Stacking Lawsuit Could Go to Trial

October 18, 2017 A lawsuit between RapidAdvance and Pearl Capital that has been making its way through the Maryland state court system for two years may be heading to trial.

A lawsuit between RapidAdvance and Pearl Capital that has been making its way through the Maryland state court system for two years may be heading to trial.

In this case, plaintiff Small Business Financial Solutions, LLC (SBFS AKA RapidAdvance) alleged that Pearl Beta Funding, LLC (AKA Pearl Capital) interfered with a loan agreement it had with a merchant when Pearl “stacked” financial obligations to Pearl on top of the obligations the customer owed to SBFS. Ultimately the merchant defaulted and SBFS wants to hold Pearl responsible for the damages it incurred.

Pearl originally moved to dismiss the suit but was unsuccessful. Later, Pearl filed a motion for summary judgment. On September 29th, that motion was denied, with the judge opining that issues of fact remained that were best left for a jury.

Unless Pearl appeals the decision or the parties settle, the case will go to a jury.

A representative for Pearl Capital declined to comment on the decision, citing ongoing litigation.

Patrick Siegfried, Assistant General Counsel for RapidAdvance, opted to tell AltFinanceDaily the following:

“The court’s decision from many months ago to reject Pearl’s motion to dismiss and its more recent decision to reject the motion for summary judgment and permit this case to go to trial confirms the anti-stacking position RapidAdvance has consistently taken. The court’s rulings make it clear that when a funding company funds a merchant knowing that doing so is a breach of the customer’s agreement with another funder and the stacker’s funding is a substantial cause of the merchant defaulting with the other funder, its actions constitute tortious interference. As a result, the company that stacked can be held liable for the losses the original funder incurs. While the outcome at trial is impossible to predict as the court will need [to] decide whether there are sufficient facts to satisfy each element, RapidAdvance is pleased that its legal reasoning on stacking has been confirmed in a written opinion and that we now have the roadmap for pursuing others that tortiously interfere with our contracts by stacking.”

Of note, is that RapidAdvance brought this case in The Circuit Court for Montgomery County, Maryland. Few other players in the industry may be able to designate Maryland as the proper venue. The standards for tortious interference may not be the same in other states. There are many circumstances in the case not discussed in this synopsis. Consult an attorney before drawing any conclusions. YOU CAN DOWNLOAD THE FULL DECISION HERE.

The case is Small Business Financial Solutions, LLC v. Pearl Beta Funding, LLC Case No. 411478-V in the Circuit Court for Montgomery County, Maryland.

Lead Generators Facing Rougher Road

October 13, 2017 Lead generators for alternative funders are facing stronger headwinds these days. The business has gotten tougher for a whole host of reasons. A pullback in alternative lending necessitates fewer leads. On top of that, funders, ISOs and brokers have gotten pickier about the types of leads they’ll accept. What’s more, stricter application of the Telephone Consumer Protection Act (TCPA) is hampering lead generators’ ability to solicit business owners. As a result, some lead generators have faded away, while others have been developing additional business lines or are broadening their reach to other areas within financial services to buoy earnings.

Lead generators for alternative funders are facing stronger headwinds these days. The business has gotten tougher for a whole host of reasons. A pullback in alternative lending necessitates fewer leads. On top of that, funders, ISOs and brokers have gotten pickier about the types of leads they’ll accept. What’s more, stricter application of the Telephone Consumer Protection Act (TCPA) is hampering lead generators’ ability to solicit business owners. As a result, some lead generators have faded away, while others have been developing additional business lines or are broadening their reach to other areas within financial services to buoy earnings.

“I don’t see any growth in the space for the next six months, or maybe a year,” says Michael O’Hare, chief executive of Blindbid, a lead generation company in Colorado Springs, Colorado. “It’s really unclear right now what’s going to happen, but we’ll see.”

The alternative funding industry has been in somewhat of a funk since spring 2016 when Lending Club grabbed headlines with a scandal that spooked the industry and also took out several senior managers, including the company’s then-CEO.

It was the first time in the industry’s relatively short history that people realized “it wasn’t all puppy dogs and ice cream,” says Justin Benton, a partner at Lenders Marketing in Santa Monica, Calif., a lead generator in the alternative funding space.

Since that time, there’s been a lot of movement in the market, including companies that are consolidating or exiting the business, pumping the brakes or making shifts in product lines, Benton says. These developments have all had a big impact on the sheer number of clients that are looking for leads, he says.

Late last year, for instance, CAN Capital Inc. stopped funding for several months, though it’s back in business as of early July. This summer, Bizfi, one of the stalwarts of the alternative financing space, began giving pink slips to staff and in August the company sold the servicing rights to its $250 million loan portfolio to rival Credibly.

There aren’t as many start-up ISOs or companies entering the alternative funding space—meaning more leads for existing funders—which, of course, is a boon for them.

“There are still roughly 75,000 business owners every week who meet the criteria for an [MCA]. Now instead of there being 5,000 options in the space, there are 2,000, so those 2,000 are gobbling it all up,” Benton says.

At the same time, however, TCPA regulations have gotten more stringent, making it dangerous to solicit businesses, says O’Hare of Blindbid. “Any phone call you make, you can get sued,” he says.

At the same time, however, TCPA regulations have gotten more stringent, making it dangerous to solicit businesses, says O’Hare of Blindbid. “Any phone call you make, you can get sued,” he says.

Large funding companies generally take TCPA very seriously—especially if they’ve gotten hit with violations, O’Hare says. Smaller funders and brokers, however, aren’t always as familiar with the restrictions; they think it’s only an issue if you’re calling consumers, as opposed to calling businesses, but that’s not the case. “A lot of businesses today are using their cell phone as a main business line and also for personal use. If you call a cell phone that’s on the DNC [Do Not Call Registry], you can potentially get sued.”

Last year, he had a situation where a plaintiff pretended to be an interested business. When he passed along the referral, the plaintiff’s attorney claimed TCPA violations and ultimately sued the funder. The funder balked, and it created numerous issues for his company.

His company now tries to educate funders about how to protect themselves from TCPA litigation. He sends out emails to funders with information about TCPA and provides contact information of attorneys who are well-versed in TCPA rules. He also provides funders with risk mitigation tactics and shares his list of known TCPA litigators so funders won’t accidentally call them. He also provides direction to clients that receive a demand letter or complaint on how to respond and offers a list of TCPA defense attorneys, if they need.

“We’ve become almost extreme in how we try to avoid problems related to TCPA,” O’Hare says.

To be sure, some of the changes lead generators are experiencing are indicative of a maturing industry.

A few years ago, lead generators could be less selective who they approached initially because the concept of alternative funding was so new to merchants, says Bob Squiers, chief executive of Meridian Leads, a lead generator in Deerfield Beach, Fla. Now, however, the cat is out of the bag, and, with business owners getting multiple calls a day, it’s harder to get their attention, he says.

“They know, they’ve heard, they’ve been pitched. There’s not too many unturned business owners. It’s about getting them at the right time.”

As a result, lead generation today requires more data to discern the good leads from the bad. Instead of going after half a million restaurants, lead generators are targeting the 20 percent that data suggests are the most viable funding candidates. “It’s more of a sniper approach than a shotgun approach,” Squiers says.

Rob Buchanan, senior sales executive at Infogroup in Papillion, Nebraska, who focuses on lead-generation for the fintech space, notes that within the past 18 months or so, clients have been going after “low-hanging fruit” when it comes to leads. They are looking for leads where business owners are actively looking for financing as opposed to relying primarily on UCC data. They are still using UCC data, but to a lesser extent than they were in the past, he says.

Rob Buchanan, senior sales executive at Infogroup in Papillion, Nebraska, who focuses on lead-generation for the fintech space, notes that within the past 18 months or so, clients have been going after “low-hanging fruit” when it comes to leads. They are looking for leads where business owners are actively looking for financing as opposed to relying primarily on UCC data. They are still using UCC data, but to a lesser extent than they were in the past, he says.

Not only do clients want very targeted and specific types of companies—but they are changing their minds more frequently about the types of businesses they’re looking for, says Matthew Martin, managing director and principal at Silver Bullet Marketing, a lead-generating and marketing company in Danbury, Conn. They might ask for businesses of a particular size or credit quality—they are even seeking to exclude businesses within certain zip codes. They are also more amenable to leads from industries they deemed too risky a few years ago.

“I have clients that are constantly changing the parameters of what they want,” Martin says.

The problem is that once you start narrowing the leads of possible merchants that can be funded, lead costs go up and many funders don’t want to pay for that, says O’Hare of Blindbid. “The glory days when everything was wide open and you could generate leads really cheaply are pretty much gone.”

Meanwhile, as some lead generators have faded into the sunset, others are forging ahead in search of new opportunities.

Benton of Lenders Marketing, for instance, says his company has started to focus its efforts in other areas of lending, including SBA, new business, mortgage, commercial, residential, auto and student loans.

Digital marketing is another area experiencing increased demand. Business owners that need money tend to use Google to find funding companies. Infogroup’s digital marketing leads these businesses directly to funders, ISOs and brokers, Buchanan says.

“More and more funders, brokers and ISOs are leaning toward doing digital marketing,” he says.

ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit

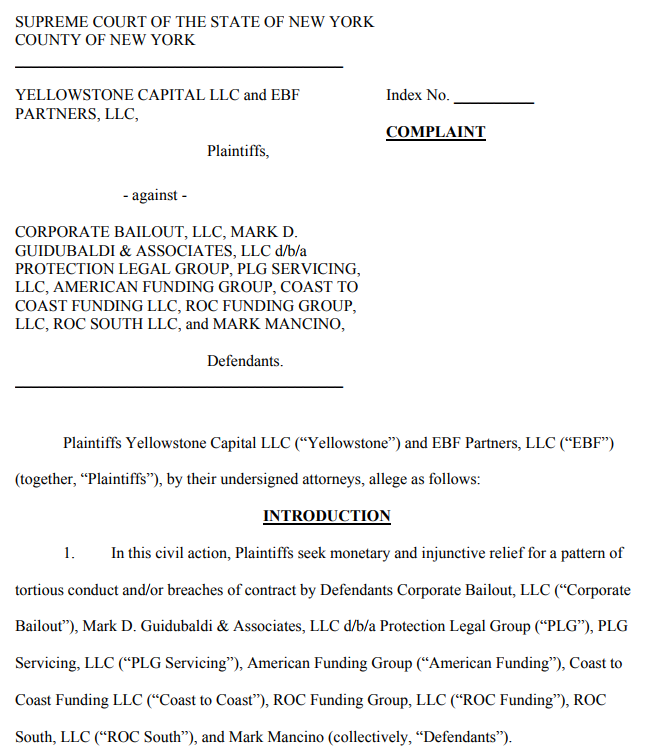

September 28, 2017 ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

The debt settlement companies “mislead the merchants as to the services they will perform and the cost to the merchant, and they also conceal their relationships with the ISO Defendants and the fact that they or their affiliates are introducing these same merchants to merchant cash advance providers like Plaintiffs only to later induce those merchants to breach their agreements with their cash advance providers,” the complaint states.

Among the named defendants are:

- Corporate Bailout, LLC

- Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group

- PLG Servicing LLC

- American Funding Group

- Coast to Coast Funding, LLC

- ROC South, LLC

- Mark Mancino

Several defendants are already best known for running an office “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street,’” according to a salacious story that graced the back cover of the New York Post last month.

One paragraph of the complaint summarizes the allegedly collaborative scheme like this:

American Funding, Coast to Coast, […] (the “ISO Defendants”) are independent sales organizations (“ISOs”), companies that ostensibly support the merchant cash advance industry by brokering merchant agreements for companies like Plaintiffs. The ISO Defendants are anything but the proverbial “honest brokers.” As alleged below, they have partnered with companies that purport to offer debt relief services to merchants who have agreements with merchant cash advance companies like Plaintiffs. In practice, for these companies, “debt relief” is a code word for deceiving merchants to breach their existing agreements with Plaintiffs and to instead pay fees to these debt relief entities. In short, they scam merchants into believing that they can save them money when, in fact, they leave these merchants in financial shambles, while causing Plaintiffs to suffer millions of dollars in losses and future los[t] profits.

“’DEBT RELIEF’ IS A CODE WORD FOR DECEIVING MERCHANTS TO BREACH THEIR EXISTING AGREEMENTS”

Central to the plaintiffs’ claim is that they have ISO agreements with the defendants and that the defendants’ conduct is a breach of those agreements. The three causes of action alleged are tortious interference with contract, conversion, and breach of contract. Plaintiffs claim that 100 merchants with more than $3 million in outstanding balances are in breach of their contracts because of the defendants’ conduct.

The complaint was prepared and filed by attorneys at Proskauer, a 142-year old law firm founded in New York City.

Debt Relief Under Fire

The small business debt relief industry has been marred by scandal in recent years. In an unrelated criminal matter being handled in the Western District of New York, the owner of Corporate Restructure Inc. (no ties to Corporate Bailout) is currently residing in the Niagara County Jail awaiting trial on charges of conspiracy to commit mail fraud, wire fraud, bank fraud and money laundering for failing to deliver the debt relief services it charged for. In that case, United States vs. Sergiy Bezrukov, Bezrukov advertised that he could reduce a merchant’s short term debt by up to 75%. He is facing up to 30 years in prison. He was also previously a merchant cash advance ISO.

Two other MCA funding companies, Pearl Gamma Funding and Pearl Beta Funding, filed a lawsuit last November against another debt relief company that calls itself Creditors Relief. The complaint in that case also alleges tortious interference with contract and is still pending.

Meanwhile, a lawsuit filed in May by famous TCPA litigant Craig Cunningham against Corporate Bailout and Mark D Guidubaldi & Associates LLC went unanswered, according to court records. Cunningham, who alleged violations of telemarketing laws, filed for a default judgment against Corporate Bailout on September 12th.

Taking Advantage

Both Yellowstone Capital and Everest would not comment on the lawsuit they filed, citing pending litigation. Sources close to them, however, contend that both companies take matters that involve merchants being taken advantage of very seriously.

“When our own ISOs work directly in concert with companies that induce merchants to breach our contracts, that’s a problem,” said one source who did not wish to be named and was speaking generally about the recent introduction of debt relief service companies to the industry. “They’re taking advantage of businesses that can’t afford to be taken advantage of.”

An email sent by AltFinanceDaily to Mark Mancino early Thursday afternoon, an individually-named defendant alleged to be affiliated with the other defendants, has not yet received a response. This story may be updated if a reply is received.

A COPY OF THE COMPLAINT CAN BE VIEWED HERE.

Square Wants to Become a Bank

September 6, 2017 Square is expected to apply for an Industrial Loan Company (ILC) bank charter this week, according to American Banker and other sources. Like SoFi, who is busy trying to do the same thing, their attempt will also face competitive resistance.

Square is expected to apply for an Industrial Loan Company (ILC) bank charter this week, according to American Banker and other sources. Like SoFi, who is busy trying to do the same thing, their attempt will also face competitive resistance.

In June, Richard Hunt, president and CEO of the Consumer Bankers Association (CBA), told AltFinanceDaily that in the case of SoFi, “The whole world is evolving, fintech is evolving. This was inevitable one way or another.” It is therefore not entirely surprising that Square is following SoFi. Others may wait to see how the regulatory debate plays out before putting in applications of their own, however.

“No one envisioned when they wrote the ILC charter that we would have fintech companies that finance mortgages and student loans from private equity capital and not deposits. It’s a new world. Like with all rules and regulations, federal regulators should periodically review longstanding policy,” Hunt said.

Several people from the banking industry argue that the ILC charter route is a loophole and that if fintech companies exploit it and screw up, they could put the entire banking system at risk.

Christopher Cole, executive vice president and senior regulatory counsel at the Independent Community Bankers of America (ICBA), previously said, “We have been fighting the ILC charter for over a decade. When Walmart tried to apply for an ILC charter in 2006 we objected at that point. And that resistance was part of the reason why they never got a charter.”

On August 25th, Congresswoman Maxine Waters requested that a hearing be held on ILC charters to weigh all the concerns before acting on new ILC applications.

Until then, just because Square wants to become a bank, doesn’t mean they will succeed in doing so.

You’re Under Arrest: Funder Takes Extreme Measures to Counter Data Theft

September 4, 2017

An employee of Yellowstone Capital was arrested last month, according to a source who witnessed the events. At the company’s behest, local police entered Yellowstone’s Jersey City office and handcuffed a female employee who was believed to be engaged in the theft and misappropriation of financial data.

A spokesperson for Yellowstone would not comment on the events nor release the name of the accused. AltFinanceDaily nevertheless obtained a photo of the individual being escorted out by police. We’ve blurred out her face to protect her identity. Several of those present, who spoke on the condition of anonymity, said that she had been employed by the company for several years.

When asked more generally about the risks of data leakage in the industry, Yellowstone Capital CEO Isaac Stern said that his company is operating on the edge of hyper vigilance. “Yellowstone is investing tons of time, money, and effort to prevent data theft,” Stern said. “We are doing everything in our power, everything, to address it, and we have even enlisted the assistance of an outside security firm.”

The incident does not stand alone. Last year, a man on Long Island pled guilty to attempted criminal possession of computer related material after being implicated in a merchant cash advance backdooring scheme.

Backdooring is industry jargon for when a broker submits a potential deal to a funder and that file ultimately leaks out to third parties whom the broker did not authorize to handle the information. Often times brokers will point their fingers at the funder for mismanaging data they suspect is escaping out the back door. Such accusations can be detrimental to a funder’s reputation not only with the broker community but also with customers they advance funds to. That’s why some funders are taking data security to new levels.

Greenbox Capital, for example, a funder in Miami, FL told AltFinanceDaily back in March that their company designed proprietary software to monitor the actions of all users on their system, which allows them to know who clicked on what when, and for how long. They also developed algorithms to detect suspicious behavior and their security team receives an alert whenever it gets triggered. Greenbox had initially conducted a 90-day probe and discovered that two employees were stealing data. They don’t want that to ever repeat itself.

Using a cell phone to take pictures of confidential data may not help rogue employees evade detection, according to several funders who have said there are methodologies to spot this behavior but declined to explain what they are. And the risk of getting caught may not merely be termination, as evidenced by arrests that have taken place thus far. These funders say there have been other arrests over the last few years but that the companies did not want to draw attention to them.

Indeed, of the two backdooring-related arrests AltFinanceDaily has reported on now, neither would officially confirm them.

“We take ISO information extremely serious,” Yellowstone’s Stern explained, lamenting that the value of deal data can inevitably foster rogue behavior, which they are constantly monitoring for.

Put another way, the personal information of a single performing client could be worth as much as $10,000 or more if it gets into the wrong hands. That’s because it could be used to offer that client a loan, advance or other service. The profit could come in the form of a commission, interest, RTR, a closing fee, or even something more nefarious like stealing their identity.

“We know about the pressure people face to illegally transmit data,” Stern said. “They think we don’t know, but we know the industry. Ultimately we will catch you.”

Why BFS Capital’s Glazer Is Passing the Torch

August 22, 2017

Marc Glazer co-founded BFS Capital in the early 2000s and has remained at the helm all this time – until now. Glazer has passed the torch over to Michael Marrache, effective last week. He isn’t going too far, as the former chief executive will remain chairman of the board working alongside Marrache on the next chapter for the MCA and small business lending company. Meanwhile the executive pair points to a future not only where there is sustainability but where there is growth.

“We’ve obviously grown the company year after year over the last 15 years, and as with every other type of business and industry there were ebbs and flows. Over the last couple of years with a significant amount of challenges going on, we as a company decided we want to continue to grow but we want to grow in a way that benefits the company from a profitability standpoint as well as serves our customers,” said Glazer.

In April 2017, BFS Capital surpassed $1.5 billion in financings since inception. The company expects to fund more than $300 million in new financings in this calendar year.

“We’ll increase our reliance on algorithmic solutions, transparency in the ISO and customer experience and we will increase the number of financing solutions. Culture is significant for us and we will continue to build on the legacy Marc created,” said Marrache.

Marrache takes the reigns at a time when the industry is at a crossroads that will leave some alt lenders in the dust while other rise to the occasion.

“The stories that were challenging in 2016 look good in 2017,” said Marrache, pointing to OnDeck’s forthcoming profitability, Kabbage’s lofty valuation, CAN Capital’s return to funding, PayPal’s acquisition of Swift Financial and Prosper looking good.

“We think alternative and non-bank lending are in a good place. And yes, some of the folks that are no longer operating in this space were overextended or may have exhibited irrational behavior for pricing or customer acquisition costs. We think what we’re witnessing is the normal lifecycle of the industry. There were lots of participants earlier. Now to participate the industry must show a bit more control and sophistication. If you execute well, the tomorrows will be better than 2016,” said Marrache.

And according to Glazer, because of the changes in the business environment over the last couple of years, it’s going to require a different skillset to take BFS Capital to the next level.

“There are clear differences between starting a company, growing a company and becoming a billion-dollar small business financing platform. We’ve needed to evolve at each stage and now again with Michael’s leadership,” he said.

For Glazer, Marrache was almost always the succession plan.

“To be fair, hiring Michael four years ago, maybe succession planning was in the back of my mind somewhat. But as our relationship developed and as he was COO for three-plus years and then president, it became apparent that Michael’s skill set, passion, desire and how he looked at culture were all similar to myself. Let’s grow, but let’s watch our numbers. Make sure we treat people fairly. And for the businesses we are financing — provide thoughtful capital to help them versus creating problems for them,” said Glazer.

More Funding

BFS Capital’s business model is comprised both of MCAs and small business loans. Alternative funding company CAN Capital does both MCAs and loans and had to pause lending until recently. For BFS, however, it’s all systems go. And that means unequivocally continuing to fund small businesses.

“Absolutely, yes. And there’s no quizzicality in mind. I would say we are going to continue funding small businesses and fund more of them this year than we did last year. And we will fund even more the year after. So absolutely,” Marrache said.

BFS Capital sells through both ISOs and directly to merchants, the former of which is where most originations derive. “There are a number of solutions we are putting together to benefit that network,” said Marrache, adding he doesn’t believe algorithmic solutions will replace underwriters.

“We have a strong legacy of customer underwriting. We believe lower level transactions can be significantly more automated. Above a certain level and certain amounts of origination, we think algorithms and data solutions at that point are a facilitator, not a replacement of our underwriting,” Marrache said.

The Legacy

There was a time when BFS Capital’s growth plans included debuting in the public markets. Those plans have since been sidelined amid a chilly investor reception for alternative lender stocks.

“We spent a lot of effort in our filing,” said Glazer. “But at the end of the day, the market for the space had softened. Going forward I think it’s really going to be a question of what the markets look like and what makes sense for our company. We will evaluate that as the situation warrants.”

IPO or not, it appears Glazer’s legacy is still being written.

“I co-founded the company 15-plus years ago. Before finance and accounting, at heart, I’m an entrepreneur. That’s what I do, what I enjoy. I love starting companies, having the vision and creating things,” he said.

As chairman of the board and a major stakeholder, Glazer will continue to be active in BFS Capital.

Tech Banks: Will Fintech Dethrone Traditional Banking?

August 20, 2017On Halloween, 2014, a largely unknown, Boston-based financial institution, First Trade Union Bank, embraced high-technology, went paperless, and officially adopted a new name: Radius Bank.

In reinventing itself, Radius did more than dump its dowdy moniker. It shuttered five of its six branches, re-staffed its operations with a tech-savvy team, instituted “anytime/anywhere” banking services, and offered customers free access to cash via a nationwide ATM network. And it teamed up with a fistful of financial technology companies to offer an impressive array of online lending and investment products.

In reinventing itself, Radius did more than dump its dowdy moniker. It shuttered five of its six branches, re-staffed its operations with a tech-savvy team, instituted “anytime/anywhere” banking services, and offered customers free access to cash via a nationwide ATM network. And it teamed up with a fistful of financial technology companies to offer an impressive array of online lending and investment products.

Today, the bank’s management boasts that, using their personal mobile phones, some 2,700 people per week are opening up checking accounts, funneling $3 million in consumer deposits into the bank’s virtual vault. That’s a stark contrast from a decade ago when the financial institution was being rocked by the financial crisis and “we couldn’t get anybody to walk into our branches,” says Radius’s chief executive, Mike Butler.

“We tried to leave that old bank behind,” he says. “We’re a virtual retail bank now, an efficiently run organization that offers high levels of customer service and Amazon-like solutions.”

Radius Bank is not alone. At a moment when there is much discussion — and hand-wringing — over the future of seemingly outmoded, highly regulated community banks, a coterie of small but nimble banks is exploiting technology and punching above its weight. Almost overnight, this cohort is combining the skill and hard-won experience of veteran bankers with the lightning-fast, extraordinary power afforded by the Internet and technological advances. As a result, these small and modest-sized institutions are redefining how banking is done.

In addition to Radius Bank, independent banks winning recognition for their bold, innovative – and profitable — exploitation of technology, include: Live Oak Bank in Wilmington, N.C., which adroitly parlays technology to become the No. 2 lender to business and agricultural borrowers backed by the U.S. Small Business Administration; Darien Rowayton Bank in Darien, Conn., which is making a name for itself with coast-to-coast, online refinancing of student loans; and Cross River Bank in Fort Lee, N.J., which does back-end work for a passel of fintech marketplace lenders.

Interestingly, there’s not much overlap. Each of the banks goes its own way. But what all the banks have in common is that each has struck out on its own, each hitting upon a technological formula for success, each experiencing superior growth.

“These are companies that understand the value of a bank charter,” says Charles Wendel, president of Financial Institutions Consulting in Miami. “They have to work under the watchful eyes of state and federal regulators. But their cost of funds is low and they can offer more attractive rates. Because they’re less likely (than nonbank fintechs) to disappear, run out of money, or get sold,” the bank expert adds, “they also have the image of stability with customers.”

These modest-sized banks are emerging as not only pacesetters for the banking industry. Along with making common cause with the fintechs — which had promised to disrupt the banking industry – they’re even beating the fintechs at their own game.

“Classically, community banks have looked to technology partners to provide technological innovation,” says Cary Whaley, first vice-president for payment and technology policy at the Independent Community Bankers of America, a Washington, D.C.-based trade group representing a broad swath of the country’s 5,800 Main Street banks. “They still do. You’re seeing more partnerships. But now you also see community banks building innovative products and services outside of that relationship. You see forward-thinking banks developing their own technology to support big ideas like marketplace lending, distributed ledger technology, and emerging payments technology.”

With its extraordinary skill at exploiting technology, Live Oak Bank – which trades on the Nasdaq and is the only public company encountered in the cohort — has become a Wall Street darling. “While several banks have adopted an online-only model, and nearly all banks are shifting more and more delivery through online channels, Live Oak was built from the ground up as a technology-based bank,” Aaron Deer, a San Francisco-based research analyst at Sandler O’Neill Partners, wrote in a recent investment note.

Driving the success of Live Oak, which operates out of a single branch in the North Carolina seacoast town and has only been in business for a decade, is the explosive growth in its SBA lending, the bank’s “core strategy,” Deer notes. Last year, Live Oak lent out $709.5 million in SBA loans in increments of up to $5 million, the federal agency reports, making it the country’s No. 2 SBA lender. It trailed only megabank Wells Fargo Bank, the third largest bank in the U.S. with $1.5 trillion in assets, which made $838.93 million in SBA-backed loans last year.

As its SBA lending has taken off, Live Oak, which qualifies as a “preferred lender” with the federal agency, boasts assets that have nearly tripled to $1.4 billion in 2016, up from $567 million two years earlier. Those are flabbergastingly fantastic growth numbers. But just as incongruously — by nipping at the heels of Wells Fargo — Live Oak has been challenging a bank more than a thousand times its asset size for dominance in SBA lending.

And, interestingly, the bank is able to book those outsized amounts of SBA loans while lending to only 15 industries out of 1,100 approved by the government agency, slightly more than 1% of the universe. That’s up from 13 industries in 2015, and Live Oak is adding two to four additional industries yearly for its SBA loan portfolio, Deer reports. Included among the industries to which the bank made an average SBA loan of $1.29 million last year: Agriculture and poultry, family entertainment, funeral services, medical and dental, self-storage, veterinary, and wine and craft-beverage.

The bank has a team of financing specialists dedicated to each of the designated industries. Among Live Oak’s current SBA borrowers are Martin Self Storage in Summerville, S.C.; Utah Turkey Farms in Circleville, Utah; Pinballz Arcade, Austin, Tex.; and Council Brewery Company in San Diego. Steve Smits, chief credit officer at the bank, told NerdWallet: “When you specialize in something, you become efficient. Because we do it every day and we have professionals and specialists, we tend to be more responsive and quicker.”

The heady combination of technological sophistication and banking expertise has allowed the lender to slash its loan-origination time to 45 days, about half the three-month industry average for SBA loans. To speed up loan sourcing and generation, the bank developed its own in-house technology, which led to the formation of the Wilmington-based technology company nCino, which was spun off to shareholders in 2014.

Live Oak did not return calls to discuss its lending strategies, but in SEC filings bank management declared: “The technology-based platform that is pivotal to our success is dependent on the use of the nCino bank operating system” which relies on Force.com’s cloud-computing infrastructure platform, a product of Salesforce.com.

Natalia Moose, a public relations manager at nCino told AltFinanceDaily in an e-mail interview: “We work with Live Oak Bank, in addition to more than 150 other financial institutions in multiple countries with assets ranging from $200 million to $2 trillion, including nine of the top 30 U.S. banks. nCino was started by bankers at Live Oak Bank who found the logistics of shuffling paperwork among loan stakeholders to be unwieldy, inefficient and time-consuming.

“nCino’s bank operating system,” Moose adds, “leverages the power and security of the Salesforce platform to deliver an end-to-end banking solution. The bank operating system empowers bank employees and leaders with true insight into the bank, combining CRM (customer relationship management), deposit account opening, loan origination, workflow, enterprise content management, digital engagement portal, and instant, real-time reporting on a single secure, cloud-based platform.”

Live Oak, meanwhile, is not resting on its technological laurels. According to Deer’s report, the bank’s parent company, Live Oak Bancshares, has formed a subsidiary to inject venture capital into fintech companies. It’s already taken a small equity stake in Payrails and Finxact, “the latter of which is developing a completely new core processor to compete against the old legacy systems used by most banks,” the Sandler O’Neill analyst writes. “Quite simply,” he asserts elsewhere in his report, “the company is far beyond any other bank we cover in its technical capabilities and the growth outlook remains outstanding.”

Five hundred and thirty-three miles due north along the Atlantic coast in southeastern Connecticut, Darien Rowayton Bank is also experiencing tremendous success as a lender using a home-grown technology platform. State-chartered by the Connecticut Department of Banking and regulated as well by the Federal Deposit Insurance Corp., the $600 million-asset bank is winning attention in banking circles for its online student-loan refinancing.

Five hundred and thirty-three miles due north along the Atlantic coast in southeastern Connecticut, Darien Rowayton Bank is also experiencing tremendous success as a lender using a home-grown technology platform. State-chartered by the Connecticut Department of Banking and regulated as well by the Federal Deposit Insurance Corp., the $600 million-asset bank is winning attention in banking circles for its online student-loan refinancing.

A few years ago, DRB, as it is known, was looking to go beyond mortgage and commercial lending — “the bread and butter for most community banks,” bank president Robert Kettenmann explained to AltFinanceDaily in a telephone interview – and was somewhat at a loss. The bank considered but then rejected the credit card business. Finally, DRB struck paydirt refinancing student loans. “Our chairman really seized on the opportunity,” Kettenmann says, adding: “It’s a $35 billion market.”

Thanks to the National Bank Act, it’s able to operate in all 50 states. As a regulated commercial bank with a strong deposit base, DRB can also offer low rates well below any state’s usury prohibitions.

What is most striking about DRB’s program is its nationwide targeting of upwardly mobile, affluent young professionals. According to a PowerPoint presentation obtained by AltFinanceDaily, all of the bank’s super-prime borrowers, who are mainly in the 28-34 age bracket, have a college degree and a whopping 93% have graduate degrees. Average income is $194,000.

Forty-eight percent of those refinancing student loans with DRB are doctors or dentists and another 22 percent are pharmacists, nurses or medical employees; only about 20% are paying off their law degrees or MBAs. The heavy concentration of refinancing in the medical field reduces economic risk in an economic downturn. Forty-three percent of the borrowers are home-owners, the rest are renters – and prime candidates for an online, DRB-financed mortgage.

Forty-eight percent of those refinancing student loans with DRB are doctors or dentists and another 22 percent are pharmacists, nurses or medical employees; only about 20% are paying off their law degrees or MBAs. The heavy concentration of refinancing in the medical field reduces economic risk in an economic downturn. Forty-three percent of the borrowers are home-owners, the rest are renters – and prime candidates for an online, DRB-financed mortgage.

(Once known as “yuppies” today this cohort is “known by the acronym ‘HENRY,’” remarks Cornelius Hurley, a Boston University banking professor and executive director of the Online Lending Institute, explaining the initials stand for “High Earners Not Rich Yet.”)

The Connecticut bank partnered with a third-party on-line vendor, Campus Door, when it commenced making student loans in 2013. In the fall of 2016, however, DRB built out its own, proprietary loan-origination system, Kettenmann reports, emphasizing that CampusDoor had been an excellent partner but that the bank wanted to exercise end-to-end control over the process. DRB employs a seven-pronged, “omni-channel” marketing approach that includes interactive marketing, affinity partnerships, digital/online advertising, direct mail, mass-media advertising, and public relations/brand awareness campaigns.

DRB’s online enrollment provides “pre-approved rates” in less than two minutes with final approval on rates in 24-48 hours. Refinancers can complete the online application at their own speed. Through May, 2017, DRB had made $2.48 billion in refinancing to 20,000 student-loan borrowers, with only ten defaults, five of which were attributed to deaths or “terminal illness.”

On Yelp! the bank has received a batch of reviews ranging from very favorable, five-star (“I had a truly wonderful experience”) to one-star (“awful” and “truly a nightmare”). Many fault the application process as laborious, describing it as “time-consuming.” But for those who have succeeded, like the reviewer who counseled “patience,” the result can be “the lowest rate with DRB…my loan payments went down $100 a month.”

![]() Just about an hour’s drive south and taking its name from its proximity to New York city just over the George Washington Bridge is New Jersey-based, state-chartered Cross River Bank, which has a reputation as a partner-in-arms to fintech companies. “We’re both users and producers of technology,” declares Gilles Gade, the bank’s chief executive.

Just about an hour’s drive south and taking its name from its proximity to New York city just over the George Washington Bridge is New Jersey-based, state-chartered Cross River Bank, which has a reputation as a partner-in-arms to fintech companies. “We’re both users and producers of technology,” declares Gilles Gade, the bank’s chief executive.

The bank provides “back-end” and infrastructure support to 17 marketplace lenders that offer a suite of lending products including personal loans, mortgages and home-equity loans. Following loan origination by a fintech company – Marlette Funding, Affirm, Upstart, loanDepot, SoFi, and Quicken Loan, among other partners — Cross River does the actual underwriting. Last year, Gade reports, the bank underwrote 1.9 million loans valued at $4-4.5 billion, about 10% of which Cross River kept on its books. The bulk of the loans are sold “back to the marketplace lenders” or to a third party. “We’ve created a high-velocity automated system,” he says.

Gade is manifestly unapologetic about the bank’s role in assisting fintechs in their competition with the banking establishment. “We’re a banking infrastructure services provider for those who want to disrupt the banking system,” he says. “Consumers expect a lot better than they’ve been getting from traditional banking services.”

Back in Boston, Radius Bank’s chief executive reports that forging partnerships with fintechs to provide the full panoply of online banking services was no easy proposition. In its mating ritual, Radius not only had to determine that a fintech company’s offerings were sound and that it had the right characteristics – most especially “a long-term, sustainable business model” – but that its corporate culture meshed comfortably with Radius’s.

Back in Boston, Radius Bank’s chief executive reports that forging partnerships with fintechs to provide the full panoply of online banking services was no easy proposition. In its mating ritual, Radius not only had to determine that a fintech company’s offerings were sound and that it had the right characteristics – most especially “a long-term, sustainable business model” – but that its corporate culture meshed comfortably with Radius’s.

After meeting with as many as 500 fintechs and after a fair amount of trial and error, Radius formed partnerships with LevelUp, which enables customers to make mobile payments; with online lender Prosper, for refinancing consumer debt and “credit rehabilitation”; with SmarterBucks, for refinancing student loans; and with online investment firm Aspiration Partners – which allows investors to name their own fees and markets itself to a predominately middle-class audience as the firm “with a conscience.”

Radius employs advertising on social media websites and employs “psychographics” to appeal to “anyone who is zealous about using technology, not necessarily millennials,” Butler says. The data show that 65% of adults in the U.S. would prefer to use a traditional bank and have face-to-face interactions with a teller, he notes, leaving the remaining 35% as Radius’s target audience.

Christopher Tremont, executive vice-president for virtual banking, told AltFinanceDaily that a typical Radius customer is 42 years old, lives in Boston, New York, Chicago “or one of the bigger cities in the West,” is a “technophile,” earns $75,000 a year, and has $100,000 in personal assets.

Radius’s performance since it went paperless has been stellar. The bank has seen a rapid rise in deposits, spurting to $782 million through the first quarter of 2017, up from $565 million at year-end 2014. With little fee income but ample deposits and low-cost funds, Radius realizes the bulk of its revenues – and profits — on the interest-rate spread generated from its loan portfolio.

The bank booked $43.5 million in SBA loans last year, ranking it in the top 50 banks on the SBA’s league tables, while carrying another $105 million in its commercial leasing business at the end of the first quarter this year. Loan generation is driving asset growth, which are currently at $973 billion, up more a third from $726 million in 2014, and Butler expects the bank’s assets to top $1 billion sometime this year.

“Community banks love that part of the business—lending money,” Butler says.

Tips From the Source: Small Businesses Told AltFinanceDaily How They Wanted Loans to be Marketed to Them

July 31, 2017

Small business owner Jim Moseley is inundated with calls from online funders—and he hates it. They frequently use unscrupulous tactics to try and get his attention. More than one has claimed to be a close friend so his assistant transfers their call. Then they try to reel him in with stories they’ve concocted about past personal connections. The unprofessional-sounding calls also irk him—where a salesman insists he’s local, but his voice sounds muffled and distant. In these instances, Moseley usually hangs up within a few seconds.

“The layer of sleaze is as thick as lard in the calls that I get,” he says.

Like many small business owners, Moseley, the chief executive of TransGuardian Inc., a shipping solutions company based in Petersham, Massachusetts, finds these types of calls extremely off-putting. In fact, it’s what made him hesitant to do online funding to begin with—until it became absolutely necessary since he couldn’t get a bank loan.

He’s not alone. As online financing proliferates, several small business owners say they are increasingly being bombarded with stacks of snail mail, multiple cold calls a day and numerous unsolicited emails offers—many of which they don’t understand and therefore won’t accept. Rather, small business owners say they prefer to work with companies that are forthcoming, provide sound advice and have taken steps to prove their credibility. They offer several tips on how funders can win more of their business.

Tip No. 1: Can the cold-calls

Several small business owners say they don’t mind when lenders follow up with them after a legitimate interaction. But they could do without the boiler-room tactics.

“It feels like a loan shark situation,” says Sean Riley, co-founder of DUDE Wipes, a Chicago-based company that makes flushable wipes for men. Riley, who has several good experience obtaining loans through Kabbage, finds the constant phone calls from firms he doesn’t know particularly vexing. He suggests lenders drop the high-pressure routines and find more effective ways to promote their services to small businesses. “These companies could be very credible. I don’t know. But I don’t perceive them as credible—and perception is reality,” he says.

Tip No. 2: Step up legitimate marketing efforts

Donna Cravotta chief executive and founder of Social Pivot PR, a Bedford, New York social media and marketing communications firm, says online funders should seek out simple, cost-effective ways to get their name in front of small businesses. For relatively little money they can sponsor local small business events. She also suggests that online lenders volunteer to speak at small business events and teach small businesses how to leverage online lending opportunities. They could also appear as guests on financial podcasts or broadcast Webinars to the small business community, says Cravotta, who has taken a few loans to fund her business, two of which were with Lending Club.

R.T. Custer, co-founder and chief executive of Vortic Watch Company in Fort Collins, Colorado, offers some additional advice: Customers don’t believe when you self-publish your testimonials. When he sees a review on a website, he wants to know how much a company has paid for that review. Instead, he relies on third party confirmations of a company’s worth. “When it’s clearly something that is not paid for, that is the best kind of advertising,” says Custer, an OnDeck customer whose business turns antique pocket watchers into wrist watches.

Tip No. 3: Deliver personal attention

As much as they hate aggressive salespeople, small businesses love personal attention from their lenders. Dana Donofree, founder and chief executive of AnaOno Intimates, a Philadelphia-based company that designs and sells apparel for breast cancer survivors, appreciates the stellar customer service she gets with OnDeck. The sales rep follows up appropriately to make sure everything is going well, but doesn’t bombard her constantly. She gets an occasional email asking if she needs more funds—but the communications aren’t overly aggressive. “Some institutions can really be sales pushy and call you several times a day. I’ve blocked more numbers than I would like to admit,” she says.

Tip No. 4: Be a resource for small business owners

Online lenders can also gain traction by helping customers better understand the financing process; many small business owners often don’t know much about financing and would appreciate getting sound advice from lenders, according to Sandy Lieberman, who co-owns Artemis Defense Institute in Lake Forest, California.

She and her husband started the business a few years ago to offer reality-based training to law enforcement, military personnel and civilians. When the business needed cash, Lieberman began searching online for a bank loan, but wound up taking a merchant cash advance instead. After a few rounds, she started getting bombarded with solicitations. “I think the stacks of mailings from companies must have been four-inches thick,” she recalls.

After additional research, she reached out to Lendio to broker an $85,000 term loan; she later took another loan for $204,000 through Lendio. While these funds have brought her business to a better place—and she has learned a lot in the process—she feels online lenders are missing out on a prime teaching opportunity.

“Some lenders think business owners know more than they already do. Some really don’t know a lot and could use more hand-holding,” she says.

In hindsight, Lieberman—who nearly destroyed her personal credit while trying to run her business—wishes a funding company had offered her a short class on financing; she would have attended, even for a small cost. Access to a finance coach—someone at the lending company who could help business owners plan proactively without ruining their personal credit—would also be a boon, she says.

“Small business owners are wearing many hats—customer service, payroll, financing, strategic planning. In the midst of all that they don’t know necessarily know how to make wise funding decisions,” she says.

Tip No. 5: Advertise

There are plenty of small businesses that need funds, but many simply don’t know where to turn. Consider a TD Bank survey of 553 small business owners in late March that found 21 percent have or will seek a loan or line of credit in the next 12 months. While the majority of these businesses plan to try their bank first, a sizeable number—11 percent—don’t know how to seek credit when they are ready. While many small businesses have found lending partners by Googling for information, others simply feel stymied by the process.

Take the case of Scott Deuty, who is having trouble obtains funds for Coolbular Inc. in Cheyenne, Wyoming, which serves as an umbrella for his kiddie ride business and his writing and publishing services. He wants to raise funds but has bad credit and doesn’t meet the revenue requirements for certain lenders. There are so many lenders; he doesn’t know how to find the right one—or one that might be willing to take a chance on him. “It’s very difficult,” he says.

Deuty’s case is an example of the paralysis that can happen when small businesses don’t know where to turn. It’s an opportunity for alternative funders to gain a leg up by marketing more appropriately to small businesses that may not know they exist—or how to find them.

Custer, of Vortic Watch, reached out to OnDeck for a bridge loan after seeing a television ad that ran during an episode of Shark Tank. He also suggests funders use online advertising to gain broader exposure. “If a business owner is trying to find a loan, they are going to Google, ‘I need a loan,’” he says.

Tip No. 6: Ramp up business referrals

Tip No. 6: Ramp up business referrals

Another way small businesses hear about lending opportunities is through business referrals. Azhar Mirza, founder of SomaStream Interactive, an e-learning solutions provider in Berkeley, California, says funders should actively seek out more referral partnerships. In 2015, his company couldn’t afford its online marketing costs. Then a lifeline came its way. Mirza received an offer from Google telling him his company was eligible for a loan to help finance the online advertising it was doing through the Google AdWords program. The offer was part of a new pilot program between Google and Lending Club to extend credit to smaller companies that use Google’s business services. SomaStream got access to the funds it needed, but in lieu of cash, the company received advertising credits with Google.

The pilot program between Google and Lending Club ended in the first quarter of 2016, but Mirza believes similar partnerships would be a great tool for online lenders. Certainly for Mirza, the timing was precipitous, he says.

Push notifications from trusted business partners can also be an effective marketing tool, when used in moderation. When Yvonne Denman-Johnson, co-founder of HootBooth Photo Booth, a Lago Vista, Texas, manufacturer of photo booth kiosks, needed money, she happened to receive a notice from Shopify, the company’s e-commerce software and hosting provider, talking about its merchant cash advance services. She has one outstanding advance through Shopify, which she is working to pay off.

Tip No. 7: Be transparent

Denman-Johnson got the funds she needed, but she feels MCA providers need to be more transparent about the effective interest rate—at the advertising stage, not at the approval stage—so small businesses can make more informed decisions without having to do all the calculations themselves. Otherwise, some small businesses might decide not to pursue this form of funding because of the unknowns. Her company almost walked away, but decided to go through the full application process. At this point, Shopify provided the effective interest rate, which was in the 12 percent range. Other funders she researched were in the 30 percent range—which she describes as “outrageously” expensive.

Indeed, small business owners want to work with funders that outline the terms clearly and offer comparisons. Lisa Ayotte, founder of Soul’y Raw, a specialty pet food provider in San Marcos, California, has had good experiences with Kabbage, On Deck and Fundbox.

Indeed, small business owners want to work with funders that outline the terms clearly and offer comparisons. Lisa Ayotte, founder of Soul’y Raw, a specialty pet food provider in San Marcos, California, has had good experiences with Kabbage, On Deck and Fundbox.

She wishes, however, that all online lenders offer more detailed information about the loan programs they offer on their website—so small businesses can weigh their options before they go through the actual application process. Small businesses want to know, for instance, whether a lender offers debt consolidation. They also want funds to spell out clearly on their websites the various types of loans offered and the underwriting criteria. Ayotte also suggests lenders provide links to online loan calculators so small businesses can understand what the terms mean to them.

Small business owners want to be told like it is. That’s one major appeal of online lending—if you’re going to be turned down, you typically know right away says Ricardo Picon, the co-owner of The Sandwich Shop, a restaurant and catering business in Williamsburg, New York.

He took an $88,000 loan in February issued by Excelsior Growth Fund, a U.S. Treasury-certified Community Development Financial Institution, but in the future, he says he would consider using a different type of online lender. It would depend on the rates, the economic times, monthly payments and closing fees, among other things. “I want transparency. I want to know if they are going to give me the money or not so I can move on. This way there are no false hopes,” he says.

Tip No. 8: Make the process as easy as possible

Small business owners also prefer to work with online lenders that make the process seamless. AJ Saleem, founder of Suprex Learning, a Houston-based private tutoring and test prep company, was proactive about searching for online lending options. He chose a loan with Lending Club in part because the process was so easy. Some applications he started, but never finished because the process was too onerous. With Lending Club, the process was quick, there were fewer questions asked and the funder asked for less documentation than some competitors, Saleem says.

To be sure, rates are really important to small businesses, but they also want to work with funders they feel are on the up-and-up. “We want a square deal,” says Moseley, the chief executive of TransGuardian. “Tell us what the deal is in an honest and professional way and if we like it we’ll do business.”