Shopify Capital’s Funding Business Grows in Q2

August 14, 2024Shopify Capital originated ~$700M in business loans and merchant cash advances in Q2. During the earnings call, Shopify CFO Jeff Hoffmeister referred to its Capital division as a “growth business” that had increased in volume. Shopify has otherwise seemed to downplay mention of this division since early last year. In terms of origination volume, the company is still not as big as Enova or Square Loans.

Shopify’s rival, Amazon, used to offer funding to its clients directly as well, but switched to referring its clients to third party lenders earlier this year.

SellersFi Surpasses $1B in Loans Since Inception, Experiences Success Through E-Commerce Funding

June 14, 2024The timing of it all was fortuitous for SellersFi. When the company announced in January that it had secured a partnership with Amazon to provide eligible Amazon sellers with access to credit lines, it was clear that its fresh equity raise and credit facility of up to $300 million were going to be put to use. SellersFi wasn’t the only partner, however, and Amazon still did most of the lending to its own sellers directly, a business it had been in for more than a decade, but it was still a big relationship to have. But then it got better. In March, Amazon announced that it would end its direct lending program and rely entirely on its partners instead. For SellersFi that meant it would have the opportunity to service even more sellers on the platform than before. Since then, SellersFi has quietly surpassed $1 billion in loans since inception.

“What we are seeing now is less competition,” said Ricardo Pero, CEO of SellersFi, in a call with AltFinanceDaily. He partially attributed that to the current interest rate environment which has impacted those with small margins. SellersFi, however, has experienced a lot of success. The company knows the e-commerce space particularly well, the only space it operates in, since its the only US lending platform also approved as a payment service provider member for Amazon. They started their relationship with Amazon as a service provider 3 years ago. While Pero said they have seen “nothing that points to a recession,” their experience suggests that even if one were to happen in the future, consumers would react by seeking out bargains on e-commerce platforms, reinforcing their position as the niche to be in. As readers may recall, a flight to e-commerce is also what happened during the pandemic.

E-commerce, however, is a broad umbrella, and Amazon is not alone in the universe. Millions of businesses rely on various platforms for e-commerce from basic templates with API connections to Shopify and more. Even big box brick and mortar retailers are waking up and rapidly inching their way into e-commerce. Walmart is just one example, which not only accommodates individual sellers on its platform but also offers merchant cash advances to them.

“The competitive landscape is changing for our clients,” Pero said. Pero added that they know what’s going on because they talk to these clients all the time and that even in the e-commerce business there are person-to-person relationships. “Customers mention their account managers by name,” Pero said. “We have a reputation as a partner to these merchants.”

One trend they’ve noticed over the last year or so is their strategy towards borrowing. While merchants have always typically used funds for things like advertising or inventory, the previous low rate environment enabled behavior where merchants could borrow first and then figure out how to spend the funds second whereas now that rates are higher there is a lot more of a deliberative approach to precisely how much they should get and what it will be used for in advance. It’s something they see all the time now and agree with. “You need to plan,” Pero said.

Shopify Capital MCA, Loan Origination Growth Appears to Slow Down

May 9, 2024Shopify Capital, the funding arm of Shopify that provides merchant cash advances and loans to merchants on its platform, experienced no increase in these related receivables in Q1 compared to Q4 2023. The company typically records significant growth in this figure each quarter. Shopify used to broadcast its origination figures far and wide in each quarterly earnings report and call but has since gotten shy about this segment of its business and no longer discloses originations. Instead, its balance sheet line item for “Loans and merchant cash advances” is virtually all there is to go by now and they were listed at $815M in Q1 vs $816M the prior quarter. This, of course, only reflects anything they’ve kept on balance sheet and could be a misleading indicator if those receivables are being sold off or taken on by a third party.

Shopify’s major rival, Amazon, never disclosed origination figures for its Amazon lending program, and in March announced that it was discontinuing its in-house lending program altogether after a 12-year run.

Shopify is still among the largest online small business lenders in the US.

Controversial Search Engine Marketing Tactic Targeted by Google

March 24, 2024 When company domain names expire, some investors snatch them up to take advantage of the residual benefits left behind. That is that if the company had a significant footprint in search engines before going out of business then it can pay big money to bring that domain name back to life and monetize its organic search traffic.

When company domain names expire, some investors snatch them up to take advantage of the residual benefits left behind. That is that if the company had a significant footprint in search engines before going out of business then it can pay big money to bring that domain name back to life and monetize its organic search traffic.

But Google hasn’t become too fond of this strategy since it’s apparently often used in a deceptive manner.

“Expired domain abuse is where an expired domain name is purchased and repurposed primarily to manipulate search rankings by hosting content that provides little to no value to users,” wrote Google as part of its new policy. “Expired domain abuse isn’t something people accidentally do. It’s a practice employed by people who hope to rank well in Search with low-value content by using the past reputation of a domain name. These domains are generally not intended for visitors to find them in any other way but through search engines. It’s fine to use an old domain name for a new, original site that’s designed to serve people first.”

Google also made changes to its core algorithm that is reducing “unhelpful, low-quality, unoriginal content in its search results by 40%.”

Once upon a time Google organic search traffic could be make or break for a company but today there are so many platforms that people are using (Think the Amazon Echo, ChatGPT, TikTok, and more) that it is merely one channel out of many on the internet to acquire customers.

What Big Publicly Traded Companies Say About Merchant Cash Advances

March 13, 2024AltFinanceDaily examined the public messaging from some of the largest publicly traded merchant cash advance facilitators in the US and this is what it found:

SHOPIFY

A merchant cash advance is a purchase of your future sales, also known as receivables. If your application for funding is accepted, then Shopify provides you a lump sum of money for a fixed fee. Under the Shopify capital agreement, this lump sum is known as the amount advanced, and the total to remit is the amount advanced plus the fixed fee. In return, you pay Shopify Capital a percentage of your daily sales until Shopify receives the total to remit. The percentage of your daily sales that you must remit to Shopify is known as the remittance rate. The amount advanced and the remittance rate depend on your risk profile.

For example, Shopify Capital might advance you 5,000 USD for 5,650 USD paid from your store’s future sales, with a remittance rate of 10%. The 5,000 USD amount that you receive is transferred to your business bank account specified in your admin, and Shopify Capital receives 10% of your store’s gross daily sales until the full 5,650 USD total to remit has been remitted. You have the option, at any time, to remit any outstanding balance in a single lump sum.

There is no deadline for remitting the total to Shopify Capital. The daily remittance amount in USD is determined by your store’s daily sales, because the remittance rate is a percentage of your store’s daily sales. The remittance amount is automatically debited from your business bank account.

DOORDASH

DoorDash Capital is a cash advance, not a loan. With a cash advance, the offer is based on your sales and account history, and includes a simple, transparent one-time fee that you’ll know before you decide to accept the offer. A loan operates using interest, which can compound over time, and often includes other fees in addition to the stated interest rate.

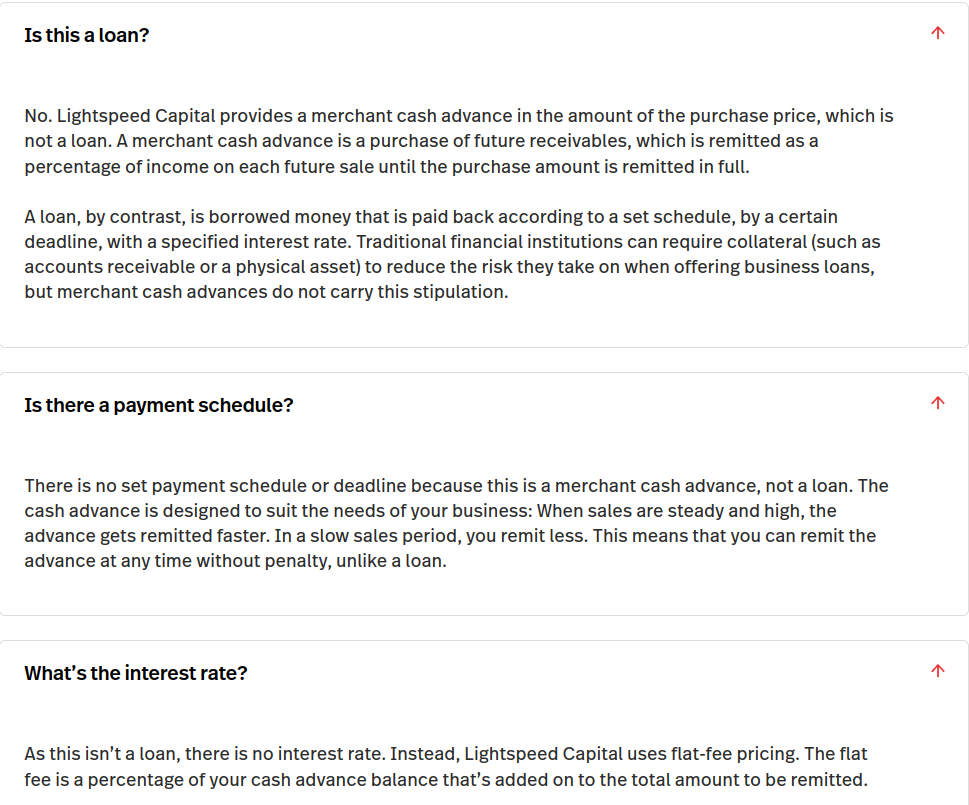

LIGHTSPEED

AMAZON

A [merchant cash advance is a] non-revolving sum of funding with flexible payment, no personal collateral required and no late fees. With flexible payment, no personal collateral required and no late fees, a merchant cash advance provides sellers funding to help run and grow their business. Unlike interest-bearing loans, the advance ties payment to a portion of a seller’s future sales for a fixed capital fee, there are no additional fees or interest charged.

NERDWALLET

Fixed withdrawals from a bank account

Merchant cash advance companies can also withdraw funds directly from your business bank account. In this case, fixed repayments are made daily or weekly from your account regardless of how much you earn in sales, and the fixed repayment amount is determined based on an estimate of your monthly revenue.

PAYPAL

A merchant cash advance is not a loan, but rather a type of financing that business owners pay back with a percentage of their future sales.

The Biggest Small Business Funders

February 21, 2024Although all of the specific data isn’t entirely available, we’ve compiled a short list of who the largest small business funders were in 2023:

1. Square

2. Enova

3. PayPal

4. Shopify

5. Amazon

6. Intuit

7. Parafin

The Top Small Business Funders Now Vs. Then

January 11, 2024Top Small Business Funders By Year

| 2008 | 2014 | 2023 |

| AdvanceMe (CAN Capital) | OnDeck | Square |

| First Funds | CAN Capital | Enova (OnDeck / Headway) |

| Merchant Cash and Capital (BizFi) | Kabbage | Shopify |

| BFS | Kapitus | PayPal |

| AmeriMerchant | Rapid Finance | Amazon |

| GBR Funding | National Funding | Intuit |

Many people look at 2023 vs 2008 and arrive at the conclusion that the fintechs rose to the top, but if one were to narrow down the definition of those players a little further, they’d notice that PayPal and Square are payment companies, Shopify and Amazon are e-commerce companies, and Intuit owns the Quickbooks accounting software. These are actually older companies that took an old idea (split-funding) and made it new again with some key changes. Although in the present moment it may feel like some of them cannot be beat (which is how the industry felt about the top funders in 2008), much can change over the course of this decade.

Keep your eye on:

- AI

- Blockchain (as payment rails, record-keeping)

- Regulation

Tips From Tibbs: Vendor Marketing Guide

November 6, 2023 The fine line between being successful and being stagnant in the equipment finance industry can easily be determined by vendor relationships. Cheryl Tibbs (CEO/Owner at Equipment Lease Co.), a veteran in the field, recently released her Vendor Marketing Guide this past October. The ten-chapter booklet covers various aspects, including vendor marketing, contact building, crafting value propositions, and more.

The fine line between being successful and being stagnant in the equipment finance industry can easily be determined by vendor relationships. Cheryl Tibbs (CEO/Owner at Equipment Lease Co.), a veteran in the field, recently released her Vendor Marketing Guide this past October. The ten-chapter booklet covers various aspects, including vendor marketing, contact building, crafting value propositions, and more.

Vendors are businesses authorized to sell equipment to end-users, Tibbs explains, and establishing a relationship with them can take a broker that is used to hunting for individual deals to instead being the recipient of multiple deals per week. But how to get that business is where most brokers get stuck.

“I think a lot of brokers get stuck with, ‘Well, how do I find vendors and what exactly is a vendor?’” she told AltFinanceDaily. “I think that chapter three sticks out in particular, just making contact, knowing how to find a vendor, what to say when you get a vendor on the hook, and how to engage with that vendor.”

Tibbs said that brokers often assume that vendors already have a bank in-house when that is not always the case. This thinking might also lead them to shoot too low even when they do solicit them.

“A lot of equipment brokers they market to vendors and say, ‘Hey, send me the stuff that your people won’t finance’ and I think if you ask for trash, you’re going to get trash,” said Tibbs. If a relationship is built properly, a broker can get the vendor’s A-paper clients, she added.

Not only does the guide breakdown vendor relationships but also provides examples of how to pursue them, whether it be email, in-person, etc. The guide is not where education ends for brokers, however. Tibbs believes it’s an on-going learning experience.

“I think if you’re making money and you’re building these relationships, that’s motivation in and of itself, to continue to sharpen your knowledge with regard to this,” she said.