Par Funding, Receiver Continue to Spar Over Its MCA Business

December 18, 2020 “From inception through 2019, [Par Funding] incurred a cash loss from operations of $136.2 million.”

“From inception through 2019, [Par Funding] incurred a cash loss from operations of $136.2 million.”

That’s the conclusion reached by Bradley D. Sharp, CEO of Development Specialists Inc (DSI), the financial advisor to the Receiver appointed in the Par SEC case.

Par has scoffed at the Receiver’s analysis of its business. “We do not necessarily begrudge attorneys, whose skill sets are often in other areas, a potential inability to understand the math that often makes for a strong and profitable financial model,” Par’s lawyers wrote in an October court filing. “There is a reason that smart, mathematically inclined people are typically hired by banks, hedge funds and financial services firms. But the Receiver and his counsel’s inability to understand Par’s business has led to all manner of baseless accusations that are easily answered in the very documents they possess but do not understand…”

Par says it was profitable and walks the Court throught its mathematical process. Sharp says Par’s assessment “is misleading and does not reflect actual operations at the company.”

Sharp alludes to Ponzi-like characteristics but refrains from using that term. “From inception through 2019, [Par] paid $231 million to investors, consisting of principal repayments totaling $135.6 million and interest payments totaling $95.4 million. [Par] could not have made these principal and interest payments to the investors without additional funds from the investors.”

Par explained that the key to its business is in the compounding:

“The merchant funding model is profitable because merchant funding returns are reinvested, either in a new or different merchant, or in an existing merchant with adequate receivables as a consolidation, or as a refinance of a merchant which may already have MCA funding from another provider. And the reinvestment begins on the merchant funding returns which commence immediately and occur daily. In very simple form, the math works as follows. Assuming $10,000 is funded to a merchant pursuant to a funding agreement providing for a funding return of $13,000 over the course of 100 daily ACH withdrawals, the agreement would provide for repayment to begin immediately with daily payments of $130. As those monies are returned, portions are used to pay operating expenses, but most of the monies are re-invested to fund other merchants. Mathematically, this means that the original $10,000 is being used to fund more than one merchant. Over the life of a single $10,000 funding, that same $10,000 can be used to fund multiple merchants, all of whom are paying funding fees in excess of the principal amount received. Thus, the original $10,000, at a 1.30 factor rate, generates $13,000 on the first merchant cash advance (MCA). Those funds are reinvested and generate $16,900 on the second MCA, and $21,970 by the third MCA – an increase of $11,970 over and above the initial $10,000. And that can happen within a year. This is the powerful compounding effect of the financial model.

That is the simplest version of the model. In practice, the model is far more sophisticated than that because the leveraging to new merchants of the MCA returns begins as soon as the MCA payments come in.”

Par additionally said:

“At the conference on October 8, 2020, the Receiver’s counsel told this Court, and many investors, that out of $1.5 million received per day from merchants prior to July 28, 2020, $1.2 million was used for new MCA funding. Thus, according to the Receiver’s counsel, only $300,000 constituted net collections, about 20%. The Receiver’s counsel appears to be suggesting that the company is not holding on to receivables but, instead, is refunding the same merchants 80% of receipts. This proposition is wrong and its assertion shows that the Receiver and his counsel do not understand the MCA business.”

One could assess that a large element of this case consists of the Receiver being like, ha! well look at this! and Par responding, well, yes, that is actually how our business works.

In fact, that is precisely the angle Par took in defending its use of funding new deals with money collected from deals previously funded.

“First, the numbers show that collections are used to fund new MCA deals,” Par’s attorneys wrote. “This may come as a total surprise to the Receiver and his counsel, but funding merchants is the business of Par. That is like criticizing Ford Motor Corp. for using its car sales income to build and sell more cars.”

Both sides agree that Par advanced over $1 billion to small businesses but Sharp says that “reloads” distorted the numbers.

“Use of reloads escalates the obligations of the merchant as each reload adds an additional ‘factor’ along with any new funds advanced,” Sharp wrote. “In [one example the reloaded funds are] subject to the factor twice; once when the funds were originally sent and again when they are included in the reload advance. The use of reloads also significantly distorts the calculation of loss rates as the advances are simply refinanced without becoming a loss.”

Sharp concludes that the true end result for Par is a much higher default rate than it lets on to.

And then there’s this

Sharp has repeatedly brought attention to a list of merchants with unusual payment and funding activity. Par countered by saying there are good explanations for each.

Amongst all of this is that company insiders are alleged to have received tens of millions in payments from Par and the Receiver is confident, in part due to DSI’s report, that Par was majorly unprofitable.

“Based on our review to date, it is apparent that [Par] would not have been able to continue to provide payments to investors, or to continue to operate, without additional funds from investors,” Sharp wrote in a December 13th report.

This case is not the first rodeo for Sharp and DSI in the merchant cash advance business. They were also assigned to manage the 1 Global Capital case.

The case is ongoing. The Court recently approved a motion to expand the Receivership estate.

Canada’s Top Lending Leaders of 2021

December 16, 2020 The Canadian Lenders Association released its 2021 Leaders in Lending awards. The association is the voice of Canada’s lending ecosystem and represents more than 100 companies in commercial and consumer lending.

The Canadian Lenders Association released its 2021 Leaders in Lending awards. The association is the voice of Canada’s lending ecosystem and represents more than 100 companies in commercial and consumer lending.

All CLA members are vetted and accredited based on their corporate standards

and values. Their role is to support the highest level of lending in Canada,

servicing a wide spectrum of business and consumer borrowers’ growth requirements.

See previous year’s leading lending companies

See previous year’s leading lending executives

2021 Award Winners:

Lending Woman of the Year

|

Tiffany Kaminsky | Co-Founder of Symend

Tiffany Kaminsky is the co-founder of Symend, a fintech that uses analytics and behavioural science to create individualized debt recovery programs. The startup, which has offices in Calgary, Toronto and Denver, received USD $52 million in funding earlier this year and plans to hire up to 200 more roles in 2021. |

|

Nicole Benson | CEO of Valeyo

Nicole Benson is the President & CEO of Valeyo, a business solutions provider to financial institutions in Canada. Nicole drives every facet of business forward, with a focus on growing, evolving, and innovating Valeyo’s suite of solutions to meet the changing needs of its clients and the financial services industry. |

|

Andrea Fiederer | CMO of goeasy

Andrea Fiederer is EVP & CMO of goeasy, a leader in non-prime financial services with over 2000 employees. Andrea is responsible for goeasy’s overall marketing and brand strategy for both the easyhome and easyfinancial business units. |

|

Elena Ionenko | Co-Founder of Turnkey Lender

Elena Ionenko is the Co-Founder of Turnkey Lender, a loan origination platform. Under Elena’s leadership, the company has entered 50+ local markets, raised over $3.5 million in venture capital and launched regional offices all over the globe. |

|

Minal Shankar | CEO of Easly

Minal is the CEO of Easly, a SR&ED financing firm. This year Minal has doubled Easly’s capital under management & customer base. Prior to leading Easly, Minal was an investment manager for the VC firm Northgate Capital and an associate in the Technology Investment Banking group at J.P. Morgan Chase. Minal holds an MBA from the NYU Stern School of Business. |

Fintech Innovator the Year

|

Flinks

Flinks is a data company that empowers businesses to connect their users with the financial services they want. |

|

REPAY

REPAY is a leading provider of vertically-integrated payment solutions. |

|

VoPay

VoPay seamlessly connects you to the banking ecosystem enabling anyone to offer efficient and simple bank account payment processing. |

|

Fundmore

FundMore.ai is an automated underwriting system that uses machine learning to streamline the Pre-Funding process for loans. |

|

Provenir

Provenir offers a suite of risk analytics tools for lenders to make adjudication faster and simpler. |

Executive of the Year

|

Jason Mullins | CEO of goeasy

Jason Mullins is the President & CEO of goeasy, a leader in non-prime financial services with over 2000 employees. Since joining goeasy in 2010, Jason has helped the company scale to $1 billion in market capitalization with compound earnings growth of 28%. Jason is a recipient of Canada’s Top 40 Under 40 Award. |

|

Wayne Pommen | CEO of PayBright

Wayne Pommen is the CEO and Founder of PayBright, a Canadian leader in the BNPL space. His firm has partnered with 7,000 domestic and international retailers, and has approved over $1 billion in consumer credit. This year PayBright was acquired by Affirm in a $340 million transaction. |

|

Lawrence Krimker | CEO of Simply Group

At just 33 years of age, Lawrence Krimker has built Simply Group into a category leader in home equipment financing. This year his firm acquired competitors Dealnet & SNAP Financial in transactions that totalled over $750 million and brought his firm to $1.45 billion in assets under management. |

|

Andrew Graham | CEO of Borrowell

Andrew Graham is the CEO and Co-Founder of Borrowell, Canada’s first fintech to provide free credit monitoring. This year Andrew launched Borrowell Boost to help the 53% of Canadians living paycheck to paycheck meet their bill payments. |

|

Maria Soklis | President of Cox Automotive

In the 6 years that Maria Soklis has led Cox Automotive Canada, the company has become a category leader in software and financing solutions for consumers and dealers across the country. Maria has also left her mark with initiatives that promote diverse and inclusive workplaces, and this year signed the BlackNorth Initiative CEO Pledge. |

Emerging Lending Platform of the Year

|

Moselle

Moselle is a digital platform that simplifies the importing workflow for small medium business owners. |

|

Moves

Moves is a financial services platform for independent “gig” workers. |

|

Vendor Lender

VendorLender is Canada’s first POS lender for dealers in the equipment finance space. |

|

Lendle

Lendle is Canada’s first interest free credit provider. |

|

goPeer

goPeer helps everyday Canadians to achieve financial freedom through Peer-to-Peer Lending |

Small Business Lending Platform of the Year

|

Merchant Growth

Merchant Growth is a leading Canadian financial technology company that specializes in small business financing. Over the past decade, Merchant Growth has supported Canadian businesses with hundreds of millions of dollars in growth financing. |

|

Loop

Launched this year, Loop builds credit & payment products specifically for online merchants. The company is operated by the LendingLoop team that popularized P2P lending in Canada. |

|

Thinking Capital

Thinking Capital is one of Canada’s best known fintech lenders to the small business sector. This year the firm has forged relationships with multiple Credit Unions and hit $1 billion in loans deployed. |

|

OnDeck

Since its launch in 2015, OnDeck Canada has |

| Clearbanc

Canadian based Clearbanc is the world’s largest e-commerce funder. Their data-driven approach takes the bias out of decision making. Clearbanc has funded 8x more female founders than traditional VC. |

Consumer Lending Platform of the Year

|

Flexiti

Flexiti is a leader in point of sale financing for retailers and has been named one of Canada’s fastest growing companies two years straight. |

|

CHICC

CHICC is one of the country’s leading rental & homeimprovement financing companies. |

|

Marble Financial

Marble uses fintech to empower Canadians to improve their credit score, manage debt, and budget to achieve financial goals. |

|

PayBright

PayBright is one of Canada’s leading buy now, pay later providers. This year the firm was acquired by BNPL giant, Affirm for $340 million. |

|

goeasy

Canada’s leading alternative financial services provider servicing non-prime Canadians through its easyhome and easyfinancial divisions. |

Auto Lending Platform of the Year

|

GoTo Loans

GoTo Loans is a fintech lender focused on helping consumers access the equity from their vehicle and the leading provider in Canada for automotive repair loans. |

|

Auto Capital Canada

AutoCapital Canada is a national auto finance company that works with dealer partners to help clients finance the purchase of new and used vehicles. This year the firm acquired competitor Rifco. |

|

Carfinco

The Western Canada based lender is a leader in non-prime lending to the auto sector. |

|

Canada Drives

Canada Drives is a leader in fintech auto lending. This year the firm hit over 400 employees and 1 million transactions, servicing consumers across Canada, the US, and the UK. |

|

Clutch

Clutch aims to bring speed and convenience to used car sales by taking the experience completely online. The fintech raised a $7 million round this year from Real Ventures. |

Technology Lending Platform of the Year

|

BDC

Launched only five years ago, BDC’s Tech Group has become a leader in lending to Canadian technology entrepreneurs. |

|

TIMIA

TIMIA is a specialty finance company that provides growth capital to technology companies in exchange for payments based on monthly revenue. |

|

Flow Capital

Flow Capital Corp. is a diversified alternative asset investor, specializing in providing minimally dilutive capital to high-growth businesses. |

|

Venbridge

Venbridge is a Canadian finance company offering non-dilutive venture debt, SR&ED financing, and tax credit consulting services. |

|

SVB

SVB has lead the technology lending movement for 35 years. The firm opened their first Canadian office last year. |

Lawyers Chime in On What a Biden Administration Could Mean for Merchant Cash Advance

November 30, 2020 In the weeks following the election, the news cycle has been heavily focused on the presidential transition’s legal aspects.

In the weeks following the election, the news cycle has been heavily focused on the presidential transition’s legal aspects.

Instead of worrying about vote recounts, merchant cash advance (MCA) companies are considering what legal changes, if any, might come after Jan 20th. Will the Biden administration spell the beginning of new regulations on the world of business to business financing?

Lawyers say that while the industry is waiting on Georgia to decide the Senate’s fate, increased regulation at the federal is unlikely to occur.

“If the Republicans hold in Georgia, and we have a split legislative branch, that means gridlock, and gridlock is great for the industry,” Catherine Brennan, partner at Hudson Cook, said. “The more progressive wing of the Democratic Party would like to put merchant cash advance under the auspices of quasi-consumer [loans,] but they won’t be able to do that with the split legislative branch.”

Brennan has a wealth of experience as a commercial finance compliance and litigation lawyer and regularly contributes to the national conversation on alternative and fintech law topics. She said that even if Democrats control the Senate, moderates may still hold back progressives from making new regulatory laws.

“There’s some moderate Democrats who understand the need for this market, they understand the product, and their constituents, in particular, use the product,” Brennan said. “I don’t see anything at the federal level that should be viewed as an existential threat to the ongoing existence of the industry.”

What Brennan does see as more likely, is the gradual adoption of MCA under preexisting executive agencies like the CFPB and FTC. She pointed to the Dodd-Frank Act implementing consumer lending data collection as a possible avenue regulators might take by pushing for data collection in the MCA space.

What Brennan does see as more likely, is the gradual adoption of MCA under preexisting executive agencies like the CFPB and FTC. She pointed to the Dodd-Frank Act implementing consumer lending data collection as a possible avenue regulators might take by pushing for data collection in the MCA space.

Still, Brennan insists that MCA firms will be OK so long as they understand the FTC can already look into commercial finance practices and that it has gone after ISOs in the past. She sees that as the number one development from a regulatory standpoint because the FTC will ultimately review what took place in the financial service markets during the pandemic and decide if action is warranted. Still, if funders have been responsible and fair, they should be in a good place.

Brennan did say that the position might be up for grabs when it comes to the head of the CFPB. The previous leader, Richard Cordray, fought with the Trump administration against his re-appointment, believing his position surpassed the president’s authority to fill. Of course, it did not, and Cordray was removed, but there is nothing stopping the Democrats from re-appointing him, Brennan said, especially when other appointees may give up valuable Congressional seats.

James Huber, a partner at Global Legal Law Firm specializing in collections, believes that even if the Senate is somehow blue and passes regulation, that MCAs that are playing by the rules would benefit. The MCA business was born under the Obama administration during the last financial crisis, and if Biden beefs up the CFPB, it would only hurt payday lenders, Huber said.

“It certainly flourished under Obama, so one might think now that it’s got its foothold and it’s here you can almost guarantee that it’s going to continue to do really, really well when there’s stricter regulation,” Huber said. “Your typical AltFinanceDaily cash advance technology company: I think they’re going to do well with their bread and butter product…”

Huber said that especially when we’re seeing businesses hurting for cash right now, b2b finance will thrive. Huber was worried about Biden’s talk about bankruptcy reform, however.

“Biden’s talked about bankruptcy reform, to make it easier for people to go through bankruptcy, and yield assets like their houses and their cars and things that,” Huber said. “That’s a concern; that would mean that you’re fraudulently applying for a loan, and that’ll be accepted. It slows down collection efforts; our main role in the MCA business is on [defaults].”

Katherine Fisher, a Hudson Cook partner who, alongside Brennan, has deep experience in MCA representation and compliance, agreed with her colleague that funders need to make sure they keep an eye open toward compliance when it comes to regulation.

“Firms that have not focused on the regulatory process need to start, and companies that have looked at it need to revisit it,” Fisher said. Funders should “expect to be comfortable if they are asked to describe how they comply and prepare to do so.”

But beyond that, she sees no doomsday event on the horizon; even if the Senate is no longer Republican-controlled, it would be up to the FTC and CFPB to set the tone. If the CFPB, for example, pushed for data collection under 1071 of the Dodd-Frank Act, it might signal a more attentive regulatory environment for MCA and factoring.

But beyond that, she sees no doomsday event on the horizon; even if the Senate is no longer Republican-controlled, it would be up to the FTC and CFPB to set the tone. If the CFPB, for example, pushed for data collection under 1071 of the Dodd-Frank Act, it might signal a more attentive regulatory environment for MCA and factoring.

Compared to 2008, when the last Democratic administration took office, MCA wasn’t on the radar, Fisher said. Now that it is on the map this time around, especially after MCA funders proved how vital they were to the SMB market during the pandemic, there will be more attention on B2B transactions.

But firms only need to think of this as a chance to make sure their practices are healthy, and most of the industry has already shown signs of doing so. Fisher pointed to the FTC’s small business finance forum last year, which included a panel of MCA representatives at the table.

“I don’t think it is a scary time. It’s an opportunity for MCA to improve their processes, make sure they are following the law,” Fisher said. “They don’t need to be afraid but need to batten down. Much of the industry has already done that, the MCA industry has been focused on adopting good practices.”

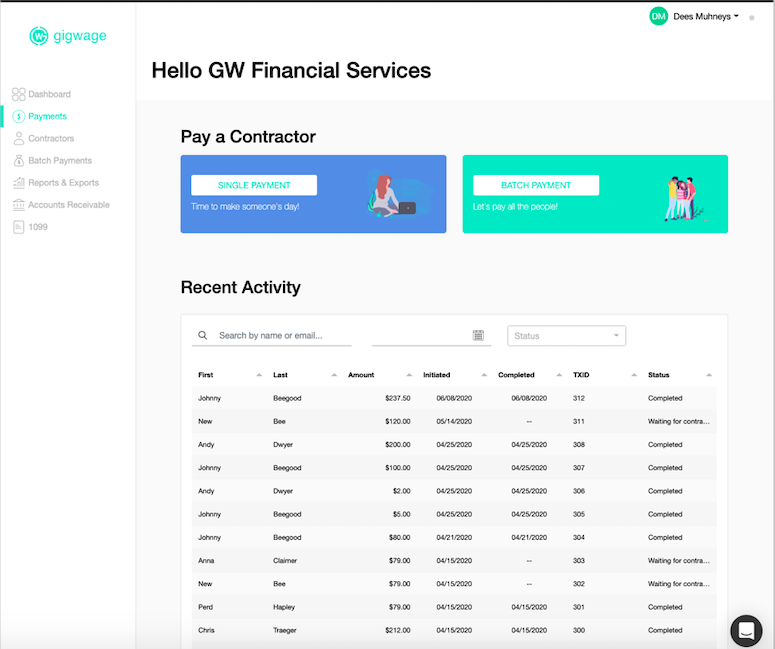

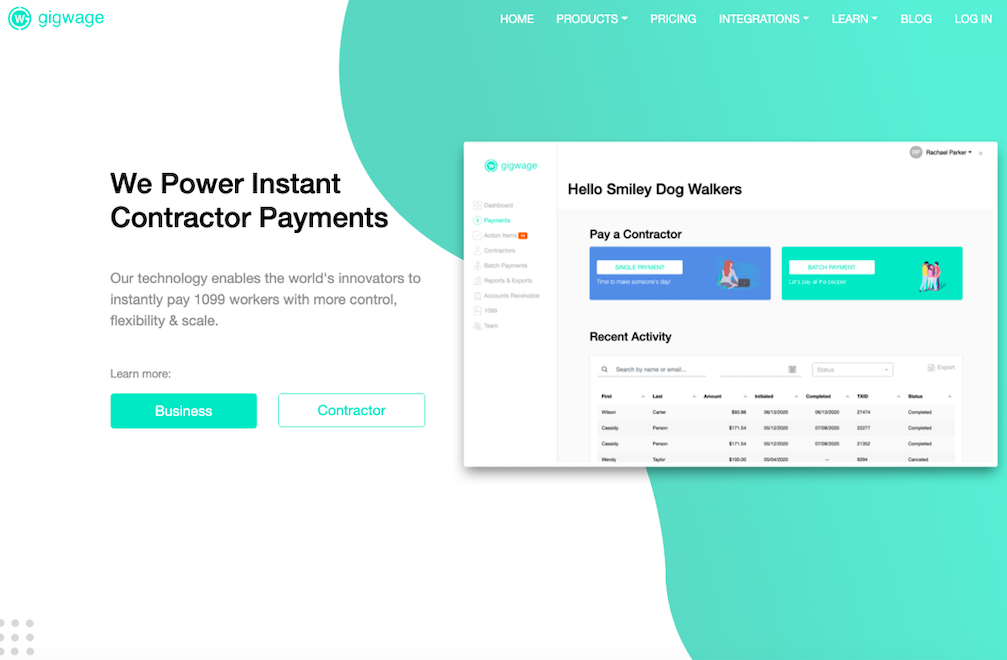

From Sales to Founder: Craig J. Lewis Talks Gig Wage’s $7.5 Million Funding Round

November 27, 2020 Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Coming to you from the heart of Dallas, Texas is a digital payroll startup, Gig Wage, that received a $7.5 million Series A funding round just last month. The founder, CEO, and writer of The Sport of Sales, Craig J. Lewis, talked about his goal to make it easier for 1099 gig workers to get paid.

Lewis made $10 million in payroll tech sales before going on to lead a firm that has seen 30% month-to-month growth this year, during a pandemic no less.

“We help businesses pay independent contractors, but because we’re so tech-centric, it’s evolved beyond just payroll,” Lewis said. “What we ended up building was financial infrastructure for the modern workforce. We help businesses get money from their customers to their contractors as fast and as flexibly as possible.”

The way Gig Wage does this, Lewis said, is by offering an online platform for the hybridization of payroll, payments, and banking from a single login. Businesses can manage their payroll needs for 1099 workers, then shift to payment needs quickly, through direct to debit, all major cards, bank transfers, and accounts receivables.

“One of the only- the only platform in the world actually that has embedded banking into payroll and payments, which is what kind of allows for this speed and flexibility that we offer,” Lewis said. “We’re like B to B to C: We help the businesses with technology and operational excellence, and because independent contractors are separate from the workplace, we provide tools for them.”

Lewis has years of experience in the payroll space- starting as a salesman for ADP small business payroll products back in 2008. Realizing he had a passion for payroll tech and getting customers the best services possible, Lewis went on to learn anything he could about the industry. Selling $10 million in software while moving across the country, Lewis landed in Silicon Valley, where he studied what it took to start a company.

“I was just awed how they thought about technology and products and company building,” Lewis said. “And I vowed to bring that to the payroll industry.”

Lews joined a startup, learned the Silicon Valley way of creating a company through an African American tech acceleration program. In 2014, Lewis founded Gig Wage to do something disruptive in the payroll space.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

As Gig Wage attests, disruption is what the 1099 gig industry needs at the very least. Lewis believed the gig economy was going to keep growing when Gig Wage started. As he watched, the gig economy ballooned into a $2 trillion industry with an estimated 65-75 million person workforce. These workers suffer from an outdated payroll system, losing an estimated 2-20% of their income to flaws in the payments system Gig Wage found.

“With the maturation of Uber, Lyft, Postmates, Doordash, Grubhub, Upwork, all of these kinds of gig economy freelancer companies, we had great growth going into 2020,” Lewis said. “In Q1, we were set up to raise our series A, and then March happened, and the terms got pulled off the table.”

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

But when the dust settled after those first shutdown weeks, Gig Wage looked at the damage and found the skyrocketing unemployment rates and furloughs had only accelerated their growth as a company.

“The gig economy was right there waiting on the workforce to provide opportunities to earn, and we were positioned perfectly to help people compete for that talent and pay people in a modern way,” Lewis said. “The pandemic has been a huge growth accelerant for us, and we think those tailwinds will only continue.”

Those winds of success came during a time of protest. Amplified in the pandemic’s backdrop, the country was waking up to the unequal disenfranchisement black people faced. Only 1% of black founder entrepreneurs ever receive VC funding, and Lewis said he is proud to have raised a significant round, given that unfair stat.

“With so much controversy and negative energy around black people in general,” Lewis said. “I think putting this positive story out there and showing this black excellence, black tech, I think it’s super important, and it’s been something that I’ve embraced. We’ve been able to be a part of putting something extremely powerful and positive into the market.”

America is finally waking up to realize something Lewis said was obvious, that black people matter, even though it can be controversial to say so. He hopes his success can help others but affirms the funding round was no charity drive.

“This is a great opportunity for us to be clear about the fact that like hey, we’ve been working on this, we’ve built a good business and a good technology,” Lewis said. “This is a big business opportunity for our investors and us. It wasn’t charity, right: This isn’t like, oh he’s black, give him some money.”

The successful funding round shows confidence in the Gig Wage platform from Green Dot, which will allow Gig Wage to offer bank accounts and debit services to independent contractors. Green Dot is one of the only fintechs with a national banking license, Lewis said, and Gig Wage is joining the Banking-as-a-Service direction that the fintech industry is headed.

Beyond payroll, Lewis can’t wait to offer other financial products to businesses as the company grows.

“When you think about the gig economy, it’s important that people get paid fast and flexibly: You’ve got to have the cash to be able to do that,” Lewis said. “We see some unique opportunities to get involved in the lending space down the line as well as we continue to build out our technologies.”

New York Commercial Finance Disclosure Bill Update

November 10, 2020 The controversial commercial finance disclosure bill that passed in New York in July, has still not been signed by Governor Cuomo.

The controversial commercial finance disclosure bill that passed in New York in July, has still not been signed by Governor Cuomo.

Technically, the governor only had 10 days to sign it while the legislature was in session and only 30 days to sign it when the legislature closed out its session for the year, which it did in July. Both deadlines have passed. But as AltFinanceDaily learned in the case of the COJ bill, the clock does not actually begin to tick until the legislature has formally “delivered” the bill to the governor.

That puts the disclosure bill and other bills not yet signed in a state of suspended animation that can carry them through until December 31st. Doing this “is done to ensure that legislation is thoroughly vetted, with extra checks to guarantee that bills are not unconstitutional and that they’ll lead to no previously unforeseen consequences.”

It’s that latter part of that, that has created concern. Even dueling small business lending trade associations disagree on what the consequences will be. The Innovative Lending Platform Association (ILPA), for example, say the bill is almost exactly what they wanted, while the Small Business Finance Association (SBFA) suggests that advocates do not even understand the bill, much less the implications.

ILPA’s CEO, Scott Stewart, told AltFinanceDaily in July that “the implications are that small businesses, certainly in New York to begin with, but we think throughout the country, will have the opportunity to really see, understand, and compare various different sources and products for financing their small businesses in terms of their expansion and success.”

SBFA’s Executive Director, Steve Denis, meanwhile, responded very soon after by saying that they don’t realize that it will subject them to massive liability and hefty fines.

“We’re for disclosure, we think there should be standard disclosure,” Denis said. “Our message to the Governor’s office is ‘Let’s take a step back.’ The Department of Financial Services needs to look at our industry, they need to get to know our industry. They are the experts that understand the space, they understand disclosure, and they understand what they need to do to bring responsible lending to New Yorkers. And we would like to work with the NYDFS and a broader industry to put forward a bill that’s led by the Governor and the Governor’s office that brings meaningful disclosure and meaningful safeguards to this industry.”

The SBFA later published the results of a study that supports their arguments.

In qualitative testing of 24 small business owners and executives who have experience taking commercial loans, the study concluded participants did not understand what APR was.

APR disclosure, of course, is the centerpiece of the entire bill.

It is still possible the bill’s language could be amended before the governor signs it. It’s happened before.

In 2017, for example, the state legislature passed a bill that would establish a 7-person task force to analyze online lending activity in the state. The bill, dubbed the Online Lending Task Force bill, called for industry participants to serve on it. The final version signed by the governor, however, was completely rewritten to the point that the online lending task force bill had completely eliminated the task force portion of it and no one was allowed to participate in any analysis except for NYDFS.

StreetShares Stops Lending Directly to Small Businesses, Records $10.7M Annual Loss

November 1, 2020 StreetShares, the online lender known for its focus on veteran-owned businesses, is no longer lending directly to small businesses, the company disclosed last week. This became effective as of October 26.

StreetShares, the online lender known for its focus on veteran-owned businesses, is no longer lending directly to small businesses, the company disclosed last week. This became effective as of October 26.

“We still offer lending products to small business customers via our LaaS clients,” the company said however.

“As of June 30, 2020, 47 banks, credit unions, and alternative lenders have contracted to use our Lending-as-a-Service (LaaS) small business financing technology.”

It defined LaaS as:

“Since the launch of LaaS, the Company has offered several LaaS packages, which include various products and services depending on the package, such as: online product presence for small business lending, web design collaboration, client-branded landing page, intelligent online loan application for small business borrowers (client-branded or StreetShares-branded), decisioning platform, loan analytics platform, and small business loan marketing services. Depending on the LaaS package, either the Company or the LaaS client will originate, underwrite, and service the small business loans. Our LaaS products and services are available in all 50 states and the District of Columbia.”

Financially, StreetShares’ June 30 fiscal year-end report revealed a massive $10.7M loss on only $4.5M in revenue. Despite the impact of covid, these figures are actually in line with (and perhaps even better than) historical performance. The company had a $12.3M loss on only $4.4M in revenue for the fiscal year prior, for example.

“Beginning in March 2020, we experienced an increase in late payments and requests from our borrowers for payment deferments. As a result, there has been an increase in predicted losses on our loan portfolio and we expect to observe an increase in our charge-off ratio in the near-term; however, we are unable to predict a long-term trend in our charge-off ratio. Beginning in March 2020, we instituted a deferment program that permitted our small business borrowers to defer loan payments as necessary due to the COVID-19 pandemic. We worked closely with our borrowers and have exited all of them from the deferment program as of this filing. We also provided, and continue to provide, certain borrowers with payment plans with reduced payments as necessary. The payment deferments or modifications made as a result of the COVID-19 pandemic consisted of short-term payment deferrals or reduced weekly payments.”

Earlier in the month of October, StreetShares announced they had secured a $10 million round of funding from Motley Fool Ventures, Ally Ventures (the strategic investment arm of Ally Financial), and individual fintech angel investors.

The OnDeck Roller Coaster of 2020

October 30, 2020 “2019 was an important year for OnDeck and we finished strong,” said OnDeck CEO Noah Breslow in the year-end earnings call that took place on February 11, 2020. “Financially, we had our second full year of profitability. And strategically, we are making significant progress positioning the company for improved performance and even greater long-term success.”

“2019 was an important year for OnDeck and we finished strong,” said OnDeck CEO Noah Breslow in the year-end earnings call that took place on February 11, 2020. “Financially, we had our second full year of profitability. And strategically, we are making significant progress positioning the company for improved performance and even greater long-term success.”

OnDeck reported net income of $28 million for 2019 and its share price closed at $4.07 the day earnings were announced, giving it a market cap of roughly $240 million. This was down significantly from its IPO value of $1.3 billion, but up from the lows it had hit in 2017 and 2019.

Over the next 30 days, however, the price fell by 50% on fears that the looming novel coronavirus could cause catastrophic disruption. The company also announced the departure of its Chief Accounting Officer.

As the industry looked on with wonder, news coming out of the company seemed strangely at odds with reality. For example, OnDeck announced a “first-ever” NASCAR sponsorship on March 10th.

“OnDeck is proud to sponsor the JR Motorsports team and driver Daniel Hemric for races during the 2020 NASCAR Xfinity Series season,” said a senior vice president of marketing at OnDeck. “So many of our small business customers are avid motorsports fans and we look forward to joining them to cheer on Daniel and the No. 8 car decked out in OnDeck colors at the Atlanta 250 and the Chicago 300.”

“OnDeck is proud to sponsor the JR Motorsports team and driver Daniel Hemric for races during the 2020 NASCAR Xfinity Series season,” said a senior vice president of marketing at OnDeck. “So many of our small business customers are avid motorsports fans and we look forward to joining them to cheer on Daniel and the No. 8 car decked out in OnDeck colors at the Atlanta 250 and the Chicago 300.”

On March 23, OnDeck closed at 70 cents. The market, it seemed, valued OnDeck at a paltry $41 million.

Publicly, OnDeck kept up the optimism. The company applied to be a PPP lender as the program was just beginning to roll out. “We are excited to be one of the fintechs delivering PPP loans as a direct lender,” Breslow said. “Our team has been working around the clock getting us ready and now we wait and hope we are approved soon!”

Publicly, OnDeck kept up the optimism. The company applied to be a PPP lender as the program was just beginning to roll out. “We are excited to be one of the fintechs delivering PPP loans as a direct lender,” Breslow said. “Our team has been working around the clock getting us ready and now we wait and hope we are approved soon!”

Simultaneously, the company suspended the funding of its “Core” loans and lines of credit to new and existing customers. The company then went on to report a Q1 net loss of $59M due to covid-related damage, wiping out all of its 2019 profits and more. It also furloughed many employees while reducing the pay for those that stayed on.

That same month, OnDeck’s management “commenced a review of potential financing options to secure additional liquidity and potentially replace [its] corporate line facility and began contacting potential sources of alternative financing, including mezzanine debt.”

The response it got was grim.

“The interest rates offered by those alternative financing sources ranged from 1-month LIBOR plus 900 basis points to 1,700 basis points (in addition to an upfront fee) and all but one required a significantly dilutive equity component,” the company later disclosed. “The one proposal that did not include an equity component was at an interest rate of 1-month LIBOR plus 1,400 basis points to 1,700 basis points.”

“The interest rates offered by those alternative financing sources ranged from 1-month LIBOR plus 900 basis points to 1,700 basis points (in addition to an upfront fee) and all but one required a significantly dilutive equity component,” the company later disclosed. “The one proposal that did not include an equity component was at an interest rate of 1-month LIBOR plus 1,400 basis points to 1,700 basis points.”

OnDeck engaged in negotiations with four potential sources of alternative financing, but two dropped out as the economic effects of the pandemic worsened. At the same time, it was speaking with Enova about something else entirely, a potential merger.

On the frontend, OnDeck was keeping the public abreast of its negotiations with creditors. The pandemic had put them in a technical breach of its terms with several of them but the company was experiencing some success with securing workouts and reprieves.

Regardless, the stock continued to trade below $1 as the world looked on to see what would become of their Q2.

On July 28th, bombshell news broke. Enova, an international lending conglomerate, announced it was acquiring OnDeck for the price of approximately $90 million.

On July 28th, bombshell news broke. Enova, an international lending conglomerate, announced it was acquiring OnDeck for the price of approximately $90 million.

“Following an extensive review of our strategic options, we believe this is the right path forward for our customers, employees, and shareholders,” Noah Breslow said on a call with Enova executives the following day.

Some shareholders had a different opinion and thought that the deal and the terms looked a little fishy, all considered. Nine different shareholder lawsuits were filed over the next two months with the intent to delay or block the acquisition.

How could this possibly be the best deal or the right path?!

That was the underlying question being posed between the lines of the various claims asserted. OnDeck ultimately settled with all the parties by releasing supplemental information to the public about its financial situation and thought process that led up to the Enova merger. All the objections appeared to fade as shareholders approved the deal by an overwhelming majority.

On October 13th, Enova announced that it had completed the acquisition of OnDeck.

But by that time, was OnDeck merely a hollowed out shell of its former self? Not quite, according to disclosures made two weeks later. Enova announced that OnDeck’s portfolio performance was already exceeding their expectations.

“On the small business side, the makeup of the demand is surprisingly similar to a year ago,” said David Fisher, CEO of Enova. “You would expect so many differences given what the economy has been through but there’s actually very very few. It’s pretty broad based. Credit quality look really really strong. If anything it’s stronger- I think it’s the stronger businesses that are trying to borrow at this point that are trying to lean into covid, not the ones that are just trying to survive so if anything on the demand there is a slight improvement on credit quality in small business.”

“On the small business side, the makeup of the demand is surprisingly similar to a year ago,” said David Fisher, CEO of Enova. “You would expect so many differences given what the economy has been through but there’s actually very very few. It’s pretty broad based. Credit quality look really really strong. If anything it’s stronger- I think it’s the stronger businesses that are trying to borrow at this point that are trying to lean into covid, not the ones that are just trying to survive so if anything on the demand there is a slight improvement on credit quality in small business.”

Fisher was also bullish going forward. “We believe now is a great time to be increasing our presence in

small business lending. The pandemic has devastated many small businesses across the country. Their

revenues are down and small business owners are digging into their savings to survive until the pandemic subsides and the economy reopens.”

Enova reported monster quarterly earnings of $94 million, a company record.

“Together Enova and OnDeck will be well positioned to further support small businesses and consumers in the wake of the pandemic,” Fisher said.

Lufax, a Chinese Online Lending Marketplace, to IPO on NYSE Next Month

October 27, 2020 Lufax, an online lending marketplace and one of China’s largest fintech companies, plans on going public by the end of the month on the New York Stock Exchange. Lufax is one of the multiple Chinese fintech companies grappling for a public offering amidst increasing tension between U.S. and Chinese markets.

Lufax, an online lending marketplace and one of China’s largest fintech companies, plans on going public by the end of the month on the New York Stock Exchange. Lufax is one of the multiple Chinese fintech companies grappling for a public offering amidst increasing tension between U.S. and Chinese markets.

Offering an online shopping mall for financial products, Lufax connects borrowers to various lending products supplied by traditional and alternative investors alike. Lufax was one of the largest, if not the largest P2P lender in China just two years ago before a major crackdown on the P2P industry forced the company to revamp completely.

Lufax plans to issue 175 million shares that will be priced from $11.5 to $13.5 each, according to a prospectus with the U.S. Securities and Exchange Commission last week. This would net the company around $2.36 billion.

The IPO would give the company around a $30 billion in valuation, lower than the $39.4 billion valuation it received in 2019 from a major backer Ping An Insurance Group.

Lufax reported more than $1 billion of profit in the six months up to June 30th, according to the filing. Last year, the firm’s assets dropped by 6.1% after a 30% reduction in transaction volumes. This was a cut of nearly all P2P transactions, in compliance with regulation from the Chinese government.

After the P2P industry grew unchecked for a decade, fraud concerns bloomed into outrage as hundreds of platforms covering hundreds of billions of dollars defaulted. According to Mckinsey, from 2013 to 2015, fintech firms offering P2P products exploded from 800 to more than 2,500 companies. More than 1,000 of these firms began to default on their debt, ballooning to an outstanding loan value of $218 billion in 2018.

In response to protests, outrage, and stadiums of helpless borrowers trying to gain their funds back from Ponzi schemes, the Chinese government cracked down hard on fraudulent firms. According to Reuters, regulators placed every P2P firm on death row, stating in 2019 that the industry had two years to switch to “small loans.” The shutdowns have cost Chinese investors $115 billion, according to Guo Shuquing, China Banking Regulatory Commission.

Pivoting away from these shutdowns, Lufax and many firms like Alibaba funded Ant Group are switching to lending marketplaces. Lufax works with 50 lending providers that hold $53 billion in assets as of June. Lufax believes that there are trillions of dollars in the untapped alternative finance market in China.