Legal Battles to Keep an Eye On

February 18, 2017CFPB

The CFPB’s organizational structure might not be unconstitutional after all. The D.C. Circuit which originally concluded it was unconstitutional, has decided to rehear the case. Oral arguments on the matter are scheduled to take place on May 24, 2017. A detailed summary of the issues can be found on The National Law Review.

TCPA law

Serial litigant Craig Cunningham is one of two petitioners behind the challenge to an FCC interpretation of what constitutes “prior express consent.” Specifically, the petitioners want to get rid of implied consent resulting from a party’s providing a telephone number to the caller. The FCC has called upon the public to comment. If the FCC indeed decides to narrow the scope of their interpretation, it would become easier for litigants like Cunningham to bring lawsuits. Read a longer brief of the issue here.

New York Lending License

Governor Cuomo’s budget proposal contains changes to Section 340 of New York’s banking law and it has the potential to completely change the alternative landscape in the state. Read a full analysis here.

Platinum Rapid Funding Group Ltd v VIP Limousine Services Inc. and Charles Cotton

After a landmark trial court decision surrounding merchant cash advance last year, plaintiff Platinum Rapid Funding Group went on to obtain a judgment against defendants in an amount exceeding $100,000. However, filed papers on the docket show the case may be heading to the Appellate Division.

Merchant Funding Services, LLC v. Volunteer Pharmacy Inc

Merchant cash advance companies may find themselves having to answer for an unfavorable ruling issued in Westchester County, New York, in which a judge vacated a Confession of Judgment and voided the underlying future receivables transaction. A more in-depth brief can be read here. Notably, the judge in that decision was the same one that decided Pearl Capital Rivis Ventures, LLC v. RDN Construction, Inc.

Lender Or Broker – Do You Know Your Partner?

December 15, 2015I probed the audience here on AltFinanceDaily a couple of times this year. Back in June 2015, I wanted to know if you knew what you were selling when it came to the merchant cash advance product? In October 2015, I wanted to know if you knew what you were buying when it came to leads versus data? So as we close out 2015 here in December, I wanted to probe the audience of AltFinanceDaily once more, this time asking: do you know your partner?

THERE’S NO SLOW DOWN COMING (THE NEW ENTRANTS WILL CONTINUE TO RUSH IN)

I’ve been asked by individuals within the industry and those outside of it, on my opinion of when the mass rush of new entrants into the market will slow down. In my opinion, the Year of the Broker will not stop in 2015, but will continue into 2016 and most likely into 2017, when the chickens finally come home to roost for the new entrants, who mostly lack the leveraged networks needed to survive and thrive, and instead are relying on one or more of the following strategies which will no longer be efficient going forward:

- UCCs

- Aged Leads

- Random SIC listing calls

- Random Yellow page calls

- Parking your car down the street and randomly walking into merchant shops

- Stacking behind a 2nd position

Those who are leveraged with quality strategic partnerships, networks and access to exclusive data records, will be the ones that control the market going forward, while others will fail to remain profitable in this ever changing, integrating and evolving marketplace that we all fight tooth and nail in.

Those who are leveraged with quality strategic partnerships, networks and access to exclusive data records, will be the ones that control the market going forward, while others will fail to remain profitable in this ever changing, integrating and evolving marketplace that we all fight tooth and nail in.

But I must ask you if you know your Partner, as this mass new entrance of players have created many documented cases of brokers having deals stolen, back-doored, commissions not paid, renewal commissions cut-off, and other unscrupulous acts. The vast majority of these documented cases are coming from broker-to-broker relationships, with one broker submitting a file to another broker, but being totally unaware of the fact that they are not working with a “direct” funder or lender.

As we go forward through our changing marketplace, where profits will get tighter, strategic partnerships will be your driving competitive advantage and where access to merchants in general from a “cold-calling” perspective will get more restrictive, you just can no longer afford to be the victim of an unscrupulous act and lose commissions. As a result, going forward, you must indeed know your partner.

THE SEVEN

The following are the seven ways that one could participate in our space:

The Referral: They are not involved in the actual sales process at all, which includes selling rates, collecting paperwork, signatures, etc. All they do is refer a person’s name, telephone number and email address, and might collect an upfront referral fee for doing so. These are usually members of a strategic partnership such as a bank, credit union, credit card processor, accounting firm, insurance firm, etc.

The Sub-Broker: They work as a broker-to-a-broker, going out and doing all of the activity involved with the sales process and submitting the package to a broker, who will then submit it to a couple of funders to “close” the deal. They would then be paid a portion of the commission that the broker gets from the funder or lender once the deal funds, so if the broker gets 6 points, the sub-broker might get 2 or 3 points. Sometimes these individuals (sub-brokers) are willingly signing up for this arrangement, and sometimes they are unwillingly signing up by believing the broker is an actual direct funder or lender, when they are not. This leads to a majority of the issues I’ve identified such as having deals stolen, deals back-doored, commissions not paid, renewal commissions cut-off, and other unscrupulous acts.

The Broker: They go out and do all of the activity involved with the sales process and submit the package to a funder or lender, then manages certain aspects of the closing process such as getting additional signatures, questions answered, stips collected, etc. They would then be paid the commission they set on the deal by marking up the funder or lender’s buy-rate. So if the buy-rate is a 1.12 for a 6 month period, and they marked it up to 1.18, they would be paid 6 points on the deal.

The Syndicate: They would basically do everything a Broker would do, but for some deals they will put some of their own capital resources on the line through syndication, it might be their own equity sources or they might use debt sources such as those from credit card no interest promo deals. The syndication process just allows them to take more money home on the deal.

The Direct Funder/Lender: They have built their own underwriting platform and formulas to lend out either merchant cash advances and/or alternative business loans with a focus on a certain level of profitability and to maintain a certain default rate threshold.

The All-In-One: This is a firm that basically is structured as a direct funder/lender, but they also broker out some deals and on those deals that are brokered out, some of them include the firm syndicating to increase their take home revenue on the deal in particular.

The Investor: This is an equity or debt source that invests capital into a direct funder/lender’s underwriting platform and formula, seeking to capitalize on the high profits that result from a merchant successfully paying back either a merchant cash advance or an alternative business loan.

KNOW A DIRECT FUNDER/LENDER WHEN YOU SEE ONE

When I first started reselling the merchant cash advance and alternative business loan products in late 2009, I noticed that one of the ways to differentiate yourself in the market was to say that you were a “direct funder”, apparently the mentality was that merchants only wanted to talk to the people who could actually do the lending.

Well, I preferred to just admit upfront to merchants that I was a broker, but just explain that the industry is complicated in terms of the pricing models that are present. If you qualify for A+ Paper pricing, you want to make sure you are submitting your package to an A+ Paper lender, otherwise, you might be a merchant with a 700 FICO, clean banks, no liens, and other A+ Paper like qualifications, but might be submitting your package to a funder that will only spit out 6 month offers at 1.35 factor rates. So if you are seeking to work with a direct funder/lender (even if they also syndicate or broker on the side), you just have to know one when you see one, by using some of the following rules of thumb:

- Licensure: Look for some type of state licensure or registration. You can usually find this out by asking the firm their corporate legal name and research this in the state database of where they are incorporated or other states of where they do business.

- Track Record: Look for a proven track record, which means they should have funded at least $10 million in volume and have in business at least 12 – 24 months.

- Fully Staffed: Look for a full office staff, by the firm being very small, this is how your deals end up getting lost, stolen, or the underwriting process drags on for seemingly forever.

- Online Identity: Look for a professionally designed website with a business email address. In addition, look for some type of online press release about the shop opening, a media interview, or news release about an equity or debt financing round. Look up the principals on LinkedIn, and the company should come up on Google as well as other online directory listings including the Better Business Bureau. If you can’t find anything about the company or the principals online in some sort of professional listing and/or publicity based format, I would move on.

THE FINAL WORD

I don’t think there’s a worse feeling one can have, to have gone through the process of spending money to generate a qualified lead, to “close” that lead by getting them to send you an application package, and then to submit the package to your supposed “funder”, only to have the deal stolen and back-doored because your supposed “funder” was nothing but an unscrupulous broker the entire time.

Making sure you select good partners is vital to your survival on this battlefield called “alternative lending”, a battlefield that we fight, scratch, and claw on daily to feed ourselves, our families, and help make the lives of small business owners more efficient than before we got here.

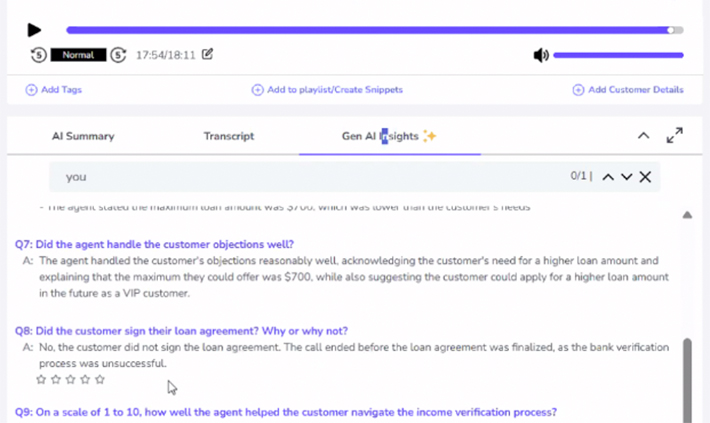

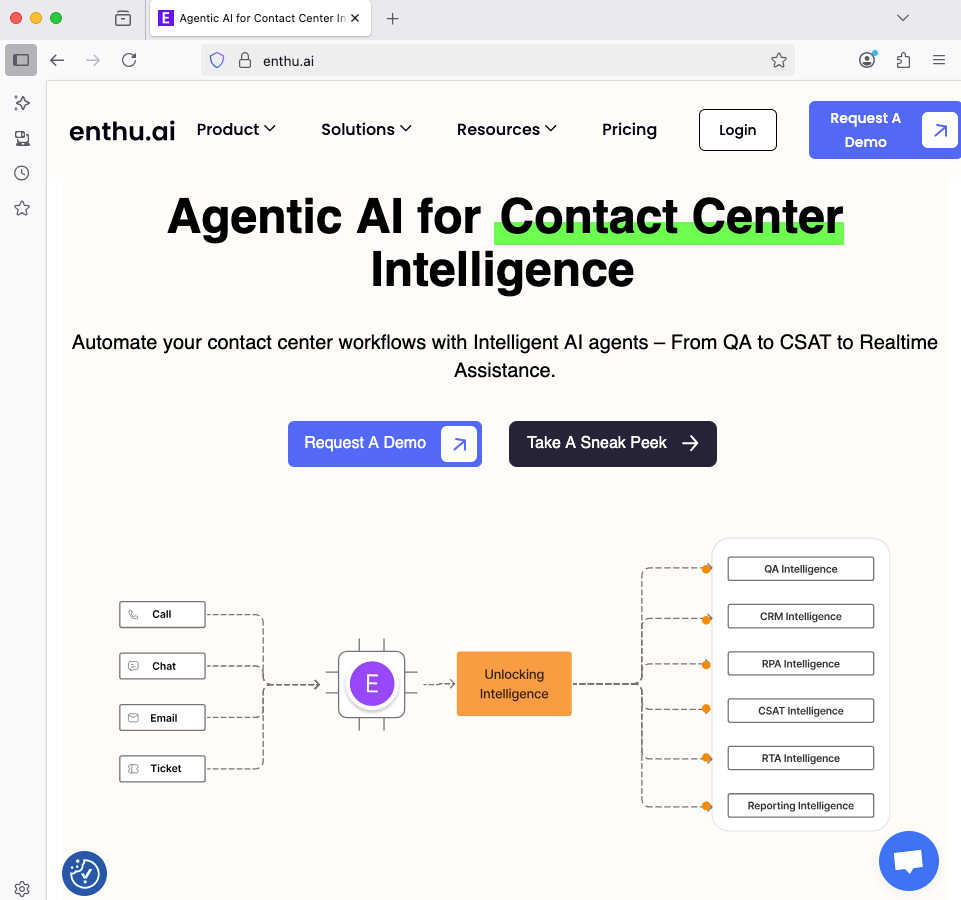

How Are Your Sales Calls Going? How One AI System Can Score Performance

July 21, 2025 The subjectivity era of evaluating sales reps is over. Sales calls can now be dissected down to every little nuance of why something went right or wrong, and it can be done at scale with no human bias. These interactions can also be aggregated to determine strengths, weaknesses, trends, compliance, confidence levels, and more, all thanks to AI and technology available right now.

The subjectivity era of evaluating sales reps is over. Sales calls can now be dissected down to every little nuance of why something went right or wrong, and it can be done at scale with no human bias. These interactions can also be aggregated to determine strengths, weaknesses, trends, compliance, confidence levels, and more, all thanks to AI and technology available right now.

“The way [our] platform works is we integrate with the dialer,” says Atul Grover, Co-founder and VP of Sales for Enthu.AI. “Typically, what we have seen with our clients, the calls are automatically pushed within two or three minutes after the conversations are done.”

With Enthu, a company’s call recordings go through their AI system to be analyzed based on either their own scorecard, the client’s, or both. Whatever the outcome of the call, lost sale, closed deal, or neither, management receives a report to see how the rep performed. Did the rep try to build rapport? What were the objections? Did they handle objections well? Did the rep sound confident when answering difficult questions? Across hundreds or thousands of calls each week, any rep can get an unbiased report card of their strengths and weaknesses. These metrics can then be compared with peers, without the worry of human bias deciding the outcome. They can’t blame the boss for simply favoring another rep, for example.

Originally, when Enthu started, they focused mainly on keyword spotting for compliance purposes, evaluating whether or not reps were saying what they were supposed to across thousands of calls. But that had its limitations.

“That’s how we started our journey, using purely keyword spotting,” Grover says, “but the challenge over there is that you can’t basically expand or scale it. So that’s why we use our AI approach, where it’s primarily intent-based rather than keyword-based. So we look at the intent of all the conversations.”

Rather than AI replacing sales reps, as some theorize might happen over time, it can be used to make them a whole lot better. And this is already being employed today. Enthu, for example, is currently being used in financial services, healthcare, home industries, property management, and more. Grover says clients are already using it to measure disparities in call performance and then using those insights to coach reps who score on the lower end.

“Our platform also offers the ability to create a playlist for the good recordings, which you can use to train your new agents,” Grover says. “So rather than training in general that’s like, ‘okay, this is our company product, this is our company offerings, you should talk like this,’ they can share those good recordings with the new agents so they can listen to how their good sales agents are doing, and then get trained on the real data.”

Recording calls and finding good ones is not a new capability, anyone can do that. But it’s the ability to identify certain call situations at scale that makes all the difference when trying to evaluate and coach. If a new objection is tripping up the team, management can pull every instance it has come up, calculate its frequency, and use that information to determine the best path forward. These are things that would typically rely on the “vibe and feel” of the sales floor, as reps relay information to the boss, who must then assess whether the trend is legitimate or just a statistical blip.

Independent analysis can also be critical when a company is evaluating a lead source or referral partner, especially if that partner is also expecting to be judged objectively. And when the lead source changes, the AI can be told in advance whether the calls are outbound or inbound, hot or cold, or how they differ from other types of calls the company handles. The resulting evaluations can then reflect those circumstances.

Success, in this way, can be gamified, allowing reps to strive for higher grades across all areas of a call and objectively compare themselves to colleagues in an emotion-free environment. The AI can score each call or aspect of a call on a scale from 1 to 10 and produce a summary score for each rep over a day, week, or month, unlocking new motivational challenges. An underperforming rep could be recognized for a top score in overcoming objections, for example, even if they didn’t close the most deals. Picture a Broker Battle, but the judge is an AI.

And it’s not just sales. Clients can also use the technology for compliance, to determine whether proper disclosures were made, correct terminology used, and whether the tone of the call remained positive.

And it’s not just sales. Clients can also use the technology for compliance, to determine whether proper disclosures were made, correct terminology used, and whether the tone of the call remained positive.

“It’s definitely going to be great help for the sales organization,” Grover says. “And if we talk about the lending industry, you talk about compliance and everything, or let’s say the collections department, because they want to make sure that their agents are not screwing up, because there’s legalities involved if they mess up anything. So that’s what our system will flag, where they are doing right or where they’re doing wrong.”

If a client wants to keep keyword spotting as part of the analysis, they can. Grover says pre-set words can be marked as zero-tolerance or flagged for management. The more data and calls the system analyzes, the better it gets.

Grover adds that even if a client isn’t ready to fully integrate Enthu, they can still use old call recordings to access analytics.

“We have some customers in that space where they don’t have a dialer but they still have the recording,” Grover says. “So our platform also allows to upload the recordings directly by the client itself, on the platform itself, where they can upload the calls manually, then you’re still going to get the same intelligence, same analytics, same scorecard mechanism, even if you upload it manually.”

B2B Finance at AltFinanceDaily

July 5, 2024 When Broker Fair first debuted in 2018, the keynote speaker was none other than Ryan Serhant, then a fast rising New York City real estate broker and star of Bravo’s Million Dollar Listing. Today he’s got his own Netflix Series called Owning Manhattan.

When Broker Fair first debuted in 2018, the keynote speaker was none other than Ryan Serhant, then a fast rising New York City real estate broker and star of Bravo’s Million Dollar Listing. Today he’s got his own Netflix Series called Owning Manhattan.

“After selling real estate for 12 years, I decided to start my own company,” Serhant says in the trailer for the first episode, “and if you can’t sell, you can’t be here.”

That New York hustle attitude was the connecting link for why Broker Fair chose him despite the broker audience being largely engaged in small business financial services at the time. But since then the small business finance broker community has become increasingly diversified in its product offerings and real estate is frequently one of the assets on the menu.

“People will be surprised how many clients have real estate, not just a [primary home], but they own just a small multifamily down the road that they never touched or tapped into,” said Julio Sencion, Principal at Alta Financial, in a recent interview with AltFinanceDaily.

Companies like World Business Lenders figured that out a long time ago while still more discovered the business during the covid recovery, leading AltFinanceDaily to produce a video miniseries about real estate investing in the summer of 2021. The guests ranged from real estate influencer Ralph DiBugnara to NestSeekers International’s Chief Economist Erin Sykes to a couple of old fashioned guys named Danny and Bruce who started investing in real estate across New Jersey long ago.

AltFinanceDaily also interviewed house-flipper turned real estate tech CEO Andrew Luong of Doorvest, did a deep dive as to why real estate was becoming the side hustle of choice in the industry, and even bought real land using the blockchain for the purpose of a story.

Equipment financing has also taken off, leading AltFinanceDaily to produce the first ever sales reality series named Equipping The Dream in 2022.

That’s been complemented by regular coverage and even sitdown interviews from Andrew Carman, Steve Geller, and George A. Parker.

AltFinanceDaily’s Sean Murray has previously presented at the International Factoring Association’s (IFA) Fintech educational event, been a guest on the Coleman Report run by renowned SBA expert Bob Coleman, and moderated panels separately for the New York Institute of Credit and the Alternative Finance Bar Association.

Murray was also the host and producer of the industry’s first ever Broker Battle which took placed in Miami Beach this past January.

AltFinanceDaily is also affiliated with the largest online small business finance community in the US, DailyFunder, and has produced nearly two dozen events since 2017.

“Back in 2018, there was a question that Serhant posed on stage to the Broker Fair audience to make sure he understood where they were coming from,” Murray said. “‘You guys are all B2B right?’ he said, and I think his characterization was spot on, because B2B is pretty much what we’ve been all along.”

AltFinanceDaily is collaborating with the Small Business Finance Association on the B2B Finance Expo that’s taking place in Las Vegas on September 23-24. For info, visit: https://www.b2bfinexpo.com

Expecting a Huge Turnout for AltFinanceDaily CONNECT MIAMI

November 29, 2023Have you heard? Prominent industry insiders are expecting a huge turnout for AltFinanceDaily CONNECT MIAMI taking place on January 11th in Miami Beach. The signature event, which this year features the FIRST EVER Broker Battle™, is drawing interest from the funder and broker community like never before. Other notable things to catch include the all-in-one broker info session called Broker Brilliance, a guest keynote from industry veteran David Goldin, technology showcases, and tons of networking! January 11th is right around the corner. See you there!

AltFinanceDaily Thanksgiving Memes 2023

November 21, 2023It’s Thanksgiving again so you know what that means? Memes! This tradition (which we’ve kept up with as often as possible) started on AltFinanceDaily in 2012. We hope you have a wonderful holiday and strong end-of-year.

And now, the memes:

See previous year memes:

2022 Thanksgiving Day Memes

2021 Thanksgiving Day Memes

2020 Thanksgiving Day Memes

2019 Thanksgiving Day Memes

2018

2017

2016

2012

Plus, don’t forget to register for AltFinanceDaily CONNECT MIAMI taking place on January 11 in Miami Beach. This year’s event will feature the first ever Broker Battle!

Kris Roglieri Bankruptcy Converted to Chapter 7, The End of NACLB?

May 15, 2024 A judge approved a motion to convert the Chapter 11 bankruptcy proceeding for the embattled Kris Roglieri to a Chapter 7. The intent behind this is to kickstart the process to sell off Roglieri’s assets for the benefit of creditors whereas before Roglieri hoped that his various wholly owned businesses could somehow continue. The trustee, however, said that such an outcome was impossible given that Roglieri did not maintain financial records, has no revenue coming in, is being investigated by the FBI for ~$100 million in allegedly missing customer funds, and has no path forward. The creditors at issue in the matter felt similarly.

A judge approved a motion to convert the Chapter 11 bankruptcy proceeding for the embattled Kris Roglieri to a Chapter 7. The intent behind this is to kickstart the process to sell off Roglieri’s assets for the benefit of creditors whereas before Roglieri hoped that his various wholly owned businesses could somehow continue. The trustee, however, said that such an outcome was impossible given that Roglieri did not maintain financial records, has no revenue coming in, is being investigated by the FBI for ~$100 million in allegedly missing customer funds, and has no path forward. The creditors at issue in the matter felt similarly.

Among Roglieri’s wholly owned assets are Commercial Capital Training Group and the National Alliance of Commercial Loan Brokers (NACLB conference), according to documents he previously submitted to the court. He owns 100% of the membership interest in each LLC. During a prior hearing, the Chapter 11 trustee asked Roglieri if he understood that he could not transfer NACLB’s assets without trustee approval after rumors swirled that he was trying to sell it. At the time, Roglieri said that there had been no serious talks in that regard. It may have been a hard sell and could still continue to be. Despite the NACLB conference’s longevity, for example, Roglieri asserted during the proceedings that he did not maintain formal financial records for it and there are no balance sheets, P&Ls, or statement of cash flows related to it. It also apparently stiffed the venue of its last event since it lists an unpaid debt of $436,237 to Caesars Entertainment in Las Vegas.

The NACLB conference has also apparently changed its name in order to distance itself from its connection with Roglieri, according to emails reviewed by AltFinanceDaily. On March 25, an official NACLB mass email communication asserted that the conference would go forward “despite uncertainties surrounding this year’s event due to unrelated legal issues” and that “we are thrilled to announce that the annual conference will proceed this November under a new rebranded name, maintaining the trusted team that has organized the event for the past 9 years.”

Following that, an official NACLB conference representative sent out emails affirming that it was rebranding to the “Commercial Loan Broker Association” and that the conference would actually take place in a new location with a different date.

The Receiver managing Prime Capital Ventures, LLC, the main entity at the heart of the Roglieri saga, filed Chapter 11 bankruptcy protection for it on Tuesday. As part of that, he stated that the entity owes more than $100 million to its creditors.

The Pain in America’s Food Supply Chain

January 29, 2021 It was last November, Mark Mavilia says, when he and three friends in Washington, D.C. rendezvoused for dinner at Ghibellina’s, an Italian gastropub in Logan Circle “specializing in Neapolitan-inspired pizzas and craft cocktails,” says the online restaurant guide “Popville.”

It was last November, Mark Mavilia says, when he and three friends in Washington, D.C. rendezvoused for dinner at Ghibellina’s, an Italian gastropub in Logan Circle “specializing in Neapolitan-inspired pizzas and craft cocktails,” says the online restaurant guide “Popville.”

Hold the pizza! Mavilia, who is art director at the Association of American Medical Colleges, couldn’t wait to tuck into the pasta-bolognese, his favorite dish. “In my opinion,” he says, “it’s the best in the city.”

Or rather was the best. When the foursome assembled outside the restaurant, they were disappointed to find Ghibellina’s had closed. “They had shut down for good,” Mavilia says, adding: “It was not boarded up. Just a note on the door thanking patrons for their support. I will surely miss the bolognese.”

The Ghibellina brand was later consolidated into a sister restaurant called Via in Ivy City.

Mavilia’s experience in Washington is typical of a nationwide phenomenon. Tens of thousands of restaurants and bars and eateries of every kind have closed their doors as the Covid-19 pandemic has ravaged the country and Americans have sharply limited their social interactions. As U.S. fatalities surpassed 410,000 in January, the economic damage to the restaurant and bar businesses has been staggering.

“Washingtonian” magazine keeps a running tab of restaurants that have closed their doors in and around the nation’s capital owing to the pandemic. In December, its tally listed 75 casualties in The District alone, including such icons as the Post Pub and Montmartre, Momofuku and Tosca, plus many more in the Maryland and Northern Virginia suburbs.

“Washingtonian” magazine keeps a running tab of restaurants that have closed their doors in and around the nation’s capital owing to the pandemic. In December, its tally listed 75 casualties in The District alone, including such icons as the Post Pub and Montmartre, Momofuku and Tosca, plus many more in the Maryland and Northern Virginia suburbs.

The area around the White House dominated by the influential K Street law firms and lobbyists, and the World Bank and International Monetary Fund has been nearly barren. With few people trickling into the central city, says Madeleine Watkins, owner of 202strong, a fitness club featuring personal trainers, her business is getting battered. Receipts are off by 80% over last year and she sees the effects all around her.

“There are definitely a lot of restaurants closed, but I’m hoping and praying that lot of it is temporary,” she says. “We need people to come downtown for Washington to be a vibrant and bustling city with coffee shops, restaurants, and sandwich shops.”

One hopeful sign: Tosca, a white-tablecloth restaurant near Metro Center which boasts an enthusiastic, upscale audience and earns 4.8 stars from customer reviews, promises to re-open in the spring. “This was my go-to Italian restaurant near my office,” declares Deborah Meshulam, a partner at multinational law firm DLA Piper and a former lead trial counsel at the Securities & Exchange Commission. “I loved their grilled Branzino and pretty much anything else they made.”

The Minneapolis Star-Tribune recently counted 94 restaurants that had closed down permanently in the Twin Cities. “Saying goodbye to a beloved watering hole, a neighborhood café or a four-star restaurant is never easy,” reporter Sharyn Jackson wrote in late December. “But in 2020, the pain kept coming as the pandemic brutalized the Twin Cities hospitality industry.”

Among the notable casualties, were Bachelor Farmer, Muddy Waters, and Fig+Farro.

Angharad Bhardwaj, communications manager at medical technology company GenesisCare and a lifeling Minnesotan, told AltFinanceDaily of her sorrow at learning that Fig+Farro had closed. “My husband and I were there for their opening, and I am so sad to see it close,” she says. “This was one of our favorite restaurants, just steps away from our condo in Uptown. We spent our first Valentine’s Day there. It was fresh vegan food. We even sat with the owner’s children one night. The little boy was helping his parents with the restaurant, taking orders.”

In Denver, online entertainment publication “Do303” recently highlighted closures of 15 area restaurants it called “the great ones that kept our hearts and bellies full for years.” Notable among the cohort was El Chapultepec, 12@Madison, and Biju’s Little Curry Shop. Michelle Parker, a Denverite who has a short commute to suburban Westminster where she is the City Clerk, says: “The feeling around town is that this has been a big loss to neighborhoods and to the food scene, which was just coming into its own as the pandemic hit.”

Nationwide, more than 110,000 restaurants, bars and food-service establishments have closed their doors, reports the National Restaurant Association, the premier Washington-based trade group representing the food-service industry. The membership includes not only restaurants, pubs and cafes but non-commercial restaurant services, cafeterias, institutions like college cafeterias, and even food services at military installations.

Nationwide, more than 110,000 restaurants, bars and food-service establishments have closed their doors, reports the National Restaurant Association, the premier Washington-based trade group representing the food-service industry. The membership includes not only restaurants, pubs and cafes but non-commercial restaurant services, cafeterias, institutions like college cafeterias, and even food services at military installations.

The food-service industry is the nation’s second largest private employer and accounts for $2.1 trillion in economic activity, reports Vanessa Sink, director of media relations at the trade group. On average, when a restaurant closes, fewer than 50 people find themselves unemployed, but it adds up. As many as eight million food-service workers – waiters and bartenders, hosts and hostesses, cashiers, general managers and dishwashers, parking valets and cooks and chefs — were out of a job at the height of the pandemic in early 2020.

Curtis Dubay, senior economist at the U.S. Chamber of Commerce in Washington, D.C., notes that a whole array of food-service jobs are interwoven into the fabric of the U.S. economy. “Anything that involves large gatherings – transportation, travel and tourism, athletic events, the theater, the hospitality industry,” he says. “In places like The Hyatt in Orlando, food-service workers are involved in setting up a ballroom for conventions and small meetings. It’s a big part of the economy.”

Since the spring, many of the lost jobs came back as restaurants were able to add take-out and delivery services. Many states and localities allowed restaurants to re-open with outdoor-seating, limited occupancy, customer-spacing, and Plexiglas booths. Through the end of November, 2020, 75% of the lost jobs were recovered but 2.1 million food-service jobs had still vaporized.

As more and more people prepare their own meals at home, the switch from dining-in to curbside and takeout services has met with limited success. For take-out people are more likely to order fast-food from Chick-fil-A or Pizza Hut and Domino’s rather than something fancy. “Who wants to spend $60 for a meal you have to eat out of a cardboard container,” one Minneapolis woman complained to AltFinanceDaily.

Restaurant closures, meanwhile, are having devastating consequences across a broad swath of society. “When a restaurant closes or has to cut back, it not only impacts the economy of the local community, it also affects the culture of the community,” says Sarah Crozier, communications director at Main Street Alliance, a 30,000-member, small-business advocacy group headquartered in Washington, D.C. “Local, independent places are where we create our memories as cities and towns. From losing the cries of “Keep Austin Weird” to stripping away the innovative recipes coming out of Raleigh, N.C., it deeply scars the culture and feeling of a place when we have only chain restaurants to fall back on.”

Adds Sink: “Restaurants are the cornerstone of communities. You often find that neighborhoods and local economies have built up around a restaurant. Restaurants provide jobs, they pay rent and contribute to the tax base. Other businesses will grow up around them. People will go to a restaurant – and then they’ll go next-door to shop.”

Food-service establishments are also long-term tenants. The “vast majority” of the closures, Sink asserts, have involved restaurants that had been in business for more than 16 years. Roughly one in six had been in operation for 30 years or more.

Backlit downtown restaurants with inviting awnings, valet parking and limousines idling out front are giving way to boarded-up buildings, many battened down with battleship-gray steel shutters. “I’ve been talking to mayors about empty storefronts and the effects of business failures,” says Karen Mills, former administrator at the U.S. Small Business Administration and a senior fellow at Harvard Business School, says. “It’s significant. It devastates the whole community and brings down the whole environment. People don’t want to go downtown to Main Street anymore.”

Many cities and towns have invested heavily to revitalize their inner cities and urban areas around restaurants and bars to add sparkle to the nightlife and draw visitors and tourists. The economic development strategies often commingle trendy restaurants and nightclubs, shops and boutiques with spruced up warehouses or old buildings converted into artists’ studios, lofts and apartments.

Some cities feature sports arenas and stadiums as a major draw, and the food offerings go beyond hotdogs, peanuts and Cracker Jack. St. Louis’s “Ballpark Village” promises, according to its website, a “buzzing, sports-themed district close to Busch Stadium with restaurants, bars and nightlife venues”; Baltimore’s Inner Harbor, which is walking distance to Oriole Park at Camden Yards, features a science center, aquarium and historic warships moored at the dock, as well as a complex of bars, eateries and music venues in a repurposed electric-power station known as “Power Plant Live!”

Some cities feature sports arenas and stadiums as a major draw, and the food offerings go beyond hotdogs, peanuts and Cracker Jack. St. Louis’s “Ballpark Village” promises, according to its website, a “buzzing, sports-themed district close to Busch Stadium with restaurants, bars and nightlife venues”; Baltimore’s Inner Harbor, which is walking distance to Oriole Park at Camden Yards, features a science center, aquarium and historic warships moored at the dock, as well as a complex of bars, eateries and music venues in a repurposed electric-power station known as “Power Plant Live!”

Beyond Main Street, restaurant closures are part of the collateral damage in suburbia as pandemic-wary people work and shop from home. “As I go around from town-to-town on Long Island and shoot out to the malls, I can see business closings everywhere,” says Ray Keating, chief economist at the Small Business & Entrepreneurship Council, a Washington-based trade group claiming 100,000 members. “When one business shutters, it affects other businesses. There’s a ripple effect.”

Adds Sink of the restaurant association: “Restaurants are often located with the anchor store inside malls. You never find any kind of mall without some sort of food court.”

When a restaurant closes its doors, it has a knock-on effect as well, sending shockwaves coursing up and down the supply chain. Prior to the pandemic, Sink reports, the industry generated $2.5 trillion in economic activity and supported 21 million jobs. Cutbacks in food service hurts “everything from butchers and farmers and distillers to the Cisco and Aramark food companies that depend on restaurants.

“It will reach farther back into the economy,” she adds, causing economic pain to such disparate businesses as cleaning companies, local plumbers, handymen, and maintenance workers. Even “technology companies that provide systems (for restaurants) to run a credit card or make reservations or keep track of service orders” are affected.

Andrew Volk, owner of the Portland Hunt & Alpine Club, a restaurant and bar with the reputation for offering possibly the tastiest cocktails in Maine, says that keeping his business going hasn’t been easy. The establishment was forced into lockdown in March and “stayed dark until Memorial Day,” he says, when it got the green light from the state to sell food and cocktails to go. On July 4, the restaurant went to outdoor seating, which it maintained until New Year’s Eve, adding heaters and umbrellas in the autumn to fend off Maine’s frigid temperatures.

Volk reckons that his restaurant’s sales were off by roughly 55 percent in 2020 over the previous year. Fully 95% of revenues go to pay expenses, including rent and utilities and employees’ wages. And the rest of the money scarcely lands in the cash register before it’s passed on to his vendors.

But as he has cut back operations, all of his vendors are feeling the pinch as well. There are no longer twice-weekly deliveries from the local package store from which, by state law, Volk is required to purchase hard liquor. His beer purchases –- craft beer prepared by Rising Tide Brewery and Oxbow Brewery, both of Portland, as well as Miller, Budweiser and Narraganset, the popular Rhode Island-made brew – are no longer so robust. Volk has also reduced his procurement of French and South African wines from importers.

Purchases of farm-to-table produce from Stonecipher Farms, Dandelion Springs, and Snell Farms, which came to a halt last March, remain diminished. The daily deliveries from Baldor Specialty Foods, a New York-based food supplier of, among myriad foodstuffs, out-of-season vegetables and citrus fruit, are less frequent.

Purchases of farm-to-table produce from Stonecipher Farms, Dandelion Springs, and Snell Farms, which came to a halt last March, remain diminished. The daily deliveries from Baldor Specialty Foods, a New York-based food supplier of, among myriad foodstuffs, out-of-season vegetables and citrus fruit, are less frequent.

Volk is still offering fresh cooked fish for take-out, including cod, trout, halibut, hake and shrimp (but not cold-water Maine lobster). Even so, he’s ordering less seafood from Browne Trading Market. He has also cut back on specialty soft cheeses he buys from several local dairy farms, including Larkin’s Gorge and Fuzzy Udder.

Other vendors affected include Portland Paper Products, which supplies him with paper goods such as toilet paper and paper towels, cleaning supplies and chemicals for the dishwasher. One bright spot for the paper products supplier: it is meeting Volk’s increased demand for take-out boxes, paper napkins and plastic utensils.

Meanwhile, Volk is not looking as much to Pratt Abbott Cleaners for freshly laundered linens such as tablecloths, napkins, and kitchen shirts. Capone Griding Company in Boston, which sharpens kitchen knives and cutlery, isn’t making as many pickups and deliveries these days.

Ian Jerolmack, owner-operator of 10-acre Stonecipher Farms in Bowdoinham, Maine, is one of Volk’s food suppliers. He has been providing fresh, farm-to-table produce to several dozen restaurants in Portland, plus a couple “up the coast,” he says, since he began tilling the Maine soil a decade ago. Now the grower of organic fruit and vegetables – a garden of delights that includes tomatoes, carrots, beets, onions, cabbage, turnips, squash, sweet potatoes, and fennel – has been feeling the economic hardship along with the restaurants.

By year-end 2020, Jerolmack says, he is down to only 15 restaurants as customers, a two-thirds attrition from his 45 customers prior to the pandemic. “Our farm was sort of unique in that it almost exclusively sold to restaurants,” he says. “They’re all in various degrees of agony,” he adds, “and I don’t know how the dust will settle. It’s been super-bizarre.”

By year-end 2020, Jerolmack says, he is down to only 15 restaurants as customers, a two-thirds attrition from his 45 customers prior to the pandemic. “Our farm was sort of unique in that it almost exclusively sold to restaurants,” he says. “They’re all in various degrees of agony,” he adds, “and I don’t know how the dust will settle. It’s been super-bizarre.”

When the restaurants went into lockdown last March, Jerolmack was faced with zero demand for his produce, and his livelihood was in jeopardy. At the same time, he was forced to reckon how much seed to plant. “There’s only one window in which to plant seeds,” he explains.

He had to decide whether to take on fulltime seasonal workers, which is not a simple proposition. In order to plant, tend and harvest his crops, he’d need to hire and house four Mexican workers under the federal government’s H-2A visa program. By law, he says, he was required to guarantee the foreign workers payment of 75% of their wages for eight months of employment. “I felt as if I were drowning,” he says. “It was a heavy weight.”

He opted to hire the H-2A workers and forged ahead with the planting, albeit at reduced acreage, consoling himself with the farmer’s ancient adage: “People always need to eat.”

With restaurants closed, his only recourse would be to sell directly to consumers. Yet Jerolmack had no online presence and was pretty much frozen out of the local farmers markets. So he turned to local restaurants and arranged to sell produce to their top customers. “I threw together a ‘farmer’s choice,’” he says, “a mixed bag of chard, carrots, onions, and beets – or whatever vegetables were in season and charged $25 a bag.”

Right away, he was able to sign up 175 customers paying $100 apiece for four weeks of produce, enough of a cushion for him to sell his “storage crops” and stay in business. Individual customers were grateful to buy the fresh organic food and avoid grocery stores, he says, the arrangement worked out for the restaurants. “They got increased foot traffic and helped their takeout business. Everybody loved it.”

By being creatively entrepreneurial and employing several direct-to-consumer sales strategies, he was able to chalk up revenues of $300,000 in 2020. That’s a hefty, 35% drop compared with the $440,000 in 2019 gross receipts. But Jerolmack says he kept five fulltime workers employed, he’s got a new consumer trade, and he’s getting ready for the 2021 planting season.

Thomas McQuillan, vice-president for strategy, culture and sustainability at wholesale food distributor Baldor, says that in a given year his Bronx-based company – with major operations centers in Boston and Washington, D.C. – delivers high-quality food to 10,000 restaurants from Portland, Me. to Richmond, Va. The wholesaler also supplies food in bulk to corporate dining rooms and cafeterias, hotels, institutions like hospitals and schools, and sports stadiums.

Baldor buys its produce from 1,000 regional farms, both big and small, and trucks in out-of-season produce from the West Coast. A visit to the company’s website discloses a vast cornucopia of edibles and victuals for sale. A few clicks discloses a gastronomic wonderland of fruits and vegetables, organics and cold cuts, meat and poultry and seafood, specialty and grocery items, dairy and cheese, bakery and pastry, and wine.

When the pandemic hit and restaurants went on lockdown, Baldor’s business plummeted by 85%, McQuillan reports, and the company reacted in much the same way as the Maine farmer. “With Covid-19,” says McQuillan, “all industries in the food business were affected. But we knew that the same number of people in our geographic area would be looking for food and we pivoted to a business-to-consumer platform and began shipping directly to people at home.

“We also knew many corporate types were no longer working in offices and, early on in the pandemic, people were fearful of going to grocery stores,” he adds, “and we began deliveries to apartment buildings all over New York. It’s not that different from delivering to a restaurant.”

According to a New York Times story, the company required a $250 minimum for consumer purchases and delivered 6,000 items within a 50-mile radius of New York City. McQuillan told AltFinanceDaily it pressed its 400-truck fleet of “sprinter vans to tractor trailers” into service for the residential deliveries. The consumer business and limited restaurant re-openings allowed Baldor “to rebound, but nowhere near pre-Covid levels,” he says. By year-end 2020, the company had furloughed 20% of its workforce.

Fresh fish is for sale on the fishmonger, outdoor seafood market.[/caption]The seafood industry was among the hardest hit by the pandemic’s throttling back the restaurant industry, says Ben Martens, executive director of the Maine Coast Fishermen’s Association. Seafood is much less likely than poultry or meat to be prepared at home or ordered for takeout. Groundfish like flaky cod, haddock, pollack, hake and flounder, he explains, are especially popular dishes in high-end restaurants in New York, Boston and Chicago.

Fresh fish is for sale on the fishmonger, outdoor seafood market.[/caption]The seafood industry was among the hardest hit by the pandemic’s throttling back the restaurant industry, says Ben Martens, executive director of the Maine Coast Fishermen’s Association. Seafood is much less likely than poultry or meat to be prepared at home or ordered for takeout. Groundfish like flaky cod, haddock, pollack, hake and flounder, he explains, are especially popular dishes in high-end restaurants in New York, Boston and Chicago.

“Seafood is a celebratory food,” Martens says. “It’s a food people embrace when things feel good. It’s covered in butter and people eat it outside when they’re with family and friends.”

Early data, he says, showed a 70% decline in “landings revenue” at the non-profit Portland Fish Exchange Auction, the major marketplace connecting fishermen with wholesalers and processors. Some fishermen and lobstermen have had some success selling directly to consumers by switching over to scallops and other seafood popular with Mainers who, Martens asserts, are somewhat more inclined to prepare seafood at home than people in other states.

But what has really given the industry a boost, he says, has been an anti-hunger program run by his trade association. Seeded with $200,000 from an anonymous donor, and bolstered with $200,000 received through the CARES Act passed by Congress last year, the program purchases seafood at a fair price and funnels it to food pantries. “Maine is the most food-insecure state in the country,” Martens says. “and high quality protein is hard for a lot of people to find.”

The program contributed enough fish portions to contribute to 180,000 meals in 2020, while helping soften economic damage to fishermen. “Now we’re seeing some stabilization with outside restaurant seating,” Martens says.

Sam Cantor, who is vice-president for sales at Gotham Seafood, a New York broker doing an estimated $16 million in sales, according to Buzzfile, sounded glum and subdued in a telephone interview with AltFinanceDaily. He reports that the company delivers salmon, tuna, lobster, King Crab legs, red snapper and other seafood directly to eateries in Manhattan as well as the tri-state region of New York, Connecticut and New Jersey.

The last year has been a burden. “A ton of places are closed — cafeterias, cafes, hotels,” he says. “People are not going to the Berkshires or the Hamptons, offices are closing. In the beginning of the pandemic when (New York Governor Andrew) Cuomo shut down indoor dining it was brutal. And it’s still a difficult situation.”

Describing layoffs at the company as “significant,” Cantor says it’s also been emotionally draining to see the misfortune that has befallen restaurant workers. “It’s been a hard thing to witness,” he says. “A lot of our relationships are with chefs and they have families.”

Gotham has had some success selling directly to consumers by revamping its website and putting money into advertising on the online platforms Facebook and Instagram, he says, but “we’re not back to 100%.”

Cantor also says he is concerned that the country’s commercial infrastructure is at risk of fracturing. “It’s more than just losing your favorite restaurant or what happens to the individual fisherman and farmer,” he says. “It takes a very intricate supply chain for you to get your favorite fish. There’s a lot of work that goes into it.

“I hope my kids don’t have through something like this,” he went on. “The home delivery has been a shining light. But we want travel and tourism to come back. We want people going back to The Garden to watch the Knicks. I’m hoping there will be a renaissance, and this is just the start of the Roaring Twenties.”