CAN Capital’s Collateral ‘Adjustment’

December 24, 2016Last month, CAN Capital disclosed that they had “self-identified that some assets were not performing as expected” on the same day that three of the company’s top executives were put on leave. Since then it’s been reported that a discrepancy arose when CAN’s old systems were not equipped to handle the shift from variable payment advances to fixed payment loans. This is notable given that CAN began doing fixed payment loans all the way back in April 2010.

The discrepancy found its way into CAN’s 2014 securitization. S&P Global Ratings recently reported on this that “there was a correction of previously misclassified assets that affected the results of the calculation of [the] adjusted performing asset balance” on CAN Capital Funding LLC Series 2014-1.

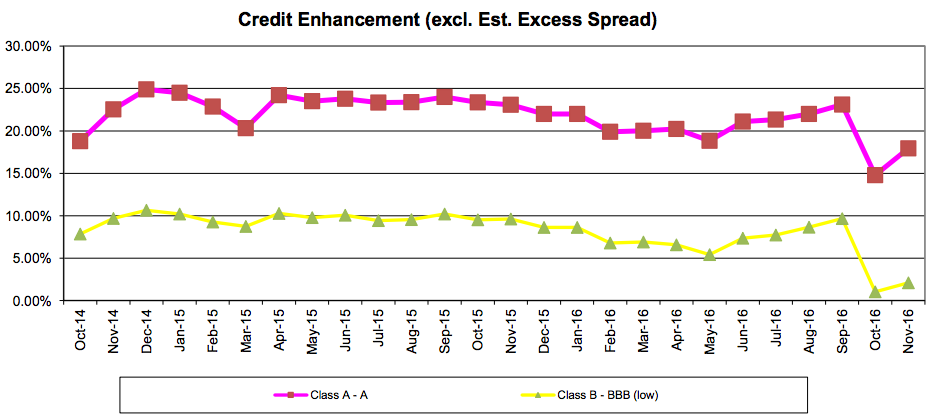

Ratings agency DBRS illustrates the collateral dip on CAN’s securitization once the classifications were reported correctly on Series 2014-1 below.

This is the first public glimpse into what CAN’s old systems got wrong and by how much.

The drop triggered a rapid amortization event, potentially causing liquidity issues for CAN, hence why new funding may be paused. The principal balance on the $200 million notes has dropped by nearly $70 million in the last two months, indicating big payouts.

The process to manage a rapid amortization event is described in the original DBRS ratings report. The implications aren’t good given that this appears to be brought on by misclassifying assets rather than a natural deterioration of loan performance.

Last week, CAN laid off nearly half of its employees as it tries to correct course.

Update: On December 25th, AltFinanceDaily published a brief of a newly discovered lawsuit filed against CAN Capital on December 19th by an aggrieved shareholder alleging the company had failed to pay her a $150,000 settlement payment.

CAN Capital Woes Continue – Layoffs Commence

December 16, 2016More information is slowly starting to come out about the recent C-level removals at CAN Capital. In the meantime, the company announced major layoffs just before the holidays. American Banker says the number is 136 employees laid off just at CAN’s Kennesaw, GA office.

Multiple brokers that have done business with CAN in the past have told AltFinanceDaily that CAN is not actually servicing renewals for existing customers or that they’re only doing them on a highly selective basis, despite what the company said two weeks ago.

The company’s chief executive officer, chief financial officer and chief risk officer were all put “on a leave of absence” in late November after discovering that “some assets were not performing as expected and that there was a need for process improvements in collections.” All of their names have been removed from the leadership page on the company’s website.

While the collective expectation has been that CAN would resume funding new business again in January, the wave of layoffs do not inspire confidence. No executive replacements have been named and CAN’s chief legal officer still remains in place as the company’s “acting chief executive.” It’s a bizarre sequence of events that seems to indicate there will not be a return to normalcy any time soon.

The CAN Capital Shakeup Is A Sign of the Times

November 30, 2016Update 11/30 7:30 pm: CAN says they are still open for business and still providing access to capital for current customers and renewal business. They are not actively seeking new business at this time, but will evaluate it as it comes in.

Part II of the industry’s season finale has begun. On Tuesday afternoon, CAN Capital confirmed that CEO Dan DeMeo had been put on a leave of absence. The chief risk officer and chief financial officer have also reportedly stepped down. Parris Sanz, the company’s chief legal officer, is now running the company, a CAN spokesperson said. His new title, acting head (which is how their statement referred to him), is perhaps a subtle clue that the company did not plan these moves far in advance. And it’s the phrasing that’s used to describe the departure of these executives that’s worth raising an eyebrow. A leave of absence? A curious fate indeed.

Part II of the industry’s season finale has begun. On Tuesday afternoon, CAN Capital confirmed that CEO Dan DeMeo had been put on a leave of absence. The chief risk officer and chief financial officer have also reportedly stepped down. Parris Sanz, the company’s chief legal officer, is now running the company, a CAN spokesperson said. His new title, acting head (which is how their statement referred to him), is perhaps a subtle clue that the company did not plan these moves far in advance. And it’s the phrasing that’s used to describe the departure of these executives that’s worth raising an eyebrow. A leave of absence? A curious fate indeed.

In an exclusive interview AltFinanceDaily conducted with DeMeo last year, he said of CAN at the time, “it’s a self-sustaining business. We’re not forced to approach the capital market to cover our burn rate. We’re cash-flow positive.”

But more recently, there’s a different tone. A spokesperson for CAN said that the company had “self-identified that some assets were not performing as expected and that there was a need for process improvements in collections.” The sudden decapitation of the company’s top officers seems a harsh consequence for this apparent underperformance, especially given that CAN has long been on the short-list as a potential IPO candidate. DeMeo himself had been with the company since 2010, having started originally as the CFO and rising to the CEO position in 2013.

While CAN Capital is a private company, they are notable in that they have originated more than $6 billion in funding to small businesses since 1998 and secured a $650 million credit facility led by Wells Fargo just last year.

Some of CAN’s ISOs report being told that originations have been put on hold until January. A source with close knowledge of the company however, said that’s not correct. The Financial Times reported though that CAN had paused new business until the end of the year and would only be servicing current customers. And they might indeed need time to upgrade their systems since American Banker cited an unnamed source that said “problems arose when CAN Capital used old systems, which were not designed to require daily repayments, to collect money owed by term loan borrowers.”

Some outsiders are not surprised by what’s going. Alex Gemici, the chief revenue officer of World Business Lenders (WBL), said that it’s an indicator that uncollateralized lending is not the panacea everyone thought it was. “What we’ve been saying all along is right there on AltFinanceDaily,” Gemici said, while directing me to the prediction they made a year ago that appears right on this website. At a December 2015 event at the Waldorf Astoria, WBL CEO Doug Naidus told a crowd comprised mostly of his company’s employees that he believed the bubble was about to burst. He doubled down on that prophecy in an interview four months ago in which he chided companies for having forsaken sound underwriting.

Is he right? In the last six months, the CEOs of Lending Club, Prosper and CAN Capital have all stepped down. Avant shed a lot of its staff. Dealstruck, Circleback Lending and Windset Capital have stopped funding. Confidence in the business side of alternative finance has also started to slip on a measurable basis before the election even happened.

“I believe companies are experiencing higher than normal losses due to a serious lack of proper underwriting practices, policies, and procedures,” said Andrew Hernandez, a managing partner at Central Diligence Group, a company that specializes in risk analysis who wasn’t commenting about any lender specifically. “As I say to people not familiar with the space, ‘putting the money out is the easy side of the business; getting it back is what proves to be the most difficult.'”

But CAN has not specifically fingered underwriting practices as the reason for their management shakeup, instead leaning towards it being a lapse in their process as the company grew. “It became clear that our business has grown and evolved faster than some of our internal processes,” they said in their statement.

The only alternative business lender funding more annually is OnDeck, a company that has garnered its fair share of criticism over its lackluster financial performance. Their stock is currently down a whopping 77% from the IPO price, but they have put on a good face for the industry they lead. The familiarity of their famous CEO and the decade in business under their belt arguably even has a calming effect on the tumultuous world of financial technology startups.

OnDeck too though, has been referenced in the context of bursting bubbles. Less than two years ago, RapidAdvance chairman Jeremy Brown voiced concern that the industry was heading into unsustainable territory, even going so far as to call out OnDeck by name. “When I see some of the business practices, offers, terms and other aspects of our business today, I am worried,” he wrote. “I am worried because I believe that 2008 has been too quickly forgotten, and very few, other than those of us that were on the front lines on the funding side at that time, appreciate what happened to outstanding portfolios at that time when average duration was 6 months and no deals were written over 8 months.”

For risk experts like Hernandez of Central Diligence Group, he thinks the newness of everything has been part of the problem. “I believe [funding companies] have faced a big hurdle in acquiring talent,” he said while adding that funding companies can be forced to hire underwriters with no prior knowledge of the product just to keep up with the growth.

While still very little is known about what exactly happened at CAN Capital, most people that AltFinanceDaily spoke with were shocked that anything could happen there at all. “It’s insane,” said the chief executive of another competitor who wished to remain anonymous. “This is CAN we’re talking about.”

A sign of the times?

Shakeup at CAN Capital – CEO and 2 other Execs Put on Leave of Absence

November 29, 2016Update 11/30 7:30 pm: CAN says they are still open for business and still providing access to capital for current customers and renewal business. They are not actively seeking new business at this time, but will evaluate it as it comes in.

CAN Capital has confirmed that CEO Dan DeMeo has gone on a leave of absence. The company’s chief financial officer Aman Verjee and chief risk officer Kenneth Gang have also reportedly stepped down. Parris Sanz, the company’s Chief Legal Officer, has been made acting head of the company, while Ritesh Gupta has been promoted to COO.

A statement from CAN Capital is below:

“As the board and our leadership team conducted our business reviews and looked at how we can best position the firm for future growth, we self-identified that some assets were not performing as expected and that there was a need for process improvements in collections. It became clear that our business has grown and evolved faster than some of our internal processes. As we work to improve these processes, the Board has named twelve-year CAN Capital veteran and senior executive, Parris Sanz acting head of the company and promoted Ritesh Gupta to COO, while Dan DeMeo, CEO, and two other members of his team are on a leave of absence. Over the past 18 years CAN Capital has consistently made decisions to position ourselves for growth and leadership in the industry and we look forward to helping small businesses succeed for many years to come.”

Some of CAN Capital’s referral partners have reported to us that the funding of new deals has been put on hold until January 2017. This could not be confirmed, however. (Update: This was later confirmed)

More than just an industry leader, CAN was founded in 1998 and is widely regarded as the first merchant cash advance company. A year ago, AltFinanceDaily featured Dan DeMeo and CAN in a story to mark their success. As of April this year, they had funded more than $6 billion since inception. In August, they secured a coveted partnership with Entrepreneur Magazine.

Having secured a $650 million credit facility last year led by Wells Fargo, they are the second largest player in the alternative business finance industry behind OnDeck.

Sanz joined the company in 2004 with more than 12 years of experience as a corporate, securities, and transactional attorney. Before joining CAN Capital, he was a senior executive and General Counsel of a specialty pharmaceutical company, the successful sale of which he led in 2003. Prior to that, Sanz was an attorney in private practice at the law firms of Latham & Watkins in Los Angeles and Paul, Hastings, Janofsky & Walker in San Francisco, where he handled a wide variety of M&A transactions, securities offerings including IPOs, and other corporate transactions, and acted as outside general counsel to a number of technology start-ups.

Sanz received his J.D. from Harvard Law School in 1993 and a Bachelor of Arts degree from U.C. Berkeley, High Honors and Phi Beta Kappa, in 1990. Sanz is admitted to practice in California and Washington, D.C., is a registered In-House Counsel in New York, and is also admitted to practice before the United States Court of Appeals for the Federal Circuit.

Bizfi Originates $144 Million in Q2; CAN Capital, Entrepreneur Media Launch Funding Center

August 16, 2016 Online small business loan marketplace, Bizfi said that it originated over $144 million in Q2 this year, a 25 percent increase compared to $116 million in Q2 last year. The New York-based company has facilitated financing for more than 3,580 small businesses through its platform.

Online small business loan marketplace, Bizfi said that it originated over $144 million in Q2 this year, a 25 percent increase compared to $116 million in Q2 last year. The New York-based company has facilitated financing for more than 3,580 small businesses through its platform.

The company forged many partnerships to expand its customer base and access to small businesses. In March of this year, Bizfi announced a partnership with Western Independent Bankers (WIB), a trade association with community and regional banks across the Western United States and in July, it joined hands with the National Directory of Registered Tax Return Preparers & Professionals (PTIN).

Bizfi also secured a $20 million investment from New York-based investment manager Metropolitan Equity Partners in June this year, supplementing the $65 million infusion in December last year to expand and optimize its funding programs and develop an effective marketing campaign to advertise those better.

In other news, small business lender CAN Capital and Entrepreneur Media launched the funding center offering funding products that include term loans — available from $2,500 up to $150,000 for a single location with range of terms from 3 to 36 months. Trak loans which are working capital loans available from $2,500 up to $150,000 and installment Loans provide funding from $50,000 to $100,000 with 2, 3, and 4 year terms and have fixed monthly payments.

CAN Capital Makes Prized Alliance With Entrepreneur Media Inc

May 2, 2016CAN Capital partnered with Entrepreneur.com to create another channel of funding small businesses.

Last month (April 7th), the 18 year old company surpassed $6 billion in small business funding and later this year, it will launch Entrepreneur Lending Powered by CAN Capital to process working capital loans on behalf of the media giant.

“As we get ready to celebrate National Small Business Week, we are excited to work with Entrepreneur Media to continue delivering on our vision of helping small businesses grow and achieve their goals through fast access to funding,” said Daniel DeMeo, CEO of CAN Capital.

The New York-based company which uses propriety data-driven models has made over 170,000 individual fundings including restaurants, medical offices and beauty salons. Last year, the company introduced two new special small business loans – TrakLoan, which adjusts daily payments with daily card sales and a monthly installment loan product offering a customer longer terms with higher transaction sizes.

The New York-based company which uses propriety data-driven models has made over 170,000 individual fundings including restaurants, medical offices and beauty salons. Last year, the company introduced two new special small business loans – TrakLoan, which adjusts daily payments with daily card sales and a monthly installment loan product offering a customer longer terms with higher transaction sizes.

This comes in the context of small businesses being underfunded. Business Insider recently reported that “only half of small businesses with $100,000 to $1 million of annual revenue received at least some of the financing they applied for from large banks in late 2015.”

As banks wrestle with tight lending practices, online lenders have filled the gap for providing quick and smaller loans to businesses who need prompt financing.

CAN Capital Crosses $6 Billion in Small Business Funding

April 7, 2016

CAN Capital has surpassed the milestone of providing more than $6 billion in working capital to over 70,000 small businesses over 18 years.

Since they have a strong track record of repeat business, the company has actually made over 170,000 individual fundings across restaurants, medical offices, beauty salons and more. Last year, the company introduced two new special small business loans – TrakLoan, which adjusts daily payments with daily card sales and a monthly installment loan product offering a customer longer terms with higher transaction sizes.

The New York-based company was founded in 1998 and uses propriety data-driven models to underwrite loans and advances. CAN Capital is one of the early companies in the space that has seen much overhaul over the past few years with a slew of new companies offering a variety of working capital products distributed through a number of channels. “There has been an evolution both in product and distribution over the years,” said Daniel DeMeo, CEO of CAN Capital. “From a single type of loan and monolithic distribution, we have come to work with big changes in underwriting and decision making,” he said.

It helps to have a favorable economic environment for small businesses to thrive in. The Federal Reserve, in its part has kept borrowing rates unchanged in a decade with only a marginal hike. Small business borrowing also peaked in February touching 17 percent after hitting a two-year low the previous month.

CAN Capital: Beyond Hyperbole

December 11, 2015 It’s usually risky to say “first,” “largest” or “best,” but CAN Capital invites those superlatives and more.

It’s usually risky to say “first,” “largest” or “best,” but CAN Capital invites those superlatives and more.

Asked whether the company’s the biggest in the alternative funding business, CEO Dan DeMeo hedges only a little with qualifiers like “might” or “probably” before proudly announcing that the company has provided access to more than $5.5 billion in working capital through 163,000 fundings to merchants operating in over 540 different kinds of businesses.

Glenn Goldman, the company’s CEO from 2001 to 2013 and now Credibly’s chief executive, doesn’t mince words about his former employer when he calls CAN Capital the biggest and most profitable small business alternative finance company in the U.S.

Cofounder and Chairman Gary Johnson proclaims without hesitation that CAN Capital was the first alternative small business finance company. His wife and cofounder, Barbara Johnson, came up with the idea of the Merchant Cash Advance in 1998 when she had trouble raising funds to promote her business, he said.

CAN Capital developed the first platform to split card receipts between the merchant and funder, and it gave birth to the idea of daily remittances, Johnson continued. Within a few years of its founding the company was turning a profit, another first in alternative finance, he claimed.

The innovation continued from there, according to Andrea L. Petro, executive vice president and division manager of Lender Finance, a division of Wells Fargo Capital Finance. She cited a couple of possible firsts she’s witnessed in her dealings with CAN Capital.

When CAN Capital received a loan from Wells Fargo in 2003, it may have been the first sizeable placement in the alternative finance industry by a major traditional financial institution, Petro said. In 2010, CAN Capital was among the first alternative funders to offer direct loans, she noted.

Petro stopped short of characterizing CAN Capital as the best in the alternative finance business, but she praised the company’s management and lauded its systems for underwriting and monitoring funding. “They continually upgrade their systems, upgrade their software, upgrade their people,” she said.

Calling CAN Capital one of the best comes naturally to Kevin Efrusy, a partner at Accel Partners and a CAN Capital board member. Accel saw opportunity in alternative finance because banks were reluctant to lend at the same time that an explosion of data on small businesses was informing the underwriting process. When Accel sought a position in the industry, it contacted CAN Capital, he said.

“Frankly, CAN Capital didn’t need or want our money,” Efrusy said. “We approached them.” Five years ago, Accel convinced CAN Capital that additional resources could help the company grow, and it bought a stake in the company.

With so many extolling the virtues of CAN Capital, AltFinanceDaily asked DeMeo for a look at the thinking that underlies the success.

PLOTTING STRATEGY

CAN Capital pursues a strategy that DeMeo visualizes as a honeycomb. In the center cell, he places the objective of “helping small businesses succeed.” The compartmental element above that provides a place for the goal of serving as “the preferred provider of financial solutions to small business,” he said. The company’s cultural values, summarized as “Care, Dare and Deliver,” reside in the compartment below the center cell as table stake underpinnings, he added.

DeMeo also describes the company as driven by four strategic planks: “1) Expand the market, 2) broaden the product set, 3) deepen relationships with customers, and 4) achieve operating excellence,” he said.

What does success look like to the company? To DeMeo, it’s dramatic growth in the number of customers, resulting in increased revenue, a more valuable company and better career opportunities. “Digital automation and customer experience are at the center of those efforts,” he said.

CAN Capital operates with a “huge appetite for ‘test and learn,’” according to DeMeo. “That’s how we keep innovation alive,” he said.

And the result of all that? The company has increased fundings by 29 percent (CAGR) and revenue by 24 percent (CAGR), with corresponding growth in earnings, DeMeo said. It has also grown its digital business by 600 percent since 2014, he noted.

AT THE WHEEL

AT THE WHEEL

DeMeo, the man at the top of CAN Capital, joined the company in 2010 as chief financial officer and became CEO early in 2013. He was previously CFO at 1st Financial Bank, and also served as CFO for JP Morgan Chase’s consumer and small business unit. DeMeo also was chief marketing officer and ran business development head for GE Capital’s consumer card unit. His career began at Citibank, where he held senior roles in marketing and customer analytics.

“I was very fortunate to work for some pedigree companies earlier in my career,” DeMeo said. “Those companies emphasized market based training and development, and I worked with very smart and hardworking people. I also had great experience in unsecured lending.” His formative years left him with great appreciation for “behavioral analytics and the quantitative, information-based approach to business finance.”

Experience convinced him, as a CEO, the importance of attention to the balance sheet and income statement. It’s vital to combine that with innovation and growth orientation, DeMeo said. He seeks to lead, inspire and motivate employees, he emphasized.

DeMeo grew up in Atlantic City, NJ, with parents who valued hard work, education and maximizing opportunity. His wife and three children have supported him in his career despite the long hours and dedication necessary for success.

At CAN Capital DeMeo has faced the challenge of managing the business through internal and external cycles. Running the company often comes down to balancing what customers want with what makes economic sense, he said. “Pigs eat, and hogs get slaughtered,” he maintained. “You can’t get too greedy.”

DeMeo runs the company without the help of a President or Chief Operating Officer. While DeMeo serves as the public face of the company, he also devotes himself to every aspect of operations, he said.

WHAT’S IN A NAME?

Although CAN Capital’s drive for technological innovation and its measured approach to fundings have remained constant, the company has renamed itself several times to fit changing times.

In November 2013, it rebranded itself publicly as CAN Capital, and the company now provides access to business loans through CAN Capital Asset Servicing Inc, and Merchant Cash Advances through CAN Capital Merchant Services.

With the CAN Capital rebranding, it dropped the umbrella name of Capital Access Network. At the same time, it retired the AdvanceMe, New Logic Business Loans and CapTap names.

Most of the company’s old names applied to products or distribution channels, DeMeo said. The company had added them when it presented a new product, such as loans, or introduced a way of going to market, like end-to-end digital technology.

Consolidating the names reflected the company’s decision to put its direct marketing efforts on equal footing with business generated by partner companies, DeMeo said. Having just one name would result in a more efficient approach to building a stronger brand, he noted.

“The opportunity is to create one brand, multiple products and omni channel distribution under one company,” he said. “For a company our size, it would be hard to create brand awareness if you had to put significant promotional support behind every one of those sub brands.”

CAN Connect is a sub-brand that has survived. “That’s not a product name or distribution channel name,” DeMeo said. “It’s the technology suite we use to connect with partners so that we can exchange information in real time.”

CAN Connect is a way to speed up the process and eliminate friction for customers and partners. For example, a partner is able to link their CRM directly into CAN Capital’s decision engine, eliminating manual steps in submitting and generating offers. For partners with a customer-facing portal, CAN Connect enables an offer to be made available in real time to a small business owner, taking advantage of data sharing APIs to tailor the marketing message to fit the prospective customer’s needs.

Attention to detail pays off in repeat business for CAN Capital, in DeMeo’s view. “Almost 70% of our merchants return for another contract,” he said

THE GENESIS

By all accounts, CAN Capital is a company born of necessity. Barbara Johnson, who had the brainstorm that became CAN Capital, was running four Gymboree playgroup franchises in Connecticut and needed funds to finance summertime direct marketing efforts for fall enrollment.

But her company didn’t have much in the way of assets to pledge, so banks weren’t interested in providing funds. Why, she reasoned, couldn’t she just borrow or receive an advance against the credit card receipts she knew would flow in when the kids came back in the autumn? Thus, she gave birth to an industry.

Barbara Johnson and her husband, direct marketing executive Gary Johnson, cofounded the company as Countrywide Business Alliance and put up their own money to build a computerized platform to split card revenue, Gary Johnson said.

Then they persuaded a card processor to partner with them. Once they were operating and had signed their first customer, venture capital began flowing their way to grow the business. These days, the Johnsons remain major shareholders.

“What made it an interesting concept was how huge the market potential was,” Gary Johnson said. “That’s what the attraction still is today.” Although Merchant Cash Advances may now seem commonplace, they were startling at first, he said. “When we first went out in the marketplace, everybody thought it was a crazy idea,” he noted.

The company earned patents on processing related to Merchant Cash Advances and daily remittances, Gary Johnson said. At first, the patents deterred potential competitors from entering the business, but the company was unable to defend the patents successfully in court. Rivals then entered the fray.

Just the same, the company became profitable early on through “deliberate decision-making, having the right people in place and being bigger than everybody else,” he said.

Much of the company’s early business came through firms that provide merchants with transaction services, and that remains the case today, DeMeo said. Many were placing point of sale terminals in stores and restaurants to accept credit cards, and working capital became an upsell or cross-sell, he noted.

The large base of business CAN Capital built with merchant services companies means it will always be an important channel for the company. Recently, new merchant sign-ups have come from more diverse channels, including cobranded and referral partners, and the fast-growing direct marketing channels.

From the beginning, the merchants receiving capital used it to grow their businesses, DeMeo said. “That feeds the whole economic system and creates jobs,” he said.

TODAY’S NUTS AND BOLTS

TODAY’S NUTS AND BOLTS

Daily remittances give CAN Capital nearly constant insight into how well customers are performing, which enables the company to discover potential issues quickly and take action. Such close monitoring also provides the company with enough information to enable funding opportunities that competitors might pass up, DeMeo said.

“The basis for our decisions is how the business performs and business-specific indicators, such as capacity and consistency, versus looking at the personal credit history of the business owner,” DeMeo noted.

Having that data also helps the company create models it can use to serve other businesses in the same classification, DeMeo said. “It’s poured into machine learning for future decisioning,” he maintained. “It’s a cool concept, right?”

The company’s 450 or so employees work in several locations. Three hundred of the total are attached to the office in Kennesaw, GA, the region where the company first set up operations. To this day, that’s where the company conducts most of its business, DeMeo said.

About 25 employees work in technology and operating support in offices in Salt Lake City because the area offers a strong talent pool and provides the company with additional time zone coverage, DeMeo said.

Some of the company’s former executives came from Western Union, which had a presence in Costa Rica. About a hundred employees are now stationed there, working on technology, maintenance and development. That location also houses back-office redundancy for the company, too.

On Manhattan’s 14th Street, the company has 30 or so employees, who include digital engineers, marketing and business development teams, the human resources lead, the chief financial officer, the chief legal officer, and the chief executive officer. The company moved its executive office there from Scarsdale, NY to take advantage of the digital boom, he said, adding that, “Google’s right around the corner.”

On Manhattan’s 14th Street, the company has 30 or so employees, who include digital engineers, marketing and business development teams, the human resources lead, the chief financial officer, the chief legal officer, and the chief executive officer. The company moved its executive office there from Scarsdale, NY to take advantage of the digital boom, he said, adding that, “Google’s right around the corner.”

Compared with most companies in alternative finance, CAN Capital has little venture capital as part of its ownership structure, DeMeo said. “It’s a self-sustaining business. We’re not forced to approach the capital market to cover our burn rate. We’re cash-flow positive.” Competitors have to borrow to fund their growth, he noted.

The company has taken on infusions of debt financing, not equity financing. In the latter, a company is selling part of itself, DeMeo said. “We raised $650 million from a syndicate with five new banks and 10 banks in total.” The company completed a securitization of $200 million the year before, he said.

CAN Capital recently introduced the new TrakLoan product that has no fixed maturity date, with daily payments that are based on a fixed percentage of card receipts. This way, payments ebb and flow with the merchant’s card sales. CAN Capital is also testing “bank-like” installment loans of as much as $500,000 with a payback period of up to four years.

And there’s nowhere to go but up, in the view of CAN Capital executives. With a market of 28 million small American merchants and penetration of between 5 and 10 percent, they see plenty of potential to keep earning superlatives.