Ford Credit and AutoFi Debut Platform for Faster, Smoother, Simpler Digital Vehicle Buying and Financing

January 24, 2017- New platform allows customers to purchase and finance a new vehicle via the dealer website; platform introduced at Ohio dealership and will roll out over time to more U.S. Ford and Lincoln dealerships

- Platform makes it fast and convenient to finance a new Ford or Lincoln at a time when many U.S. adults say they want to spend less time at dealerships, while still going to their dealer to “sign and drive”

- Ford Credit makes equity investment in AutoFi as Ford Credit continues pursuing technology to make the financing experience better

There’s a new way for customers to purchase or finance a new Ford vehicle in minutes – right from a dealership website from anywhere, on any device – through a new platform from Ford Motor Credit Company and financial technology company AutoFi.

There’s a new way for customers to purchase or finance a new Ford vehicle in minutes – right from a dealership website from anywhere, on any device – through a new platform from Ford Motor Credit Company and financial technology company AutoFi.

In addition, Ford Credit has made an investment in AutoFi as Ford Credit continues pursuing technological advances to make the financing experience better.

“By combining our fast and efficient credit-decision process with AutoFi’s online capability, we are making the customer experience faster, smoother and simpler,” said Lee Jelenic, Ford Credit director of mobility. “With its experience in used-vehicle online financing and well-developed platform, AutoFi makes it easier for us to adopt new technology quickly to meet evolving consumer expectations.”

The AutoFi platform can be used now at Ricart Ford in Groveport, Ohio, and will roll out over time to more Ford and Lincoln dealerships across the United States. The introduction comes as 83 percent of Americans say they would like to spend as little time at the dealership as possible when shopping for or buying a car, according to a new survey of more than 1,000 U.S. adults conducted online by Harris Poll on behalf of Ford Motor Company. Many of those same people, however, still want to touch and feel their new vehicle before signing on the dotted line. The new platform provides the best of both worlds.

Through the dealer website, customers have a transparent and seamless purchase and finance experience from anywhere on their mobile phone, tablet or computer. Once the online part of the transaction is complete, all customers need to do is sign the paperwork when they collect their new Ford.

Consumers may shop for a new Ford in the showroom or from anywhere via the Ricart Ford website. After selecting a vehicle, they can apply for credit and receive a decision, choose the financing terms that make sense for them, and then review and select optional vehicle protection products – completely online on their own time. Customers then can review a final summary of the financing terms and schedule time to complete the transaction and pick up the vehicle.

“AutoFi’s platform will help cut the time people spend arranging financing and improve the experience dealerships can deliver for their customers, no matter where they are in the car-buying journey,” said Kevin Singerman, CEO of San Francisco-based AutoFi. “We think this will be a game changer for both consumers and dealers, and we are thrilled to work with Ford Credit to make this happen.”

“Technology is transforming just about every type of financed consumer purchase, and this new digital capability will help make that change for automotive purchases and deliver great experiences,” said Rick Ricart, Sales and Marketing vice president at Ricart Ford. “We are excited to be the first Ford dealership in the pilot.”

# # #

About Ford Motor Credit Company

Ford Motor Credit Company is a leading automotive financial services company. It provides dealer and customer financing to support the sale of Ford Motor Company products around the world, including through Lincoln Automotive Financial Services in the United States, Canada and China. Ford Credit is a subsidiary of Ford established in 1959. For more information, visit www.fordcredit.com or www.lincolnafs.com.

About AutoFi

AutoFi is a technology company transforming the way cars are bought and sold. The company’s platform allows auto dealers to sell vehicles completely online by connecting buyers with lenders in a fast, easy and transparent process. AutoFi’s team includes industry leaders from enterprise software, finance, automobile and consumer sectors who previously worked at companies including Lending Club, PayPal, and SunGard. AutoFi’s investors include Ford Motor Credit Company, Crosslink Capital, Lerer Hippeau Ventures, Laconia Capital Group, Basset Investment Group, Eniac Ventures, 500 Startups and Silicon Valley Bank. For more information, visit www.autofi.com.

About the Survey

This study was conducted online within the United States by Harris Poll on behalf of Ford Motor Company between November 28 and December 5, 2016, among a nationally representative sample of 1,217 adults ages 18 years and older. This online survey is not based on a probability sample and therefore no estimate of theoretical sampling error can be calculated.

Contacts

Ford Credit

Margaret Mellott

313.322.5393

mmellott@ford.com

or

AutoFi

Justin Hamilton

202.630.5426

Media@autofi.com

Confessions of a Fintech Chief Data Scientist

January 8, 2017 My name is Justin Dickerson. For most of 2016, I was the Chief Data Scientist at Snap Advances (Snap), a funding company of merchant cash advances based in Salt Lake City, Utah. I can’t discuss my awesome work at Snap for obvious reasons. And fortunately, I don’t need to in order to make the key points I want to convey through this article. That’s because I’ve also been a senior level data scientist at two other companies, and I’m also a well-regarded statistician who holds one of the most prestigious credentials offered by the American Statistical Association.

My name is Justin Dickerson. For most of 2016, I was the Chief Data Scientist at Snap Advances (Snap), a funding company of merchant cash advances based in Salt Lake City, Utah. I can’t discuss my awesome work at Snap for obvious reasons. And fortunately, I don’t need to in order to make the key points I want to convey through this article. That’s because I’ve also been a senior level data scientist at two other companies, and I’m also a well-regarded statistician who holds one of the most prestigious credentials offered by the American Statistical Association.

One discovery over the past year prompted me to start collecting my thoughts for this article. I was looking at the financial performance of On Deck Capital (the largest company in the alternative fintech industry which is also publicly traded) through the first nine months of 2016 relative to the same period in 2015. Gross revenue increased more than $22 million while net income for the same period fell nearly $50 million. I’m not an accountant, but that doesn’t sound good to me. And let’s face it, this fact doesn’t surprise anyone in our industry, especially given what’s happening at CAN Capital. But one interesting and overlooked fact is worth considering. According to my Linkedin search, there were between 30 and 40 data scientists (all levels) working for On Deck Capital during the same time period in which they lost $50 million. So, not only does On Deck Capital lose a lot of money, it appears they need a lot of intellectual horsepower to figure out how to do so.

And here we are today. We’re looking at an industry full of companies trying to navigate the abyss of hyper-aggressive originators and spiraling default rates. If you’re a Chief Data Scientist for one of these companies, you’re undoubtedly feeling the heat from your management team. The problem is simple. How do you grow your business (or even stabilize it) in an environment where you have to take too many uncomfortable risks? We’ll ignore the fact this question has plagued much larger industries for many years (e.g., trying to compete against Wal Mart in the retail space). Boards of Directors in alternative fintech have short memories and believe this is a unique problem to their industry and era. As a result, data scientists are at a premium as they’re seen as key players in how to resolve this crisis and steer their companies to safe harbors. Well, here is my opinion. They’re dead wrong, and here is why.

Data Scientists Are Tactical, not Strategic

This statement may end up being the most controversial thing said in the data science industry this year. But let me make my case. Of those 30-40 data scientists working for On Deck Capital, more than 80% of them have a Master’s degree in a field of study synonymous with data science. Specifically, many of them attended Columbia University’s Master’s degree program in Operations Research. The four required courses for that degree are: Optimization Models and Methods, Introduction to Probability and Statistics, Stochastic Models, and Simulation. From there, students can choose from one of six concentrations (all but one of which are targeted toward quantitative methods). Further, students selected for this program already have highly refined quantitative skills as demonstrated by the pre-requisite courses for admission (e.g., multivariate calculus, linear algebra, etc.). So, in essence, the program takes really smart quantitative people (quants) and makes them even smarter quants, while sprinkling in 6 elective courses which may or may not provide an opportunity to learn something about the “real” world of business.

Make no mistake, the students attracted to programs such as these generally aren’t the professionals you send to meet with investors and pitch them on new strategic directions for a company. They are the professionals who sit in cubicles and spend their days writing code. They are experts in programming languages such as R, Python, Java, Scala, and many others. Ironically, they are enslaved to similar rules which govern the same supervised machine learning algorithms they create each day. They aren’t allowed to “get out of the box” and see the “forest through the trees.” If I’m portraying them as a bit robotic, that’s intentional on my part.

I don’t want to leave the impression data scientists can’t think for themselves. Specifically, those who earn a PhD are known to have such skills and are often praised for their abilities to rise above the technical chains of their existence and offer strategic direction to an organization. But they are few and far between in the data science factory found deep in the bowels of companies like On Deck Capital. Instead, more and more alternative fintech companies seek out the same “cookie-cutter” data scientist who can check off the same boxes on the hiring list. This means the data scientist role is relegated to a part of the company lacking diversity of thought, creativity, and the organizational respect needed to save a company from itself.

The Law of Diminishing Returns

One of the most intelligent questions asked of me within the alternative fintech industry was, “do we really have enough data to justify so many data scientists?” As a Chief Data Scientist, you always want to answer that question with an emphatic, “YES!” Even better, you may tell your management team you need even more data scientists to make a “real and lasting contribution to the company.” After all, the existence of your team depends on it. But when you’re away from the management team and thinking about the structure of your department, the honest Chief Data Scientist knows the company is at risk of experiencing the law of diminishing returns.

All of us can recognize the law of diminishing returns from our freshman year Economics course. In short, it’s the concept of achieving less than a one to one relationship between an additional unit of input relative to the resulting measured output. For example, the reduction in default rate for a financial product is hardly ever proportional to the number of data scientists employed by the company to predict default rates. In fact, I would argue once you have more than two or three data scientists, even the largest organizations would have a difficult time justifying the payroll investment based on proportional gains in default rate management.

So, why do companies like On Deck Capital have so many data scientists? I believe it’s more akin to the comfort food we all like to eat in the winter. There is hardly anything as satisfying as my grandmother’s homemade chili during a cold Utah night. And the more of it I get, the warmer I feel! The problem is the chill of winter eventually fades and the light of day shone on financial statements eventually begs the question of whether we’ve simply eaten too much.

Make no mistake, NO organization needs endless amounts of data scientists to be successful. In fact, I would argue two or three excellent data scientists armed with superior data science/machine learning platform technology such as those offered by IBM, Microsoft, or DataRobot is more than enough to guide an organization to success. The key when thinking about staffing a data science department is to think in terms of credibility. If I have three data scientists each armed with PhD training, 15 years of industry experience, and the tools (such as a great machine learning platform) to do the mundane parts of data science usually done by legions of Master’s degree data scientists, am I more credible in the organization than I am with 30 quants who all grew up in an economy where nothing bad ever happened to financial institutions? If you want your data scientists to help your organization, you’ve got to be willing to let them into the board room and present digestible recommendations for action. So the question becomes, do I have a team that is credible enough to meet such a standard?

The Supremacy of Domain Expertise

I learned a lot during my time as a Chief Data Scientist. Since leaving Snap, I’ve established two companies. The first is Crossfold Analytics. This is my data science consulting company. We only serve the fintech industry and we spend most of our time building real-time machine learning prediction services for small to mid-sized fintech companies. And I think we’re darn good at it! The second company is Crossfold Capital. This is my independent sales organization (ISO) focusing on merchant cash advance, business loan, and factoring products. It was when I established Crossfold Capital that I learned the most valuable lesson of all about data science in alternative fintech. Nothing will ever replace the experience of working in the trenches of the business (what I call “domain” expertise). In alternative fintech, this is generally working within the trenches of a sales organization. If I could go back in time and start over as Chief Data Scientist at Snap, I would start my job by underwriting files and selling merchant cash advances for a month. Absolutely nothing I learned in math, statistics, or any quantitative subject can replace what I’ve learned running my own ISO in just the past two months. I wish every alternative fintech company would adopt a training program for data scientists that allowed them to spend their first month in the field calling on clients and working with potential customers. If you understand the business, you can bring immeasurable value to your company by blending that understanding with your technical skills as a data scientist. I truly believe such an approach could take the power of a data scientist and magnify it three-fold. Otherwise, you end up having a rogue department of quants that people in the trenches of the business either don’t understand or don’t trust.

My Recommendation to Alternative Fintech Companies

Based on what I’ve learned as an alternative fintech data science professional, I would make three recommendations to all companies in our industry. First, hire diverse talent. It’s imperative a data scientist knows enough about coding to be effective at building predictive models. But I would trade extensive coding expertise for a data scientist who also had a Bachelor’s or Master’s degree in business administration. We don’t need an army of robots in data science. We need gifted thinkers who also happen to have advanced technical skills. Second, don’t “over-eat” even though it can be cold outside. More data scientists aren’t going to solve your problems. In fact, hiring the same type of data scientist only encourages “group-think” which can actually be very detrimental to your organization. Focus on building a credible data science department, not a massive data science department. Finally, put your smartest people in the dirt of the business. Have them spend a week underwriting files. Then send them to sell your products with one of your ISO managers. Don’t treat your data scientists as fragile figurines. As a good friend of mine from Texas says about his gun collection, “they may be worth a lot, but they’re so dirty from hunting you wouldn’t know it!”

I hope my confessions help your organization navigate both fair seas and choppy water.

My Marketplace Lending 2017 Projections

January 8, 2017 LendIt co-founder Peter Renton has projected that there won’t be any new industry IPOs this year. While I don’t know if I’d say he’s wrong (a year is a long time), one thing that has changed since 2014 is a shift away from the “tech” label. When OnDeck went public, they positioned themselves as a technology company. Today, they more closely identify themselves as a non-bank commercial lender. Lending Club too was a “tech company.” Now they might be more appropriately characterized as an online consumer lender, especially since their competitors are traditional financial institutions like Discover Bank and Goldman Sachs. So the public markets in 2017 may not be ready for a tech company that can lend but they may be ready for a lending company that has tech. The difference is real.

LendIt co-founder Peter Renton has projected that there won’t be any new industry IPOs this year. While I don’t know if I’d say he’s wrong (a year is a long time), one thing that has changed since 2014 is a shift away from the “tech” label. When OnDeck went public, they positioned themselves as a technology company. Today, they more closely identify themselves as a non-bank commercial lender. Lending Club too was a “tech company.” Now they might be more appropriately characterized as an online consumer lender, especially since their competitors are traditional financial institutions like Discover Bank and Goldman Sachs. So the public markets in 2017 may not be ready for a tech company that can lend but they may be ready for a lending company that has tech. The difference is real.

On regulation, while a Trump presidency may mean that federal regulatory threats will subside, my projection is that the judiciary system will instead play a prominent role in 2017. Whether it’s state courts or federal courts, expect the rules of engagement in marketplace lending or merchant cash advance to become more clear than ever before.

I think it would be easy to predict consolidation in 2017, so more than that, I believe some companies will just wind down and others who arrived too late to the game will just move on to something else. That’s not necessarily a pessimistic outlook since this will give the more serious players a chance to flex their muscles and continue strong growth. This is a natural cycle in any industry that experiences a rapid growth phase.

There will be at least one black swan event. We don’t know what we don’t know.

Lastly, if you want to come up with your own predictions you should attend the 2017 LendIt Conference this March in NYC as it’s the best opportunity to take the temperature and size up the future. I have been to the last three annual LendIt USA conferences and in my opinion each has set the tone for the rest of the year.

You can get 15% off the registration price with Promo Code: AltFinanceDaily17USA.

SmartBiz Loans Ranked Number One Provider of Traditional SBA 7(a) Loans Under $350,000

December 5, 2016SAN FRANCISCO, CA – December 5, 2016 – SmartBiz Loans, the first SBA marketplace and bank-enabling technology platform, has ranked as the number one provider of non-Express, SBA 7(a) loans under $350,000 for the 2016 government fiscal year. SmartBiz also ranked number five among providers of under $350,000 traditional SBA 7(a) and Express 7(a) loans combined.

“SmartBiz’s success in this year’s SBA 7(a) ranking demonstrates how technology can support banks in meeting the needs of small businesses,” said Evan Singer, CEO of SmartBiz Loans. “SmartBiz is committed to creating the leading marketplace for both banks and small business owners, by matching small business owners with the bank best suited to their needs and enabling a higher percentage of SBA loans to be approved.”

SmartBiz generated $200 million in funded SBA 7(a) loans through its bank lending partners, which helped them earn the top spot. The data used is based on SBA lending data released in November, reflecting its 2016 fiscal year which ended on Sept. 30. Wells Fargo Bank, which was ranked just below SmartBiz, generated $155 million in funded non-Express SBA 7(a) loans under $350,000. This is the first time a technology platform and marketplace has achieved the number one position in SBA’s ranking of 7(a) loans.

“Small businesses are the driving force of the economy,” said Ann Marie Mehlum, retired Associate Administrator, Office of Capital Access, U.S. Small Business Administration. “By supporting them, the SBA and lending partners like SmartBiz are investing in the economy as a whole.”

SmartBiz is revolutionizing SBA lending. Its marketplace helps increase approval rates by automatically directing businesses to the right lender, while its advanced software streamlines the SBA loan application, underwriting and origination process. In this way, SmartBiz fills a critical gap in the small business loan market and enables small businesses nationwide to grow without settling for the sky-high rates of alternative online lenders or undergoing the typically slow and tedious traditional bank process.

About SmartBiz Loans

SmartBiz Loans is a unique combination of an online SBA loan marketplace and a bank enabling technology platform. The company’s online software provides SBA preferred lenders customized and automated origination, underwriting and documentation, making approval and funding fast and easy. Sophisticated algorithmic sorting in the SmartBiz marketplace also enables higher approval rates for small businesses because the right applications are automatically directed to the right bank. SmartBiz is based in San Francisco and was founded in 2009 by a team of experienced financial services entrepreneurs with backing from leading venture capital firms including Investor Growth Capital, Venrock, First Round Capital, Baseline Ventures, and SoftTech VC. Learn more at www.smartbizloans.com.

The CAN Capital Shakeup Is A Sign of the Times

November 30, 2016Update 11/30 7:30 pm: CAN says they are still open for business and still providing access to capital for current customers and renewal business. They are not actively seeking new business at this time, but will evaluate it as it comes in.

Part II of the industry’s season finale has begun. On Tuesday afternoon, CAN Capital confirmed that CEO Dan DeMeo had been put on a leave of absence. The chief risk officer and chief financial officer have also reportedly stepped down. Parris Sanz, the company’s chief legal officer, is now running the company, a CAN spokesperson said. His new title, acting head (which is how their statement referred to him), is perhaps a subtle clue that the company did not plan these moves far in advance. And it’s the phrasing that’s used to describe the departure of these executives that’s worth raising an eyebrow. A leave of absence? A curious fate indeed.

Part II of the industry’s season finale has begun. On Tuesday afternoon, CAN Capital confirmed that CEO Dan DeMeo had been put on a leave of absence. The chief risk officer and chief financial officer have also reportedly stepped down. Parris Sanz, the company’s chief legal officer, is now running the company, a CAN spokesperson said. His new title, acting head (which is how their statement referred to him), is perhaps a subtle clue that the company did not plan these moves far in advance. And it’s the phrasing that’s used to describe the departure of these executives that’s worth raising an eyebrow. A leave of absence? A curious fate indeed.

In an exclusive interview AltFinanceDaily conducted with DeMeo last year, he said of CAN at the time, “it’s a self-sustaining business. We’re not forced to approach the capital market to cover our burn rate. We’re cash-flow positive.”

But more recently, there’s a different tone. A spokesperson for CAN said that the company had “self-identified that some assets were not performing as expected and that there was a need for process improvements in collections.” The sudden decapitation of the company’s top officers seems a harsh consequence for this apparent underperformance, especially given that CAN has long been on the short-list as a potential IPO candidate. DeMeo himself had been with the company since 2010, having started originally as the CFO and rising to the CEO position in 2013.

While CAN Capital is a private company, they are notable in that they have originated more than $6 billion in funding to small businesses since 1998 and secured a $650 million credit facility led by Wells Fargo just last year.

Some of CAN’s ISOs report being told that originations have been put on hold until January. A source with close knowledge of the company however, said that’s not correct. The Financial Times reported though that CAN had paused new business until the end of the year and would only be servicing current customers. And they might indeed need time to upgrade their systems since American Banker cited an unnamed source that said “problems arose when CAN Capital used old systems, which were not designed to require daily repayments, to collect money owed by term loan borrowers.”

Some outsiders are not surprised by what’s going. Alex Gemici, the chief revenue officer of World Business Lenders (WBL), said that it’s an indicator that uncollateralized lending is not the panacea everyone thought it was. “What we’ve been saying all along is right there on AltFinanceDaily,” Gemici said, while directing me to the prediction they made a year ago that appears right on this website. At a December 2015 event at the Waldorf Astoria, WBL CEO Doug Naidus told a crowd comprised mostly of his company’s employees that he believed the bubble was about to burst. He doubled down on that prophecy in an interview four months ago in which he chided companies for having forsaken sound underwriting.

Is he right? In the last six months, the CEOs of Lending Club, Prosper and CAN Capital have all stepped down. Avant shed a lot of its staff. Dealstruck, Circleback Lending and Windset Capital have stopped funding. Confidence in the business side of alternative finance has also started to slip on a measurable basis before the election even happened.

“I believe companies are experiencing higher than normal losses due to a serious lack of proper underwriting practices, policies, and procedures,” said Andrew Hernandez, a managing partner at Central Diligence Group, a company that specializes in risk analysis who wasn’t commenting about any lender specifically. “As I say to people not familiar with the space, ‘putting the money out is the easy side of the business; getting it back is what proves to be the most difficult.'”

But CAN has not specifically fingered underwriting practices as the reason for their management shakeup, instead leaning towards it being a lapse in their process as the company grew. “It became clear that our business has grown and evolved faster than some of our internal processes,” they said in their statement.

The only alternative business lender funding more annually is OnDeck, a company that has garnered its fair share of criticism over its lackluster financial performance. Their stock is currently down a whopping 77% from the IPO price, but they have put on a good face for the industry they lead. The familiarity of their famous CEO and the decade in business under their belt arguably even has a calming effect on the tumultuous world of financial technology startups.

OnDeck too though, has been referenced in the context of bursting bubbles. Less than two years ago, RapidAdvance chairman Jeremy Brown voiced concern that the industry was heading into unsustainable territory, even going so far as to call out OnDeck by name. “When I see some of the business practices, offers, terms and other aspects of our business today, I am worried,” he wrote. “I am worried because I believe that 2008 has been too quickly forgotten, and very few, other than those of us that were on the front lines on the funding side at that time, appreciate what happened to outstanding portfolios at that time when average duration was 6 months and no deals were written over 8 months.”

For risk experts like Hernandez of Central Diligence Group, he thinks the newness of everything has been part of the problem. “I believe [funding companies] have faced a big hurdle in acquiring talent,” he said while adding that funding companies can be forced to hire underwriters with no prior knowledge of the product just to keep up with the growth.

While still very little is known about what exactly happened at CAN Capital, most people that AltFinanceDaily spoke with were shocked that anything could happen there at all. “It’s insane,” said the chief executive of another competitor who wished to remain anonymous. “This is CAN we’re talking about.”

A sign of the times?

Q3 2016: Confidence in the Small Business Financing Industry’s Success Down Slightly

November 29, 2016Confidence in the industry’s continued success was down among small business financing CEOs in the third quarter, according to the latest survey conducted by Bryant Park Capital and AltFinanceDaily. At 75.8%, it’s the lowest level recorded since surveying began late last year.

Respondents were not asked the reasoning for their confidence score, but the sentiment may have been influenced by what seemed like an impending Clinton presidency at the time and the 4 more years of regulatory pressure on financial services that would’ve continued as a result. The survey was conducted before the election. Also, the correction taking place in the consumer space with companies like Prosper and Avant have allowed a general feeling of pessimism to waft through the alternative financing universe.

Still, at 75.8%, which is still well into positive territory, the mood is probably best described as cautiously optimistic. The euphoria in Q1 at 91.7%, preceded the resignation of Lending Club’s founder and CEO, which symbolically burst alternative lending’s bubble.

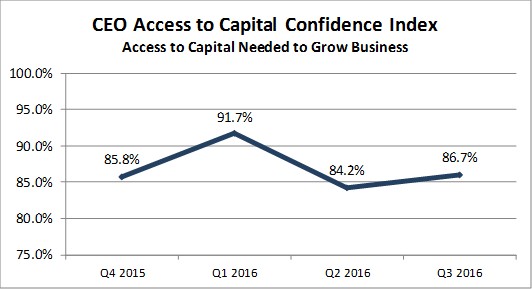

Curiously, industry CEOs were slightly more confident in their ability to access capital needed to grow their business. Respondents were not asked what their capital source options were or the respective costs, but it signals that there are still plenty of investors interested in the space.

Bryant Park Capital and AltFinanceDaily also produce a comprehensive full-year industry report, available to anyone for $495. To purchase the 2015 report, you can contact me at sean@debanked.com

It’s Here: Artificial Intelligence Changes MCA Broker’s Business, Improves Bank Underwriting and Debt Collection

November 22, 2016In this age of man versus the machine, the case for artificial intelligence and machine learning does not need many vociferous advocates.

Some predict that revenues from fintech startups using AI and predictive models is set to jump by 960 percent or to $17 billion by 2021. We might be closer to that number than we think, considering 140+ AI startups raised a total of $958M in funding in Q3’16, alone.

While healthcare, cybersecurity and advertising are frontiers of AI innovation, the growth and momentum of big data in finance (spurred by online lending) is fast bringing fintech to the forefront. In lending, specifically, data has become the new currency. It’s not so much that lenders didn’t use data for decision making earlier, but the data available then, wasn’t as rich or as extensive. A loan approval decision that just required a decent FICO score and assessment of character has expanded to include data points like a business’ social media presence, reviews, and owners’ background history.

Today, artificial intelligence in fintech has grown to tackle cybersecurity threats, act as a personal assistant, track credit scores and perform sentiment analysis to predict risk — making automated underwriting just the tip of the iceberg for what artificial intelligence and machine learning can do for the financial services industry. AltFinanceDaily spoke to three fintech upstarts that have taken AI beyond underwriting.

AI Assist

When Roman Vinfield started his ISO, Assure Funding in early 2015 with 16 openers, five chasers and three closers, little did he know that a business intelligence software would replace 85 percent of his staff for the same productivity. He stumbled onto Conversica, a AI-powered virtual sales assistant and was convinced to give it a try.

When Roman Vinfield started his ISO, Assure Funding in early 2015 with 16 openers, five chasers and three closers, little did he know that a business intelligence software would replace 85 percent of his staff for the same productivity. He stumbled onto Conversica, a AI-powered virtual sales assistant and was convinced to give it a try.

“I hadn’t heard anything like an artificial-intelligence sales assistant,” said Vinfield. “The results we got within a month of using it were unbelievable.” Within the first month, Vinfield made $35,000 in revenues by spending just $4,000 and eventually reduced his staff of 24 to 4 people. He was so sold on its potential for the merchant cash advance industry that after prolonged negotiations, he secured the rights to be the exclusive reseller of the software, and called it AI Assist. The software is now used by leading MCA companies like Yellowstone, Bizbloom and GRP Funding.

While Conversica’s clientele includes auto and tech giants like Oracle, Fiat, Chrysler and IBM, for the financial services industry, it’s marketed and sold to MCA and lending companies through AI Assist. It integrates easily with CRM software like Salesforce and creates a virtual sales assistant avatar that tracks old leads and reestablishes engagement. In the lead generation race, where a 3-5 percent response rate could be considered good, the response rate for Conversica has been 38 percent.

Designed to be akin to a human sales assistant, Conversica’s technology can determine a lead’s interest based on the response and set up a conversation with the sales department to follow up. “Your Conversica virtual assistant is an extremely consistent, personable and tireless worker. She doesn’t get sick and never needs a break. She never gets discouraged, and she improves with each engagement,” says the AI Assist website.

True Accord

True Accord

Personal chat assistants for money management and sales is one of the popular modes of AI implementation in fintech, given it’s scalability in lending for functions like debt collection. One company that does this, is True Accord. True Accord, similar to AI Assist uses automation software to schedule and send messages to customers by the company’s “Automated Staff”

The San Francisco-based company was founded by Ohad Samet who has over 11 years of machine learning experience in finance. The idea came to Samet while he was working as a chief risk officer at payments and e-commerce company Klarna, underwriting loans worth $2 billion. “While working at Klarna, I realized how big a piece debt collection is and I did not like the way it was done,” said Samet. “I needed machine learning to change it.”

Samet founded True Accord in 2013 to develop a debt collection AI assistant and today the company works with leading banks, credit card companies and food delivery services and has collected over half a billion dollars. It establishes targeted communication with the customer less frequently than traditional collection agencies and allows customers to pay their dues over mobile, which accounts for 35 percent of collections for the company.

“We humans don’t want to accept it but the reality is that, when it comes to scale, machines make better decisions than humans,” said Samet. “Machines are consistent, they are not tired, not angry, don’t fight with the significant other and all of this makes for better accuracy, better cost structure and better returns of scale.” While this might be true, building an efficient, compatible and compliant model is harder than it might seem.

James.Finance

Since AI tools do not come in a one-size-fits-all package, its application can be as varied as the range of companies that use it. Building an AI framework that aligns with a company’s targets while being compliant to regulatory mandates can be an uphill task.

Since AI tools do not come in a one-size-fits-all package, its application can be as varied as the range of companies that use it. Building an AI framework that aligns with a company’s targets while being compliant to regulatory mandates can be an uphill task.

Recognizing this opportunity, James.Finance, a Portugal-based startup is using artificial intelligence to help financial institutions like banks build their own credit scoring models. Founder and CEO Pedro Fonseca, describes James as a “narrow AI” for a specific purpose of guiding risk officers to build machine learning models that follow regulatory compliance.

The startup works with consulting agencies or partners to reach out to banks. It offers a trial run of the software, which it calls a ‘jumpstart,’ where a risk officer is provided with James’ technology and in 24 hours, he or she will have to beat it with their in-house AI software.

“And we are consistently able to beat the models,” said Fonseca. The company won the startup pitch at Money 20/20 in Copenhagen earlier this year after receiving an uproarious response in Europe. Fonseca wants to divert his attention to the US’s fragmented banking market, which is dotted with smaller banks and credit unions. “The US is a perfect target for us. We are looking to work with local consultancies that know the problems of a bank intimately.”

As these entrepreneurs vouch for it, the current state of AI use in fintech is just the tip of the iceberg. And anything man can do, machines can do faster and better, right?

Prosper Files 10Q, Revenues and Originations Shrink

November 17, 2016

The slight delay with Prosper’s 10-Q filing is over. The company originated $311.8 million in loans in Q3 versus $445 million in the previous quarter. Revenues were $24 million, down from $28 million in Q2.

The filing delay was said to have been attributed to a recent arbitration decision. That decision and financial impact were disclosed in their report. “On November 17, 2016, Prosper and Colchis [one of their earlier loan buyers] entered into a Settlement and Release Agreement, pursuant to which Colchis has agreed to terminate the Colchis Agreement and waive all rights conferred under such agreement in exchange for a $9 million cash payment by Prosper and equity. Prosper expects to make the $9 million cash payment in the fourth quarter of 2016.”

$9 million is a lot for Prosper who reported only $31.8 million in cash on their balance sheet.

The company has run up a $70 million loss on just $108 million in revenues so far this year, compared to a $17 million loss on $140 million in revenues for the first 9 months of 2015.

Revenues in Q3 year-over-year are down by nearly 60% while originations are down by more than 70%.

Earlier this week, Prosper’s CEO, Aaron Vermut, and executive chairman, Stephan Vermut, both stepped down from their posts.