Small Business Finance Industry Mulls What’s in The Rearview, Is Optimistic For Rest of 2022

April 14, 2022 The small business finance industry is looking ahead to anticipated growth for the remainder of the year, despite new challenges ahead. With massive government aid fading in the rearview, some industry players now have had the time to consider what the impact of it was as they move onward into the future.

The small business finance industry is looking ahead to anticipated growth for the remainder of the year, despite new challenges ahead. With massive government aid fading in the rearview, some industry players now have had the time to consider what the impact of it was as they move onward into the future.

Bob Squiers of Meridian Leads expressed his view on the topic, “a lot of our customers, mostly the ISO shops, many of them converted and started selling and pitching the government programs. So in that sense it kind of helped keep those guys afloat, helped keep our business going. A lot of what we do in the marketing side, translated for those government programs. But then it did also squash the demand for the cash advance.”

In some cases, government funding has helped merchants pay off pre-existing obligations in a timely manner. Matthew Washington, founder and CEO of Moneywell GRP, noted, “An educated business owner is using the financing options available as they see fit for the timing. Someone that is waiting to get an SBA or an EIDL is more susceptible to take a bridge product to get them through that time gap,” he said. “As long as you’re working with the merchant and pushing out good products and you know what is on the rise, I think it has done nothing but help in some cases.”

Trucking became one of the number one fields that made up a large percentage of submissions during the pandemic, industry insiders say. However, with gas prices increasing, business with trucking could go down. Other businesses such as restaurants, where only a third received funding last year from the government, are desperate for funding.

“There’s tons of restaurants left that haven’t yet received their funding. So we could be seeing a lot of exposure in that industry,” stated Michael Yunatan of Specialty Capital. “But overall, I definitely do feel that we’ll be seeing an uptrend in our numbers across the board.”

“We definitely do think the industry is growing as a whole,” said Yunatan. “Even though we are a new player in the space we have been growing.”

Chad Otar, founder and CEO of Lending Valley, said, “We need to keep monitoring the interest rates that are coming up from the Federal Reserve, we need to make sure we’re not heading towards a recession, we need to make sure that we’re able to fully have the capital ready, in order to be able to deploy at a reasonable rate.”

Otar acclaimed the indirect benefit of large tech companies operating in the space with a competing product, arguing that the presence of PayPal and Amazon are helping to bring exposure to the industry overall.

“And now that Kabbage is back as well, since they partnered up with American Express, it’s gonna help us out to be able to push the product more into the mainstream,” said Otar. “So I believe there will be a growth in the industry.”

North Mill Announces Pricing of Largest Securitization Ever at $371M

March 4, 2022 MARCH 4, 2022 – NORWALK, CT – North Mill Equipment Finance LLC (“NMEF”) announced today the closing of its fifth commercial equipment backed securitization (ABS), NMEF Funding 2022-A (“NMEF 2022-A”). The $371,070,000 transaction represents North Mill’s largest ABS issuance to date, surpassing its $236,588,000 ABS issuance in March 2021. The transaction was well-received by institutional investors despite being in the market during a period of heightened macroeconomic volatility, pricing on the day of Russia’s invasion into Ukraine. North Mill had no investors drop their order post announcement of the invasion, and ultimately priced at a WAL-adjusted spread of 1.54%. The transaction featured twenty-three investors, eight of whom were first time investors in NMEF.

MARCH 4, 2022 – NORWALK, CT – North Mill Equipment Finance LLC (“NMEF”) announced today the closing of its fifth commercial equipment backed securitization (ABS), NMEF Funding 2022-A (“NMEF 2022-A”). The $371,070,000 transaction represents North Mill’s largest ABS issuance to date, surpassing its $236,588,000 ABS issuance in March 2021. The transaction was well-received by institutional investors despite being in the market during a period of heightened macroeconomic volatility, pricing on the day of Russia’s invasion into Ukraine. North Mill had no investors drop their order post announcement of the invasion, and ultimately priced at a WAL-adjusted spread of 1.54%. The transaction featured twenty-three investors, eight of whom were first time investors in NMEF.

NMEF 2022-A featured five tranches of notes, achieving an 88.35% advance rate through the Class D note. The Transaction was rated by Kroll Bond Rating Agency, Inc. (“KBRA”), who assigned a lower base case rating agency loss assumption for NMEF 2022-A vs. the company’s preceding issuance (“NMEF 2021-A”), permitting North Mill to achieve higher proceeds through the capital stack (88.35% in NMEF 2022-A vs. 86.03% in NMEF 2021-A). The $371.1MM transaction was backed by $420MM in equipment loan and lease contracts, $72MM of which will be contributed via a 3-month prefunding period post-close.

“I’m extremely proud of the team’s execution on this transaction, especially during such a challenging macro-economic environment and geopolitical discord,” said North Mill’s President and Chief Operating Officer, Mark Bonanno. “The base case loss assumption assigned to this transaction by the rating agency was 115bps lower than our 2021 ABS transaction which is a testament to the quality of North Mill’s underwriting and servicing model and a validation of our business strategy of targeting higher credit quality obligors, diversified equipment and industry types, and a refined list of third-party originators with whom we partner to offer financing solutions.”

Truist Securities, Inc. served as sole book runner for the transaction.

About North Mill Equipment Finance

North Mill Equipment Finance originates and services small to mid-ticket equipment leases and loans, ranging from $15,000 to $1,000,000 in value. A broker-centric private lender, the company accepts A – C credit qualities and finances transactions for many asset categories including construction, transportation, vocational, medical, manufacturing, printing, franchise, renovation, janitorial and material handling equipment. North Mill is majority owned by an affiliate of WAFRA Capital Partners, Inc. (WCP). The company’s headquarters is in Norwalk, CT, with regional offices in Irvine, CA, Dover, NH, Voorhees NJ, and Murray, UT. For more information, visit www.nmef.com.

AltFinanceDaily’s Top Five Stories of 2021

December 20, 2021 deBanked’s most read stories of 2021 were similar but different to those read in 2020. We broke them down into categories by popularity.

deBanked’s most read stories of 2021 were similar but different to those read in 2020. We broke them down into categories by popularity.

1. Scandal

A South Florida business apparently masquerading as a small business finance company, was by far and away the most read story of 2021. Authorities now believe that it was a $200M+ ponzi scheme with more than 5,500 investors. Unlike other alleged schemes that have rocked the finance world, thousands of people believe the allegations are not true and have rallied around the CEO.

2. Domain Life after Death

The Death of a Thousand Financial Companies, the leading story of AltFinanceDaily’s March/April 2021 magazine issue, was the 2nd most popular across 2021. In it, AltFinanceDaily went undercover to find out what happened to the domain names of financial companies that went out of business. The findings were terrifying. (See: Video discussion about the story)

3. Real Estate Investing

Think what you want about crypto as the future because when it came down to it, AltFinanceDaily readers were vastly more interested in real estate investing. Why Funders Are Investing in Real Estate As Their Side Hustle of Choice was the 3rd most read story of 2021. “[Real estate is] just a way that people who have been successful and spin off a lot of cash for their businesses see as a safe way to diversify their income,” said a lawyer that was interviewed for the story.

4. Regulation

It was a close call between several stories pertaining to regulation. While interest in CFPB-related activity ranked high, so too did a court decision in Florida that ruled on the legality of merchant cash advances. The New York commercial financing disclosure law was also top of mind for many readers as was interest in proposed legislation in Maryland.

5. An Exit

The fall of LendUp, an online consumer lending company, was apparently of great interest in 2021. After some difficult encounters with regulators, the company ceased lending operations. “Although we are no longer lending, we also offer a series of free online education courses designed to boost your financial savvy fast,” the company’s website now says.

Velocity Group USA Names Keith Nason President, Launching KapSource in Q1 2022

December 16, 2021 Melville, NY – December 16th, 2021 – Velocity Group USA is pleased to announce Keith Nason as the newly appointed President. In conjunction with stepping into the role as President, Nason will continue to hold his position as Chief Operating Officer, building on business development strategies and appointing new members of Velocity Group’s executive team.

Melville, NY – December 16th, 2021 – Velocity Group USA is pleased to announce Keith Nason as the newly appointed President. In conjunction with stepping into the role as President, Nason will continue to hold his position as Chief Operating Officer, building on business development strategies and appointing new members of Velocity Group’s executive team.

“We have undergone many necessary changes over the past year, but the change we are most excited about is appointing Keith Nason as the President of Velocity Group. He has extensive industry experience, as well as the knowledge, innovation and vision to drive growth in 2022. I have no doubt these qualities will help set us apart from our competitors as we continue to expand our business,” said Lisa Gioia, Chief Executive Officer

Nason is an industry veteran with over eight years of experience within the Merchant Cash Advance market, specializing in both top and bottom-line growth, building infrastructure and security, data integrity, risk models, technology, and securing capital through multiple channels.

“Over the last 12 months, we’ve invested a tremendous amount of time, energy, and capital in our team, product, infrastructure and data security, as well as our process. Doing so has positioned us for significant growth in 2022 and beyond,” commented Nason.

He also credited his institutional investors as being a key to success by having faith in the long-term goals of the company, and confidence in the new team to prioritize long-term success over strictly short-term returns. Nason also stated, “It’s a true testament to the team that we were able to completely rebuild our business foundation while still funding over $100MM and producing record returns to our investors.”

With the revamp of the company infrastructure and data security, Velocity Group USA will be launching KapSource within the first quarter of 2022, a “business in a box” model that will allow other members of the industry to use its proprietary technology to increase conversions, alongside a marketplace in which brokers can fund their owns deals and create additional revenue streams through Velocity’s capital sources.

How a Former Banker is Servicing Clients that Turned Down Alternative Funding Offers

December 15, 2021 What do brokers do with the clients that don’t want to pay the costs of an alternative product, but are still too underqualified for traditional financing?

What do brokers do with the clients that don’t want to pay the costs of an alternative product, but are still too underqualified for traditional financing?

Juan Caban, CEO and Co-Founder of Financial Lynx, has leveraged his interpersonal relationships as a former banker with his passion for networking and his discovery of a niche type of client into a business that is now spread across 44 states. Lenders aren’t the only ones turning down deals, the applicants do too, he says.

Caban built a referral business by talking to people, being an active member of the industry, and taking advantage of pandemic-induced halts in business to research the best ways to serve a section of business owners that prior to Financial Lynx, were either using less attractive products or never taking on financing at all.

“I’m a big networker,” said Caban. “I always go out, I meet a lot of people, I always get referrals from a lot of different areas.” He spoke about how as a decade-long banker with major banks, he knew right off the bat in his career that traditional financing was excluding financially-sound merchants who weren’t meeting overzealous bank qualifications.

“I would meet people who want to do business with me and I would present it to my bank, but it was always a challenge,” Caban said. “You want to help out a client, but you’re limited to the credit appetite of the bank that you are working for. After getting frustrated and declining a lot of clients, I wanted to seek out how I can help these clients out.”

After leaving the traditional finance world in 2019, Caban began work at an alternative lender, where the doors to a variety of new options opened up for him.

Caban still felt limited in his abilities to get deals done because of the confines funders mandate through their qualifications, and left to start his own company within seven months. After seeing a market in financing for merchants who fall between the high risk and traditional financing qualification threshold, he began talking to people across the financial community about what products exist for these types of clients.

“I used my banker network, I probably know about 200 bankers here in New York, and I started asking them, ‘hey, do you have a program in your bank that can help this type of client?’” Seeing that merchants with good credit and no desire to pay a 40% cost of capital were being pushed aside throughout the industry, Caban decided to pursue a business out of servicing this type of merchant.

“What I found was that there are some banks out there that as long as [the merchant] has a 700 FICO score, has been in business at least two years, and are considered to be in a preferred industry, some banks are willing to lend in some cases 20% of annual sales, up to $250,000, with just an application and one year of tax returns.”

The lending services being provided through Financial Lynx based on these qualifications are bank lines of credit that revolve and renew annually.

Caban described the qualifications for this type of financing as a look into the business owner themselves, and not as much into the business. “[These banks] focus on you as an individual and if you have personal credit.”

The concept took off.

“I started working exclusively with one MCA broker shop, they were calling hundreds of businesses a day,” said Caban. “They were trying to sell [merchants] cash advances obviously because it is a very lucrative commission business, but anything that was non-cash advance, or didn’t fit the cash advance space, or merchants who wouldn’t accept the expensive cash advances, they would refer that client to me.”

The twist is that the banks don’t pay him a commission so he has to charge a fee to the merchant once the financing is completed.

“At the end of the day I feel good because I am providing the client with something that they couldn’t find on their own,” Caban said. “So I am helping the client, and almost 100% of my clients are satisfied with what they have, because they’re getting cheap financing, 5% instead of 30% money, so even with my 10% consulting fee to connect the client, it’s still 50% cheaper than what they would’ve gotten in any type of cash advance.”

The biggest hesitancy Caban sees from alternative finance companies in terms of working with his niche product and client is the patience required in dealing with bigger banks. “Everything is quick in MCA, [brokers] get approved today, get funded today, and get paid tomorrow. I say look, I can provide the client what you’re looking for, but it is a three week process.”

“The ones that say, ‘hey we want to do what’s best for the client,’ they buy into it, they send us referrals on a constant basis,” Caban continued. “The ones that say ‘it’s taking too long, they’re not into it’ and I tell them ‘you’re going to lose that client eventually.’ As opposed to losing them, make some money out of it before you leave them.”

Trying to convince the legitimacy of his product seems to be part of the daily ritual for Caban. “Having a bank line of credit is considered a unicorn in the industry. Everyone says that they have it, but it’s not really a line of credit. We’re actually providing true lines of credit. It’s truly a revolving line of credit.”

“It’s always a thing where it’s like, are you for real?”

New York’s Fourth Judicial Department Affirms Its Settled Law That MCA Agreements Are Not Usurious

November 16, 2021 New York’s Appellate Division for the Fourth Judicial Department in the Supreme Court of New York issued a landmark decision for the merchant cash advance industry on November 12th.

New York’s Appellate Division for the Fourth Judicial Department in the Supreme Court of New York issued a landmark decision for the merchant cash advance industry on November 12th.

By affirming the original decision issued in Kennard Law P.C. DBA Kennard Law and Alfonso Kennard v High Speed Capital LLC (Index No: 805626/2020), the Appellate Division agreed that among other things that it is settled law in New York that the underlying purchase and sale of future receivables agreement at issue in the case is not a usurious loan.

On June 10, 2020, plaintiffs filed their lawsuit against the defendant, asking the Court to vacate a confession of judgment on the basis that the defendant’s underlying contract dated back on August 24, 2017 was really an unenforceable criminally usurious loan.

The defendant moved to dismiss and the judge granted the motion, holding that:

1. Plaintiffs’ claim of usury is barred by the one-year statute of limitations applicable to usury based claims.

2. Plaintiffs have failed to plead a cognizable cause of action upon which to seek relief.

3. Plaintiffs have no recoverable damages.

4. Plaintiffs’ claims are barred by documentary evidence and settled law in New York holding that the parties’ underlying agreement was not a usurious loan.

Plaintiffs appealed, hoping that the Fourth Department would be persuaded by their arguments that the agreement was usurious. It wasn’t. Instead the Appellate Division unmistakably and unanimously affirmed the original judgment.

The decision demonstrates that there is consensus across judicial departments. Kennard in the Fourth Department (Western New York) is similar to Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC in the First Department (Manhattan and the Bronx) circa 2018.

Coincidentally, the attorney representing the losing parties, Amos Weinberg, is the same in both landmark cases.

The attorney representing High Speed Capital was Christopher Murray of Stein Adler Dabah & Zelkowitz, LLP.

Appalachian Crowdfunder Gives Take on Business Lending

November 2, 2021 View from outside of Pittsburgh, PA

View from outside of Pittsburgh, PAGeorge Cook, whose family has been running a small community bank in rural Appalachia for over 130 years, has grown up in a world surrounded by banking in some of the most rural parts of America. Now the CEO of Honeycomb Credit, Cook has taken to a crowdfunding platform to start lending to businesses in his area. Cook shared his thoughts with AltFinanceDaily about the state of lending, and how his product competes with ones already available on the lending market.

Cook spoke about how when he growing up, he always had a fascination with the relationship between the consumer and their banks combined with the difficulties for those consumers to get access to capital. “I spent a lot of time thinking about community banking, especially local capital,” said Cook.

When discussing competing products in the lending space, Cook thinks that his product will innovate his area with a style of lending that benefits both the borrower and investor. It appears that he thinks products like MCAs have become partially antiquated.

“I think the downside of [MCA] is inherently when your value proposition is fast money, you’re going to have a negative selection,” said Cook, when asked about fintech’s role in innovating small business lending. “You’re going to have a lot of desperate businesses who need money fast, which means you inherently have to charge a high interest rate and that has [deterred] a lot of business owners.”

George Cook, CEO, Honeycomb Credit

George Cook, CEO, Honeycomb CreditCook referenced how the complexity of some MCA deals prevent small businesses from using them. “We talk to a lot of business owners who really don’t understand what a merchant cash advance is, they get caught in a debt trap, and it’s not a good situation. For me, I think the next evolution is, not saying merchant cash advances are going away, but I think they’ve been over extended. I think they’ve been overapplied in places where they don’t make sense.”

Cook hinted at new fintech loan products that have elements of MCA popping up in the lending world, as fintech innovates the industry.

“I think now we’re going to see the fintech space start to right the issue, come up with other capital solutions that make sense for small businesses for longer term capital. I think we’re going to see a lot of term loan products that act with different data and different attributes coming to bear, [thus] being able to bank these businesses.”

After working in fintech building big data credit analytics products prior to starting Honeycomb, Cook claims he saw a major issue with small businesses having access to capital long ago. He saw that the qualifications needed for business loans were the same as ones needed for consumer loans, and many small businesses just didn’t qualify for the capital they needed.

“[The system] didn’t work as well for small business lending because you know, small businesses don’t have as much operating history, they don’t have clean data sets, they’re not keeping their books really well, there’s not really a good data aggregator of small business data.”

Cook continued to speak about the issues with banks evaluating a small businesses’ credit and how this was causing a low approval rating. “A coffee shop looks a lot different than a fitness studio and those look a lot different than a manufacturing plant,” he said. “We were actually seeing a really large decrease in small business lending across the country.”

According to Cook, his company allows investors to take their money and put it right back into the community. He also claims that each one of his customers can expect returns ranging from six to twelve percent on an investment.

Honeycomb makes money on success fees, which are the closing costs on the loan. There’s also an investor fee to get a foot in the door.

“One of the things we’ve found is whenever you have retail investors, you have local people in the community voting with their wallets on these small business loans,” said Cook. “So we’re able to do small business loans in a way that no one else has been able to.”

Fintech Déjà Vu: Wait, Has This All Happened Before?

October 6, 2021 All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

Touted as the “5-minute online business loan,” the ad for LoanWise ran in newspapers starting in 1999. That was 22 years ago. Back then, LoanWise was described as a marketplace that connected small businesses with lenders where borrowers could comparison shop for loans.

Provident Bank was the first to join the platform, where it would approve between $5,000 – $50,000 in as little as five minutes. At the time, the Los Angeles Times said that there were only 2,160 matches on Google for the phrase “small business finance.”

“2,160 is a big number no matter how you look at it,” the Times reported.

There’s over 6 million today by comparison.

LoanWise had set up 10 lenders on the platform by the end of 1999, with names that included American Express, Compass Bank, and PNC Bank. There was competition as well. Business Finance Mart and America’s Business Funding Directory also connected interested borrowers with lenders, according to the Times.

Today, all 3 websites no longer exist, forgotten vestiges from the land before fintech.

Or has this all happened before?

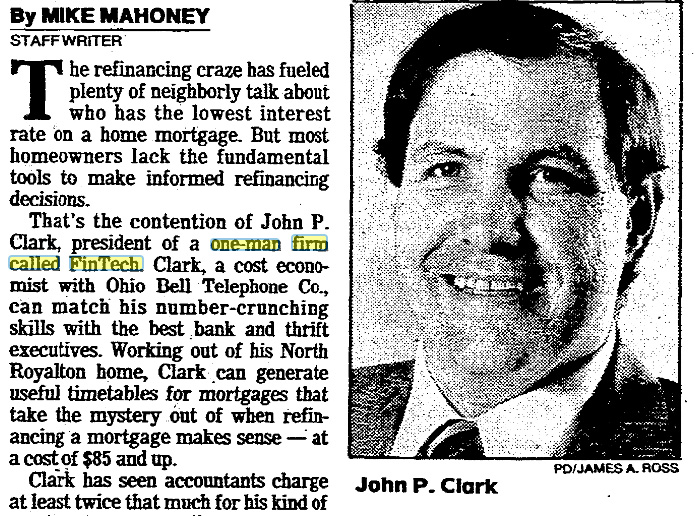

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

“Clark can generate useful timetables for mortgages that take the mystery out of when refinancing a mortgage makes sense,” wrote The Plain Dealer. Had it been 2021, Clark sounds like it would have been a billion dollar fintech app.

It was not a one-off.

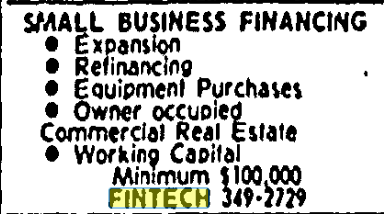

Fintech was the place to call if you wanted a working capital small business loan in San Antonio, TX starting in 1989. Ads for Small Business Financing advised people to call Fintech to get their business funded.

You could also just subscribe to the newletters. The Financial Times had four “FinTech Newsletters” in 1989 that were dedicated to covering electronic office, advanced manufacturing, telecom markets, and mobile communications. The price was £344 to £395 per year to receive them bi-weekly.

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

But hey, it’s all just a coincidence that ideas were roughly the same thirty years ago. Out in say, Des Moines, Iowa in the 1960s, for example, none of these things would’ve occurred to anyone.

Or would they have?

Sidney Feintech, a supermarket owner, expanded his store in 1963 to sell appliances, car batteries, clothing, and televisions. He got the idea that selling on credit would boost sales so he formed his own in-house credit company so that customers could Buy Now, Pay Later. Innocent enough, except the newspapers mispelled his last name.

“Fintech,” the papers said, had gotten into the credit business.

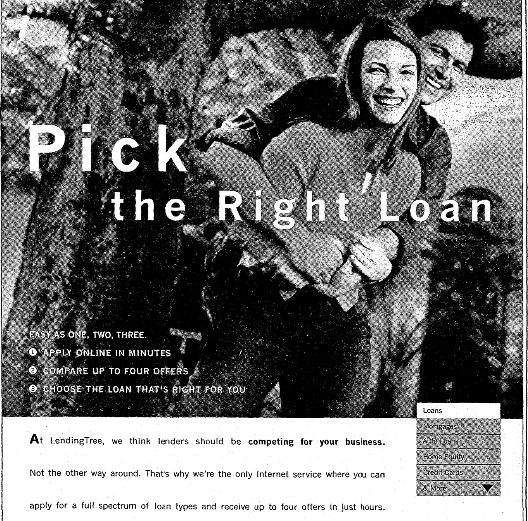

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

“I thought, ‘why can’t I put my information somewhere and let the banks compete for my business,” Lebda said. Launching a website, his company went on to generate $460 million worth of loans in just the fourth quarter of 1999 alone.

“There are other sites on the internet where you can apply for a loan, but those sites are operated by the lenders themselves,” Lebda said at the time. “We don’t lend money; that’s what makes us unique.”

That website was LendingTree, a company that today still has over 900 employees and a market cap of $1.8B. And Lebda is still the CEO.

In 1999, the hardest part was educating consumers to shop for loans online.

“Consumers have always done this one way, and this requires a behavioral change,” said consultant James Punishill in 1999. “In the old world, you’d pick up the newspaper and see a bunch of rates.”

“I knew from the start this would work because consumers really hate getting loans,” Lebda said at the time. “The market is huge and it’s perfect for e-commerce.”