Your Default Rate Is Too Low, And It’s Hurting You

November 22, 2022 There may be no word as terrifying to stakeholders in the merchant cash advance business than the term ‘defaults’.

There may be no word as terrifying to stakeholders in the merchant cash advance business than the term ‘defaults’.

In an industry where a significant portion of revenue is generated from daily or weekly automatic withdrawals from a merchant’s bank account, defaults can cause deep and lasting problems. Not only do they eat into profits, but they damage relationships with banks and processors- both of which are essential to the success of any merchant cash advance company. Defaults can also be contagious: if one merchant in a large portfolio decides to stop making payments, it can have a ripple effect that leads to other merchants doing the same thing.

All these are reasons why MCA companies go to great lengths to avoid defaults at all costs: they exhaustively screen merchants before approving them for funding and do all the due diligence needed to ensure they can follow realistic payment plans. They also attach a fee to every deal to cover the percentage of the deal they expect will not come back, and conventional thinking would be to aim to keep that number as low as possible.

That’s a lot of work to keep that default rate low, but what would you think if I were to contend your default rate is too low, and it’s hurting your bottom line?

Fear of defaults is paralyzing MCA funders and inevitably leading them to leave opportunities-and money- on the table.

Better Accounting Solutions has been the leading accounting firm in the MCA space for over a decade, and has seen this across the board:

Many MCA companies have adopted a risk-averse approach to avoid defaults, opting for sure-fire deals in higher positions, rather than taking calculated risks that could enhance their bottom line. In the name of capitalizing on low-risk deals with a lower chance of default, many companies choose to fund deals where they charge smaller fees than what they could be charging if they choose to fund deals others are wary of taking.

Let’s look at two deal examples for an example of my thesis:

Average Andrew is the perfect merchant for an MCA company. He is getting a $100,000 advance with a deal length of 7 months (140 days) and with his rock-solid history, his default rate is a meager 6%. The RTR on the deal is 44%, the UR fee is 7%, broker’s commission is 10%, meaning the profit on this deal will be $35,500- a net unit profit percentage of 35%, profiting $5000 a month. He is a great client, and a pleasure to work with.

Now let’s examine his buddy, Reformed Ricky. He’s made some mistakes in the past and now wants a business advance to grow the business he believes is The One. No one else wants to touch him, so you offer him a deal of $35,000. Because he is a riskier advance proposition, you can raise the RTR to 49%, and the UR fee to 12%. On a deal like this, the commission is around 14% and the default rate will be a whopping 18% on a merchant like this, but the profit to be made on this deal is $10,150- a 29% net unit profit, getting $3,383.33 monthly profit over the length of the deal.

Now, looking at the structures of both deals, why would I advocate that someone advancing Reformed Ricky instead of Average Andy? What’s the advantage of working with the weaker merchant over the perfect one?

It’s simple:

Because of his history, you can set the duration of Reformed Ricky’s deal to 60 days (3 months). That means according to the terms of his deal, your profit is 9.67% a month. You’ll be stunned to learn that when you break down your monthly profit on Average Andy’s deal, it is a considerably smaller percentage of 5.00%!

This means every month you’re making more back on the smaller deal, and are getting it to work for you by placing it into new deals and generating more income for you, because of its shorter term. If you’re only taking deals with longer outstanding balances, it will take you a considerably longer amount of time just to make a smaller profit percentage.

This means every month you’re making more back on the smaller deal, and are getting it to work for you by placing it into new deals and generating more income for you, because of its shorter term. If you’re only taking deals with longer outstanding balances, it will take you a considerably longer amount of time just to make a smaller profit percentage.

On top of this, we also have to account for the compounding effect you will quickly be seeing when you take these ‘riskier deals: because you’re earning more money per month due to the shortened duration of supposedly weaker deals, you will be able to turn it around more times per year, supercharging your growth quicker than what you’d be seeing you stuck to only ‘traditionally-safe’ deals.

I’m not advocating for funders and brokers to be irresponsible and create a new and much less entertaining version of The Big Short, throwing money around to people that don’t stand a chance of paying it back.

I am saying that they should consider funding merchants and positions they were wary of till now, and responsibly assessing the opportunities and upside for them at those positions.

Of course, this doesn’t mean that you should mindlessly funnel money into every deal that comes your way. You still need to be responsible and vet your investment opportunities carefully, and of course, if it turns out you’re picking the wrong deals and your default rate explodes, you will have to reevaluate your approach.

However, working from a place of fear is not the way to grow and thrive, certainly in this business. Moreover, by avoiding risk altogether, MCA companies are likely to become less competitive over time. After all, it’s only through taking risks and innovating that businesses can thrive in today’s rapidly changing world, especially in the rapidly evolving and growing MCA industry, where more and more people are seeking to find their niche.

A great number of successful investors in MCA companies have complained to me that their partners are too conservative with the deals they are choosing to fund and leaving too much capital in the bank, costing the investors higher facor rates instead of working for them.

This approach is a way to break away, and ahead, of the pack, because only by taking the opportunities others keep passing by will MCA companies be able to grow and compete in the long run.

Shopify Funds $507.6M in Q3, Expands MCAs and Loans to Australia

October 27, 2022Shopify Capital originated $507.6M in merchant cash advances and loans in Q3, up from $416.4M in Q2. The increase was assisted in part by the company’s expansion into Australia, bringing the total countries that Shopify funds in to four (US, UK, Canada, AUS).

Shopify is the largest e-commerce platform after Amazon but the two companies are in the same ballpark when it comes to lending originations, and Shopify is potentially doing more.

Shopify generated total revenue of $1.4B in Q3.

“In Q3, we delivered another solid quarter of GMV, revenue, and gross profit dollar growth against the high inflationary environment,” said Amy Shapero, Shopify’s CFO. “From an operational perspective, we recalibrated our organizational structure, successfully rolled out a new compensation framework, and began integrating Deliverr into Shopify. Looking ahead, the flexibility of our platform, breadth of solutions, pace of innovation, and disciplined investment approach position Shopify well to realize the enormous opportunity ahead.”

Lavu Adds MCA Product Through Partnership With Parafin

October 7, 2022 It’s not just DoorDash that Parafin has partnered up with to provide MCA funding. Last week, the restaurant software company Lavu launched Lavu Capital to help restaurants owners access capital.

It’s not just DoorDash that Parafin has partnered up with to provide MCA funding. Last week, the restaurant software company Lavu launched Lavu Capital to help restaurants owners access capital.

“We are a restaurant software company that focuses on small and medium restaurants,” said Saleem S. Khatri, CEO of Lavu. “Think of your favorite restaurants that have one or two locations that are really really popular, that are ingrained in the community. We do everything from point of sale to online ordering, payment processing, and anything a restaurant would need to start and grow their business.”

Khatri said that one thing they noticed is that these restaurants have a fundamentally hard time getting loans and that led them to connect with Parafin. Parafin’s product is an advance on future sales, not a loan, and their offerings have been simply integrated into Lavu’s technology. Parafin automatically generates an offer for restaurant owners that they can see in their Lavu dashboard.

“…it’s just really beautifully designed,” said Khatri. “It basically says, ‘Hey, you have an offer to borrow up to $5,000. Do you want it yes or no?’ And you just click ‘yes’ and you’re good to go, the money deposits straight into your bank account, and then you have a repayment schedule. And it just pulls it directly from your bank account according to that repayment schedule.”

Khatri says they haven’t really begun to market the product yet and they’ve just started off with a limited base of customers but that the plan is to roll it out to all their customers around the US. They’d even do it with their customers outside of the US if they could, but the tech is not set up to do that just yet.

“This is going to be a feature and an offering that really really benefits our customers because it gets to the heart of what they need, which is they’re in constant need of liquidity, they’re in constant need of kind of tools to run their business better,” Khatri said. “And it just really fits our portfolio of products that we offer to these customers. So the reception has been awesome.”

The Merchant Marketplace Announces Its New Launch with Industry Powerhouse Executive

September 19, 2022 BALDWIN, NEW YORK SEPTEMBER 19, 2022 – The Merchant Marketplace, a leading fintech platform provider of direct financing to small and midsize businesses, announced today the launch of its new leadership with backing from industry powerhouse executives. The company’s new leadership team brings over 75 years of collective financial, technology, and business experience within its core leadership group: Adam Schwartz as CEO and Kevin Harrington, the Original Shark Tank Investor, will serve as a Strategic Partner. This partnership will revolutionize how merchants and independent sales organizations (ISO’s) obtain capital for growing their merchant’s businesses, changing the game for entrepreneurs throughout the United States.

BALDWIN, NEW YORK SEPTEMBER 19, 2022 – The Merchant Marketplace, a leading fintech platform provider of direct financing to small and midsize businesses, announced today the launch of its new leadership with backing from industry powerhouse executives. The company’s new leadership team brings over 75 years of collective financial, technology, and business experience within its core leadership group: Adam Schwartz as CEO and Kevin Harrington, the Original Shark Tank Investor, will serve as a Strategic Partner. This partnership will revolutionize how merchants and independent sales organizations (ISO’s) obtain capital for growing their merchant’s businesses, changing the game for entrepreneurs throughout the United States.

“We are looking to change the industry by using a true fintech platform to facilitate transactions amongst ISO’s, merchants, and the Merchant Marketplace,” said Merchant Marketplace CEO Adam Schwartz. “We understand the challenges many small business owners face when trying to secure financing to help make their dreams a reality. The Merchant Marketplace is happy to be a resource for entrepreneurs by providing them access to capital so they can build a successful business.”

The Merchant Marketplace created a proprietary syndication platform that offers real time data and full transparency. In most instances, the company will offer ISO’s a two percent syndication as bonus for every deal that it funds, with the ability to syndicate more funding if needed. ISO’s can earn another stream of income by being vested in every deal they fund with the Merchant Marketplace, as well as earn a referral fee. The platform also offers a profit-sharing program and technology tutorials to show ISO’s how to engage with the platform to help achieve the best end results.

“The merchant cash advance market has been witnessing an escalation in growth over the past few years with the help of innovation. Our technology integrates with over 25 different third parties to give us complete insights into our merchants, giving us the ability to make offers with lightning speed and efficiency. We understand the needs of our clients and we want them to be part of the process. We do not want to be seen as just another funder; we want to be seen as a business partner for our ISO’s,” said Merchant Marketplace Director of ISO Relations, Justin Strull.

For questions on the service and to sign up as an ISO, contact Justin Strull at 516-980-4932 or email in to justin@merchantmarketplace.com

About Kevin Harrington

As an original “shark” on the hit TV show Shark Tank, the creator of the infomercial, pioneer of the As Seen on TV brand, and co-founding board member of the Entrepreneur’s Organization, Kevin Harrington has pushed past all the questions and excuses to repeatedly enjoy 100X success. His legendary work behind the scenes of business ventures has produced more than $5 billion in global sales, the launch of more than 500 products, and the making of dozens of millionaires. He’s launched massively successful products like The Food Saver, Ginsu Knives, The Great Wok of China, The Flying Lure, and many more. He has worked with amazing celebrities turned entrepreneurs including, Billie Mays, Tony Little, Jack LaLanne, and George Foreman to name a few. Kevin’s been called the Entrepreneur’s Entrepreneur and the Entrepreneur Answer Man, because he knows the challenges unique to start-ups and he has a special passion for helping entrepreneurs succeed.

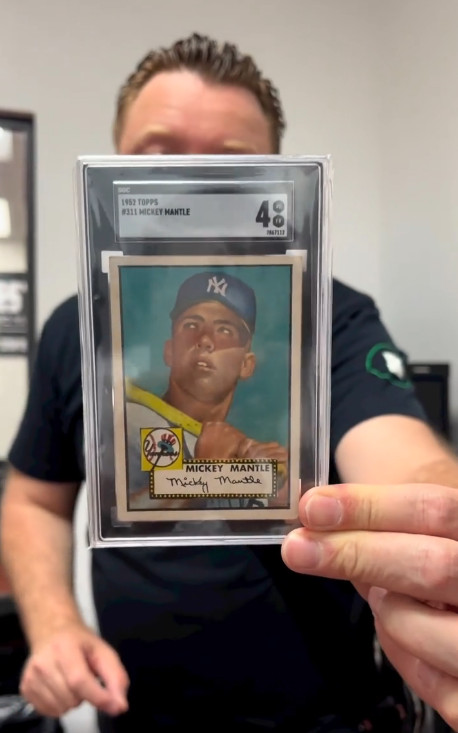

Got a Mantle, Bryant, or Mahomes Card? This Company Wants to Fund You

September 12, 2022 Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

The value of the Mantle sale came as no surprise to one budding entrepreneur in South Florida. On Instagram, he’d been talking about Mantle cards for weeks, even going so far as to hold up another ’52 Topps Mantle card to the camera to promote what his company can do, which is provide quick cash advances to owners of valuable sports cards.

The entrepreneur’s name is Edward Siegel, CEO of Card Fi. Siegel’s no stranger to the alternative finance space because he spent about a decade in the MCA industry, most recently as the founder of Bitty Advance, which he sold in 2020. Since then, Siegel returned to his roots and early passion of his youth.

“I had a background in sports cards as a collector, you know as a kid, but then in my early twenties, I was promoting card shows at malls,” Siegel said. “I was heavily into the hobby, setting up the card shows and promoting them and doing player appearances where players come in and do an autograph appearance.”

That was back in the late 80s, early 90s, according to Siegel.

When Covid hit and he exited his most recent company, he noticed a massive resurgence in the sports trading card market. His next business ultimately became Card Fi, a company that will evaluate the market value of a card and make an advance against it. There’s obviously risk involved so they take possession of the card for the duration.

“We have to get a hold of these cards and we’re responsible for them and then we vault them in our in-house bank vault,” Siegel said. The cards are stored in a highly secure climate controlled environment. Card Fi shows the vault off frequently in its Instagram videos.

Such a business requires large amounts of capital so Siegel went searching for investors, a pursuit that led him to a unique place, an Instagram Live pitch competition hosted by famed CEO and reality TV star Marcus Lemonis. Siegel entered himself in as a contestant, knowing full well that the odds of even being chosen to present his business to Lemonis were about a million-to-one.

Somehow, he was called up to pitch.

“So [businesses] went on there during the quarantine and you pitched your business,” Siegel explained. “I went on there and I pitched it […] And he understood it and he thought it made sense.”

The moment eventually led to a deal with Lemonis’ company and Card Fi was on its way.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

“If we look at it, there’s two different markets, you have the modern card market [where] I would say it’s basketball [that leads the pack],” he said. “For the vintage card market it’s baseball.”

Football is huge as well, he explained. A Patrick Mahomes rookie card, for example, an NFL Quarterback that’s still currently playing, recently fetched $861,000. There are only one of five like it in the world, the scarcity playing a major role in the value. Meanwhile, a Justin Herbert rookie card, an NFL Quarterback who’s only in his third year was already receiving bids above $1 million at the time this story was being written.

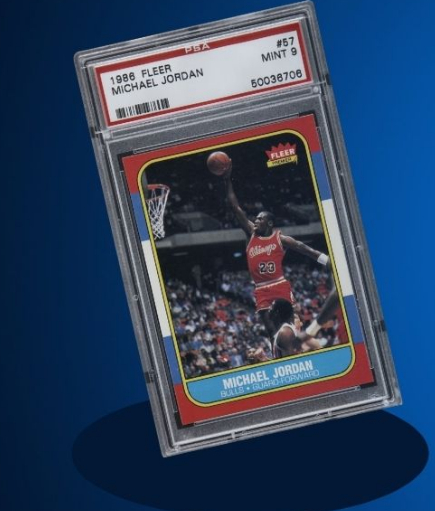

“It really depends on the card itself,” Siegel explained. “Some players might be known for having better careers but then you have cards that have more scarcity to them. Something that’s a one of one or maybe a very low populated card and a graded PSA 10 could very well be worth more than a [Michael] Jordan rookie because it has scarcity in it.”

PSA refers to cards that have been verified as authentic and graded on the condition of the card itself. Ten is the highest level a card can receive. Card Fi will only work with graded cards to avoid any funny business when it comes to advancing funds based upon the value.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

“This financing benefits the market as loans and cash advances have become an increasingly asked-for offering among trading card collectors,” said Chad Fister, PWCC’s CFO in a story that originally appeared on Sportico. “Enabling our clients to access liquidity through a menu of capital offerings is key as trading cards continue to prove themselves to be a valuable tangible asset class.”

For Card Fi, customers that take an advance can track everything through an online portal, including details about their cards, payments, and balance.

“We want to note that we built a full-service automated underwriting and collection platform to where, whether it’s the customer or the broker, they can log into our system and put the description of the card into the system and it’s going to automatically underwrite it and price it out,” Siegel said.

That description sounded like something straight out of the fintech industry of his past, especially the component about brokers.

“Just like the MCA space, we have a whole partnership side, a broker side, where brokers can refer us customers just as an affiliate where they just send the info over,” Siegel said. Similarly, they can earn a commission if a transaction is completed, he explained.

In this industry, brands like Topps, Upper Deck, and Panini have become the bread and butter for Card Fi. Even though it’s all business for Siegel these days, he couldn’t help but mention a particular card he had a personal attachment to.

“My personal favorite card in my collection is the 1965 Topps Joe Namath rookie card,” Siegel said. “Of course being a die hard New York Jets fan, that has to be my favorite card.”

Grand Opening of Latin Financial’s New Office Joined by Public Officials, Family, and Friends

June 4, 2022 Just a few miles outside of Hartford, cars exited the highway and advanced towards a quieter part of Connecticut. The aptly named “Beaver Road” is home to Wethersfield’s US Postal Service building on one side and the Connecticut Farm Bureau building on the other. Drivers veered towards the latter and pulled into a parking lot situated behind a literal babbling brook. There are other tenants besides the Farm Bureau in the expansive brown-bricked commercial-use building as indicated by a sign outside, but the business that people had come to celebrate hadn’t even been added to it yet.

Just a few miles outside of Hartford, cars exited the highway and advanced towards a quieter part of Connecticut. The aptly named “Beaver Road” is home to Wethersfield’s US Postal Service building on one side and the Connecticut Farm Bureau building on the other. Drivers veered towards the latter and pulled into a parking lot situated behind a literal babbling brook. There are other tenants besides the Farm Bureau in the expansive brown-bricked commercial-use building as indicated by a sign outside, but the business that people had come to celebrate hadn’t even been added to it yet.

Nevertheless, the blue and white balloons waving in the wind outside the back entrance were a clue that this was the right place. Inside, on the first floor, a line of people found the large plated logo of Latin Financial, a small business that helps other small businesses obtain working capital.

Already personally acquainted with the firm led by Sonia Alvelo, she led myself and others on a tour of the company’s new space. Latin Financial employees were easily identifiable by their blue company shirts, but others wore green to signal that they were part of a sister company named Sharpe Capital. Sharpe is spearheaded by Brendan P. Lynch.

Both brands previously operated in nearby Newington but outgrew what they had. When the ceremony officially kicked off with some impromptu speeches, the prominence of those assembled became evident. It included, among others, the Better Business Bureau, the local Chamber of Commerce, and the Connecticut Children’s Hospital.

Wethersfield’s mayor, Michael Rell, was also there. Rell welcomed Latin Financial to the neighborhood, echoing the note sang by other government officials.

Connecticut State Senator Matthew Lesser shared his appreciation for Alvelo and her company’s mission to provide capital to underserved small businesses both in the state and across the nation. Lesser explained that the state legislature had recently decided to delay a proposed commercial financing bill (Senate Bill 272) so that it could further assess the input from companies like Latin Financial and the potential impact it would have before moving forward. A version of the bill will be reintroduced next year.

Meanwhile, Joseph Rodriguez, Deputy State Director for US Senator Richard Blumenthal’s office, said that he was impressed by the company’s accomplishiments and contributions to the community. He presented Alvelo with a Certificate of Special Recognition signed by Blumenthal in honor of her new office and for her service to Connecticut Small Businesses.

Werner Oyanadel, Latino and Puerto Rican Policy Director at the Connecticut General Assembly’s Commission on Women, Children, Seniors, Equity & Opportunity, said that Alvelo had “been a good partner of [their] work at the Capitol” and that “Latin Financial is filling a big void assisting new businesses and Latino entrepreneurs’ access to needed reources.”

Employees of both Latin Financial and Sharpe appeared excited by all the fanfare while friends and family members were proud to share in the moment. Alvelo ceremoniously cut a blue ribbon for the cameras and in conversations that followed it became known that they were hiring.

Alvelo has previously spoken at Broker Fair in New York and AltFinanceDaily CONNECT Miami. She has been a primary source of information for AltFinanceDaily since 2016 on matters regarding small business financing in Puerto Rico.

Business Loan Seekers Likely to Consider Numerous Options, Study Says

April 25, 2022 New data published in the annual FinTech Lending Study published by Smarter Loans revealed that 40% of business loan seekers compare more than six options.

New data published in the annual FinTech Lending Study published by Smarter Loans revealed that 40% of business loan seekers compare more than six options.

Though this study focused on the Canadian market, it may partially explain a finding in the US, that more small business owners seeking capital are seeking out a merchant cash advance as a potential option than ever more. (A Federal Reserve study said that 10% of SMB capital seekers sought a merchant cash advance in 2021). That would make sense if business owners are obsessively applying to multiple sources for the sake of making more comparisons.

But even while they shop, they might not always be satisfied with what they learn, nor the outcome. Smarter Loans reported that only 60% of business loan seekers felt informed about their options while 40% of business owners that went forward with a business loan were not satisfied with their loan provider.

When examining both the business loan and consumer loan market, Smarter Loans says that loan seekers are more likely to receive their funds the same day they apply than ever before. (53% of those surveyed received funds within 24 hours of applying.)

Click here To view the full 2022 FinTech Lending Study published by Smarter Loans.

New Domain Name Gold Rush Sets Up Possible Battle for Future of SMB Finance

April 25, 2022 If you could have businessloan.com or businessloans.com as your website, would you jump on the opportunity to get it?

If you could have businessloan.com or businessloans.com as your website, would you jump on the opportunity to get it?

It’s evident that the market for keyword-based domains has evolved over time. Couldn’t get the .com? You could’ve tried to get the less coveted .net or .org. Don’t like those? Today, you can get the .business, .deals, .financial, .loan, .loans, or hundreds of other customized tlds. With so many to choose from, most experts in the field would advise that if you don’t own the .com version, to not even bother getting cute with customizations for your brand or keyword because customers will just get confused.

But recently, another domain name market has quietly been gaining steam. It’s for something called a .eth, an Ethereum blockchain-based crypto address shortener by the Ethereum Name Service. It’s not necessarily something one could use to build a website with, at least not yet. Originally envisioned as a way to condense long impossible-to-remember crypto wallet addresses into memorable words, users have started to buy up a bunch of keywords that may be familiar to AltFinanceDaily readers. Just to name a few:

- businessloan.eth

- businessloans.eth

- smbloans.eth

- merchantcashadvance.eth

- ach.eth

- syndication.eth

- lending.eth

- ppploan.eth

- underwriting.eth

- brokers.eth

- loanbroker.eth

- mca.eth

- factoring.eth

- funding.eth

- backdoored.eth

At face-value, this might appear to be a vanity crypto play, one in which one could send crypto to your-name-here.eth instead of trying to type out a long address like: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. But an ENS domain name holds much more potential than just that. It’s moving towards becoming the backbone of one’s identity in the upcoming era of the web called web 3.0 (web3 for short). Instead of having to remember passwords for hundreds of websites, identity can be validated through one’s digital wallet. Such a concept is not theoretical. It’s already being used.

Take seanmurray.eth for example. You could send eth, bitcoin, litecoin, or dogecoin to it, but at the same time it’s connected to an email address and a url (this one). Plus it’s linked to an NFT avatar (broker #7 from The Broker NFT collection) which is in that wallet. I can use it to do an e-commerce online checkout in 5 seconds without ever needing to enter any payment information even if I’ve never visited the site before. It’s faster than PayPal and with less steps involved. I can connect it to my twitter account, OpenSea, or use it to vote in an official poll without ever having to create an account on something. The wallet is the identity verification. The .eth name, therefore, has the potential to become the defining baseline of who or what one is on the internet. Not theoretically. It’s already happening.

Take seanmurray.eth for example. You could send eth, bitcoin, litecoin, or dogecoin to it, but at the same time it’s connected to an email address and a url (this one). Plus it’s linked to an NFT avatar (broker #7 from The Broker NFT collection) which is in that wallet. I can use it to do an e-commerce online checkout in 5 seconds without ever needing to enter any payment information even if I’ve never visited the site before. It’s faster than PayPal and with less steps involved. I can connect it to my twitter account, OpenSea, or use it to vote in an official poll without ever having to create an account on something. The wallet is the identity verification. The .eth name, therefore, has the potential to become the defining baseline of who or what one is on the internet. Not theoretically. It’s already happening.

Crypto is already starting to creep into the small business finance industry. In August, a funding company announced that it would begin offering commissions and fundings in crypto because of the speed potential. Far from being a gimmick, brokers started to choose crypto payments over ACH or a wire because of how fast it would be. There’s also no chargeback risk with crypto.

Currently, the owner of mca.eth has listed the domain for sale on OpenSea at a price of 20 eth (approximately $60,000). That’s less than what MerchantCashInAdvance.com sold for in 2011. Perhaps the value of an Ethereum Name Service domain holds less promise than a website that ranked well on Google in 2011. But then again, being well ranked on Google is not as important as it used to be. It’s impossible to say what, if any impact web3 will have on the small business finance industry long term, but for now there are those out there quietly buying up names like ach and funding and syndication on the chance that they will become something.