Breakout Capital is BACK

July 17, 2019

SecurCapital Corp has acquired the lending business of Breakout Capital Finance.

Breakout was founded in 2015 by Carl Fairbank, a former investment banker, and quickly made a splash in the burgeoning small business lending industry. The company has raised significant capital and is a principal member of Innovative Lending Platform Association (ILPA), a trade group that among other things, created SMART Box, a uniform loan disclosure meant to enhance transparency across the industry.

Earlier this year, however, the company suspended originations.

But that’s poised to change. The deal with SecurCapital, a supply chain and financial service provider headquartered in California, means that Breakout is on track to resume originations as early as next week, according to the company. And there’s other changes afoot.

Tim Buzby, who previously served as the company’s CFO is now the President & CEO. Buzby is well primed for the job. He’s a former CEO of Farmer Mac, a company he spent 17 years with.

Carl Fairbank, who previously served as CEO of the lending business, will provide strategic guidance during the transition, the company reports. He will no longer have a day-to-day role.

“After four years as Founder and CEO of Breakout Capital Finance, this transaction begins the next chapter of Breakout Capital’s lending business,” Fairbank is quoted as saying in a company announcement. “SecurCapital is also committed to the proliferation of best practices to drive change in the broader market. I believe Breakout Capital, in partnership with SecurCapital, is now well positioned for substantial growth, especially with its commitment to FactorAdvantage.”

Fairbank is reportedly shifting his focus toward driving innovation in artificial intelligence, machine learning, and blockchain.

Breakout Capital has also hired McLean Wilson, former CEO of Charleston Capital (fka Drift Capital Partners), an asset manager in the SME space, and former CEO of inFactor, a factoring company, as Chief Credit Officer.

In an interview with Breakout’s new CEO Tim Buzby and VP Jay Bhatt (who has been with the company since the very beginning), they said that the company’s risk criteria and credit box will remain the same as it was previously, with potential to even expand it down the road. The company pressing the originations pause button from approximately February to July, therefore, shouldn’t be interpreted as a weakness of the company’s business model. Rather the acquisition and changes should suggest the opposite.

Steve Russell, CEO of SecurCapital, commented, “We’re delighted to have found a highly respected team and innovative business model in the small business finance space. I share the founder’s vision of the massive potential of the FactorAdvantage lending solution and believe we now have the platform and capital to rapidly grow this industry-changing product. We couldn’t have found a better business to complement SecurCapital’s strategic vision for empowering small businesses.”

Two SecurCapital executives have also been placed on Breakout’s board of directors.

Buzby confirmed that operations will resume as normal. The business address and business name will remain the same with one notable difference; That being that the name has been shortened from Breakout Capital Finance to Breakout Capital. It’s also now being operated by a subsidiary of SecurCapital.

Apple’s Credit Card Looms Despite No Clear Launch Date

July 14, 2019 “A new kind of credit card. Created by Apple, not a bank.”

“A new kind of credit card. Created by Apple, not a bank.”

Now plastered across Apple’s website, these words signal the company’s next advancement into finance with Apple Card, the new credit card service it is launching later this summer. And they’re only half true.

While it is a novel take on credit cards, it’s not entirely free of banking’s influence, as Goldman Sachs has partnered with Apple for it. According to Margaret Keane, CEO of Synchrony Financial, the largest provider of store credit cards, there “were a lot of us” bidding for the partnership with Apple, “us” being banks and card providers, but Goldman came out on top.

The spoils of war being won in this case are a 2023 earnings-per-share gain of 2% by 2023 for Goldman, as well as the responsibility of managing all card payment disputes. The latter of which being an anomaly amongst Apple services, as the company has a history of overseeing all aspects of the customer experience.

What Apple stands to gain in comparison is a 1% gain by 2023. Being below the industry average, neither of these forecasts are something to be excited about. But these figures aren’t surprising, with the card offering no fees and low interest rates it appears as if Apple Card will be launched with the hope of staking some of the market share rather than seeing profits soar.

Offering financial statements and analysis via an app, as well as being available in two forms, a digital card in Apple Wallet and a titanium card that features no numbers on it, front or back, Apple Card bares a striking similarity to the recent trend of app-based banking witnessed in Europe, with the likes of N26 and Revolut booming in popularity in previous years.

Where Apple differs from these companies is that it specializes in credit, thus it offers a range of features unique to both the format and their position as a near-omnipresent tech giant. Auto-fill integration with Safari; cash back on each purchase made with Apple Card, being 3% on any Apple products purchased, 2% on non-Apple purchases, and 1% when using your Apple Card at a vendor who doesn’t accept Apple Pay; an APR range of 13.24-24.24; and options for when you’d prefer to pay your interest, complete with clear payment schedules, are all being promised. As well as this, Apple is hoping to combat the common inconvenience of cryptic merchant names that pop up in statements. Jennifer Bailey, Vice President of Apple Pay, explained that “With Apple Card we use machine learning and Apple Maps to transform this mess into names and locations that you’ll recognize.”

All of this was outlined back in March, when Tim Cook took to the stage in Cupertino, California to claim that Apple is making the “most significant change” to credit cards in five decades. But months have passed since this assertion, and as the vague release date of “summer” offers no specificity to Apple fans who are holding their breath, those who are curious about Apple Card are left to be satisfied by the infrequent reviews that slip out from Apple employees who are enrolled in the program’s beta.

We’ll find out if the wait will be worth it sometime soon, probably, but until then there’s always the 1986 Apple credit card that can be ogled at until Apple Card is released to the public.

Expansion Capital Group Names Herk Christie Chief Operating Officer

June 28, 2019 Sioux Falls, SD — Expansion Capital Group ECG) today announced the appointment of Herk Christie from VP of Operations to Chief Operating Officer. Christie will oversee the company’s underwriting, IT, analytics, and merchant support and services departments. Christie, has been with ECG since March 2016 and has played a critical role in the growth of ECG and its many successes.

Sioux Falls, SD — Expansion Capital Group ECG) today announced the appointment of Herk Christie from VP of Operations to Chief Operating Officer. Christie will oversee the company’s underwriting, IT, analytics, and merchant support and services departments. Christie, has been with ECG since March 2016 and has played a critical role in the growth of ECG and its many successes.

ECG, headquartered in Sioux Falls, SD, is a technology-enabled specialty lender that leverages data and analytics to offer customized solutions to small businesses.

Since inception, ECG has connected over 12,000 small businesses nationwide to approximately $350 million in capital. Christie’s appointment comes as ECG continues to see increased growth in its small business lending platform that utilizes technology, data, and analytics to drive user experience and increase access to capital. Christie will lead ECG’s internal operational infrastructure to meet the growing demand for its expanded services.

“ECG continues to put Sioux Falls on the map for financial technology innovation by creating products and solutions that have won the hearts and minds of our customers,” said Christie. “I am incredibly energized to help lead the company to its next phase of innovation and operational excellence as we expand product options to suit the evolving needs of small businesses across America.”

Vincent Ney, CEO of ECG, said, “Herk understands how to create a culture and environment where our hardworking employees have the opportunity to maximize their growth potential within a range of businesses opportunities. Herk’s leadership in our operational strategy has been a key driver in ECG’s growth and success.”

——–

About Expansion Capital Group

Expansion Capital Group (“ECG”) is headquartered in Sioux Falls, SD with an additional office in Wilmington, DE. ECG is a technology-enabled specialty lender that leverages data and analytics to offer customized solutions to small businesses. Since inception in 2013, ECG has provided approximately $350 million in working capital to small businesses throughout the United States. Continued investment in its lead referral partnerships, technology platform, people, and its proprietary risk-based analytics modeling platform has positioned ECG to increase its origination volume by approximately forty percent since 2018. This investment and growth has led ECG to be recently recognized as the 802nd Fastest Growing Private Company in America and the 2nd Fastest in South Dakota by Inc. 5000, as well as the Best FinTech to Work by SourceMedia.

For business inquiries, please contact newpartners@expansioncapitalgroup.com.

For job inquiries, please contact khillberg@expansioncapitalgroup.com.

More

DeBanked: Thanks to ECG, South Dakota is on the Alternative Lending Map

Argus Leader: Here are the South Dakota firms honored on Inc. 5000 list of fastest-growing businesses

Consumer Affairs: Best Business Loan Companies

Are The Bankers Taking Over Fintech?

June 27, 2019

For Rochelle Gorey, the chief executive and co-founder of SpringFour, a “social impact” fintech company, mingling with industry movers and shakers at this year’s LendIt Fintech Conference was just what the doctor ordered. “I went mainly for the networking opportunities,” Gorey told AltFinanceDaily.

SpringFour, which is headquartered in Chicago, works with banks and financial institutions in the 50 states to get distressed borrowers back on track with their debt payments. It does this by digitally linking debtors with governmental and nonprofit agencies that promote “financial wellness.

The indebted parties—more than a million of whom had referrals that were arranged by Gorey’s tech-savvy company last year—constitute not only household consumers but also commercial borrowers. “Small businesses face the same issues of cash flow as consumers, and their business and personal income are often combined,” she says. “If their financial situation is precarious, it’s super-hard to get credit, a line of credit, or a business loan.”

Although Gorey felt “overwhelmed” at first by the throng of 4,000 conference-goers at Moscone Center West in San Francisco—roughly the same number as attended last year, conference organizers assert— her trepidation was short-lived. It wasn’t too long before she was in circulation and having chance encounters and serendipitous interactions, she says, with “all the right people at the workshops and at the tables in the Expo Hall.”

Although Gorey felt “overwhelmed” at first by the throng of 4,000 conference-goers at Moscone Center West in San Francisco—roughly the same number as attended last year, conference organizers assert— her trepidation was short-lived. It wasn’t too long before she was in circulation and having chance encounters and serendipitous interactions, she says, with “all the right people at the workshops and at the tables in the Expo Hall.”

Armed, moreover, with a “networking app” on her mobile phone, Gorey was able to arrange targeted meetings, scoring roughly a dozen, 15-minute tete-a-tetes during the two-day breakout sessions. These included audiences with community bankers, financial technology companies, and “small-dollar” lenders. “And it went both ways,” she says. “I had people reaching out to me”—just about everyone, it seemed, appeared receptive to “finding ways to boost their customers’ financial health.”

Gorey’s success at networking was precisely the experience that the event’s planners had envisioned, says Peter Renton, chairman and co-founder of the LendIt Fintech Conference. Organizers took pains to make schmoozing one of the key features of this year’s gathering. Not only did LendIt provide attendees with a bespoke networking app, but planners scheduled extra time for meet-ups. “We had around 10,000 meetings set up by the app,” Renton says, “about double the number of last year.”

AltFinanceDaily did not attend the LendIt USA conference on the West Coast this year. But the publication sought out more than a half-dozen attendees—including several financial technology executives, a leading venture capitalist, a regulatory law expert, and the conference’s top administrators—to gather their impressions. While informal and manifestly unscientific, their responses nonetheless yielded up several salient themes.

The popularity—and effectiveness—of networking was a key takeaway. Most seized the opportunity to rub elbows with influential industry players, learn about the hottest startups, compare notes, and catch up on the state of the industry. Most importantly, the event presented a golden opportunity to make the introductions and connections that could generate dealmaking.

“My goal this year was to strike more partnerships with lenders and fintech companies,” says Levi King, chief executive and co-founder at Utah-based Nav, an online, credit-data aggregator and financial matchmaker for small businesses. “We had great meetings with Fiserv, Amazon, Clover Network (a division of First Data), and MasterCard,” he reports, rattling off the names of prominent financial services companies and fintech platforms.

James Garvey, co-founder and chief executive at Self Lender, an Austin-based fintech that builds creditworthiness for “thin file” consumers who have little or no credit history, said his goal at the conference was both to serve on a panel and “meet as many people as I could.”

Self Lender is in its growth stage following a $10 million, series B round of financing in late 2018 from Altos Ventures and Silverton Partners. Garvey reports having meetings with Bank of America and venture capitalist FTV Capital “over coffee” as well as F-Prime Capital, another venture capitalist. “It’s just about building a relationship,” he said of making connections, “so that at some point, if I’m raising money or want to partner, I can make a deal.”

There was a concerted effort to recognize women, as evidenced by a packed “Women in Fintech” (WIF) luncheon that drew roughly 250 persons, 95% of whom were women. (“Many men are big supporters of women in fintech and we didn’t want to exclude them,” Renton says). The luncheon was preceded by a novel event—a 30-minute, ladies-only “speed-networking” session—which attracted 160 participants, reports Joy Schwartz, president of LendIt Fintech and manager of the women’s programs.

At the luncheon, SpringFour’s Gorey says, “it was empowering just to see lot of women who are senior leaders working in financial services, banks and fintechs.” The keynote speech by Valerie Kay, chief capital officer at Lending Club, was another highlight. “She (Kay) talked about taking risks and going to a fintech startup after 23 years at Morgan Stanley,” Gorey reports, adding: “It was inspiring.”

The women’s luncheon also marked the launch of LendIt’s Women In Fintech mentor program, and presentation of a “Fintech Woman of the Year” award. The recipient was Luvleen Sidhu, president, co-founder and chief strategy officer at BankMobile, a digital division of Customers Bank, based near Philadelphia, which employs 250 persons and boasts two million checking account customers.

I am honored to be the 2019 Fintech Women of the Year and thrilled that @BankMobile won Most Innovative Bank. It’s very exciting to be recognized by @LendIt Fintech with this prestigious award and I congratulate the finalists in all the categories. https://t.co/qjADuKEMrB pic.twitter.com/hFJVFw1fLS

— Luvleen Sidhu (@LuvleenSidhu) April 11, 2019

BankMobile, which also won LendIt’s “Most Innovative Bank” award, has an alliance with Upstart to do consumer lending and a partnership with telecommunications company T-Mobile. Known as T-Mobile Money, the latter service provides T-Mobile customers with access to checking accounts with no minimum balance, no monthly or overdraft fees, and access to 55,000 automated teller machines, also with no fees. (At its website, T-Mobile Money describes itself as a bank and uses the slogan: “Not another bank, a better one.”)

The impressive salute to women notwithstanding, their ranks remained fairly thin: just 733 attendees identified themselves as “female” on their registration forms, LendIt’s Schwartz says, a little more than 18% of total participants. Seventy-five of the 350 total speakers and panelists—or 21%—were female. (Schwartz also reports that another 157 registrants selected “prefer not to say” as their sexual orientation, while 22 checked the box describing themselves as “non-conforming.”)

In LendIt’s defense, AltFinanceDaily, who caters to a similar audience, regularly reviews its readership demographics using several tools. They have consistently indicated that women make up 18% – 23% of the total, in line with what LendIt experienced at its most recent event.

By all accounts, many panels were informative, jampacked and attendees were engaged. King, who moderated a panel on regulatory changes in small business lending, which dealt with such topics as California’s commercial “truth-in-lending” law and controversial “confessions of judgment” laws, says: “They didn’t have to lock the door but the room was pretty full and people seemed to be paying attention. I didn’t see people studying their cellphones.”

The Expo Hall was teeming with budding fintech entrepreneurs, financial services companies and multiple vendors hawking their wares. But as numerous fintechs were angling to forge lucrative symbiotic relationships with banks, some participants—even those who were hailing the conference for its networking and deal-making opportunities—lamented the heavy presence of the establishment.

The banks’ ubiquitousness especially vexed Matthew Burton, a partner at QED Investors, an Arlington, (Va.)-based, venture capital firm and a veteran fintech entrepreneur. Before signing on with QED last year, Burton had been the co-founder of Orchard Platform, an online technology and analytics vendor for fintech and financial services companies which was purchased by fintech lender Kabbage.

Not only did bankers seem to playing a more prominent role at the LendIt conference, Burton notes, but “big four” accounting firm Deloitte had signed on as a major sponsor. “The energy level seemed a bit lower than in past years,” Burton told AltFinanceDaily. “It’s not like people were depressed but it wasn’t bubbling with excitement. A couple of years ago we thought all these new fintechs would replace the banks,” he explains. “Now the discussion is over how to partner and collaborate with banks. It’s not as exciting as when everyone thought banks were dinosaurs.

“I couldn’t really tell if there were more bankers attending this year,” Burton adds, “but it sure felt like it.”

King, the Nav executive, told AltFinanceDaily: “It was a little bit subdued. I don’t know if it was nervousness about the economy or politics, but the subject of risk came up more often in side conversations with venture-backed businesses and banks and alternative fintech lenders. One large bank we deal with,” he adds, “told me it’s spending most of its time working on risk.”

Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute who participated in a standing-room-only session on state and federal fintech regulation, declares: “I’ve been to three of their conferences, including one in New York, and I would say that this one did not have as much pizzazz. It may be that the industry is maturing.”

For his part—when asked whether there was a palpable absence of passion this year—LendIt’s Renton told AltFinanceDaily: “I would say that it felt more businesslike. Fintech has had a lot of hype and we have had conferences that were ridiculously over-hyped in 2015 and 2016. And in 2017 (the mood) was much more somber. This one felt optimistic and businesslike.”

There were 750 bankers in attendance, almost one in five participants. “The number of bankers was not up significantly” over last year, Renton says, “but the seniority of the bankers was higher. We worked very hard to get senior bankers to attend this year.”

Renton was bullish on the closer ties developing between nonbank online lenders and banks. That was reflected as well in the several panels exploring ways to develop partnerships between the two sides. He noted that a session called “How Banks are Matching Fintechs on Speed of Funding and User Experience” drew a heavy crowd. “It brought more bankers than we’ve ever had before,” Renton says.

Moderated by Brock Blake, founder and chief executive at the fintech Lendio, the panel was composed of three bankers: Ben Oltman, the Philadelphia-area head of digital lending and partnerships at Citizens Bank; Gina Taylor Cotter, a senior vice-president at American Express (the highest-ranking woman at the company); and Thomas Ferro, a senior marketing manager at Bank of America. “The banks came to LendIt not just to learn but to decide whom they’re going to partner with,” Renton says. “Fintechs need banks and banks need fintechs. That is the narrative you hear on both sides.”

(Asked whether any banks sponsored this year’s conference, Renton replied: “They are not sponsoring yet in any number but we are working on that.”)

OnDeck, a top-tier fintech lender to small-businesses in the U.S., which has been making forays abroad to Australian and Canadian markets, is an enthusiastic champion of the fintech-bank union. So much so that it claimed LendIt’s “Most Promising Partnership” award for the cooperative relationship it struck with Pittsburgh-based PNC Bank, which uses OnDeck’s platform to make small business loans. (Among the partnerships that OnDeck-PNC beat out: Gorey’s SpringFour, which was named a finalist in the competition for its association with BMO Harris Bank.)

“We were the first fintech lender to strike a true platform relationship with a bank,” Jim Larkin, head of corporate communications at OnDeck says, noting that the PNC deal follows on the New York-based fintech’s similar, innovative arrangement with J.P. Morgan Chase. “Others may do referrals,” he explains. “What we do is actually provide the underlying platform to accelerate a bank’s online lending capabilities. We deliver the software and expertise to construct the right type of online lending engine.”

Meanwhile, there was avid interest about the stock performance of publicly traded fintechs—for example, Square and GreenSky—both of which had seen their share prices tumble and then recover.

Burton noted that, among venture-backed firms, the most excitement seemed to be coming from Latin America. “Everyone was very bullish on a Mexican company, Credijusto, an alternative small business lender that was written up the in the Wall Street Journal,” he says. “It’s not going public yet but it had a large debt-and-equity raise of $100 million from Goldman Sachs. And SoftBank Group announced a $5 billion Latin American tech fund.

“There was a lot of talk,” he adds, “about how money was flowing into Mexico and Brazil.”

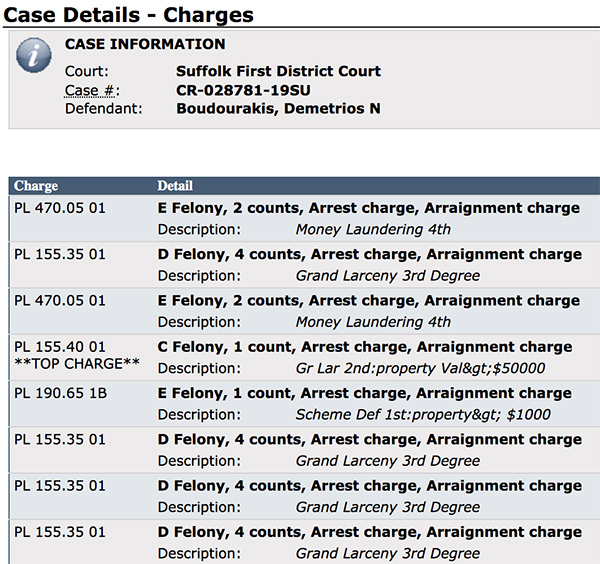

Long Island Business Loan Brokers Arrested in Bust

June 13, 2019 The owner of a Long Island based ISO/loan brokerage and several employees have been arrested, Newsday reports. Demetrios Boudourakis, whom deBanked has previously reported on, is charged with grand larceny, money laundering and other crimes for his role in an advance fee loan scheme. Boudourakis allegedly led a fraud ring that stole more than $2 million from small business owners nationwide. Six other defendants have also been charged with related crimes. They include Nadim Afzali of Hicksville, Tanya Balbi of Farmingdale, Christopher Looney of Bethpage, Joseph Johnson of Brentwood, Jude Brun of Elmont, and Michelle Soccodato of Hicksville.

The owner of a Long Island based ISO/loan brokerage and several employees have been arrested, Newsday reports. Demetrios Boudourakis, whom deBanked has previously reported on, is charged with grand larceny, money laundering and other crimes for his role in an advance fee loan scheme. Boudourakis allegedly led a fraud ring that stole more than $2 million from small business owners nationwide. Six other defendants have also been charged with related crimes. They include Nadim Afzali of Hicksville, Tanya Balbi of Farmingdale, Christopher Looney of Bethpage, Joseph Johnson of Brentwood, Jude Brun of Elmont, and Michelle Soccodato of Hicksville.

The investigation began last year and involved numerous agencies, including the Suffolk and Nassau police and sheriff’s departments, New York State Police, the FBI and the Drug Enforcement Administration.

The investigation began last year and involved numerous agencies, including the Suffolk and Nassau police and sheriff’s departments, New York State Police, the FBI and the Drug Enforcement Administration.

According to Newsday, “Boudourakis and his associates, through the dark web, obtained the names of people who had been denied loans. They would then call those people to tell them they had qualified for loans but would have to pay interest and fees upfront.”

According to Long Island Business News, law enforcement agents who executed search warrants at several locations recovered electronic equipment, three handguns, a sawed-off shotgun and a pill press. The investigation leading up to the bust included court-authorized eavesdropping and audits of financial records and physical and electronic surveillance.

Previously, AltFinanceDaily reported that JTT Funding, Boudourakis’ company, had been accused of forging a Confession of Judgment and impersonating rival companies. Those were civil cases, not criminal cases. Court records show that those cases remain ongoing.

Among the company names the ring used in the alleged scheme were Federal Business Lenders, Federal Business Funding, JTT Funding, JTT Global Holdings, Inc. Blackrock Funders, Inc. and Blackrock, Inc. It is possible that some of those names closely resemble names of competitors and the actual companies have not been accused of any wrongdoing.

Boudourakis is a retired MMA fighter. His nickname in the ring was “The Tyrant.”

ForwardLine, One of the Original Funding Companies, is Back

June 5, 2019 Steve Carlson, CEO, ForwardLine

Steve Carlson, CEO, ForwardLineForwardLine Financial originated well over $65 million in loans in 2018, according to CEO Steve Carlson. ForwardLine would not share its origination numbers, but Carlson said the company is comfortably on the AltFinanceDaily list of top originators. ($65 million is the lowest origination number on the list).

Last week, the company announced that it secured a $100 million credit facility from Credit Suisse AG and Neuberger Berman private equity funds. This is the company’s largest credit facility to date. Its previous credit facility was with East West Bank and that relationship is still in place.

ForwardLine is a direct marketer that provides working capital loans of up to $200,000 to small businesses.

Carlson told AltFinanceDaily that ForwardLine, which was founded in 2003, has been scaling its business dramatically over the past year and a half. This is no coincidence. Instead, Carlson said this is the result of years worth of planning following a majority investment in ForwardLine in 2015 by a private equity firm called Vistria Group.

“We spent 2016 and 2017 very thoughtfully building out a technology platform, a data infrastructure, and a management team to scale the business,” Carlson said. “We’re now actioning on that plan. So this is all part of a multi-year strategy.”

A company statement said that the company’s loan performance in 2018 was record-breaking. ForwardLine increased year-over-year total originations by over 300% in the first quarter of 2019.

Carlson said that the new facility will be used primarily to grow the business. ForwardLine is located in Woodland Hills, CA, and it employs 110 people, more than half of whom work in the sales department. Other employees include underwriters and data and analytics people.

MCA Company Files 15 COJs Against a Medical Practice, Dispute Arises Over Alleged Forgery

May 29, 2019 A New Jersey physician was one day going about his usual business, and the next day found himself an unwitting judgment debtor for almost $2,000,000 based on more than a dozen forged Confessions of Judgment (COJs) of which he had no knowledge. That’s the scenario described in papers by the physician’s attorney suing New York-based Itria Ventures, LLC. Itria is a subsidiary of its more well known parent company Biz2Credit.

A New Jersey physician was one day going about his usual business, and the next day found himself an unwitting judgment debtor for almost $2,000,000 based on more than a dozen forged Confessions of Judgment (COJs) of which he had no knowledge. That’s the scenario described in papers by the physician’s attorney suing New York-based Itria Ventures, LLC. Itria is a subsidiary of its more well known parent company Biz2Credit.

In the span of 19 months, Itria funded a medical practice 19 times (an average of once a month), putting the practice on the hook for millions of dollars in purchased receivables. In March 2017, Itria declared one of those agreements to be in default and filed a COJ in the Supreme Court of New York, successfully securing a judgment in the amount of $245,114. Despite this, Itria continued to enter into at least 3 more funding contracts with them after defaulting.

The relationship would sour as Itria attempted to enforce its New York judgment in New Jersey with vigor. According to Court papers filed in Bergen County, Itria sought to have a judgment debtor, a doctor, arrested after he allegedly did not respond to an information subpoena or attend a deposition. In September 2018, a judge denied Itria’s application for an arrest warrant as the parties were reportedly in discussions to resolve.

When those discussions failed, Itria claimed that 14 more of the 19 contracts were also in default as they went ahead and filed 14 new COJs against the medical practice parties in March 2019. All told, Itria’s judgments add up to around $1.9 million. And just as Itria had previously, they began the procedure to enforce them.

But there’s a twist. The COJs and the contracts might have forged signatures for one of the parties.

On April 18th, Itria Ventures was sued by the very same doctor they sought to have arrested.

“Those confessions of judgment appear to bear my signature and have been filed against me but are fraudulent and forgeries because I did not sign them and the signature on them is not mine,” the plaintiff argued. Itria is a co-defendant alongside several entities that make up the medical practice, two notaries, Itria’s attorneys, and the plaintiff’s own brother, who is also a doctor.

Plaintiff’s claims of forgeries are onerous given that notaries were present, but the evidence is compelling given that on several contracts a notary attested that he appeared before her to sign it when there is surprisingly no signature there at all.

“This is a fraud even the most sophisticated lawyers would have trouble spinning in their favor. This fraud is shocking to the conscience,” the plaintiff’s attorney argued.

In instances where plaintiff’s signature is present, plaintiff alleges that his brother forged his signature and that the notaries fraudulently went along with it. In addition to the alarming variations in his signature, the plaintiff’s attorney pointed out an instance where a signature appears to be not only forged but a photocopied forgery.

Accordingly, the plaintiff is seeking to have all the judgments as they pertain to him personally, vacated.

Itria wasn’t convinced the allegations held weight given that it was the first time forgery had been raised in 2 years of communications. Documents filed appear to show there have been discussions to resolve for some time. They separately pressed forward on May 13th to have a Court appoint a post-judgment receiver over the medical practice.

Itria has relayed to AltFinanceDaily that their enforcement efforts have been in compliance with all laws and court rules and that they’ve worked with these debtors in a cooperative fashion to attempt to provide them with the opportunity to resolve their financial difficulties. For example, Itria says they (a) provided these debtors with a reduced/modified payment plan, (b) provided them, for an extended period of time, with a de facto forbearance from enforcement to allow them to ‘catch their breaths,’ and to attempt to resolve their financial difficulties by seeking financing elsewhere or otherwise , and (c) at the debtor’s request, assisted them in attempting to obtain alternate financing for many of their business needs, not just to make Plaintiffs whole.

On May 29th, the judge ordered a preliminary injunction enjoining Itria from enforcing the 15 judgments against the plaintiff only and any other judgments “purportedly executed by plaintiff.” The catch is that the plaintiff must post a $1.3 million bond by June 7th. If it’s ultimately determined that the injunction was not warranted, the plaintiff will be responsible for all of Itria’s costs and damages related to the injunction. Itria is not enjoined, however, from enforcing the judgments against any of the plaintiff’s co-defendants.

The case is listed under Index Number 154067/2019 in The New York County Supreme Court.

BFS Capital Joins ILPA

May 23, 2019

The Innovation Lending Platform Association (ILPA), a group of online small business financing and service companies, announced today the addition of BFS Capital. ILPA is known for creating the Straightforward Metrics Around Rate and Total Cost (SMART) Box.

“We believe that transparency matters,” Ruddock told AltFinanceDaily.

“BFS Capital is committed to being both a responsible and an innovative lender,” Ruddock said. “Our membership in the ILPA allows us to work with industry leaders who are dedicated to advancing standards and best practices in the critical small business lending marketplace… [and] we believe that clarity and transparency is critical in helping [small businesses] make educated and informed financial decisions.”

As a new member of ILPA, BFS will join current members including OnDeck, Kabbage, BlueVine and 6th Avenue Capital.

“We applaud Mulligan Funding and BFS Capital for committing to adopt fair and transparent disclosure best practices to ensure small businesses are well informed when seeking funding,” said ILPA CEO Scott Stewart. (ILPA announced that Mulligan Funding has joined the association as well).

BFS is also a member of the Small Business Finance Association (SBFA) and Ruddock told AltFinanceDaily that BFS will remain a member of that trade association as well.

Separately, BFS announced today that it has named Fred Kauber as the company’s new Chief Technology Officer and Chief Product Officer. Kauber was previously with fintech marketplace platform CAIS Group and he served in senior roles at First Data, Dun & Bradstreet and IBM.

“I’m confident that Fred is the right person to advance both our vision and our capabilities [at BFS,]” Ruddock said.