagney about the viability of the marketplace model. Cagney had previously addressed Baker in an American Banker article by writing, “It is true that an MPL [Marketplace Lender] needs a buyer to originate loans — without one, the marketplace needs to raise rates until a buyer emerges. If there is no buyer, MPLs simply stop lending — they won’t start originating underwater loans.”

Stop lending?

Seemingly willing to undermine his own assertions, Cagney told the WSJ less than a year later a different story. “In normal environments, we wouldn’t have brought a deal into the market, but we have to lend. This is the problem with our space.” The environment of which he spoke then of course, was one where loan buyer interest was simply not as high as they would’ve liked, and thus it was becoming a “problem.”

Cagney’s reversal played right into Baker’s point, that a marketplace lender has to keep issuing loans to survive. When those loans don’t have organic buyers, at least in SoFi’s case, the weird idea of launching a hedge fund to potentially artificially keep up loan originations was proposed.

For Lending Club, their Plan B to keep things going is to simply buy their own loans if no buyers are available. Lending Club has a strong balance sheet and could potentially have success with this, for a time of course. The problem is that it would be taking on the credit risk of those loans as a result and put its retail note buyers at risk in the process.

Here’s why: When investors use the Lending Club platform, they are lending money to Lending Club and Lending Club is using that money to lend to borrowers. Investor yield might be tied to the performance of the notes they acquire but the credit risk is ultimately Lending Club itself. If Lending Club goes kaput, note holders would have a major problem, one that hasn’t really been a possibility until now because Lending Club hasn’t kept much risk on its balance sheet. That might soon change, according to their recent quarterly earnings report, where they say they might have to balance sheet some loans. Investors then wouldn’t really be participating in some disruptive peer-to-peer sharing economy revolution, but rather become very much like bondholders in an unregulated non-depository financial institution. And that smells horrifyingly risky. Throw in the fact that Lending Club is facing class action lawsuits, one of which alleges them to be a Racketeer Influenced Corrupt Organization. Does this sound like the kind of bond you want to invest in if you’re an unaccredited retail investor?

What Laplanche actually did or what a grand jury finds are unimportant in the grand scheme of what’s already been revealed. The only thing that matters is that when buyers dry up (whether for rational or irrational reasons), the entire system’s foundation shakes. The marketplace as it was supposed to be anyway, certainly can’t forever operate as a marketplace when it has shareholders who expect ever-increasing revenues and profits. According to Cagney’s original libertarian fantasy, nothing should theoretically be going on balance sheet. Lending Club should just be lending less, and if there are ultimately no buyers, the company should shut down until such a day that buyers return. One could only imagine that conversation with shareholders.

At the LendIt Conference last month, Renaud Laplanche joked with the crowd about cutting off the sleeves of his Lending Club jacket to make the Lending Club vest he sported on stage during his keynote speech. But was it just the sleeves that were missing? Speaking so confidently, Laplanche projected the authority of an emperor, perhaps one we’ve all been introduced to before.

“Was it really just the sleeves that have been cut away?” You may have thought to yourself for a split second. Or is it possible that the emperor of the marketplace, unbeknownst to the crowd, was simply wearing no clothes at all?

Business Loan Brokers and MCA ISOs Call it Quits

May 17, 2016

Hard times reported just a month ago are already turning into farewells

Hard times for those facilitating small business financing solutions are starting to cause a visible exodus from the space. In their wake, industry vendors have told AltFinanceDaily of unexpected credit card charge disputes for leads long past purchased or for ISO software previously paid for.

One failed ISO who lasted just 14 months aired it all out on an industry forum. “I do have to say the entire journey was not fun or lucrative. I lost $250,000 of my own money [and] could not broker a deal to save my life,” he wrote. From what he could also tell during his experience, is that nobody else around him was really making any money either.

He’s not alone in feeling this way. Another user just two months earlier started a thread with this title, “Does anyone really make money in merchant cash advance?” In it, he wrote, “The merchant cash advance industry sucks. I’ve been in this business for now 1 year after 20 years of sales experience and what I find is that this industry is the craziest thing I have ever seen.”

Some sales reps or ISO owners are simply venting frustrations and continuing on but others are writing real goodbye letters. A few days ago for example, one long-time MCA industry consultant wrote on LinkedIn that he was “done with merchant cash advance” and that he had finally moved on to something that made him happy, which from the looks of it, is a career in playing Poker full time.

Gil Zapata of Lendinero wrote to AltFinanceDaily in an email about what’s happening out there. “Lead generation is expensive,” he said. “Most people think that obtaining a new client is just cold calling. Wrong. There is a cultivation process.”

And part of it may be a misunderstanding of what the sales process is like, he insinuates. “Many people who have tried entering this industry think it’s the mortgage business,” he said. “It’s not.”

On forums, users often attribute some of the issues to “low grade professionals,” salespeople who would clearly benefit from more training. They’re part of the reason why an official training course is in the works and should be available some time this year.

“Good agents are not easy to find. Recruiting, hiring, and training is costly,” said Zapata.

And even then with the right salespeople, he added that “a lot of the internet leads are dead deals or not the best leads. Forming partnerships is not easy if you are looking to generate massive deal flow.”

Bright Spot

Unlike some who are throwing in the towel, Zapata is not going anywhere. Neither is another sales rep who contacted AltFinanceDaily off the record. Just 16 months in to the business, he’s reportedly funding more than $500,000/month just from cold calls and claims that he is not stacking any deals. He admittedly says that he eats at his desk and never leaves. Being an equity trader in a prior life is what helped him succeed at this, he said.

“Some ex-stock brokers who can pound the phones can do very good,” Zapata said. “We only lose deals to hot shot brokers in N.Y. who were aggressive stock brokers or sold some sort of financial product out of Wall Street.”

Indeed, just last week AltFinanceDaily learned that a sales rep from NYC that we had previously spoke with had just bought a red Lamborghini to celebrate his long and hard fought success. He’s not even 30-years-old yet and business is obviously going well.

Indeed, just last week AltFinanceDaily learned that a sales rep from NYC that we had previously spoke with had just bought a red Lamborghini to celebrate his long and hard fought success. He’s not even 30-years-old yet and business is obviously going well.

More than a year ago, I wrote that it had become much too late to get into this business if all you had was a couple thousand bucks in startup funds. At Transact 16, one attendee told me they believed that the absolute minimum needed to stand a chance in setting up your own ISO shop at this point was $250,000, purely because marketing costs have skyrocketed.

Might it really take the cost of a new Lamborghini to start an ISO these days? If true, that would ironically mean that as a generation of disenchanted brokers make their way for the exits, they may be passed by an entirely new generation of brokers riding exotic Italian cars on their way in.

Even so, they should heed caution from those that have spent years in the trenches. “This industry is not as easy as it seems,” Zapata wrote. “Cost can eat you up alive.”

GAME OVER: Is The Marketplace Lending Model Dead?

May 17, 2016

Lending Club received a Department of Justice grand jury subpoena on May 9th, according to the company’s quarterly earnings report, the same day that the resignation of their iconic CEO was announced. Grand juries are selected to decide if a criminal indictment should be brought against a party. The timing of the subpoena is suspicious because it leads one to suppose that a federal prosecutor had listened in on the May 9th earnings call, read news reports, decided there might be criminal activity, summoned jurors and issued a subpoena all within hours of the original announcement.

The WSJ, which did a great job reporting the details of the events leading up to Laplanche’s ouster, was not able to pin down the smoking gun that “convinced directors that more drastic action was needed,” just that the board had been “presented with evidence” that Laplanche knew many details of the $22 million loan sale.

A highly likely possibility (and this is just my theory) is that someone at Jefferies, the investment bank that Lending Club fudged the numbers on and ultimately bought $22 million worth of loans back from, tipped off federal authorities as to what took place with the loan sale.

Contrary to what people think about Wall Street, many bankers are scared to death about having knowledge of something that could lead to investors being harmed. Someone at Jefferies (and again just my theory) very well could have been so bothered by what Lending Club did, that they made sure the authorities knew what transpired. In doing so, they would probably have been viewed positively for blowing the whistle on bad behavior.

Cue a prosecutor’s interest, a grand jury, and likely a subpoena to individuals who would’ve had direct knowledge of the transaction. In my opinion, nothing would convince a board of directors more to give their famous CEO 24 hours to resign or be fired than having acquired knowledge of a grand jury investigation.

According to the WSJ, by Thursday, May 5th, Laplanche was removed as board chairman. On May 6th, he resigned. Over the weekend, he emailed friends from a new personal address, and on May 9th it was announced that he had resigned. That same day, Lending Club (the company), received a grand jury subpoena, of what I theorize was probably part of an investigation that was already in progress.

We may never know the full truth, but a seemingly innocent chain of events has clearly spiraled out of control to the point where over the course of a single week, Lending Club’s business model is seemingly coming undone. If nobody wants to buy loans or notes from their marketplace, then they are essentially out of business.

The dearth of interest in buying the loans they originate given the recent news has forced the company to disclose that it might actually have to use its own money to fund loans. No buyers, no business. So what else can they do? For one, they admit that they may need to reduce the volume of loans they originate, and that in doing so, it would likely have material adverse impact on their business.

These consequences have been predicted for years. What happens when investors just don’t want to buy the loans? How could a company where 90% of the income comes from loan origination fees provide continuous value to shareholders in an environment where there are no longer buyers?

Notably, veteran banker Todd Baker has been one of the most vocal on this issue. Six months ago, he publicly challenged SoFi CEO Mike Cagney about the viability of the marketplace model. Cagney had previously addressed Baker in an American Banker article by writing, “It is true that an MPL [Marketplace Lender] needs a buyer to originate loans — without one, the marketplace needs to raise rates until a buyer emerges. If there is no buyer, MPLs simply stop lending — they won’t start originating underwater loans.”

Stop lending?

Seemingly willing to undermine his own assertions, Cagney told the WSJ less than a year later a different story. “In normal environments, we wouldn’t have brought a deal into the market, but we have to lend. This is the problem with our space.” The environment of which he spoke then of course, was one where loan buyer interest was simply not as high as they would’ve liked, and thus it was becoming a “problem.”

Cagney’s reversal played right into Baker’s point, that a marketplace lender has to keep issuing loans to survive. When those loans don’t have organic buyers, at least in SoFi’s case, the weird idea of launching a hedge fund to potentially artificially keep up loan originations was proposed.

For Lending Club, their Plan B to keep things going is to simply buy their own loans if no buyers are available. Lending Club has a strong balance sheet and could potentially have success with this, for a time of course. The problem is that it would be taking on the credit risk of those loans as a result and put its retail note buyers at risk in the process.

Here’s why: When investors use the Lending Club platform, they are lending money to Lending Club and Lending Club is using that money to lend to borrowers. Investor yield might be tied to the performance of the notes they acquire but the credit risk is ultimately Lending Club itself. If Lending Club goes kaput, note holders would have a major problem, one that hasn’t really been a possibility until now because Lending Club hasn’t kept much risk on its balance sheet. That might soon change, according to their recent quarterly earnings report, where they say they might have to balance sheet some loans. Investors then wouldn’t really be participating in some disruptive peer-to-peer sharing economy revolution, but rather become very much like bondholders in an unregulated non-depository financial institution. And that smells horrifyingly risky. Throw in the fact that Lending Club is facing class action lawsuits, one of which alleges them to be a Racketeer Influenced Corrupt Organization. Does this sound like the kind of bond you want to invest in if you’re an unaccredited retail investor?

What Laplanche actually did or what a grand jury finds are unimportant in the grand scheme of what’s already been revealed. The only thing that matters is that when buyers dry up (whether for rational or irrational reasons), the entire system’s foundation shakes. The marketplace as it was supposed to be anyway, certainly can’t forever operate as a marketplace when it has shareholders who expect ever-increasing revenues and profits. According to Cagney’s original libertarian fantasy, nothing should theoretically be going on balance sheet. Lending Club should just be lending less, and if there are ultimately no buyers, the company should shut down until such a day that buyers return. One could only imagine that conversation with shareholders.

At the LendIt Conference last month, Renaud Laplanche joked with the crowd about cutting off the sleeves of his Lending Club jacket to make the Lending Club vest he sported on stage during his keynote speech. But was it just the sleeves that were missing? Speaking so confidently, Laplanche projected the authority of an emperor, perhaps one we’ve all been introduced to before.

“Was it really just the sleeves that have been cut away?” You may have thought to yourself for a split second. Or is it possible that the emperor of the marketplace, unbeknownst to the crowd, was simply wearing no clothes at all?

Expansion Capital Group Joins The $100 Million Club

May 13, 2016 Expansion Capital Group has officially lent its one hundred millionth dollar since inception. In an e-mail, the Sioux Falls, South Dakota-based lender said they’re proud of the small businesses they’ve helped along the way. And they’re helping them at increasing speed, records indicate. The company celebrated its $50 million milestone less than 9 months ago, which means they’re lending more than $50 million a year.

Expansion Capital Group has officially lent its one hundred millionth dollar since inception. In an e-mail, the Sioux Falls, South Dakota-based lender said they’re proud of the small businesses they’ve helped along the way. And they’re helping them at increasing speed, records indicate. The company celebrated its $50 million milestone less than 9 months ago, which means they’re lending more than $50 million a year.

In November, the company announced the closing of a $25 Million credit facility through Northlight Financial and Bastion Management to support their rapid growth.