Gold Rush: Merchant Cash Advances Are Still Hot

August 18, 2019

Last year, when Kevin Frederick struck out on his own to form his own catering company in Annapolis, the veteran caterer knew that he’d need a food trailer for his business to succeed.

He reckoned that he had a good case for a $50,000 small-business loan. The Annapolis-based entrepreneur boasted stellar personal credit, $30,000 in the bank, and a track record that included 35 years of experience in his chosen profession. More impressively, his newly minted company—Chesapeake Celebrations Catering—was on a trajectory to haul in $350,000 in revenues over just eight months of operations in 2018. And, after paying himself a salary, he cleared $60,000 in pre-tax profit.

But Frederick’s business-credit profile was so thin that no bank or business funder would talk to him. So woeful was his lack of business credit, Frederick reports, that his only financing option was paying a broker a $2,000 finder’s fee for a high-interest loan.

Luckily, he says, everything changed when he discovered Nav, an online, credit-data aggregator and financial matchmaker.

Based in Utah, Nav had him spiff up his business credit with Dun & Bradstreet, a top rating agency and a Nav business partner. This was accomplished with a bankcard issued to Frederick’s business by megabank J.P. Morgan Chase. Soon afterward, he says, Nav steered him to Kapitus (formerly Strategic Funding Source), a New York-based lender and merchant cash advance firm that provided some $23,000 in funding.

“They led me in the right direction,” Frederick says of Nav. “A lady there (at Nav) helped me with my credit, warning me that the credit card I’d been using had an effect on my personal credit. Then she led me to Kapitus, all probably within a week.”

Now, Frederick has his food trailer. He reports that its total cost—$14,000 for the trailer, which came “with a concession window, mill-finished walls, and flooring” plus $43,000 in renovations—amounted to $57,000. Equipped with a full kitchen—including refrigeration, sinks, ovens, and a stove—the food trailer can be towed to weddings, reunions, and the myriad parties he caters in the Delmarva Peninsula. In addition, Frederick can also park the trailer at fairgrounds and serve seafood, barbeque, and other viands to the lucrative festival market.

Now, Frederick has his food trailer. He reports that its total cost—$14,000 for the trailer, which came “with a concession window, mill-finished walls, and flooring” plus $43,000 in renovations—amounted to $57,000. Equipped with a full kitchen—including refrigeration, sinks, ovens, and a stove—the food trailer can be towed to weddings, reunions, and the myriad parties he caters in the Delmarva Peninsula. In addition, Frederick can also park the trailer at fairgrounds and serve seafood, barbeque, and other viands to the lucrative festival market.

Meanwhile, the caterer’s funders are happy to have him as their new customer. The people at Kapitus, to whom he is making daily payments (not counting weekends and holidays), are especially grateful. “Nav provides a valuable service,” says Seth Broman, vice-president of business development at Kapitus. “They know how to turn coal into diamonds,”

Nav does not charge small businesses for its services. As it gathers data from credit reporting services with which it has partnerships—Experian, TransUnion, Dun and Bradstreet, Equifax—and employs additional metrics, such as cashflow gleaned from an entrepreneur’s bank accounts, Nav earns fees from credit card issuers, lenders and MCA firms.

The company has close ties to financial technology companies that include Kabbage and OnDeck, and also collaborates with MCA funders such as National Funding, Rapid Finance, FundBox, and Kapitus. “We give lenders and funders better-qualified merchants at a lower cost of client acquisition,” says Caton Hanson, Nav’s general counsel and co-founder, adding: “They don’t have to spend as much money on leads.”

As banks have increasingly shunned small-business lending in the decade since the financial crisis, and as the economy has snapped back with a prolonged recovery, alternative funders—particularly unlicensed companies offering lightly regulated, high-cost merchant cash advances (MCAs)—have been piling into the business.

And service companies like Nav—which is funded by nearly $100 million in venture capital and which reports aiding more than 500,000 small businesses since it was founded in 2012—are thriving alongside the booming alternative-funding industry.

Over the past five years, the MCA industry’s financings have been growing by 20% annually, according to 2016 projections by Bryant Park Capital, a Manhattan-based, boutique investment bank. BPC’s specialty finance division handles mergers and acquisitions as well as debt-and-equity capital raising across multiple industries and is one of the few Wall Street firms with an MCA-industry practice. By BPC’s estimates, the MCA industry will have more than doubled its small business funding to $19.2 billion by year- end 2019, up from $8.6 billion in 2014.

Bankrolled by a broad assortment of hedge funds, private equity firms, family offices, and assorted multimillionaire and billionaire investors on the qui vive for outsized returns on their liquid assets, the MCA industry promises a 20%-80% profit rate, reports David Roitblat, president of Better Accounting Solutions, a New York accountancy specializing in the MCA industry. Based on doing the books for some 30 MCA firms, Roitblat reports that the range in profit margins depends on the terms of contracts and a funder’s underwriting skills.

The numerical size and growth of the MCA industry is hard to ascertain, reports Sean Murray, editor of AltFinanceDaily (this publication), which tracks trends in the industry and sponsors several major conferences. “So much is anecdotal,” Murray says.

Even so, the evidence that MCA companies are proliferating—and prospering—is undeniable. Over the past two years, AltFinanceDaily’s events, which experience substantial attendance from the MCA industry, have consistently sold out, requiring the events to be moved to larger venues. In Miami, attendance in January this year topped 400-plus attendees, Murray reports, roughly double the crowd that packed the Gale Hotel in 2018.

Similarly, the May, 2019, Broker Fair in New York at the Roosevelt Hotel drew more than 700 participants compared with the sellout crowd of roughly 400 last year in Brooklyn. (Despite ample notice that this year’s Broker Fair at the Roosevelt was sold out and advance tickets were required, as many as 40-50 latecomers sought entry and, unfortunately, had to be turned away.)

The upsurge of capital and the swelling number of entrants into the MCA business has all the earmarks of a gold rush. “Everybody and his brother is trying to get a piece of the action,” asserts Roitblat, the New York accountant.

And there are two ways to hit paydirt in a gold rush. One way is to prospect for gold. But another way is to sell picks and shovels, tents, food, and supplies to the prospectors. “If you can find a way to service the gold rush, you can make a lot of money,” says Kathryn Rudie Harrigan, a management professor and business-strategy expert at the Columbia University Graduate School of Business. “It’s like profiteering in wartime.”

And there are two ways to hit paydirt in a gold rush. One way is to prospect for gold. But another way is to sell picks and shovels, tents, food, and supplies to the prospectors. “If you can find a way to service the gold rush, you can make a lot of money,” says Kathryn Rudie Harrigan, a management professor and business-strategy expert at the Columbia University Graduate School of Business. “It’s like profiteering in wartime.”

As Professor Harrigan suggests, cashing in on the gold rush by servicing it has parallels across multiple industries. Consider the case of Charles River Laboratories, which has capitalized on the rapid development of the biotechnology industry over the past few decades.

As scientists searched for biologics to battle diseases like cancer and AIDS, the Boston-area company began producing experimental animals known as “transgenic mice.” Informally known as “smart mice,” Charles River’s test animals are specially designed to carry human genes, aiding investigators in their understanding of gene function and genetic responses to diseases and therapeutic interventions. (The smart mouse’s antibodies can also be harvested. “Seven out of the eleven monoclonal antibody drugs approved by the Food and Drug Administration between 2006 and 2011,” according to biotechnology.com, “were derived from transgenic mice.”)

In the MCA version of the gold rush, a bevy of law and accounting firms, debt-collection agencies and credit-approval firms, among other service providers, have either sprung to life to undergird the new breed of alternative funder or added expertise to suit the industry’s wants and needs. (This cohort has been joined, moreover, by a superstructure of Washington, D.C.-based trade associations and lobbyists that have been growing like expansion teams in a professional sports league. But their story will have to wait for another day.)

Rather than being exploitative, supporting companies serve as a vital mainstay in an industry’s ecosystem, notes Alfred Watkins, a former World Bank economist and Washington, D.C.-based consultant: “A gold miner can’t mine,” he says, “unless he has a tent and a pickaxe.”

And in the high-risk, high-reward MCA industry, which can have significant default rates depending on the risk model, many funders can’t fund if they don’t have reliable debt collection. Many of the bigger companies, says Paul Boxer, who works on the funding side of the industry, have the capability of collecting on their own. But for many others—particularly the smaller players in the industry—it’s necessary to hire an outside firm.

One of the more widely known collectors for the MCA industry is Kearns, Brinen & Monaghan where Mark LeFevre is president and chief executive. The Dover (Del.)- based firm, LeFevre says, first added MCA funders to its client roster in 2012; but it has only been since 2014 that “business really took off.”

LeFevre won’t say just how many MCA firms have contracted with him, but he estimates that his firm has scaled up its staff 35%-40% over the past five years to meet the additional MCA workload. The industry, LeFevre adds, “is one of the top-growth industries I’ve seen in the 36 years that I’ve been in business.”

He also says, “People in the MCA industry know a lot about where to put money, but collections are not one of their strong points. They need to get a professional. It gives them the free time to make more money while we go in behind them and collect.”

If repeated dunning fails to elicit a satisfactory response, KBM has several collection strategies that strengthen its hand. The big three, LeFevre says, are “negotiation, identifying assets, and litigation.” He adds: “We have a huge database of attorneys who do nothing but file suit on commercial debt internationally. Then we can enforce a judgment. You don’t want someone who just makes a few phone calls.”

Because business has become so competitive, LeFevre says, he won’t discuss his fee schedule. As to KBM’s success rate, he says no tidy figure is available either, but asserts: “Our checks sent to our clients are more than most agencies because of our proprietary collection process.”

Jordan Fein, chief executive at Greenbox Capital in Miami and a KBM client told AltFinanceDaily: “We work with them. They’re organized and communicate well and they know to collect. They’re on the expensive side, though. I’ve got other agencies that I use that are cheaper.”

Debt-collection firm Merel Corp, a spinoff from the Tamir Law Group in New York, might be a lower-cost alternative. Formed in just the past 18 months to service the growing MCA industry, Merel typically takes 15%-25% of whatever “obligation” it can collect, says Levi Ainsworth, co-chief operating officer.

A successful collection, Ainsworth asserts, really begins with the underwriting process and attention to detail by the funders. “Instead of coming in at the end,” he says, “we try to prevent problems at the start of the process.”

For an MCA firm dealing with an excessive number of defaults, Merel sometimes places one of its employees with the funder to handle “pre-defaults,” for which it charges a lower fee. The collections firm has also built a reputation for not relying on a “confession of judgment.” Now that COJs have been outlawed for out-of-state collections in New York State, Merel’s skills could be more in demand.

Better Accounting Solutions, which has its offices on Wall Street, is another service-provider promising to lighten the workload of MCA firms by providing back-office support. The company is headed by Roitblat, a 36-year- old former rabbinical student turned tax-and-accounting entrepreneur. Since he founded the company with two part-time employees in 2011, it’s ballooned to some 70 employees.

Roitblat does not have all of his firm’s eggs in one MCA basket. His firm handles tax, accounting and bookkeeping work for law firms, the fashion industry, restaurants and architectural firms. Even so, he says, thirty MCA clients— or more than half his clientele—rely on the firm’s expertise, three of whom were just added in June. His best month was January, 2018, when six funders contracted for his services. “Growth in the MCA industry has been explosive,” he says.

MCA accounting work has its own vagaries and oddities. For example, because of the industry’s high default rate, Roitblat notes, a 10%-slice of every merchant’s payment is funneled into a “default reserve account.” And when an actual default occurs, credits are moved from the receivables account to the default reserve account.

Roitblat takes pride that his firm’s MCA work has passed audits from respected accounting firms like Friedman, Cohen, Taubman and Marcum LLP. Moreover, he has helped clients uncover internal fraud and, in one instance, spotted costly flaws in a business model. An early MCA client, Roitblat says, had no idea that “he was losing close to $100,000 a month by spending on Google ads.”

Better Accounting also keeps its rates low. The firm typically assigns a junior accountant to handle clients’ accounts while a senior manager oversees his or her work. “He (Roitblat) does a fantastic job,” says David Lax, managing partner of Orange Advance, a Lakewood (N.J.)-based MCA firm. “They understand the MCA business. And even if your business is small, they can set up the infrastructure and do the work more economically and efficiently than you can. You’d have to create the position of comptroller or senior-level accountant,” Lax adds, “to equal their work.”

Top-notch competence and low rates, Lax says, are not the only reasons he often refers Roitblat’s firm to fellow MCA companies. “The only thing better than their work,” he says, “is the people themselves.”

Whether it’s oil and gas, banking and real estate, construction, health care or high-technology—you name it—lawyers have an important role across nearly every industry. So too with the MCA industry where, as has been shown, there is an especially high demand for attorneys skilled at winning debt-collection cases.

To hear Greenbox’s Fein tell it, a skilled lawyer handling debt collection can write his or her own ticket. A talented attorney, he says, not only retrieves lost money and prevents losses, but enables the funder to “offer the product cheaper than the competition.

“We use a ton of attorneys in 35 states in the U.S. and in Canada,” Fein adds, “and you have no idea how many attorneys we go through until we find a good one.”

Until recently, much of the MCA industry’s success has resulted from a hands-off, laissez faire legal and regulatory environment—particularly the legal interpretation that a merchant cash advance is not a loan. The industry has also benefited from the fact that most credit regulation focused on consumer credit and not on business and commercial financings.

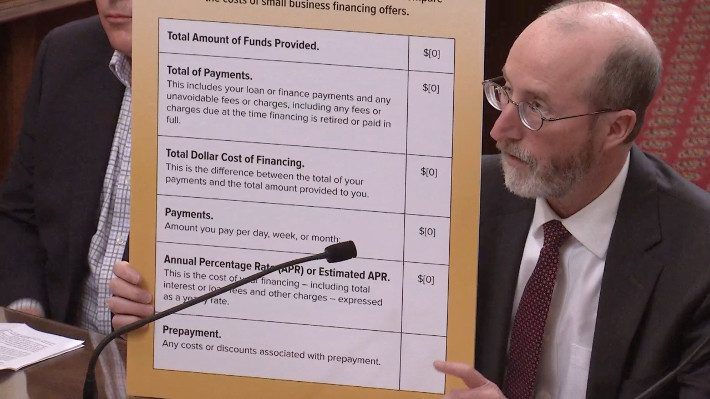

But now, as the MCA industry is maturing and showing up on the radar screens of state legislatures, Congress, regulatory agencies, and the courts, there is heightening demand for legal counsel. In just the past 12 months, California passed a truth-in-lending statute requiring MCA firms not only to clearly state their terms, but to translate the short-term funding costs of MCAs into an annual percentage rate. The state of New York, as has been noted, passed legislation restricting the use of COJs.

Moreover, notes Mark Dabertin, special counsel at Pepper Hamilton, a top national law firm based in Philadelphia, the state of New Jersey is contemplating licensing MCA practitioners. The Minnesota Court of Appeals recently determined in Anderson v. Koch that, because of a “call provision” in a funding contract, a merchant cash advance was actually a loan.

And, Dabertin warns, the Federal Trade Commission, which has the authority to treat a merchant cash advance as a consumer transaction—replete with the full panoply of consumer disclosures and protections—is training its gunsights on the industry. “On May 23,” Dabertin reports in a memo to clients, “the FTC launched an investigation into potentially unfair or deceptive practices in the small business financing industry, including by merchant cash advance providers.”

These pressures from government and the courts will only make doing business more costly and drive up the industry’s barriers to entry. Failing to stay legal, moreover, could not only result in punitive court judgments, but render an MCA firm vulnerable to legal action by their investors.

“It’s inevitable that the industry will evolve,” Dabertin says, and firms in the industry will have to self-police. “They will need to hire counsel and a compliance staff,” he adds. “You can’t just do it by the seat of your pants.”

Funding Circle Originated $377M of US Loans in First Two Quarters of 2019

August 8, 2019Funding Circle originated $377M of loans in the US in the first six months of 2019, according to their latest public report. The company said that “growth was proactively controlled” and that they tightened higher risk band lending and increased prices. They’ve now loaned more than $2B cumulatively in the US since inception and their growth is being led by “new borrowers” that are being lured away from traditional lenders.

Funding Circle still lags behind PayPal, OnDeck, Kabbage, Square Capital, and Amazon in the US in loan origination volume, according to the AltFinanceDaily small business finance rankings. Its closest competitors by volume are BlueVine, National Funding, and Kapitus.

California DBO Making Progress On Finalizing Rules Required By The New Disclosure Law

July 29, 2019 Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

The DBO then issued a public invitation to comment on how that format should work. They got 34 responses. Among them were Affirm, ApplePie Capital, Electronic Transactions Association, Commercial Finance Coalition, Fora Financial, Equipment Leasing and Finance Association, Innovative Lending Platform Association, International Factoring Association, Kapitus, OnDeck, PayPal, Rapid Finance, Small Business Finance Association, and Square Capital.

On Friday, the DBO published a draft of its rules along with a public invitation to comment further. The 32-page draft can be downloaded here. The opportunity to comment on this version of the rules ends on Sept 9th.

You can review the comments that companies submitted previously here.

Merchant Relationship Status: It’s Complicated

May 14, 2019

Brokers will often say that building strong relationships with their merchants is critical to their success. John Celifarco, Managing Partner at Horizon Financial Group, a five person ISO in Brooklyn, said that the advantage they have over larger competitors is the relationships they’ve developed with their merchants. Celifarco’s office is even in a streetfront store, where a number of their merchants are actually neighboring stores. Celifarco sees this as a strength.

But Michael Bernier, Vice President of 1 West Finance, a 14-person brokerage based in New York, said that things have changed as competition has increased in the space.

Customers gravitate towards companies that can provide them with not only the best pricing, but also the best user experience, which is why we believe so many new players in the space have achieved scale so quickly.

While customer relationships are important, funders in the space that are improving their speed, efficiency, and pricing are going to win the deals.

“In general, if [end users] find a better price on Amazon, 9 times out of 10 they’re going to buy that product on Amazon, regardless of the sales person on the phone” Bernier said.

Bernier suggests that rate or speed may win the customer but another more legally-binding circumstance may guide the relationship accordingly.

Kapitus CEO Andy Reiser served as moderator.

“Contractually, we own the customer,” said National Funding CEO Dave Gilbert on a panel at Broker Fair. “But we work in conjunction with the broker.”

Fellow panelist and Chairman of Rapid Finance, Jeremy Brown, said that he used to say what Gilbert said, but now says: “We own the loan. [And] we have the right to first renew the customer.”

Brokers seeking a very cozy relationship with their clients should therefore consider what rights and responsibilities are afforded to them under their referral contracts so that there’s no confusion with actions taken by either party with the customer down the road.

“I get close to people very quickly, it’s just who I am,” Kemp, a broker, told AltFinanceDaily in an interview last year. “And in my opinion it works to my advantage because I have merchants that renew with me multiple times a year. And I know that no matter how many calls they get [from other brokers], they’re going to turn to me. I know that they trust me.”

Likewise, Chad Otar, CEO of Excel Capital in New York, has said that building trust with merchants is very important and is what leads to renewal business. Otar introduced one of his merchants, a marketing company, to his other clients. A few of them ended up working with the marketing company, which was a win for everyone and led to even stronger word of mouth from Otar’s merchants.

“I don’t think anyone owns the customer,” said CEO of BFS Capital Mark Ruddock on the panel alongside Gilbert and Brown. “Customers are a privilege, not a right.”

Broker Fair 2019 Makes Major Splash in the Heart of Manhattan

May 10, 2019

If a tiny ray of light were created from every conversation about small business financing, then the Roosevelt Hotel in midtown Manhattan would have been tantamount to the sun on May 6th. It was the site of AltFinanceDaily’s 2nd annual Broker Fair and the grand old lobby was abuzz with brokers, funders and vendors from across the industry. And it wasn’t only the lobby. The hallways and ball rooms and bathrooms were filled with people in jackets or dresses with colorful conference badges hanging from their necks. You could not open your eyes without seeing a Broker Fair attendee.

The day kicked off with an address to the crowd by AltFinanceDaily’s founder and president Sean Murray.

He spoke to a packed audience in one of the hotel ballrooms that was actually the site of a famous scene in the 1987 movie, “Wall Street,” starring Charlie Sheen and Michael Douglas. It was in this scene where one of the most well-known lines, “Greed is good,” was delivered in a speech by the character Gordon Gekko, a ruthless businessman played by Michael Douglas.

He spoke to a packed audience in one of the hotel ballrooms that was actually the site of a famous scene in the 1987 movie, “Wall Street,” starring Charlie Sheen and Michael Douglas. It was in this scene where one of the most well-known lines, “Greed is good,” was delivered in a speech by the character Gordon Gekko, a ruthless businessman played by Michael Douglas.

In Murray’s speech, he acknowledged the classic financial thriller, but gave it a twist.

“Funding small business is good,” Murray said. “It’s not greed that’s good. Aligned interests are good.”

This very room was a marriage of old and new. The 1924 room with soaring ceilings and crystal chandeliers was packed with mostly young faces in a still relatively new industry. The stage was simple, the chairs sleek, and colored strobe lights circled the ceiling in what created a fresh energy.

The first panel of the day, called “The Great Debate,” was dominated by discussion of technology among the CEOs of some of the largest companies in the small business funding industry: National Funding, Rapid Finance, BFS Capital, and Kapitus.

“Technology is an inevitability and a powerful way for brokers to stay relevant,” BFS CEO Mark Ruddock told AltFinanceDaily. “The question is, ‘Does that preclude the small [brokers] who don’t have the money to invest in technology?’”

He sees great opportunity for software platforms that can connect an individual broker to lenders, similar to how Shopify connects small mom and pop retailers to a wider consumer audience.

One of the other CEOs on the panel said he was bullish on digitally savvy brokers and all of them seemed to agree that brokers should offer more products.

“Having a broader set of products benefits brokers because they become the go-to person for merchants rather than simply serve a transactional function,” Chairman of RapidAdvance Jeremy Brown told AltFinanceDaily.

For brokers looking to expand their product offerings, there was a well-attended session called “Commissions with Factoring and Leasing” that was led by factoring and leasing professionals, Phil Dushey and Edward Kaye, respectively.

Meanwhile, the co-founders of the successful brokerage Everlasting Capital, led a session called “How to Scale Your Broker Shop” which included advice on everything from hiring to customer acquisition and social media marketing. One of the founders, Josh Feinberg, had his marketing person follow him around with a video camera throughout the day.

There were also sessions on regulations affecting the industry, plus a session called “Operating with Integrity: Why Ethics Matter.”

“The speakers are very relevant,” said Dexter Bataille, a broker at Pivotal Funding in Florida who attended Broker Fair. “And the panels are really good too.”

“AltFinanceDaily always finds ways to make the shows more professional,” said Senior Sales Leader at Reliant Funding Nicolas Marr, who flew in from California to attend the conference. “The details really count.”

In another hotel ballroom, Broker Fair attendees meandered around high tables where event sponsors had representatives talking about their products and handing out free t-shirts and pens. As the day wound down and Broker Fair’s “networking happy hour” approached its end at 6 p.m., the figurative sun (created by small business finance conversations) began to set at the Roosevelt Hotel. But a crowd of about 100 lingered at the hotel bar, buzzing away, eager to make just a few more connections.

The small business financing sun will rise again on July 25 at deBank’s next event, AltFinanceDaily CONNECT in Toronto. Tickets are already available.

Amazon Now Among The Top Online Small Business Lenders in The United States

May 8, 2019

Amazon has joined PayPal, OnDeck, Kabbage, and Square as being among the largest online small business lenders. On Tuesday, Amazon revealed that it had made more than $1 billion in small business loans to US-based merchants in 2018. Amazon says the capital is used to build inventory and support their Amazon stores.

By selling on Amazon, “SMBs do not need to invest in a physical store or the costs of customer discovery, acquisition, and driving customer traffic to their branded websites,” the company says. Small and medium-sized businesses selling in Amazon’s stores now account for 58 percent of Amazon’s sales. More than 200,000 SMBs exceeded $100,000 in sales on Amazon in 2018 and more than 25,000 surpassed $1 million.

You can view the full report they published here.

| Company Name | 2018 Originations | 2017 | 2016 | 2015 | 2014 | |

| PayPal | $4,000,000,000* | $750,000,000* | ||||

| OnDeck | $2,484,000,000 | $2,114,663,000 | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 | |

| Kabbage | $2,000,000,000 | $1,500,000,000 | $1,220,000,000 | $900,000,000 | $350,000,000 | |

| Square Capital | $1,600,000,000 | $1,177,000,000 | $798,000,000 | $400,000,000 | $100,000,000 | |

| Amazon | $1,000,000,000 | |||||

| Funding Circle (USA only) | $792,000,000 | $514,000,000 | $281,000,000 | |||

| BlueVine | $500,000,000* | $200,000,000* | ||||

| National Funding | $494,000,000 | $427,000,000 | $350,000,000 | $293,000,000 | ||

| Kapitus | $393,000,000 | $375,000,000 | $375,000,000 | $280,000,000 | ||

| BFS Capital | $300,000,000 | $300,000,000 | $300,000,000 | |||

| RapidFinance | $260,000,000 | $280,000,000 | $195,000,000 | |||

| Credibly | $290,000,000 | $180,000,000 | $150,000,000 | $95,000,000 | $55,000,000 | |

| Shopify | $277,100,000 | $140,000,000 | ||||

| Forward Financing | $210,000,000 | $125,000,000 | ||||

| IOU Financial | $125,000,000 | $91,300,000 | $107,600,000 | $146,400,000 | $100,000,000 | |

| Yalber | $65,000,000 |

FTC Forum on Small Business Financing & Merchant Cash Advances

May 7, 2019At the FTC Forum on Small Business Financing & Merchant Cash Advances this morning, FTC regulators asked questions of a panel of industry representatives about controversial topics, including the use of COJs. Below are some closely paraphrased responses.

On Confessions of Judgment (COJs)

Scott Crocket, Founder & CEO, Everest Business Funding

The role of COJs is a conversation worth having. What’s the right balance?

We choose only to use them for deals of $100,000 or more. And COJs apply for only 3% of our business. So if there was a ban on COJs, it wouldn’t really affect us. It might just limit the amount we would fund.

The Bloomberg stories are not representative of what we do. We don’t file a COJ when a business is slowing down, but only when we suspect fraud.

Jared Weitz, CEO, United Capital Source

90% to 95% of our deals do not include COJs. And for those where we do use COJs, we give merchants a document that has a description of what it is so that they’re comfortable with it. We tell them that they have to be comfortable with it before they take it.

Jesse Carlson, Senior Vice President & General Counsel, Kapitus

After we saw the extent of the use of confessions of judgement by certain individuals/companies, as a trade association, we at the Small Business Finance Association (SBFA) decided to include in our code of conduct a ban on the use of confessions of judgement if you’re a member of the SBFA.

Part of the reason why we do include COJs is because we’re very careful with our underwriting.

On True-ups

Jesse Carlson

We have 5 to 10 employees who speak with merchants when they are having unforeseen financial challenges and we’ll adjust their ACH repayment. Some companies treat the percentage of the company’s sales as an absolute. We’ll offer them modifications.

Scott Crocket

We remind merchants that the true-up is available.

Ami Kassar, Founder & CEO, Multifunding LLC

Many funders are not as forgiving as these funders say they are.

Kate Fisher, Partner, Hudson Cook

Some MCA funders reached out to merchants affected by the hurricane in Texas and the forest fires in California to adjust their payments.

Jared Weitz

Other funders stopped requesting payments altogether from merchants who were affected by these natural disasters.

Brokers / Aggressive Marketing

Jared Weitz

A broker of an MCA deal has to give the commission back if the merchant fails within 90 days.

Jesse Carlson

We work with about 100 brokers/ISOs at a given time and we do background checks on them.

Scott Crocket

We do background checks on brokers and we monitor their behavior. We don’t hesitate to cut off a relationship with an ISO. We do spot checks, but we don’t monitor every ISO every day.

The Federal Trade Commission hosted a forum on small business financing including loans and merchant cash advances to examine trends and consumer protection issues in this marketplace.

The forum began at 8:30am and concluded at 1pm. Among some familiar names that spoke are:

- Jared Weitz, CEO, United Capital Source

- Scott Crockett, Founder & CEO, Everest Business Funding

- Christian Spradley, Head of Policy & Senior General Associate Counsel, OnDeck

- Kate Fisher, Partner, Hudson Cook

- Ami Kassar, Founder & CEO, Multifunding LLC

- Jesse Carlson, Senior Vice President & General Counsel, Kapitus

- Sam Taussig, Head of Global Policy, Kabbage

- Lewis Goodwin, Banking Lead, Square Capital

Has PayPal Eclipsed OnDeck in Small Business Loans?

April 26, 2019

It’s been said that Kabbage is on pace to surpass OnDeck in small business loan originations, but PayPal has already done it.

When PayPal announced a working capital program in the Fall of 2013, few were predicting that the initiative would propel them to the top of the small business lending charts. Just two years later, however, the payment processing giant had already loaned more than $1 billion to small businesses.

Today, that number is over $10 billion, according to a comment made by PayPal CEO Dan Schulman on the company’s Q1 earnings call.

That figure would suggest that they had loaned approximately $9 billion from Fall 2015 to the end of Q1 2019. OnDeck, by comparison, loaned $7.5 billion since Fall 2015 through Q4 2018. Several other data sources, including previous statements from PayPal that they had surpassed more than a billion dollars in quarterly small business funding in 2018 (already more than OnDeck), indicate that PayPal has become #1 on the AltFinanceDaily small business funding leaderboard.

PayPal’s growth was helped in part by its acquisition of Swift Capital in 2017.

Two of the top four are payment processors:

| Company Name | 2018 Originations | 2017 | 2016 | 2015 | 2014 | |

| PayPal | $4,000,000,000* | $750,000,000* | ||||

| OnDeck | $2,484,000,000 | $2,114,663,000 | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 | |

| Kabbage | $2,000,000,000 | $1,500,000,000 | $1,220,000,000 | $900,000,000 | $350,000,000 | |

| Square Capital | $1,600,000,000 | $1,177,000,000 | $798,000,000 | $400,000,000 | $100,000,000 | |

| Funding Circle (USA only) | $500,000,000 | |||||

| BlueVine | $500,000,000* | $200,000,000* | ||||

| National Funding | $427,000,000 | $350,000,000 | $293,000,000 | |||

| Kapitus | $393,000,000 | $375,000,000 | $375,000,000 | $280,000,000 | ||

| BFS Capital | $300,000,000 | $300,000,000 | ||||

| RapidFinance | $260,000,000 | $280,000,000 | $195,000,000 | |||

| Credibly | $180,000,000 | $150,000,000 | $95,000,000 | $55,000,000 | ||

| Shopify | $277,100,000 | $140,000,000 | ||||

| Forward Financing | $125,000,000 | |||||

| IOU Financial | $91,300,000 | $107,600,000 | $146,400,000 | $100,000,000 | ||

| Yalber | $65,000,000 |

*Asterisks signify that the figure is the editor’s estimate