Shopify’s Funding Automation Key to Its Growth

May 2, 2018![]() Canadian e-commerce company Shopify (NYSE:SHOP) has a business funding arm called Shopify Capital that issued $60.4 million in merchant cash advances in Q1 this year, according to the company’s earnings report yesterday.

Canadian e-commerce company Shopify (NYSE:SHOP) has a business funding arm called Shopify Capital that issued $60.4 million in merchant cash advances in Q1 this year, according to the company’s earnings report yesterday.

The funding operation offers an MCA product exclusively to merchants that are customers of Shopify. The company helps small business owners create online stores, with products ranging from web design to marketing and analytics. Currently, Shopify supports more than 600,000 small businesses worldwide.

Shopify Capital was launched in April 2016, but a company representative said it wasn’t until April 2017 that it started using algorithms 100 percent to automate offers of capital to merchants.

“What Shopify can see is a lot of patterns in a merchant’s [online] store,” a company spokesperson told AltFinanceDaily. “How engaged is that merchant? What has their GMV (Gross Merchant Volume) been? How spotty is their GMV? How often do they sell? There’s a bunch of different factors that help us predict GMV going forward. And as [our] algorithm gets better and smarter, we are able to get more granular in our offers.”

Many of Shopify Capital’s small business owner clients are new business owners who would not qualify for loans from banks, but need money to expand their businesses.

“Business owners typically spend copious hours putting an application together and funds typically take two to three weeks to receive,” a different Shopify spokesperson said. “Shopify Capital is designed to provide our merchants with timely access to Capital without putting them through additional financial stress…[And] merchants receive financing based on our predictive technology to determine what makes sense for their business in their trajectory.”

Shopify was founded in 2004 and is headquartered in Ottawa, Canada.

Tech Banks: Will Fintech Dethrone Traditional Banking?

August 20, 2017On Halloween, 2014, a largely unknown, Boston-based financial institution, First Trade Union Bank, embraced high-technology, went paperless, and officially adopted a new name: Radius Bank.

In reinventing itself, Radius did more than dump its dowdy moniker. It shuttered five of its six branches, re-staffed its operations with a tech-savvy team, instituted “anytime/anywhere” banking services, and offered customers free access to cash via a nationwide ATM network. And it teamed up with a fistful of financial technology companies to offer an impressive array of online lending and investment products.

In reinventing itself, Radius did more than dump its dowdy moniker. It shuttered five of its six branches, re-staffed its operations with a tech-savvy team, instituted “anytime/anywhere” banking services, and offered customers free access to cash via a nationwide ATM network. And it teamed up with a fistful of financial technology companies to offer an impressive array of online lending and investment products.

Today, the bank’s management boasts that, using their personal mobile phones, some 2,700 people per week are opening up checking accounts, funneling $3 million in consumer deposits into the bank’s virtual vault. That’s a stark contrast from a decade ago when the financial institution was being rocked by the financial crisis and “we couldn’t get anybody to walk into our branches,” says Radius’s chief executive, Mike Butler.

“We tried to leave that old bank behind,” he says. “We’re a virtual retail bank now, an efficiently run organization that offers high levels of customer service and Amazon-like solutions.”

Radius Bank is not alone. At a moment when there is much discussion — and hand-wringing — over the future of seemingly outmoded, highly regulated community banks, a coterie of small but nimble banks is exploiting technology and punching above its weight. Almost overnight, this cohort is combining the skill and hard-won experience of veteran bankers with the lightning-fast, extraordinary power afforded by the Internet and technological advances. As a result, these small and modest-sized institutions are redefining how banking is done.

In addition to Radius Bank, independent banks winning recognition for their bold, innovative – and profitable — exploitation of technology, include: Live Oak Bank in Wilmington, N.C., which adroitly parlays technology to become the No. 2 lender to business and agricultural borrowers backed by the U.S. Small Business Administration; Darien Rowayton Bank in Darien, Conn., which is making a name for itself with coast-to-coast, online refinancing of student loans; and Cross River Bank in Fort Lee, N.J., which does back-end work for a passel of fintech marketplace lenders.

Interestingly, there’s not much overlap. Each of the banks goes its own way. But what all the banks have in common is that each has struck out on its own, each hitting upon a technological formula for success, each experiencing superior growth.

“These are companies that understand the value of a bank charter,” says Charles Wendel, president of Financial Institutions Consulting in Miami. “They have to work under the watchful eyes of state and federal regulators. But their cost of funds is low and they can offer more attractive rates. Because they’re less likely (than nonbank fintechs) to disappear, run out of money, or get sold,” the bank expert adds, “they also have the image of stability with customers.”

These modest-sized banks are emerging as not only pacesetters for the banking industry. Along with making common cause with the fintechs — which had promised to disrupt the banking industry – they’re even beating the fintechs at their own game.

“Classically, community banks have looked to technology partners to provide technological innovation,” says Cary Whaley, first vice-president for payment and technology policy at the Independent Community Bankers of America, a Washington, D.C.-based trade group representing a broad swath of the country’s 5,800 Main Street banks. “They still do. You’re seeing more partnerships. But now you also see community banks building innovative products and services outside of that relationship. You see forward-thinking banks developing their own technology to support big ideas like marketplace lending, distributed ledger technology, and emerging payments technology.”

With its extraordinary skill at exploiting technology, Live Oak Bank – which trades on the Nasdaq and is the only public company encountered in the cohort — has become a Wall Street darling. “While several banks have adopted an online-only model, and nearly all banks are shifting more and more delivery through online channels, Live Oak was built from the ground up as a technology-based bank,” Aaron Deer, a San Francisco-based research analyst at Sandler O’Neill Partners, wrote in a recent investment note.

Driving the success of Live Oak, which operates out of a single branch in the North Carolina seacoast town and has only been in business for a decade, is the explosive growth in its SBA lending, the bank’s “core strategy,” Deer notes. Last year, Live Oak lent out $709.5 million in SBA loans in increments of up to $5 million, the federal agency reports, making it the country’s No. 2 SBA lender. It trailed only megabank Wells Fargo Bank, the third largest bank in the U.S. with $1.5 trillion in assets, which made $838.93 million in SBA-backed loans last year.

As its SBA lending has taken off, Live Oak, which qualifies as a “preferred lender” with the federal agency, boasts assets that have nearly tripled to $1.4 billion in 2016, up from $567 million two years earlier. Those are flabbergastingly fantastic growth numbers. But just as incongruously — by nipping at the heels of Wells Fargo — Live Oak has been challenging a bank more than a thousand times its asset size for dominance in SBA lending.

And, interestingly, the bank is able to book those outsized amounts of SBA loans while lending to only 15 industries out of 1,100 approved by the government agency, slightly more than 1% of the universe. That’s up from 13 industries in 2015, and Live Oak is adding two to four additional industries yearly for its SBA loan portfolio, Deer reports. Included among the industries to which the bank made an average SBA loan of $1.29 million last year: Agriculture and poultry, family entertainment, funeral services, medical and dental, self-storage, veterinary, and wine and craft-beverage.

The bank has a team of financing specialists dedicated to each of the designated industries. Among Live Oak’s current SBA borrowers are Martin Self Storage in Summerville, S.C.; Utah Turkey Farms in Circleville, Utah; Pinballz Arcade, Austin, Tex.; and Council Brewery Company in San Diego. Steve Smits, chief credit officer at the bank, told NerdWallet: “When you specialize in something, you become efficient. Because we do it every day and we have professionals and specialists, we tend to be more responsive and quicker.”

The heady combination of technological sophistication and banking expertise has allowed the lender to slash its loan-origination time to 45 days, about half the three-month industry average for SBA loans. To speed up loan sourcing and generation, the bank developed its own in-house technology, which led to the formation of the Wilmington-based technology company nCino, which was spun off to shareholders in 2014.

Live Oak did not return calls to discuss its lending strategies, but in SEC filings bank management declared: “The technology-based platform that is pivotal to our success is dependent on the use of the nCino bank operating system” which relies on Force.com’s cloud-computing infrastructure platform, a product of Salesforce.com.

Natalia Moose, a public relations manager at nCino told AltFinanceDaily in an e-mail interview: “We work with Live Oak Bank, in addition to more than 150 other financial institutions in multiple countries with assets ranging from $200 million to $2 trillion, including nine of the top 30 U.S. banks. nCino was started by bankers at Live Oak Bank who found the logistics of shuffling paperwork among loan stakeholders to be unwieldy, inefficient and time-consuming.

“nCino’s bank operating system,” Moose adds, “leverages the power and security of the Salesforce platform to deliver an end-to-end banking solution. The bank operating system empowers bank employees and leaders with true insight into the bank, combining CRM (customer relationship management), deposit account opening, loan origination, workflow, enterprise content management, digital engagement portal, and instant, real-time reporting on a single secure, cloud-based platform.”

Live Oak, meanwhile, is not resting on its technological laurels. According to Deer’s report, the bank’s parent company, Live Oak Bancshares, has formed a subsidiary to inject venture capital into fintech companies. It’s already taken a small equity stake in Payrails and Finxact, “the latter of which is developing a completely new core processor to compete against the old legacy systems used by most banks,” the Sandler O’Neill analyst writes. “Quite simply,” he asserts elsewhere in his report, “the company is far beyond any other bank we cover in its technical capabilities and the growth outlook remains outstanding.”

Five hundred and thirty-three miles due north along the Atlantic coast in southeastern Connecticut, Darien Rowayton Bank is also experiencing tremendous success as a lender using a home-grown technology platform. State-chartered by the Connecticut Department of Banking and regulated as well by the Federal Deposit Insurance Corp., the $600 million-asset bank is winning attention in banking circles for its online student-loan refinancing.

Five hundred and thirty-three miles due north along the Atlantic coast in southeastern Connecticut, Darien Rowayton Bank is also experiencing tremendous success as a lender using a home-grown technology platform. State-chartered by the Connecticut Department of Banking and regulated as well by the Federal Deposit Insurance Corp., the $600 million-asset bank is winning attention in banking circles for its online student-loan refinancing.

A few years ago, DRB, as it is known, was looking to go beyond mortgage and commercial lending — “the bread and butter for most community banks,” bank president Robert Kettenmann explained to AltFinanceDaily in a telephone interview – and was somewhat at a loss. The bank considered but then rejected the credit card business. Finally, DRB struck paydirt refinancing student loans. “Our chairman really seized on the opportunity,” Kettenmann says, adding: “It’s a $35 billion market.”

Thanks to the National Bank Act, it’s able to operate in all 50 states. As a regulated commercial bank with a strong deposit base, DRB can also offer low rates well below any state’s usury prohibitions.

What is most striking about DRB’s program is its nationwide targeting of upwardly mobile, affluent young professionals. According to a PowerPoint presentation obtained by AltFinanceDaily, all of the bank’s super-prime borrowers, who are mainly in the 28-34 age bracket, have a college degree and a whopping 93% have graduate degrees. Average income is $194,000.

Forty-eight percent of those refinancing student loans with DRB are doctors or dentists and another 22 percent are pharmacists, nurses or medical employees; only about 20% are paying off their law degrees or MBAs. The heavy concentration of refinancing in the medical field reduces economic risk in an economic downturn. Forty-three percent of the borrowers are home-owners, the rest are renters – and prime candidates for an online, DRB-financed mortgage.

Forty-eight percent of those refinancing student loans with DRB are doctors or dentists and another 22 percent are pharmacists, nurses or medical employees; only about 20% are paying off their law degrees or MBAs. The heavy concentration of refinancing in the medical field reduces economic risk in an economic downturn. Forty-three percent of the borrowers are home-owners, the rest are renters – and prime candidates for an online, DRB-financed mortgage.

(Once known as “yuppies” today this cohort is “known by the acronym ‘HENRY,’” remarks Cornelius Hurley, a Boston University banking professor and executive director of the Online Lending Institute, explaining the initials stand for “High Earners Not Rich Yet.”)

The Connecticut bank partnered with a third-party on-line vendor, Campus Door, when it commenced making student loans in 2013. In the fall of 2016, however, DRB built out its own, proprietary loan-origination system, Kettenmann reports, emphasizing that CampusDoor had been an excellent partner but that the bank wanted to exercise end-to-end control over the process. DRB employs a seven-pronged, “omni-channel” marketing approach that includes interactive marketing, affinity partnerships, digital/online advertising, direct mail, mass-media advertising, and public relations/brand awareness campaigns.

DRB’s online enrollment provides “pre-approved rates” in less than two minutes with final approval on rates in 24-48 hours. Refinancers can complete the online application at their own speed. Through May, 2017, DRB had made $2.48 billion in refinancing to 20,000 student-loan borrowers, with only ten defaults, five of which were attributed to deaths or “terminal illness.”

On Yelp! the bank has received a batch of reviews ranging from very favorable, five-star (“I had a truly wonderful experience”) to one-star (“awful” and “truly a nightmare”). Many fault the application process as laborious, describing it as “time-consuming.” But for those who have succeeded, like the reviewer who counseled “patience,” the result can be “the lowest rate with DRB…my loan payments went down $100 a month.”

![]() Just about an hour’s drive south and taking its name from its proximity to New York city just over the George Washington Bridge is New Jersey-based, state-chartered Cross River Bank, which has a reputation as a partner-in-arms to fintech companies. “We’re both users and producers of technology,” declares Gilles Gade, the bank’s chief executive.

Just about an hour’s drive south and taking its name from its proximity to New York city just over the George Washington Bridge is New Jersey-based, state-chartered Cross River Bank, which has a reputation as a partner-in-arms to fintech companies. “We’re both users and producers of technology,” declares Gilles Gade, the bank’s chief executive.

The bank provides “back-end” and infrastructure support to 17 marketplace lenders that offer a suite of lending products including personal loans, mortgages and home-equity loans. Following loan origination by a fintech company – Marlette Funding, Affirm, Upstart, loanDepot, SoFi, and Quicken Loan, among other partners — Cross River does the actual underwriting. Last year, Gade reports, the bank underwrote 1.9 million loans valued at $4-4.5 billion, about 10% of which Cross River kept on its books. The bulk of the loans are sold “back to the marketplace lenders” or to a third party. “We’ve created a high-velocity automated system,” he says.

Gade is manifestly unapologetic about the bank’s role in assisting fintechs in their competition with the banking establishment. “We’re a banking infrastructure services provider for those who want to disrupt the banking system,” he says. “Consumers expect a lot better than they’ve been getting from traditional banking services.”

Back in Boston, Radius Bank’s chief executive reports that forging partnerships with fintechs to provide the full panoply of online banking services was no easy proposition. In its mating ritual, Radius not only had to determine that a fintech company’s offerings were sound and that it had the right characteristics – most especially “a long-term, sustainable business model” – but that its corporate culture meshed comfortably with Radius’s.

Back in Boston, Radius Bank’s chief executive reports that forging partnerships with fintechs to provide the full panoply of online banking services was no easy proposition. In its mating ritual, Radius not only had to determine that a fintech company’s offerings were sound and that it had the right characteristics – most especially “a long-term, sustainable business model” – but that its corporate culture meshed comfortably with Radius’s.

After meeting with as many as 500 fintechs and after a fair amount of trial and error, Radius formed partnerships with LevelUp, which enables customers to make mobile payments; with online lender Prosper, for refinancing consumer debt and “credit rehabilitation”; with SmarterBucks, for refinancing student loans; and with online investment firm Aspiration Partners – which allows investors to name their own fees and markets itself to a predominately middle-class audience as the firm “with a conscience.”

Radius employs advertising on social media websites and employs “psychographics” to appeal to “anyone who is zealous about using technology, not necessarily millennials,” Butler says. The data show that 65% of adults in the U.S. would prefer to use a traditional bank and have face-to-face interactions with a teller, he notes, leaving the remaining 35% as Radius’s target audience.

Christopher Tremont, executive vice-president for virtual banking, told AltFinanceDaily that a typical Radius customer is 42 years old, lives in Boston, New York, Chicago “or one of the bigger cities in the West,” is a “technophile,” earns $75,000 a year, and has $100,000 in personal assets.

Radius’s performance since it went paperless has been stellar. The bank has seen a rapid rise in deposits, spurting to $782 million through the first quarter of 2017, up from $565 million at year-end 2014. With little fee income but ample deposits and low-cost funds, Radius realizes the bulk of its revenues – and profits — on the interest-rate spread generated from its loan portfolio.

The bank booked $43.5 million in SBA loans last year, ranking it in the top 50 banks on the SBA’s league tables, while carrying another $105 million in its commercial leasing business at the end of the first quarter this year. Loan generation is driving asset growth, which are currently at $973 billion, up more a third from $726 million in 2014, and Butler expects the bank’s assets to top $1 billion sometime this year.

“Community banks love that part of the business—lending money,” Butler says.

The Tesla of Alternative Lending

May 16, 2017 Tesla has autopilot. Apple has Siri. And Upstart has its own high-tech software model that places the startup in a category of its own for online lending. All three of these companies may be very different but what they have in common is a reliance on artificial intelligence and machine learning for their proprietary technology.

Tesla has autopilot. Apple has Siri. And Upstart has its own high-tech software model that places the startup in a category of its own for online lending. All three of these companies may be very different but what they have in common is a reliance on artificial intelligence and machine learning for their proprietary technology.

“You hear so much about how Tesla cars will drive themselves, how Google or Amazon home assistants talk to you to as if you’re human. In lending we are the first company to apply these types of technologies to lending,” Dave Girouard, Upstart co-founder and CEO told AltFinanceDaily.

So what is machine learning exactly, particularly as it relates to finance? One of the main components that goes into machine learning is not looking at the same data everybody else does. “We are known for looking beyond FICO and the credit report. We look at who the employer is, what industry you work in, where you went to college, what you studied, several hundred variables affect how we price credit,” he said.

Upstart, a direct-to-consumer lending platform, uses artificial intelligence and machine learning for everything from verifying a potential borrower’s identity, to making a credit decision, to pricing credit. Today 25 percent of the company’s loans are 100% automated.

“This is a radical departure from the industry,” said Girouard. “It’s a function of being able to build more automation to verify information about the borrower.”

Indeed the differences between machine learning and traditional credit models is kind of like comparing a self-driving vehicle to walking.

“The whole term machine learning implies that software gets smarter and better on its own with no human intervention. Every day thousands of repayments are made to Upstart along with delinquencies, and defaults. As this happens the software is adjusting its pricing on the next loan, learning in real time every day,” Girouard said, without even the slightest concern of tipping his hand.

“We have a several year head start and a data science team that are math and statistics PhDs. These are the types of people hired by Google or Tesla or Amazon. Traditional consumer credit doesn’t tend to have machine learning skills,” he added.

Nevertheless his vision for artificial intelligence and machine learning in the lending community is far greater than as it applies to Upstart alone. “We think virtually all flavors of lending will depend on AI/ML within 10 years. We’re at the very early stages, but it’s hard to imagine a successful lender anywhere who doesn’t use similar technology over time,” Girouard said.

Inside Upstart

Upstart is a hybrid lender that funds 20% of loans from their balance sheet. Two months ago they began licensing software as a service (SaaS). The software is managed by Upstart but it appears on the partner’s website. “A bank could use our technology to originate loans,” said Girouard, adding that the company is in conversations with two-to-three dozen banks about future partnerships.

The machine learning approach seems to lend itself to favoring certain demographics. In the case of Upstart, this happens to be millennials, evidenced by the lender’s average customer age of 28, almost all of whom have college degrees.

“Obviously we understood early that the millennial generation doesn’t have 20 years of credit history and they have a hard time getting loans. It struck us, tell me you wouldn’t give a loan to a 25 year old just because they have a thin credit file? It doesn’t make sense. What if they studied at Stanford and work at Google? There is more to be known about an individual than a FICO score,” said Girouard.

Perhaps the greatest evidence of whether or not Upstart’s approach is working is to catch a glimpse of the company’s balance sheet. Upstart expects to reach the $1 billion milestone for loan originations in calendar 2017. And perhaps even more telling is they anticipate being profitable by the summer. “An IPO for us would be a couple of years out,” Girouard said.

That timing could be perfect, particularly considering Wall Street’s apparent love/hate relationship with some players in the alternative lending space.

“People tend to paint the whole industry with one brush and it’s not a very pretty brush at the moment. But soon they will begin to appreciate there is a significant difference between these companies. Upstart really does have a very differentiated and unique product,” said Girouard.

Re-Banked

April 23, 2017

Just a few years ago, the financial services community was fixing for a battle of David and Goliath proportions—with scrappy, upstart online lenders threatening to rise up and vanquish the fearful and mighty brick and mortar banks. Instead, the unexpected happened: a number of well-respected online lenders and banks set aside their battle arms and began looking for ways to collaborate with their rivals—offloading loans, making referral agreements and establishing more formal partnerships, for example.

“In the real world, sometimes David wins. Sometimes Goliath wins. Just as plausibly, sometimes both sides carve up a market and they often have different offerings that target unique customers,” says Brayden McCarthy, vice president of strategy at Fundera, a New York-based marketplace for small business lending that works with a variety of lenders, including traditional banks.

Certainly, the change didn’t happen overnight. But over time, both online lenders and banks have been forced to tailor their expectations more closely to market realities. Despite their fast growth trajectory, several online lenders have come to realize that they lack several things many banks have, namely a strong, time-tested brand, a solid customer base and ample capital. Banks, meanwhile, have realized that their slow start out of the gate with respect to technology is a severe competitive disadvantage, and that they need more nimble, savvy partners to stay in the game.

Given these shifts, more and more online lenders and banks are taking the approach that if you can’t beat ‘em, join ‘em. Although some industry leaders are actively pursuing strategies that put them in direct competition with banks, partnerships of varying degrees between traditional banks and alternative players are increasingly common. As a result, the lines separating the two are getting increasingly blurry.

“Market forces are acting as a shotgun at the wedding. Whether the two sides are entirely comfortable with the marriage is irrelevant, they need one another,” says Patricia Hewitt, chief executive of PG Research & Advisory Services LLC in Savannah, Georgia. “They’re stronger together than they are alone.”

The evolution of Square is a prime example. The San Francisco-based company really packed a punch in the merchant services world with its mobile card reader designed for small businesses. From there, the payments company sought additional ways to diversify, eventually turning to merchant cash advance as a way to help small business customers obtain funds quickly. Then, in March of last year, Square moved into online lending, teaming up with Celtic Bank of Utah to offer small business loans online. The partnership got off to a running start. In its most recent earnings report, Square said it facilitated 40,000 business loans totaling $248 million in the fourth quarter of 2016—up 68 percent year over year—while maintaining loan default rates at roughly 4 percent.

Even SoFi, the San Francisco-based online lender that has been pointedly outspoken in its anti-bank rhetoric, now has bank-like aspirations. In February, the lender acquired mobile banking startup Zenbanx, giving it the ability to offer checking accounts and credit cards in 2017. Also in February, SoFi teamed up with Promontory Interfinancial Network to enable community banks to purchase super-prime student loans originated by the online lender. Large banks have been buying SoFi loans for several years.

COLLABORATION IS THE WAVE OF THE FUTURE

Many see collaboration between banks and online lenders as a logical step in the industry’s evolution. Online disrupters have forever changed the face of lending—in the same way that online brokerage shaped the financial advisor industry, according to Bill Ullman, chief commercial officer of Orchard Platform.

“There’s a tendency to want to view things as either black or white, online lenders vs. banks. The reality is that the entire financial services industry is undergoing a transformation with technology as the core driver,” he says. “I am of the view that both traditional financial services companies and fintech players can survive and thrive,” Ullman says.

For its part, Orchard recently inked a deal with Sandler O’Neill that provides access to the Orchard platform for the investment bank and brokerage firm’s bank and specialty finance clients. The deal is expected to help small banks better evaluate their options with respect to online lending opportunities.

Partnerships between online lenders and banks take many forms. Some of them are behind the scenes, where marketplaces sell loans to banks or banks informally refer customers. Others are more public. For example, in September 2015, Prosper and Radius Bank of Boston teamed up to offer personal loans to certain customers through the bank’s website using the Prosper platform. Customers can borrow from $2,000 to $35,000 in this manner.

Then in December 2015, JPMorgan Chase and OnDeck joined forces in order to dramatically speed up the process of providing loans to some of the banking giant’s small business customers. In April 2016, Regions Bank and Avant announced a partnership to better serve customers who don’t meet Regions’ credit criteria.

Avant’s customers typically have a credit score between 600 and 700, while Regions sets the bar higher. “The benefit for banks is that they do not need to worry about a platform taking away customers that meet their own credit criteria,” according to Carolyn Blackman Gasbarra, head of public relation at Avant.

She notes that Avant expects to replicate this model with more banks in 2017. “Lately many platforms and banks have come to realize their counterparts are more friend than foe,” she says.

Given the changing tides, industry watchers expect to see more relationships develop between online lenders and banks over time. These could include referral agreements, technology licensing arrangements, formalized revenue-sharing partnerships and perhaps even outright acquisitions.

PARTNERSHIP ADVANTAGES

Certainly, working together can be mutually beneficial for both online lenders and banks. For new online lenders and other fintech players, partnering with an established bank allows them to bypass significant regulatory and compliance hurdles because the necessary requirements are already in place.

“Why jump through all the hoops when you can just have a buddy system with an existing lender?” says Kerri Moriarty, head of company development at Cinch Financial, a Boston-based company dedicated to helping people make smarter investment decisions.

Fintechs that license their technology to banks still have to meet the high standards of third-party vendors determined by bank regulators, notes Stan Orszula, co-head of the fintech team at the Chicago law firm Barack Ferrazzano Kirschbaum & Nagelberg LLP.

“But it’s still less onerous than being a direct lender,” says Orszula, who works closely with banks and fintech providers on legal, regulatory and corporate issues. “They are learning that they need banks. They really do.”

Even seasoned online lenders that have a regulatory framework in place can benefit from bank relationships by using banks’ established brands as leverage. “Everyone knows Chase, Bank of America and American Express,” says McCarthy of Fundera. “They have a solid name and a solid in-built customer base to be able to offer product to them,” he says.

Teaming up with a bank gives added credibility to an online lender, at a time when the public’s confidence has faltered due to highly publicized troubles at certain firms. “Partnering has a very important signaling effect that these online players are here to stay,” McCarthy says.

Banks, meanwhile, need the nimbleness and innovation that online lenders provide. “Banks realize they have to catch up with the fintech disrupters,” says Mark E. Curry, president and chief executive of SOL Partners, which provides strategic management and information technology consulting services to financial services companies.

DIFFERENT TYPES OF PARTNERSHIP OPPORTUNITIES ABOUND

When it comes to partnerships between banks and online players, there are numerous options. In the small business lending space, for example, McCarthy of Fundera says he expects banks to continue buying loans from online lenders, as they have been for many years. He also expects more banks will route declined applicants to online lenders or online loan brokers. “This is a partnership that will allow them to make up some incremental revenue by referring business,” he says.

In addition, McCarthy says he expects banks to make products available through online marketplaces and use an online lender’s technology for online loan applications. He also expects banks will use online lenders’ technology for underwriting and servicing loans.

Years ago, before John Donovan joined Bizfi, he recalls talking to a salesman for a large national bank. The bank didn’t offer a lending product that he could give to small businesses and the salesman was losing customers as a result. “That’s where we see a lot of those opportunities,” says Donovan, chief executive of the online marketplace for small business loans.

For instance in March 2016, Bizfi partnered with Western Independent Bankers, a trade association, for over about 600 community and regional banks, to link small business clients to financing options through Bizfi. Many banks don’t offer small business loans below $150,000, whereas the average loan Bizfi does is $40,000, Donovan says, adding that the company would like to develop additional relationships similar to its agreement with Western Independent Bankers.

In the future, he predicts fintechs will continue to be more receptive to the idea of working with banks and vice versa, as the industry digests the impact of deals that are still in their early days.

FINDING STRATEGIC GROWTH OPPORTUNITIES

As banks and online lenders become increasingly accustomed to working together, there may be more opportunities for strategic acquisitions. For instance, Sandeep Kumar, managing director of Synechron, a global consulting and technology firm, expects to see banks—especially mid-tier players that don’t have the resources to innovate like big banks buying lending-related start-ups. He says banks will likely be most interested in companies that can help them with AI and other techniques to pinpoint where they should spend more efforts on cross-selling and customer profiling, for example. “There are many start-ups in this area that have very compelling technology,” he says.

On the other hand, Chris Skinner, an independent commentator at The Finanser Ltd., a research and consulting firm in London, points out that the two cultures don’t always mesh. “Quite a few startups have young, entrepreneurial founders that would loath the idea being acquired by a bank. So it really depends on the circumstances,” he says.

Valuation differences between large banks and leading online lenders may also be a sticking point for some deals, Ullman of Orchard points out. Banks’ concern over their valuation “will place a certain amount of restraint and discipline on the tech M&A activities they pursue,” he says.

ANTICIPATING TROUBLE IN PARADISE

While increased collaboration between online lenders and banks sounds good on the surface, John Zepecki, group head of product management for lending at D+H in San Francisco, urges both sides to proceed with caution. “You have to find an arrangement where you don’t have conflict,” he says. “If your innovation partner also is a competitor, it’s a challenge. If you have an inherent conflict, it doesn’t get better over time.”

That’s one reason why companies like Chicago-based Akouba have come on the scene. In Akouba’s case, its goal is to provide banks with the technology such that they don’t have to partner with an online lender that has the potential to compete for business. “We don’t compete with the bank in any way whatsoever,” says Chris Rentner, the company’s founder and chief executive.

Akouba’s business lending platform—which the American Bankers Association endorsed in February—provides banks with leading edge technology that integrates the bank’s own unique credit policies into a convenient, online process—from application to documentation— all the way to closing and funding. The bank uses its own credit policies, originates its own loans and owns the entire brand and customer relationship.

Rentner says he started the business with the idea in mind that the online lending model wouldn’t be sustainable long-term and that working alongside banks—as opposed to competing head to head— was the direction to go. “The idea that they could somehow get all of the consumers out of the banking world and onto their platforms was never going to happen. That’s why we exist today,” he says.

Managing Risk in Small Business Lending

March 16, 2017 Two years ago, I left a promising career at PayPal, a major technology giant, for what some considered a risky move: I joined BlueVine, a young fintech startup. My title: vice president of risk.

Two years ago, I left a promising career at PayPal, a major technology giant, for what some considered a risky move: I joined BlueVine, a young fintech startup. My title: vice president of risk.

This year, I took on an even bigger role when I was named chief risk officer of the Silicon Valley company, which offers working capital financing to small and medium-sized businesses.

My promotion comes at a time when risk is becoming a bigger concern in fintech, which is ushering in big changes in banking and financial services.

Fintech revolutionizes financial services

Data science technology has dramatically improved access to financing and the way we manage our money. The fintech wave that began with my former company, PayPal, and the world of payments, has spread to other aspects of personal finance, from mortgages to student and auto loans to investing.

This expansion was accompanied by growing concern that the fintech boom is fraught with risks that, if left unchecked, could lead to a major bust in the financial services industry that could in turn cause harm to the broader economy.

In a speech in January, Mark Carney, the governor of the Bank of England, cited the need to “ensure that fintech develops in a way that maximises the opportunities and minimises the risks for society.” “After all, the history of financial innovation is littered with examples that led to early booms, growing unintended consequences, and eventual busts,” he said.

Risk management as key to success

Risk management certainly has been a focus area for BlueVine from the beginning.

BlueVine joined the revolution in small business financing in 2014 when it rolled out an innovative online invoice factoring platform.

Factoring is a 4,000-year old financing system that allows small businesses to get advances on their unpaid invoices by providing easy, convenient access to working capital. BlueVine transformed what had been a slow, clunky, paper-based solution into a flexible and convenient online financing system that enables entrepreneurs to plug cash flow gaps that often hamper business growth.

Because the BlueVine platform is based on cutting-edge data science technology that can process and analyze information to make quick funding decisions, managing risk inevitably became a major challenge in building our business. As Eyal Lifshiftz, our founder and CEO, recalled in a recent column, in BlueVine’s first month of operation, almost every other borrower defaulted.

In fact, that was partly the reason Eyal invited me to join his team. BlueVine serves small and medium-sized businesses seeking substantial working capital financing of up to $2 million. To succeed, we needed to build a robust data and risk infrastructure.

Small startup with big data needs

Joining BlueVine also posed a personal challenge.

At PayPal, where I started as a fraud analyst and then moved into the company’s data science division where I helped develop behavior-based risk models, I had enormous amounts of data to work with to do my job. Now, I was joining a young startup with very limited data history, but with big data needs.

This meant putting together exceptional and experienced teams of data scientists and underwriters and developing a technology that becomes progressively more precise and accurate as it draw lessons from our steadily expanding data and underwriting decisions. It was important for us to have a group of super smart, highly-motivated and technologically-strong people working closely with a team of experienced and sharp underwriters.

Here’s how the process works: Our underwriters develop a robust methodology which is then translated into detailed logic decision trees.

Each decision tree includes dozens, even hundreds of branches, made up of question sets on different underwriting situations.

For example, a decision tree could focus on approving new clients coming from a specific industry, such as transportation or construction, or on increasing the credit line for a client with a specific financial profile.

A typical decision tree would drill down on further financial questions: What’s the expected cash-flow of the business in three to six months? What’s the pace at which it has accumulated debt over the past year? Are the business sales seasonal in a material way?

The questions could also focus on non-financial areas: Does the company’s website look professional? How does it compare with major companies in its industry? Does the business actively maintain its Facebook and Twitter accounts?

The goal is to build a risk infrastructure that steadily becomes more efficient in answering questions in an automated, large-scale and highly accurate manner. Our data scientists leverage multiple external data sources and use dynamic advanced machine learning models to answer these questions pretty much in real-time and with a high degree of accuracy.

So it’s a combination of technology and human input. There will always be gray areas, questions and situations that cannot immediately be addressed by our computer models.

But as the models get better and more robust, the gray areas will shrink. Our models are constantly and automatically enhanced, re-trained and expanded by the most recent data and input from our underwriters.

Think of it as the fintech version of Deep Blue and AlphaGo, the powerful computer programs that famously outplayed topnotch chess grandmasters. Both programs were based on similar principles: the more they played, the more knowledge they absorbed and the more formidable they became at chess.

Technology and teamwork

An even better example is the self-driving car powered by Google’s artificial intelligence technology. Human input is still required, but the more driving the car does, the smarter and more autonomous it becomes.

Building our risk infrastructure is an ongoing process for BlueVine. But it already has helped us steadily expand our reach, making us stronger, smarter and even faster in financing small and medium-sized businesses.

In just a couple of years, the strides we’ve made in managing risk more effectively enabled us to increase our credit lines to $2 million for invoice factoring and $100,000 for business lines of credit, which means we’ve been able to serve bigger businesses with bigger financing needs.

While we initially focused mainly on small businesses with annual revenue of under $250,000, today we have an increasing number of clients with annual sales of more than $1 million and increasingly, we’ve been able to serve clients with revenue of more than $10 million a year.

By the end of 2016, BlueVine had funded roughly $200 million. We’re on track to fund half a billion dollars by the end of this year.

We’ve accomplished this in a time of heightened skepticism about fintech in general and alternative business lending in particular. But rather than scoff at this skepticism, I’d point out two things.

First, fear often accompanies the rise of a new technology. Second, in the wake of the 2009 financial crisis, it’s prudent to raise hard questions about the rapid emergence of new financial technologies.

While building technologies and companies that can provide financial services faster and easier is a laudable goal, It’s wise to move cautiously and with humility.

The BlueVine experience underscores this.

Risk is still a challenge we take on every day. But we have found ways to take it on confidently and effectively with a vigorous combination of technology and teamwork.

Ido Lustig is Chief Risk Officer of BlueVine.

Merchant Cash Advance Accounting Q&A

May 25, 2016

As a successful and knowledgeable Merchant Cash Advance accountant I often receive questions from MCA business owners and syndicators. In the last tax season, my accounting firm recognized that many of the questions we receive are distinctly similar. In the following article I address the most common questions my accounting office receives.

Question #1: When I am accounting for my Merchant Cash Advance company isn’t a cash advance accounted for in the same way as a loan? It looks the same on a spreadsheet so isn’t the interest calculated in the same way as a normal loan?

Yoel Wagschal CPA: No. Merchant Cash Advance companies do not have interest. If you have interest then what you have is a loan business, not a Merchant Cash Advance business. Loans use an entirely different method of accounting. If you are still accounting for your Merchant Cash Advances as loans with interest then you will have regulatory issues. If you tell an IRS agent that you are not a loan company but they see your books are exactly like a loan company, how do you think that will end for you? Loans and interest are in a different world. You are the last person who wants to combine those two worlds. You need to see how they do their books at an accounts receivable factoring company and model yourself after them. They do it the way my accounting firm presents it.

Question #2: Your article mentions two ways in which Merchant Cash Advance Companies can account for transactions (cash basis and accrual). Are those the only two ways in which my accounting can be processed?

Yoel Wagschal CPA: I guarantee you would have a big argument if you brought 100 accountants together and asked them all this question: How do I recognize revenue in an accrual basis (from a GAAP standpoint) if I am allowed to take the entire income this year? You would have all kinds of voices and differences of opinions because there is no guidance for this industry. I have done the research and structured an accounting methodology. I’ve spoken with the biggest firms and dealt with the biggest names in this industry. I do have a passion for MCAs. When it comes to a tax standpoint, if you file a cash basis and you want to minimize your exposure, there is really only one way to do it. Those two ways (cash and accrual) can be kept so that they are converted from one to the other at the end of the year. Hence, if you want to prorate the income portion of your receivable (cash basis) I would still keep the books on accrual then convert it at the end of the year. You could do this with a single journal entry because it simplifies the bookkeeping process. You end up with an accrual basis financial statement and a cash basis tax return.

Question #3: I keep being told that my tax liability is based on the difference between what I spend (including funding merchants) and what I receive. For example, if we fund 100K and collect 140K in 140 days how should we keep our books? Right now we don’t recognize any income until we get back the initial funding, even if we renew the merchant over and over. Please elaborate on how revenue should be accounted for. I want to minimize my tax liability but I also want to be sure that this is the correct way to go about it.

Yoel Wagschal CPA: I have a very simple quiz:

YWCPA: Do you trust your accountant?

MCA: Yes. Yes, I do.

YWCPA: You should not. Even if you were my own client I would tell you the same thing. Why do you trust your accountant?

MCA: Because they are a professional. This is what they went to school for. This is what they do for a living.

YWCPA: Do you consider yourself a smart person?

MCA: Yes, I do.

YWCPA: Is it possible that you are smarter than your accountant? Is it possible that they simply learned a different trade than you?

MCA: Yes, that is possible.

YWCPA: Ok, then you should use your own IQ to see if what your accountant says makes sense. If your accountant tells you something that doesn’t make sense about your own business, and you believe your accountant because this is their job then you are not using your high IQ. This is especially true if you have strong negative feeling towards what you are being told. I am not telling you to jump to conclusions. I am saying you should ask questions. Think about this for as long as it takes. Your accounting should be clear and understandable to you.

I am a college professor. When I teach the principals of accounting I always start with debits and credits. I start here because students must know this concept through and through in order to be good accountants. It is the basis of all accounting. New students struggle with the logic behind this principle and I always respond that there are two options: The first option is simply to trust me. They can memorize the information and never know what it means. The second option is to completely understand. This is the option that both my students and Merchant Cash Advance business owners must choose. You, as the business owner, must understand where your own numbers come from. You must understand the foundation of your own accounting. You are entitled and responsible to understand it because of what you must sign on your company’s tax returns.

YWCPA: Do you know what you are signing on the tax return?

MCA: Do I know…?

YWCPA: Do you know what the fine print says directly above where you sign? It says:“Under penalty of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.” That is what you sign. Now, do you know what the preparer has to sign?

MCA: The same thing…?

YWCPA: The preparer signs an acknowledgement that they got paid! What I am saying is that you, the business owner, is ultimately responsible for the numbers that are on your tax return. It is you, not the preparer, who certifies that the numbers are legitimate. Of course, accountants are bound by Circular 230 and code of ethics but the level of responsibility is much higher proportionately to the tax payer than to the tax preparer.

Recognizing income only when a deal pays off is clearly, in my humble opinion, “Fraud and Tax Evasion”. I would not sign off on such a tax return. It goes even further that a lot of people who are saying this type of stuff will add that a renewal is an extension of payment and you don’t have to recognize this until the renewal is completely paid off. In this theory you can be in business for 50 years making billions of dollars and pay zero tax. If you were an IRS agent, would you accept that position?

MCA: Mmmm… What’s your point?

YWCPA: Just answer the question. If you were the IRS agent, would it help if the taxpayer told you “my accountant said it was fine”?

MCA: NNNnno.

YWCPA: That’s my point.

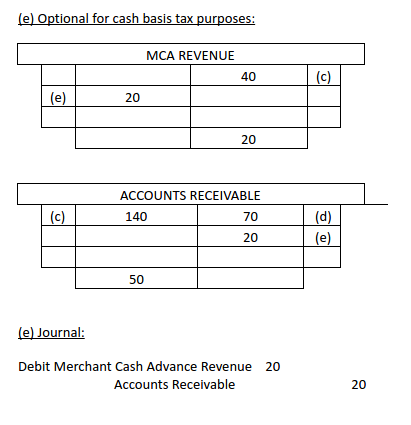

Question #4: When my company advances funds to a merchant how do I account for this? Also, how do I account for my company’s income with cash basis (tax return)?

Yoel Wagschal CPA: Ok, we know that in cash basis accounting we don’t recognize revenue before it is actually received. For instance, a grocery store that lets a customer take an order on credit doesn’t recognize revenue at that point. Income is recognized when funds come in.

Now we will think about the Merchant Cash Advance industry. Let’s start with when you advance funds to a merchant. For this example you advance 100k to a merchant and the payback is 140k. The 100k you send to that merchant should not be expensed. That 100k should stay on your balance sheet. You don’t recognize any income because you haven’t collected any income yet.

At the end of the year we have collected half of the advance. It started with 100k funded and 140k to collect. Now we have collected 70k. The most rational way to decide which part of the 70k goes down on the balance sheet and which part should be recognized as income is to prorate it. You should show that half has been collected which means that half of your income should be recognized now. We show it now because you have, in fact, collected revenue.

Question #5: For cash basis (tax return) purposes, when do we realize a loss? How do you show and what do you call the write off of uncollectible merchant cash advances?

Yoel Wagschal CPA: This is a very good question. There are some weird things going on in this industry because normally in a business you don’t exchange money to make money. On a cash basis tax return you would not see a receivable on the cash basis balance sheet. Concurrently, you would not see any bad debt.

Bad debt is usually not something that you see on a cash basis tax return. However, if you really look at the IRS regulations they do understand that even in a cash basis business there are bad debt expenses. Why wouldn’t you usually see bad debt expense? It is because you never recognize any income from the money you didn’t receive. Even with a cash basis tax payment, when a taxpayer lends money to a vendor (in a ‘normal business situation’) and that vendor doesn’t pay the taxpayer back, we know the taxpayer is entitled to take a bad debt expense.

In the Merchant Cash Advance situation, where we exchange money to make money, what could be more of a ‘normal business situation’? This is how your business works so if a merchant does not pay you back then you are entitled to a bad debt expense (of course, the actual realizable cash loss). This bad debt expense gets realized when the Merchant Cash Advance company is certain they are not going to get paid. In the rare situations where you have already written off a bad deal and the merchant does end up paying, you will need to reduce your bad debt expense for the following year or you can add it to your income for the following year.

As far as labeling, I believe the IRS wouldn’t care what you call it. I understand why you want to label it differently. The truth is that this comes only out of the fear that an amateur might look at it. A real trained knowledgeable professional will understand it. Bottom line is, it is perfect (although not normal) for a cash basis taxpayer to have a bad debt expense. But, you can see nothing here is the norm. So do we care for the amateur or for the expert?

Question #6: (This is for “syndicators” which we define here as entities who provide funds to MCA companies before those funds are sent to merchants). Should I do my books whenever I get a payment, week to week, or in one lump sum? From a GAAP or accounting perspective do we use immediate revenue recognition or the deferred method?

Yoel Wagschal CPA: If you want to simplify your bookkeeping I suggest after the fact accounting. Just be sure to maintain absolute consistency. At the end of the year your accountant should be able to take your information, adjust it to a proper trial balance, and create your year end reports. However, if you do not maintain the highest degree of accuracy and consistency then your accounting work will be much more time consuming and potentially flawed.

In my office we have all different types of clients. We have clients who want their books maintained on a live basis. This means we are responsible for taking the information off their MCA platforms and processing it in the accounting system.

We also have clients who want weekly reports. This is a more tempered measurement of the MCA activity. It paints the MCA picture in broader strokes while still maintaining absolute control where tax liability is concerned.

Finally we have clients who only want monthly or yearly reports. This almost completely separates the deal-to-deal MCA activity from the accounting activity. It leaves my accounting firm with the responsibility of tax liability and accounting while the MCA company does their own MCA deal tracking. Whichever approach works best for the individual companies is what you should choose.

In all of these cases there is one fundamental accounting rule and that is 100% consistency. I teach all of my clients to be very disciplined. We recommend having one bank account that is strictly used for funding and receiving money and a completely separate account for operations. For the larger clients we recommend they fund from one account and receive in another account. There is no problem shifting money between these accounts because when an accountant looks at your books it is very easy to follow your transactions.

After you have separated the accounts we can do the actual accounting work for you. However, as we are about to explain the basic journal entries for MCA accounting we caution you to remember this ‘Breaking Bad’ example. In the TV Show Breaking Bad the show’s star (Walter White) explains why he is irreplaceable. Someone else cannot simply step in and recreate his product. His argument is that he is a chemist with multiple advanced degrees as well as years of experience and research. He cannot simply impart all of the knowledge he has to someone in a matter of days. No one can match his intellect simply by watching his actions. His explanation is that a less experienced person would not be able to know if something was off. How would a less experienced person know if one of the ingredients was the wrong type? How would they know if the temperature was slightly off or the cooling phase took too long?

The same practical concept must be applied here, when you are doing the accounting for your MCA transactions. If there was an error in the journal entries, if a procedure was misunderstood and then applied over and over again, if a large transaction was classified incorrectly – how would you know? Only a highly skilled accountant with knowledge of the MCA industry will be able to look over your work and make sure that all of the procedures have been followed correctly. We are about to provide the most basic journal entries for MCA accounting. However we insist you use caution in implementing these entries. We stress that you should consult with a trained accountant who can understand the procedures and recognize mistakes.

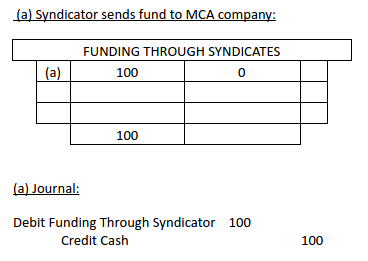

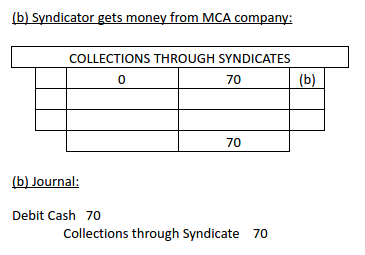

First, we start by looking at an entity who sends funds to an MCA company. As this is where the money trail starts, this is where we will start as well. When a syndicator sends funds to an MCA company they should set up a temporary ledger account. We usually call this “funded thru syndicates”. Every time they send money to the MCA company this entry will show a credit to cash and a debit to this temp account. It won’t have any meaning now but it will have a lot of meaning at the end of the year when they need to produce their financial statements. When this syndicator receives back their money they should debit cash and credit a different account. We usually call this different account ‘collections through syndicates’.

Now, the number of this type of transaction is going to depend entirely on how many deals the syndicator gets involved with and how often they receive cash back from the MCA company. Let’s say there are an accumulation of small transactions that happen over the year. Their outcome is going to be that their ‘funding through syndicate’ account is going to have a debit balance. For the sake of this example, we will make that debit balance 100k. Their ‘collections thru syndicate’ account is going to have a collective credit balance. For this example we will say the credit balance is 70k. As we said, these transactions will not have much meaning when you are processing them individually, but now they will show the bigger picture to your accountant (and hopefully to you!).

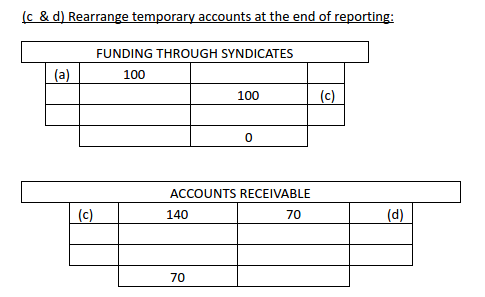

The ‘funded through syndicate’ account is at 100k because the syndicator provided the MCA company with 100k (which then went to merchants). Of course, they are not only getting 100k back. In this business the syndicators must make money on the funds they provide. For the sake of this example, the syndicator will look to get back 140k. Now you see that balance outstanding is 70k.

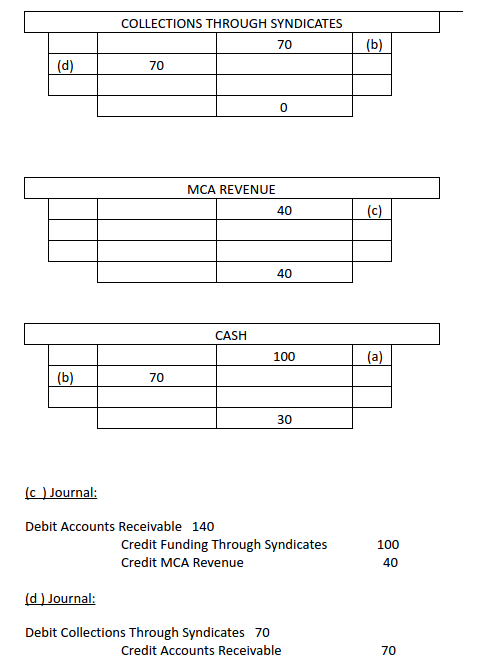

The MCA receivable has a debit balance of 70k, which is what they owe and their revenue is 40k. That’s the difference between the 140k and the 100k.

Now the temp accounts are down to zero. The next step looks at the 70k receivable. We know that 20k of it is uncollected revenue. Based on what we have before, which is used for cash basis purposes, I will add another journal entry crediting merchant cash receivable 20k. This will bring down my receivable to 50k which represents the principal portion of the 100k. This shows the syndicator gave the MCA company 100k and half of it is collected. Now we debit MCA revenue and that brings down the syndicator’s revenue from 40k to 20k for cash basis.

As far as GAAP is concerned we don’t have special guidance for this industry. The industry is very unique. We do have the principal of industry practices constraint. I have been very involved in this industry for years. I had a lot of talks with dozens of people all over the country. Investors, funders, creditors, ISO’s, professionals, etc, basically all walks of life connected to this industry. I do feel and believe that the way everyone wants and expects to see the reporting is the way I explained it. As far as MCA companies are concerned they do recognize revenue when your performance obligation has been completed; that is funding. Everything the funder does in the future is collecting their money. There is no performance that this merchant wants from the funder. As a matter of fact the merchant (customer) would be very happy if the funder ceases his activity which is strictly collections. In all other cases where we see revenue being deferred the company still has an obligation to perform. For example, prepaid phone service or insurance both provide services after the bill has been paid. Regarding uncertainty, I feel that this is no different than uncollected receivables. This is why we have a bad debt provision. The bad debt is based on historical performance of each one’s experience. As a side note, I do see a pretty consistent ratio across the line. Uncertainty leads you to the subject of derivatives. Derivatives are uncertain and unknown. Everything is underlined by a future event in the market value of a later date. This is different, as I explained. For instance, a grocery store’s AR is not certain in regards to how much they are going to collect. That is why we always work with fair estimates.

Question #7: How does this journal entry affect my tax returns? Won’t the IRS want it explained? Do they need to see it on each merchant cash advance or all in one entry?

Yoel Wagschal CPA: The IRS is not in the habit of asking to see your internal accounting unless they are performing an audit. They want to see the final result which is your tax return. This is the final report you provide to them. If you are audited then you have to substantiate your numbers and they ask for your ledger. If this happens they will see one journal entry (the one we just discussed) and they will ask how you got to those numbers. Here you will need to provide all the necessary backup, which you will undoubtedly have in your excel sheets, platforms, and correspondence. My accounting firm keeps a detailed record of all financial information we receive. When we do the final journal entry we keep and file all of the source documents that were used to calculate those numbers. We suggest you do the same not simply because the IRS may ask for them but because your investors may ask, your partners may ask, or you may need to present this information in order to diversify your business portfolio. The most important reason to have accurate and reliable financial information is, of course, that it will be used by the business owner – YOU!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Alternative Business Funding’s Decade Club

October 22, 2015 The working capital business is a very different animal now than it was a decade or so ago when many of today’s established players were just starting out.

The working capital business is a very different animal now than it was a decade or so ago when many of today’s established players were just starting out.

“At that time, the industry was a bunch of cowboys. It was an opportunistic industry of very small players,” says Andy Reiser, chairman and chief executive of Strategic Funding Source Inc., a New York-based alternative funder that’s been in business since 2006. “The industry has gone from this cottage industry to a professionally managed industry.”

Indeed, the alternative funding industry for small businesses has grown by leaps and bounds over the past decade. To put it in perspective, more than $11 billion out of a total $150 billion in profits is at risk to leave the banking system over the next five plus years to marketplace lenders, according to a March research report by Goldman Sachs. The proliferation of non-bank funders has taken such a huge toll on traditional lenders that in his annual letter to shareholders, J.P. Morgan Chase & Co. chief executive officer Jamie Dimon warned that “Silicon Valley is coming” and that online lenders in particular “are very good at reducing the ‘pain points’ in that they can make loans in minutes, which might take banks weeks.”

The burgeoning growth of alternative providers is certainly driving banks to rethink how they do business. But increased competition is also having a profound effect on more seasoned alternative funders as well. One of the latest threats to their livelihood is from fintech companies, like Lendio and Fundera,for example, that are using technology to drive efficiency and gaining market share with small businesses in the process.

“Established lenders who want to effectively compete against the new entrants will need to automate as much decisioning as possible, diversify acquisition sources and ensure sufficient growth capital as a means to capture as much market share as possible over the next 12 to 18 months,” says Kim Anderson, chief executive of Longitude Partners, a Tampa-based strategy consulting firm for specialty finance firms.

Of course, there is truth to the adage that age breeds wisdom. Established players understand the market, have a proven track record and have years of data to back up their underwriting decisions. At the same time, however, experience isn’t the only factor that can ensure a company will continue to thrive over the long haul.

WORKING TOWARD THE FUTURE

Indeed, established players have a strong understanding of what they are up against—that they can’t afford to live in the glory of the past if they want to survive far into the future.

“With every business you have to reinvent yourself all the time. That’s what a successful business is about,” says Reiser of Strategic Funding. “You see so many businesses over the years that didn’t reinvent themselves, and that’s why they’re not around.”

Strategic Funding has gone through a number of changes since Reiser, a former investment banker, founded it with six employees. The company, which has grown to around 165 employees, now has regional offices in Virginia, Washington and Florida and has funded roughly $1 billion in loans and cash advances for small to mid-sized businesses since its inception.

One of the ways Strategic Funding has tried to distinguish itself is through its Colonial Funding Network, which was launched in early 2009. CFN is Strategic Funding’s secure servicing platform which enables other companies who provide merchant cash advances, business loans and factoring to “white label” Strategic Funding’s technology and reporting systems to operate their businesses.

“When you’re in a commodity-driven business, you have to find something to differentiate yourself,” Reiser says.

FINDING WAYS TO BE DIFFERENT

That’s exactly what Stephen Sheinbaum, founder of Bizfi (formerly Merchant Cash and Capital) in New York, has tried to do over the years. When the company was founded in 2005, it was solely a funding business. But over the years, it has grown to around 170 employees and has become multi-faceted, adding a greater amount of technology and a direct sales force. Since inception, the Bizfi family of companies has originated more than $1.2 billion in funding to about 24,000 business owners.

Earlier this year, the company launched Bizfi, a connected online marketplace designed specifically to help small businesses compare funding options from different sources of capital and get funded within days. Current lenders on the platform include Fundation, OnDeck, Funding Circle, CAN Capital, SBA lender SmartBiz, as well as financing from Bizfi itself. Financing options on the platform include short-term funding, equipment financing, A/R financing, SBA loans and medium term loans.

Earlier this year, the company launched Bizfi, a connected online marketplace designed specifically to help small businesses compare funding options from different sources of capital and get funded within days. Current lenders on the platform include Fundation, OnDeck, Funding Circle, CAN Capital, SBA lender SmartBiz, as well as financing from Bizfi itself. Financing options on the platform include short-term funding, equipment financing, A/R financing, SBA loans and medium term loans.

Sheinbaum credits newer entrants for continually coming up with new technology that’s better and faster and keeping more established funders on their toes.

“If you don’t adapt, you die,” he says. “Change is the one constant that you face as a business owner.”

David Goldin, chief executive of Capify, a New York-based funder, has a similar outlook, noting that the moment his company comes out with a new idea, it has to come up with another one. “If you’re not constantly innovating you’re in trouble,” he says. “It’s a 24/7 global job.”

Capify, which was known as AmeriMerchant until July, was founded by Goldin in 2002 as a credit card processing ISO. In 2003, the company began focusing all of its efforts on merchant cash advances. Four years later, the company made its first international foray by opening an office in Toronto. The company continued to expand its international presence by opening up offices in the United Kingdom and Australia in 2008. The company now has more than 200 employees globally and hopes to be around 300 or more in the next 12 months, Goldin says. The company has funded about $500 million in business loans and MCAs to date, adjusted for currency rates.

THE CULTURE OF CHANGE

Five or six years ago, Capify’s main competitors were other MCA companies. Now the competition primarily comes from fintech players, and to keep pace Capify has made certain changes in the way it operates. From a human resources standpoint, for instance, Capify switched from business casual attire to casual dress in the office. The company has also been doing more employee-bonding events to make sure morale remains high as new people join the ranks. “We’ve been in hyper-growth mode,” he says.

CAN Capital in New York, another player in the alternative small business finance space with many years of experience under its belt, has also grown significantly (and changed its name several times) since its inception in 1998. The company which began with a handful of employees now has about 450 and has offices in NYC, Georgia, Salt Lake City and Costa Rica. For the first 13 years, the company focused mostly on MCA. Now its business loan product accounts for a larger chunk of its origination dollars.

This year, the company reached the significant milestone of providing small businesses with access to more than $5 billion of working capital, more than any other company in the space. To date, CAN Capital has facilitated the funding of more than 160,000 small businesses in more than 540 unique industries.

Throughout its metamorphosis to what it is today, the company has put into place more formalized processes and procedures. At the same time, the company has tried very hard to maintain its entrepreneurial spirit, says Daniel DeMeo, chief executive of CAN Capital.

One of the challenges established companies face as they grow is to not become so rule-driven that they lose their ability to be flexible. After all, you still need to take calculated risk in order to realize your full potential, he explains. “It’s about accepting failure and stretching and testing enough that there are more wins than there are losses,” says DeMeo who joined the company in March 2010.

ADVICE FOR NEWCOMERS

As the industry continues to grow and new alternative funders enter the marketplace, experience provides a comfort level for many established players.

“The benefit we have that newcomers don’t have is 10 years of data and an understanding of what works and what doesn’t work,” says Reiser of Strategic Funding. With the benefit of experience, Reiser says his company is in a better position to make smarter underwriting decisions. “There are many industries we funded years back that we wouldn’t touch today for a variety of reasons,” he says.

Experienced players like to see themselves as role models for new entrants and say newcomers can learn a lot from their collective experiences, both good and bad. Noting the power of hindsight, Reiser of Strategic Funding strongly advises newcomers to look at what made others in the business successful and internalize these best practices.

One of the dangers he sees is with new companies who think their technology is the key to long-term survival. “Technology alone won’t do it because that too will become a commodity in time,” he says.

Over the years Strategic Funding has learned that as important as technology is, the human touch is also a crucial element in the underwriting process. For example, the last but critical step of the underwriting process at Strategic Funding is a recorded funding call. All of the data may point to the idea that a particular would-be borrower should be financed. But on the call, Strategic Funding’s underwriting team may get a bad vibe and therefore decide not to go forward.

“We look at the data as a tool to help us make decisions. But it’s not the absolute answer,” Reiser says. “We are a combination of human insight and technology. I think in business you need human insight.”

Seasoned alternative funding companies also say that newbies need to implement strong underwritingcontrols that will enable them to weather both up and down markets.

The vast majority of newcomers have never experienced a downturn like the 2008 Financial Crisis, which is where seasoned alternative financing companies say they have a leg up. Until you’ve lived through down cycles, you’re not as focused as protecting against the next one, notes Sheinbaum of Bizfi. “Every 10 years or 15 years or so, there seems to be a systemic crisis. It passes. You just have to be ready for it,” he says.

Goldin of Capify believes that many of today’s start-ups don’t understand underwriting and are throwing money at every business that comes their way instead of taking a more cautious approach. As a funder that has lived through a down market cycle, he’s more circumspect about long-term risk.

One of the biggest problems he sees is funders who write paper that goes two or three years out. His company is only willing to go out a maximum of 15 months for its loan product, which he believes is s a more prudent approach. He questions what will happen when the economy turns south—as it eventually will—and funders are stuck with long dated receivables. “You’re done. You’re dead. You can’t save those boats. They are too far out to sea,” Goldin says.

One of the biggest problems he sees is funders who write paper that goes two or three years out. His company is only willing to go out a maximum of 15 months for its loan product, which he believes is s a more prudent approach. He questions what will happen when the economy turns south—as it eventually will—and funders are stuck with long dated receivables. “You’re done. You’re dead. You can’t save those boats. They are too far out to sea,” Goldin says.

Having a solid capital base is also a key to long-term success, according to veteran funders. Many of the upstarts don’t have an established track record and need to raise equity capital just to stay afloat—an obstacle many long-time funders have already overcome.