Real Estate Lender Patch of Land Sells $250 Million in Loans

February 11, 2016 Real estate lending platform Patch of Land announced that it signed a $250 million agreement with an east coast based credit fund to purchase its loans in a forward flow arrangement.

Real estate lending platform Patch of Land announced that it signed a $250 million agreement with an east coast based credit fund to purchase its loans in a forward flow arrangement.

The reluctance to name the city or state of the fund suggests that in doing so would too easily reveal who it is.

Patch, an LA-based lender which uses a data-driven underwriting model, promises investors a risk adjusted return with extensive available data to support the underlying credit decision on each loan.

The company founded in 2013 had raised a million in seed funding and $125,000 in debt in 2014, followed by $23 million in Series A funding last year. And it has funded more than 200 projects, with an average blended rate of return to investors of 12 percent

This is continued evidence of institutional interest in loans generated by marketplace lenders. JP Morgan Chase bought loans worth a billion dollars from Santander Consumer USA Holdings Inc earlier this month. The bank also partnered with OnDeck in December of last year to facilitate the underwriting of the bank’s small dollar small business loan program.

In an interview with Bloomberg, Funding Circle’s CEO Sam Hodges said that it’s the first of many such partnerships to come where big banks will realize the potential of fast-growing fintech startups.

Love of Sales Turned Shy Student into LA Real-Estate YouTube Powerhouse

December 18, 2020 “When the Pandemic first started, a lot of the classes we worked with just canceled, everything went downhill,” Loida Velasquez, an LA-based real estate broker, said. “But starting in June until now— everything turned around. Inventory is so low, and there are so many buyers, most houses are selling in 24 hours. I’ve never seen a market like this before.”

“When the Pandemic first started, a lot of the classes we worked with just canceled, everything went downhill,” Loida Velasquez, an LA-based real estate broker, said. “But starting in June until now— everything turned around. Inventory is so low, and there are so many buyers, most houses are selling in 24 hours. I’ve never seen a market like this before.”

It’s a seller’s market like you can’t believe right now, said Velasquez, and that’s what she specializes in: running a cold-calling, door-knocking real estate firm that jumps on expired listings, revamps properties, and sells them on the open market.

After five years of rapid success, Velasquez has taken her charisma to social media, creating a series of Youtube videos to help other brokers find the success she has in the real estate world.

“When I started my real estate career, I remember trying to find videos of people sharing their experience, but most of them were men: I didn’t find many women,” Velasquez said. “So I told myself, ‘you know what, I’m going to start creating videos to put out my journey so people can see what it’s like not only as a real estate agent but as a younger woman in this business.’ And that’s how my channel started.”

Velasquez has also begun teaching online courses for brokers who need help developing their skills. She offers an all-encompassing approach, including cold calling and knocking on doors, that she said many modern brokers don’t use anymore, even though they never became any less viable.

“I knew that the old school approach of cold calling and door knocking was something that a lot of agents don’t like to do,” she said. “So if I became very good at it, I knew that I was going to become successful a little faster than someone who doesn’t incorporate that type of prospecting.”

It has set her apart, and part of why she launched online classes: her videos on real estate were so successful other agencies were telling their trainees to watch her work. Many agencies don’t offer adequate training, Velasquez said, some give out unethical advice. When newly licensed brokers find Velasquez, she said she stands out as an agent with standards and knowledge of the industry.

It has set her apart, and part of why she launched online classes: her videos on real estate were so successful other agencies were telling their trainees to watch her work. Many agencies don’t offer adequate training, Velasquez said, some give out unethical advice. When newly licensed brokers find Velasquez, she said she stands out as an agent with standards and knowledge of the industry.

That knowledge comes in the form of hard-earned experience, one that includes making slip-ups along the way, something she said ocassionally still happens. It’s all part of the game, she explains. Many of her leads come in from her online networking now, but her techniques are still honed to reach out to sellers looking for a knowledgeable agent who knows the market.

“A lot of my business comes from social media, whether it’s from agents that watch me and send me referrals, or just consumers that are trying to learn what it takes to buy or sell a house,” Velasquez said. “But aside from that, I still cold call a lot of ‘for sale by owners’ and expired. Many of them still want to sell, but they had to pull their home off the market. Many of them didn’t have a good relationship with the last agent and want to find someone else who can do a better job.”

And that relationship comes in the form of Velasquez calling out of the blue, flipping the house successfully in a matter of weeks, sometimes two or three sales every month.

Things were not this easy for what outwardly looks like a charismatic, polished agent; Velasquez attests that she was quiet and anxious even to present a school project before she found her love of sales.

“I was the shyest person ever, and I was terrified of talking in group projects,” Velasquez said. “If people from my past saw me, they would never guess I would be doing public speaking events and would have never known this is what I would become.”

Velasquez was a sociology major before getting a side job as a brand ambassador, traveling to conventions and selling face to face to customers. Everything changed.

“Telling people about the product, getting paid to talk to people, helped me get myself out of my shell and comfort zone,” She said. “I don’t know why I was scared of talking to strangers, but it helped me get out there, and I switched my major to marketing.”

After she went back to get an MBA in 2015, she started making Youtube videos and found her passion. She said that with determination, anyone could get over hurdles and find success. Selling real estate is not what it looks like on TV, but Velasquez noted the hard work is worth it for the payoff.

“After the turning point, I started to see people responding ‘because of this video, I got my first listing.’ I said, if I need to get myself out of my comfort zone to help people, this is something I know I need to do,” Velasquez said. “If you stay focused and surround yourself with the right people, you’ll make it. There will be many times you will doubt yourself, and it is not like what you see on TV.”

Forget the Metaverse, I Bought Real Land

February 20, 2024 In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

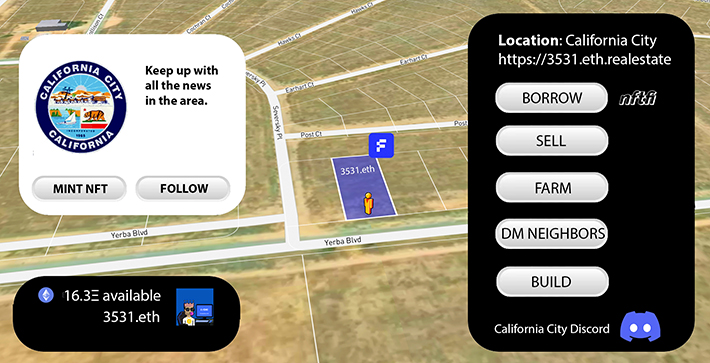

All of this history was something I breezed through right before I impulsively clicked a button on my screen asking me to confirm my purchase for a lot there. One click. That’s apparently all it took to become the newest member of a potential future neighborhood in California City, one that might not ever come to fruition. But how I found it in the first place is the real story. It appears that in the modern era this sleepy desert outpost has become a bit of an experimental laboratory for something relatively new in the real estate world, converting properties into NFTs.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Founded in 2018 and backed by investors like Mark Cuban and Zain Jaffer, properties tokenized by Fabrica “can be traded instantly, used as collateral and are compatible with all NFT platforms,” the company states. “The product automates sales transactions, facilitating title transfer, payments and regulatory compliance.” Fabrica facilitates the on-ramping of your land into an NFT and even provides its own marketplace for buyers and sellers. That’s where I got mine. Interested parties can read up on a property’s on-chain history and even check the title. There’s also a cool little Google Earth-like animation that flies the user to their specific plot of land. The experience feels a lot like buying a plot of virtual land in a video game or the metaverse except this land is real. That means that sleek little NFT in your digital wallet comes with real responsibilities like property taxes, which Fabrica works to keep the owner informed about. It also means any and all liabilities of property ownership. The upside is that you can go and visit it in real life and even develop it. You can’t do that in a video game.

Although I’ve counted six properties in California City that are immediately identifiable as NFTs, it’s hardly the only place in the United States where this is being done. Properties available for sale as NFTs as of this writing include locations across Colorado, Arizona, New Mexico, San Bernardino-CA, and even Orange, New York. Some are very remote and speculative, while others are a part of normal civilization and priced accordingly. Buyer beware of course given the serious nature of these assets.

Perhaps one of the biggest obstacles to understanding how this is all possible is the widespread misconception of what NFTs are. Most of the American population lives under the mistaken impression that NFTs are cartoon art pictures like Bored Apes or CryptoPunks that were all the rage in 2021 and to some extent are still popular in niche circles, but almost anything can be tokenized. More recently, for example, domain names are being converted into NFTs to facilitate faster sales and quicker payouts. The same is true now here with land. Not only can land ownership change hands in the blink of an eye by transferring the NFT but one can also easily tap into the value by pledging it on a peer-to-peer NFT loan marketplace like NFTfi. Fabrica officially announced a partnership with NFTfi this past December, for example. The possibilities are endless

For the perpetual skeptics of all things blockchain that are convinced real business will only ever be done in the real world, a visualization of an NFT on a crypto wallet app might not be all that convincing, especially if the icon for it is situated right next to one of those expensive monkey pictures that kids wouldn’t shut up about years ago. The proof then is in the adventure. With a drive of less than two hours from Downtown Los Angeles, there’s a little plot of land on a quiet street known as Yerba Boulevard. It’s covered in weeds and reddish soil. Empty plains make up most of the backdrop but the suburbs are very slowly creeping their way there. In fact, I’ve since learned who my neighbor is across the street. It’s a 26,000 square foot cannabis facility that was just built in 2022. I bet the owners would be into NFTs (😂). Since that facility is up for sale, numerous 3D surrounding views exist of my plot. Turns out I can even walk to the airport. It’s not much but it’s home to me and all I could afford for the purpose of this story and learning what it was all about. Maybe those 400,000 planned residents will eventually want my land and it’ll make me a millionaire. Ah the allure of California City.

Fundomate Announces $50 Million Line of Credit to Bring Embedded Automated Funding and Real-Time Banking to Payments and SMB Marketplaces

September 30, 2021

Los Angeles, September 30, 2021 — Fundomate, a leading embedded finance provider of automated business funding solutions and real-time banking tools for merchant-facing platforms, announced the closing of a $50 million line of credit with Revere Capital today. The new line of credit is Fundomate’s largest to date.

Fundomate will leverage the credit facility to scale up its partnerships with merchant-facing businesses and grow the company’s new white-label banking platform. The platform enables merchant-facing platforms and marketplaces to rapidly expand their product suite and enhance engagement by offering automated financing and embedded banking tools under their own brand.

“With the closing of the $50 million credit line, Fundomate can scale its proven automated funding platform via its one-touch funding tool already embedded within 100+ payment processing partners and marketplaces”, says Sam Schapiro, CEO and Founder of Fundomate. “We’re excited to also focus on our new embedded real-time banking platform, which uses AI and advanced forecasting to provide our partners the ability to offer their customers free short-term working capital that’s available for immediate use.”

“With the closing of the $50 million credit line, Fundomate can scale its proven automated funding platform via its one-touch funding tool already embedded within 100+ payment processing partners and marketplaces”, says Sam Schapiro, CEO and Founder of Fundomate. “We’re excited to also focus on our new embedded real-time banking platform, which uses AI and advanced forecasting to provide our partners the ability to offer their customers free short-term working capital that’s available for immediate use.”

Revere Capital Managing Director Christopher Gilker said, “We’re incredibly excited to grow with Fundomate. As I tell all my colleagues, Fundomate is a company at the right place at the right time. The team is ambitious, and I have no doubt the company will disrupt the fintech, payments, and banking space in a big way.”

Revere Capital Managing Director Suman Mallick commented further, saying, “I’m very excited about Fundomate’s potential to change how businesses manage their banking and credit needs. I believe the company will benefit from strong secular tailwinds and has vast opportunities for growth with merchant-facing businesses throughout the US.”

Waterford Capital structured and arranged the line of credit on behalf of Fundomate. Dave Piotrowski, Managing Director at Waterford Capital, said, “Fundomate has an advantage over others in the merchant finance space through the products offered through their payment processor partners. This financing relationship with Revere Capital will help take the company to the next level and further broaden their competitive advantage.”

About Fundomate

Fundomate is an innovative fintech company that operates in the alternative lending space and provides both direct-to-business and white-labeled turnkey solutions, enabling merchant-facing platforms to offer alternative funding products to their customers as a value-added proposition.

The company has deployed over $100M to more than 2000 merchants across various industries in

the United States.

About Revere Capital

Revere Capital is a private credit manager with expertise in lower middle-market real estate bridge lending & specialty finance. The firm’s disciplined underwriting utilizes fundamental real estate analysis and research, emphasizing intrinsic value to create a diversified portfolio for investors. Revere also specializes in financing other commercial interests, consumer interests and insurance-backed interests. With a national footprint, Revere Capital offers speed, certainty of execution, and creativity to structure loans to fit borrowers’ needs and provide contractual income for investors.

About Waterford Capital

Waterford Capital is a leading arranger of structured finance and asset securitization transactions. The firm advises specialty finance companies and asset managers in connection with warehouse credit facilities, private placements of asset-backed securities, whole loan sale programs, and mezzanine and equity capital raises.

The SEC Already Suffered a Major Defeat in the Par Funding Battle – But Who is the Real Loser?

August 8, 2020 While the news media, regulatory agencies, and law enforcement are high-fiving each other over the course of events in the Par Funding saga (a lawsuit, a receivership, an asset freeze, and an arrest), there lies a major problem: The SEC already suffered a major defeat.

While the news media, regulatory agencies, and law enforcement are high-fiving each other over the course of events in the Par Funding saga (a lawsuit, a receivership, an asset freeze, and an arrest), there lies a major problem: The SEC already suffered a major defeat.

On July 28th, rumors of a vague legal “victory” for Par Funding circulated on the DailyFunder forum. The context of this win was unknowable because the case at issue was still under seal and nobody was supposed to be aware of it.

Cue Bloomberg News…

In December 2018, Bloomberg Businessweek published a scandalous story about a Philadelphia-based company named Par Funding. And then not a whole lot happened… that is until Bloomberg Law and Courthousenews.com published a lengthy SEC lawsuit less than two years later that alleged Par along with several entities and individuals had engaged in the unlawful sale of unregistered securities.

At the courthouse in South Florida, those documents were sealed. The public was not supposed to know about them and AltFinanceDaily could not authenticate the contents of the purported lawsuit through those means. According to The Philadelphia Inquirer, the mixup happened when a court clerk briefly unsealed it “by mistake” thus alerting a suspiciously narrow set of news media to the contents. AltFinanceDaily was the first to publicly point this out.

At the courthouse in South Florida, those documents were sealed. The public was not supposed to know about them and AltFinanceDaily could not authenticate the contents of the purported lawsuit through those means. According to The Philadelphia Inquirer, the mixup happened when a court clerk briefly unsealed it “by mistake” thus alerting a suspiciously narrow set of news media to the contents. AltFinanceDaily was the first to publicly point this out.

In court papers, some of the defendants said that they learned of the lawsuit that had been filed under seal on July 24th from “news reports.” Bloomberg Law published a summary of the lawsuit on its website in the afternoon of July 27th.

“It is fortuitous that the Complaint was initially published before it was sealed,” an attorney representing several of the defendants wrote in its court papers. “Otherwise, [The SEC] would have likely accomplished its stealth imposition of so-called temporary’ relief, that would have led to the unnecessary destruction of a legitimate business.”

The day after this, on July 28th, a team of FBI agents raided Par Funding’s Philadelphia offices as well as the home of at least one individual. Rumors about the office raid landed on the DailyFunder forum just hours later, along with links to the inadvertently public SEC lawsuit now circulating on the web.

The day after this, on July 28th, a team of FBI agents raided Par Funding’s Philadelphia offices as well as the home of at least one individual. Rumors about the office raid landed on the DailyFunder forum just hours later, along with links to the inadvertently public SEC lawsuit now circulating on the web.

The New York Post caught wind of the story and published a photo of an arrest that had taken place fifteen years ago, creating confusion about what, if anything, was happening. Nobody, was in fact, arrested.

The SEC lawsuit was finally unsealed on July 31st, along with the revelation that Par Funding and other entities had been placed in a limited receivership pursuant to a Court order issued just days earlier. The receivership order was a massive blow to the SEC. It failed to obtain the most important element of its objective, that is to have the court-ordered right to “to manage, control, operate and maintain the Receivership Estates.” The SEC specifically requested this in its motion papers but was denied this demand and others by the judge who leaned in favor of granting the Receiver document and asset preservation powers rather than complete control of the companies.

The language of the Court order was interpreted differently by the Receiver, who immediately fired all of the company’s employees, locked them out of the office, and then suspended all of the company’s operations which even prevented the inbound flow of cash to the company (of which in the matter of days amounted to nearly $7 million). The SEC did successfully secure an asset freeze order.

In court papers, Par Funding’s attorneys wrote that: “The Receiver’s and SEC’s actions are ruining a business with excellent fundamentals and a strong financial base and essentially putting it into an ineffective liquidation causing huge financial losses. In taking this course of action against a fully operational business, the key fact that has been lost by the SEC, is that their actions are going to unilaterally lead to massive investor defaults.”

The Receiver, in turn, tried to fire Par Funding’s attorneys from representing Par. Par’s attorneys say that the Receiver has communicated to them that it is his view “that he controls all the companies.”

The Receiver, in turn, tried to fire Par Funding’s attorneys from representing Par. Par’s attorneys say that the Receiver has communicated to them that it is his view “that he controls all the companies.”

“The SEC is simply trying to drive counsel out of this case, as an adjunct to all the other draconian relief that they insist must be employed to ‘protect the investors,'” Par’s attorneys told the Court. “Due Process is of no regard to the SEC.”

As lawyers on all sides in this mess assert what is best for “investors,” seemingly lost is the collateral damage that is likely to be thrust on Par’s customers. The Philadelphia Inquirer has repeated the SEC’s contention that Par made loans with up to 400% interest. Bloomberg News has called Par a “lending company” whose alleged top executive is a “cash-advance tycoon.”

A review of some of Par’s contracts, however, indicate that they often entered into “recourse factoring” arrangements. “This is a factoring agreement with Recourse,” is a statement that is displayed prominently on the first page of the sample of contracts obtained by AltFinanceDaily.

Parallels between the business practices of Par Funding and a former competitor, 1 Global Capital, have been raised at several junctures in the SEC litigation thus far. But some sources told AltFinanceDaily that in recent times, Par has been offering a unique product, one that is likely to create disastrous ripple effects for hundreds or perhaps thousands of small businesses as a result of the Receiver’s actions (even if well-intentioned).

The “Reverse”

Par offered what’s known as a “Reverse Consolidation,” industry insiders told AltFinanceDaily. In these instances Par would provide small businesses with weekly injections of capital that were just enough to cover the weekly payments that these small businesses owed to other creditors.

One might understand a consolidation as a circumstance in which a creditor pays off all the outstanding debts of a borrower so that the borrower can focus on a relationship with a single lender. In a “reverse” consolidation, the consolidating lender makes the daily, weekly, or monthly payments to the borrower’s other creditors as they become due rather than all at once. Once the other creditors have been satisfied, the borrower’s only remaining debt (theoretically) is to the consolidating lender.

Par does not appear to have offered loans but sources told AltFinanceDaily that Par would provide regular weekly capital injections to businesses that could not afford its financial obligations otherwise. Par, in essence, would keep those businesses afloat by making their payments.

Par does not appear to have offered loans but sources told AltFinanceDaily that Par would provide regular weekly capital injections to businesses that could not afford its financial obligations otherwise. Par, in essence, would keep those businesses afloat by making their payments.

That all begs the question, what is going to happen to the numerous businesses when Par breaches its end of the contract by failing to provide the weekly injections?

As the Receiver makes controversial attempts to assert the control it wished it had gotten (but didn’t), the press dazzled the public on Friday with the announcement that an executive at Par Funding had been arrested on something entirely unrelated, an illegal gun possession charge. The FBI discovered the weapons while executing a search warrant on July 28th but waited until August 7th to make the arrest.

It remains to be seen what the 1,200 investors will recover in this case or what will become of the Receiver in the battle for control, but sources tell AltFinanceDaily that the authorities are all fighting over the wrong thing.

They should all be asking “what’s going to happen to the small businesses when their weekly capital injection doesn’t come in the middle of a pandemic?”

New RealtyMogul CIO Praises the Company’s Avoidance of Land, Hotel and Development Investments

January 23, 2018Los Angeles’ RealtyMogul promoted Chris Fraley from interim chief investment officer to permanent CIO, earlier this month. After the announcement, Fraley told commercial real estate publication, Bisnow, that the company’s “fairly conservative approach” has put it in an optimal position at this point in the current real estate cycle.

“There is certainly a feeling that we are at the top of the cycle given this is one of the longest economic expansions in the past century, from a time perspective,” he told Bisnow. “It is a relief that RealtyMogul has taken a fairly conservative approach by focusing mainly on income investments and light value-add and avoiding traditionally riskier assets like land, hotels and development.”

In 2017, RealtyMogul eclipsed several internal records and finalized transactions holding $566 million worth of capitalization.

Fraley believes that the company can “significantly increase” that number this year.

The Yale grad joined the company in June, bringing over 20 years of experience to the role. Former posts include a tenure as partner at Rockwood Capital, which preceeded the launch of his own real estate investment company, Evolve.

“Being on the operator side of the business really helped me appreciate all the hard work that goes into managing a real estate project,” Fraley said while discussing Evolve with Bisnow. “It has certainly given me greater insight on how to evaluate a potential operating partner as an investor.”

Fraley also shared that when he initially joined the company in an interim capacity in June, he did not intend to stay on full-time.

He gave partial credit for his decision to become a permanent member of the team to the company’s ability to merge research and data with technology.

‘We Serve a Fragmented Market That is Ripe for Disruption,’ says Patch of Land CEO

June 3, 2016$484 million: That’s how much real estate crowdfunding platforms attracted in 2015, which was three times of that the previous year. There are an estimated 125 such portals and the new SEC rule which allows non accredited investors some leniency to invest in these projects. To demystify real estate crowdfunding, AltFinanceDaily spoke to Patch of Land’s CEO Paul Deitch to unravel the concept, measure the momentum of investor interest and the regulatory environment. Here are excerpts from the interview.

What’s on the horizon for Patch of Land this year?

Now that Patch of Land’s model is proven, we will be adding complimentary products for the real estate entrepreneur and investor, accompanied by a broadening of funding strategies. For example, we recently launched the new midterm loan product that addresses the opportunity in the $4 trillion single-family rental space.

How is the investment momentum different from that in ‘08-’09?

One of the biggest changes between then and now has been the enactment of the JOBS Act, which actually came about as a result of investment conditions in ‘08-’09. Peer-to-peer lending came into existence during the 2008 Recession when consumers and small businesses could not rely on banks for their funding needs. In 2012, President Obama signed a historic bill called the JOBS Act (Jumpstart Our Business Startups Act), allowing companies to raise working capital in the form of debt and equity via a crowdfunding model. When the SEC implemented Title II of the JOBS Act in 2013 it allowed companies to publicly solicit, via Internet marketing, their equity and debt offerings; private placements could now be advertised. Marketplace lending is an evolution of peer-to-peer lending, defined by the participation of traditional financial institutions purchasing the loans being issued by P2P lenders.

Whom do you consider your competition in the industry and how do you differentiate yourself from them?

We approach the competition question from a different perspective. One would think that other online lenders or real estate crowdfunding companies are our competition but they are not. We are all working towards creating more efficiency, transparency and access to real estate and investments. The market that Patch of Land is serving is fragmented, locally delivered, and highly manual — it is ripe for disruption. Banks are exiting the space due to capital and liquidity constraints and hard money lenders are limited by a single source of capital and local footprint. Unlike these offline incumbents, Patch of Land has a national footprint, and uses proprietary software to quickly and reliably make first lien position loans, pre-fund those loans, and then crowdfund the financing from thousands of investors (both individuals and institutions) on a fractional or whole loan basis.

Who regulates P2RE? And what are the challenges there?

P2RE and the real estate crowdfunding sector is regulated by the SEC. Patch of Land operates under Title II, Regulation D, Rule 506(c) whereby we can only accept investments from accredited investors, as defined by the SEC. This is a strict regulation that requires thorough diligence and vetting of the accredited status of the investor. The biggest challenge we face is that we have many retail investors who want to invest with us and we cannot accommodate them.

How are the ripples in the capital markets affected or will affect business?

Capital markets volatility has not had an adverse effect on our business. Our capital sources are very diversified and are not dependent on large capital market players. Over 90 percent of our loan volume has been, and continues to be, funded by crowd capital. We have on-boarded multiple institutions of various sizes that buy loans on a fractional basis, in addition to the whole-loan forward flow agreements in place.

How is crowdfunding for real estate different from marketplace lending specifically?

Crowdfunding for real estate, specifically when referencing debt, is a subset of marketplace lending. Patch of Land is a ‘real estate marketplace lender’ because we focus specifically and exclusively on debt and do not offer any equity projects for funding. Equity deals are crowdfunding deals, not marketplace lending deals. Therefore, a real estate marketplace lender that transacts with individual investors can be considered a crowdfunding platform, and a crowdfunding platform that does not transact in debt is not a marketplace lender. Two other elements that differentiate crowdfunding from marketplace lending are: 1) prefunding, where the platform fully funds the loans upfront and therefore is not engaging in crowdfunding that usually involves raising capital first, before disbursing it to the sponsor/borrower; 2) marketplace lending includes institutional and individual investors who participate in loan purchases, whereas a crowdfunding model is focused exclusively on individual investors.

How is crowdfunding poised to change real estate investing?

Traditional real estate (debt or equity) can be highly time consuming. We offer an alternative to have real estate debt as part of a portfolio, bringing both new and experienced investors all the data they need to make a decision. Most would never have the time to aggregate this much data on their own, through traditional methods. Crowdfunding allows capital to flow more easily to across the nation, rather than locally, to places and projects that might have been shut out or simply left behind because they were too difficult to assess, evaluate and understand, or were the purview only of local investors and gatekeepers “in the know”. Crowdfunding puts investors in the driver’s seat, giving them the power to pick and choose investments that meet their personal risk/return needs. It allows for investment strategies that are both more “bespoke,” and yet more diversified -both in the way of product type and geographies, all through fractional investments across a technology enabled, online platform. Investors not only have broader choices of where to invest, but they can do it from their mobile phones in seconds.

Maxim Commercial Capital Delivered Creative Financing Solutions in Q3 2025

October 13, 2025LOS ANGELES, CALIF. (October 13, 2025) – Maxim Commercial Capital (“Maxim”) announced it countered industry trends during the third quarter of 2025 by delivering essential hard asset secured financing to small and mid-sized businesses across the nation. Maxim is a national provider of loans and leases from $10,000 to $3 million collateralized by class 6 and 8 trucks, trailers, construction and agricultural heavy equipment, and real estate. The company fuels entrepreneurship by offering attractive financing rates and terms for underserved market segments, including startups and borrowers with challenged credit.

“It was a noteworthy quarter for our team,” noted Michael Kianmahd, Maxim’s CEO. “Despite the industry-wide slowdown in originations, we stayed on course to structure and fund deals during trying economic and market conditions. We were thrilled to welcome Lyndon Elam as Chief Operating Officer and continued to develop and roll out performance enhancing technology tools.”

Maxim experienced a good flow of applications for over-the-road (OTR) used truck and trailer financing during the period. While strong demand held used truck prices steady, many lenders retracted, leaving vendors and buyers scrambling for reliable financing. Funded deals during the period included a $45K 2020 Kenworth T680 with 528K miles for 26% down for a subprime startup owner operator with a 621 FICO; a $48K 2020 Kenworth T680 with 501K miles for 25% down for an experienced subprime owner operator with a 581 FICO; and a $23K 2020 Utility Dry Van for an existing customer with challenged credit for 25% down.

In addition to OTR trucks and trailers, Maxim is a leader in financing vocational trucks, such as tow trucks and dump trucks, and helping borrowers consolidate expensive MCA debt by lending against owned heavy equipment and real estate. As equipment leasing rates became more expensive during the period, Maxim received applications from borrowers with strong contracts seeking to purchase equipment.

Creatively structured deals during the third quarter include 60% purchase financing for a newer, rapidly growing construction company to buy a $40K 2025 Equipter RB4000 to improve efficiency on construction sites. Traditional lenders had turned down the business owner due to her 681 FICO, newly opened $60K auto loan, and $25K in student loan debt. Another startup entrepreneur with a business plan to haul construction material and a committed driver got the $106K 2020 Mack GRANITE 104BR Dump Truck she wanted for 34% down, despite her 541 FICO and discharged bankruptcy from 2018.

“One reason I was attracted to join Maxim is their creative, flexible approach to working with equipment vendors, finance brokers, and borrowers,” said Elam. “Our team takes the time to optimize financing structures, such as by asking about excess equipment or real estate collateral to improve advance rates or helping a borrower understand true affordability based on cash flow. This results in high approval to submission rates which is a key goal for all lenders.”

About Maxim Commercial Capital

Maxim Commercial Capital helps small and mid-sized business owners nationwide by providing loans and leases (“financing”) from $10,000 to $3 million secured by trucks, trailers, heavy equipment, and real estate. It funds equipment purchase financings and leases, working capital, and debt consolidations. Maxim’s more creative financing structures leverage equity in real estate and owned heavy equipment to facilitate growth and preserve customers’ cash. As a leading provider of transportation equipment financing, Maxim supports startup and experienced owner-operators and non-CDL small fleet owners by funding loans and leases for class 8 and class 6 trucks, trailers, and reefers. Learn more at www.maximcc.com or by calling 877-776-2946.

###

Contact:

Michael Kianmahd, CEO

Maxim Commercial Capital

michael@maximcc.com

(213) 984-2727