Competing Factions Hurt Alternative Lending’s Message

September 10, 2015 It’s over. Legislators and regulators in Washington DC know alternative lenders exist, and there’s no going back. There will be regulations that impact the industry in some way. That seems to be a definite at this point. What aspects will be regulated and to what extent however is yet to be determined.

It’s over. Legislators and regulators in Washington DC know alternative lenders exist, and there’s no going back. There will be regulations that impact the industry in some way. That seems to be a definite at this point. What aspects will be regulated and to what extent however is yet to be determined.

And here’s the important thing you need to know about that impending conversation with folks in DC; They’re not up to speed on many of the issues being debated between industry insiders, and honestly probably won’t be for a long time, if ever.

They’re literally on square one. So if you were secretly hoping that regulators were on the verge of outlawing stacking, excessive broker fees, or high interest rates, you’re going to be very disappointed. I would argue that more than likely they’d have no idea what you were talking about if you broached these issues with them and it would come across like this:

And that’s because they’re trying to fully understand more basic things such as, why would a small business borrow money online as opposed to a bank? And what does marketplace lending really mean and how does it work?

Folks in DC are genuinely curious about the basics. They want to understand because they don’t want to be caught not understanding and ignorantly lead the nation into another financial crisis. That’s why the Treasury recently issued a Request For Information. You should notice how there’s nothing about stacking in it, but rather more fundamental issues like whether or not marketplace lending is helping borrowers that were historically underserved.

You have to applaud the Treasury’s approach because informed regulations, if that’s what this all leads to, would be much better than uninformed regulations.

The process could easily be jeopardized however if everyone’s so caught up in choosing teams, sides, and points of view that they believe are the “right” ones with the hope of scoring nothing other than perceived political points.

If this is what folks in DC see while they are in the information gathering stage, well then it’s probably not going to be a good outcome for anyone:

Companies that buy future receivables with daily payments and lenders originating 3-year loans with monthly payments actually have a lot in common on the fundamental level. They’re both bank alternatives. And for a number of reasons, small businesses are choosing them over more traditional sources. That’s where the conversation needs to begin.

The opportunity to communicate with rule-makers shouldn’t be squandered on complaints about what other people are doing, but rather on the what, why, and how for small business.

The worst thing that could happen is that divisive language within the industry leads to a regulatory result that negatively impacts all the parties involved, including the small businesses that benefit from this improved system of accessing capital.

Surely there is a way forward for everyone…

The Official Business Financing Leaderboard

June 20, 2015A handful of funders that were large enough to make this list preferred to keep their numbers private and thus were omitted.

| Funder | 2014 |

| SBA-guaranteed 7(a) loans < $150,000 | $1,860,000,000 |

| OnDeck* | $1,200,000,000 |

| CAN Capital | $1,000,000,000 |

| AMEX Merchant Financing | $1,000,000,000 |

| Funding Circle (including UK) | $600,000,000 |

| Kabbage | $400,000,000 |

| Yellowstone Capital | $290,000,000 |

| Strategic Funding Source | $280,000,000 |

| Merchant Cash and Capital | $277,000,000 |

| Square Capital | $100,000,000 |

| IOU Central | $100,000,000 |

*According to a recent Earnings Report, OnDeck had already funded $416 million in Q1 of 2015

| Funder | Lifetime |

| CAN Capital | $5,000,000,000 |

| OnDeck | $2,000,000,000 |

| Yellowstone Capital | $1,100,000,000 |

| Funding Circle (including UK) | $1,000,000,000 |

| Merchant Cash and Capital | $1,000,000,000 |

| Business Financial Services | $1,000,000,000 |

| RapidAdvance | $700,000,000 |

| Kabbage | $500,000,000 |

| PayPal Working Capital* | $500,000,000 |

| The Business Backer | $300,000,000 |

| Fora Financial | $300,000,000 |

| Capital For Merchants | $220,000,000 |

| IOU Central | $163,000,000 |

| Credibly | $140,000,000 |

| Expansion Capital Group | $50,000,000 |

*Many reputable sources had published PayPal’s Working Capital lifetime loan figures to be approximately $200 million in early 2015, but just a couple months later PayPal blogged that the number was more than twice that amount at $500 million since inception. The print version of AltFinanceDaily’s May/June magazine issue stated the smaller amount since it had already gone to print before PayPal’s announcement was made.

Is Alternative Lending An Illusion? (LendIt 2015 Summary)

April 18, 2015More than 2,400 people packed into the LendIt conference last week in New York City and everywhere you turned, startups were boasting of their ability to lend billions of dollars to underserved consumers and businesses. Companies not even old enough to have attended last year’s LendIt conference had reportedly lent tens of millions or hundreds of millions of dollars already. Is it all an illusion?

Investors circled like hawks to try and grab an opportunity into this exploding market. Alternative lenders were practically being tackled by VCs, Private Equity firms, and specialty finance lenders:

Technological innovation is disrupting the status quo, attendees echoed. Surely banks can afford to develop new technology to compete, so why haven’t they? Lendio’s Brock Blake wasn’t afraid to challenge the Short Term Business Lending Panel on this. “Is there real innovation happening or is there regulatory arbitrage?” he asked.

The panelists mostly agreed that it was a combination of both. Stephen Sheinbaum, founder of Merchant Cash and Capital (MCC) and BizFi, said “regulation is not something that scares us in any way.” That’s not surprising considering MCC has survived more than ten years in business and fellow panelist CAN Capital has survived more than seventeen.

But for the newer players entirely reliant on third party brokers or dependent on a Reg D exemption to issue securities, their success may indeed be regulatory arbitrage. And time is on their side.

Karen Mills, the former head of the Small Business Administration asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

It’s the brokers that worry some folks most, an issue that PayPal and Square Capital do not have to contend with at all. OnDeck CEO Noah Breslow stated, “there is always going to be a set of customers that want to shop and want to have help.”

Kabbage’s Kathryn Petralia explained that only 2% of their business comes from brokers and their fees are capped at 4%. CAN Capital’s Jason Rockman argued that it’s about working with brokers that share their values. MCC’s Sheinbaum said, “you have to be willing to not do business with some of the unscrupulous players out there.”

But while these industry captains minimized the role that brokers play, 2015 is already being dubbed the Year of the Broker.

The regulatory environment isn’t the only issue to be worried about, skeptics argued. There was cautious alarm about the market’s viability when interest rates rise or the economy takes a turn for the worse.

“I think there’s going to be a shakeout,” said Steve Allocca of PayPal. MCC’s Sheinbaum explained that when he sees other funders doing deals that don’t appear to make sense, to not feel pressured to do them as well. “Stick to your disciplines. Stick to your guns,” he preached.

Fundation CEO Sam Graziano argued that small business lending is already very risky. The lifetime default rate on 7(a) SBA Loans is 20%, he said. Graziano, who hates the term alternative lending prefers to refer to the industry as digitally enabled lending.

And digitally enabling is something that OnDeck has focused on. In Breslow’s presentation, he said that applying offline for a loan takes 33 hours of work on average. Banks are shuttering branches at a record rate, he added.

Banks are dead, said many in attendance. Kathryn Petralia of Kabbage disagreed. “The death of banks has been greatly exaggerated,” she argued on a panel.

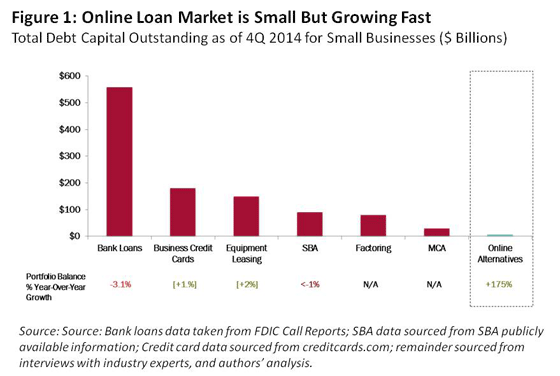

Indeed, Mills’ report shows that total outstanding debt on business loans by banks dwarfs the alternatives by more than 50 to 1.

But former U.S. Treasury Secretary Larry Summers is convinced the tide is turning.”The conventional financial sector has, in important respects, let all of its main constituents down over the last generation, and technology-based businesses have the opportunity to transform finance over the next generation,” he said during the keynote speech.

With conference sessions looking and feeling like a cramped NYC subway during rush hour, the popularity of alternative lending is no illusion.

But healthy skepticism is at least creeping in while the industry marches forward. Changes in regulations, interest rates, and economic activity will separate those simply riding a wave from those that have created something real. Expect companies that exhibited at this year’s conference to be gone by 2016 or 2017, said several panelists.

The final count of LendIt attendees was 2,493 people. 150 people who tried to register at the last minute were turned away. More are expected to attend next year.

Objectively, alternative lending appears to be very real.

A Peek Inside Yellowstone Capital

April 1, 2015When the banks say ‘no,’ alternative financing companies are saying ‘yes,’ sometimes. While costs may run high, there is still a limit on risk that a lender like OnDeck Capital and their competitors can accept.

In January of 2011, Kabbage stated their approval rate on volume-eligible applicants was only 55%. In February of this year, they said it’s about 80%. And a year ago, CAN Capital CEO Dan DeMeo told Forbes their approval rate was almost 70%. Similarly, a Biz2Credit report estimated the approval rate for alternative lenders in 2014 to be around 64% on average.

This indicates that approximately 20% – 35% of small businesses are being declined yet again. These are America’s exiles and they don’t fit into the neat little underwriting boxes that alternative lenders have crafted. Being declined by an alternative lender does not necessarily mean the business isn’t healthy or viable, but rather it could be because they exhibit some characteristic that today’s risk algorithms disqualify. Volatile sales activity, short time in business, poor credit, and atypical SIC codes are just a few of the reasons that a business could be rejected by a lender like OnDeck.

Consequently, an entire Plan C market has sprung up to service the small businesses that have been cast aside by the algorithms. And it’s huge. At the center of it all is Yellowstone Capital, a New York City-based merchant cash advance provider that has carved out its own niche. Founded in 2009, Yellowstone was one of a handful of pioneers that introduced ACH payments to an industry that relied entirely on split-processing.

Yellowstone does not publish their annual funding volume, but according to insiders not authorized to speak on the record, the numbers dwarf many industry behemoths including Square Capital, a company that funded more than $100 million in the last twelve months. And there’s some interesting changes happening there behind the scenes.

Yellowstone does not publish their annual funding volume, but according to insiders not authorized to speak on the record, the numbers dwarf many industry behemoths including Square Capital, a company that funded more than $100 million in the last twelve months. And there’s some interesting changes happening there behind the scenes.

Last year, Yellowstone gave up an equity stake to a New York-based hedge fund in exchange for capital. Just recently however, Yellowstone CEO Isaac Stern led a management buyout to reportedly better position themselves for growth.

As part of the arrangement led by Stern and backed by a private family office, the hedge fund has been bought out and Stern is the only remaining company co-founder to retain an equity stake.

Additionally, private equity turnaround expert Jeff Reece has come on as President. Reece is a former Director of Cogent Partners, a boutique, private equity-focused investment bank and advisory firm.

Josh Karp is remaining the company’s Chief Operating Officer.

Jake Weiser is staying on as General Counsel.

Above all, the changes are more than just a few new faces in management. Yellowstone has already rented an additional floor at 160 Pearl Street, bringing the total floors they occupy there now to three.

Above all, the changes are more than just a few new faces in management. Yellowstone has already rented an additional floor at 160 Pearl Street, bringing the total floors they occupy there now to three.

Notably, the company has endured some negative press in the past of which they are well aware, but they have no shortage of supporters. I contacted two ISOs that claim to have worked with them and asked for their opinion on the Yellowstone experience.

Len Gelman of Allied Capital Corp couldn’t say enough good things about his account manager there, “He fights for every deal I submit, no matter how small or how difficult it may be to get done,” said Gelman. “He always takes my calls and responds to my emails and texts no matter how late it may be.”

And Arty Bujan of Cardinal Equity said, “Working with Yellowstone opened a door of business for me that really wouldn’t have existed without their unique approach to funding what some may call less desirable merchants.”

With a new management team and strong capital backing, Stern and Reece appear to be laying the groundwork to scale.

According to company insiders, Yellowstone is also working to expand their box beyond just high risk businesses and plan to service the middle market risk class. That would in effect also make them a Plan B option.

Their new underwriting depth could spare business owners from that second ‘no.’

It’s Okay For a Business to Act Like a Business

February 10, 2015 A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

McCarthy wrote that achieving a transformation, “will depend in part on facilitating greater transparency, accountability, and fairness across our sector, and reining in predatory actors.” He cuts right to the chase by attacking lenders all while ignoring the reality that businesses are regularly preying on financial companies too, especially in the technology age.

It’s an epidemic. There is actually an entire industry association that is dedicated to preventing repeat merchant fraud. Respecting that small business is the backbone of this country though, it probably wouldn’t be appropriate to draft a Lenders’ Bill of Rights, whereby merchants promise not to deceive, lie, or commit fraud against them. Instead the industry deals with it quietly, investing in new risk infrastructure and ultimately passing the costs on to the good borrowers.

Merchants aren’t inherently bad, but neither are the companies that provide them with financial services. Let’s agree that the world is good but that bad actors exist.

McCarthy’s argument for a Small Business Borrowers’ Bill of Rights is premised on the assumption that in every commercial financing transaction, one side is painfully unaware and uneducated about what’s going on around them despite being an owner, president, or CEO of a company.

I think a dose of self-deprecating reflection is healthy and 2014 definitely brought out many discussions about how to increase transparency and better serve small business. But there’s a line between self-improvement and self-loathing that nobody should lose sight of.

It’s okay to make a profit

It’s okay to make a profit

Imagine that the CEO of a widget retailer grossing $2 million a year is looking for a new widget wholesaler to buy product from. The CEO sits down with a prospective wholesaler and asks for a quote. The wholesaler says they have deals with domestic widget manufacturers and Chinese exporters and based upon these relationships and the circumstances they can sell them in bulk at a price of $2 per widget. Unbeknownst to the retailer, the wholesaler quoted a competing retailer a price of only $1.80 per widget earlier that day. But this is business and if the wholesaler can charge more to this company, he will.

Unsure if he should accept the terms, the retailer pulls out a Widget Retailers’ Bill of Rights and demands the wholesaler charge not a penny more than what would adequately compensate the wholesaler for his work in the name of fairness. He also demands to be presented with unbiased facts on costs, benefits, and risks of every widget manufacturer, so that they can compare products on an apples-to-apples basis without pressure. And if they don’t do this, they will get Washington involved.

If you think this is supposed to be silly, it’s not. It’s McCarthy’s worldview applied. What’s missing from this scenario is that the wholesaler has a widget cost basis of about $1 and is selling them for $1.80 to $2.00, a nice margin. The retailer will sell these widgets for $10 a piece in their stores for an even better margin.

Maybe it’s the consumer that ends up getting screwed on price but even that seems unlikely since widgets are selling off the shelves at lightning speed. So what would be fair and adequate compensation for every party involved? What if the manufacturers are producing widgets for 7 cents each? Is there another layer of possible unfairness here?

Everybody has some kind of incentive and that’s how a marketplace works. If the price is too high, customers won’t buy, they’ll negotiate the price down or they’ll shop elsewhere.

In McCarthy’s Bill of Rights, he rejects the very notion of self-interest. “Some lenders charge higher interest rates just because they can,” he writes. This is how capitalism works. Find your customers price point and sell for a profit. Don’t forget we’re talking about commercial transactions only here!

You ever wonder why they’re called deals?

I’m reminded of someone from the peer-to-peer lending world that once asked me why folks refer to merchant cash advances as deals. They’re not loans, they’re not units, they’re deals!

And true to their deal making roots, terms on them are almost always negotiable. Two companies come together to make a deal… get it? Traditional merchant cash advances are also not loans. They’re literally contracts negotiated by businesses to sell future revenues at a discount in return for upfront cash flow. The concept couldn’t be any more commercial.

And over on the lending side, McCarthy might have you believe that the average small business CEO is unsophisticated shark bait in this unfair world so I pulled up the stats on the industry’s most famous small business lender. According to the S-1 filing, 90% of OnDeck Capital’s borrowers gross between $150,000 and $3.2 million a year in revenue and have been in business for an average of 7.5 years. These are bright companies.

Curiously there’s a group of financiers that are unabashedly capitalist. They will charge whatever they can get away with, take half a business if they want and even call their customers shark bait to their faces. Hopefully they clean up their act before Washington steps in! Thankfully the regulators have not yet put an end to ABC’s Shark Tank though I’m sure McCarthy will propose they do so.

That means you too Marcus Lemonis… Rumor has it you do things to make money all while applying high pressure sales tactics on TV to get people to agree and without telling the business owners the unbiased facts about every other financing option in the entire marketplace.

If it’s okay on TV, it has to be okay in real life.

Business on a deeper level

Business on a deeper level

I didn’t mean to take a stab at Brayden McCarthy personally but his message reflected a culmination of emotions that some people feel in this industry when they’re struggling to keep up. They can’t believe that a client would take something more expensive when they had an offer for something less expensive. Almost 7 years ago I competed against another salesman for a client to whom we both made almost the exact same offer; Same advance amount, same holdback %, same closing fees, but a different receivable purchase amount. The ONLY difference was that the other guy’s price was $2,000 more expensive. Everything else was the exact same and he knew it. And you know what happened? He went with the more expensive offer…

I remember confronting that salesman about it a few days later after I had let my anger cool down. A lot of thoughts had gone through my mind, that perhaps the other guy had lied, coerced him, or conducted some kind of shady trick. Why else could this have happened?! It seemed completely illogical. Of course it was none of those things. The other salesman developed a strong rapport with the customer and they spent most of their time talking about football on the phone.

“He freaking loved me,” the salesman said.

“That can’t be it,” I thought. Still hurt and determined to get the truth, I sent the lost prospect a very long email complete with mathematical formulas (I even used exponents, square roots, and fancy squigglies for good measure) to show how much he would’ve been better off with my offer. He responded almost immediately. “You see, this is exactly why I didn’t go with you,” he wrote.

While I was busy trying to open the customer’s eyes to the magic of the Black-Scholes model, the other salesman was talking to him about whether or not Eli Manning was really franchise quarterback material.

Still a very inexperienced salesman at the time, I had learned a new truth. Business went deeper than just prices, market efficiencies, and a desire to make money, it was also about relationships. Treating one side like an uneducated idiot has become a cornerstone of regulations to protect consumers, and perhaps even rightfully so but imagine the widget retailer grossing $2 million a year walks into a business negotiation and is immediately told that he is too dumb and too unaware to not only understand how to assess a deal but to foresee the consequences of his own decisions if he makes a deal.

Transparency is good, relationships are greater. There’s no need to codify sour emotions into an awkward Bill of Rights. Let two businesses make a deal. It doesn’t have to be the smartest, the fairest, or the best, just something both ultimately agree to. I can’t imagine it any other way.

Mayor Rahm Emanuel Declares War on Merchant Cash Advance

January 16, 2015 FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

Mayor Rahm Emanuel will call on state and federal agencies to regulate business to business lenders. Emanuel said cash advance companies have accelerated their marketing efforts in recent months, resulting in small businesses taking loans they cannot afford.

The article states that business owners have turned to the City of Chicago for help in paying back loans with high rates of interest.

While the mention of APRs reaching into the ranges of triple digits is supposed to shock you, one business lender that charges such rates recently went public and had been backed by Google Ventures, Fortress Investment Group, Goldman Sachs, and Peter Thiel.

Less than 30 days ago we were celebrating these companies as the solution to a problem that has plagued small businesses for all time, access to capital.

While Emanuel is obviously famous for being the 23rd White House Chief of Staff and Obama’s right hand man for a period in his first term, he is not the first mayor to consider the role merchant cash advance companies and high interest business lenders have in cities across America.

All the way back in 2008, the U.S. Conference of Mayors (USCM) adopted a resolution titled, Protecting Main Street Small Business Owners from Predatory Lenders, from which some of the excerpts below are from:

WHEREAS, merchant cash advance companies have already lent approximately $2 billion at egregious rates and have been quoted in leading main stream media publications such as Forbes, Business Week, Dallas Morning News, and American Banker claiming that their new originations have increased 75% in the first half of 2008

WHEREAS, as with payday lenders and predatory lenders in the home mortgage community, Mayors need to take a leadership role to scrutinize predatory merchant cash advance companies, educate small business owners of the dangers posed by these firms, and increase awareness and promotion of alternative, more affordable funding sources to support this vital segment of our economy

BE IT FURTHER RESOLVED, that to protect the general health and viability of their small business communities, cities should investigate whether they can effectively regulate or ban merchant cash advances.

3 months after this resolution was passed, Lehman Brother’s collapsed and the economic crisis was in full swing.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

Who do they think rolled up their sleeves and kept local economies alive when things were at their worst?

While non-bank funding can obviously be expensive, countless business owners have praised merchant cash advances in particular as a solution that came through when none other were available.

Emanuel will learn that companies such as Square and PayPal are part of the crowd that provides merchant cash advances. This is not a shadow industry. Non-bank business-to-business financing is already becoming less expensive nationwide.

According to Fox, the Commissioner of the Chicago Department of Business Affairs and Consumer Protection said the goal is to offer small business owners loans at affordable rates with full disclosure.

Merchant cash advance companies would undoubtedly feel the same way. The dilemma is that advocates of affordable rates tend to really mean single digit rates. When single digit rates are not possible given the risk, they seem to argue that no financing should be given at all, leaving the business to fail or miss out on an opportunity. That’s the exact type of flawed thinking alternative financing companies address…

Ironically, a report from the Federal Reserve Bank of Cleveland last week concludes that small business job creation is lagging with a possible culprit being a lack of access to credit.

Coming out of the most recent recession, however, job creation by small businesses has lagged, and the new business formation rate continues to fall. While it is not clear that these trends are driven by weaker borrowing or limited access to loans, it is evident that businesses need adequate credit to succeed and grow. As such, policy makers should not lose sight of the trends related to small business credit, even with the recent positive reports showing improvements.

And of course in a supposed exposé on merchant cash advances that aired on Chicago Public Radio in November, clips of an interview I did with them were aired to fit the narrative of merchant cash advance as predatory. When asked by the interviewer what a small business owner should do if they didn’t understand a contract, I advised that they hire an attorney or an accountant, and if they couldn’t afford those then to find somebody they felt qualified to offer an opinion. “They should always get a 2nd set of eyes to review a contract if they don’t understand,” I said.

My advice did not air, nor did my explanation that there were two separate types of products that they were confusing as one, one being loans and the other being purchases of future receivables. I suppose it didn’t fit the characterization they were going for.

As quoted in Fox, Financial Advisor Kent Travis advised business owners to “read the documents, don’t sign anything on the spot, make sure you read it thoroughly and if you have trouble understanding it seek the advice of an advisor, CPA, an attorney or a financial planner.”

I couldn’t have said it better myself because I already did.

And in an interview I had with former Congressman Barney Frank, a chief architect of the Dodd-Frank Wall Street Reform and Consumer Protection Act, Frank voiced his opposition to regulations on business-to-business lending in early 2014.

There’s one thing the Fox story does mention that’s hard to argue with and that’s the need for greater transparency. I am all in favor of that.

—————–

For those that haven’t already signed up, this is a reminder that the Law Office of Pepper Hamilton LP is hosting a lunch at their office in New York on January 27th to specifically discuss the merchant cash advance industry’s future.

Interested in discussing legal issues, best practices, and the path forward for alternative business financing? Are you an ISO or funder interested in sharing your thoughts? Send me an email to let me you know if you’d like to attend. sean@debanked.com.

—-

Watch the Fox news report about merchant cash advances:

Despite FinTech Disruptions, Many Thing Stay The Same

January 5, 2015 2014 was an unbelievable year!

2014 was an unbelievable year!

I kicked off last year by opening an account with Lending Club so that I could understand their product. Today I have tens of thousands of dollars invested on their platform and picking up new loans has become part of my daily routine. You could say I’m not surprised they went public a few weeks ago.

I also launched the industry’s first trade publication and ran it as both publisher and chief editor. We produced 6 issues and distributed more than 20,000 print copies combined. Unfortunately the publication will not be continuing further. It is wild to think that it both started and concluded in 2014 as the magazine had a cult-like following.

7 conferences in 4 cities. Las Vegas (twice), San Francisco, New Orleans, and here in New York. I spoke at two of them. Hoping for at least 1 Miami conference this year. Please??? It’s so cold here right now.

OnDeck Capital took a lot of flak in 2014 from both industry insiders and the media. They shrugged it all off and went public on December 17th. Considering they’ve operated on the fringe of the merchant cash advance industry for so long, it was one of those things you had to see to believe. I didn’t get inside the building but I saw the IPO was real from the outside.

I started off 2014 not knowing what a Bitcoin was. Now I have a copy of the entire blockchain, operate a full node (don’t worry I have port 8333 open), have 10 dedicated mining devices running 24/7, have made purchases with bitcoin, conducted countless transfers, and just finished coding a working prototype application using Coinbase’s API. And when I realized that bitcointalk.org and my cryptography books weren’t enough to satisfy my appetite, I found myself talking about bitcoin on IRC; #bitcoin and #bitcoin-pricetalk on irc.freenode.net. I also know who Satoshi Nakamoto really is now too but he made me promise not to tell anyone.

I rebranded Merchant Processing Resource to AltFinanceDaily, retiring a name I’ve used for 4 years.

I interviewed former Congressman Barney Frank, one of the two architects of the Dodd-Frank Wall Street Reform and Consumer Protection Act (it was only a few questions).

I got asked by a credible movie producer if I would help him on a storyline for a script about Wall Street and the alternative business lending industry. Don’t worry I turned it down!

I jumped on the payment disruption bandwagon and used Square to process credit card transactions all year. You should know that I previously did merchant account sales. I could’ve boarded my own account and set my own fees but I went with Square anyway.

I finally got set up to syndicate on merchant cash advances.

I ran my first 5k in Central Park.

I moved to a different part of Manhattan.

Of course a whole lot more happened. It was a roller coaster year which leads me to believe that 2015 will be impossible to predict. There’s a lot more room to grow in FinTech but it might be time for fresh ideas. Everyone and their mom built an online lending marketplace platform in 2014.

Similarly, it’s also a tough time to become a loan broker or MCA ISO especially if you’re undercapitalized. The easy profit ship has sailed. Press 1s and UCCs aren’t winning business models, at least not ones that will invite outside capital or ensure survival long term.

2014 changed finance but in many ways it stayed the same.

It still takes 2-4 days to confirm an ACH didn’t reject! This is annoying all around. If I add funds to Lending Club on a Monday, it’s not accessible until Friday evening. If you debit a merchant on Monday, you won’t really know if you have it until a few days later. Believe it or not I actually mailed out more checks in 2014 than in any other year of my life. The ACH system appears to be fine until you use something that is far more advanced, something I will probably write about over the next month. Instantaneous payments, low transaction fees, no bank involvement. Yeah, it’s time for ACH to go away…

And with banks, well… I have opened business bank accounts over the last few years with 3 different banks. The one I opened in 2014 required a two hour in-person interview, a process that involved filling out forms by hand and being threatened that the government would shut everything down in a heartbeat if they found out that I so much as breathed wrong on an ATM. It was a repeat of prior account opening experiences. Although I’ve never had an account closed for doing anything wrong (because I’m not actually doing anything wrong), it is easy to see how much regulatory pressure banks are under. Swiping your debit card upside down could cause the entire bank to get an Operation Choke Point subpoena. They want your business but they’re scared to death of anything you might do with a bank account.

All the major peer-to-peer platforms of 2014 became centralized. Lending Club and Prosper don’t even fall in the p2p category anymore. The market trend has been to create a platform designed for the little guys and then hand it over to a bank or institutional money to do all the funding. In some ways it’s easier to deal with a handful of big players instead of thousands or millions of retail investors. But with the regulatory environment uncertain on so many new investment products, it’s probably also safer to deal with institutional investors, lest the regulators claim they violated a consumer protection law they thought up this morning.

Banks continue to be the biggest obstacle to innovation because at the end of the day, all payments flow through them. How can one deBank and truly disrupt?

Hopefully we’ll find out in 2015. Happy belated New Year.

My Journey to Bitcoin

November 30, 2014 Count me amongst the libertarians, anarchists, and digital lunatics. I made an online purchase using bitcoin… and it was insanely easy.

Count me amongst the libertarians, anarchists, and digital lunatics. I made an online purchase using bitcoin… and it was insanely easy.

The first person I shared my experience with was a friend who works in automotive manufacturing, someone who operates outside the world of alternative finance. He thought I was crazy or rather he was more confused than anything. “Wait, bitcoin?” he asked. “I thought that was a scam that went out of business two years ago.”

Stunned by his remarks and disappointed with his lack of excitement for me, I told a few more friends about what I had accomplished. They had all heard the term, but none of them knew what it was. Oddly, most seemed to believe that bitcoin had already been revealed as a con and was something from years past, a scheme that came, got hacked and failed.

Not so long ago I was in their shoes. I received my first education in bitcoin this past fall, September 22, 2014 to be exact at the 3rd Annual Tomorrow’s Transactions NYC Unconference hosted in Google’s New York headquarters.

It’s a con?

Famous money laundering expert and author Jeffrey Robinson gave a blistering assessment of bitcoin the currency, which he described as a hoax perpetuated by “libertarian anarchists.” His contentious indictment was half warning, half sales pitch for his latest book, BitCon, which I bought the day it was released.

Robinson argued that bitcoin adoption, while minuscule, was still greatly exaggerated.

There are fewer card-carrying members of #BitcoinCanada than #Starbucks in #Calgary. BitCon: http://t.co/lQecBgwRdp

— Jeffrey Robinson (@WritingFactory) November 2, 2014

He explores several challenges in his book, one of which can be summed up as:

Why would someone exchange dollars into bitcoin only to have to convert their bitcoin back into dollars?

It’s a great question, but it’s something I’ve done every time I’ve traveled abroad. Dollars to euros and then euros back to dollars. Dollars to pounds, dollars to canadian dollars, etc. But why do an exchange at all when the counterparty prices their goods or services in dollars?

Spend $ to buy #bitcoin to pay for #Blackfriday stuff priced in $. Where's the logic? #BitCon— Jeffrey Robinson (@WritingFactory) November 29, 2014 http://t.co/U26d35G0u9

Benefits

Assuming bitcoin’s value against the dollar wasn’t volatile, I can think of three immediate reasons:

1. I don’t have to enter in my credit card number on a website and risk it being hacked or stolen.

2. I can make a payment online if I don’t have a credit card or debit card.

3. I can spare the merchant the payment processing fees.

Let’s forget about point one for now because it’s easy to overlook the pervasiveness of point two. According to the FDIC’s latest National Survey of Unbanked and Underbanked, 25 million people in the country do not have access to a bank or banking products at all. Poverty is a main driver of that but curiously 34.2% of respondents in that group cited that they don’t like dealing with banks or don’t trust them as a reason. 30.8% said that account fees were too high or too unpredictable.

And that’s just the unbanked. 1 out every 5 households in the country is underbanked. They have a bank account but have also obtained financial services and products from non-bank alternative financial services providers in the prior 12 months.

To those of us that rely on banks for everything this may seem extreme, perhaps even downright unbelievable. Coincidentally, Robinson wasn’t the only notable figure at the New York Unconference. He was joined by Lisa Servon who later spoke about her hands-on experience with the unbanked and underbanked. A professor of urban policy at the New School in New York, Servon got a job as a check casher/payday lender in a storefront on a busy corner in downtown Berkeley, California to learn about these households on the front lines.

Consumers can be intimidated by banks she said at the Unconference, especially minorities. Even people who can afford to use banks opt not to. A sample of her experience was published a month ago in the New York Times.

Moving on to point three, accepting bitcoin can either be free or vastly less expensive than accepting a credit card payment. Payment processing fees are significant in commerce. I know this because I accept credit card payments through both Square and PayPal in another business I run and it costs me nearly 3% per transaction. I’ve also sold merchant processing for years and have priced hundreds if not thousands of accounts.

You know that thing American Express invented called Small Business Saturday where consumers are encouraged to spend money at small businesses? Paying with your AMEX card is encouraged of course and AMEX charges about 3.5% to the merchants on every sale.

By going dollars->bitcoin->dollars, you can do even more to help small business by saving them the fee. Granted, most consumers probably wouldn’t jump through any hoops to save a business money especially if it meant trying to figure out how to convert your dollars into something they perceive as “a scam that went out of business two years ago.”

I’ve read all the warnings about bitcoin already and have even been lectured by Robinson personally:

@financeguy74 A fool and his money… the numbers don’t lie. Enjoy Vegas.

— Jeffrey Robinson (@WritingFactory) November 4, 2014

and yet what intrigued me most about bitcoin aside from the transaction costs, was the fact that it was not run by a government.

What if?

Five years ago I had a sinking feeling. The safety and security of the U.S. economy was put to the test. Stock prices fell, lending dried up and millions of Americans actually began to ask themselves, what if? As in what if the dollar collapses? What if your bank account suddenly became worthless? What if you had to suffer for the mistakes others in your country made?

In 2009, a colleague and I pledged to stick together should an eventual economic apocalypse happen. Our plan was simple:

1. Exchange all our money for a gigantic gold brick and two shotguns

2. Sit on gold brick and guard it with those shotguns

Survival would remain possible by chiseling off pieces of the gold brick and exchanging them for food and water. We’d each take turns sleeping and hopefully survive until things returned to normal, if ever.

A fantasy to be sure, and it was great for laughs to break up the day, but what if?

My apocalyptic paranoia is one of many stereotypes of the bitcoin faithful, but I have no interest in exchanging 100% of my dollars to bitcoins. And no, I don’t think the dollar is going to collapse tomorrow. I am intrigued however by a currency that eludes governmental control. We can all keep a gold brick in our back pockets, even if it’s small, and even if it’s digital. If for no other reason, it’s a small hedge for peace of mind.

It’s quite ironic that while critics talk up the dollar’s superiority and the strength of the U.S. government, only 14% of Americans approve of how Congress is handling its job. Not to mention that the nation is at this very moment $18 trillion in debt, a number very unlikely to be made whole. Remove the term bitcoin from the conversation and it’s quite likely the average person would at least be amenable to the possibility of a non-governmental currency.

Perhaps as Americans we are somewhat blind to risks, that we feel nothing catastrophic could possibly to happen to us. To many it is literally unthinkable. A completely independent currency has its merits both now and in far bleaker times.

Of course should the apocalypse occur and all you have is bitcoin, rest assured you will be able to buy a shotgun since you can pay for them with bitcoin:

The get rich quick crowd

Here lies another criticism of bitcoin, that everyone is holding it and no one is spending it. Far from idle, there are currently more than 80,000 bitcoin transactions per day. Without prohibitive transaction fees though, volume is a poor measure of adoption since I could easily send bitcoins back and forth between accounts I own and classify them as transactions.

There are indeed those holding and not spending. Rampant speculation is both a cause of volatility and an argument for its long term unsustainability. Speculators are hoping the digital currency will appreciate and make them filthy rich. If that day never comes, a big sell off will cause its value to drop.

And therein lies the argument… when or if the speculators leave, will that spell the end of bitcoin?

If bitcoin had no practical uses outside of being another digital currency like World of Warcraft gold, then bitcoin would likely be a con, a predictable one that probably would’ve combusted already.

There may actually be a massive market correction in the future. At the current moment, Coinbase reports that 1 btc = $376.23. On November 14th, I paid $397 for 1 btc. It lost about 5% of its value in two weeks, a tough percentage to stomach for the faint of heart, and most certainly the average consumer. It’s also equal to the plunge the S&P 500 took between October 8th and October 16th so such short term volatility exists in other mainstream assets.

I’m not necessarily speculating though. I spent almost half my bitcoins shopping on Overstock on Black Friday, an experience I will detail in another post. A 5% swing might be acceptable for an investment but it’s quite ugly for a currency and this fuels the misinformation that bitcoin is a scam, con, or has already gone out of business two years ago.

1 btc could drop to $100 or $10 after a furious market shakeout and it wouldn’t change how I felt about it. It could also rise back up to $1,000 or higher. That volatility is enticing, almost sexy, but it’s the lack of transaction fees and governance by mathematics rather than actual governments that have me hooked

White knight

Still, bitcoin is waiting for a few white knights, merchants willing to price their goods and services in bitcoin. For years, I have priced advertisements on this website in dollars, but to show my support, I will soon be pricing them in bitcoin going forward. Dollars will still be accepted of course, but those Paypal fees hurt. Paypal costs me 3% in a split second. Is a 5% loss in bitcoin value over two weeks really that wild by comparison?

Still, bitcoin is waiting for a few white knights, merchants willing to price their goods and services in bitcoin. For years, I have priced advertisements on this website in dollars, but to show my support, I will soon be pricing them in bitcoin going forward. Dollars will still be accepted of course, but those Paypal fees hurt. Paypal costs me 3% in a split second. Is a 5% loss in bitcoin value over two weeks really that wild by comparison?

I think not.

Bitcoin is more than a currency. It’s not the euro, the yen, or the peso. It’s a detachment from governments and banking. It’s self-control. Without the private key, your bitcoins can’t be seized.

We live in a world today where everybody has their hand in your money. Just look at what happens when you pay for a cup of coffee using your credit card. The following parties all get paid a percentage:

- The small business owner

- The small business owner’s merchant account representative

- The merchant account representative’s company (the ISO)

- The payment processor (the processor settling the transaction)

- The acquiring bank (the payment processor’s bank that is authorized to use the payment networks)

- The payment networks (Visa, mastercard, etc.)

- The customer’s card issuing bank (The bank that issued the card to the customer gets a percentage of every sale made with that card)

- The state (where there is sales tax)

If you thought bitcoin was insane, what do you call a system where eight parties need to get paid to facilitate the sale of a cup of coffee? And my example was simple. There are typically more parties involved that that.

I don’t want to give the impression that you can evade taxes with bitcoin. I have every intention to stay on the up and up with governments. But remove the tax man and the merchant from the equation, and one has to wonder what the heck is going on with the other six parties, all of whom will ultimately decide if your transaction is acceptable to them. They decide, not you. They can freeze your funds if they don’t like the transaction and they do. It happens to merchants all the time.

Your money is not really yours. You have rights to it, but only to an extent. It can be garnished, frozen or confiscated. That’s the price of liquidity and relative stability. If you can afford to color outside the lines, where you can remove the six bankers and their control, why not experiment? There’s something pure about it, liberating. And when you add in the fact that it’s governed by math, it’s more than that, it’s beautiful.

deBank

If you are under the impression that bitcoin is intimidating, a scam or out of business, well then I encourage you to step out of governments for a minute, to deBank, and take a walk on the digital side. I’m not going to convert all my dollars to bitcoin and you shouldn’t either. Try it out with some extra cash.

If you are under the impression that bitcoin is intimidating, a scam or out of business, well then I encourage you to step out of governments for a minute, to deBank, and take a walk on the digital side. I’m not going to convert all my dollars to bitcoin and you shouldn’t either. Try it out with some extra cash.

Sure, you’ll be in company with libertarians, anarchists, and lunatics. And yes, there’s the paranoid, the speculators, and those transacting in illicit goods and services. The beginning of the Internet and computers was much the same way with the unix and linux faithful.

Perhaps bitcoin needs a Steve Jobs, a Bill Gates, to package up something simple and suitable for the average household. Every American would appreciate squirreling away a little something that is out of reach of government and banks.

The vast majority of Americans already don’t trust congress, and 92 million Americans are already underbanked or unbanked. In 2014 buying a cup of coffee involves paying eight people and the government has spent $18 trillion that it doesn’t have. You have to start to wonder who the real lunatics are. Consumers are waiting for something… even if it’s just a little peace of mind, a hedge, a gold brick in their back pocket, the feeling of independence, freedom, control. Something…

I AltFinanceDaily and loved it. Now it’s your turn.