How Regulators Like to Be Approached

October 22, 2018

On the first day of Money 20/20 yesterday, a panel of current and former regulators discussed how the regulatory environment can help emerging fintech companies and how the leaders of such companies ought to interact with regulators. “How do regulators want to be approached?” was a question presented to the panel.

“The first person I hear from I don’t listen to,” said Paul Watkins, Director of the Office of Innovation for the U.S. Bureau of Consumer Financial Protection (BCFB). He clarified with AltFinanceDaily after the panel discussion that this is in reference to his previous regulatory role as Civil Litigation Division Chief at the Arizona Office of the Attorney General. He said that this “first person” he doesn’t listen to refers to the lobbyist. Watkins continued: “The second person might have something interesting to say and the person who is quiet maybe knows what’s going on, and I’m interested to learn from them.” The “second person,” he explained, might be the CEO of a company and the “quiet person,” he said, would often be a non-senior level employee at a company who really sees what’s happening on the ground level.

Melissa Koide, who once served as the U.S. Treasury Department’s Deputy Assistant Secretary for Consumer Policy, said that she always appreciated hearing directly from the innovators themselves about their relationships with banks.

“It can be valuable to make trips to [visit regulators,]” Koide said.

Koide is now CEO of FinRegLab, a financial services research organization that examines how technology and data can help achieve public policy that leads to a more efficient and inclusive marketplace.

Chris Camacho, President and CEO of the Greater Phoenix Economic Council said that elected officials want to hear from industry leaders.

“Engage [legislators] thoughtfully and educate them,” Camacho said.

GOING NATIONAL: How David Gilbert Built One of the Largest Small Business Lenders in the Country

October 17, 2018 When Ty Austin, who owns a florist shop in West Palm Beach, secured a $5,000 loan from National Funding last year, he was happy to have working capital and could build inventory for mini-gardens and landscaping,

When Ty Austin, who owns a florist shop in West Palm Beach, secured a $5,000 loan from National Funding last year, he was happy to have working capital and could build inventory for mini-gardens and landscaping,

The experience, moreover, was surprisingly pleasant. “The guy I worked with was really cool,” Austin says, referring to the sales representative at the San Diego-based financial technology firm. “It turned out that he was getting married and I ended up giving him and his fiancé advice on floral arrangements.”

The borrowing worked out so well that the Floridian, who is 46 and the sole proprietor of Austintatious Designs, re-upped for a second loan of $12,000 to help purchase a commercial van. The van will be used to transport flowers, plants and tools while doubling as a billboard-on-wheels. “It gives me more ‘street cred,’” he jokes.

To register his approval with National Funding, Austin went online to TrustPilot and posted a rave review of the sales rep: “James Johnson Rocks!”

Pam, a Texas wellness coach who provides clients with an array of holistic health therapies, needed extra money to buy an infrared sauna to add to her portfolio of services. But her credit rating was “poor,” she told AltFinanceDaily in an e-mail interview, “from when I changed careers and lost my health and struggled to make my credit card and student loan payments on time.”

Like Austin, Pam — who asks to be identified by her first name —found National Funding through an online search. And she too secured $5,000, although her transaction was structured as a merchant cash advance, rather than a loan. The terms of the MCA require a daily debit from her bank account. She reckons that the total cost of the MCA to be roughly $1,500.

Pam pronounces herself satisfied with the deal and mightily impressed with the way National Funding treated her. The process took about three days — and would have gone even quicker if she’d located her professional licenses sooner. Best of all, she says, the agent at the company tailored the financing to suit her circumstances. “They were great as far as getting my questions answered, even listening to my past situation, which others may not have cared about,” she says.

Pam pronounces herself satisfied with the deal and mightily impressed with the way National Funding treated her. The process took about three days — and would have gone even quicker if she’d located her professional licenses sooner. Best of all, she says, the agent at the company tailored the financing to suit her circumstances. “They were great as far as getting my questions answered, even listening to my past situation, which others may not have cared about,” she says.

“They really wanted to get me an option that they knew I’d be able to repay,” Pam adds. “They said they were in the business of helping small businesses grow rather than putting them in a hard financial situation.”

The positive experiences that Austin and Pam had with National Funding are not isolated instances. Rather, they are representative of clients’ dealings with the company. Witness its online reviews from business borrowers at TrustPilot which go back three years, run for 36 pages, and merit National Funding a 9.4 rating on a scale of 10. That’s a straight-A grade on any report card. Although there’s the occasional naysayer — four percent assert that their experience was “poor” or “bad” (and some negative comments can be blistering) — the weight of the reviews is almost embarrassingly positive.

Typical postings find that National Funding and its agents win kudos for, among other things, being “prompt and professional,” providing service that is “hassle free and about as friendly as you can be,” and even being “accommodating and gracious.” A man named Al McCullough spoke for many when he declared: “My experience was great. Professional and on time. Couldn’t ask for more.”

All of which helps account for why National Funding — its 230 employees working out of a sleek suburban office building guarded by a tall stand of palm trees in San Diego — is a rising star in the world of alternative business lending and financial technology. In 2017, the company raked in $94.5 million in revenues, a 24.8 percent bounce over the $75.7 million recorded a year earlier and nearly fourfold the $26.7 million posted in 2013.

All of which helps account for why National Funding — its 230 employees working out of a sleek suburban office building guarded by a tall stand of palm trees in San Diego — is a rising star in the world of alternative business lending and financial technology. In 2017, the company raked in $94.5 million in revenues, a 24.8 percent bounce over the $75.7 million recorded a year earlier and nearly fourfold the $26.7 million posted in 2013.

In recognition of the company’s three-year growth rate of 142%, Inc. magazine included National Funding in its current list of the country’s 5,000 fastest-growing companies, the lender’s sixth straight appearance on the coveted roster. Since its inception in 1999, National Funding reports that it has originated more than $2 billion in loans to some 35,000 borrowers.

The company’s impressive performance has similarly merited accolades for David Gilbert, the 43-year-old chief executive who started the company on little more than a shoestring and whom employees regularly describe as “visionary.” Among Gilbert’s trophies: Accounting firm Ernst & Young recently presented him with its “Entrepreneur of the Year 2017 Award” for San Diego finance.

At first glance, the San Diego financier doesn’t look too much different from its cohorts. The company proffers unsecured loans of $5,000 to $500,000 to a mélange of small businesses in all 50 states and across multiple industries, including retail stores, auto repair shops, truckers, construction companies, heating-and plumbing contractors, spas and beauty salons, cafes and restaurants, waste management, medical and dental clinics, and insurance agencies.

To qualify for financing, a prospective borrower should have been in business for a year, have at least $100,000 in revenues, and boast a personal credit score of at least 500. While there’s no collateral required for loans, National Funding insists on a personal guarantee. The website reviewer NerdWallet cautions borrowers that this “puts your personal assets and credit at risk if you fail to repay the loan.”

Along with unsecured loans, National Funding offers equipment leasing – usually for heavy trucks and construction equipment – as well as merchant cash advances. The equipment lease is secured by the machinery. As in the case of Pam, the wellness coach cited above, MCAs are debited daily, the money automatically withdrawn from bank accounts.

There are a number of businesses that National Funding disdains, no matter how stellar their credit. “We won’t finance casinos, strip bars, tobacco, or firearms,” Gilbert says. “We’re not going to support industries like that.”

For CEO Gilbert, doing business ethically is a signature feature of the company. Among other things, National Funding presses its salespeople to steer clear of putting people into dodgy loans that are likely to default. “We’re lending capital,” Gilbert says, “and one of our core values is the way we support our customers. Are we placing people with the right product to meet their needs or are we being selfish? The best way to be customer oriented is to get a better understanding of what capital will do for them.”

That corporate ethos, coupled with the company’s remarkable performance, has raised its profile while earning it a measure of esteem among industry peers. “What I do know about National Funding,” says Douglas Rovello, senior managing partner at Fund Simple, a lender and broker in the Tampa area, “is that they have five or six different programs and set their rates high but competitively. They’re known for fitting their products to a client’s needs,” he adds. “And in a business that has its share of bad actors, they have a reputation as a company with a conscience.”

A company with a conscience. Customers come first. And yet National Funding turns heads with its sales production of roughly 1,000 financings a month and triple-digit growth rate. So how do they it? A good place to start is with Gilbert, whose leadership skills, business acumen, and second-to-none work ethic “set the tone,” says Kevin Bryla, the company’s 52-year-old chief marketing officer.

For his part, Gilbert credits his family background and an upbringing in which education and academic achievement were strongly encouraged. The fifth of six children, he’s the only one who opted for a business career. “There are three doctors, two lawyers – and me,” Gilbert says.

The son of a prominent physician, his mother a homemaker and volunteer docent at the nearby Nixon Library for the past 25 years, Gilbert grew up in Yorba Linda. He attributes his keen interest in business to observing how his father, a pathologist, operated his own laboratory, which employed 60 people. “It was the business side of medicine that fascinated me,” he asserts.

The son of a prominent physician, his mother a homemaker and volunteer docent at the nearby Nixon Library for the past 25 years, Gilbert grew up in Yorba Linda. He attributes his keen interest in business to observing how his father, a pathologist, operated his own laboratory, which employed 60 people. “It was the business side of medicine that fascinated me,” he asserts.

Even so, his two closest friends at the University of Southern California — fraternity brothers Marc Newburger and Sean Swerdlow– tell a somewhat different story. They remember Gilbert as someone who found his true calling, his métier, during his college years. Enrolled initially in pre-med courses, he was a diligent student but, his friends assert, manifestly unsuited for a career in medicine.

“Formative,” says Swerdlow, the older of the two fraternity brothers and now a management consultant based in Southern California, “would be a very good word” to characterize that period during which Gilbert abandoned medicine in favor of the world of commerce. In 1997, he earned a bachelor’s degree in business administration “with an emphasis in entrepreneurship.”

But it was fraternity life just as much as the classroom, his friends agree, that shaped him and foreshadowed his future. “It wasn’t ‘Animal House,’” Swerdlow says of Alpha Epsilon Pi. “We boasted the highest GPA (grade point average) on fraternity row.”

Nonetheless, Gilbert took to the social life and camaraderie that the fraternity offered with gusto, and his friendship with the colorful Newburger was especially fateful. A freewheeling entrepreneur today, Newburger takes a measure of credit — Gilbert’s disapproving parents might have preferred the word “blame” — for contributing to his fraternity brother’s metamorphosis. “Dave hated all of his pre-med classes,” Newburger insists. “He had zero stomach for it. He was so much like I was: a natural people person and a born entrepreneur.”

Newburger is the quintessential soldier of fortune. After college, he tried his hand as an actor, supporting himself by playing poker and getting paid to be a contestant on TV game shows including “The Dating Game,” “Card Sharks,” and “3’s A Crowd.” He’s now the co-president and co-inventor of Drop Stop, a patented device that “minds the gap” between a car’s front seat and the console and prevents coins, keys, glasses, and mobile phones from disappearing down that rabbit hole. (Drop Stop really took off after Newburger and his business partner appeared on the television show “Shark Tank” and scored a $300,000 capital injection from celebrity-investor Lori Greiner who took a 30% stake in the company and slapped her name on the brand.)

Back at the frat house, Newburger and Gilbert collaborated on business ventures. The pair once sold T-shirts sporting an off-color message about USC’s archrival, the University of California at Los Angeles. “The (anti-UCLA) message was pure hatred,” Newburger recalls. “But it was just for the day of the football game and it was all in fun.”

At first, sales at the stadium were lackluster. USC students kept trying to bid down the price or importune them to throw in an extra tee. As for the game itself, USC’s chances for victory looked equally unpromising. As time ran out, however, the Trojan quarterback completed a Hail Mary pass and USC won. The two fraternity brothers grabbed the bundle of shirts and sprang into action. “We got to the exit just in time and sold out in a matter of seconds,” Newburger recalls.

Newburger takes credit too for introducing his friend to Las Vegas’ gaming tables. Gilbert, his friend says, immediately demonstrated a knack for counting cards, handling money, and taking risks. “It was typically blackjack,” recalls Swerdlow, who sometimes accompanied them. “We didn’t have much money then. But there were moments when Dave would bet a big pile of chips. He’s willing to make a bet and live with the consequences.”

Sports are another of Gilbert’s enthusiasms. His friends say that, whether he’s returning serve at ping pong or standing over a putt — he plays to an 11 handicap at golf – he wants to win. Remarks Newburger: “He’s competitive to the point that — when he beats you — he wants the Goodyear blimp flying overhead to announce his victory.”

Gilbert, who is married with two children, is legendarily loyal to friends and family. While most members of a college fraternity might keep up with old companions after graduation by exchanging greeting cards and attending college reunions, Gilbert goes the extra mile.

He once footed the bill for Swerdlow to travel with the USC football team to an away game, arranging it so that his fraternity brother could view the action from field-level. After Newburger had a recent health scare (no worries, he’s O.K.), Gilbert rounded up a couple of dozen fraternity brothers and their wives (or companions), and put together a four-day bash in his buddy’s honor. The event was held at Cabo, the Mexican beach resort in Baja California, and Gilbert underwrote a fair amount of the cost. “He shares his success with his friends,” Newburger says, adding: “I don’t know anybody who works harder on friendships.”

He once footed the bill for Swerdlow to travel with the USC football team to an away game, arranging it so that his fraternity brother could view the action from field-level. After Newburger had a recent health scare (no worries, he’s O.K.), Gilbert rounded up a couple of dozen fraternity brothers and their wives (or companions), and put together a four-day bash in his buddy’s honor. The event was held at Cabo, the Mexican beach resort in Baja California, and Gilbert underwrote a fair amount of the cost. “He shares his success with his friends,” Newburger says, adding: “I don’t know anybody who works harder on friendships.”

Many of the personality traits described by friends and colleagues — tenacity and competitiveness, self confidence and leadership — played a key role in the development and success of National Funding, which Gilbert founded just two years out of college with $10,000 borrowed from his uncle, Howard Kaiman, of Omaha.

He’d worked a couple of quick jobs right after college, including a stint at small-business lender Balboa Capital, but he was always destined to be his own boss. Gilbert’s start-up was called Five Point Capital and, at first, it was located in the affluent Chatsworth section of Los Angeles and concentrated on equipment leasing.

“The first two years we were a cold-calling company and then we got into direct mail and saw some success and then we moved to San Diego and started to scale up the company,” Gilbert says. The decampment, he explains, was “for the quality of life, but we also felt we could hire from a better talent pool than L.A. We wanted to set ourselves apart.”

By 2007, Five Point was cranking up operations, revenues shot to $28 million and its headcount totaled 210 employees. “Then the Great Recession hit” in 2008-2009, Gilbert says. The company was forced to furlough 140 employees, two-thirds of its workforce. Yet even as it retrenched, the company managed to branch out. It began making merchant cash advances, Gilbert says, and, also in 2007, it linked up with CAN Capital to do broker financings. “We were pretty well known and they were looking for partners for factoring and leasing,” Gilbert explains.

It took time to recover after the financial crisis. But by 2013 – the year that Gilbert re-branded his company “National Funding” – the company was able to hire back as many as 15% of its laid-off employees (most had found other jobs, in many cases relocating to Silicon Valley, Gilbert reports). By then, the company had secured a $25 million credit facility from Wells Fargo Bank, which allowed it to move up the food chain to “become a balance-sheet lender,” Gilbert says, and offer a wider selection of financing options.

Key to driving the company’s phenomenal growth has been its flood-the-zone marketing and sales strategies. The company spends $16 million annually on marketing using a full panoply of channels and media, both online and offline. These include direct mail and targeted marketing, paid advertising, search-engine optimization or SEO, and sports sponsorships. “We try to build a whole range of marketing mechanisms,” explains marketing chief Bryla, “and when you get the mix right, they all help each other.”

Gilbert is a big believer in the benefits of sports marketing, the company’s website featuring the logos of the San Diego Padres (baseball), and Anaheim Ducks and Los Angeles Kings (hockey). Ever the faithful alumnus, Gilbert and his company back USC football as well. During the 2015 2016 college football season, the company paid for naming rights for what became, for one night, the “National Funding Holiday Bowl” at Qualcomm Stadium.

Gilbert is a big believer in the benefits of sports marketing, the company’s website featuring the logos of the San Diego Padres (baseball), and Anaheim Ducks and Los Angeles Kings (hockey). Ever the faithful alumnus, Gilbert and his company back USC football as well. During the 2015 2016 college football season, the company paid for naming rights for what became, for one night, the “National Funding Holiday Bowl” at Qualcomm Stadium.

Janet Fink, department chair at the McCormack School of Sports Management located at the University of Massachusetts-Amherst, told AltFinanceDaily that sponsorship programs can easily cost a million dollars or more. “It’s not cheap,” she says. “When a company sponsors a team, they get a number of benefits. One is that they get to put the team’s logo on their website. The idea is that fans are passionate or have an affinity for the team and that it will rub off on a sponsor.

“Sports enthusiasts,” Fink adds, “often make good customers. When you have enough disposable income to go to these sporting events, you’re probably a good prospect for a loan.”

The sponsorships — which include civic involvement such as offering Holiday Bowl tickets to members of San Diego’s large military contingent as well as to company employees — also build good will in the community and team spirit among the workforce. (National Funding also makes an effort to hire veterans, says Bryla.)

Gilbert believes in the old adage that you have to spend money to make money. The company spends $14 million rewarding its network of outside brokers. Inside the company, high-performing salespeople are compensated with commissions, bonuses and an assortment of rewards, including resort trips.

But sales representatives’ must conform to company guidelines. Justin Thompson, National Funding’s sales chief, explains that the “customer comes first” philosophy is not just a slogan but a core value. “We’re not a factory spitting out widgets,” Thompson says. “We’re here to build relationships and sell a repeatable product. We want that customer to come back to us. Every loan is customized. Six of ten customers who pay off their loans come back for a second financing. Whether your business is dog grooming or you’re an asphalt company,” he adds, “people will do business with people they like and trust.”

Using the software program “customer relationship management” (CRM), National Funding expends a lot of effort gathering data on its business customers and extrapolating the information for use in credit evaluations. But the use of technology only goes so far.

Gilbert reckons that the art of the deal involves about “70 percent algorithm and 30 percent people.” He adds, “You still need the people component to look at credit profiles. The algorithm spits out a recommendation but we still need the human element.”

Gilbert reckons that the art of the deal involves about “70 percent algorithm and 30 percent people.” He adds, “You still need the people component to look at credit profiles. The algorithm spits out a recommendation but we still need the human element.”

If there’s a fly in the National Funding ointment, it’s that the company’s fees can be more expensive than a bank loan.

But borrowers who have been denied loans at a bank or other lender are likely to overlook those costs. Austin, the florist in West Palm Beach, for example, came to National Funding when his bank, North Carolina-based BB&T Bank, gave him the cold shoulder despite the $15,000 in deposits that he averages each month. “I’ve been with them for six years,” he fretted, “and they treated me shabbily.”

Even more grateful was Jimmy Frisco, of Annapolis, who is co-owner with his wife of Lisa’s Luncheonette, a business that includes a food trailer and several cafeterias located in the city’s office buildings. They employ about a dozen people.

Frisco had taken a nasty spill and was laid up for seven months. Health insurance covered the $18,000 in medical costs but he and Lisa fell behind in their bills and needed working capital to pay for food purchases and other business expenses. By the time a flyer from National Funding popped up in his mailbox, he and his wife “had been turned down by several other lenders, including banks,” he says, adding: “Things happen in life and we don’t have the best of credit.”

Getting that loan for $25,000 from National Funding took just three days. Frisco’s health is much improved and business is back to normal. He won’t discuss the terms of the financing, other than to say “it was reasonable.”

He adds: “There were no problems with National Funding, no hassle with the paperwork. They’re great people to work with.”

NYIC – IFA Northeast – AFBA – AltFinanceDaily Conference Recap

October 17, 2018

Yesterday, the New York Institute of Credit (NYIC) hosted a conference in Manhattan with attendees from several segments of the commercial finance industry, including factoring, MCA, and asset based lending. Approximately 100 registrants gathered at Arno Ristorante in the garment district section of midtown. In addition to local New York firms, attendees travelled from as far as Chicago and California to be at the event.

“By all accounts, it was a big success,” said Harvey Gross, Executive Director of the NYIC, which recently celebrated its 100th anniversary. The half-day conference was a collaboration of the NYIC, the Alternative Finance Bar Association (AFBA), the IFA Northeast, and AltFinanceDaily.

“The joint conference was truly groundbreaking,” said Lindsey Rohan, a cofounder of the AFBA, who also moderated a legal panel. “Having the various business models that make up the alternative finance space in the same room created an opportunity for honest and impactful conversation. While we only scratched the surface and I have many new questions, I’m confident that new business relationships were created and this will open the door to a continued exchange of ideas.”

Nineteen panelists, many of them executives at financial companies and lawyers, contributed to four panels that filled the afternoon with lively and thoughtful conversation. Regulations coming out of California and just recently from New Jersey, were hot topics of discussion.

AltFinanceDaily founder Sean Murray moderated a panel on Best Practices. “These type of collaborative events are necessary as commercial finance offerings continue to expand. Education and debate create a more fluid marketplace,” Murray said.

Andrew Bertolina, whose company Finvoice offers factors and asset-based lenders a sleek software solution, said it was “great to see everyone at the Lending Conference and cross-pollination of MCA, factors and fintech players. Most cross-pollination at this IFA NYIC event than in prior factoring events.” Bertolina is the co-founder and CEO.

Robert Zadek, an attorney with Buchalter said, “that was a great meeting. It was so instructive to hear intelligent, honorable representatives of factoring and of alternative finance, who share clients and have overlapping products cordially comparing notes and sharing somewhat different views of the marketplace and the future of SMB financing. It is fascinating to see how much each can learn from the other, and to witness how such different financial products are moving towards each. The lesson – adapt or perish.”

The conference was sponsored by Change Capital, Finvoice, law firm Platzer, Swergold, Levine, Goldberg, Katz & Jaslow LLP, Aurous Financial, and Financial Poise.

Is Your Firm Ready for Machine Learning?

October 15, 2018Artificial intelligence such as machine learning has the potential to dramatically shift the alternative lending and funding landscape. But humans still have a lot to learn about this budding field.

Across the industry, firms are at different points in terms of machine learning adoption. Some firms have begun to implement machine learning within underwriting in an attempt to curb fraud, get more complex insights into risk, make sounder funding decisions and achieve lower loss rates. Others are still in the R&D and planning stage, quietly laying the groundwork for future implementation across multiple areas of their business, including fraud prevention, underwriting, lead generation and collections.

“It’s entirely critical to the success of our business,” says Paul Gu, co-founder and head of product at Upstart, a consumer lending platform that uses machine learning extensively in its operations. “Done right, it completely changes the possibilities in terms of how accurate underwriting and verification are,” he says.

While there’s no absolute right way to implement machine learning within a lender’s or funder’s business, there are many data-related, regulatory and business-specific factors to consider. Because things can go very wrong from a business or regulatory perspective—or both—if machine learning is not implemented properly, firms need to be especially careful. Here are a few pointers that can help lead to a successful machine learning implementation:

Using machine learning, funders can predict better the likelihood of default versus a rule-based model that looks at factors such as the size of the business, the size of the loan and how old the business is, for example, says Eden Amirav, co-founder and chief executive of Lending Express, a firm that relies heavily on AI to match borrowers and funders.

Machine learning takes hundreds and hundreds of parameters into account which you would never look at with a rule-based model and searches for connections. “You can find much more complex insights using these multiple data points. It’s not something a person can do,” Amirav says.

He contends that machine learning will optimize the number of small businesses that will have access to funding because it allows funders to be more precise in their risk analyses. This will open doors for some merchants who were previously turned down based on less precise models, he predicts. To help in this effort, Lending Express recently launched a new dashboard that uses AI-driven technology to help convert business loan candidates that have been previously turned down into viable applicants. The new LendingScore™ algorithm gives businesses detailed information about how they can improve different funding factors to help them unlock new funding opportunities, Amirav says.

Lenders and funders always have to be thinking about what’s next when it comes to artificial intelligence, even if they aren’t quite ready to implement it. While using machine learning for underwriting is currently the primary focus for many firms, there are many other possible use cases for the alternative lenders and funders, according to industry participants.

Lead generation and renewals are two areas that are ripe for machine learning technology, according to Paul Sitruk, chief risk officer and chief technology officer at 6th Avenue Capital, a small business funder. He predicts that it is only a matter of time before firms are using machine learning in these areas and others. “It can be applied to several areas within our existing processes,” he says.

Collection is another area where machine learning could make the process more efficient for firms. Machines can work out, based on real-life patterns, which types of customers might benefit from call reminders and which will be a waste of time for lenders, says Sandeep Bhandari, chief strategy and chief risk officer at Affirm, which uses advanced analytics to make credit decisions.

“There are different business problems that can be solved through machine learning. Lenders sometimes get too fixated on just the approve/decline problem,” he says.

“Most underwriters don’t have enough data to effectively incorporate AI, deep learning, or machine learning tools,” says Taariq Lewis, chief executive of Aquila, a small business funder. He notes that effective research comes from the use of very large datasets that won’t fit in an excel spreadsheet for testing various hypotheses.

Problems, however, can occur when there’s too much complexity in the models and the results become too hard to understand in actionable business terms. For example, firms may use models that analyze seasonal lender performance without understanding the input assumptions, like weather impact, on certain geographies. This may lead to final results that do not make sense or are unexpected, he says.

“There’s a lot of noise in the data. There are spurious correlations. They make meaningful conclusions hard to get and hard to use,” he says.

The more precise firms can be with the data, the more predictive a machine learning model can be, says Bhandari of Affirm. So, for example, instead of looking at credit utilization ratios generally, the model might be more predictive if it includes the utilization rate over recent months in conjunction with debt balance. It’s critical to include as targeted and complete data as possible. “That’s where some of our competitive advantages come in,” Bhandari says.

Underwriters also have to pay particularly close attention that overfitting doesn’t occur. This happens when machines can perfectly predict data in your data set, but they don’t necessarily reflect real world patterns, says Gu of Upstart.

Keeping close tabs on the computer-driven models over time is also important. The model isn’t going to perform the same all along because the competitive environment changes, as do consumer preferences and behaviors. “You have to monitor what’s going well and what’s not going well all the time,” Bhandari says.

Certainly, as AI is integrated into financial services, state and federal regulators that oversee financial services are taking more of an interest. As such, firms dabbling with new technology have to be very careful that any models they are using don’t run afoul of federal Fair Lending Laws or state regulations.

“If you don’t address it early and you have a model that’s treating customers unfairly or differently, it could result in serious consequences,” says Tim Wieher, chief compliance officer and general counsel of CAN Capital, which is in the early stages of determining how to use AI within its business.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

To be sure, regulation around AI is still a very gray area since the technology is so new and it’s constantly evolving. Banking regulators in particular have been looking closely at the issues pertaining to AI such as its possible applications, short-comings, challenges and supervision. Because the waters are so untested, there can be validity in asking for regulatory and compliance advice before moving ahead full steam, some industry watchers say.

Upstart, for example, which uses AI extensively to price credit and automate the borrowing process, wanted buy-in from the Consumer Financial Protection Bureau to help ease the concern of its backers as well as to satisfy its own concerns about the legality of its efforts. So the firm submitted a no-action request to CFPB. The CFPB responded by issuing a no-action letter to Upstart in September 2017, allowing the company to use its model. In return, Upstart shares certain information with the CFPB regarding the loan applications it receives, how it decides which loans to approve, and how it will mitigate risk to consumers, as well as information on how its model expands access to credit for traditionally underserved populations.

The No-Action Letter is in force for three years and Upstart can seek to renew it if it chooses.

Theoretically firms could have a computer underwriting model constantly updating itself without having a human oversee what the model is doing—but it’s a bad idea, industry participants say. “I believe there are companies doing that, and it’s a risky thing to do,” says Scott M. Pearson, a partner with the law firm Ballard Spahr LLP in Los Angeles.

During review of the models—and before implementing them—people should carefully review the models and the output to make sure there’s nothing that causes intrinsic bias, says Kathryn Petralia, co-founder and president of Kabbage, which is one of the front-runners in using machine learning models to understand and predict business performance.

“If you’re not watching the machine, you don’t know how the machine is complying with regulatory requirements,” she says.

Kabbage has teams of data scientists regularly developing models that the company then reviews internally before deploying. The company is also in frequent contact with regulators about its processes. Petralia says it’s very important that firms be able to explain to regulators how their models work. “Machines aren’t very good at explaining things,” she quips.

As a best practice, Pearson of Ballard Spahr says lenders and funders shouldn’t use any machine learning model until it’s been signed off on by compliance. “That strikes a pretty good balance between getting the benefits of AI and making sure it doesn’t create a compliance problem for you,” he says.

While AI has many benefits, industry participants say alternative lenders and funders need to be mindful of how it can be applied practically and effectively within their particular business model.

Craig Focardi, senior analyst with consulting firm Celent in San Francisco, contends that the classic FICO score continues to be the gold standard for credit decisions in the U.S. He warns firms not to get overly distracted trying to find the next best thing.

“Many fintech lenders have immature risk management and operations functions. They’re better off improving those than dabbling in alternative scoring,” he says, noting that data modeling is an entirely separate core competency.

Indeed, Lewis of Aquila cautions underwriters not to view AI as a silver bullet. “AI is just one tool out of many in the lenders’ toolbox, and our industry should use it and respect its limitations,” he says.

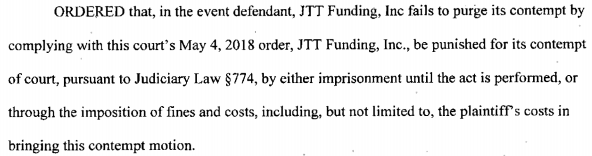

ISO Pretending to be Funder May Be Sent to Jail

October 14, 2018A New York Supreme Court judge ordered on Thursday that Long Island-based ISO JTT Funding either be fined or sent to prison if it does not comply with a previous restraining order obtained by NYC-based funder Accel Capital.

Accel alleges that JTT funding has been impersonating it through correspondence and on contracts, a scheme that was outed when merchants claimed they had been duped into sending thousands of dollars upfront to JTT (disguised as Accel) to obtain a loan yet never received one. Accel responded by suing JTT and obtained a restraining order on default when the defendant failed to respond.

According to the Financial Times, JTT Funding is owned by Queens-born mixed martial arts fighter Jim “The Tyrant” Boudourakis. In his October 2017 interview with the publication, Boudourakis said, “There was a learning curve, going from being a fighter to a salesman. But I’m good with people.” FT also reported that his company had 18 full-time salespeople and was funding $4 – $5 million per month.

In an unrelated suit, JTT Funding is accused of forging a confession of judgment.

The Accel Capital suit can be found in the New York Supreme Court under Index Number: 153447/2018

OnDeck Small Business Online Lending Tops $10 Billion

September 12, 2018OnDeck is the world’s largest non-bank online small business lending platform.

Federal Reserve says small businesses are turning to online lenders in record numbers

NEW YORK, N.Y., September 12, 2018 – – OnDeck® (NYSE: ONDK), today announced it has achieved a milestone in the Financial Technology (FinTech) industry, becoming the first non-bank online lender to surpass $10 billion in total loans originated to small businesses. OnDeck, with operations in the United States, Canada and Australia, is now the world’s largest non-bank online lender to small business by total loan volume.

The achievement by OnDeck, a pioneer of the FinTech lending industry, is the latest indication that small businesses increasingly prefer to seek financing online. According to the recent Small Business Credit Survey from the Federal Reserve, small business owners are turning to online lenders in record numbers. In 2017, 24 percent of small businesses seeking credit applied online, up from 21 percent the previous year. Not only did the total number of loan applications to online lenders increase in 2017, but satisfaction rates of small businesses soared almost 50 percent year-over-year.1

OnDeck provided its first small business loan online in 2007, taking just 11 years to pass $10 billion in total loan volume in a digital lending market it helped create. The majority of OnDeck’s lending occurred in the last few years as it gained scale, with the company originating $2.1 billion in loans in 2017 alone.

“If reaching $10 billion dollars in total loan volume online tells us anything, it’s that the days of old-fashioned lending to small businesses are numbered,” said Noah Breslow, Chairman and Chief Executive Officer, OnDeck. “We created OnDeck because we believed the Internet could revolutionize and speed up the way underserved small businesses access capital. Today, we are helping to fill a credit gap across hundreds of industries by providing fast, secure and transparent loans that enable small businesses to grow, generate economic activity and create jobs. We look forward to providing billions more in financing and powering the small business lending migration to the online model via our OnDeck-as-a-Service platform.”

Small businesses are the economic backbone of America, accounting for more than 99% of all U.S. companies1 and employing over half of all private sector workers2. However, they still face a growing credit gap. According to the Federal Reserve survey, 54% of small businesses report credit shortfalls3 and lower-income communities are disproportionately impacted. Traditional large banks deny 44% of all small business loan applications3 and many are steadily exiting the small business credit market. Since 2008, small business lending from traditional sources has fallen over 20%4.

Identifying the developing credit gap over a decade ago, OnDeck transformed the means by which small businesses access capital, using proprietary technology and a small business credit scoring system, the OnDeck Score®, to more efficiently evaluate a business’ creditworthiness and make lending decisions in real time. OnDeck provides term loans and lines of credit to small businesses and can supply customers with funding in as little as one business day. The economic impact of this online lending activity is substantial. Immediate infusions of capital enable small businesses to purchase inventory, cover operational costs, or expand without delay, which can stimulate economic growth and help create jobs in their communities.

OnDeck and the Impact of Online Lending on the Economy

An Analysis Group report commissioned by OnDeck in 2015 analyzed the economic impact from the first $3 billion OnDeck lent to small businesses. The report estimates that those loans powered $11 billion in business activity and created 74,000 jobs nationwide. In 2018, OnDeck announced it had provided small businesses more than $10 billion in capital.

In May of 2018, a report on small business online lending in the United States revealed that OnDeck and four other small business lending platforms funded nearly $10 billion in online loans from 2015 to 2017, generating $37.7 billion in gross output and creating 358,911 jobs and $12.6 billion in wages in U.S. communities. The upsurge in online lending is filling a critical financing gap for small businesses across industries, according to NDP Analytics, a Washington, D.C.-based economic research firm. See the NDP Report here: http://www.ndpanalytics.com/online-lending/

OnDeck Company Timeline

Download here: https://www.ondeck.com/wp-content/uploads/2018/09/10-year-timeline-02.pdf

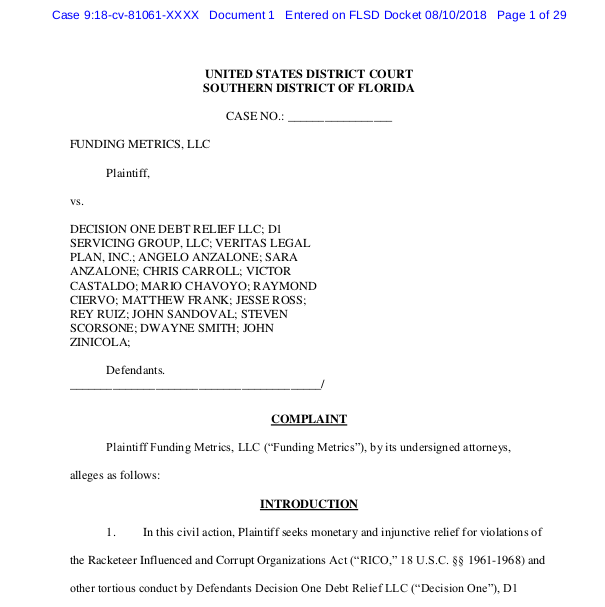

War on Debt Settlement Continues: 16 Defendants Sued in RICO Case

September 6, 2018

Fourteen individuals and two companies (including Decision One Debt Relief) were sued by Funding Metrics in Federal court last month for allegedly “conducting a nationwide illegal debt restructuring scheme through numerous acts of mail and wire fraud.”

The suit, which stems from the defendants’ interference with Funding Metrics’ merchant cash advance customers, makes six claims, among them financial damages resulting from state and federal crimes. Per the complaint:

“Defendant Decision One (along with its affiliate/alter ego D1 Servicing) fraudulently presents itself as being able to renegotiate and restructure merchant agreements with Plaintiff and other funding companies. It has established a deceptive business practice of making misleading and often outright false representations to merchants under contract with Plaintiff promising that, with its help, these merchants will save money on those contracts by defaulting on them. Decision One tells merchants that they can safely stop paying cash advance funding companies like Plaintiff; that it will go to work for them promptly; that it can reduce their debt by 60-80% or more; and that they will be provided with a Veritas insurance plan to cover legal expenses arising from their defaults, once cash advance companies exercise their rights under agreements with their merchants, as they inevitably will. Based on these misrepresentations, the merchants default on their contracts with their funders – that is, at Decision One’s direction, they stop paying their funders and instead pay Decision One – although Decision One does not even expect to achieve results for the merchants. The result is a fraud on the merchants and tortious interference with the contracts Plaintiff have with them.”

The suit is just the latest bomb dropped on the exploding debt settlement industry. AltFinanceDaily began covering the controversy surrounding debt settlement in late 2016 after the owner and employees of an upstate New York debt settlement company were arrested for charging merchants to restructure their merchant cash advances and then not actually performing any services. The owner, Sergiy Bezrukov, was charged with money laundering, bank fraud, mail fraud, wire fraud and conspiracy to defraud. Bezrukov has been locked away in jail for almost two years awaiting trial. He is facing a maximum of 30 years. Two of his employees pled guilty, Vanessa Cardona to bank fraud and Dustin Walker to conspiracy to commit bank fraud.

Since then, nearly a dozen major lawsuits have been filed by merchant cash advance companies against other debt settlement companies that are alleged to be carrying out similar schemes. One of those sued companies, NJ-based Corporate Bailout LLC, was featured on the cover of the New York Post last summer for being “the craziest office in America.” Corporate Bailout was sued by both Yellowstone Capital and Everest Business Funding which later resulted in a very public settlement agreement that forced Corporate Bailout to fork over $500,000 to the two MCA companies.

Decision One Debt Relief, sued now by Funding Metrics, was also originally a co-defendant alongside MCA Helpline in a lawsuit filed by Everest Business Funding earlier this year. In February, after determining the two were not related, Everest dropped the claims against Decision One only. The suit against MCA Helpline is still pending.

Around that same time, a representative for Decision One revealed to AltFinanceDaily that the company was on track to be doing more than $100 million a year in business.

Bezrukov, by contrast, who currently resides in a Niagara County New York jail, is accused of having only obtained $1.2 million throughout his entire debt settlement venture’s existence. Although Decision One is not being charged criminally, the private civil suit alleges damages caused by a violation of criminal statutes including RICO.

The Funding Metrics suit against Decision One was filed in the Southern District of Florida under ID# 9:18-cv-81061.

Grooming The Best Sales Reps

August 22, 2018The best sales reps have a lot in common – they’re smart, honest, likable, well-organized, thick-skinned and hungry for success. They navigate the difficult early days of their careers in the alternative small-business funding community by persevering despite long hours, countless outbound telephone calls and meager commissions.

“Persistency is really, really the key – putting in the time,” says Evan Marmott, CEO of Montreal-based CanaCap and CEO of New York-based CapCall LLC. “It’s not always easy, but you’ve got to stay late, make the phone calls, send the emails and do the follow-ups. It’s a numbers game.”

Being relentless counts not only when pursuing merchants but also when matching merchants with funders, Marmott emphasizes. “If they can’t get an approval one place, they’re going to shop it out until they get approval someplace else so they can monetize everything that comes in,” he says.

“It’s all mindset and work ethic,” in sales, according to Joe Camberato, president at Bohemia, N.Y.-based National Business Capital. His company works to create a culture that supports the right mindset by working with a firm called “Delivering Happiness.” Together, they forge to a set of core values based on integrity, innovation, teamwork, empathy, and respect for fellow employees, clients and clients’ businesses.

National Business Capital employees learn to live those ideals by working and playing together on the company volleyball team, through work with local and national charities, and at company mixers and staff picnics, Camberato maintains. “We adapt and change, and we’re committed to helping small businesses grow,” he says of the company culture, “and we have fun while doing all that.”

Likeability helps build relationships with customers, says Justin Thompson, vice president of sales for San Diego-based National Funding. “People will do business with people they like and trust,” says Thompson. “It’s really about establishing a relationship first and then establishing quality discovery.” From there, presentation and execution become paramount, he says.

Methodology can make the difference between success and failure in sales, observes Justin Bakes, co-founder and CEO of Boston-based Forward Financing LLC. “Have a defined process and stick to it,” he advises. A well-organized approach inspires trust among clients, establishes and maintains a great reputation; and fosters understanding of the customers’ needs, wants and business operations that help the rep choose the right financing option and appropriate funder. Using technology to wrangle multiple leads and high volume counts for a lot, too, he says.

It’s all part of the consultative approach to sales, says Jared Weitz, CEO of Great Neck, N.Y.-based United Capital Source. Long ago, sales reps may have succeeded by mimicking carnival barkers, sideshow pitchman and arm-twisting medicine-show peddlers. Thankfully, those days have ended – if they ever really existed. Most of today’s successful salespeople earn clients’ respect by becoming knowledgeable, trusted business consultants, says Weitz.

THE CONSULTATIVE SALE

“Someone calls, and there are two ways of handling a deal, right?” Weitz asks rhetorically. Using one method, a salesperson can say, “We’ll fund you this much at this rate today – are we good?” he says. The other way calls for understanding the client’s business – how long has it been open, does it make more cash deposits or credit card deposits, would it be best-served by an advance, a loan, an equipment lease or a line of credit, how much can it afford in monthly payments?

Establishing how the merchant intends to use the funding plays a crucial role in the consultative sale, Marmott agrees. Objections can arise when a merchant learns that receiving $100,000 this week will require paying back $150,000 in four or five months, he notes. So it’s essential to demonstrate that using the money productively will more than pay for the deal. A trucking company can realize more income if it deploys two more trucks, or a restaurant can increase revenue by placing another bar outside for the summer, he says by way of example.

“A lot of salespeople ask a business owner what they need the money for,” observes Thompson. “The merchant says, ‘Inventory,’ and the rep stops right there. I train my reps at National Funding to go two or three clicks deeper.” Examples abound. When does the merchant need the inventory? From whom do they order it? How long does it take to ship? How long does it take to turn it over? What are the shipping terms?

The consultative approach can require salespeople to pose a lot of open-ended questions that can’t be answered yes or no, according to Thompson. Ideally, the conversation should adhere to the 80-20 rule, with the client talking 80 percent of the time and the sales rep speaking 20 percent, he asserts, adding that “a lot of times it’s reversed in this industry.”

Sometimes, however, salespeople should set aside the time-consuming consultative approach and instead find funding for a merchant as soon as possible. That’s true when the business owner can make an opportune purchase of inventory or when it’s time to acquire a competitor quickly. More often, however, it pays to take the time to understand the merchant’s needs and search out the best type of funding for that particular case, top sales people maintain.

Much of the alternative small-business finance industry has caught on to the importance of the consultative approach to sales as the array of available alternative financial products has grown beyond the industry’s initial offerings of merchant cash advances, according to Weitz. The days of scripted pitches and preplanned rebuttals to objections have ended, he says. Today, management trains reps for success.

THE RIGHT TRAINING

Are top salespeople born that way? “Some people hit the ground running, but sales can be taught – that’s for sure,” Weitz says. “The tougher thing to teach is integrity.” Much of the training process focuses on learning the products to enable a rep to make a consultative sale and shoulder financial responsibility, he maintains.

Believing that some people are born to sell provides a crutch to avoid learning what really works, according to Bakes. Training can teach a smart, motivated person how to succeed, he maintains. They don’t have to be born that way.

However, some people do seem born to exert influence, which can translate into sales prowess, says Thompson. Still, those born with a strong work-ethic can overcome other deficiencies, he notes. The work ethic drives them to “come in every day,” he notes. “They’re organized and disciplined. They follow the National Funding philosophy, and they make a ton of money.”

National Funding trains salespeople to view their craft as being defined by two broad elements – art and science, Thompson continues. The science proves easier to master and includes asking the right questions to learn about the customer and the deal. The hard part, the art of the sale, consists of getting to know the business owner, building a relationship and demonstrating expertise. In one example, that’s based on learning how many trucks are in the fleet, whether they’re long-haul or short haul and whether they use dumpsters versus box trailers, he says.

Beyond those important basics, training should be ongoing because selling techniques change slightly as new products and systems emerge, according to Weitz. “One of the things I like about being a broker is the ability to pivot and add another arrow to your quiver,” he says.

Salespeople at United Capital Source talk sales among themselves almost nonstop, which amounts to daily sales training, Weitz observes. That can take the form of describing a challenge and explaining how to overcome it, he notes. A particularly good idea merits an email to the group to share the new piece of wisdom. It’s a matter of constantly refining the approach.

Training can help sales reps understand the businesses their clients run, according to Marmott. Knowing the margins in a restaurant, for example, can help the salesperson explain that the increase in revenue from an expansion will quickly pay the cost of capital, he notes.

Training should teach new employees how business works because common elements arise in enterprises ranging from dog grooming to asphalt paving, Thompson notes. There’s inventory, marketing, employee expense, payroll taxes, insurance and 401k’s in almost any business. “We teach all that to the reps,” he says. Then after conversations with thousands of merchants, reps have a solid foundation in the workings of businesses.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

New hires spend much of their time working with mentors for the first six months and a team leader who works with them indefinitely, Camberto continues. The company sometimes hires in groups and sometimes hires individually, he notes.

National Funding provides three eight-hour days of regimented classroom training on the fundamentals to each of the four groups of 12 to 17 hired each year, says Thompson. The classes cover processes, sales strategy, marketing and the lender matrix. Next comes three months of working with a sales manager dedicated to working with the class. After a total of nine to 12 months, management knows which reps will succeed.

Some shops operate on the opener-closer model, with less experienced salespeople qualifying the merchant by asking questions like how long they’re been in business and how much revenue they bring in monthly, Marmott says. If the merchant qualifies, the newer salesperson who’s working as an opener then hands off the call to an experienced closer to complete the deal. Good openers become closers, but opening isn’t easy because it requires lots of calls, he notes.

National Funding doesn’t use the opener-closer approach because the company believes reps should Participate “from cradle to grave,” Thompson says. “They hunt the business down, build the relationship and handle the transaction from A to Z.” East Coast shops often focus on cold calling and use the opener-closer model, while West Coast shops tend to invest more in marketing and reject the opener-closer method, he noted.

But where do these top salespeople come from?

THE RIGHT BACKGROUND

Prospective sales reps who have just finished college should have a grounding in communications or business, Weitz believes. Experience in sales and a familiarity with dealing with merchants helps prepare reps, he notes. Job history doesn’t have to be in the finance industry. Someone who’s sold business services in a Verizon store or worked for a payroll company, for instance, has been dealing with small-business owners and may succeed more quickly than those without that background.

Sales experience in other industries counts, Bakes agrees, especially in businesses that require dealing with a large number of leads. “Organization and process is just as important as being born with the traits of a salesperson,” he opines.

Life experience that breeds a positive attitude can prove vital, says Marmott. That’s especially important in the beginning when a new rep might take home a paltry $300 in the first month. Later, when the rep has a $50,000 month, he or she will see that their optimism wasn’t misplaced, he declares.

GUYS WHO ARE HUNGRY”

“The biggest thing I look for is guys who are hungry,” Marmott maintains. I don’t need somebody with a doctorate or a master’s degree or even a degree,” he says. “I need somebody who is going to put the work in.” Of a roomful of 25 new reps, two or three will succeed and stay on the job, he calculates. “You get to eat what you kill. If you’re not killing anything, you don’t get to eat.”

“We look for potential candidates who come from backgrounds of rejection,” says Thompson. Their previous sales experience has taught them not to take the answer “no” personally. “It’s part of the business and you continue to move on.”

Although most regard the financial services industry as a white-collar pursuit, “it has blue collar written all over it,” Thompson says, referring to the work ethic required for success. But it’s not just the volume of work. Sixty good phone calls generate more business than 300 mediocre calls, he emphasizes.

GETTING UP TO SPEED

Succeeding at sales requires taking the time to form relationships, understand guidelines, become familiar with lenders and acquire a working knowledge of how clients’ businesses operate, Camberato says. How long does it take? “It’s a solid year,” he contends while conceding that most who succeed operate at a fairly high level before then.

Others disagree about what constitutes being up to speed and how much time’s necessary to achieve it. “I’ve seen it take 30 days, and I’ve seen it up to 120 days,” says Weitz. “The hope is that it’s within 60.”

A salesperson should start feeling better after 30 days and should start feeling good after 60 days, Marmott says. Management can usually identify the strong and the week reps within two to three weeks, he says. “You get the lazy ones that drop out, the guys who aren’t making any money, the ones who aren’t putting the effort in,” he says. “The first two weeks are the toughest because you’re learning the product and how to sell it.”

“It depends on the person,” Bakes says of the time needed to begin selling successfully. “It takes time. It is not something that will just happen overnight.” About six months should suffice to become confident as a closer, he estimates.

Even when sales reps hit their stride, some outsell others, Marmott notes, citing the 80-20 rule that 80 percent of the business comes from 20 percent of the salesforce. Outbound sales to merchants who may feel beleaguered by offers of funding requires more effort than when a merchant makes an inbound call to seek funding, he adds.

And even the best salespeople need great marketing and tech support from the their companies, sources agree.

INVESTING IN SALES

A shop just starting out might have a marketing budget as low as $2,500 a month, which won’t do much more than pay for direct mail pieces that might prompt a few potential clients to pick up the phone, Weitz says. With a little more money to spend, a shop can begin buying leads, he notes. “Don’t break the bank before you understand what formula works for you,” he advises.

“The key to sales is marketing,” says Marmott. “You can be the best sales guy but if you don’t have anything qualified to call or follow up with, it’s a waste of time.” Social media doesn’t work as well for business-to-business contact as it does for business-to-consumer marketing, he says. Pay per click and key words have become more expensive and isn’t as cost-effective as it once was, especially for smaller shops, he contends. Mailers can work but require heavy volume and repetition, he says, adding that could mean at least 25,000 pieces and at least three mailings.

Besides allocating marketing dollars, companies can invest in sales by paying new sales staffers a salary instead of forcing them to rely on commissions to eke out subsistence during the tough early days. National Business Capital pays a salary at first and later switches reps to commissions and draw, Camberato says. “An energetic person interested in sales can plug into our platform, get trained and do very well,” he continues. “We believe in you, as long as you believe in us.”

National Funding provides recruits with a salary and commissions so that they have enough income to get by and still reap rewards when they help close a deal, Thompson says.

Investment in technology can help salespeople set priorities, eliminate some of the drudge work in the sale process, measure the sales staff member’s success or lack of success, and provide a consistent experience for customers, notes Bakes. “Because of the way our technology is set up we can hold people accountable,” he adds.

Every salesperson and every shop should organize the workflow by using a lead-management system or customer relationship management tool (CRM) – such as Zoho or Salesforce –instead of operating with just a spreadsheet, Weitz says.

Brokers can invest in sales through syndication, which means putting up some of the funds involved in a deal. Forward Financing favors syndication in some cases because it aligns the salesperson and the funder, thus demonstrating the sales rep’s belief in the validity of the deal and ensuring a willingness to continue servicing that customer, Bakes says.

Some shops offer monthly bonuses for outstanding sales results, but Weitz believes awarding incentives weekly makes more sense. With a monthly cycle, some reps tend to slack off for the first week or so because they believe they can make up for lost time later. With weekly rewards, there’s not much room for downtime, he notes.

Whatever form investment takes, it can help build a sterling reputation and a free-flowing “pipeline.”

THE RIGHT REPUTATION

“Reputation is huge,” especially for repeat business and referrals, Marmott says. Once a merchant has received funding, a blizzard of sales call can follow. Treating customers right by maintaining ethical standards and helping them during hard times can guard against defection to a competitor touing low prices, he says.

Reputation requires differentiation, which usually occurs online, by email or over the phone, notes Bakes. Factors that enhance reputation include referrals by satisfied customers and real-world testimonials from actual customers and good ratings on social media sites, he says.

While it’s still uncertain what role social media plays in the industry’s reputation-building efforts, it appears that text messages elicit quick responses if the client has agreed to communicate with the company via that format, Bakes says. He notes that unwanted text messages won’t work. Email messages provide more information than text messages but seem less likely to prompt response, he says.

THE RIGHT GOAL

So, where does the effort to succeed at sales lead? It’s the foundation for building “the pipeline” – the name given to the flow of renewals, referrals and leads that makes every day not just busy, but busy in a productive and profitable way. As a rep’s pipeline takes shape, the cost of acquiring new business also goes down, Marmott says. “It just grows from there,” he says of the successful salesperson’s endeavors at building a pipeline of business. It’s what successful salespeople seek.