The point of sale isn’t what it used to be

December 16, 2011 “I’m sorry sir but our credit card machine just went down. Can you wait 11 minutes while I activate a card reader on my iPhone so I can take your payment?”

“I’m sorry sir but our credit card machine just went down. Can you wait 11 minutes while I activate a card reader on my iPhone so I can take your payment?”

11 minutes. That’s how long it took Sean, the founder of the Merchant Processing Resource to set up a merchant account with Square. The point of sale is changing quickly. Dial-up terminals are becoming more and more like their carbon copy imprint predecessors and there’s no way to stop the changing tide. According to Square, 1 out of every 8 merchants in the U.S. uses Square to process credit cards.

The revolution in payments seems to have gone over the heads of Merchant Cash Advance (MCA) providers, a financial industry that purchases future card revenues of small businesses. If the big MCA players have plans in the works to overcome the obstacle of capturing revenues, they certainly haven’t made them public.

We first sounded the warning bell to the industry back in May, 2011, in an article that characterized the modern merchant as having four methods of accepting electronic payments: Desktop POS software, a terminal, PayPal, and mobile payment software. This payment makeup directly leads to rising costs of the MCA product. The ultimate result of our warning was…nothing. MCA providers have for the most part shrugged off the changes in the point of sale, rather than stay ahead of the curve. It’s a shame.

The Electronic Transactions Association (ETA) recently created a certification, a nationally recognized level of excellence for the payment industry employed to become true professionals. A Certified Payment Professional (CPP) will be best equipped to work with business owners and they are required to be knowledgeable on the subject of MCA, as indicated in the CPP handbook. The reverse is unfortunately not required of those employed in the MCA industry, where underwriters mostly hail from the worlds of lending or leasing. Bankcard is certainly not their strong point.

There is a big void of bankcard knowledge in the risk assessment of MCAs. Underwriters are accustomed to reviewing “batch data,” the amount settled out by a merchant, normally once at the end of the day. But press an underwriter for an explanation of where the batch came from, if the technology was PCI compliant, or what would happen to their interchange rates if they delayed settlement for a few days, and you’ll likely catch them scratching their head.

I once personally experienced this firsthand when a relatively new MCA firm sent a 3rd party site inspector to visit a clothing store prior to approval. The inspector’s report and photographs indicated that there was no physical credit card terminal on site but that a USB swiping unit was attached to a desktop computer at the register to accept card payments. The MCA provider declined the deal based on the report since the lack of a credit card machine flew in the face of the processing statements they received. I appealed the case to the CEO, who responded by e-mail with, “The merchant is showing $7,000 a month in credit card sales but when we visited the store, there’s apparently no credit card machine there. The statements we have must be fabricated.” Flabbergasted, I pointed out that the merchant uses desktop POS software and a swiping unit and that it had been verified in the inspector’s report. The last e-mail I received from the CEO was, “I don’t know what you mean by their computer accepting credit cards. Is this PayPal? We don’t do PayPal. We only fund merchants who process on site and they don’t seem to process on site. The deal remains declined.”

Just because I haven’t cited the name of the company, doesn’t mean this exchange wasn’t real. It was and It’s even more embarrassing because their goal was to be in the top three largest funders of MCA in the country. They’re still in business but they’ve suffered some major setbacks.

USB card readers have been in use for a long time and we recently had the pleasure of hearing from Richard Freedkin, the Co-founder of USBSwiper.com. We asked if the mobile pos software revolution was impacting the desktop industry. He shared this, “I don’t think that the USB card readers are being threatened per se… however; I believe that the Mobile Payments industry will make a dent. There will always be people using computers for their POS especially at more fixed locations and Internet access is much cheaper than mobile phone data plans that are required for processing to work.”

And while he’s probably right that the desktop POS experience isn’t going away, they’re not standing on the sidelines either. “We are also about 6 weeks from releasing our new beta version of our software for iPad, iPhone, iPod Touch and Android systems. We will also have a swiper for that platform as well. So we will offer the best of both worlds.”

Great firms innovate so we’re waiting…waiting…waiting for the MCA players to follow suit. If 1 out of 8 merchants are using Square, then the MCA industry is ignoring at least 1 out of every 8 merchants or failing to capture total card revenues from their merchants that use it.

Besides, technology companies like Roam Data are claiming that their mobile payments device has 3x the capabilities of Square. With Text2Pay, you can just SMS text someone funds or better yet, FaceCash allows consumers to make payments using their phone and their FACE!

Capturing payments directly from a merchant account is what made the MCA industry so popular but it could also be their downfall. If a merchant can activate a new account in 11 minutes, then surely there must be an increased focus on the overall banking and financial picture of a small business before purchasing future revenues. That might be where underwriters with lending backgrounds excel but if they don’t know bankcard, then they don’t know squat.

The point of sale isn’t what it used to be…

– The Merchant Cash Advance Resource

Occupy Main Street?

October 10, 2011 We didn’t protest… but we decided to see who was. Nowhere in the strange crowd did we find outraged business owners. Could the occupiers of Wall St. also be fighting against Main St.?

We didn’t protest… but we decided to see who was. Nowhere in the strange crowd did we find outraged business owners. Could the occupiers of Wall St. also be fighting against Main St.?

Wall St. bankers might have a lot of money, but small businesses employ the most jobs in America. Chances are if you are unemployed, unhappy, or overworked, it will ultimately be Main St. that will save you. But for time being, nobody is hiring. Business owners are pointing the fingers at banks, citing the lack of loans has stalled expansion. Excuses, excuses…

Wall St. might have perverted capitalism to enrich themselves, but Main St. has done just the opposite lately. When presented with an opportunity, thousands of businesses are unwilling to take the risk. “We’re just holding on for right now,” is a phrase we hear way too often from Mom and Pop shops.

We posed this question to an unnamed ‘Occupy Wall St.’ protester today:

MPR: “If we gave you $10 today, could you turn it into $20? “

PROTESTER: “Hell, I could turn it into $100. You can make money on a lot of stuff going on down here.”

Capitalism lives… It’s the drive and execution that enables someone with $1 to turn it into $2, $5, or $100 in a marketplace. It’s an intuition that Americans are born with, even those with anarchistic tendencies yelling in protest against it.

But something has happened to our beloved Main St.

Opportunities to grow are being passed up, and with that the ability to hire more workers. The rich get richer by investing their capital and taking risk. In a competitive marketplace, we must always seek out ways to grow, expand, and improve. “Holding on” is not a strategy, at least not one that will lead to hiring. Stability does not prepare you for downturns, nor will it make you rich in the long term. Stability is actually the beginning of a long road that will one day lead you to being mad at those who got rich.

The math is simple. If you turn $1 into $1.10 everyday, while somebody else turns $1 into $2, expect yourself to be very poor by comparison 20 years from now. Whether you have a small retail store or a national franchise, don’t let your guard down, take chances, think big, and elbow your way to the top 1%. You’ll create a lot of jobs on the way.

Once you’re ready to turn $1 into $2, don’t worry about the lack of bank loans, Merchant Cash Advance providers will offer you $1 in return for $1.30. You net the profits and can redo it as often as you like. Naysayers will tell you it’s expensive and it would be if you didn’t invest the dollar. Rebuilding the economy begins with small business. Show them growth, show them jobs, show them how you were born to turn one dollar into two…

AltFinanceDaily

http://www.merchantprocessingresouce.com

Learn about Merchant Cash Advance Here

Some video clips we took while we were at the Wall St. protest:

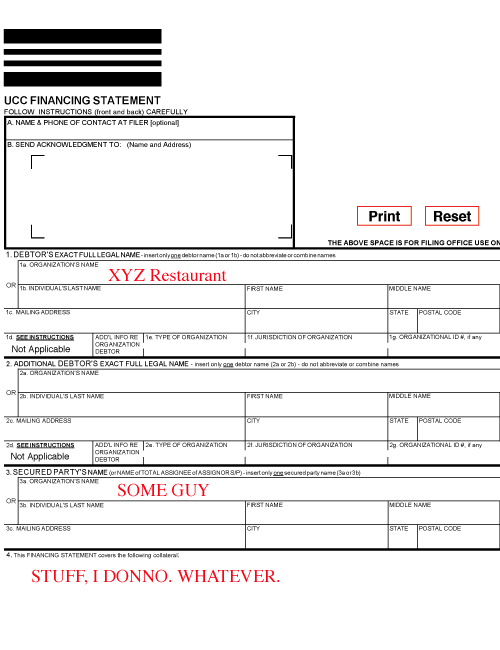

Let’s Play ‘Solve That UCC Filing!’

August 23, 2011

Underwriters have shared with us that it is more challenging than ever to determine if a merchant has an existing MCA balance already. Integrity Payment Systems, a merchant processor in Chicago, recently stated that they have signed on nearly 100 split funding partners. This is astounding given that we only list 24 officially recognized funding firms in our database. Sounds like we could use an update.

The challenge is not so much that WE don’t know who is funding merchants, but rather MCA firms don’t know. We’ll be the first ones to tell you that a retrieval percentage used to be black and white on a merchant statement. If not, you couldn’t miss that big fat UCC-1 lien by a known MCA firm. Those were the easy days when you saw “Secured Party: Fast Capital” and you could phone them up to verify a balance or find out what the scoop was.

Nowadays, there are lockbox programs, ACH debit programs (both variable and fixed payments), and a whole slew of creative structures to make MCA financing possible. The North American Merchant Advance Association(NAMAA) has an exclusive live network of funding activity. That means any NAMAA member can login to make sure that another member doesn’t already have an outstanding balance with the merchant they are about to fund. This database is an invaluable tool to the industry’s success and yet it has one major flaw, there are ONLY 12 members!

So let’s run through a scenario:

——

Mr. MCA Underwriter is analyzing an application and supporting documents. There is nothing being deducted from the 6 months worth of merchant statements. The bank statements look clean. The credit is good. Everything is pointing towards an approval until they do a UCC search. There are a few terminated UCC’s from over 5 years ago by Bank of America, back when bank lending actually existed. There is nothing since then, except for one by a so called ‘ABC LLC’. There is an address for ABC LLC but there is no contact information for them and a web search reveals nothing about their location or what it is. The UCC language is generic and indicates that it is a lien on the debtors property. Mr. MCA Underwriter has seen plenty like it before but asks the merchant about it anyway. The merchant indicates ABC LLC leased them all their equipment including a new oven and freezer. Everything adds up, the deal is approved, and subsequently funded.

Five days later Mr. MCA Underwiter gets a call from an upset individual with accusations that the merchant’s processing receivables already belong to someone else, an ABC LLC. The individual is a reseller of MCAs normally but has funded 5 clients with his own money(a trend becoming more popular. Read here). He funds those deals under a nondescript company, ABC LLC so that nobody will figure out what it is and solicit his client. Mr. MCA Underwriter explains there was no evidence of repayment of a MCA. It turns out the merchant defaulted 7 months prior and hence the 6 months worth of documentation were clean.

—-

For the past few years, it has been very common for resellers to search UCC databases by secured party, thus revealing ALL of the clients that particular secured party or MCA provider has funded in that state. Those clients are then solicited with the appeal of better rates on a MCA and incentives to get bought out. For some MCA providers, this has had a disastrous effect on retention.

ABC LLC successfully protected themselves on that front because no one was able to identify them as a MCA provider. Thus there was little chance their clients would be revealed. However, the strategy backfired when it became unclear that the merchant’s future credit card receivables had been sold.

ABC LLC’s strategy is becoming extremely common. Many MCA providers are resorting to using code names as the secured party to throw UCC hunters off the trail. We list a lot of those code names HERE. Combine that with the fact that hundreds of people are now funding their own accounts and we have a big mess of no UCCs, confusing UCCs, and incorrectly filed UCCs(some funders are filing them in the state they operate in instead of the state the merchant operates in).

Mr. MCA Underwriter is facing a lack of clues and it would not be surprising if the industry starts to see a resurgence in advance stacking. If anyone would like to anonymously share UCC code names that we do not have included in our records, please e-mail them to merchantprocessingresource@gmail.com

As the industry evolves, so will the issues. In our opinion, MCA providers should be plainly clear on the arrangement they have with their clients. No judge is going to listen to a story about code names, misleading UCC language, or why you don’t file at all. A UCC-1 is intended to be a public notice and is meant to be found. Small businesses will benefit by the expansion of the MCA industry but poor use of UCCs will inhibit the rate of growth.

And that’s our 2 cents…

-The Merchant Cash Advance Resource

../../merchantcashadvanceresource.htm

Did Somebody Say the End of the Credit Card Industry?

August 23, 2011

We check our site’s inbox once a day and usually receive some compliments, feedback, or industry secrets. But over the last two days, more than 15 people e-mailed us this link: The End of Credit Cards is Coming. This was followed by a barrage of comments such as “Does this mean the end of the Merchant Cash Advance industry as well?” or “It looks like your site topics are going to be obsolete.”

If any industry is poised to take a hit as a result of this “payment evolution”, it’s likely to be the manufacturers of plastic and magnetic strips. (The companies that make the cool shiny holograms on the back may also suffer.) If you actually READ through the article, it discusses an industry progression towards contactless payments. A contactless payment is still an electronic payment and it involves the same networks and banks. Saying the declined use of physical rectangular plastic cards will result in the end of the electronic payments industry as whole is like saying that the less frequent use of flutes and banjos will result in the end of music.

All sarcasm aside, this progression towards contactless payments indicates the merchant processing industry is on the verge of an explosive rebirth. Here’s why:

Equipment Sales and Leases

New technology to accept contactless payments will be required. If plastic cards are slowly phased out, retailers will have absolutely no choice but to purchase or lease equipment to accept contactless payments. (Sales and Leasing boom)

Increased Interchange profits for banks

The growth of contactless payments will likely cause Visa and MasterCard to increase certain interchange categories. They will rationalize this by providing proof that contactless security costs more.

New Payment Networks

Every merchant needs to accept both Visa and MasterCard branded cards in order to survive. In some regions of the country, it’s also important to accept American Express. Though American Express charges merchants more, they can’t afford not to have it. That being said, the above referenced article mentions the formation of a new super power payment network called ISIS to rival the current players. ISIS was formed by AT&T, T-Mobile, Verizon, Discover and Barclays Bank. Since ISIS is indepedent from the other payment networks, they will be able to create their own “interchange” and cost structure. I am inclined to believe that costs will not be lower than what’s commonplace in the current marketplace.

Increased Electronic Payments Usage

For the past 4 years, we’ve been lectured repeatedly by the government, teachers, and financial experts that credit cards are bad. During that same time period, we’ve also celebrated the importance and efficiency that phones/smart phones have brought into our lives. Blackberries, iPhones, Droids, texting, apps, skype, and wireless internet are the bread and butter of our daily lives. So what is the public inclined to infer with phones capable of making electronic payments?

- Credit Cards Payments Bad

- Smart Phone Payments Good

As long as Smart Phone is Good, consumers don’t need to feel guilty over their usage of credit. I’m sure we’ve all seen the debt counseling talk shows where they take an out of control spending housewife and force her to cut up her credit cards. She cries a little, acknowledges her problem, and then in a symbolic gesture of triumph, cuts up her cards. The entire charade portrays the plastic card as the perpetrator of the woman’s debt problems. One thing I don’t expect to see any time soon is a woman being lectured by a debt counselor to smash her iPhone with a hammer to stop her out of control spending. “In order to conquer your debt, I want you to go home and burn all 5 of the Droids on your family plan.”

BECOME DEBT FREE

Join the thousands of people who are breaking their scissors on their phones, buying new scissors, and then smashing their phones with a hammer. Say “Forget it to Credit” because there’s no app for your spending problems!

Those rectangular plastic cards may be on their way out but contactless payments are going to bring billions to the merchant processing industry. Happy processing!

-AltFinanceDaily

What’s Going on in California?

August 23, 2011

The people have spoken! Many of our readers have sent e-mails wondering why we don’t have any coverage on the recent events in California. So here goes:

If you’re out of the loop, a nearly 3 year old lawsuit against one of the major Merchant Cash Advance (MCA) providers is coming to a close. Their name is not important, but it is a firm we revere still to this day. The story takes place in California, where a group of merchants in 2008 contested their Merchant Cash Advance was actually a loan, not a sale. In the other 49 states, MCA has been virtually undisputed for years but California law has shades of Gray.

There is one cardinal rule for making a loan in California and that’s to be licensed to do so. The case struck at the heart of what MCA is all about, a sale of future card payment receivables for a discounted price today. So why would a buyer of future cash flows need a lending license? The answer is not a short one and it was a heated debate that spanned 3 years.

There is one cardinal rule for making a loan in California and that’s to be licensed to do so. The case struck at the heart of what MCA is all about, a sale of future card payment receivables for a discounted price today. So why would a buyer of future cash flows need a lending license? The answer is not a short one and it was a heated debate that spanned 3 years.

It comes as no surprise that the end result was a stalemate. Both sides exhausted their time and energy until they called it quits with a settlement. Over $4 Million dollars will be paid to the legal team representing the plaintiffs. That’s big bucks for a group that was unable to prove over the course of 3 years the need for a lending license to conduct a sale.

While the affected merchants, attorneys, and the MCA provider are eager to move on, a particular California law firm seems to have grabbed the baton. As of early March 2011, at least 3 other MCA providers are now facing the same situation. We’ve seen the court filings and it’s essentially the same challenge and question of licensed lending.

However, when considering the absolute unlikelihood that these independent lawsuits would have come together at the same time without extreme goading by their class representation attorneys, we are highly suspicious of the motives behind them. The timing implies that merchants funded by MCA provider A, MCA provider B, and MCA provider C all approached the same law firm at the same time with the same problem. This may have been possible if each provider structured a deal in the exact same manner. Rather, each provider used different contract language and there is no commonality between them outside of the tendency to all describe their product as a “Merchant Cash Advance”.

We are therefore inclined to believe this law firm is taking the “throw shit at the wall and hope something sticks” approach. Keen to the $4 Million windfall to be reaped in the case described above, it is reasonable to believe these attorneys went searching for customers of all MCA providers and invited them to be plaintiffs in their frivolous suits. There’s no precedence that they’ll win, but there is for a settlement, and a settlement could mean millions of dollars in representation fees.

Some of The Merchant Cash Advance Resource’s top connections can attest that this particular law firm spent a substantial amount of time surfing the net for all MCA providers in California. Using their web traffic analytics and tracing the activity to their domain name, it certainly appears they’re going shopping for “victims.” If we are right, expect more lawsuits from them in the next few months.

To add insult to injury, these events coincide with tough economic times. MCAs are widely celebrated as the easiest, most flexible financial option available to small businesses today. Over half a billion dollars was funded in 2010 alone. With the Federal Government struggling to do the same, it is troubling that a few slick lawyers are seeking to take the lifeline away.

Treasury offers funds to spur business lending

The SBA is in shambles, the unemployment rate is extraordinary, and banks are unwilling to lend. That’s not a great combination for America’s small business owner. Fortunately MCA providers have filled the gap. If steps are taken to discourage them from operating in California, millions of dollars will disappear from the state’s economy. That means less jobs, less sales, and less growth. And if that day should come, don’t point the finger at the Governor, The Federal Reserve, Obama, or the banks. You’ll be able to thank a few lawyers that robbed Californians for their own personal gain. The truth hurts.

– The Merchant Cash Advance Resource

What Recovery? Small Businesses are Still Suffering

August 23, 2011

Experts claim the economy is getting better, but average Americans have yet to claim the same. According to the March Discover Small Business Watch Survey, 54% of small business owners said the U.S. economy is getting worse. The sentiment seems to fly in the face of the stock market’s surge forward, as well as a declining unemployment rate. As of the latest March jobs report, unemployment ticked an inch downward to 8.8%. Sadly, the official unemployment rate does not count individuals that have been unemployed for an extended period of time or have given up looking for work altogether, traits that characterize many of the ACTUAL unemployed in this country. (Find out who the labor force consists of)

The unemployment rating system loses accuracy in prolonged recessions and therefore 8.8% is not valid, nor worth comparing to previous months. In an Interview with Reuters, Bill Cheney, the Chief Economist at John Hancock Financial Services stated, “It is always possible that as the job market improves, people will start looking again and the unemployment rate could go up.” That being said, the one true measure of the economy is the voice of the people.

improves, people will start looking again and the unemployment rate could go up.” That being said, the one true measure of the economy is the voice of the people.

As a member of the U.S. Chamber of Commerce, the Merchant Cash Advance Resource is constantly tuned in to the issues of small business owners. And guess what? We’re not hearing much positive feedback there either. The lending and capital markets continue to be a pressing factor, but federal, state, and local government regulations are stymieing innovation and expansion as well. From the Chamber, “With increasing uncertainty and government barriers threatening America’s economic recovery–Congressional leaders are reaching out to business owners to hear what is hindering their growth and what can be done to remove barriers.” (Watch the videos and interviews here)

In the face of discouraging news, access to capital is slowly making a comeback but not from the banks. Alternative financial firms providing a product known as a Merchant Cash Advance will buy your future credit card sale receivables in exchange for a big chunk of cash today. Different from a loan and becoming widely accepted, businesses all over the country are taking advantage of the most innovative form of financing available. In a true level playing field, ‘mom and pop’ shops are just as eligible as the major franchises to receive up to $250,000.

Next month, the experts could claim an unemployment rate of 0%. So long as the statistics fail to reflect reality, it becomes more frustrating for Americans who continue to live through a recession that never actually ended. High unemployment, scarce capital, and job killing regulations still plague commerce. We’re not experts ourselves, but if 54% of business owners testify that things are getting worse, they probably are. With the Dow at a 52 week high, now is a great time to sell…

– The Merchant Cash Advance Resource

Small Business Lending Faces Extinction

August 4, 2011

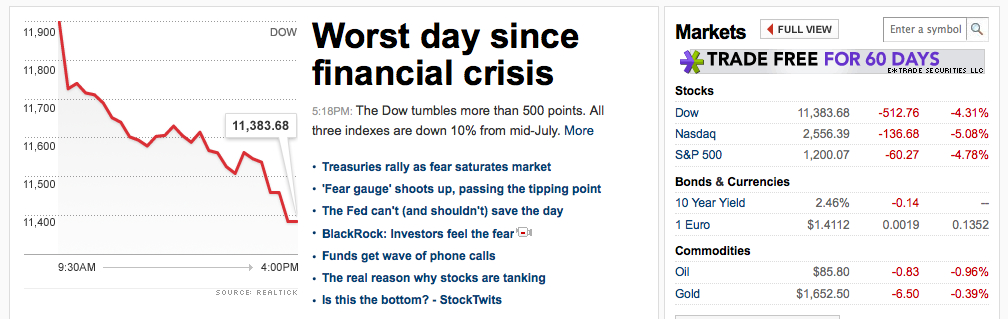

Small Business Lending is about to drop even further. It has to. Today’s 512 point kick to the groin was less about fear of the future and more about the issues we’ve been unwilling to acknowledge in the past. Let’s not water down the facts:

The economy is not growing.

There is no recovery.

There is no improvement.

That is it. There’s been far too many “growth is slow but…” rationalizations in which dismal results are chalked off as seasonal, aberrational blips, just because they don’t fit in line with our delusions of recovery. We all saw today coming, let’s not kid ourselves. See our evidence:

Seasonally Adjusted Weekly First Time Unemployment Insurance Claims:

Figures that fall below 400,000 are considered to be conducive to hiring and growth.

3/26/2011 392,000

4/02/2011 385,000

4/09/2011 416,000

4/16/2011 404,000

4/23/2011 431,000

4/30/2011 478,000

5/07/2011 438,000

5/14/2011 414,000

5/21/2011 429,000

5/28/2011 426,000

6/04/2011 430,000

6/11/2011 420,000

6/18/2011 429,000

6/25/2011 432,000

7/02/2011 427,000

7/09/2011 408,000

Source: Department of Labor http://www.dol.gov/opa/media/press/eta/ui/current.htm

News outlets have published more recent figures, with the data indicating claims above 400,000 for each of the last three weeks of July. Seventeen straight horrible weeks show no signs of improvement in the job market.

Small Business Loans Drop by $15 Billion in Q1

Greece Has 100% Chance of Default

http://blogs.wsj.com/source/2011/06/20/greece-will-default-but-not-yet

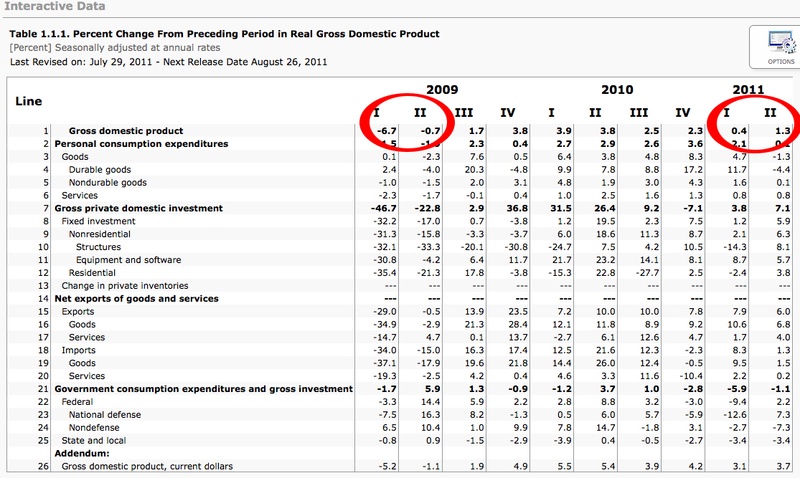

GDP is Shrinking

Rate of GDP growth is declining. The first quarter was dangerously close to a recession.

SOURCE: http://www.bea.gov/iTable/iTable.cfm?ReqID=9&step=1

U.S. Still at Risk for Debt Downgrade

http://www.reuters.com/article/2011/08/03/us-markets-forex-downgrade-idUSTRE7725ZK20110803

Food Stamp Use Rises to Record 45.8 Million

“Nearly 15% of the U.S. population relied on food stamps in May, according to the United States Department of Agriculture.”

ADDITIONAL INFORMATION: http://money.cnn.com/2011/08/04/pf/food_stamps_record_high/index.htm

Stock Market Experiences Ninth Worst Single Day Drop in History on August 4th, 2011

SOURCE: CNN Money

———

Where is the good news? There isn’t any. For the first time in a long time, the media isn’t able to keep up the recovery lie any longer. And the Federal Reservce is powerless to help. Interest rates have been kept near 0% for the past couple years and the $14,000,000,000,000+ deficit hinders their ability to issue more stimulus. Yikes!

Small business lending has been on the decline for awhile but the lack of fear in the market has kept the dirt tucked under the rug. Bankers were under the impression that there was a recovery in motion and now that they’ve become aware otherwise, it’s about to get really ugly.

To illustrate what’s already happening, a friend of ours manages the retail underwriting department for a large national bank. He spoke to us under the condition of anonymity and had this to say about their recent shift in policies:

“We are still lending but we’re using a ‘1:1 cash collateral rule’. What that means is, if a business wants to borrow $100,000 they must already have at least $100,000 in cash or cash equivalents on their books. The cash itself isn’t the collateral, it’s just a prerequisite to ensure they are especially equipped for a future cash-flow crisis. $100,000 of real collateral is still required but at this point we don’t ever want to be put in the situation where we’re chasing down a borrower to sell off their assets. Our loans don’t yield nearly enough to survive even just one default. People always joke that banks won’t lend unless the borrower doesn’t need the money. Now we won’t lend unless you already have the money!“

And so we’re entering a dark age, a slow approach back into a recession that we never actually came out of. There’s no reason to think that this will cause banks to increase lending and it is highly doubtful that it will remain at its current levels.

=====================

* Recently added. These poor creatures need your help!

=====================

So what’s the prognosis? The Merchant Cash Advance industry may soon have it’s so-called ‘Moment‘, but not because the small business community demands it, but because there won’t be anything else left…

– The Merchant Cash Advance Resource