Making Cents of Short Term Business Lending

June 22, 2014Where do you see yourself in 5 years? Perhaps you’ve seriously planned what you’ll be doing in mid-2019 or maybe you at least have an idea of how things will play out. It’s only a half a decade after all so how hard could it be to foresee the future?

Surely all of us saw the DOW surging 5 years ago and got rich right?

Did New Yorkers factor Hurricane Sandy into their 5 year plan back in 2009?

It’s only 5 years, what could possibly happen to a small business in that time?

As I recently logged onto LendingClub to invest in consumers loans, I began to wonder just how safe the 60 month terms were. Not that I have a lot of options since LendingClub only offers 3 or 5 year terms, but the latter is unquestionably risky. The borrower might look good now, but where in the heck will they be in 5 years? I can’t even begin to guess.

Mortgages, student loans, and car leases aside, I can think of very few reasons to use a 5 year loan from a personal perspective, mainly because that’s an extremely long commitment. For a small business, such a term far exceeds the rationale behind “working capital”, the reason oft-cited by businesses seeking less than $200,000.

The Small Business Administration’s website speaks of this:

Businesses that are seasonal or cyclical often require more working capital to stay afloat during the off season. Although your company may make more than enough to pay all its obligations yearly, you must ensure you have enough working capital at any one time to meet your short term obligations. For example, a company may do significantly more business over the holidays, resulting in large payoffs at the end of the year. However, the company must have enough working capital to buy inventory and cover payroll during the off season as well, when revenues are lower.

Working capital may come in handy for something like inventory for which the business probably expects to sell it all off in less than a year. Can you imagine still making monthly payments in 2019 for inventory you bought with a loan in 2014?

I bet this guy can’t:

And if the financial picture looks great and they have a long term need, why not go out 5 years?

Verizon replaced Washington Mutual. But a Verizon store, that will last forever…

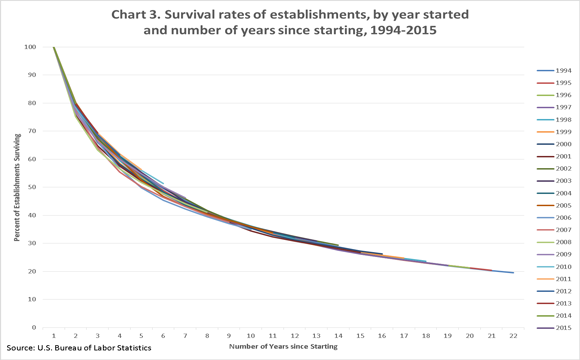

Only 41.1% of retail businesses live to experience their 5th birthday.

And even then when business types are aggregated, making it past year 5 doesn’t ensure lifelong success. Don’t confuse established with safe:

In fact, even borrowers are opting for shorter term loans with higher interest rates than long term loans with lower interest rates. Part of that is due to the lower net dollar cost paid for the loan said OnDeck Capital CEO Noah Breslow in an interview with Peter Renton:

5 years ago I used to spend way too much time on Instagram. Oh wait, no I didn’t… there was no such thing as Instagram.

What do you think is the best bet for this CD store? A 3-6 month working capital loan or a 5 year term loan?

Giving a borrower a lengthy repayment term ensures they will be able to pay you back right?

Above is the result of my $25 contribution towards a 5-year LendingClub loan issued on May 16th. They missed the very first payment. I’m really looking forward to the next 59 months…

In 2019, everything will be business as usual, won’t it Madam President…

As short term business lending critics herald the emergence of 3-5 year term business loans, I think it’s important to remember that they are catering to a market that likely has different goals. Long terms are often not appropriate for borrowers with working capital needs. The CEO of RapidAdvance, Jeremy Brown discussed this in an article he wrote for DailyFunder more than a year ago.

Our industry is based on providing working capital to merchants. By its very definition, working capital is less than 12 months. Longer term deals are permanent capital, even when they are repaid over 15-24 months.

As a borrower, the very idea of committing yourself to monthly payments 5 years from now should be considered very seriously. The average length of a marriage prior to a divorce is 8 years. For past or future divorcees, a 5 year loan is more than half as long as a marriage!

Alternative lenders should be asking themselves if they really have the data and underwriting skills necessary to make accurate predictions that far out in the future. Working capital underwriting models are not applicable as long term assessments.

If you’re going to make 5 year business loans, make sure to take advantage of Google maps. Take a look back at the business location and the ones surrounding it over the last few years. You may not feel so safe about your investment…

Electronic Payments Industry changing Forever – All Points Bulletin!

August 23, 2011Electronic Payments Industry Changing Forever – ALL POINTS BULLETIN

Posted on December 17, 2010 at 8:36 PM

Attention business owners and to all those employed in the merchant processing and Merchant Cash Advance industry. The world is changing and not at the ‘global warming will one day kill us all’ pace. It’s happening right now. Remember that little thing called the Wall Street Reform and Consumer Protection Act that passed in July? There was a little itty bitty part in there that we so happened to broadcast and critique in detail on our site, known as the Durbin Ammendment. Take a look the law’s summary, particularly #3. On the evening of December 16th, the Federal Reserve Board delivered an early Christmas present to all the debit card networks and big banks. The gift contained the government’s proposed debit card fee changes, or as some bank executives might tell you, “they mailed us 10 sticks of dynamite.” If you’re serious about this business, read through the 176 page document that every news agency is trying to sum up in 3 paragraphs.

Visa’s stock plunged on the news

Debit cards accounted for 35% of all non-cash transactions in 2009. The proposed changes seek to cap the fee charged for accepting a debit card to a maximum of 12 cents. According to the report issued by the Board, here’s what businesses are paying now:

“Networks reported that debit and prepaid interchange fees totaled $16.2 billion in 2009. The average interchange fee for all debit transactions was 44 cents per transaction, or 1.14 percent of the transaction amount. The average interchange fee for a signature debit transaction was 56 cents, or 1.53 percent of the transaction amount. The average interchange fee for a PIN debit transaction was significantly lower than that of a signature debit transaction, at 23 cents per transaction, or 0.56 percent of the transaction amount. Prepaid card interchange fees were similar to those of signature debit, averaging 50 cents per transaction, or 1.53 percent of the transaction amount.”

Debit interchange fees have always been assessed as a percentage of the sales amount. The larger the transaction size, the higher the fee. Debit cards are most frequently used for smaller purchases but a flat cap on transaction fees regardless of transaction size is a game changer. Now twist this with the fact that interchange fees are almost disappearing altogether and one needn’t think too hard about the unintended consequences.

MasterCard issued a statement immediately. “Experience demonstrates that consumers, not banks or payments networks are the biggest losers as a result of this regulation,” said Noah Hanft, MasterCard’s general counsel. “This type of price control is misguided and anti-competitive, and in the end is harmful to consumers.” Visa hasn’t provided any useful feedback at this time but has openly condemned the report.

The Board acknowledges that some card issuers can’t even cover their own costs with the 12 cent transaction fee in effect. This Board’s direct response to this dilemma is that they simply don’t care. “An issuer with costs above the cap would not receive interchange fees to cover those higher costs. As a result, a high-cost issuer would have an incentive to reduce its costs in order to avoid a penalty.”

Thank you Federal Reserve for the feeble minded, anti-capitalistic solution. “Just lower your costs or we’ll fine you.” The outrage is warranted because the proposal isn’t really a proposal at all. This is the new order granted to the government after the passage of the Wall Street Act back in July. The payment networks and banks may comment on this proposal but effective July 21, 2011, this simply becomes law.

This is the equivalent to forcing all the businesses in America to lower their retail prices under penalty of law as the solution to dealing with consumers whining about the recession.

Additionally, the Board constantly refers to the life cycle of a debit sale to being a 4 party transaction. There is:

* The bank that issued the card to the customer

* The customer

* The business that the customer shops at and uses the debit card

* The acquiring bank that the business uses to accept debit cards

The payment networks are what allow the acquiring banks to communciate with the banks that issued the debit cards. The networks have costs associated with their service, infrastructure, and overhead. The 12 cents per transaction is the combined total that can be charged between both the acquiring bank, payment network, and issuing bank. There’s not a whole lot to go around.

While the Federal Reserve and congress are patting themselves on the back and high fiving eachother for saving the economy (by sticking it to the big banks), the end result will be the loss of millions of jobs, the elimination of debit cards, an increase in other bank fees, the end of all debit rewards programs, the end of electronic payments quality, the end of electronic payments assurance, and the collapse of the free market economy. Give me a high five. Not!

Here’s what will happen and why:

* The Board ignores or does not understand the electronic payments industry business model. The debit card business is not a 4 party transaction. The acquiring bank party encompasses multiple layers and parties in itself. Acquiring bank —> Payment Processor —> Indepedent Sales Office —> Sales Agents. Debit transaction costs are marked up at each level to create a competitive marketplace. The electronic payments industry employs millions of people. With a 12 cent cap and no markup abiliity, those millions of workers will lose their jobs overnight.The majority of this business is commission based, with processors and sales agents directly taking home solely what’s generated on the markup of debit/credit fees of their clients.This is probaby the most blatent and incredibly obvious oversight. There can be no competitive market because costs are fixed and there can be no sales because there is no money for anyone to earn on markups. National unemployment will rise several percent over the course of a few months.

* Rewards debit cards can no longer exist. Card issuing banks currently pay their customers rewards by charging businesses more for accepting a rewards card transaction. Since a bank no longer has that ability, rewards cards can no longer exist.

* Debit cards become a moot point for banks. With no profit incentive to put them in the hands of customers and no ability to compete on price, there is no incentive for debit networks or cards to continue.

* Quality, fraud protection, and assurance will suffer. Banks whose own costs are higher than the imposed cap face fines by the Federal Reserve unless they cut costs. Therefore the government is not only incentivizing poor quality, but in fact making it mandatory.

* Ever hear of too big to fail? This industry is too big to be messing with. These are the actual national and international money networks through which trillions of dollars move through every day. Mandating poor quality, eliminating all competition, and removing profit incentives will de-evolutionize the flow of money altogether.

The Board will review and allow comments through March 31st, at which point this industry will meet its maker. Yes, it’s that’s serious.

-AltFinanceDaily

../../

Consumers Can Help Businesses Saves on their Credit Card Processing

August 23, 2011

Attention business owners and to all those employed in the merchant processing and Merchant Cash Advance industry. The world is changing and not at the ‘global warming will one day kill us all’ pace. It’s happening right now. Remember that little thing called the Wall Street Reform and Consumer Protection Act that passed in July? There was a little itty bitty part in there that we so happened to broadcast and critique in detail on our site, known as the Durbin Ammendment. Take a look the law’s summary, particularly #3. On the evening of December 16th, the Federal Reserve Board delivered an early Christmas present to all the debit card networks and big banks. The gift contained the government’s proposed debit card fee changes, or as some bank executives might tell you, “they mailed us 10 sticks of dynamite.” If you’re serious about this business, read through the 176 page document that every news agency is trying to sum up in 3 paragraphs.

Visa’s stock plunged on the news

Debit cards accounted for 35% of all non-cash transactions in 2009. The proposed changes seek to cap the fee charged for accepting a debit card to a maximum of 12 cents. According to the report issued by the Board, here’s what businesses are paying now:

“Networks reported that debit and prepaid interchange fees totaled $16.2 billion in 2009. The average interchange fee for all debit transactions was 44 cents per transaction, or 1.14 percent of the transaction amount. The average interchange fee for a signature debit transaction was 56 cents, or 1.53 percent of the transaction amount. The average interchange fee for a PIN debit transaction was significantly lower than that of a signature debit transaction, at 23 cents per transaction, or 0.56 percent of the transaction amount. Prepaid card interchange fees were similar to those of signature debit, averaging 50 cents per transaction, or 1.53 percent of the transaction amount.”

Debit interchange fees have always been assessed as a percentage of the sales amount. The larger the transaction size, the higher the fee. Debit cards are most frequently used for smaller purchases but a flat cap on transaction fees regardless of transaction size is a game changer. Now twist this with the fact that interchange fees are almost disappearing altogether and one needn’t think too hard about the unintended consequences.

MasterCard issued a statement immediately. “Experience demonstrates that consumers, not banks or payments networks are the biggest losers as a result of this regulation,” said Noah Hanft, MasterCard’s general counsel. “This type of price control is misguided and anti-competitive, and in the end is harmful to consumers.” Visa hasn’t provided any useful feedback at this time but has openly condemned the report.

The Board acknowledges that some card issuers can’t even cover their own costs with the 12 cent transaction fee in effect. This Board’s direct response to this dilemma is that they simply don’t care. “An issuer with costs above the cap would not receive interchange fees to cover those higher costs. As a result, a high-cost issuer would have an incentive to reduce its costs in order to avoid a penalty.“

Thank you Federal Reserve for the feeble minded, anti-capitalistic solution. “Just lower your costs or we’ll fine you.” The outrage is warranted because the proposal isn’t really a proposal at all. This is the new order granted to the government after the passage of the Wall Street Act back in July. The payment networks and banks may comment on this proposal but effective July 21, 2011, this simply becomes law.

This is the equivalent to forcing all the businesses in America to lower their retail prices under penalty of law as the solution to dealing with consumers whining about the recession.

Additionally, the Board constantly refers to the life cycle of a debit sale to being a 4 party transaction. There is:

- The bank that issued the card to the customer

- The customer

- The business that the customer shops at and uses the debit card

- The acquiring bank that the business uses to accept debit cards

The payment networks are what allow the acquiring banks to communciate with the banks that issued the debit cards. The networks have costs associated with their service, infrastructure, and overhead. The 12 cents per transaction is the combined total that can be charged between both the acquiring bank, payment network, and issuing bank. There’s not a whole lot to go around.

While the Federal Reserve and congress are patting themselves on the back and high fiving eachother for saving the economy (by sticking it to the big banks), the end result will be the loss of millions of jobs, the elimination of debit cards, an increase in other bank fees, the end of all debit rewards programs, the end of electronic payments quality, the end of electronic payments assurance, and the collapse of the free market economy. Give me a high five. Not!

Here’s what will happen and why:

- The Board ignores or does not understand the electronic payments industry business model. The debit card business is not a 4 party transaction. The acquiring bank party encompasses multiple layers and parties in itself. Acquiring bank —> Payment Processor —> Indepedent Sales Office —> Sales Agents. Debit transaction costs are marked up at each level to create a competitive marketplace. The electronic payments industry employs millions of people. With a 12 cent cap and no markup abiliity, those millions of workers will lose their jobs overnight.The majority of this business is commission based, with processors and sales agents directly taking home solely what’s generated on the markup of debit/credit fees of their clients.This is probaby the most blatent and incredibly obvious oversight. There can be no competitive market because costs are fixed and there can be no sales because there is no money for anyone to earn on markups. National unemployment will rise several percent over the course of a few months.

- Rewards debit cards can no longer exist. Card issuing banks currently pay their customers rewards by charging businesses more for accepting a rewards card transaction. Since a bank no longer has that ability, rewards cards can no longer exist.

- Debit cards become a moot point for banks. With no profit incentive to put them in the hands of customers and no ability to compete on price, there is no incentive for debit networks or cards to continue.

- Quality, fraud protection, and assurance will suffer. Banks whose own costs are higher than the imposed cap face fines by the Federal Reserve unless they cut costs. Therefore the government is not only incentivizing poor quality, but in fact making it mandatory.

- Ever hear of too big to fail? This industry is too big to be messing with. These are the actual national and international money networks through which trillions of dollars move through every day. Mandating poor quality, eliminating all competition, and removing profit incentives will de-evolutionize the flow of money altogether.

The Board will review and allow comments through March 31st, at which point this industry will meet its maker. Yes, it’s that’s serious.

-AltFinanceDaily