Amazon Wants to Add Fintech Companies to its Shopping Cart

April 5, 2016

It’s Amazon’s turn to go shopping and it wants to buy fintech companies.

The e-commerce giant just turned the heat up on fintech and said that it will look to acquire startups as the dust around valuations settles. It made its foray into payments in 2013 with ‘Pay with Amazon’ a payment tool integrated on other websites for Amazon customers. Now, the service has 23 million users worldwide.

On Monday, (April 4th), at the Money 2020 Summit in Copenhagen, it announced that it will extend the service to third party merchants hosted on its marketplace.

“The Amazon Payments Partner Program provides Partners with the tools and resources needed to extend the trust and convenience of the Amazon experience to their merchant customers,” Patrick Gauthier, vice president of Amazon Payments, said in a press release. Which is another way of saying that wherever merchants go, Amazon will follow.

This announcement comes after Square released a similar service last week (March 30th) with APIs of its payment integration tool for merchants to use on their sites. Amazon is simultaneously stepping into the turfs of PayPal and Visa while threatening smaller but strong rivals like Square and Stripe. As far as customer acquisition goes, the company doesn’t have to look beyond its own marketplace and what seems like a small step for Amazon could be a giant leap for the industry. The company coincidentally also makes loans to its own customers, just like both Square and PayPal.

Startups in payments and lending are making hay while the sun shines bright. And in this case, that’s nearly half of all the fintech dollars invested. If Amazon is hunting for a good deal, it might be a bit longer in what still seems to be a seller’s market — there are over 152 fintech startups deemed ‘unicorns’ or having valuations of at least $1 billion.

But maybe Amazon is the corrector the market needs?

Watch out Bank Tellers, Robots are Coming for your Job

March 31, 2016 Watch out bank tellers, robots are coming for your job.

Watch out bank tellers, robots are coming for your job.

Investment in private fintech companies and upstarts has grown ten fold from $1.8 billion in 2010 to $19 billion in 2015 and in the same time, bank staff has been slimming down as investors bet on automated finance to eventually overthrow banking. Already, 46 percent of private funding has gone to lending companies selling cheaper loans easily.

The ambition to oust bank behemoths however will need continuous fueling. As things stand now, these lenders are nowhere close to managing that coup. Revenue impact from the digital banking upstarts cause a one percent dent in the $850 billion global banking revenue.

It may be negligible but not to be neglected, investors might say. In the US, online lenders like Lending Club and Prosper Loans sold loans worth $8 billion last year and are looking at a target market of $254 billion, 8 percent of the total consumer credit market.

In its report, Citigroup predicts that US and European banks will shed 1.7 million jobs by 2025 as the banking sector undergoes its own “Uber moment,” forcing banks to automate some lines of business. Anthony Jenkins, former Barclays CEO translates this to halving the number of branches and people over the next few years. If this is an eventuality, different markets will take different paths to get there.

While Nordic and Dutch banks have cut total branch levels by around 50 percent from recent peak levels, branch openings in the top US cities including Seattle, Denver and Dallas have increased between 2-17 percent in the last five years. Part of the reason is because customers still have to visit a branch for identity verification but mostly the benefits (easy access, brand recall) of having a bank branch in wealthy states outweighs the costs involved. “With wealth concentrated in the top cities in the US, a strong branch presence in these cities allows banks to capture wealth,” the report said.

Though the transition of the branch’s role from transactions to advisory/consultancy is imminent, the pace has been gradual, about 11-13 percent since peak pre-crisis. That number could reach 30 percent by 2025. As for the US, there are 15 percent less tellers than there were in 2007.

But the banks want in and are willing to pay. Citigroup and Goldman Sachs have been active in seeding fintech rivals. In the last five years, Citigroup has invested in 13 companies including Square.

Is it time to make another David and Goliath reference?

Funding Circle To Expand Bay Area Staff

March 17, 2016 P2P Lender Funding Circle will expand its Bay Area staff by ten percent.

P2P Lender Funding Circle will expand its Bay Area staff by ten percent.

The company plans to hire 20 people in risk and compliance, product engineering and sales teams. Funding Circle’s marketplace connects borrowers, mostly small business merchants and investors. The company makes money in origination and servicing fees.

The San Francisco-based company was founded in 2010 in the United Kingdom and was launched in the US in 2013. It employs 550 people globally and has so far funded $2 billion to 15,000 businesses.

Earlier this month, Funding Circle announced that it hired former Executive Board Member of the European Central Bank (ECB), Jörg Asmussen, to join its board. This aligns with the company’s streak of boosting manpower. Last year, it hired top executives from Barclays and American Express to head its global risk and analytics team.

Google Culls Online Lenders – Pay or Else?

March 15, 2016Can you become one of the biggest or most successful online lenders without Google? A search layout update may be inadvertently culling the herd.

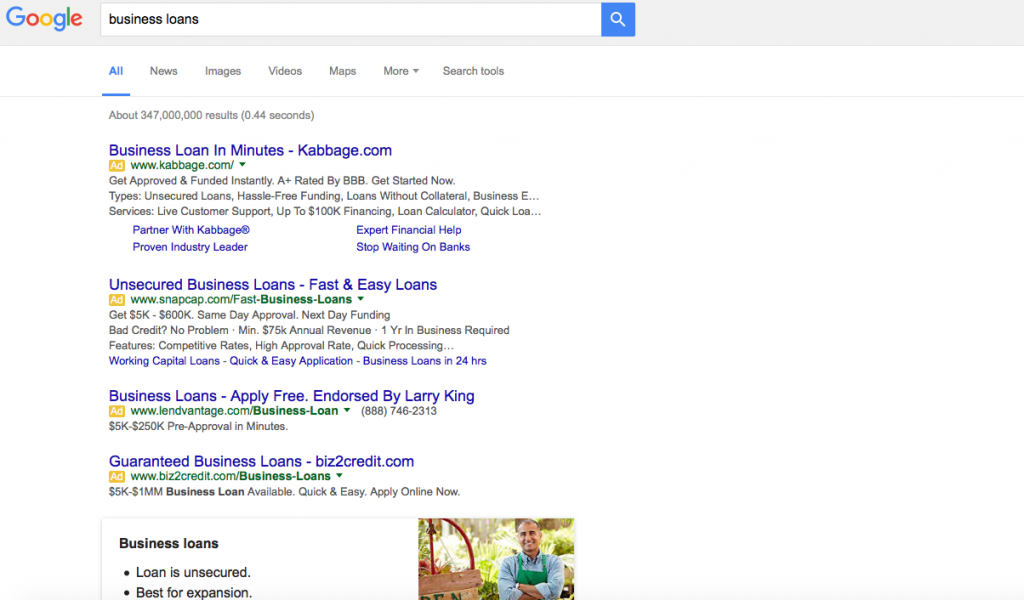

In late February, Google eliminated ads from the right side of the page while adding another layer to the top and bottom. When factoring in features like site links, the effects on organic search has been devastating. Non-paid links are now entirely below the fold for many commercial keywords, which means users may limit their selections entirely to ads. Here’s an example of a full screen browser window on a Macbook Air when searching for Business Loans:

Brad Geddes, a Google Adwords marketing author, expert and consultant, has said the Click-through rate (CTR) on this new 4th ad placement is skyrocketing. “Depending on the keyword, position 4 is going to have a 400%-1000% CTR increase,” he said on Webmaster world. And while side links and bottom links were never a huge factor anyway (less than 15% of click-throughs), Geddes believes a consequence of this change is that fewer ad slots means higher cost bids to rank on the 1st page. “Companies with thin margins are going to have a lot of words fall to page 2,” he wrote.

In summary: Fewer ad placements, higher costs per click, decreased likelihood of organic click-throughs.

And the online lending industry is already feeling the burn. Several funders and ISOs on the commercial side have told AltFinanceDaily in confidence that the online lead gen battle has been lost or that they have been temporarily sidelined by the increase in costs. At least one funder is refocusing their efforts entirely on the ISO channel after a horrible experience with Pay-Per-Click.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

On one industry forum, ISOs have reported that the cost of acquiring a merchant cash advance or business loan deal from Pay-Per-Click is ranging from $700 to $1,200. “PPC for premium keywords as high as $40 at times. Ugly. Real ugly,” one user wrote. Another user wrote, “It’s not just Adwords that is saturated. The whole market is saturated. Lenders and the onslaught of new brokers are making it tough. Lenders with programs like Funding Circle and Kabbage, and with all the advertising money in the world to burn and get direct traffic.” And still another believes that online ads are simply inviting the lowest hanging fruit. “Internet leads have the highest level of fraud,” said one sales manager.

Notably, many of the top 8 funders are only competing for a limited number of competitive keywords or may not even be running Adwords at all. PayPal and Square for example, focus only on their existing payment processing customers despite being “online lenders.”

It’s too early to tell what effects Google’s ad changes will have on the online lending industry, though a couple of companies who were paying just enough to extract clicks from side ads have indicated the change is for the worse and they have suspended their campaigns.

The natural alternative to paid search, organic search, is seldom discussed anymore as a realistic strategy these days, in part because the rankings might be rigged anyway.

One irony that’s pervasive in the online lending industry is that borrowers are being targeted offline where it’s potentially more affordable. In a discussion thread that garnered 76 posts last fall, ISOs and funders suggested that direct mail, referrals, UCCs, cold calling, radio and even going out and shaking hands, were pegged as “what’s next” for marketing. Pay-Per-Click was only mentioned once and only in the context of it being something that had long ago been made too expensive for small and mid-size companies.

The cost of making these things work might be why so many funders are hoping that brokers can figure it out. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” said Nulook Capital’s Jordan Feinstein in an interview with AltFinanceDaily last month.

With Google becoming even more competitive now though, perhaps United Capital Source’s Jared Weitz summed it up best. “Marketing is getting more expensive and only the ones who can afford to pay can play,” Weitz said.

Analytics Startup Gets $5 Million in Seed Round from Soros, Jefferies

March 14, 2016 Another day, another fintech round.

Another day, another fintech round.

George Soros-led Soros Fund Management and Jefferies Group invested $5 million in portfolio management and loan analytics platform, DV01 a New York-based startup that was founded in 2014 by Perry Rahbar, a former JP Morgan mortgage bond trader.

The platform advises investors on which loans to refinance through marketplace lenders like Prosper and Lending Club. Bloomberg reported that Soros had committed $2 million to the company in a separate round of financing.

As the marketplace for loans grows, so does the market to judge those marketplaces. Today, there are over a dozen startups working in big data analytics providing a wide net of services like forex trading portals, digital advisory platforms and social network for investors.

Specifically speaking of credit risk analytics, last year, PeerIQ secured $6 million in total funding from Morgan Stanley CEO John Mack and former Citigroup chief Vikram Pandit. But that is only a fraction of venture capital dollars. As far as funding goes, lenders are still the cream of the fintech crop where American fintech companies raised $7 billion over 351 venture capital-backed deals in 2015 with SoFi, Zenefits, Avant and Prosper Loans as frontrunners. This trend is likely to continue in the context of the recent IPOs in the industry. The noteworthy fintech IPOs like OnDeck, Lending Club and Square debuted with a bang but are struggling to find ground.

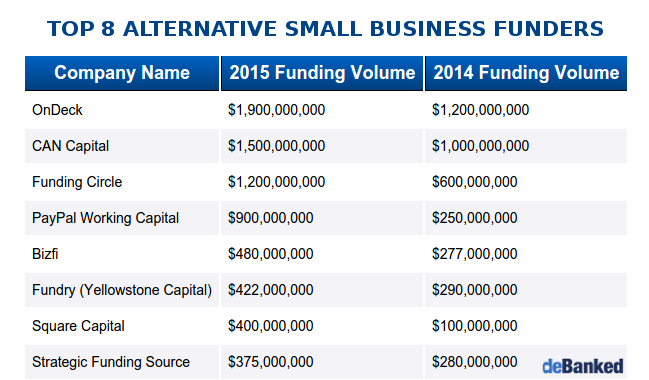

The Top 8 Small Business Funders

March 13, 2016Whether they do loans or merchant cash advances, here are the top 8 alternative small business funders:

This list originally appeared in a story about Square’s Q4 Earnings and has been republished individually here in case anyone missed it. The figures were either disclosed to AltFinanceDaily directly or are a best estimate based on publicly available materials. This list is not comprehensive and in instances where no reliable data could be obtained, the company was just omitted. A larger list will appear in AltFinanceDaily’s March/April Magazine issue so make sure you subscribe if you haven’t already.

Is Online Lending the Cream of the Fintech Crop?

March 10, 2016 American fintech companies raised $7 billion over 351 venture capital-backed deals in 2015 and leading the pack were online lenders like SoFi, Zenefits, Avant and Prosper Loans.

American fintech companies raised $7 billion over 351 venture capital-backed deals in 2015 and leading the pack were online lenders like SoFi, Zenefits, Avant and Prosper Loans.

A new report released by CB Insights and KPMG shows a record spike in VC-backed fintech deals, hitting $14 billion globally and making up 73 percent of all VC funding. The purview of fintech included companies in lending, payments, personal finance, bitcoin and equity crowdfunding.

In the U.S., the pack was led by marketplace lender SoFi raising over $1.35 billion, with SoftBank investing a billion in the San Francisco-based startup. Other noteworthy investments included $500 million into payroll service startup Zenefits, online lenders Avant and Affirm, which provide installment loans and credit scoring services.

Other Highlights

- Major corporations participated in one of every four fintech deals

- Investment in bitcoin and blockchain was up 76 percent annually

- 14 of the 19 fintech ‘unicorns’ (startups with a billion dollar valuation) were in lending and payments

- Citigroup (13 deals) and Goldman Sachs (10 deals) led investing in VC-backed fintech startups in the past four years.

- Top fintech companies of the year were Lending Club, Square and OnDeck Capital.

Yellowstone Capital Welcomed to New Office Location By City Mayor

March 8, 2016 It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

The company has officially relocated from 160 Pearl Street in Manhattan to 1 Evertrust Plaza in Jersey City. On their first day in the new location, Jersey City Mayor Steven Fulop made an appearance and posed for a photo with company executives Isaac Stern and Jeff Reece to celebrate their arrival. Aside from outgrowing the NYC office that they operated from for years, Yellowstone was wooed to the State by the New Jersey Economic Development Authority to create jobs in the area in exchange for a tax incentive. The hundreds of employees they bring with them to the neighborhood now will also serve to stimulate Jersey City’s burgeoning economy.

The company originated close to half a billion dollars in funding for small businesses in 2015.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. AltFinanceDaily was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. AltFinanceDaily was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

A clear view of NYC’s Freedom Tower from many of the floor’s windows assures them that they are not that far.