The Bad Broker And Merchant Due Diligence

November 15, 2017 There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

AltFinanceDaily was contacted by a victim of the fraud, Noah Grayson, managing director and founder of Encino, Calif.-based South End Capital. Grayson said the real victims are the merchants who get taken advantage of by these scams. In this case it was a New York-based small business owner who took on too many MCAs.

Grayson is quick to point out the MCAs were not at fault and each may have even thought they were the first position funder since it all unfolded so quickly. “They’re just trying to do business and provide financing to businesses, and they got burned as well. They’re going to take some degree of financial loss because of this and maybe more,” Grayson said.

False Pretenses

When Grayson reviewed an email that he received from the borrower, which included a copy of the LOI, he knew immediately that it was fraudulent and the borrower had been misled. “It was a fraudulent LOI and we had no record of the borrower or the brokers who provided it in our system,” Grayson exclaimed.

As it turns out, the borrower was tricked by the fake LOI that sought to leverage the reputation of South End Capital’s brand to coerce him into taking out $260,000 of MCAs from four separate funders. They did it under the false pretense that South End Capital would then consolidate those positions in 10 days and extend as much as $900,000 more in working capital to grow the business.

To be clear, South End Capital does offer a genuine MCA consolidation loan program. Grayson had never agreed to consolidate the business owner’s MCA positions, however, or provide an additional $900,000. That part was fabricated. This left the merchant holding the bag for more than a quarter of a million dollars in MCAs, placing his business, which has been successful since the 1960s, on the brink of bankruptcy protection in the interim because of the crippling weekly payments.

Fraud Prevention

Andi McNeal, research director at the Association of Certified Fraud Examiners, or ACFE, said she has seen this before, only on the consumer side of the industry. “Loan consolidation fraud for credit card debt is very common in the consumer space, and it’s not surprising to know that similar schemes are popping up in the small business space, too,” she said.

She went onto explain that because a small business is typically run by a small management team who typically aren’t trained in fraud prevention, they often adopt the same mindset as they do in personal finances. They don’t always have the necessary checks and balances in place, which can place them at risk of being victimized by such schemes.

“Sometimes they’re not savvy enough to detect those types of scams coming at them,” she noted. “Certainly, big businesses can fall prey to this, but it’s less common.”

Staying on Defense

The recent saga unfolded over a period of six weeks. Meanwhile Grayson has outlined some red flags for small businesses to watch out for to prevent becoming the next victim to a new fraud.

“If what you’re being told seems suspicious or doesn’t make sense, question it. Ask questions and get more information,” said Grayson.

Another rule of thumb is to stick to the document in front of them. Again, this may just be a case of a few bad apples spoiling the bunch, but sometimes brokers tell small businesses something contrary to what appears in front of them on the official document. “The LOI spells it out,” said Grayson, adding that when in doubt the borrower should defer to the document.

The merchant should also take it upon themselves to call the lender whose name is on the LOI to verify its authenticity before signing it or providing any upfront fees.

“In this case, it was a fraudulent document and it didn’t help out the borrower but calling us to confirm it initially would have. Most of the time, looking at what’s written out on paper from the verified source will help and getting a verbal or email confirmation from the actual lender, certainly will,” Grayson said.

Another defensive step merchants can take is to simply review the website of the brokers and funders and look for names, press releases and past closings, details which Grayson noted were all missing from the broker in question’s site.

“Anybody can say they make loans and provide financing. They could tomorrow put up a website for a couple bucks and say they’re a lender and start taking applications. But just because there’s a website doesn’t mean they’re legitimate,” Grayson said.

He’s suggesting merchants check out the names of the principals and employees on the site. Google is their friend to check for any history of loans closing. Look for closing announcements and any complaints tied to the entity in question. Call the Secretary of State Department and inquire about any complaints.

At the end of the day, it comes down to the merchant doing their homework. “A lot is on him. He should have done more research, absolutely. But anybody can be coerced or tricked if the right things are said,” said Grayson.

If a merchant does find themselves in a situation where they fall victim to a fraud, there are steps they should take. McNeal said that while each situation is unique, a good first step is always going to be to reach out to a trusted legal counsel.

“They can help guide you through the process of what the options are. Do you have recourse? Does the situation call for insurance to help cover the losses? They also can advise on which law enforcement or government agencies are the most helpful – should the case be referred to the local authorities or do they need to bring in the FBI,” the ACFE’s McNeal advised.

More Pervasive

Grayson’s fear is that this is not an isolated incident. He has reason to be cynical, as this was the second incident this year resembling the most recent situation that they have experienced.

The first incident was relayed to South End Capital by a handful of borrowers about one specific MCA broker. No fraudulent documents were ever recovered, but the borrowers recalled the harrowing details of the incident

“Per the multiple borrowers, the broker used our real LOIs and lied to borrowers about how to interpret them to coerce tens of thousands of dollars in upfront fees from them. For example, for an LOI we issued for our SBA loan program that listed what SBA guarantee fees would be due at closing, he would convince them that that fee was his and they needed to pay it to him upfront to proceed,” Grayson explained.

The small business owner at the center of the scandal declined to comment, and it’s unclear whether they were the one to initiate the original communication with the broker or vice versa.

Lights, Camera, Crypto-Transaction – How a Lending Journalist Raised Millions to Build Magic Lamps Through the Murky World of Initial Coin Offerings

November 15, 2017

This past July, the winner of the Best Journalist Coverage category at the 2017 LendIt Conference Awards, announced that he would be stepping outside of his journalistic endeavors to raise money for a futuristic lamp company. The product, dubbed Lampix, is described as a lamp with a projector, a camera, specifically placed light-emitting diodes (LEDs), and a cloud-enabled computer. On the company’s “Medium” blog, Lampix promises that the product is “designed to transform any flat horizontal surface into an interactive computer.”

The man behind Lampix, George Popescu (whose Lending Times news site competed against and beat out fellow finalist AltFinanceDaily at the LendIt Awards), makes for an interesting case study in alternative finance. That’s because Lampix shunned traditional capital-raising methods by relying on an Initial Coin Offering (or ICO), an unregulated blockchain-based corporate event which is similar to an initial public offering. Rather than purchasing shares, as is the case in an IPO, investors in an ICO receive digital tokens instead of shares. In August, Lampix raised $14.2 million through its ICO*.

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

In case details published by the UK’s Insolvency Service on August 1st, the agency announced that Popescu was disqualified from serving as a company director.

Mr Popescu breached his fiduciary duties to act in the best interest of Boston Prime Limited (“Boston Prime”) and/or failed to ensure that both Boston Prime, as the regulated firm, and him individually, as the approved person, complied with the Financial Conduct Authority (“the FCA”) rules and guidance.

$6.2 million was transferred out of the company to a company named FXDD. Boston Prime’s receiver is presently suing FXDD seeking the return of the funds to the company. Proceedings are ongoing. Mr. Popescu is not under investigation and there are no legal proceedings at this time against Mr. Popescu.

It’s an inauspicious beginning for someone financing the “lamp of the future” using an unregulated and controversial strategy. Even so, when its ICO concluded on August 19, Lampix declared its gambit a success after raising $14.2 million through the sale of its digital tokens, which are known as PIX.**

By mid-November, the market value of those digital tokens, which exist on the Ethereum blockchain, had dropped by 50%, causing Lampix investors to suffer losses of $7 million. Unlike shareholders in publicly traded companies, token buyers have few investor protections. It’s not clear they are even considered to be actual investors at all. Buried in the fine print of Lampix’s 85-page “white paper” – a convenient way to avoid the label of prospectus – is a disclaimer. “Buyer should not participate in the [PIX] Token Distribution or purchase [PIX] Tokens for investment purposes. [PIX] Tokens are not designed for investment purposes and should not be considered as a type of investment.”

Additional disclaimers, moreover, declare that the white paper is not a prospectus, that the tokens “are not securities, commodities, swaps on either securities or commodities, or a financial instrument of any kind.”

But the distinction has not deterred people from joining in the frenzy of buying digital tokens like PIX. So much so, TechCrunch reports companies employing this strategy had raised nearly $800 million by means of ICOs in the first half of 2017.

And the SEC is not exactly excited about ICOs. “Fraudsters often use innovations and new technologies to perpetrate fraudulent investment schemes,” a July 29 directive by the SEC states. “Fraudsters may entice investors by touting an ICO investment ‘opportunity’ as a way to get into this cutting-edge space, promising or guaranteeing high investment returns. Investors should always be suspicious of jargon-laden pitches, hard sells, and promises of outsized returns. Also, it is relatively easy for anyone to use blockchain technology to create an ICO that looks impressive, even though it might actually be a scam.”

On September 29, moreover, the SEC brought an enforcement action against REcoin Group, charging Los Angeles businessman Maksim Zaslavskiy and two companies he controls with defrauding investors “in a pair of so-called initial coin offerings (ICOs) purportedly backed by investments in real estate and diamonds,” an SEC press release said.

The SEC alleges that Zaslavskiy and his companies –REcoin Group Foundation and DRC World (also known as Diamond Reserve Club) — have been selling unregistered securities, and that “the digital tokens or coins being peddled don’t really exist.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Deborah Meshulam, a partner in the Washington office of law firm DLA Piper and a former SEC enforcement official, told AltFinanceDaily: “Regarding the lack of equity ownership, Lampix is seeking to establish that the tokens are not securities. Whether the SEC would agree should it decide to look into the offering depends on the facts and circumstances. The SEC staff would look past form to substance to assess whether the sale of the tokens constitutes an investment contract under legal standards. If so, then the SEC would view the Lampix offering as a securities offering. It may be that Lampix (or its lawyers) already vetted the offering with the SEC but I don’t know the answer.”

Popescu tells AltFinanceDaily in an e-mail interview, “We had to respect all securities rules and regulations of course, respect the Howey test and so on. There were no hoops to jump through as we are not trying to avoid anything or prevent anything. We honestly built a token to build a community to help us crowdsource (mine) pictures for all applications among which, Lampix.”

“Each PIX token,” the Lampix website explains, “will be used as a form of payment to picture image miners, voters and app developers or to purchase a Lampix, cloud computing and apps.”

Meshulam also notes that the June, 2017, date of the Lampix white paper pre-dates the SEC’s enforcement activity in this area. She adds, “The statement that ‘token sales or ICOs are not currently regulated by the U.S. Securities and Exchange Commission may be very literal in the sense that there is not a specific regulation, but the SEC has stated that, in the right situation, ICOs are subject to the US federal securities laws.”

Erin Fonte, an attorney in the Austin, Texas, office of Dykema Cox, and the leader of the firm’s regulatory & compliance group, says, “The ICO stuff is so up-in-the-air. The SEC is looking at it closely. But it’s fairly new. And some of them (ICO’s) have been tied to fraud and Ponzi schemes. If a client came to us (seeking advice), we’d want to vet the people behind the offering.”

But what of Lampix, the company that won the Augmented and Virtual Reality category of the South by Southwest (SXSW) Accelerator Pitch Event earlier this year in March – and put a pretty feather in the cap of Popescu?

Popescu’s resume is no doubt impressive. He holds a trio of master’s degrees in various scientific and technological disciplines, including one from Massachusetts Institute of Technology. And he is a serial entrepreneur who lays claim to having founded 10 companies: they include, according to his LinkedIn profile, online lending, a craft beer brewery, an exotic sports car-rental space, a hedge fund, a peer-reviewed scientific journal, and a venture-debt fund.

He’s charmed journalists like Forbes contributor Roger Aitken, who declared: “The founders (of Lampix)…believe that Lampix will impact humans as much as computers or smart phones in the future…Think Tom Cruise in Minority Report. Imagine your room in five years: you will be able to use any surface around you as if it was a computer. The ability to transform any surface into an interactive computer (augmented reality) is going to unleash applications we have not even conceived of.”

The Lampix website hyped its ICO with the aid of an infographic listing “active product inquiries” the company has in its pipeline, the likes of which includes Amazon, Apple, Samsung, Microsoft, Sony, IBM, BMW, Bloomberg, PwC, and the Aspen Institute. With all of these names seemingly lining up, it begs the question: Why did Lampix choose the controversial route of an ICO to raise capital?

But it’s hard to determine the seriousness of these corporate relationships. Florin Mihoc, Lampix’s Strategic Partnerships & Development Advisor, said he could not assist us with confirming any of them, citing the slow and cumbersome bureaucracy of dealing with Fortune 500 companies. He did invite us to try reaching out to some of them on our own, which we did.

Bloomberg is one of the few acknowledging a relationship with Popescu’s company. Chaim Haas, head of innovative communication at Bloomberg, told AltFinanceDaily that the New York-based media and financial communications company “collaborated” with Lampix. Bloomberg, he says, “has used Lampix hardware in its fellowship program (Bloomberg AR Fellows) as a prototype for augmented reality applications.” But Haas declined to elaborate on whether Bloomberg’s relationship with Lampix was more than an experimental one.

Edward Caldwell, director of public relations for East Coast markets and sectors at Pricewaterhouse Coopers, the Big Four accounting firm, declined to comment about Lampix. “We can’t discuss individual companies, clients or engagements,” he reports.

Douglas Farrar, senior manager for communications and public affairs at the Aspen Institute, told AltFinanceDaily that he could find no business relationship between Aspen and Lampix. “I have gone down quite a few rabbit holes here,” he said in an e-mail, “But I’m coming up empty.”

When Popescu was directly confronted about this, he wrote, “The companies would only figure [in the infographic] if they actually themselves reached out to us and we exchanged emails with somebody from that entity. Most of these entities have many people and most of the companies’ people will have no idea [that] somebody else in the company is talking to us.”

Telephone calls and e-mail requests for comment to Microsoft were not returned.

A spokesperson using BMW of USA’s official twitter account, however, responded to an inquiry by saying they were a customer of Lampix, “but only for office usage.”

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Balina asked Popescu the softball question, could he show viewers a demonstration of the product? Popescu admitted he wasn’t prepared to do that and when he attempted to set one up on the fly, it didn’t work. The incident is notable because Lampix has been promoting the video through its social media network.

Popescu corroborates a number of details about the ICO, however. He confirmed the ICO price of a PIX token to be 12 cents, the US dollar price people had to pay per token. Cryptocurrency exchanges, where token speculators can buy and sell tokens online, show the trading value of a PIX token currently hovering around 6 cents, which translates into roughly a 50% loss in value.

Investors feeling hurt by such a loss can’t contest the purchase of PIX tokens with their credit card issuers. That’s because of a requirement that token sales had to be purchased with ether (ETH), the currency of the Ethereum blockchain. While ether is arguably similar to Bitcoin, it operates on an entirely different blockchain.

To participate in the ICO, in a Youtube video, Lampix also explained to purchasers, for example, how they could first buy ether with dollars through an online exchange known as Coinbase** before forwarding the ether to a digital wallet. Next, investors were instructed to send the ether from the digital wallet to a specially designated PIX address. An automated “smart contract” would then release the appropriate amount of tokens to the buyers’ digital wallets 31 days after the ICO was consummated.

It’s a byzantine procedure. And for investors – especially for those who are not exactly tech-savvy – the rigmarole makes it nearly impossible for them to recover their money should they feel buyer’s remorse. Neither the video nor the Lampix white paper mentions any buyer restrictions. Indeed, Lampix’s white paper specifies that “anyone” in the global market can participate. That means that an investor could theoretically be underage or a citizen of Iran or North Korea. (When asked what steps Lampix took with regards to KYC/AML, Popescu said, we “implemented the standard ones with partners specialized in it.”) Investors could even be citizens of the UK where Popescu is banned from being a company director.

And global they are. AltFinanceDaily interviewed Rudy (whose last name we are withholding), a graduate student who lives in Singapore that says he bought approximately $2,200 worth of PIX tokens during the ICO. The drop in value has gotten him so frustrated that he’s contacted securities regulators in the United States to investigate Lampix. Despite the caveat in the white paper that tokens are not an investment and should not be used for investment purposes, Rudy said he considered himself to be an “investor” and that his reason for buying the tokens was to sell them in the future for a profit.

Popescu, who wasn’t asked about Rudy’s experience specifically, told AltFinanceDaily that Lampix is not selling PIX tokens as an investment but rather to primarily build a community. “What people do with the tokens is their choice and we cannot prevent them,” he asserted.

English is not his first language but Rudy said, “I think that [the] SEC should regulate ICOs in the USA. There are no rules currently, teams can promise anything before the ICO and forget everything after the ICO. Things have to change, there should be legal pressure on crypto teams.”

Rudy added that he was “so enchanted” by Lampix’s ideas that he had promised himself not to sell the tokens for at least two years even if they were losing value. He conceded that he was not a tech expert. But, he says, the award at the SXSW competition was an important milepost to him.

AltFinanceDaily found 700 more people interested in Lampix on the company’s official Telegram channel. The chat history since September 20, which we were able to obtain, has been dominated by talk of the PIX token’s trading value. Those bemoaning the low price regularly use the term “investors” to describe themselves – never mind that the white paper specifies that PIX tokens are not supposed to be an investment or to be used for investment purposes.

The chat’s administrator, who uses the nickname Chester, identifies himself as a “community manager” at Lampix. At one point he too refers to PIX holders as investors. “Hey guys,” he wrote in the channel on October 1, “Lampix is a company, not a single person, we don’t do things that quick, but pretty quick and we try not to confuse our investors by telling you unconfirmed news. Be patient, things will be just fine.”

Laura Toma, another community manager for Lampix, responded to complaints about the depressed price in the channel by saying, “The issue is that people want to get rich in a month.”

Indeed, investors hound not only the community managers, but also Popescu himself, who frequently joins in on the chat and fields questions about the trading price of PIX. “You should care more about the company revenue, clients, users.” Popescu replied to one user.

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

Others keep the faith. “PIX will be the real Aladdin’s magic lamp,” writes one user. Another hyperbolically predicts the price will “fly out of the earth, fly to the moon, and finally fly out of the galaxy.”

There is very little discussion about the use of the product itself while numerous inquiries are written in Mandarin. “Lampix has a lot of Chinese investors,” writes one. Other users self-identified as citizens of Russia, Romania, and France. Meanwhile, Toma writes, “Yes, there are investors from USA as well.”

Despite the losses that investors have so far experienced with Lampix, among other concerns, Popescu isn’t limiting himself to just one ICO. According to his online statements, Popescu is connected as an “advisor” to another company engaged in an ICO. AirFox, a Boston-based start-up launched by two Google alumni, provides free data to mobile phone users in return for eyeballing advertising. In early October, Airfox’s ICO raised $15 million. But a month later its AIR tokens, which sold for two cents apiece during the ICO, had lost 75% of their trading value. That means investors in AIR, the company’s ICO ticker symbol (which is becoming an increasingly ironic moniker) have seen more than $11 million go up in smoke almost overnight.

Popescu says in their defense, “The AIR tokens are meant to solve a real problem, of remunerating people who watch ads in exchange of getting more data and minutes on their mobile phone. The ecosystem is still being worked upon, the product is not live. Once the ecosystem is live we will see what really happens. Until then the token is mostly being handled by speculators. The price can therefore vary widely and it doesn’t reflect their true value.”

Even as Lampix and AirFox have been racking up massive losses for investors, Popescu announced on November 5 in a LinkedIn post that he would be involved in five more ICOs.

Among them is DropDeck Technologies, at which Popescu is listed as the chair of the advisor board; its ICO is scheduled for November 21. Another company, Factury, for which he is listed as an advisor, is initiating its ICO on December 15.

He’s an ambitious man.

And his ICO familiarity hasn’t escaped the scrutiny of PIX investors. “I find it strange that you are directing 5 other ICOs,” writes one user in the Telegram chat on November 4. “To make Lampix big, this will require a CEO [who is working] full time working on the project.”

Popescu responds personally. “I am working full time on the project but people have asked me to advise on their ICOs and this grows Lampix’s notoriety a lot in the crypto space,” he writes. He offered further assurances that he wouldn’t be advising those companies’ projects beyond their ICOs.

In an email to AltFinanceDaily, he writes, “I run right now Lending Times, Lampix and Block X Bank only. The ICOs are just customers of Block X Bank. I have built about a dozen companies in 9 years, sold a few, closed a few. Each company has a team to help me, I am not doing this alone. For the ICOs I am more or less involved as an advisor / helping them project-manage their ICOs. How to run 3 companies? It’s about being effective, organized, delegating, partnering and being productive. Oh and I don’t watch TV, so maybe I have a few more hours per day than the average person. I do work long hours.”

Block X Bank, through which Popescu extends his efforts toward other ICOs, is described on the company website as “a boutique investment consulting company specializing in connecting blockchain projects with funding.”

In all of these ICOs, money is seemingly being created out of thin air. A consultant who was hired by AltFinanceDaily to help analyze the technical aspects of both ICOs and smart contracts determined that Lampix raised much more than just the $14.2 million in token sales. In addition to the 114 million PIX tokens sold to investors, our consultant explained, the company also issued 220 million tokens to itself. At the ICO price of 12 cents apiece, those tokens would theoretically be worth $26.4 million – a huge piece of the total ICO pie that Lampix could sell on cryptocurrency exchanges if it wanted to rake in even more money.

There’s a kicker too. At scheduled intervals over the next four years, the smart contract that made PIX tokens possible in the first place is slated to automatically create – and allocate – 330 million new tokens to Lampix. Thus, when Lampix raised $14.2 million in August, the company reserved $66 million worth of PIX tokens for their corporate use.

Popescu said in his e-mail to AltFinanceDaily that these company tokens are for “corporate usage like employee incentives, M&A, other company investments…etc.”

It’s a mind-boggling sum of money for the development of a futuristic lamp whose followers mostly seem to reside on internet chats like Telegram, reddit, and bitcointalk.org.

And this has occurred despite the company’s withholding any information regarding Popescu’s status in the UK. Balina, who interviewed Popescu on Youtube, told AltFinanceDaily he wished he had known about his disqualification in the UK. “This is definitely a big issue and I wish I would have known about it so that either my audience or I could have asked him this directly on the live stream,” he said.

AltFinanceDaily asked Paul Savchuk, Co-founder, CEO, and Chief Product Officer at Cryptocurrency Capital LLC, a US-based hedge fund that only invests in utility tokens as commodities, if Popescu’s ban in the UK would have been relevant information in the Lampix ICO. “Yes, that might be a red flag for us in some cases and require us to perform additional research,” he wrote in an emailed response. “We look at management very seriously – especially since a lot of projects are treated like startups and management is a key component to whether or not many of these ICOs can make it. We try to find such events and spot red flags whenever we conduct our due diligence research on ICOs. The reason: each project has something that needs to be improved. ‘Red flag’ – sometimes conversely can lead to a great opportunity when other market participants ignored it or were too skeptical.”

Mr. Savchuk further said, “Lampix is a perfect example of a coin that on the surface looks very promising, but when you dig a little deeper, you do find red flags that can dampen the excitement for this investment.”

And yet Savchuk spoke rather positively of the Lampix product after reading their white paper. “We believe the project is looking to change the current AR/VR tech industry,” he said, referring to augmented reality/virtual reality. “The project is promising for two reasons. First, they have multiple companies in their pipeline. Second, they have a legitimate product which they will manufacture and sell. They are one of the few blockchain products to offer a tangible product with the ability to disrupt the market.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

With regard to the price drop, Savchuk said, “This is a danger for all purchasers of ICOs. Sometimes it’s caused by token purchasers (swayed by) fear and greed and (hoping for) easy money and fast money. I doubt somebody sold Apple Inc.’s stock right after its IPO. It is also very difficult to restrict exchanges from allowing massive pump and dumps. That’s not even mentioning the difficulty of measuring the value of tokens,” Savchuk concluded. “Consequently, such projects are struggling with low credibility. However, it also creates a possibility for those who believe in the idea and product on a long-term run.”

Popescu downplays the significance of the UK issue. The root of the debacle, he says, is the result of Boston Prime – the company he previously ran – being forced into bankruptcy by the actions of a company he is now suing called FXDD. “FXDD bought the companies and then bankrupted them and that’s why Boston Prime [went bankrupt],” he writes. “Myself personally and each company separately are suing FXDD for this. UK has archaic laws where if you are a director of a bankrupted company you get disqualified from being a director again for a time. Attorneys charge about 40,000 GBP to defend this automatic case and I weighed the pros and cons and decided to ignore it as I have no plans to be a director in the UK for time being.”

Investors unhappy with underperforming ICOs may be willing to challenge their legality. On October 25, for example, a class action lawsuit was filed against Tezos, a computer networking project that raised $232 million in one of the largest ICOs ever. In a complaint, the lead plaintiff alleges that, among other things, Tezos unlawfully engaged in the unregistered offer and sale of securities and fraud in the offer or sale of securities. “In July 2017, Defendants conducted an ICO in which they sold 607,489,040.89 tokens (dubbed ‘Tezzies’ or ‘XTZ’) in exchange for digital currency worth approximately $232 million at the time,” the complaint reads. The plaintiff, who purchased 5,000 Tezzies, feels he was misled about the company and the offering.

Internal squabbling at Tezos which has delayed the release of its product and the sheer amount of money at stake have put the company on the map with the mainstream media and business press. The New York Times, Wall Street Journal, and Fortune as well as news services Reuters and Bloomberg have all covered the allegations of fraud.

The day before the class action lawsuit was filed, moreover, a AltFinanceDaily reporter attended an explosive session at Money2020 in Las Vegas that saw Tezos co-founders, Arthur and Kathleen Breitman, attempting to give a status report of the company. A crowd that had gathered outside prior to the doors opening had attendees speculating whether the Breitmans “would actually show their faces” in the midst of all the drama.

To date, no lawsuits have been filed against Lampix despite the drop in the token’s value.

At a cryptocurrency/ICO meetup in NYC in October, a AltFinanceDaily reporter met with executives at one company preparing an ICO who said they would not allow American investors to participate because of securities-enforcement fears. Pressure is mounting in the Far East as well. Citing their illegality, Chinese regulators in September issued a blanket cease-and-desist order on all ICOs in their country. What that means for Lampix’s Chinese investors bears watching.

Popescu says that Lampix supports regulation in China. “Of course, all Chinese people have to follow Chinese regulation,” he writes.

Meanwhile, on the product front, Popescu says that right now a Lampix lamp can be purchased for $10,000, a tidy sum because they must be hand-made. “We plan to improve the manufacturing costs and then we’re planning to do a kickstarter early next year for around $500 [per] Lampix,” Popescu told AltFinanceDaily in his e-mail interview.

But for investors, it always comes back to the trading value of PIX. On October 25, one investor asks Popescu if the company will buy back its own PIX tokens at the ICO price to pump up their market price. “If you want a pump and dump please go to other companies,” Popescu responds. “We are here for 5-10 years to build a $100 billion dollar company and compete with Apple.”

And it all began with an ICO.

“ICOs also help with bootstrapping the user base – breaking the chicken and egg problem,” Popescu also explains in his e-mail to AltFinanceDaily. “In addition, given that Lampix is looking to crowdsource images, we prefer many different people hold PIX tokens rather than 2-3 VC funds. And last but not least I think tokens are better rewards for the community (liquid, mark to market, etc.) than illiquid instruments.”

Not everyone agrees that PIX is the most liquid instrument to grow the community. US Dollars come to mind, for example. “Let’s say I’m a customer,” one investor poses to Chester, a Lampix community manager. “I want to use the cloud computing service but then I see I have to pay with PIX. I have no experience in crypto and have no idea how to do that. I just want to use your service fast and don’t want to buy PIX coins first before I can make use of it. Will there be a fiat option?”

Chester is awed by the idea. “Well, you are so professional,” he writes. “Man, you are good. You are good, the question you threw just hit the spot seriously. I guess there is always something Lampix needs to figure out and choose the best solution. Technically speaking they are jolly good at this point, but it doesn’t mean it’s perfect.”

Chester, who assures him that he isn’t being sarcastic, goes on to refer to the investor who asked that fairly elementary question as a “big shark” that is “born to bite.”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

The responses fly in:

“Buying my Lambo”

“Travel to Paris”

“Buy an island”

“Buy my mum her dream home”

“Quit my job and start up something for me”

“Pay off mortgage and be financially free”

“Buy house in Miami, buy Lambo, enjoy life”

“Retire”

“Easy. Buy more crypto”

Meanwhile on Telegram, where investors continue to engage Lampix management on a daily basis, Dante offers a sobering reminder of what they’ve bought into, “We don’t have equity, we only have tokens,” he writes. “And we are taking a big risk.”

* The amount of tokens sold multiplied by the 12 cent ICO price doesn’t exactly match the dollar amount Lampix says they had raised. That’s because Lampix not only issued bonus tokens to buyers at each stage of their ICO but also because the market value of ether, which users had to convert to from dollars to buy PIX, had fluctuated when they reported how much they raised. Like Bitcoin, the value of ether is volatile.

** The smart contract Lampix wrote to launch Lampix’s tokens into existence specifically named them PIX tokens and dubbed their publicly identifiable symbol to be PIX.

*** Coinbase is a respected digital currency wallet platform based in San Francisco.

CFC on the Front Lines of the MCA Regulation Battle

November 6, 2017

As the US Senate attempts to reach a bipartisan agreement on relaxing some of the rules in the Dodd Frank legislation of 2010 that would treat banks more favorably, the MCA industry is having to fend off legislation and regulation of its own at the state and federal levels that could position funders in a similarly crippling position.

MCA regulation has been thrust into the spotlight for a number of reasons, not the least of which has been the Consumer Financial Production Bureau (CFPB). The CFPB is moving forward with the Dodd-Frank Section 1071 rulemaking process for data collection regarding small business lending, a sector of the market for which they do not have jurisdiction, sources say.

Front and center in the policy discussions has been the Commercial Finance Coalition (CFC), a merchant cash advance trade association that is coming up on its two-year anniversary in December. While federal policymakers appear to be listening, state legislatures have been a more difficult nut to crack.

The CFC’s Influence

In its short two-year history, the CFC has been one of the most vocal if not the most influential trade organization lobbying on behalf of the MCA industry, having attended 70 congressional meetings and having led advocacy efforts for the industry in the halls of Albany, Sacramento, Illinois and Washington, D.C.

Dan Gans, executive director of the CFC, has been the voice of the MCA industry on Capitol Hill and has been invited to testify in key congressional hearings. “For whatever reason, the CFC has really become the voice and has taken an active part in the so far successful advocacy efforts to educate and mitigate potential harm to our members’ ability to deploy capital to small businesses that need access,” Gans told AltFinanceDaily.

Most recently the CFC participated in a fly-in, one of two such events this year, to Washington, D.C. in which the association’s counsel Katherine Fisher of Hudson Cook, LLP testified.

In her testimony Fisher said: “The MCA and commercial lending spaces are sufficiently regulated by existing federal and state laws and regulations. Both MCA companies and commercial lenders must comply with laws and regulations affecting nearly every aspect of their transactions, from marketing and underwriting through servicing and collection.”

She went on to explain: “Even if they comply with every applicable law and regulation, small business financers must also be wary of the Federal Trade Commission’s powerful authority to prevent unfair or deceptive acts or practices.”

Fisher told AltFinanceDaily she received a “positive” response to her testimony from funders but has not heard anything from lawmakers.

Gans said Fisher did a fantastic job in articulating the needs and status of the industry.

“She presented a very good case as to why the industry is currently adequately regulated. We don’t feel there is a need for federal regulation. In some cases, less regulation would allow our members to deploy more capital and help more small businesses,” Gans said.

The sweet spot for MCAs, Gans explained, are transactions under $100,000 and probably in the $24,000 – $40,000 range. He said the industry does a fantastic job of being able to deploy financial resources to small businesses in a timely manner that neither banks nor SBA lenders can match. He’s not suggesting MCA is for everybody but for some businesses it’s an essential product that can help. There have been many success stories.

“Competition is all over the place. But that’s great for the merchant. The more options that merchants have, the more we can enforce best practices and more competitive rates. And the more we can keep the government from impeding people from getting into this space, the better off small businesses are going to be,” said Gans.

Setting the Record Straight

The CFC was formed with the mindset that the organization, which is currently comprised of CEOs of small- and medium-sized funders, would take a proactive rather than a reactive approach to industry regulation. In its two-year history the CFC has tasked itself not only with educating policymakers on the role of MCA funders for small businesses but also with undoing the misinformation and misconception surrounding the anatomy of an MCA.

“Unfortunately, because MCA uses the term cash advance in its product name, uninformed people will often confuse MCA as some form of payday lending. And so that has been one of our biggest challenges, educating members of congress and committees that there is absolutely no correlation between MCA products and what their views of consumer payday loans is,” said Gans, adding that the CFC has had to communicate that MCA is a version of factoring has been around for more than 1,000 years.

A common thread that the CFC has been able to weave with lawmakers has been the diverse geographical representation of both the trade group and the House and Senate.

“Most venture capital is deployed in a few spots – New York, California and Texas – and it’s a cliff to get to those three states. So, one nice thing that I take pride in is my members are looking all around the country regardless of the geographic location. That helps us with policymakers, most of whom are not from the New York City metropolitan area or Silicon Valley. It’s nice being able to look at them in the eye and tell them we care just as much about your district as you do,” he said.

The Road Ahead

The CFC has an ambitious long-term agenda, one that includes raising their profile in the industry and participating in events.

“I think one of the ambitions we have is to have an organization where funders and brokers can be at the same table and work though some of the issues impacting the industry and try to make sure people are doing things in the right and best way.”

The trade group is planning to partner up with AltFinanceDaily for Broker Fair 2018 and they’re looking to bolster membership.

“The industry has had a lot of free riders that are benefiting from our advocacy efforts but not supporting it. So, from my perspective, if you’re in this industry, particularly in the MCA space, we’d like to expand membership. If we grow our membership, we can do more things, engage more states and expand our lobbying team,” said Gans. “The more members we have, the more we can do to advance the ball and protect the interests of the industry.”

The CFC will need all the help it can muster given the fight ahead to fend off regulation particularly in Washington, Albany and Sacramento. “I think we could see some harmful regulations and potentially legislation over time. Some of those bad ideas that emanate in states have a tendency to percolate into Washington. If at some point there is a less business-friendly administration in the future, we could see all those ideas get some traction at the federal level,” Gans warned.

6th Avenue Capital Secures $60 Million Commitment For Merchant Cash Advance Funding

November 2, 2017Highly Experienced Executive Team Offers Flexible Financing Options to Small Businesses

New York City – November 2, 2017 – 6th Avenue Capital, LLC (“6th Avenue Capital”), a leading provider of small business financing solutions, announced today its securement of a $60 million commitment from a large institutional investor. The investor made their commitment based on 6th Avenue Capital’s industry-leading underwriting, compliance standards and processes. 6th Avenue Capital will draw from this commitment to offer merchant cash advances to small businesses through its nationwide network of Independent Sales Organizations (“ISOs”) and other strategic partnerships, such as banks and small business associations.

6th Avenue Capital launched formal operations in 2016 to help finance small businesses that are often ineligible for funding due to traditional underwriting criteria. 6th Avenue Capital evaluates each application for funding individually and keeps the merchant’s short and long-term needs in mind including, most importantly, what they can afford. 6th Avenue Capital also understands that small businesses may need funding quickly. The company’s data-driven underwriting processes, expertise and technology can give the merchant secure and equitable approvals of qualified requests and funding within hours.

Leading the team, CEO Christine Chang oversees all strategic aspects of 6th Avenue Capital. She also serves as COO to sister company Nexlend Capital Management, LLC. She brings more than 20 years experience in institutional asset management, including alternative lending. Previously, Chang served as Chief Compliance Officer at Alternative Investment Management, LLC, COO at New York Private Bank & Trust and Vice President at Credit Suisse. She serves on the board of Blueprint Capital Advisors, LLC and Bottomless Closet, a not-for-profit empowering economic self-sufficiency in disadvantaged NYC women.

“Our mission at 6th Avenue Capital is to help small businesses grow, and we continue to expand our existing network of ISO and strategic partners to ensure these businesses have access to capital in hours,” said Chang. “Our leadership team of financial industry experts has extensive experience navigating multiple economic cycles. We know how to serve merchants and how to deliver quickly while meeting the highest operational standards for our investors.”

COO Darren Schulman joined the team in March 2017. Schulman is a 20-year veteran of the alternative finance and banking industries. He is responsible for oversight of 6th Avenue Capital’s origination, underwriting, operations and collections, as well as strategic initiatives. Schulman served previously as COO at Capify (formerly AmeriMerchant), a global small business financing company, and President and CFO at MRS Associates, a Business Process Outsourcing (BPO) company specializing in collections. In addition, Schulman was an Executive Vice President at MTB Bank.

“We form strong relationships with the merchant and consider it essential for our underwriters to speak to every merchant, on every deal, regardless of its size,” said Schulman. “We also make our underwriters available for discussions with ISOs whenever necessary. We are proud to offer competitive volume-based commissions, buyback rates and white label solutions.”

About 6th Avenue Capital, LLC

6th Avenue Capital is changing the small business financing landscape by offering a data-driven underwriting process and fast access to capital. The company employs a unique blend of industry experts and is committed to the highest operating standards, high touch merchant service, including a policy of direct merchant access to underwriters. 6th Avenue Capital is a sister company of Nexlend Capital Management, LLC, a fintech investment management firm founded in 2014 and focused on marketplace lending (consumer loans). For more information, visit www.6thavenuecapital.com.

# # #

LendUp May Have a Leg-up

November 1, 2017

AltFinanceDaily recently sat down with LendUp CEO Sasha Orloff and COO Vijesh Iyer at an auspicious time. The company, an online lender that provides consumers with alternatives to payday loans and credit cards, is uniquely positioned in the wake of the CFPB’s 1600+ page Payday loan rule that was issued in early October.

And that’s not exactly an accident. Orloff says the company was founded (5 years ago) with the expectation that the CFPB would issue an eventual rule. “At the time, we had no idea what it was going to be but I could imagine that if they were going to write a federal rule that it would completely change the industry,” he said.

Orloff’s journey, as he tells it, began by reading Banker to the Poor, which inspired him to move to rural Honduras nearly 15 years ago to help the Grameen Foundation, a non-profit that focuses on providing loans and education to the poorest of communities. He was only 21 at the time. After a three-year tour, he moved on to roles at The World Bank, Citi, and finally starting in 2012, LendUp.

When LendUp was being envisioned, he explains, the smart phone was making it possible for consumers to access financial services outside of what was in their neighborhood and bank technology was the last thing that was going to become modernized.

“The CFPB rule was going to make it harder for banks to work with underserved consumers,” he says. “So we said let’s start a financial services company that focuses exclusively on the people that have the least amount of options and let’s start reinventing [these] products one at a time.”

And with that, they consulted academics, educators, government officials, and people from the industry. “How do you give somebody credit in an emergency fashion that can change it from a trap into an opportunity? And so we did that and it turned out the rule looked really similar to what we did,” he explains.

“I think there’s a lot of things they got right [about the CFPB rule],” he says in regards to how to eliminate debt traps. LendUp, for example, doesn’t allow customers to roll over their loans, they have to pay off their loans in full before they can consider borrowing again. Rollovers were a big sticking point for the CFPB when they published their rule last month. Their official announcement on the matter had stated that “many borrowers end up repeatedly rolling over or refinancing their [payday] loans, each time racking up expensive new charges. More than four out of five payday loans are re-borrowed within a month, usually right when the loan is due or shortly thereafter. And nearly one-in-four initial payday loans are re-borrowed nine times or more, with the borrower paying far more in fees than they received in credit.”

One piece of the payday alternative puzzle is in the underwriting. COO Vijesh Iyer, an alumni of both Capital One and PayPal, says “we basically use a variety of data sources, both the traditional bureaus and as what we call the non-traditional bureaus.” For the credit card product, LendUp will pull credit from a traditional bureau. “For the small dollar loan product we use non-traditional CRAs,” he says. Their team of data scientists tries to extract the most significant signals out of all of the data sources they have at their disposal. “That’s really valuable when you’re dealing with a subprime customer where the reason why someone could be underserved or subprime is very different. We all have different life stories and we’re really trying to figure out the differences which we get from multiple signals, multiple data sources.”

“The easiest person to convince that we’re a better product is an existing payday user,” Orloff says. “because it’s slightly cheaper at the beginning, it gets much cheaper over time. It has a lot more flexibility. It gives people for the first time the opportunity to report to the credit bureaus. It teaches you better financial behavior. You can do it on a mobile phone. You can get alerts and reminders…”

Meanwhile, payday borrowers always have to pay the same amount, Orloff contends. The loan terms don’t improve, he says. One notable advantage a LendUp borrower might experience is that when they first run into trouble with making a LendUp loan payment, they can get a few extra days leeway at no extra charge, which usually comes as a welcome surprise.

Granted, a LendUp loan’s APR can still look pretty steep. A calculator on their website offers an example of one that is 458.86% APR. Orloff says a part of understanding that is understanding what a consumer’s options are and what the costs to process the applications are. A 220% APR might only equate to something like $30 total in fees depending on what the loan terms are, he explains. Their borrowers don’t get paid in APR though he says, they get paid in dollars. “They care about what’s the total cost of credit in terms of dollars.”

“Our customers pay more than that on overdraft fees,” Iyer adds. “Every time they have a slight overdraft, even if it’s for a dollar, even if it’s 10 cents. Even if it’s two dollars. No one ever tries to evaluate what the APR for that is. But that is their fee and this is also a fee.”

But more than anything else, it’s about whether the borrower’s and lender’s interests are aligned, Iyers contends. Right now, LendUp believes they’re doing the right thing at the right time.

—

This interview was conducted at Money2020 in Las Vegas

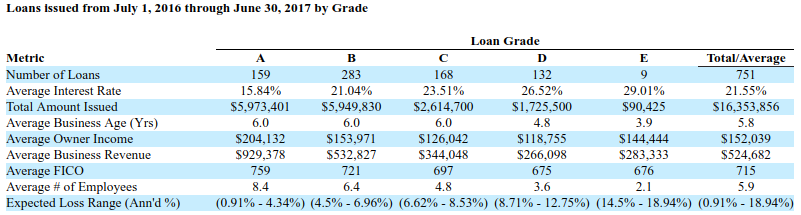

StreetShares Reports $6.2M Loss For Fiscal Year 2017

October 31, 2017StreetShares, the veteran-run small business lender, continued to post sizable losses, according to their June 30th fiscal year-end financial statements. The company had a $6,193,154 loss on only $2,168,067 in revenue. While StreetShares has generated significant buzz for their particular focus on military-owned small businesses, the lender only made 751 loans in the 12-month period and there is no requirement that the businesses they lend to actually be military-owned.

The company spent more on payroll and payroll taxes alone ($3,258,960) than they earned in revenue. They had 32 full-time employees and 1 part-time employee as of June 30th.

“As an early stage, venture-funded company that is not yet profitable, we rely heavily on capital investments to fund our operations,” the company wrote in their annual report. “Based on our current financial situation, it is likely we will require additional capital within the next twelve months beyond our currently anticipated amounts to fund the operations of the Company.”

The chart plotting their loan performances by grade below is from their annual report:

Their loan amounts typically range from $2,000 to $150,000 and require weekly payments for anywhere from 3 months to 3 years.

Even though the company spent nearly triple on marketing in this fiscal year ($1,727,478) versus the previous year ($579,331), revenue only doubled.

StreetShares plans to raise additional capital towards the end of this year through a Series B Round.

CommonBond Closes $248 Million Securitization, Secures Inaugural S&P Rating of AA

October 27, 2017NEW YORK (October 27, 2017) – CommonBond, a leading financial technology company that helps students and graduates pay for higher education, today announces the close of a $248 million securitization of refinanced student loans. The offering’s most senior notes achieved AA ratings from Moody’s, S&P, and DBRS – Aa2, AA, and AA (high), respectively – the company’s highest ratings to date.

The transaction was CommonBond’s fifth and largest to date. Investors submitted $1 billion in orders, making the deal more than four times oversubscribed. Goldman Sachs served as structuring agent, co-lead manager, book-runner, and co-sponsor. Barclays and Citi also served as co-lead managers and book-runners on the transaction, while Guggenheim Securities served as co-manager.

“Investor demand for CommonBond paper has never been greater,” said David Klein, CommonBond CEO and co-founder. “The strong market reception is a reflection of our pristine credit quality, continued ratings progression, and track record of consistent results.” Klein added, “As a programmatic issuer, we look forward to continuing to bring consistently high performing bonds to the market, providing investors with world-class capital deployment options.”

The transaction was the first of CommonBond’s to be rated by S&P, who assigned AA ratings to the transaction, alongside similar ratings from Moody’s and DBRS. Moody’s and DBRS also recently upgraded CommonBond’s ratings on previous deals in recognition of the company’s strong credit performance.

The securitization marks a significant period of growth for CommonBond, which earlier this year introduced student loans for current undergraduate and graduate students nationwide, to complement its established student loan refinance product. CommonBond is the only financial technology company to offer a full suite of student loan solutions, including new student loans to current students and refinanced student loans to graduates. The company has funded over $1 billion in student loans, and continues to grow its enterprise platform, CommonBond for Business™ – which enables employers to contribute a monthly payment to employees’ student loans, in addition to offering an evaluation tool for employees to determine their best repayment options.

About CommonBond

CommonBond is a financial technology company on a mission to give students and graduates more transparent, simple, and affordable ways to pay for higher education. The company offers refinance loans to college graduates, new loans to current students, and a suite of student loan repayment benefits to employees through its CommonBond for Business™ program. By designing a better student loan experience that combines advanced technology with competitive rates and award-winning customer service, CommonBond has funded over $1 billion in loans for its tens of thousands of members. CommonBond is also the first and only finance company with a “one-for-one” social mission: for every loan it funds, CommonBond also funds the education of a child in need, through its partnership with Pencils of Promise. For more information, visit www.commonbond.co.

The Voice of Main Street – Small Businesses Share Their Experience With Non-bank Finance

October 18, 2017

If she hadn’t scored the $250,000 loan through Breakout Capital in 2015, Jackie Luo says, the commercial-software firm she heads in Baltimore could not have made the “strategic hires” and purchased the new server to support additional customers and maintain the company’s 30% growth rate.

“Without that infusion of capital” from the McLean (Va.)-based lender, says Luo, chief executive at E-ISG Asset Intelligence, the software solutions provider would have been hard-pressed to deploy the “bandwidth and capacity” necessary to meet burgeoning demand.

And demand there is. Luo says billing for her company’s services helping more than 100 businesses and government agencies improve operational efficiency by keeping tabs on multiple assets — human, financial and equipment — topped $1.5 million last year, up from $1 million in 2015. This year, moreover, E-ISG is on track to collect nearly $2 million.

Meantime, she says, the $250,000, 10-year note at 6% interest she obtained with the help of Breakout was both a good deal and convenient: she reports securing the financing in three weeks, compared with the six months that a commercial bank would likely have taken. In addition, she’s been able to forge a better relationship with Breakout than with a faceless financial institution.

“We are a small business,” she says, “and we’d be just one in a million at a big bank like Wells Fargo. They wouldn’t give us much attention.” With Breakout, Luo adds: “I have the freedom to make decisions about infrastructure investments without worrying about the short-term. And I don’t have to deal with people second-guessing me.”

Had she not gotten the financing, moreover, “I would not be able to pay myself,” she says. “I’d have to use my salary as working capital.”

Luo is not alone. Her company’s story of finding much-needed capital from a nonbank financial company is increasingly common. It has always been challenging for small businesses to obtain credit from a big bank — roughly a financial institution larger than $10 billion in assets. But the small and community banks that have been the lifeblood for small businesses have also been winding down their small-business lending as well, according to a March, 2016, working paper published by the Federal Reserve Bank of Philadelphia.

“As recently as 1997, small banks, with less than $10 billion in assets, accounted for 77% of the small business lending market share issued by commercial banks,” co-authors Julapa Jagtiani and Catharine Lemieux write in “Small Business Lending: Challenges and Opportunities for Community Banks.” However, the market share dropped to 43% in 2015 for small business loans with origination amounts less than $1 million held by depository institutions.

“The decline is even more severe for small business loans of less than $100,000,” they add, “where the market share for small banks under $10 billion declined from 82% in 1997 to only 29% in 2015.”

The Philadelphia Fed study notes that alternative nonbank lenders are filling a widening gap. “By using technology and unconventional underwriting techniques, many alternative lenders are competing for borrowers with offers of faster processing times, automatic applications, minimal demands for financial documents, and funding as soon as the same day.” And the Fed study finds that it’s likely that nonbank lenders, which are growing rapidly, are having a positive effect by “increasing the availability of credit, particularly to newer businesses that do not have the credit history required by traditional lenders.”

The Philadelphia Fed study notes that alternative nonbank lenders are filling a widening gap. “By using technology and unconventional underwriting techniques, many alternative lenders are competing for borrowers with offers of faster processing times, automatic applications, minimal demands for financial documents, and funding as soon as the same day.” And the Fed study finds that it’s likely that nonbank lenders, which are growing rapidly, are having a positive effect by “increasing the availability of credit, particularly to newer businesses that do not have the credit history required by traditional lenders.”

Meantime, the Small Business Administration reports that small businesses remain essential to the health of the U.S. economy. Businesses with fewer than 500 employees account for 55% of overall employment in the U.S., according to the agency, and are responsible for creating two out of every three net new jobs. Which means that alternative funding sources — which do not, it is worth noting, depend on depositors’ money, as banks do — are playing an increasingly important and largely unrecognized role in the country’s economic fortunes, notes Cornelius Hurley, a law professor at Boston University and executive director of the Online Lending Policy Institute. “They’re still a small percentage of the overall lending picture,” he says of nonbank financial companies, “but they’re an emerging force and a lot of small businesspeople certainly depend on them. If they disappeared tomorrow,” he adds, “a lot of businesses would be wiped out too.”

To find out what is happening in the real world, AltFinanceDaily interviewed small business owners around the country: among others, a Houston sports medicine provider, a Connecticut restaurateur, a Midwestern truck hauler, and a Maryland hardware-store owner. Some recounted being shunned by banks because of poor credit while others registered unhappiness with traditional financial institutions as inconvenient and impersonal. While some who turned to alternative lenders admitted they would have preferred not to be paying dearly for borrowing or for cash advances, most said the tradeoff was worth it.

The existence of alternative lenders has made it possible for these businesspeople to meet payrolls, pay contractors and suppliers even when business was slow or billings stalled. Customers with alternative funders – in addition to Breakout’s customers, AltFinanceDaily spoke to clients of Pearl Capital Business Funding and Merchants Advance Network– also reported that they were able to purchase or replace equipment and maintain inventory, hire additional employees and accept new customers, pay for upkeep and upgrades of their business’s physical plant, and make other expenditures necessary to keep operations up-and-running.

Jason, for example, who heads a family business in Louisiana manufacturing and selling pesticides (and who asked to be identified only by his first name), reports that his suppliers began demanding that he pay in advance for chemical feedstock after he took a “financial hit following a nasty divorce.”

The roughly $1 million (annual sales) business — which was started by his parents back in 1960 — furnishes chemicals mainly to cotton farmers and homeowners in Louisiana and Texas, most of whom purchase the company’s products through feed and hardware stores. Jason says he spends a substantial amount of time on the road handling sales and distribution.

His suppliers not only require him to pay for the chemicals upfront but, following his divorce, they now insist upon larger purchases as well. Following the departure of a previous lender, he says, Breakout stepped in with an $80,000, 12-month loan in March, 2016, which he was able to repay within six months. This was followed by a $60,000 borrowing in March, 2017, which he again paid down early – in 90 days, Jason says – and the account manager at Breakout “went to bat for me and gave me an additional discount for early payment.”

His suppliers not only require him to pay for the chemicals upfront but, following his divorce, they now insist upon larger purchases as well. Following the departure of a previous lender, he says, Breakout stepped in with an $80,000, 12-month loan in March, 2016, which he was able to repay within six months. This was followed by a $60,000 borrowing in March, 2017, which he again paid down early – in 90 days, Jason says – and the account manager at Breakout “went to bat for me and gave me an additional discount for early payment.”

Had Breakout not provided external funding, Jason says, he would have been “wiped out.” He adds with feeling: “It would have meant the end of me.” And sinking the fortunes of the company would also have spelled job losses for five employees, including both his son, who works part-time, and his sister, the business’s co-manager. “Now I’m out of the hole,” he says.

In Houston, Anna, co-owner of a physical therapy and sports medicine concern, was interviewed in August just before Hurricane Harvey loomed on the horizon. “We’d been around for four years and growing rapidly,” she says, asking to be identified only by her first name, and “we couldn’t keep up with the growth.”

Anna recalls that a few years ago (she is vague about the exact dates) the company needed $50,000 to $60,000 to add equipment and staff to meet the growing demand. Because of some “ups and downs” in her business and credit history, however, a bank loan was out of the question. “My credit wasn’t the best,” Anna says, “and we had not been in business the five-to-seven years that most banks want.” She began casting about for financing and quickly saw that factoring would not be a suitable choice for a business like hers, which depends heavily on third-party payments from health insurance providers. “Companies using factoring are taking money based on credit card payments,” she says, “and we’re not a restaurant or a bar. So we can’t pay a percentage of every transaction.” Typically, she notes, getting paid by an insurance company involves a “90-day turnaround.”

Anna went online, did some research, and talked to three or four nonbank lenders searching for the “right kind of company.” That led her to Breakout. “What I really liked about them is that they did a lot of due diligence on our field,” she says. “They did their homework, asking us: ‘What are your collections and payroll? How much outstanding debt do you have?’ They also asked to see our actual bank statements.”

Anna went online, did some research, and talked to three or four nonbank lenders searching for the “right kind of company.” That led her to Breakout. “What I really liked about them is that they did a lot of due diligence on our field,” she says. “They did their homework, asking us: ‘What are your collections and payroll? How much outstanding debt do you have?’ They also asked to see our actual bank statements.”

Despite the high level of due diligence that Breakout performed, Anna says, it only took “maybe three or four days” for the loan to be approved and for the money to land in her bank account. Before long, she was off to the races. With the added capital, she hired three more employees – bringing the employee headcount to 18 — purchased more gym equipment, made payroll, and paid off miscellaneous expenses.

The added capacity and fortified staff, meanwhile, enabled the company to “almost triple its volume,” the entrepreneur says. And not only did the financing “put me in a good financial place,” Anna adds, but after repayment, Breakout made it possible for her to effect a merger with a competitor by approving a second loan for about $30,000. “The best thing about Breakout,” she says, “has been the communication. One time I did need to make a payment two or three days late. But I just called (the account manager). I was very surprised because these kinds of companies are seen as a last resort. But it was like they were investing in us.”

John Speelman, who owns Poolesville Hardware in Poolesville, Md., can boast a raft of five-star Yelp reviews online. “Extremely helpful and friendly service, surprisingly good selection (and) the complete opposite of a big box hardware chain,” raves one customer. “It is so rare to find a well-stocked store that has helpful personnel—makes this store a real gem!” says another fan.

For his part, Speelman attributes much of his hardware store’s popularity to the financing arrangement that he’s been able to work out over the past eight years with Merchants Advance Network, a Fort Lauderdale (Fla.)-based alternative funder. “It takes money to make money,” is one of his pet aphorisms.

Located roughly 35 miles west of the White House, the hardware store boasts a clientele who tend to arrive in BMW’s rather than the pickup trucks that predominated a decade or so ago in this exurban community of some 5,000 denizens. Whatever their class background, though, they’re looking for items that are not a good match for an online purchase. “People don’t buy a toilet plunger, a can of paint or picture-hanging stuff online,” Speelman says. “Because they want to do that today,” he says, “they won’t order with Amazon.”

“One industry that has not been impacted” by online merchandisers, he adds, “is the garden center. They’ll buy a garden hose, weed killer and seeding,” he explains of his regular customers. “And light bulbs” while they’re there, he adds. “We’re like the 7-Eleven — a convenience store.”

To guarantee that convenience, Speelman pays cash-in-advance for most of his inventory, and banks have not been helpful. He contrasts the relationship he has with Michael Scalise, the chief executive at Merchants Advance, with loan officers at commercial banks. “It’s hard to get a loan for anything in retail,” he says. Never mind that he maintains “a high credit rating and I never bounce a check,” he went on. “There are no more local banks. At M&T Bank, all the managers I knew are gone and there’s always a new teller. The banking industry is a revolving door.” So he opts for capital from Merchants Advance “when I need 30-40-50 grand in a day, I use Mike’s money” even though the cost can be as steep as 25%, he says. If he doesn’t have something in stock – specialty items like ammo boxes, a Sugarplum tent, as many as 32 packs of size D batteries, metric measuring tapes – he can put in a special order with suppliers. But he prides himself on the full panoply of wares on his shelves. “You can’t sell from an empty cart,” is another of his favorite sayings.

Lori Hitchcock, who also draws capital from Merchants Advance, is manifestly displeased with the banking industry. She’s an owner with her husband of Hitchcock Trucking, the couple’s 60-year-old family business, which is located on a ten-acre tract in Webberville, Mich., situated between Detroit and Lansing, the state capital.

Of her experience with banks, Hitchcock says: “At the time we went with (Merchants Advance), banks weren’t lending. And they’re still not lending. We’re considered high-maintenance and high-risk. Banks don’t want a bunch of trucks” should they foreclose on a loan, she observes. “If you’re a farmer, they can take all your land. Great! In this crazy world you live in, it’s hard to get the banks interested.”

The Hitchcock family’s fleet of ten Peterbilt semis hitch up to more than 20 trailers and truck bodies – flatbeds, dump trucks, vans, and refrigerated trucks or “reefers” – and haul grain, sweet corn, onions, celery, fertilizer, and soft drinks across the Midwest. Most recently, she says, the family business took out $80,000 from Merchants Advance to expand its fleet and buy another reefer trailer and a backhoe. “Out here in the country, you always need a backhoe,” she says.

The Hitchcock family’s fleet of ten Peterbilt semis hitch up to more than 20 trailers and truck bodies – flatbeds, dump trucks, vans, and refrigerated trucks or “reefers” – and haul grain, sweet corn, onions, celery, fertilizer, and soft drinks across the Midwest. Most recently, she says, the family business took out $80,000 from Merchants Advance to expand its fleet and buy another reefer trailer and a backhoe. “Out here in the country, you always need a backhoe,” she says.

To satisfy her lender, the company makes daily ACH payments. “I’m not going to lie and say that things aren’t tight,” she says. “It is a burden. You just have to have constant cash-flow – which we do have. And it’s important to have good relationships…I can usually tell three weeks in advance if (making payments) is going to be challenging. So it all comes down to being loyal to people.”

Whatever the struggle to keep up with debt payments, it beats using her own money. “My husband and I are raising a family,” Hitchcock says, “and it’s nice having the cash so you’re not putting your personal earnings into the company.”

In Manchester, Conn., a stone’s throw east of Hartford, Corey Wry says that he wouldn’t be able to operate his two, highly rated restaurants just off Interstate 84 – Corey’s Catsup & Mustard and Pastrami on Wry – if he didn’t have funding from Pearl Capital, a New York (N.Y.)-based alternative funding company. A graduate of Johnson & Wales University in Providence, a restaurant-and hotel school, Wry describes himself as “a culinary guy” whose first love is serving food that’s both innovatively prepared and delicious. He candidly admits that his credit hit “rock bottom” after a confluence of untoward events.