AltFinanceDaily Announces SPAC

April 1, 2021April Fools 2021

deBanked employees were summoned to an all-hands meeting in the company’s modest Brooklyn, NY headquarters yesterday afternoon to bear witness to a special announcement.

deBanked employees were summoned to an all-hands meeting in the company’s modest Brooklyn, NY headquarters yesterday afternoon to bear witness to a special announcement.

“We’re launching a SPAC,” AltFinanceDaily president and chief editor Sean Murray said to a stunned room. “I’ve been writing about fintech for more than ten years, but an inspirational meme posted by a bot on twitter got me thinking. And I was just like, ‘You know what? F*** it, let’s just buy the whole fintech industry.'”

Everyone quickly agreed that it was a genius move.

“What was the last stimulus? like what, $1.9 trillion or something? We’ll raise at least 10x that amount in our IPO,” he continued. “No financial technology company is off limits, we’re going to buy them all. I can’t believe no one has thought of this yet!”

Murray realized that such a brilliant strategy was likely to rattle the largest banks and he said that he had already placed calls to Jamie Dimon at JPMorgan and David Solomon at Goldman Sachs to ease them into his swift rise to financial power.

“I mean did I actually speak to them? Technically per se not really, but I heard them speak on Clubhouse of which I am an elite exclusive member,” Murray said.

When pressed for details about this Clubhouse conversation, Murray backpedaled and said he actually just read an article about Clubhouse but that the article referenced Elon Musk and that he was basically just as important as the famed bankers. Several sources who wished to remain anonymous said that Murray was only invited to Clubhouse after shamelessly begging for an invitation on twitter.

Attempts to verify his membership revealed a profile picture where he is giving a thumbs up while holding a glass of scotch, one of which he said came from a bottle that cost more than I would ever make in my whole life. A fact check, however, revealed that it was really just expired apple juice that a building maintenance worker had left out near the common area garbage disposal.

When asked to explain this, Murray said, “Bro, why do you think we’re doing a SPAC? Once we have the money, we’ll be drinking freaking Apple computers!”

By the end of the big company meeting, Murray pulled out a joint and began puffing it furiously through a mouth hole he cut open in his 7 simultaneously-worn covid masks, prompting one staff member to ask if his fanciful plan was at all related to New York’s newly enacted marijuana law.

“Wait, you mean this sh*t’s legal now?” he asked. “F***, make it two SPACs then!”

April Fools 🙂

Square Officially Becomes a Bank

March 2, 2021 Square launched its own industrial bank Monday, after receiving a charter from the FDIC. The Salt Lake City, Utah-based bank will begin underwriting business loans under the Square Financial Services title.

Square launched its own industrial bank Monday, after receiving a charter from the FDIC. The Salt Lake City, Utah-based bank will begin underwriting business loans under the Square Financial Services title.

“Bringing banking capability in-house enables us to operate more nimbly,” CFO and Chair of the new bank Amrita Ahuja said, “which will serve Square and our customers as we continue the work to create financial tools that serve the underserved.”

Square had previously offered credit products through a partnership with Utah-based Celtic bank. The move answers the questions “buy or build” when it comes to fintech banking. Many fintech firms, some of who even claimed to be anti-bank alternatives, have made the switch to either partnering with a nationally chartered bank or outright becoming a bank themselves.

“We thank the FDIC and Utah DFI for their partnership enabling us to reach this milestone, and look forward to continuing to expand access to financial services at this critical time for small businesses,” Ahuja said.

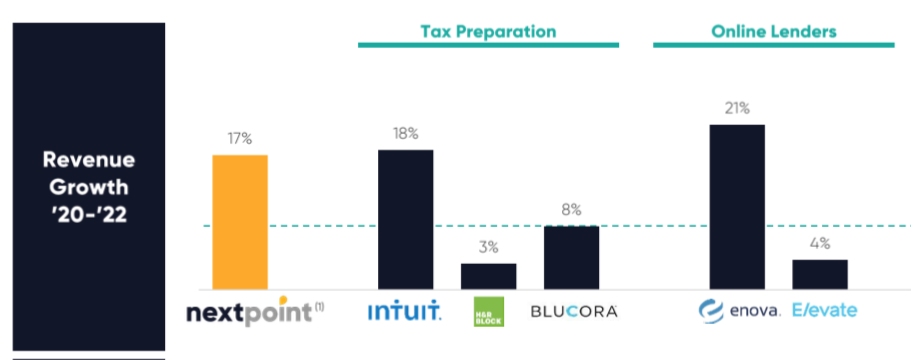

LoanMe, Liberty Tax Merger to Take on Intuit, Enova

February 22, 2021NextPoint Financial will combine LoanMe’s business, consumer, and mortgage lending with Liberty Tax’s tax preparation business, according to merger announced on Monday. Liberty’s “2,700+ locations in the US and Canada” will become consumer and SMB loan shops.

The new firm will also offer Merchant Cash Advances; LoanMe launched MCA funding in January and expects to fund $15 million in MCAs in 2021. Based on the acquisition prospectus, NextPoint will be a tax readiness firm, with the added suite of financial products as a value and growth builder.

Ramping up consumer, installment, and MCA lending, paired with the third-largest tax-prep business in the U.S, NextPoint expects to compete directly with Intuit, H&R Block, Enova, and Elevate.

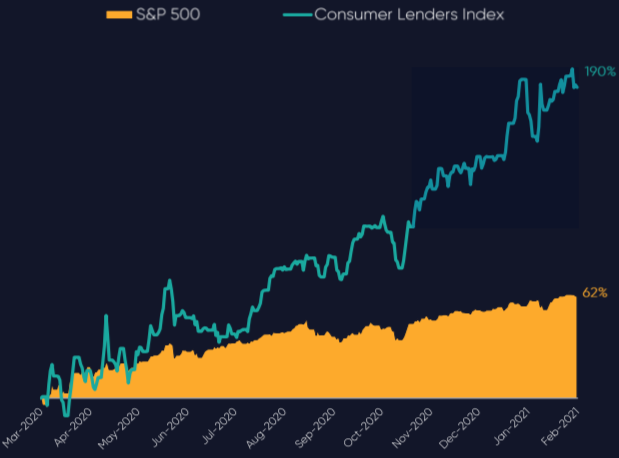

Fintech firms are setting themselves apart from the competition as one-stop shops for everything a business needs, including MCA products. Why branch into financial services now? NextPoint found that this year alt lenders have outperformed the S&P500 three times over.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses,” the investor presentation reads. “To get to the next point in their financial futures.”

Intuit offers a variety of financial products, like business loans through Quickbooks Capital, alongside their popular, 60%+ market share of tax prep software. H&R began offering small $1,000 lines of credit this year, but not much more.

The team leading the new company, NextPoint Financial, will feature execs like Brent Turner as CEO, Mike Piper CFO, both keeping their previous Liberty Tax positions. Jonathan Williams, former president and founding shareholder of LoanMe, will become president of lending.

Why Funders Are Investing in Real Estate As Their Side Hustle of Choice

January 25, 2021

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

At that point, Ribeiro’s fledgling company still wasn’t generating much revenue. “I thought, ‘Man, I just can’t get a lot of loans done right now. I only have three or four employees.’ That’s how I got into the real estate industry.” Twelve years later and at the height of a global pandemic, Ribeiro is simultaneously running two thriving ventures —US Business Funding, and a portfolio of hundreds of rental properties he now owns.

At a time when fintech startups and other industry innovators are looking for investors, alternative lending execs like Ribeiro are instead choosing to put their money in real estate to beef up their investment portfolios. Although some execs shy away from talking publicly about their real estate dealings, citing the fact that they don’t want too much exposure, the consensus is that there’s a lot of money to be made in buying, selling and renting property – if you know what you’re doing.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

To Ribeiro, real estate offers a few major advantages: It’s a tangible asset. You can leverage it as it appreciates in value. Deductions make it so you pay very little in taxes. And it offers significant cash flow. “It’s the best investment you can make,” he says.

What makes real estate an especially good fit for alternative lending and fintech execs is that they possess the skills, resources and financial literacy to succeed at it.

“Real estate is a long-term gain,” Ribeiro says. “The industry we’re in is a cash-flow cow. People who are doing well are printing money. But what can you do with that money? You can put it in the stock market, but you won’t control much. Then you pay capital gains on it.”

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

“If you’re a cash advance guy and COVID happened, then you’re not doing very well,” he says. “If you diversified your assets by doing real estate and cash advance, you’re able to weather these downturns a lot more easily than you would otherwise.”

Rianda has not yet counseled any of his own cash advance clients on real estate matters. But based on his insights from working with both areas, he says real estate would be a logical move for MCA executives, and he’s seen some of his clients in the bankcard industry buy up properties.

“One of my clients had a portfolio of merchants and sold it for a few million, then flipped over to real estate. So it’s a means (to an end),” Rianda says.

‘Snowball effect’

Ribeiro has relied on a simple strategy to steadily build his portfolio of residential properties: Buy. Fix. Leverage. Repeat.

“I feel like the portfolio is doubling every couple of years. It’s just a snowball effect,” he says.

After Ribeiro buys a home, he waits about six months before he has it appraised and fixes it up in the meantime.

“If you go to the bank within the first six months of purchasing it, they’re going to give you the actual market value of whatever you purchased the house for,” he says. “If you wait six months, they’ll reappraise the home and give its true market value, which could be another 40, 50 or 60 percent. And so now you’re going to have a lot more equity in the house, and you’re going to get a lot more money when you leverage that home to go buy the next one.”

Ribeiro says he sees lots of people making the mistake of buying a home, and then going to the bank a week or two later for a loan.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Depreciation refers to one of the key tax benefits of real estate. Since owning a rental property is technically a type of business because it generates income, the property is considered a business asset. The IRS allows you to deduct the cost of acquiring that asset – the property – over the span of its useful life. For residential properties, the IRS sets a standard depreciation period of 27.5 years.

So if you buy a $100,000 property with a $20,000 land value, $80,000 of the asset is considered depreciable. Over the course of 27.5 years, you can take an annual deduction of just over $2,900 a year.

The trick, Ribeiro says, is to stick to lower-priced properties with an 80/20 home-to-land value. Most of his properties are single- and multifamily homes between southern California and Las Vegas.

Like Ribeiro, Rianda’s investor clients concentrate on one geographic area to find the best properties. “They look at the area for a long time, understand the area,” he says. “In my neighborhood, three blocks can make a 50 percent difference in the price of a house. You need to focus on a particular geographic area and do a lot of transactions in it.”

Small portfolio, big impact

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

“For me, it’s just a really good second income stream and a way to have a secure return of 4.5% to 6.5% a year,” he says.

Growing up, Weitz got a feel for real estate by watching his uncles invest in multifamily properties. At one point, Weitz’s uncle owned 15 different multifamily homes, and Weitz would help do the maintenance on them.

Eight years ago, Weitz invested in his first two-family home and has fixed and flipped eight properties since then. He currently owns two two-family homes and invests primarily in multifamily homes in Long Island, Brooklyn and Queens. Over the next five years, he plans to pick up at least two more four- or eight-family properties. Working with a small portfolio of residences in his home state has allowed Weitz to have full control over managing his properties and to turn a good profit.

“I think for me, it just offers more liquidity,” he says. “It’s an asset I can sell and liquidate at any time. That’s really important for me.”

Ideally, Weitz would like for his investment to build generational wealth that he can pass down to his son. With many people in the U.S. unable to qualify for mortgages, Weitz sees real estate investing as an opportunity to help the economy by giving renters a place to live and put down roots. “Depending on the neighborhood, you can put yourself in a situation where you have good renters for 20 to 30 years. They want to raise their families and have their kids grow up there,” he says.

Litigation among the pitfalls

Even though Ribeiro has had success with his business model, he cautions that there’s considerable risk involved with real estate.

“I love the industry. It’s a passion. It’s beyond my wildest dreams of the size of the portfolio and how well it performs,” he says. “But don’t think it’s all cupcakes and unicorns. There’s a lot to the madness. That’s why not everyone can replicate the model.”

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

As an attorney, Rianda says his real estate clients call on him not just for the purchase of the property, but for various issues that occur during the ownership period.

Here’s one scenario: A property owner has a tenant who isn’t paying rent, so the property owner sues the tenant. But while the lawsuit proceedings are under way, the tenant declares bankruptcy, which puts a stall on further litigation.

“There are people who understand the system and can make it difficult for you to get them out (of the property),” Rianda says, adding that it’s important to have legal counsel readily available. “You need someone who has really done this a lot and knows how the system works to get that person out of the rental property as quickly as possible.”

To minimize liability, Ribeiro has divided his properties into about 10 different business entities – each with a separate umbrella insurance policy.

Rianda sees his own real estate investor clients follow this strategy by grouping multiple homes under the name of an LLC. “If you personally own all these various assets, there’s the potential that if something catastrophic happened at one, it could bleed into all your other properties and potentially put them at risk,” he says.

Dual careers

Ribeiro’s real estate investments and finance company both serve as full-time occupations for him. Some years, he’ll focus more on one area than on the other, depending on market conditions. He spent more time on real estate between 2008 and 2013; then his business needs flip-flopped when real estate prices started going back up. This past year, he’s directed more attention to the finance company because of COVID, which necessitated some operational changes and a need to help clients who had been trying to get PPP loans. But he’s also started investing in commercial real estate, which has taken a hit because of companies forgoing office space to save overhead costs while employees work remotely.

Ribeiro expects to start seeing more mortgage defaults on lower-level homes in 2021 and 2022, after forbearance periods are over. And he’s been leveraging his assets to start buying more properties around the second quarter of the new year. “I think it will be a good time to start buying heavy again,” he says.

An attractive investment vehicle

With the pandemic weakening business portfolios, secondary investment options might sound like just what the doctor ordered.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

“As time goes on, I’m starting to see my clients go back into their lending,” Rianda says.

Even as clients start to recoup their business, Rianda sees the wisdom in other investments and says cash advance executives are well suited for real estate. “It’s just a way that people who have been successful and spin off a lot of cash for their businesses see as a safe way to diversify their income,” Rianda says. “It’s something I find that people who are doing well in their business do, regardless of what business they’re in. So cash advance guys are just following the things people have done for years.”

Ribeiro cautions that people who get into real estate should look at it as a 10-year investment minimum, and not just a two- or three-month stint.

“It’s not a lottery ticket, and it’s not an overnight race,” Ribeiro says. “This is a long-term gain. But it’s a very lucrative gain from a cash-flow perspective and a tax perspective. I don’t think there’s a more attractive vehicle than real estate.”

Biden SEC Pick: MIT fintech professor, helped create Dodd-Frank

January 21, 2021 As President Biden’s executive appointments await senate approval, crypto and security holders will be waiting anxiously for one in particular: Gary Gensler. A seasoned financial expert in and out of the public and private sector, Gensler most recently taught blockchain finance classes at the MIT Sloan School of management. What will this crypto researcher bring to the SEC?

As President Biden’s executive appointments await senate approval, crypto and security holders will be waiting anxiously for one in particular: Gary Gensler. A seasoned financial expert in and out of the public and private sector, Gensler most recently taught blockchain finance classes at the MIT Sloan School of management. What will this crypto researcher bring to the SEC?

By looking at his past research topics, and class syllabi, there may be some foreshadowing. Much of his focus has been on emerging fintech in business. Gensler doesn't just support innovation in banking and finance; he has been actively teaching grad students how to build blockchain-based businesses for the past couple of years.

Last spring, he taught a course called "Fintech: Shaping the Financial World" focused on leveraging blockchain tech and AI.

"This technology has real potential as a catalyst for change in the world of finance and the broader economy," Gensler said in testimony before Congress. “Though there are many technical and commercial challenges yet to overcome, I’m an optimist and want to see this new technology succeed.”

When it comes to regulation, Gensler is light, explicitly stating in an interview with another MIT researcher, “we must preserve the freedom for firms to fail,” and that “it’s best to show some flexibility.” While it is true that activity of any significant size has to be contained within the current regulatory framework,” Gensler said, “the government should put smaller firms in “a regulatory sandbox.”

Before teaching about bitcoin, Gensler worked at Goldman Sachs, where he made partner by 30 years old, the youngest ever to make partner at the time. He went on to lead the team that advised the NFL in the most lucrative TV in history in 1990.

After leaving Goldman, Gensler worked in the US Treasury and eventually chairman of the Commodity Futures Trading Commission under Obama. Though he calls for easy regulation for smaller firms, His work at the CFTC following the 2008 financial crisis culminated in the 2010 Dodd-Frank act.

When it comes to cryptocurrencies, Gensler has said the regulatory framework would “guard against illicit activities, protect investors and their funds, and promote market integrity.”

He has said cryptocurrency, in general, is both a security and a commodity. Some coins like Ripple are more securities, while Bitcoin is not.

Official Who Wants to “Wipe Out” Merchant Cash Advance Will Be Next CFPB Head

January 18, 2021 Rohit Chopra, an FTC Commissioner, will take over as head of the Consumer Financial Protection Bureau under incoming President Joe Biden, sources say.

Rohit Chopra, an FTC Commissioner, will take over as head of the Consumer Financial Protection Bureau under incoming President Joe Biden, sources say.

Chopra’s name made the rounds in 2020 when he told NBC News that he was looking for a “systemic solution” that can “wipe out” all merchant cash advance companies.

His candid comments aligned with an official statement he put out in August in which he opined that the structure of MCAs “may be a sham since many of these products require fixed daily payments…”

He further added that there were “serious questions as to whether these merchant cash advance products are actually closed-end installment loans, subject to federal and state protections including anti-discrimination laws, such as the Equal Credit Opportunity Act, and usury caps.”

His transfer to the CFPB could be viewed as unwelcome news for the MCA industry as the agency is currently in the process of finalizing the types of financial institutions it believes it should maintain some jurisdiction over. Originally, MCA companies were poised to be excluded from the data reporting requirement set forth by Section 1071 of Dodd-Frank but that could very well soon change.

2021: The Year of Uncertainty

January 7, 2021 For alternative lenders and funders, 2021 is starting out with a question mark and will lead (hopefully) to a resounding exclamation point of recovery.

For alternative lenders and funders, 2021 is starting out with a question mark and will lead (hopefully) to a resounding exclamation point of recovery.

Many industry participants waved goodbye to 2020 with relief, and are welcoming a bounce-back in 2021, despite some trepidation about potential bumps along the way and how long a full recovery will take. While things started to improve somewhat toward the latter half of 2020 after grinding to a halt earlier in the year, the pandemic is still raging, with economic growth highly dependent on the immunization trajectory. Then there’s the incoming Democratic administration and the possibility of new rule- making, along with January’s runoff elections in Georgia that could change the balance of power in the Senate, and thus impact the new president’s law- making abilities.

Beyond these macro-issues, the funding industry is also dealing with its own uncertainties. Small business lenders and funders have been hit particularly hard, with underwriting decidedly more difficult in this environment. Some industry players have been forced to find alternative revenue streams in order to ride things out. Not only that, but there are scores of small businesses still reeling from pandemic-induced shutdowns and lighter foot traffic, with some gloomy estimates about their ability to bounce back. Many alternative players are weighing diminished returns against a widely-held bullish outlook for the industry long-term. Many are simply hoping they can hunker down and stick it out long enough and to avoid additional carnage and consolidation that’s widely expected over the short-term.

Ultimately things will get better, but it’s unclear precisely when, says Scott Stewart, chief executive of the Innovative Lending Platform Association. “It’s going to be a bumpy ride for the next year to figure out who is going to be able to survive,” he says.

Here’s a deeper dive into how industry participants see 2021 shaping up in terms of the challenges, competition, M&A, regulation, changing business model, expansion opportunities and more.

SPECIFIC CHALLENGES FOR SMALL BUSINESS FINANCERS

Companies that focus on consumer financing haven’t struggled quite as much amid the pandemic as their small business brethren, and they could continue to see demand grow in 2021. Even amid high unemployment rates, many consumers still need loans for home repairs or as a stop-gap to pay necessary expenses, helping to mitigate the impact on firms that focus on personal loans.

Small business financers, however, got pummeled in 2020 and the situation remains precarious, especially given the prognosis for small companies broadly. Consider that 163,735 Yelp-listed businesses closed from the beginning of the pandemic through Aug. 31—at least 97,966 of them permanently. Further underscoring how dire the situation is for small businesses, 48 percent of owners feared not earning enough revenue in December to keep their businesses afloat, according to a recent poll by Alignable, an online referral network for small businesses. What’s more, 50 percent of retail establishments and 47 percent of B2B firms could close permanently, according to the poll of 9,204 small business owners.

A SHRINKING COMPETITIVE LANDSCAPE

For many lenders and funders, the latter part of 2020 proved more successful for originations, though business is still a far cry from before the pandemic. A number of players who suspended or reduced business operations for a period of time during the first wave of the pandemic have dipped their toes back in and are in the process of trying to adapt to the new normal. For some, though, the challenges may prove too great, industry observers say. Given that many brokers and funders that were on the fringe have been hurt by the pandemic, more shake- out can be expected, says Lou Pizzileo, a certified public accountant who advises and audits alternative finance companies for Grassi in Jericho. N.Y.

And, with fewer competitors, there will be more of a need for those who are left to pick up the slack, says Peter Renton, founder of Lend Academy. Beyond being a lifeline for many alternative financers, PPP loans helped open the eyes of many small businesses who hadn’t previously considered working with anyone but a bank. In the beginning, when it was so difficult for small businesses to get these funds, they looked beyond banks for options and some found their way to online providers. This could be a boon for the industry going forward since alternative providers are now on the radar screen of more small businesses, says Moshe Kazimirsky, vice president of strategic partnerships and business development at Become.

He predicts that larger, stronger players will gradually ease some of their lending and funding criteria early on in 2021, but no one is expecting a quick revival, with some predicting it could be well into 2022 before the industry is on truly stable footing. “I think it’s going to be a very slow recovery,” Kazimirsky says.

M&A

In 2020, the industry saw bellwethers like Kabbage and OnDeck get swallowed up, and with so many businesses pinched, there are likely to be more bargains ahead from M&A standpoint, Pizzileo says. “The damage from Covid is palpable; we just haven’t seen the real impact of it yet,” he says.

No matter what product you are providing, if you’re a smaller player who can’t find your way, you’re going to have a hard time staying in business,” says Stewart of the Innovative Lending Platform Association. “There will be some collateral damage going into next year,” he predicts.

In terms of likely buyers, Renton says he expects other fintechs to step in, and possibly even mid-size community banks snap up some alternative providers. If you can buy something for “a song” it’s compelling, he says. “I expect to see a few more offers that are too good to refuse,” he says.

CHANGING BUSINESS MODELS

Pizzileo, the CPA, predicts there will be ongoing opportunities in the year ahead for well-positioned, strong businesses with available capital. In some cases, however, this may require tinkering with their existing ways of doing business.

Before the crisis, some lenders applied the same or very similar lending model across industries. “That is going the way of the dinosaur. That’s not going to be a successful model going forward,” Renton says. Lenders will focus more on having a differentiated model for the businesses they serve. “I think the crisis created this necessity to treat each industry on its own merits and create a model that has some level of independence, he says.

The year ahead is also likely to be one in which e-commerce lending continues to thrive. According to the third quarter 2020 report from the U.S. Census Bureau, U.S. retail e-commerce stood at $209.5 billion, up 36.7% year over-year. E-commerce accounted for 14.3% of total retail sales in Q3. Because it’s such a high-growth area, and many businesses that didn’t have this vertical before are moving in this direction and more lenders are focusing on it and growing that part of their business, says Kazimirsky of Become.

It will also be interesting to watch how lenders and funders continue to reshape themselves. Sofi, for instance, is continuing to pursue its goal of receiving a national bank charter. Other lenders and funders may also seek to reinvent themselves as they attempt to stay afloat and compete more effectively.

“Monoline lenders that rely on a single product will have more difficulty supporting customers in the wake of Covid,” says Gina Taylor Cotter, senior vice president and general manager of global business financing at American Express, which purchased Kabbage in 2020. “Small businesses need multi-product solutions to not only access working capital, but also real-time insights to help them be more prudent with their cash flow and accept contactless payments safely to encourage more business,” she says.

CHANGES IN RISK MODELING

Another pandemic-driven change is that lenders have had to tweak their risk modeling. Everyone understands the economy is not in the greatest spot, but their challenge in 2021 will be developing a way to assess future losses in the absence of a baseline, says Rutger van Faassen, head of product and market strategy for the benchmarking and omnichannel research group at Informa Financial Intelligence.

Consumer behaviors have changed, for instance. So even though the pandemic will end, it’s too soon to say what the structural impacts on an industry will be and how that affects the desirability of lending to especially hard-hit businesses, such as restaurants, cruise lines and fitness centers. “Clearly the behavior that everyone is showing right now is because of the pandemic. The question is: how will people behave once the pandemic ends,” he says.

“In the meantime, a lot of lenders will have to do more in-the-moment decision-making, until we get to a point when we’re truly in a new normal, when they can start recalibrating models for the longer-term,” he says.

OPPORTUNITIES TO HELP SMALL BUSINESSES

One certainty in the year ahead is the need to help existing small businesses with their recovery, says Cotter of American Express. “Small businesses represent 99 percent of all jobs, two-thirds of new jobs and half of the non-farm GDP in America. Our country’s success depends on small businesses, and financial institutions have a great opportunity to meet their needs to recover and return to positions of growth in 2021,” she says.

How to make this happen is something many alternative financers will grapple with in 2021. Another opportunity may exist in providing funding solutions to new businesses or those that have pivoted as a result of the pandemic. Cotter points to the inaugural American Express Entrepreneurial Spirit Trendex, which found 76% of businesses have already pivoted their business this year and 73% expect to do it again next year. “New-business applications have reached record heights as entrepreneurs pivot and adapt, indicating a surge of new ventures that will require financial solutions to build their business,” Cotter says.

REGULATORY WATCH

Several regulatory issues hang in the balance in 2021, including state-based disclosure laws, expected rules on third-party data aggregation and demographic data collection, and the status of a special purpose charter for fintechs, says Ryan Metcalf, head of U.S. public policy, regulatory affairs and social impact at Funding Circle. With a new administration coming in, the regulatory environment could become more favorable for measures that stalled during Trump’s tenure.

Armen Meyer, vice president of LendingClub and an active member of the Marketplace Lending Association, says he’s hoping to see a bill pass in 2021 that requires more transparency for small business lending. He would also like to see more states follow the lead of California and Virginia and make the 36% interest rate standard of Congress’s Military Lending Act, which covers active- duty service members (including those on active Guard or active Reserve duty) and covered dependents, the law of the land. “We’re calling for this to be expanded to everybody,” he says.

CANADA

Meanwhile, our neighbors to the North have their own challenges and opportunities for the year ahead. The alternative financing industry in Canada originated out of the 2008 recession when banks restricted their credit box and wouldn’t lend to certain groups. While conditions are very different now, “this period of economic uncertainty is going to be an incredible fertile period of time for fintechs to come up with new and interesting and creative credit products just like they did entering the last financial crisis,” says Tal Schwartz, head of policy at the Canadian Lenders Association.

Open banking continues to be on the Canadian docket for 2021 and how the framework shapes up is of utmost interest to fintech lenders in Canada. Schwartz says he’s also hopeful that alternative players in Canada will have a role to play in subsequent government- initiated lending programs. He’s also expecting to see more growth in the e-commerce area, particularly when it comes to extending credit to e-commerce companies and in financing solutions at checkout for online shopping.

AltFinanceDaily’s Top Five Stories of 2020

December 28, 2020DeBanked’s Top 10 most read stories of 2020 all involved the Payment Protection Program (PPP). It was by far the hottest topic in small business financial services for the year. As a result, we consolidated our most read stories into FIVE categories and this is what our readers consumed most in 2020!

1. PPP

The Payroll Protection Program saga boiled down to one major question early on in the pandemic: Who, if anybody, would be able to lend the money out on the government’s behalf? PPP Lender Requirements was the most read story on AltFinanceDaily in 2020, followed by the world being curious to find out who was the biggest PPP lender. On April 22, AltFinanceDaily was the first to spread the story that Ready Capital (Knight Capital‘s parent company) was the largest PPP lender in the US for Round 1.

The Payroll Protection Program saga boiled down to one major question early on in the pandemic: Who, if anybody, would be able to lend the money out on the government’s behalf? PPP Lender Requirements was the most read story on AltFinanceDaily in 2020, followed by the world being curious to find out who was the biggest PPP lender. On April 22, AltFinanceDaily was the first to spread the story that Ready Capital (Knight Capital‘s parent company) was the largest PPP lender in the US for Round 1.

2. NY’s Disclosure Bill

The biggest non-PPP story of the year was a bill passed in New York that was signed by the governor at Midnight on Christmas Eve. SB 5470, which some have dubbed “The Small Business Truth in Lending Act,” is slated to completely overhaul the non-bank small business lending market in the state. The bill was passed by the legislature in July.

The biggest non-PPP story of the year was a bill passed in New York that was signed by the governor at Midnight on Christmas Eve. SB 5470, which some have dubbed “The Small Business Truth in Lending Act,” is slated to completely overhaul the non-bank small business lending market in the state. The bill was passed by the legislature in July.

3. OnDeck

It’s difficult to overstate how much of a rollercoaster it was for the stalwart fintech lender in 2020. OnDeck started the year with optimism, announcing a NASCAR sponsorship in March just as the company’s stock suddenly plummeted by 30%. By the time summer rolled around, the company was no longer engaged in non-PPP lending activities and was battling in a fight for its life with its creditors. In July, OnDeck was acquired by Enova, which led to shareholder lawsuits over the terms and disclosures tied to the deal. Somehow, by year-end, OnDeck managed to pull itself back together, thanks to its new parent company. It successfully originated $148M worth of loans in Q3.

It’s difficult to overstate how much of a rollercoaster it was for the stalwart fintech lender in 2020. OnDeck started the year with optimism, announcing a NASCAR sponsorship in March just as the company’s stock suddenly plummeted by 30%. By the time summer rolled around, the company was no longer engaged in non-PPP lending activities and was battling in a fight for its life with its creditors. In July, OnDeck was acquired by Enova, which led to shareholder lawsuits over the terms and disclosures tied to the deal. Somehow, by year-end, OnDeck managed to pull itself back together, thanks to its new parent company. It successfully originated $148M worth of loans in Q3.

Wow, just wow.

4. Covid-19

The impact of Covid was a close 4th on AltFinanceDaily’s top read list. In March, AltFinanceDaily published a writeup of How Small Business Funders [Were] Reacting, an interesting glimpse into the pandemic as it was just unfolding. At that time, attitudes ranged from confidence in being prepared to being convinced it was time to shut everything down. One notable takeaway from the commentary is that nobody surmised that the situation would persist for the entire rest of the year.

The impact of Covid was a close 4th on AltFinanceDaily’s top read list. In March, AltFinanceDaily published a writeup of How Small Business Funders [Were] Reacting, an interesting glimpse into the pandemic as it was just unfolding. At that time, attitudes ranged from confidence in being prepared to being convinced it was time to shut everything down. One notable takeaway from the commentary is that nobody surmised that the situation would persist for the entire rest of the year.

Capify CEO David Goldin made an early bold prediction, however. “I would not be surprised if we learn in the next few weeks that the President of the United States has it,” he said in an interview with AltFinanceDaily in mid-March. President Trump was diagnosed with Covid-19 less than six months later on October 6th.

5. Scandal

Three scandals were a near-tie for views in 2020 so we’re revisiting them all here.

Three scandals were a near-tie for views in 2020 so we’re revisiting them all here.

Brendan Ross & Direct Lending Investments – Brendan Ross, the former CEO of a very popular fintech lending hedge fund, was indicted on August 11th. Federal officials including the SEC, say that Ross defrauded investors while managing more than $1 billion in assets. Ross’s “unwinding” began in 2019 when he suddenly resigned from the firm and wrongdoing was alleged.

Jonathan Braun – Jon Braun, made infamous by a Bloomberg Businessweek profile, checked into FCI Otisville earlier this year after having been sentenced the previous May for drug related offenses. Braun resurfaced in the news this summer when the FTC announced civil charges against him for alleged acts related to a company named Richmond Capital Group, LLC. The New York State Attorney General filed its own charges against Braun and affiliates at the same time.

Par Funding – A financial services firm based in Philadelphia generated major headlines this year after the SEC filed a lawsuit against the company that ultimately resulted in it being placed in receivership. A series of stunts and accidents got the SEC’s case off to a rocky start, but the likelihood of Par ever restarting its business has diminished to almost nothing.