TakeCharge Capital Acquires SBS Capital

July 29, 2013For early release on Merchant Processing Resource:

NEWINGTON, CT- TakeCharge Capital, LLC, an MCA and Loan Service Provider based in Connecticut, proudly announces the acquisition of SBS Capital, LLC a financial services company providing merchant cash advances and credit card processing based in Newington, Connecticut. SBS Capital will rebrand its company under TakeCharge Capital and has appointed Aaron Shimkowitz COO of TakeCharge Capital, former VP of SBS. “TakeCharge’s MCA Portfolio now encompasses 28 Million in Funding to small-mid sized businesses nationwide, including 400+ credit card processing merchants added to the TakeCharge Payments Portfolio respectively.” stated Sam Kota, CEO at TakeCharge.

NEWINGTON, CT- TakeCharge Capital, LLC, an MCA and Loan Service Provider based in Connecticut, proudly announces the acquisition of SBS Capital, LLC a financial services company providing merchant cash advances and credit card processing based in Newington, Connecticut. SBS Capital will rebrand its company under TakeCharge Capital and has appointed Aaron Shimkowitz COO of TakeCharge Capital, former VP of SBS. “TakeCharge’s MCA Portfolio now encompasses 28 Million in Funding to small-mid sized businesses nationwide, including 400+ credit card processing merchants added to the TakeCharge Payments Portfolio respectively.” stated Sam Kota, CEO at TakeCharge.

To accommodate growth, TakeCharge Capital has relocated from 705 North Mountain Road in Connecticut to prime 4,000 square ft facility located on 2600 Berlin Turnpike in Newington Connecticut. “With about 100,000 drivers passing through the turnpike everyday and over 32,000 businesses within a 30 Mile Radius, the Berlin Turnpike marks the first storefront location in our New Retail Strategy. The end-to-end model coupled in a retail environment is by far the best user experience, as we’ve learned from outside industry leaders such as apple and the gap” states Shimkowitz.

In addition to the expansion, TakeCharge Capital has promoted:

- George Korhonen- SVP of Business Development at TakeCharge Capital. In this new role, Mr. Korhonen will continue to develop TakeCharge’s core business and lead new partnerships within the trucking and medical industries.

- Rebeqa Abrams- VP of Operations at TakeCharge Capital. In this new role, Ms. Abrams will continue to manage business operations and direct new operational initiatives to reduce costs and increase overall company efficiency.

And newly appointed:

- Aaron Shimkowitz- Chief Operations Officer at TakeCharge Capital, former VP at SBS. In this new appointment, Aaron will spearhead and oversee all operations, accounting and day to day corporate responsibilities.

- Nicole Beaudry- VP of Funding at TakeCharge Capital, former Director of Cash Management at SBS. In this new appointment, Nicole will oversee funding partnerships and refinance department.

- Jennifer Burke- VP of Sales at TakeCharge Capital, former Executive Underwriting Specialist at SBS. In this new appointment, Jennifer will oversee sales and portfolio retention.

“This partnership with Aaron’s team, further attributes to our long-term strategy of creating a google-like culture with top notch talent and a passion to design technology specifically for the small business community we serve.” states Kota.

TakeCharge Capital, LLC, based in Newington Connecticut is a privately-held financial technology company providing loan and payment services to business owners nationwide. For more information, visit http://www.takechargecapital.com or email info@takechargecapital.com. To speak directly with a TakeCharge Representative reach us Toll-free at 877-417-9473.

The Alternative Business Lending Worker Shortage

July 1, 2013“You open 40 accounts, you start working for yourself. Sky’s the limit.“

Is the dream getting harder to sell? The alternative business lending industry is booming and so much so that many job openings are going unfilled. I am asked on almost a daily basis if I know any experienced sales people that are looking for work. There really aren’t that many people out there with a strong merchant cash advance background and I think it’s impacting how fast this industry can grow. On the one hand, the industry is a lot less sophisticated than it used to be. Hold on for a second and allow me to explain myself. There was a good chunk of time in this business where saying the word, loan could get you fired. Loan?! Are you kidding? We buy future receivables at a discount!

Anyone could sell a prospect on working capital but only a select group of people could explain the purchase of future sales properly all while justifying the relatively high cost. And an even smaller group of people could take the deal to the next step and discuss the merchant’s current 3 tiered or interchange based rates, pick out the junk costs, and sell them on a better deal with a new payment processor. And an even smaller group of people could sell the merchant on the idea of using a new terminal due to PCI compliance issues or acquirer compatibility. And an even smaller group of people could sell or lease the merchant a new terminal instead of swapping out their current one or lending one for free with a multi-year contract. And still an even smaller group of people could convince the underwriter to approve their file in order for the 5 closed sales to even go through. Merchant cash advance in the traditional manner was and is a highly complicated multi-layered sale. The men and women that churn(ed) these deals out month after month on a consistent basis are nothing short of pros. Let’s not forget that payment processors have underwriters too so even after 6 closes, the payment processor could decline the approval of a merchant account, nuking the entire deal from start to finish.

Do you have any idea how comical it was when the mortgage brokers invaded the industry as the housing market neared collapse? They had no idea what they were doing and some of them barely lasted for 90 days before saying “I give up, this makes no sense.”

In today’s market, there’s a faster learning curve. I’d estimate that 55-60% of all new deals being funded with daily repayment in this country are using direct debit ACH to collect. Some funders and brokers lean towards this model so much so that they report funding more than 90% of their deals on ACH. That’s good news for new account reps because there isn’t much to learn about the product. There’s the amount being funded, the cost, and a daily debit to pay it back. Pretty simple stuff. This isn’t to say it’s not a tough sell or that it’s not competitive, because it is both of those things. Companies that swear by the ACH product have a hiring advantage because they don’t necessarily need salespeople with MCA specific experience. Almost any financial sales background will work or even no experience at all.

The smaller part of the industry is a mishmash of the old school sophisticated reps and the newbies that rely on the old schoolers to help them out with anything technical. When companies post ads saying they are looking for MCA sales reps with experience, they’re implying that they want people that can handle the multi-layer sale. A good craigslist ad should say:

Are you hungry?!

Must be able to do the following in a single phone call while driving at least 65 MPH on the Brooklyn Queens Expressway regardless of whether or not traffic is backed up:

- Convert a Micros POS system

- Lease an additional wireless terminal for off-premise sales

- Shave 12 basis points off the non-qualified tier (but make it back up by adding a $15 monthly statement fee)

- Close a 150k deal on a 1.40 (but know that the reduced factor rate is coming out of YOUR end)

- Write in a 6% closing fee

- Cut off 47 cars in traffic without hitting them

- Eat a slice of greasy pizza with your left hand without getting a single drop on your lap

Oh and below it will be a note that says “THIS POSITION IS COMMISSION BASED ONLY, NO DRAW, SELF-STARTERS WANTED, HOURS ARE 7-7 Mon-Sat“. Don’t laugh. This was the MCA industry for a time and a lot of people did very well in it. If you wanted to make money, you had to be able to do it all. For some of you, it’s still this way.

Oh and below it will be a note that says “THIS POSITION IS COMMISSION BASED ONLY, NO DRAW, SELF-STARTERS WANTED, HOURS ARE 7-7 Mon-Sat“. Don’t laugh. This was the MCA industry for a time and a lot of people did very well in it. If you wanted to make money, you had to be able to do it all. For some of you, it’s still this way.

And let’s face it, the split-funding market may shrink but it will never die. Split-funding’s advantage is the ability to finance businesses that have poor cash flow. The risk of a bounced check is removed when payments are diverted to the funder by the payment processor. You hear that kids? You should be brushing up on your payment processing-ology.

Even as the ACH market boom continues, there are whispers of woe as funders deal with ACH rejects and closed bank accounts. It’s no surprise then that some companies are looking for pros, not just bodies to put on the telephone. It seems as the product has become less sophisticated, merchants have become more sophisticated. In 2007, I’d be willing to bet that more than 90% of small businesses had never even heard of a merchant cash advance and that was basically the only alternative available. In 2012 I actually did a presentation to a large room of business owners about merchant cash advance and none of them had ever heard of it until I taught them about it. That’s astounding!

Now I don’t think that many more people know about the purchase of future credit card sales in 2013 specifically, but I am inclined to believe that 90% of merchants are at least aware that alternatives to bank loans exist. And when they encounter somebody offering an alternative, they do their homework and check these companies out online. They get 2nd opinions and question why they have to switch processing when four other account reps said they don’t have to. They ask for better deals, longer programs, and they look you up on facebook to see who you really are. This is a different sales environment than what there used to be. The lowest price, the fastest process, or the most charming personality won’t guarantee you’ll win anything. Seeing that you’re backed by Wells Fargo or learning that Peter Thiel is on your company’s board of directors might be the hook, line and sinker for a business with a full plate of options at their disposal. Yes, it’s a different world, a different sale, and even a different product.

Now I don’t think that many more people know about the purchase of future credit card sales in 2013 specifically, but I am inclined to believe that 90% of merchants are at least aware that alternatives to bank loans exist. And when they encounter somebody offering an alternative, they do their homework and check these companies out online. They get 2nd opinions and question why they have to switch processing when four other account reps said they don’t have to. They ask for better deals, longer programs, and they look you up on facebook to see who you really are. This is a different sales environment than what there used to be. The lowest price, the fastest process, or the most charming personality won’t guarantee you’ll win anything. Seeing that you’re backed by Wells Fargo or learning that Peter Thiel is on your company’s board of directors might be the hook, line and sinker for a business with a full plate of options at their disposal. Yes, it’s a different world, a different sale, and even a different product.

Funders and brokers need human resources to keep up with the fast pace of growth and there’s not too many of the old school guys looking for work. Not to mention that fewer people are willing to work on a 100% commission only basis these days. During and after the financial crisis, the herd of out-of-work financial service people flocked to whatever opportunity the could find. It was like you could throw a fishing net in front of the Lehman Brothers entrance and use it to scoop up 50 brokers as they all ran out the door for the last time. Newly minted graduates wanted to build their resumés instead of remaining unemployed. Some people were willing to work all 31 days of a month just for the opportunity even if they walked away with zero dollars at the end of it. Although the economy hasn’t recovered much, that hunger has relaxed and job seekers are being a bit more selective of the opportunities they choose. They want a base salary (even if small), benefits, and vacation time. Somewhere out there in another universe, Ben Affleck’s younger self is crying at the thought of this. “Vacation time?”

So when you put up an ad on LinkedIn or Craigslist and say you’re looking for 10 guys with MCA experience, just know that breed is in short supply and high demand. If you’re heavy on ACH, you can train new guys quick but they’re not going be equipped to take on the multi-layered sale if the tide turns back towards split-funding. There are tons of job openings out there for sales reps but those spots aren’t as easy to fill as they used to be.

“You become an employee of this firm, you will make your first million within three years. I’m gonna repeat that – you will make a million dollars.”

Happy hiring.

– Merchant Processing Resource.com

../../

MPR.mobi on iPhone, iPad, and Android

MCA Industry Continues Expansion

April 3, 2013 It’s said that one way to measure success or growth of an industry is to count how much capital is being raised. In that case, Kabbage and On Deck Capital have been on fire lately.

It’s said that one way to measure success or growth of an industry is to count how much capital is being raised. In that case, Kabbage and On Deck Capital have been on fire lately.

Early this morning, Kabbage announced they had secured a new $75 million line, after having just raised $30 million 6 months ago. The Forbes article announcement states that Kabbage has funded 60,000 deals to date and predicts to fund 100,000 deals in 2013 alone, a figure hard to comprehend considering that’s equivalent to the amount of transactions Capital Access Network has managed to do over the course of 15 years. I understand that Kabbage may do smaller, shorter term deals, but Capital Access Network has dominated MCA for a long time. Could Kabbage really do 100,000 deals this year? I’m unsure about this one.

Are traditional MCA funders missing out by letting Kabbage rule Ebay, Amazon, and Etsy unchecked? Is the Internet really that different than the brick and mortar market? Late last year, Amazon entered the financing market but for the purpose of strengthening their selling partners, so there are several reasons funders are tapping that market.

Paypal has been sitting on the sidelines and is perhaps considering jumping in the ring themselves. They are beta testing now with Ebay sellers.

Merchant Cash Advance is exploding in all directions. Did you hear that Yellowstone Capital funded $700,000 to a restaurant with the help of Strategic Funding Source? That’s a lot of money for a restaurant!

Where’s the Reserve?

February 15, 2013 5 years ago it was merchant account sales. These days it’s all about the average daily ending balance in the business bank account. As the alternative business lending industry evolved, so too did the criteria to qualify, and nothing is more important now than historical cash flow. I spent a lot of time underwriting MCAs and one thing I noticed is that having a significant cash reserve is the exception, not the rule. Many small business owners I’ve encountered rely on overdraft protection just to pay their bills instead of using it as a backup cushion for the extremely rare circumstance that a check clears at the wrong time. The applicants with $1,000, $5,000 or $10,000 in daily reserves are treated very favorably in underwriting because heck, they can probably afford to take on debt. And then there’s the business owners with $20,000, $30,000 or $50,000 stashed away in the business account, a curious rarity that can actually throw up red flags.

5 years ago it was merchant account sales. These days it’s all about the average daily ending balance in the business bank account. As the alternative business lending industry evolved, so too did the criteria to qualify, and nothing is more important now than historical cash flow. I spent a lot of time underwriting MCAs and one thing I noticed is that having a significant cash reserve is the exception, not the rule. Many small business owners I’ve encountered rely on overdraft protection just to pay their bills instead of using it as a backup cushion for the extremely rare circumstance that a check clears at the wrong time. The applicants with $1,000, $5,000 or $10,000 in daily reserves are treated very favorably in underwriting because heck, they can probably afford to take on debt. And then there’s the business owners with $20,000, $30,000 or $50,000 stashed away in the business account, a curious rarity that can actually throw up red flags.

“Why is this merchant applying for capital when they’ve got $30,000 sitting in the account right now? Something doesn’t add up here,” an underwriter might say. But the only thing that doesn’t add up is the fact that so many businesses are running on fumes. We’ve got a few small business owners writing about matters from their perspective on The Frontline, and we took great interest in something written by Chef Angela Bell. As a restaurant owner, she believes it is important to keep a cash reserve equal to a minimum of 3 months expenses. Depending on the size of the restaurant and seasonality, that reserve may need to be able to cover an entire year. This includes rent and salaries!

It seems in practice, this rule is constantly violated. Maybe holding on to extra cash hurts the competitive edge, maybe a cash reserve existed but was consumed during an emergency, or maybe the business just isn’t doing that great. There are a lot of possibilities to explain the disappearance of cash reserves, and I’m not faulting the businesses for being in this situation, but rather pointing out that in my experience, money seems to go out as fast as it comes in.

This isn’t a 2013 problem or a financial crisis problem. It’s a small business problem and one that has been around for decades. It’s why the purchase of future credit cards spawned into existence. The original Merchant Cash Advance (MCA) program wasn’t created to help people with poor credit, it was designed to help the businesses that had no cash reserves. If a business has $2,000 in deposits every day but also $2,000 in withdrawals, there’s a good chance a debt payment will bounce. Even with 750 credit, no bank would ever take the risk on a business like that, and that’s where MCA came in. Assuming the business’s plans were sound, an MCA funder would withhold a percentage of merchant account sales before they were even transferred to the business’s bank account. That eliminated the risk of bounced checks for the funder and put the burden of operating on tight cash flow on the small business. Funders then reduced the strain by withholding less in times of weak sales and more in times of strong sales. The percentage system was the bridge to ensure the relationship was not predatory.

I’ve heard the frustrated replies from a business owner that was declined for weak or negative balances. They often sound something like this “Well, if I had cash I wouldn’t be needing a loan from you now would I?!” I feel for these people, I really do, but their approach to debt is misguided. Debt is not something you take on when you are out of money so you can continue business as usual. Debt is for growth or to be used as a temporary cash flow measure. Banks approve applicants that don’t need money because those that NEED IT are more likely to default.

I’ve heard the frustrated replies from a business owner that was declined for weak or negative balances. They often sound something like this “Well, if I had cash I wouldn’t be needing a loan from you now would I?!” I feel for these people, I really do, but their approach to debt is misguided. Debt is not something you take on when you are out of money so you can continue business as usual. Debt is for growth or to be used as a temporary cash flow measure. Banks approve applicants that don’t need money because those that NEED IT are more likely to default.

MCA was the good faith option for small business owners that cried foul over the banks that wouldn’t lend to them. How could there be NOBODY willing to take a chance on them? And so MCA funding companies came along and did what the masses demanded, but at a cost to compensate them for the significant risk.

Today, there is high demand for merchant loans, loans that are evaluated based on a daily average bank balance and monthly revenue. Many people will get less than they want and others should consider traditional MCA instead. Those few that are at the breaking point and believe a loan will allow them to pay past due bills and keep them afloat are better off not applying at all. And for the rest that are contemplating using the $50,000 cash reserve they built up to expand should seriously consider financing instead to protect their cushion as best they can.

Tomorrow, the health inspector could close your doors, vandals could destroy your valuable assets, or the town could perform massively disruptive construction right outside the front steps that cripples sales for months. If you’re running on fumes, you’ll run out of gas. Always keep the cash reserve tank full and nobody will be able to stop you.

– Merchant Processing Resource

../../

MPR.mobi on iPhone, iPad, and Android

MCA Industry More Fractured

February 1, 2013 Everyone agrees that the Merchant Cash Advance (MCA) industry has grown substantially over the last few years. Our best calculations estimated that $600 million in MCA deals took place in 2010. Some believed that figure was too low, especially when Capital Access Network (CAN) projected they would fund $700 million all by themselves in 2012. Could CAN really be funding more alone than what the entire industry including them funded in 2010?

Everyone agrees that the Merchant Cash Advance (MCA) industry has grown substantially over the last few years. Our best calculations estimated that $600 million in MCA deals took place in 2010. Some believed that figure was too low, especially when Capital Access Network (CAN) projected they would fund $700 million all by themselves in 2012. Could CAN really be funding more alone than what the entire industry including them funded in 2010?

The debate starts there because they have put a large focus on their NewLogic subsidiary, a company that specializes in short term loans, not MCAs. And like NewLogic, much of the growth the industry experienced in the last few years has not been centered around split-funding purchases of credit card sales, but on the alternatives. We’ve made it a point in previous articles to point out the lack of consensus on what the product is being called now, especially since everyone is offering their own version of short term financing. We even went so far as to say that by 2015, the term MCA won’t even exist anymore. We may have exaggerated a bit, but after playing around with Google’s Trends tool, we realized that prediction was much more than a hunch.

If MCA has grown so much in the last few years, why is it that 38% more people searched for MCA on Google in December 2007 than they did in December 2012? Why is it that searches for MCA information peaked in February 2009 and never recovered? According to Google’s search data, nearly 50% fewer searches are being made for MCA today than there were three years ago.

Notice that MCA as a term did not really exist on the Internet prior to June 2007. We presented our estimate of when that term was coined in Before it was Mainstream. It first appeared in print in May 2005, but didn’t pick up traction until March, 2006 in private Internet forums. The first Merchant Cash Advance Internet blog began in July 2007, weeks before people began to first start searching for information about the term. It is very likely they were also trying find the blog itself.

So is Google’s data just plain wrong? Is something fishy? The only thing wrong is the belief that the MCA industry is just about MCAs. The creation of alternatives and the recent practice of private labeling have contributed to the decline of MCA.

three new terms: merchant loans, ach loan, merchant financing

Business Cash Advance takes a dive. Seriously, who calls it that anymore? Merchant Funding is on the way back up.

There were 500% more searches for small business loans in April 2004 than there were in December 2012.

So what does this all mean? We leave you to draw your own conclusions. 2007-2009 was a period of sudden mass awareness of MCA but there has never been as much money in the industry as there is now. There are experts that say business owners feel that the recession never ended, causing them to continue hunkering down instead of seeking financing to expand. There are insiders who will attribute this to the negative stigma the product had and the need to call it something else. We believe the most likely suspect though, is the fracturing of the MCA industry. It’s possible that people aren’t typing “small business loans” or “merchant cash advance” into Google because so many companies are promoting alternative financing options that people are looking for those specific products instead.

Whatever the answer is, it appears that alternative business financing has grown tremendously but the MCA term has not. Share your thoughts about this with us. We want to hear theories.

– Merchant Processing Resource

../../

MPR.mobi on iPhone, iPad, and Android

Social Media for Small Business: Food for Thought

January 29, 2013Here’s an interesting trend: blog posts on the subject of the “decline” of social media. Within 90 seconds you can locate three such articles on Forbes.com:

- 3 Reasons You Should Quit Social Media In 2013

- Facebook, Twitter? Can The Decline of Social Media Come Fast Enough?

- Why I Dumped My Smartphone – 2 Months Into Building My Personal Innovation Lifestyle

OK, so three articles can’t be considered a “trend” – but they definitely provide some food for thought.

Should You Quit Social Media in 2013?

The very notion that people are suggesting there might be value in at least “taking a break” from social media should get our attention. Take the three reasons J. Maureen Henderson gives in her article for doing so:

- It harms your self-esteem

- Your blood pressure will thank you

- Online is no substitute for offline

Henderson is speaking to personal self-esteem and gives the example that there are those of us who might feel better about ourselves if we weren’t constantly exposed to technology that forced us to compare ourselves to and compete with over-achieving peers. Yes, it can be personally humbling to discover the jerk you sat next to in biology graduated from Harvard when you barely made it out of State. Small business owners overdosing on social media just might have a similar problem trying to duplicate the social media activities of large competitors whose marketing budget is a big as their small businesses’ net worth – which can be very discouraging and demotivating.

Personal social media activity definitely can get pretty ugly. Name calling, ostracizing, bullying and just generally disrespectful communications can certainly cause your blood pressure to rise. Small business owners can have a similar reaction to preserving and protecting their online brand reputation. While it’s great to be able to communicate directly with customers and clients, the flip side is small business owners don’t have total control over the conversation any longer. Even if you’re monitoring your own platforms (for example comments on your business Facebook page), there’s always the opportunity that you could be missing some “flaming” commentary about your business online somewhere out there on the Internet.

Henderson notes a study stating that one-quarter of those surveyed feel they haven’t fully experienced real-life events due to activities necessary to place those real events on virtual social media platforms. She also points out that most people looking for a job do so online even though 70% of jobs are never posted online and are instead filled via in-person networking. Here is a lesson small business owners might want to take to heart – the impact, effectiveness, and value of getting in front of your customers and clients “in-person.” Real customer experiences are as important as virtual customer experiences.

Are People Dumping Their Smartphones?

We could give you a ton of statistics, but the short answer is a definite NO. As a matter-of-fact, the trend now is major increases in consumers using mobile devices to stay connected online. Some people may be becoming less enamored with “traditional” social media – but we’re definitely going to see an increase (at least for the foreseeable future) in the use of these devices according to a wide variety of studies by reliable resources such as Mashable.

The point is small business owners need to be aware that social media is constantly evolving (and most likely always will be evolving.) And that fact is both a blessing and a curse for small business owners. Certainly having new ways to effectively engage consumers along the “pathway to purchase” is a valuable opportunity. The threat can be not only keeping up with new technologies, but also the ways those technologies impact consumer behavior.

Even “expert advice” can be both confusing and in conflict. For example, here are two predictions in an article you can find at business2community.com:

Joey Sargent, Principal, BrandSprout Advisors: In 2013, we’ll see more social maturity in both B2C and B2B applications. Business will get “social smarts” and more fully integrate social media into their day-to-day operations across the organization. This means less social for social’s sake, and more focus on social media as a legitimate business tool to facilitate communication, engagement and loyalty.

Jayme Pretzloff, Online Marketing Director for Wixon Jewelers: Going into 2013 social media will impact sales more than any other metric because of the continued integration as a marketing platform and the acceptance of users to be marketed to. In 2011, almost 70% of users said that no social media platform influenced their buying decision and in 2012, that was cut in half to 35%. In 2013, this number will be decreased significantly again because these sites have become an integral way to gain access to information on companies, promotions and products.

Bill Corbett, Jr., President of Corbett Public Relations: The hype proliferated by “marketing” people about the tremendous business generating benefits of social media for small business will wind down.

Beverly Solomon, Creative Director at musee-solomon: People are over saturated with social media. They will gradually remove themselves from all but a few networks, blogs, etc. So many ads come in everyday that they have lost their impact. Most people just delete them before reading them. Social media will function more to alert friends of rip-offs than to encourage sales. Only the most clever sales campaigns will have any impact. More and more advertisers will be leaving social media and returning to snail mail, print and other traditional ads. Social media will continue to be a dating hook up, gossip fest and avenue for “gurus” to sell seminars. But real businesses will use social media less and less.

Who’s Right?

With such conflicting advice from subject matter experts – how is a small business owner to know who to listen to? Fortunately this question is easy to answer: Listen to your customers and clients because they – and only they – know how they prefer to be contacted as well as what the content of those communications must be in order to be of value and meaningful to them. This means small business owners need to find out where their target market “hangs out.” Are they already online and using social media? If so, how and where? If not, why not and what other ways would they like to hear from you?

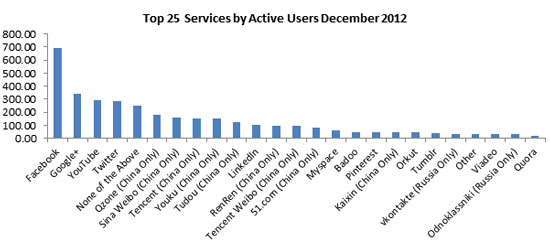

The one constant advantage of social media is the ability to communicate with your market. But it is certainly not the only channel. As for our position on the matter? We’re making social media a bigger priority. We’ve just gotten more involved on Google+, a social network that just passed twitter and youtube to be the 2nd most used platform in the world.

It might be time for the everyday small business owner to take a peek at the big G, especially if they feel like Facebook isn’t delivering.

Guest Authored

– Merchant Processing Resource

../../

MPR.mobi on iPhone, iPad, and Android

Surprise! We Are the Market

January 13, 2013Merchant Cash Advance (MCA) is an alternative to a small business loan. Look around. MCA players have spent so much energy on gaining mainstream acceptance, that we’ve become oblivious to reality. We ARE the small business lending market. There are alternatives out there such as credit cards and SBA loans, but they are industries of their own. Small businesses in 2013 really only have one place to obtain fast unsecured short term financing, and that’s here, the MCA industry. That assumes of course that you agree with our definition of MCA, which we stopped limiting to a purchase of future credit card sales some time ago.

Over the past few months, we began to realize that the only small business lenders making headlines are people we know. Is the country that small or does MCA dominate the market that much?

A glimpse at the sponsored advertisements on Bing in the NYC region:

Where are the multi-billion dollar banks? If $15 a click isn’t in their budget, something is wrong, and it may possibly be due to the fact that business loans aren’t on their priority lists.

Lenders, brokers, and bankers on the front lines can’t stop talking about MCA. It is a recurring theme in their columns:

The alternative financing industry is growing rapidly and, I believe, will continue to grow in 2013. These lenders are extremely entrepreneurial and are leaving the banks behind with their speed and use of technology. Many are backed by premier investment banks and Silicon Valley venture capital powerhouses — investors who understand that entrepreneurs and small-business owners are throwing up their hands in frustration over how long it can take to get a loan from a bank, especially if the loan is backed by the S.B.A. More and more businesses are willing to pay the price of the alternative lenders just to be able to get their capital and move on.

-Ami Kassar

The State of Small Business Lending – NY Times 1/8/13

Ami’s Column on NY Times

Cash advance companies, accounts receivable financiers, factors, and micro lenders all have become increasingly more attractive funders for three reasons: flexibility, use of technology, and speed.

-Rohit Arora

Three Reasons for the Rise of Alternative Lending – Fox Business 11/29/12

Rohit’s column on Fox Business

Here’s a dilemma that might have contributed to the growth of MCA… Banks don’t like offering loans and business owners don’t like applying for them if it’s hard:

There’s a large small business segment that needs and wants to borrow on a commercial basis, but their needs are very small. Business owners want $10,000, $20,000 or $30,000 loan–the average is somewhere around $25,000. Traditionally, that’s been a very unprofitable business for a bank. Some banks argue that they are willing to lose money on those loans because they can make it up in deposits. But what happens when the borrower has no deposits? It’s a very tough balancing act.

– The Federal Reserve Bank of San Francisco

A newsletter report that reveals banks lose money on small business loans

Community Investments Volume 8; No 4; Fall 1996

Business owners say the documentation involved is overwhelming. They’ve also found the qualification terms almost impossible to meet.

– Catherine Clifford

Feedback reveals that a burdensome application process and extensive paperwork requirements are enough to discourage business owners even if the loans carry 0% interest.

CNN 1/26/10

Thousands of researchers publish statistics on bank lending every month. Not only do they all contradict each other but journalists that use this data to make bold claims often fail to acknowledge that an increase in bank lending has nothing to do with the applicants, the economy, or the banks themselves. It has to do with the Government. We all know that the SBA will cover the losses banks incur, but there are programs that go one step further. The Federal Government actually bribes banks to make loans. For example, the Small Business Lending Fund is a dedicated investment fund that encourages lending to small businesses by providing capital to community banks. Meaning, covering the losses on defaults doesn’t seem to be enough, so they’ll actually provide the money to make the loans as well.

Click to see full size on mobile

According to the SBA, small business bank borrowing totaled $584.1 billion in the third quarter of 2012. That number dwarfs the volume produced by the MCA industry, but its not an apples to apples comparison. A loan of $1 million dollars is within the range of a small business loan by the SBA, an amount atypical (though not impossible) in the MCA world. Banks are also prodded and coddled by the Government so much that it has reached the extent that we dare claim they are an extension of the Federal Government itself. There’s some food for thought for the Occupy Wall Street movement! They also conveniently got bailed out when they were on the verge of failure, a safety net that MCA companies don’t have.

According to the SBA, small business bank borrowing totaled $584.1 billion in the third quarter of 2012. That number dwarfs the volume produced by the MCA industry, but its not an apples to apples comparison. A loan of $1 million dollars is within the range of a small business loan by the SBA, an amount atypical (though not impossible) in the MCA world. Banks are also prodded and coddled by the Government so much that it has reached the extent that we dare claim they are an extension of the Federal Government itself. There’s some food for thought for the Occupy Wall Street movement! They also conveniently got bailed out when they were on the verge of failure, a safety net that MCA companies don’t have.

Subtract the Federal Government’s meddling and there is only one profitable form of B2B lending, Merchant Cash Advance. That is of course again if you accept our definition. There are many young B2B lending firms that claim to be an alternative to MCA, who then go on to describe their product in a manner that is textbook MCA.

Our thesis may be debatable and lacking in concrete proof, but we’re not writing dissertations here. Business owners are increasingly looking to the Internet for loan information and it’s obvious what they’re finding. One would expect a quick Internet search to bring up ads for the billion dollar powerhouses, you know the ones that are given millions to lend out and then millions again when the loans go bad. Instead we find companies owned by friends or friends of friends. The small business loan market isn’t run by anonymous Wall Street kingpins, it’s run by a small community of entrepreneurs that all started from the ground up. Only the community isn’t so small anymore. There was once a handful of MCA companies claiming to be an alternative to a small business loan. Now there are a handful of companies claiming to be an alternative to MCA. It doesn’t take a genius to figure out why that is. After years of fighting to be recognized in the market, something remarkable happened, we became the market itself…

– Merchant Processing Resource

../../

Movember Rocked!

December 1, 2012 Movember: Mo’ Merchants, Mo’ Deals

Movember: Mo’ Merchants, Mo’ Deals

The pre-holiday season is usually big in the Merchant Cash Advance (MCA) industry but this year seemed different. We’ve been saying that we’ve entered a new era for a long time, but it’s finally starting to seem real. It feels like 2007 again in a way, when everybody was getting rich and nobody even knew what the heck they were selling. It took years for account reps to finally stop referring to advances as loans and by then it was too late because the ACH loan industry was born.

E-mails like this don’t happen very much anymore:

You know… the ones where the deal would be blatantly shotgunned to multiple companies at once. The major broker shops would “accidentally” CC everyone instead of BCC to let the funders know who was in charge.

That’s not to say that deals don’t get shopped, Some do, but the circumstances have changed. To minimize the risk of being flooded with bad paper, funders ask resellers to put their money where their mouth is. The syndication game has become THE game in town and it’s led to Super ISO networks like the Factor Exchange. A user on the DailyFunder that seems to be intimately familiar with Factor Exchange is quoted as explaining the model like this:

The “mom and pop” ISOs and “Onesy-Twosey” brokers are backed by one giant ISO network and The Factor Exchange assumes half of the risk by syndicating 50% on nearly ever deal…

The massive volume of FEX submissions to lenders gives the ISOs power to negotiate for better rates and terms, One point of submission reaches 15+ lenders, the merchants credit is only pulled once, and the commission is passed straight through to the ISOs because FEX makes their money from participation.

Companies like this empower the smaller brokerages…

Who Did Mo’ Deals in Movember?

Yellowstone Capital broke their single day funding record… TWICE. This actually happened on back to back days. Executive management reported that they funded approximately $3 million in 48 hours.

Who Got Mo’ Money?

Wall Street wizard and business professor, Steven Mandis acquired a stake in Bethesda-based RapidAdvance. The news is all the more interesting with the fact that RapidAdvance is easily one of the top 5 largest players in MCA. Single individuals don’t exactly just walk through door and buy a stake in companies like this. Mandis is taking on a Strategic Advisor position and it’s our guess Rapid is about to enter another major phase of growth.

Who Got Mo’ Likes?

Merchant Cash and Capital’s (MCC) facebook fan page has gotten thousands of Likes since the third week of Movember when they announced their charity campaign. For every new Like until December 7th, MCC is donating $1 to the American Red Cross to help people that were affected by Hurricane Sandy.

Who Got Mo’ Wins?

RapidAdvance was the first team to clinch the playoffs in the MCA industry fantasy football league for charity. Something tells us that Mandis is behind their incredible winning streak.

Who got Mo’ Leads?

You did if you bought leads from either one of our lead advertising partners, Meridian Leads or SmallBusinessLoanRates.com.

Lendio has also been making a splash on the MCA lead scene with Dave Young being a big contributor on DailyFunder. To discuss pricing, he can be reached at dave.young[at]lendio.com

Who lied Mo’?

According to CNN’s statistics, 247 million people in the U.S. went shopping on Black Friday. That’s equal to the entire American population over the age of 14. Something doesn’t smell right with these numbers. It’s our guess that CNN is using Mitt Romney’s polling experts. 😉

But someone else lied just a little bit Mo’. On Movember 26, 2012, PRWeb published a release that claimed ICOA Inc., a small tech company in Rhode Island was acquired by Google for $400 Million. The release turned out to be a hoax as part of a stock pump and dump scheme. Many critics have been left wondering why PRWeb didn’t do anything to verify its authenticity. Considering PRWeb is such a widely used PR service in the MCA space, we can testify that they’ll pretty much publish anything so long as you pay the fee. Some smaller companies use it as part of their SEO campaigns, which explains why there are so many strange looking releases out there that seem to repeat the same keyword in every sentence.

ABC Funding Co Just announced a program that will help small businesses in need of cash by providing these small businesses in need of cash with a special type of financing that will hep them if they are a small business in need of cash. Not exactly New York Times material…

Will Movember be followed by Make-a-lot-of-Doughcember? We’ll find out!

– Mo’chant Processing Resource

../../