PayPal & LendUp Bridge Financial Inclusion Gap

July 25, 2017

PayPal put its stamp of approval on fintech startup LendUp, evidenced by a strategic investment by the eBay spinoff in recent weeks. In doing so PayPal demonstrated its commitment to non-prime borrowers, which is the demographic that San Francisco-based LendUp targets.

The pairing brings together the chief executives of two companies – Sasha Orloff and Dan Schulman of LendUp and PayPal, respectively — who have been at the forefront of fintech and who together will likely play an expanded role together.

“People care about the ability to build credit and about having a safe product and a really great user experience. We are aligned with PayPal there. Dan is a pioneer in financial inclusion. He is a ringleader in the industry. There is an exciting momentum from an executive leader with a voice for financial inclusion from one of the largest and most successful fintech companies,” Orloff told AltFinanceDaily.

PayPal’s mission is similar.

“LendUp and PayPal share a vision of reimagining financial services and offering innovative solutions to people typically underserved by the traditional financial system. PayPal has made a strategic investment in LendUp to help this fintech innovator continue to grow and broaden its positive impact on improving financial health,” according to a PayPal spokesman.

LendUp focuses on the emerging middle class, including those who were left behind in the wake of the financial crisis. Orloff pointed to a macroeconomic shift beginning in 2008 with the creation of Dodd Frank, which is contributing to a deep well of financial exclusion. “More than half of the country has a credit score below 680 and are excluded from many bank products,” Orloff added.

Meanwhile as online lending has taken root banks have demonstrated a stubborn inability to become tech focused

Second Time Around

Orloff and Schulman are no strangers to one another. Previously the LendUp chief was senior vice president at Citi Ventures, Silicon Valley’s maiden venture capital firm for early stage fintech, while the PayPal president and CEO served as group president of enterprise growth at American Express.

“Through the process I met Dan Schulman [then] at American Express. He was a big champion of financial inclusion. He had been tooting the horn at AMEX for a long time and had been leading their financial inclusion revamp,” said Orloff.

While at Amex Schulman was LendUp’s executive sponsor before taking the helm at PayPal. Soon after the teams reconnected and recognized even more possibilities beyond the PayPal ecosystem, such as providing access to credit and helping borrowers to build a credit score. There is also the massive PayPal database to consider.

“PayPal has a bigger reach and a more relevant audience,” said Orloff, declining to tilt his hand to the specific ways in which LendUp and PayPal will partner. “We have a lot of conversations in the works. That is absolutely part of the investment and we are excited,” noted Orloff.

LendUp earlier this year surpassed the $1 billion threshold for loan originations since the company was founded half a decade ago.

“We are a balance sheet lender,” said Orloff. “But we just continue to grow so quickly that we’re going to need to diversify our funding sources over time. We set up structures to do that now, and [investor] Victory Park is an amazing supporter,” said Orloff, pointing out that LendUp just doubled its access to capital with a $100 million credit facility to fund loan growth. “Eventually we will outgrow them as a single funding source. And that will come up soon.”

LendUp’s trifecta of offerings include credit cards, loans and financial education. The education is delivered via online videos and courses that highlight how much bad credit can cost borrowers, evidenced by $250,000 in fees paid by an average consumer with bad credit over their lifetime, according to LendUp stats. LendUp provides tools to help people to improve their credit score, ultimately making it easier and cheaper to borrow money. LendUp has saved its customers nearly $150 million in fees and interest.

Meanwhile LendUp and Beneficial State Bank recently announced an expansion of their credit card, the L Card, which should quadruple the availability of the Visa product.

“We launched the card recently and already by just having a simple and transparent credit card we’ve gotten a top rating in the credit card space,” said Orloff, adding that there is more to come. “We are going to completely revolutionize what credit cards mean for the emerging middle class. We are going to bring innovation that has not happened before. We are almost ready to launch and share that.”

Orloff expects that LendUp will grow in “overwhelming influence” over the course of the next year.

Grameen Bank Effect

For his part, Orloff has always had a penchant for helping the poor, evidenced by his efforts with the Grameen Foundation supporting financial services in rural and under-served areas. His work with the foundation was inspired after reading Nobel Peace Prize winner Dr. Muhammad Yunus’ book Banker to the Poor.

From there he moved on to Citi, where he did credit underwriting before joininig Silicon Valley’s maiden venture capital firm for fintech, Citi Ventures. In 2012 LendUp was born and Orloff has been determined to provide good structured products with embedded education that can help to make people more successful ever since.

PayPal’s Merchant Cash Advance Program Grows, Performance Improves

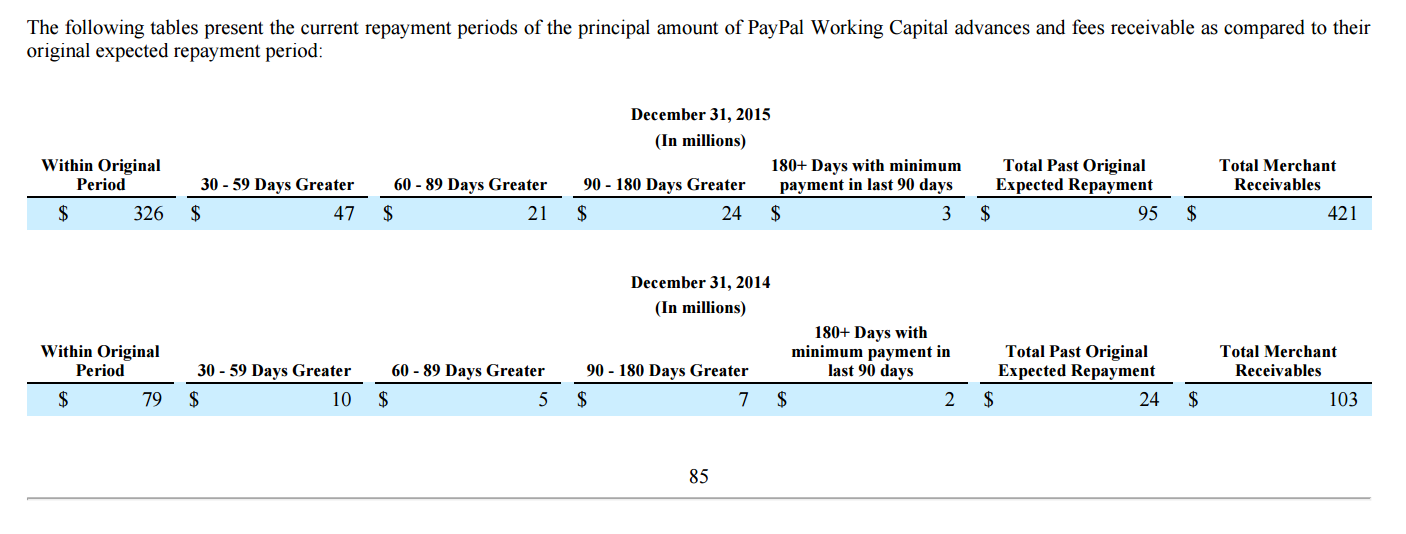

February 27, 2016The PayPal Working Capital program has advanced more than $1 billion to small businesses since inception. Rooted in merchant cash advance methodology since PayPal withholds a percentage of each transaction until receiving payment in full, they are not actually buying future receivables. Rather, they originate loans through WebBank, the same Utah-chartered industrial bank that OnDeck uses. But OnDeck’s payments are fixed and PayPal’s are tied to sales activity.

PayPal’s loans therefore don’t have a fixed term but they evaluate historical sales activity and use that to project a loan payoff usually within 9 to 12 months. According to their Q4 2015 earnings report, their 2015 results performed just as well if not better than their 2014 results.

$421 million was outstanding at the end of 2015 compared to $103 million at the end of 2014. 77% of the $421 million was on pace to pay off within 30 days of their planned projections. 11.16% was on pace to finish 30-59 days beyond them. PayPal broke it down by dollars in their earnings report.

But we’ve broken it down into percentages below:

| Total outstanding balance | Within Projections | 30-59 days greater | 60-89 days greater | 90-180 days greater |

| $421 million | 77.43% | 11.16% | 4.99% | 5.70% |

| Total outstanding balance | Within Projections | 30-59 days greater | 60-89 days greater | 90-180 days greater |

| $103 million | 76.70% | 9.71% | 4.85% | 6.80% |

PayPal borrowers cannot simply stop accepting PayPal payments in order to avoid loan repayment. They are required to pay at least 10% of their total loan amount (loan + the fixed fee) every 90 days so that they make consistent repayment progress regardless of their sales volume. Notably, their website warns, “If you do not meet the requirements in the above policies and your loan goes into Default status, your entire loan balance could become due and limits could be placed on your PayPal account.” For businesses that depend on PayPal sales, that is certainly a downside worth avoiding.

Is PayPal’s Working Capital Program a Mistake?

October 5, 2013 A few weeks ago, PayPal announced the launch of their Working Capital program as a way to help small businesses in need. They classify it as a loan but the explanation for how it works is textbook merchant cash advance. A percentage of each PayPal sale is withheld and applied as a reduction to the merchant’s balance. PayPal joining the booming merchant cash advance/alternative lending market is really no surprise. After all, RapidAdvance just got acquired by the same group that owns Quicken Loans. We’re in a new era of alternative finance.

A few weeks ago, PayPal announced the launch of their Working Capital program as a way to help small businesses in need. They classify it as a loan but the explanation for how it works is textbook merchant cash advance. A percentage of each PayPal sale is withheld and applied as a reduction to the merchant’s balance. PayPal joining the booming merchant cash advance/alternative lending market is really no surprise. After all, RapidAdvance just got acquired by the same group that owns Quicken Loans. We’re in a new era of alternative finance.

PayPal is respected as a payments company but are they ready for the high risk world of merchant cash advance financing? Critics are not so sure. Industry insiders have watched dozens of funding providers jump into the market with aggressive rates, attempt to undercut the competition, and acquire a lot of marketshare. The results are usually disastrous.

For years, journalists believed that the high cost of capital provided by non-bank lenders was fueled by the desire for immense profit. They didn’t understand the risks involved or realize that some funding providers weren’t even turning a profit at all. Last year, Opportunity Fund, a non-profit small business lender revealed that to make loans at 12% APR would fail to even cover costs. The for-profit sector of the industry charges factor rates (different than Annual Percentage Rates) between 1.14 and 1.50, not including fees. I explained this variance once before in The Fork in the Merchant Cash Advance Road.

So did PayPal learn anything from an industry that has been in existence for 15 years? It doesn’t look like it:

Doing some simple math (Total to be repaid / Loan Amount), the factor rates range from 1.04 to 1.12, figures that will probably only make sense if their average client has greater than 720 FICO, many years in business, and is virtually perfect on paper and in reality. Perhaps PayPal knows that and will decline 95% of applications or perhaps they believe their clients will buck the trend. I mean, is it possible that a corporate monster like PayPal could make a boneheaded mistake?

A 1.04 deal? Seriously? This has disaster written all over it. There are some people that believe that the losing proposition is intentional…

You can follow the discussion about this on DailyFunder.

Revenue Based Financing Continues to Spread at Global Pace

September 30, 2025 Earlier this month, Uber Eats joined the revenue-based financing movement by partnering with Pipe Capital.

Earlier this month, Uber Eats joined the revenue-based financing movement by partnering with Pipe Capital.

Karl Hebert, Vice President of Global Commerce and Financial Services at Uber, said of it, “We are happy to team up with Pipe to bring working capital to Uber Eats. Restaurants are our partners at Uber, and the backbone of our communities, yet many struggle with access to capital.”

It’s an unsurprising step considering rival DoorDash rolled out a merchant cash advance program nearly four years ago, though Uber arguably began experimenting with MCAs nearly ten years ago. And Uber is hardly doing it just to do it. Uber, for example, rolled out Uber Eats Financing, a revenue based financing product in Mexico through a partnership with R2 this past January, which went so well that they also rolled it out in Chile months later.

📢 Announcing a big milestone for R2 & @Uber!

Following a successful launch in Mexico, we’ve expanded our partnership with Uber Eats to Chile — bringing frictionless access to capital to thousands of merchants across the region. https://t.co/61WgP1ZtHy

— Roger Larach (@rogerlarach) April 30, 2025

In Chile with R2, the service is described as taking place entirely within the Uber Eats Manager App with a 5-minute application process and payments made automatically and deducted by a fixed percentage from sales made using the platform.

In the US with Pipe, it says that the Uber Eats App Manager will show capital offers from Pipe that are customized based on restaurant revenue, cash flow, and business performance.

Uber joins Amazon, Walmart, Shopify, Intuit, Stripe, DoorDash, PayPal, Square, GoDaddy, Wix, Squarespace and others in offering a revenue-based financing product.

Revenue-based financing as a product type is available in but not limited to the US, Canada, Mexico, Chile, UK, Germany, Ireland, Spain, South Africa, Nigeria, India, Hong Kong, Netherlands, Australia, Japan, Brazil, Singapore, and more.

The Great Concession, How the MCA Product Effectively Proved It Was Right All Along

September 26, 2025 There was no greater irony than the State of Texas banning ACH debits from sales-based financing providers at the same time that the State of Washington was celebrating the coming age of sales-based financing. In Texas, for example, the motivation for curbing sales-based financing was built on the premise that “this type of financing has raised significant concerns about predatory lending and that state attorneys general as well as the Federal Trade Commission have obtained high-profile judgments against such financing for predatory practices.” Meanwhile, in Washington, the motivation for the state holding the opposite opinion was that sales-based financing “increases access to capital for small businesses in Washington state, particularly those that have been historically underserved or underbanked.”

There was no greater irony than the State of Texas banning ACH debits from sales-based financing providers at the same time that the State of Washington was celebrating the coming age of sales-based financing. In Texas, for example, the motivation for curbing sales-based financing was built on the premise that “this type of financing has raised significant concerns about predatory lending and that state attorneys general as well as the Federal Trade Commission have obtained high-profile judgments against such financing for predatory practices.” Meanwhile, in Washington, the motivation for the state holding the opposite opinion was that sales-based financing “increases access to capital for small businesses in Washington state, particularly those that have been historically underserved or underbanked.”

How did these states reach the opposite conclusion?

There’s no caveat to how the Washington State program works. The State’s Department of Commerce partnered with Grow America and the operation is backed by a federal grant (SSBCI-21031-0048) to roll out and administer a revenue-based financing program as part of Washington’s State Small Business Credit Initiative. It’s sales-based financing or in this case revenue-based financing (which is the more common phrase these days). Grow America’s revenue-based financing program utters a very familiar phrase in its marketing.

“The months you generate more revenue, you pay a higher amount, when business is slower you pay less,” the company advertises.

This was at one time the signature calling card of a merchant cash advance, but now such features have been repackaged and rebranded into something similar but different, and everybody is doing them.

The Grow America program applies a 20% holdback on adjusted monthly revenue and requires a minimum monthly payment of $1,000 if the 20% holdback does not generate at least $1,000 for the month. Merchants can get approved for anywhere from $50,000 to $1 million. The product is marketed as having a 1.24 factor rate and an estimated 14.27% APR with a 3-year term. As industry participants are aware, increasing sales would translate into increasing payments, which means a rapidly paid off loan could potentially result in a final outcome APR in the triple digits, far and away from the “estimate.”

The irony is that the notable benefits of a similar product, merchant cash advances, which have no minimum monthly payments, no fixed term, and are not absolutely repayable, are eliminated when restructured in this way and presented as “revenue-based financing loans.” Revenue-based financing loans take the underlying structure of MCAs (payments tied to sales) and then strip away the benefits. However, when structured as loans, the argument often goes that they are likely to be cheaper, which may be true on average, but is not always true.

Indeed, Grow America leads specifically with price as for why its product, similar to its privately owned competitors, are the better option:

“There are a lot of online lenders offering revenue-based loans that promise instant approvals, but their terms are intentionally confusing, and the fees are high,” Grow America advertises. “Our lenders aren’t like that. They’re mission driven.”

In Texas, the author of the bill that banned debits from such financing providers “informed the [legislative] committee that commercial sales-based financing has become a popular financing option for small businesses desperate for credit and that, unlike traditional loans, this type of financing is repaid as a percentage of future sales or revenue.”

Indeed, it is very popular. The largest providers or brokers of such financing today whether structured as a purchase or loan, are household names like Amazon, Walmart, Shopify, Intuit, Stripe, DoorDash, PayPal, Square, GoDaddy, Wix, Squarespace and more. Some structure them as a purchase and call it a merchant cash advance and some structure it as a loan and call it revenue-based financing. In either case, payments are tied to the percentage of future sales or revenue.

In egregious cases of wrongdoing one way or another, such incidents have historically been a result of deceptive marketing or payments from a merchant exceeding the contracted amount. In New York, when transactions are structured as a purchase, courts generally look to make sure that the agreements have a reconciliation provision in the agreement, whether the agreement has a finite term, and whether there is any recourse should the merchant declare bankruptcy. Legally speaking, the products have become pretty well defined and understood in the court system.

Like Washington State, GoDaddy, which recently announced its new merchant cash advance program, markets its product in an almost identical fashion.

“If your sales go up, the MCA will be paid sooner; if the sales are slow, it’ll take longer,” GoDaddy says.

Same message.

Washington State requires merchants to make a minimum payment every month and a balloon payment if not fully repaid within 3 years. GoDaddy, by contrast, advertises no minimum payment amount, no set payment schedule, no penalties, and no late fees. One’s a loan, one’s a purchase.

While the best course of action is best left to the merchants, there appears to be a near-universal concession that the underlying nature of how merchant cash advance agreements were contemplated, payments tied to sales, made strong logical business sense all along. Washington State emphasizes this fact.

“We know that your business has its own needs and loans with fixed payment amounts may not be the best option for you,” they advertise. “The revenue-based financing fund offers loans with flexible payback terms so you can grow your business immediately and pay back your loan based on your varying revenue.”

Recent studies also now highlight the benefits of cash-flow-based underwriting.

In Sharpening the Focus: Using Cash-Flow Data to Underwrite Financially Constrained Businesses, “The paper finds that adding cash-flow information substantially increases the predictive signal of models that rely primarily on the business owners’ personal credit scores and firm characteristics.”

There’s also Square, the largest revenue-based financing provider in the US, that has explained why this system just works better. Square says that they can fund more businesses and have higher payment success rates than if they were to follow more conventional methods of underwriting and repayment.

“Square Loans addresses [the credit] gap by using near real-time business data to assess creditworthiness, evaluating metrics such as transaction volume and revenue patterns to offer short-term loans — with repayment on average in 8 months,” Square wrote in a White Paper. “This allows for a more accurate and timely understanding of a business’s capacity to borrow and repay. And loan repayments are higher during periods when business is stronger and reduced when sales are lower.”

What’s the sentiment these days on payments tied to sales revenue? The market has spoken.

ACH, Wire, and Soon Stablecoin Transfers?

June 30, 2025“Many of the users out there today are not aware of stablecoins, or not interested in stablecoins, and they should not be,” said Jose Fernandez da Ponte, PayPal’s SVP of blockchain, crypto and digital currencies to CNBC. “It should just be a way in which you move value, and in many cases, is going to be an infrastructure layer.”

Stablecoins, blockchain-based units typically pegged to the US Dollar, are taking off. According to Visa, for example, $3.7 trillion worth of stablecoins were transacted in the last 30 days alone. Since there’s no speculation angle to be gained from holding them, the value of using stablecoins versus other methods of payments is primarily speed and cost. As an infrastructure layer, traditional lenders may want to keep an eye on developments there. For example, where ACHs may become too costly or impossible to utilize efficiently, USD-> Stablecoins-> USD could become a viable mechanism to sweep funds from a traditional bank account to a third party. Borrowers may not ever even need to know or be aware that blockchain rails are being used to transmit payments. Lenders too need not be burdened by crypto and instead merely leave the conversion of one to the other and back to a payment service.

This is not the domain of edgy upstart fintechs any longer either. According to American Banker, “The progress of the GENIUS Act has spurred banks to forge stablecoin strategies, with Citigroup, Bank of America and dozens of others considering launching their own stablecoin, joining a stablecoin consortium or both.” Additionally, stablecoin issuer Circle just applied for a national bank charter.

🚨34% of ETH transactions now involve stablecoins, driving network activity near all-time highs pic.twitter.com/iTWBCHZT6b

— matthew sigel, recovering CFA (@matthew_sigel) June 30, 2025

While much of the early blockchain utopian ideals speculated that commerce may be transacted with bitcoin, using the rails to transact in dollars may be a much more near-term and universally accepted method.

Texas Commercial Sales-Based Financing Bill Gets Last Minute ACH Ban Amendment

May 27, 2025The Commercial Sales-Based Financing bill that passed through the Texas House of Representatives two weeks ago has now also passed through the Senate, but with a rather controversial amendment. In the Senate version, passed yesterday, and viewable on the right hand side of this document, sales-based financing providers would not be allowed to automatically debit a merchant’s account unless they have a “validly perfected security interest in the recipient’s account under Chapter 9, Business & Commerce Code, with a first priority against the claims of all other persons.” That means any sales-based funding (like an MCA or revenue-based financing loan) would be prohibited from debiting merchants automatically unless they were in true first position. And not just a first position MCA, but first position on all arrangements the merchant has altogether. AND it would have to be perfected in accordance with this statute.

The Senate Amendment:

CERTAIN AUTOMATIC DEBITS PROHIBITED.

A provider or commercial sales-based financing broker may not establish a mechanism for automatically debiting a recipient’s deposit account unless the provider or broker holds a validly perfected security interest in the recipient’s account under Chapter 9, Business & Commerce Code, with a first priority against the claims of all other persons.

Since the main difference between what the Senate and House passed is that one sentence prohibiting automatic debits, they have until June 2nd to decide which version of the passed bill is final.

Sales-based financing is broad. While the term encompasses sales-based purchase transactions (MCAs), firms like Walmart and PayPal engage in loan-based sales-based financing. Both firms, for example, are registered sales-based financing providers in the state of Virginia.

The Texas Senate amendment language is new. It does not resemble anything passed in a state commercial financing disclosure law to date.

An estimated 10% of all sales-based financing in the US takes place with Texas-based businesses.

The Largest Sales-Based Financing Providers

May 27, 2025Who are some of the largest sales-based financing providers in the US? The following companies are repaid as a percentage of sales or revenue, in which the payment amount may increase or decrease according to the volume of sales made or revenue received by the recipient:

| Sales-Based Financing Providers |

| Square |

| PayPal |

| Amazon (via Parafin) |

| Walmart (via Parafin) |

| Shopify |

| Intuit |

| Stripe |

| DoorDash (via Parafin) |

The State of Washington has also recently announced it will be offering sales-based financing through a Department of Commerce initiative.

Among those listed above, Square recently published a White Paper on the impact of its sales-based financing.

“Square Loans has opened credit to populations who traditionally have had less access to business loans. As of the third quarter of 2024, approximately 58% of Square Loan customers are women-owned businesses, compared to the industry average of 19%.38 And 15% of Square Loans go to Black/African-owned businesses compared to an industry average of 6.6%, while 14% of loans go to Hispanic/Latinx-owned businesses compared to the industry average of 11.3%.”