Snapshot On Australia: Growth In The Making

August 30, 2019

The Australian alternative lending market continues to gain momentum, bolstered in part by increased awareness, heightened competition and growing dissatisfaction with the status quo.

Indeed, there’s been significant growth in the few years since AltFinanceDaily first wrote about the nascent alternative lending business down under. Notably, Australia’s alternative funding volume surpassed $1.14 billion in 2017, up 88 percent from $609.59 million in 2016, according to the latest data available from KPMG research. It’s the largest country in terms of total alternative finance market volume in the Asia Pacific region, excluding China, according to KPMG.

To be sure, the Australian market is still relatively small—at least compared with the U.S. Digging deeper, the largest share of market volume in 2017—the latest data available—came from balance sheet business lending, accounting for more than $574 million, according to KPMG. P2P marketplace consumer lending had the second largest market volume at $256 million. Invoice trading was the next largest segment of the Australian alternative finance market, accounting for $142.65 million, according to the KPMG report.

Its small size notwithstanding, what makes the Australian market particularly interesting is the potential promise it holds for the companies already established there and the opportunities it may offer to new entrants that find ways to successfully compete in the market.

Certainly alternative lending opportunities in Australia are growing, as awareness increases and the desire by consumers and businesses for favorable rates and faster service intensifies. The Australian alternative lending market is similar to Canada in that a small number of large banks dominate the market both in terms of consumer lending and small business lending. But, like in Canada, alternative lenders are gaining ground amid a changing customer mindset that values speed, favorable rates and a digital experience.

Equifax estimates that alternative finance volume in Australia is now growing at about 10 percent to 15 percent per year; that compares to a decline of approximately 20 percent for some major traditional lenders in terms of credit growth, says Moses Samaha, executive general manager for Equifax in Sydney. This presents an opportunity for alternative lenders to serve parts of the market the banks don’t want and those that are more attuned to a digital experience.

Even so, challenges persist. For instance, digital disruptors are still working on gaining brand awareness, and the market is only so big to be able to accommodate a certain number of alternative players. Time will time whether there will be consolidation among alternative lenders and more bank partnerships, which haven’t been so successful to date. “It doesn’t feel like they are as active as they were announced to be,” Samaha says.

At present, the Australian market consists of a few dozen alternative lenders pitted against four major banks. RateSetter, SocietyOne and Wisr are among the largest alternative players in the consumer lending space. On the small business side, Capify, GetCapital, Moula, OnDeck, Prospa and Spotcap are some of the leading companies. PayPal Working Capital also has a growing presence in the Australian small business lending market.

New lenders continue to eye the Australian market for entry, but it’s not an easy market to crack, according to industry participants. The market consists of mostly home-grown players and that’s not expected to change drastically. (Capify, OnDeck and Berlin-based Spotcap are notable exceptions. Another U.S. major player, Kabbage, previously provided its technology to Australia’s Kikka Capital, but that agreement is no longer in force.)

There can be a steep learning curve when it comes to outsiders doing business in Australia. What’s more, there’s no longer the first-to-market advantage that existed a decade or so ago. It’s also a relatively limited market in terms of size, which can be off-putting. Australia has a population of around 25 million, making it less populated than the state of California, with an estimated 39.9 million residents.

Still, for alternative players that are able to successfully navigate the challenges the Australian market presents, there’s ample opportunity to grab market share away from traditional players—similar to the pattern that’s emerged elsewhere around the globe.

Take consumer lending, for example. The unsecured consumer lending market in Australia sits at about $70 billion, with the large banks occupying maybe a 90 percent share of that, says Mathew Lu, chief operating officer of Wisr (previously known as DirectMoney Limited). Compared with other markets such as U.K. and the U.S., who went through a similar journey around a decade ago, “Australia is probably three or four years into that same journey of growth. It’s shifting and changing,” he says.

Alternative lenders have made strides in undercutting the large banks by offering generally lower rates and typically faster loan times. Unfavorable press related to bank lending practices has also benefited alternative lenders. Lu refers to these conditions as “a perfect storm” for growth.

Wisr, for instance, saw loan origination volume spike 409 percent in fiscal year 2018. The company secured $75 million in loan funding agreements last year and boasts more than 80,000 customers, according to a company presentation.

Marketplace lender, SocietyOne, which in March reached $600 million in loan originations, is another example of an alternative lender that has benefited from the momentum. The company— celebrating its 7th anniversary this summer—is hoping to reach $1 billion in loans by 2020, according to its website.

RateSetter—another major player in this space—has also experienced significant growth since launching in Australia in 2014, and is now funding over $20 million in loans each month, according to its website. In April, the company soared past $500 million in loans funded and in May it saw a record number of new investors register. The company has more than 15,000 registered investors by its own account.

One question for the future is whether the consumer alternative lending space in Australia will ultimately be too crowded amid a spate of new entrants. Wisr’s Lu says “there’s a big question mark” regarding how many alternative lenders the market can sustain. “Will there be a level of consolidation or amalgamation? These are questions ahead of us,” he says.

One question for the future is whether the consumer alternative lending space in Australia will ultimately be too crowded amid a spate of new entrants. Wisr’s Lu says “there’s a big question mark” regarding how many alternative lenders the market can sustain. “Will there be a level of consolidation or amalgamation? These are questions ahead of us,” he says.

For its part, alternative lending to small businesses is also a growing force within Australia. As a testament to the development of this market, in June 2018, a group of Australia’s leading online small business lenders released a Code of Lending Practice, a voluntary code designed to promote fair terms and customer protections. Currently, the Code only covers unsecured loans to small businesses. Signatories include Capify, GetCapital, Moula, OnDeck, Prospa and Spotcap.

Capify—an early entrant to Australia—has been pursuing businesses there since 2008. The company, which integrated its U.S. business in 2017 to Strategic Funding Source (now called Kapitus) is now operating only in Australia and the U.K. In Australia, it has executed more than 7,500 business financing transactions for Australian businesses and has more than 50 staff members in its Australian offices.

The company recently closed a deal with Goldman Sachs for a $95 million line of credit for growth in Australia and the U.K., which includes building out its broker program to increase distribution and technology investment.

David Goldin, the company’s chief executive, says Capify is hoping to grow its Australian business between 25 percent and 30 percent in 2019. The company is looking at M&A activity as well as organic growth.

Since Capify has been in the market, he has seen a number of new entrants—some more successful than others. One concern Goldin has is the lack of experience by some of these competitors. Many aren’t pricing the risk properly and not underwriting prudently to be able to weather a downturn, he says. They are so new, he questions whether they have the expertise to be able to survive a downturn given what he characterizes as pricing and underwriting missteps.

“You can’t go out 24 months on a 1.25 factor rate – that’s crazy,” he says, referring to some contracts he’s seen. “I’ve seen this movie in the U.S. before and it doesn’t end well.”

Meanwhile, competition has driven down prices and made moving quickly on potential leads more of a necessity. When leads come in today, if you’re not on the phone in 30 minutes, you could lose it to a competitor, he says.

Meanwhile, competition has driven down prices and made moving quickly on potential leads more of a necessity. When leads come in today, if you’re not on the phone in 30 minutes, you could lose it to a competitor, he says.

While the small business market is an enticing one for alternative lenders, raising awareness of their offerings continues to be a challenge.

“The small business market is fragmented and raising awareness is expensive,” says Beau Bertoli, co-founder and co-chief executive of Prospa, another prominent small business lender in Australia. “There hasn’t been much innovation in small business banking, but many Australians still don’t think of switching from banks and traditional lenders,” he says.

That said, more small businesses are turning to alternative lenders and these companies say they expect growth to increase over time. Recent research commissioned by OnDeck found that 22 percent of small and medium-sized businesses would consider an online lender, up from 11 percent in the past. This could be buoyed further by the introduction of Open Banking in Australia, which was set to be introduced in Australia in 2019, but this was pushed back to early 2020.

“We look forward to the introduction of Open Banking in Australia as it should allow lenders to use incremental data points to improve risk modeling, and increase competition in the SME lending space, ultimately providing SMEs with improved access to cashflow solutions to grow and run their businesses,” says Cameron Poolman, chief executive of OnDeck in Australia.

Bertoli of Prospa, which recently listed on the Australian Stock Exchange, says the Australian alternative lending market will also benefit from strong support from industry and government to increase competition and improve consumer and small business outcomes. The government recently established a $2 billion Australian Business Securitisation Fund, which is a huge win for small business, he says, that will ultimately make the finance available to small business owners more affordable by lowering the wholesale cost of funds for alternative lenders. “We expect this will boost credibility and consideration of alternative lenders among small business owners,” he says.

Declining property values is another factor helping alternative lending. “In November 2018 we saw the largest annual fall in property prices in Australia since the global financial crisis in 2009,” says Simon Keast, managing director of Spotcap Australia and New Zealand.

“As property prices decline, business owners find it more difficult to use their home as loan security and as such, turn to alternative lenders such as Spotcap that can provide them with unsecured loans for their business,” he says. What’s more, the SME Growth Index in March showed for the first time that business owners are almost as likely to turn to an alternative lender as they are to their main bank to fund growth, says.

“As property prices decline, business owners find it more difficult to use their home as loan security and as such, turn to alternative lenders such as Spotcap that can provide them with unsecured loans for their business,” he says. What’s more, the SME Growth Index in March showed for the first time that business owners are almost as likely to turn to an alternative lender as they are to their main bank to fund growth, says.

Overall, the market opportunity for alternative lending to small businesses is compelling, says Bertoli of Prospa. “We estimate the potential market for small business lending in Australia is more than $20 billion per annum and we’ve penetrated only about 2 percent of the market so far. There are 2.3 million small businesses in Australia, and they’re crying out for capital,” he says.

Keast of Spotcap says he expects to see more banks and non-financial enterprises looking to leverage the technology fintech lenders have built to provide swift and digital lending products to small businesses. He offers the example of a partnership Spotcap, a German-based company, has with an Austrian Bank to provide same-day finance to SMEs in Austria as an example of the types of partnerships the company could also seek in Australia. “We have already partnered with an Austrian Bank that is leveraging our lending platform to provide same-day finance to SMEs in Austria, and there is plenty of interest for similar partnerships on the ground here,” he says.

OnDeck, meanwhile, expects to see a shake-out within the alternative finance sector, which will result in a smaller number of bigger players, with the ability to scale and serve multiple customers with a variety of products, according to Poolman, the company’s chief executive.

For his part, Goldin of Capify is bullish on the Australian small business market, but he cautions others that it’s not a gold rush type of place where everyone who comes in can make money.

“The state of California has more opportunity than the entire continent of Australia,” he says.

Born To Borrow

August 26, 2019 Consumer debt has surpassed $4 trillion for the first time, and it’s continuing its ascent into the stratosphere. It’s getting big enough to trigger the next recession, and financial education isn’t changing the underlying consumer behavior.

Consumer debt has surpassed $4 trillion for the first time, and it’s continuing its ascent into the stratosphere. It’s getting big enough to trigger the next recession, and financial education isn’t changing the underlying consumer behavior.

Personal loan balances shot up $21 billion last year to close 2018 at a record high of $138 billion, according to a TransUnion Industry Insights Report. The average unsecured personal loan debt per borrower was $8,402 as of the end of last year, TransUnion says.

Much of the increase in consumer debt has emerged with the rise of fintechs— such as Personal Capital, Lending Club, Kabbage and Wealthfront—notes Rutger van Faassen, vice president of consumer lending at a U.S. office of London-based Informa Financial Intelligence, a company that advises financial institutions and operates offices in 43 countries.

In fact, Fintech loans now comprise 38% of all unsecured personal loan balances, a larger market share than any of the more traditional institutions, the TransUnion report notes. Banks’ market share has decreased from 40% in 2013 to 28% today, while credit unions’ share has declined from 31% to 21% during the same time period, TransUnion says.

Fintechs are also gaining at the expense of the home- equity market, van Faassen maintains. “They’re eating away at some of the balance that maybe historically was in home-equity loans,” he says. While total debt is increasing, the amount that’s in home equity loans is actually shrinking, he notes.

Fintechs are also gaining at the expense of the home- equity market, van Faassen maintains. “They’re eating away at some of the balance that maybe historically was in home-equity loans,” he says. While total debt is increasing, the amount that’s in home equity loans is actually shrinking, he notes.

What’s more, fintechs are changing the way Americans think about credit, van Faassen continues. Until recently, consumers experienced a two step process. First, they identified a need or desire, like a washer and dryer or home renovation. Realizing they didn’t have the cash to fund those dreams, they took the second step by approaching a financial institution for a loan.

If consumers chose a home equity line of credit to procure the cash, they had to wait for something like 40 days from the beginning of the application process to the time they got the money, van Faassen says. “You really had to be sure you wanted something,” or the process wasn’t worth the effort, he says.

Fintechs have removed a lot of the “pain” from that process, van Faassen says. With algorithms helping to assess the risk that an applicant can’t or won’t repay a debt and digitization easing access to financial records, fintechs can quickly evaluate and make a decision on an application. Tech also helps assess applicants with thin or nonexistent credit files, which broadens the clientele while also contributing to total consumer debt.

Meanwhile, mimicking an age old process in the car business, merchants are beginning to make credit available at the point of sale. Walmart, for example, recently signed a deal with Affirm, a Silicon Valley lender, to provide point-of-sale loans of three, six or 12 months to finance purchases ranging from $150 to $2,000. Shoppers apply for the loans by providing basic information on their mobile phones and don’t have to talk to anyone in person about their finances. Affirm’s CEO Max Levchin has called the underwriting process ‘basically instant.”

If that convenience comes at too high a cost, it doesn’t matter much because borrowers can later find another finance vehicle with better terms, van Faassen says. “So if I get the money at the point of sale, which might have been zero for six months and then it steps up to 20-plus percent, there is no problem with refinancing that debt,” he says.

But there’s a downside to the ease of borrowing, van Faassen cautions. It could trigger the next recession, even though unemployment remains low. Despite modest recent gains, wages have remained nearly stagnant for years. That means an increase in interest rates could lessen consumers’ ability to pay off their debts, he says.

Meanwhile, at least some large mortgage lenders have begun running into problems, a situation that bears an eerie resemblance to the beginning of the Great Recession that struck near the end of 2007, notes a report in luckbox magazine, a publication for investors. Stearns Holding, the parent of Sterns Lending, the nation’s 20th largest mortgage lender, filed for bankruptcy protection just after the July 4 holiday, the luckbox article says.

Meanwhile, at least some large mortgage lenders have begun running into problems, a situation that bears an eerie resemblance to the beginning of the Great Recession that struck near the end of 2007, notes a report in luckbox magazine, a publication for investors. Stearns Holding, the parent of Sterns Lending, the nation’s 20th largest mortgage lender, filed for bankruptcy protection just after the July 4 holiday, the luckbox article says.

Another worrisome sign with regard to the possibility of recession is emerging as institutional investors buy into the peer to peer lending market. Institutional investors bought batches of sliced and diced home mortgage securities that helped bring about the Great Depression.

Then there’s the nagging notion that the country and the world are becoming ripe for recession simply because no downturns have occurred for a while. Talk to that effect was circulating at the recent LendIt Conference, van Faassen observes. Fintech executives often come from the banking world and thus still find themselves haunted by the specter of the Great Recession. That’s why they’re already beginning to tighten underwriting for consumer credit van Faassen says.

One difference this time around lies in the fact that nothing about the increase in consumer debt appears to be hidden from public view, van Faassen says. Before, investors fell victim to the mistaken impression that risky mortgage-backed securities were rated AAA when they weren’t.

Plus, the increase in peer-to-peer lending could keep the economy going even if big financial institutions freeze the way they did during the Great Recession, van Faassen notes. “Hopefully, with the new structures that are out there, we can keep liquidity going,” he says. That raises key questions for the alternative small- business funding community. The industry came into being partly as a response to banks’ tightened lending policies during the Great Recession, so perhaps a downturn isn’t such a bad thing for the sector. But a downturn for the economy in general could cripple merchants’ ability to pay off debt.

But all bets are off during hard times. In the last recession the conventional wisdom that consumers make their mortgage payment before paying other bills was turned on its head. Instead of making the house payment—because foreclosure would take several months—people were choosing to make their car payments so they could get to work. Nobody really knows ahead of time what will happen in a recession, van Faassen notes.

After all, economics relies to at least some degree upon the often-irrational financial decisions of the general public. And science demonstrates that it’s no easy task to convince consumers to handle their cash, credit and debt responsibly, says Mariel Beasley, principal at the Center for Advanced Hindsight at Duke University and Co-Director of the Common Cents Lab (CCL), which works to improve the financial behavior of low- to moderate-income households.

“For the last 30 years in the U.S. there has been a huge emphasis on increasing financial education, financial literacy,” says Beasley. But it hasn’t really worked. “Content-based financial education classes only accounted for .1 percent variation in financial behavior,” she continues. “We like to joke that it’s not zero but it’s very, very close.” And that’s the average. Online and classroom financial education influenced lower-income people even less.

Lots of other factors influence financial behavior, Beasley notes. How much a person saves, for example, depends upon how much they make, what their bank tells them and what practices they encountered at home as children, she says. The CCL has been finding out some other things, too.

Lots of other factors influence financial behavior, Beasley notes. How much a person saves, for example, depends upon how much they make, what their bank tells them and what practices they encountered at home as children, she says. The CCL has been finding out some other things, too.

In one example of its findings, it discovered that putting an amount for a minimum payment on a credit card decreases how much consumers pay. That happens because listing a minimum payment amount creates an anchor, and borrowers adjust their payment upward from there, Beasley says. If the card carrier doesn’t specify a minimum, consumers tend to adjust downward from the full amount they owe. “It turns out to be incredibly powerful,” she contends.

It’s the kind of problem that shows financial institutions haven’t devised many systems to reduce consumer debt by speeding up repayment, Beasley maintains. In this example, suggesting higher payments would prompt some consumers to pay off their debt more quickly.

In an exception to standard practice, a credit card company called Petal does exactly that by placing a slider on its website to help borrowers determine the amount of their payment, she notes.

Meanwhile, people tend to base financial decisions on the examples they see other people set, Beasley says. Problems arise with that tendency because they may see one neighbor spending money freely to dine in restaurants but don’t see any of the many neighbors eating at home to save money. They see a neighbor driving a new car but don’t know how much that neighbor is setting aside for retirement.

That’s why most people overestimate how much others spend to dine out in restaurants, Beasley says. When shown the error, most reduce their own spending in restaurants, she notes, but within two weeks their behavior returns to its original level, their newfound knowledge “drowned out by the noise in the world,” she says.

That’s not good for consumers or small businesses, but help is on the way, according to John Thompson, chief program officer of the Financial Health Network, a national nonprofit research and consulting firm that works with financial institutions and other companies to improve consumer financial health.

As part of that mission, the Network has formulated procedures to assess the financial health of individuals and small businesses, Thompson says. It’s too early to say whether the tool will help with loan underwriting, he notes, but financial wellness determines the ability to pay back debt, he notes.

The Network also publishes the U.S. Financial Health Pulse, which recently pronounced just 28% of Americans financially healthy, meaning that they have sufficient income, savings and planning to handle an unexpected expense and act on the decisions they make. About 55% are relegated to various stages of coping, and 17% find themselves in a vulnerable state.

So Americans aren’t feeling financially secure, and they’ve borrowed $4 trillion to reach that unenviable state. They’re borrowing more and learning virtually nothing useful about their financial errors. Thompson has a way of summing up the situation. “It’s crazy,” he says.

Turning a New Leaf: Banking Committee Chairman Says It’s High Time for New Cannabis Company Regulations

August 19, 2019 Recent years have seen a surge of popularity for the legalization of cannabis movement across the United States. Beginning with the normalization and legalization of the herb for medicinal use, and then the outright legalization of it in California, Colorado, Oregon, Nevada, Alaska, Michigan, Vermont, Massachusetts, Maine, Washington, and D.C., most states now support legalization in some form (ie. medicinal use being allowed, or at very least access to CBD products) with the exception of three.

Recent years have seen a surge of popularity for the legalization of cannabis movement across the United States. Beginning with the normalization and legalization of the herb for medicinal use, and then the outright legalization of it in California, Colorado, Oregon, Nevada, Alaska, Michigan, Vermont, Massachusetts, Maine, Washington, and D.C., most states now support legalization in some form (ie. medicinal use being allowed, or at very least access to CBD products) with the exception of three.

According to Kris Krane, Co-founder and President of 4Front, a leading multi-state cannabis company, and contributor to Forbes, support for legalization has steadily increased 1-2% each year since the 1970s, with the recent state-wide legalization legislation bumping those figures up. But while support amongst the populace as well as within certain corners of the government has grown, infrastructural support that is regulated by politicians has lagged.

Specifically, since their legalization, cannabis companies have been unable to open bank accounts due to strict federal restrictions. As a result, cannabis companies, the majority of which being small businesses, have a harder time paying employees, vendors, and taxes; find it tough to acquire start-up capital; struggle to finance themselves in the face of unforeseen expenses; and are subject to the increased security risks that come with holding onto high quantities of cash. As well as these repercussions, such federal hurdles lead to many cannabis companies receiving finance via equity investments, to which Krane says, “the owners of cannabis businesses own far less of their companies than they would in any other industry.”

Viewed alongside the growing attitude to “legalize it,” such financial handicapping paints a picture of the industry that is all smoke and no fire. Krane described the situation as “one of the greatest challenges for cannabis businesses today,” but the tide may be turning.

Idaho Senator Mike Crapo (R), who is the Chairman of the Senate Banking Committee and who has historically been an ardent opponent of legalization, appears to have changed his tune on the matter. When asked if legislation would be required to end the barriers faced by cannabis businesses, Crapo responded “I think so, yeah.”

Idaho Senator Mike Crapo (R), who is the Chairman of the Senate Banking Committee and who has historically been an ardent opponent of legalization, appears to have changed his tune on the matter. When asked if legislation would be required to end the barriers faced by cannabis businesses, Crapo responded “I think so, yeah.”

The comment came after Crapo surprised his peers by holding a committee hearing on allowing cannabis businesses to access banks. Which seemed in opposition to his initial anti-legalization view as well as starkly unaligned with his state’s stance, Idaho being one of the three aforementioned states in which all cannabis-related products are outlawed. Nevertheless, Crapo continued on in the opposite direction of his previous convictions after the hearing, saying, “I think all the issues got well vetted. We now need to, I think, move forward and see if there’s some way we can draft legislation that will deal with the issue.”

Conveniently, such legislation is in the works. The SAFE Banking Act of 2019, put forward by Congressman Ed Perlmutter (D), seeks to solve the issue by lifting the red tape surrounding cannabis companies’ lack of access to banking. Support for the bill is growing, and as proven by Crapo, further support could come from unlikely places.

Fellow Republican, Senator Cory Gardner, explained that “merely having the hearing on marijuana banking issues was a ‘historic moment in the Senate’ … It shows that this isn’t just a regional issue, but a national issue that needs to be addressed … There was some criticism that the Republican attendance wasn’t there, but if they wanted to blow it up they would’ve been there. So I look at that as sort of an acknowledgment that this is now just a status quo issue and not something that they’re going to try and interfere with.”

While on the other side of the aisle, Senator Catherine Cortez Masto (D) said that she “would like to see it as a positive step forward. I support doing something in this country for these states that have legitimized marijuana businesses … I have always been concerned about potential money laundering or crimes that are sort of around these all-cash businesses. By having a financial system, it helps.”

Still, despite there being bipartisan support for the SAFE Banking Act the question of Mitch McConnell looms. Being the Senate Majority Leader, McConnell has influence over which legislation reaches the Senate floor for debate. And while McConnell may have borne the title of “Cocaine Mitch” with pride before, the narcotics-tinged buck stops there as the Kentuckian has gone on record saying he would not support the legalization of cannabis.

Still, despite there being bipartisan support for the SAFE Banking Act the question of Mitch McConnell looms. Being the Senate Majority Leader, McConnell has influence over which legislation reaches the Senate floor for debate. And while McConnell may have borne the title of “Cocaine Mitch” with pride before, the narcotics-tinged buck stops there as the Kentuckian has gone on record saying he would not support the legalization of cannabis.

Interestingly, McConnell is a proponent for the legalization of hemp. Saying that hemp is “a completely different plant than its illicit cousin,” McConnell’s view is born from his state’s agriculture-intense economy. “Everything from clothing to auto parts” can be made from hemp – a sentiment once isolated to communes, is now being publicly uttered by one of the most conservative contemporary Republicans.

Nevertheless, Kris Krane remains an optimist about future legislation as “there seems to be a growing consensus that cannabis banking reform is necessary,” likely due to worries over security. Crapo’s change of mind “represents a growing awareness among federal legislators that blocking cannabis businesses from accessing banking services is a security concern, and even members who may not support overall cannabis reform are increasingly willing to help resolve the banking issue. It is looking more and more possible that the Safe Banking Act [sic] could become law in the next year.”

Enova’s Small Business Division Garner’s Limelight in Q2

August 16, 2019 Late last month, Enova released its second quarter report for 2019. Generally bearing positive news, the report asserts that the company is in a good position due to increasing demand, growth in various areas, and reductions in financing costs.

Late last month, Enova released its second quarter report for 2019. Generally bearing positive news, the report asserts that the company is in a good position due to increasing demand, growth in various areas, and reductions in financing costs.

Total revenue is up from Q2 2018, rising 13% from $253 million to $286 million, just as net income has risen from $18 million to $25 million.

“We are pleased to report another quarter of solid financial results that exceeded our expectations on both the top and bottom line,” said Enova CEO David Fisher in the earnings call. “Our strong financial performance was driven by solid demand, stable credit, and efficient marketing spend. We continue to demonstrate our ability to produce sustainable and profitable growth and our second quarter results further validate this balanced approach.”

Speaking more specifically about which divisions of Enova have excelled, Fisher highlighted the small business sector, which is composed of Headway Capital and The Business Backer. “NetCredit and our small business financing products were the primary growth drivers during Q2, with domestic revenue up 19% year over year … Our products are clearly gaining traction with customers, resulting in originations increasing 140% year over year, and small business now represents 12% of our book at the end of Q2.”

Jim Granat, Enova’s Head of Small Business Financing, chalked such gains up to “having a great team, a good strategy, and a great company behind us that has the ability to invest in the analytics, tech, and people.” The strategy he speaks of is titled ‘Faster and Easier,’ a modus operandi began by him after his arrival to the company in 2018. It is data-driven and involves incorporating certain individual operations of Headway and Business Backer, and streamlining these processes so that the brands overlap for particular actions. Implemented with the belief that “doing it internally would lead to speed and ease externally,” ‘Faster and Easier’ appears to be working, if one takes Fisher’s comments and the report as affirmation.

“We’ve been working really hard and hopefully the results of that show in the fruits of these efforts,” said Granat. “We are just in the beginning of what we can accomplish, these projects take a while and we are incredibly excited about the second half of 2019, let alone 2020 and beyond.”

Chinese Funder MYBank Using Advanced Tech to Provide Capital

August 1, 2019 MYBank, the largest non-bank funder in China, is using new technological systems to approve loan applicants. The company, which is backed by Alibaba founder, second richest person in China, and former English teacher Jack Ma, is now in its fourth year of operations and has thus far provided 2 trillion yuan ($290 billion) in funding to 16 million customers.

MYBank, the largest non-bank funder in China, is using new technological systems to approve loan applicants. The company, which is backed by Alibaba founder, second richest person in China, and former English teacher Jack Ma, is now in its fourth year of operations and has thus far provided 2 trillion yuan ($290 billion) in funding to 16 million customers.

Having partnered with Ant Financial Services, a payment processing company which Ma is also involved in, MYBank has received access to a host of data. In order to apply for a loan, SMB owners give access to their real-time payment records, and from the analysis of these, as well as the non-bank’s own risk-management appraisal system which runs through over 3,000 variables, a judgment is made as to whether or not to fund the applicant.

Ant also provides MYBank with other tech, such as facial recognition software to detect fraud, and aids them with their implementation of cloud-computing and big data. But as well as these methods is another system unique to China: social credit. Currently in its pilot stages, this national reputation system is set to rival traditional credit score systems. It works by increasing or decreasing a citizen’s rating based off whether they perform a good or bad action. Yell at someone unnecessarily on your commute? Your social credit scores lowers. Help an old woman cross the street? It’ll go up.

When discussing how the system could be implemented, MYBank President Jin Xiaolong gave the example of a small business owner who, upon forgetting to return a borrowed umbrella, finds it harder to get a loan. As well as this, Bloomberg reported in 2018 that a very poor social credit score could lead citizens to being barred from staying at luxury hotels, buying high-end real estate, and enrolling their children in elite schools. The flip side of this is that those with impeccable ratings will receive discounts when commuting, relaxed scrutiny when seeking financial aid, and priority when applying to schools.

Made possible by data-tracking tech, social credit scores appear to be almost revolutionary for the alternative finance industry. Partnered with the other technological tools available to MYBank, the company could experience previously unseen heights of successful loans. Or rather it does already, with default rates at approximately 1%.

Accessible via a few taps on a smartphone, MYBank’s application process takes 3 minutes and due to automation, customers are often instantly approved with funds being made available straight away. One customer described this shift in supply as “unimaginable” and praised how easy it now was to find capital as soon as he needed it.

MYbank also revealed Tuesday that it intended to raise $871 million at a valuation of approximately $3.5 billion.

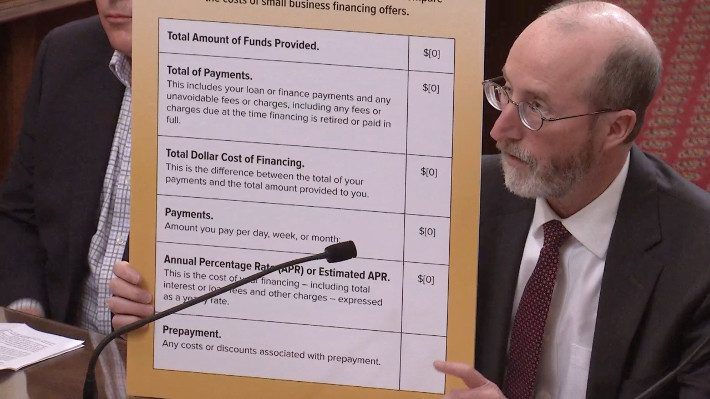

California DBO Making Progress On Finalizing Rules Required By The New Disclosure Law

July 29, 2019 Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

The DBO then issued a public invitation to comment on how that format should work. They got 34 responses. Among them were Affirm, ApplePie Capital, Electronic Transactions Association, Commercial Finance Coalition, Fora Financial, Equipment Leasing and Finance Association, Innovative Lending Platform Association, International Factoring Association, Kapitus, OnDeck, PayPal, Rapid Finance, Small Business Finance Association, and Square Capital.

On Friday, the DBO published a draft of its rules along with a public invitation to comment further. The 32-page draft can be downloaded here. The opportunity to comment on this version of the rules ends on Sept 9th.

You can review the comments that companies submitted previously here.

AltFinanceDaily CONNECT Toronto Kicks Off Today

July 25, 2019Welcome to The Omni King Edward Hotel |

|

|

Don’t be late! Registration and networking starts at 1:30pm at The Omni King Edward Hotel in Toronto.

Schedule of events:

Be sure to introduce yourselves to each of our sponsors and listen to our great speakers. |

||||||

|

|

||||||

|

|

CAN Capital Hired a New CFO: Here’s His Take On The Company

July 23, 2019 The last 12 months have seen plenty of developments within the offices of CAN Capital. September witnessed the announcement of a new credit facility of $287 million with Varadero Capital. January brought news of the hiring of a new CEO. And now, completing the hat trick is CAN’s employment of John McNeill as its CFO.

The last 12 months have seen plenty of developments within the offices of CAN Capital. September witnessed the announcement of a new credit facility of $287 million with Varadero Capital. January brought news of the hiring of a new CEO. And now, completing the hat trick is CAN’s employment of John McNeill as its CFO.

Coming from years of experience in finance, with firms such as Ocwen Financial and Zume, McNeill is stepping into his role with an optimism normally reserved for those at the offset of a new business. Saying that due to recent restructuring, new hirings, and CAN’s re-evaluation of its position in the market over the previous two years, McNeill believes that the company “feels like it’s a nimble startup.” Albeit a startup that has been in the industry for over 20 years.

Founded in 1998 by a small business owner who struggled to be approved for a business loan, CAN has been cemented as a legacy figure within the alternative finance industry. Having persevered through the ’08 crash as well as other economic hiccups over the past two decades, CAN is uniquely positioned in that it has 20 years worth of experience and data, not to mention the personnel who have stuck around to become veterans as well, to guide them through the current moment of market saturation.

And it is the synergy between these two aspects of CAN, the new and the old, that initially drew McNeill to the company. The opportunity to work alongside people who have decades of experience in the market, as well as those who have only been there a few months longer than himself, led McNeill to view CAN as an anomaly, where it’s “like being the new guy, but with all of the tools of historical experience.”

This freshness tempered by lessons learned in the past is also attributed by McNeill to CAN’s CEO, Edward J. Siciliano, who’s worked in commercial financing, sales, marketing, and operations for over 30 years; and who has aimed to expand operations, both technologically and geographically, since his taking up of the role.

McNeill believes that there continues to be plenty of the market left to expand into, saying there’s “still a lot of opportunities to make money and to help secure funding for businesses across America.”