Ikea Invests in BNPL Service, Will Use Own Brand for Lending

August 31, 2021 Ikea’s majority parent company Ingka Group announced on Tuesday that they will join the buy-now-pay-later (BNPL) space with Jifiti, a group that offers flexible payment options. Jifti will also allow Ikea to keep their name, making it appear to consumers that Ikea is offering the service themselves — not a third party.

Ikea’s majority parent company Ingka Group announced on Tuesday that they will join the buy-now-pay-later (BNPL) space with Jifiti, a group that offers flexible payment options. Jifti will also allow Ikea to keep their name, making it appear to consumers that Ikea is offering the service themselves — not a third party.

What separates Jifiti from other BNPL services is their willingness to allow companies to use their own names in the borrowing process, so the company themselves appear as the lender. This use of their own brand in the checkout process when offering the BNPL service encourages customers to use the service as Ikea’s brand recognition and reputation are universally top tier in their industry. Combined with their business model of cost efficiency and great service through do-it-yourself assembly, customers may be intrigued to use BNPL if they are under the impression that they are borrowing from a company they already trust.

Jifiti will require credit checks, and may charge interest to buyers who choose to utilize the payment options, but Ikea has the option to pay the interest on products financed through these services in a promotional capacity, to encourage customers to use the service to purchase more. By taking a stake of $20 million in Jifiti and not just using their service, Ingka group will be able to see how these tools are utilized and get insight on how the industry works between both the lending process, consumer payback, and default rates throughout Jifiti’s entire book of business.

This is one of the many moves in an exploration of the financial scene for Ikea’s parent company, as Ingka Group acquirred 49% of Swedish Bank Ikano in Feburary. It seems as if as the company is looking to host a full array of financial services both in store and online at Ikea sometime in the future.

Despite offering access to credit for more expensive items previously, Ikea will partner with Jifiti so that consumers can have access to flexible payment options on products that aren’t priced in the thousands. While it may encourage customers to overspend or indulge if they choose to use the service, those same customers will not be able to purchase in the future if they’re still paying off their previous purchases.

A Lawsuit Against Marcus Lemonis & Others is Alleging That “The Profit” Is Scamming Small Businesses

August 22, 2021 Marcus Lemonis, the star of CNBC’s show The Profit, is no stranger to litigation, but a proposed amended complaint recently filed against him in a year-old dispute really lets loose. The 165-page grievance reads like its own reality show, in which plaintiffs assert that Lemonis is nothing more than a fraud.

Marcus Lemonis, the star of CNBC’s show The Profit, is no stranger to litigation, but a proposed amended complaint recently filed against him in a year-old dispute really lets loose. The 165-page grievance reads like its own reality show, in which plaintiffs assert that Lemonis is nothing more than a fraud.

“While he pretends to be savior on TV to save businesses, Lemonis actually and purposefully sets out to acquire them for himself and ruin them financially,” plaintiffs contend.

Forbes turned the allegations in the proposed amended complaint into an exposè about Lemonis and his TV show, leading with a photo of him that is captioned, “The Profit or Profiteer?” It racked up more than 33,000 views in the first 24 hours at last count by AltFinanceDaily.

But the lawsuit filed by Nicolas Goureau, Stephanie Menkin, and ML Fashion, who were first filmed for the show in 2014, is a bit overshadowed by the fact that this is their 2nd amended complaint and that a motion to dismiss their previous one was already pending.

The latest one highlighted by Forbes is communicated to the public as being the culmination of an “eight-month investigation” carried out with the help of a “former district attorney and a top law school professor, and a world renown psychiatrist that was spurred by the coming forward of no less than seventy (70) family businesses that have been destroyed…”

The identities of the people who carried out the “investigation” are not shared and the 70 “destroyed businesses” are not co-plaintiffs. At times, it is hard to take the complaint seriously when it casually asserts sensational facts, like one that says a participant on the show killed themselves but it doesn’t say who they were, where they worked, or any other details about the death.

Plaintiffs are seeking at least $12 million in damages and they have just added NBC Universal Media, LLC as a defendant.

Lemonis contends that the plaintiffs earned $3 million for their labor and that they charged $1.3 million in personal expenses on the company credit card.

Overall, it’s probably unwelcome press for the show given that the eighth season just debuted. Many people in the small business finance community are fans of the show. In 2017, Lemonis personally criticized Kabbage, saying that they weren’t a friend of small business.

Lemonis is currently hosting a contest on twitter where small businesses are competing to win $10,000 by submitting their pitch.

Win $10,000 for your business …. Make your best pitch … must use #TheProfit to submit your pitch pic.twitter.com/8CuZAN5SJ0

— Marcus Lemonis (@marcuslemonis) August 21, 2021

Reliant Funding Announces Steve Kietz as New CEO

August 10, 2021Industry veteran and former Chief Marketing Officer is appointed Chief Executive Officer of the leading alternative finance company

San Diego, CA (August 10, 2021) – Reliant Funding, a leading small business finance company, today announced that it has named Steve Kietz to the role of Chief Executive Officer. Kietz previously served as the firm’s Chief Marketing Officer. The industry veteran will guide Reliant Funding on its mission to continue providing world-class, customized finance solutions for American Small Businesses.

As CMO, Kietz was instrumental in expanding Reliant Funding’s marketing, risk and technology initiatives. He is a seasoned financial services professional with a more than 30-year track record of leading successful teams and is widely recognized as an industry leader in cultivating strategic partnerships. Prior to joining Reliant, Kietz served as President of Inte Q, was Founder and CEO of Mobile Money Ventures (which was acquired by Intuit), and held leading roles at Citi and JP Morgan, including President of Citibank Direct. Outside the profession, Kietz has volunteered as Vice President of the Familial Dysautonomia Foundation for over 30 years.

Commenting on his appointment, Kietz said, “I’m excited and grateful for the opportunity to lead Reliant Funding into a new era, where we are positioned as industry leaders in delivering value to our customers. The company has a long history of providing outstanding financial solutions to small businesses and I am deeply humbled to continue this legacy. I am excited to lead a team of great people and I look forward to continuing to execute our mission.”

Commenting on his appointment, Kietz said, “I’m excited and grateful for the opportunity to lead Reliant Funding into a new era, where we are positioned as industry leaders in delivering value to our customers. The company has a long history of providing outstanding financial solutions to small businesses and I am deeply humbled to continue this legacy. I am excited to lead a team of great people and I look forward to continuing to execute our mission.”

Reliant Funding has grown rapidly as it seeks to help small businesses across the country in achieving their financial goals, having provided nearly $2 billion in funding to over 30,000 companies since 2008. The nationally recognized company works to provide tailored financial solutions, regardless of business size. Reliant Funding is owned by Angelo Gordon, a leading global alternative investment firm that provides research-driven investment solutions, driven by their 30+ years of expertise.

Art Peponis, Head of Private Equity at Angelo Gordon, said, “Steve has been instrumental in building Reliant Funding to the leading alternative finance company it is today and has been pivotal in its ability to continue to provide support to small businesses impacted by the devastating COVID-19 pandemic. His decades of expertise, innovative perspective and dedication to our people and small businesses made him the perfect fit as the new CEO of Reliant Funding. We’re confident that he will continue to provide American small businesses with the access to funding they need and the service that assists them in accomplishing their goals. The future is bright for Reliant Funding.”

For more information on Reliant Funding, please click here.

Reliant Funding, headquartered in San Diego, provides customized, short-term funding to small and mid-sized businesses nationwide. For more information, please visit www.reliantfunding.com.

Angelo Gordon, headquartered in New York City, is a global alternative investment company, focused on credit and real estate. For more information, please visit www.angelogordon.com.

Cross River Bank Makes Moves as Fintech Acquirer, VC

July 13, 2021 Known in the space as the fintech partner bank, Cross River took another step down the path leading the industry: Last month, the bank bought PeerIQ, a company that does data analytics for loan underwriting. The bank also launched a venture capital arm to continue investing in startup fintechs in a more formalized way- though they have been partners for years.

Known in the space as the fintech partner bank, Cross River took another step down the path leading the industry: Last month, the bank bought PeerIQ, a company that does data analytics for loan underwriting. The bank also launched a venture capital arm to continue investing in startup fintechs in a more formalized way- though they have been partners for years.

“PeerIQ is a company we’ve known for a number of years; we’ve been working with them, partnering with them and in various ways for two or three years,” Phil Goldfeder, Senior Vice President of Public Affairs at Cross River, said. “We recognized that we would probably better serve our customers and partners if we came together, so we’re happy that we’re able to acquire Ram [Ahluwalia, CEO of PeerIQ] and his team at PeerIQ and we’re excited about the collaboration moving forward.”

PeerIQ will function as a part of Cross River, bringing intelligent analytics to every transaction. Cross River, located 14 floors up just across the George Washington Bridge in New Jersey, has about $13.5 billion of assets and has originated more than $46 billion in loans since 2008, Bloomberg estimates. The way forward, as Goldfeder said, was through innovation, leveraging tech and teams like PeerIQ’s to better serve clients. That also means using the formal VC branch to help new firms grow their platforms and future acquisitions.

“Number one is to grow on PeerIQ’s core business, providing data analytics, and creating technology in the secondary market, but more importantly, for Cross River to help our partners and our clients serve,” Goldfeder said. “There’s, no question that we will continue to explore companies that would help strengthen Cross River and the fintech ecosystem and provide additional services to our partners.”

The bank has over 15 partnerships with top fintechs, like publicly traded Affirm, Rocket Loans, Coinbase, and private firms funded through VC rounds like Stripe. The bank most recently became a significant part of the PPP government emergency loan program. Ranking among giants like JP Morgan and Bank of America, Cross River ranked 6th overall for dollar amount approved. According to the bank, they doled out 490,000 PPP loans for a total of $13 billion, making up 4% of the entire program volume.

The bank has over 15 partnerships with top fintechs, like publicly traded Affirm, Rocket Loans, Coinbase, and private firms funded through VC rounds like Stripe. The bank most recently became a significant part of the PPP government emergency loan program. Ranking among giants like JP Morgan and Bank of America, Cross River ranked 6th overall for dollar amount approved. According to the bank, they doled out 490,000 PPP loans for a total of $13 billion, making up 4% of the entire program volume.

The way forward is clearly through embracing what it always has been at its base: the bank across the Hudson that is willing to partner with upstart brands and help them take over the world. With a flurry of consolidation purchases in the “post-pandemic” world (if that isn’t too early to say) that are only going to increase, Cross River seems to be on to something. Goldfeder said that Covid showed the rest of the world what the fintech space has known for ten years, that added value for customers and partners means innovation.

“Post-pandemic, where I think there was a larger recognition from the financial services industry of the need to innovate,” Goldfeder said. “Cross River is always known that we need to innovate… The post-pandemic dynamic we recognize that there’s tremendous value in creating a more formal venture arm to examine, explore companies that we can invest in to help them grow, help them succeed, and …. increase our support of our partners.”

Bloomberg reported Cross River is in secret talks to raise $200 million of funding at a valuation of $2.5 billion or more. The bank previously raised $100 million in 2018 in a round led by KKR, AltFinanceDaily reported, and in 2016 raised $28 million.

After Funding Millions, Alt Financier Hosts Funding CEO Challenge

May 25, 2021 Leo Kanell, a funder from Utah, runs the 7 Day Funding CEO Challenge, a seven-day marathon video livestream of inspirational and educational funding content.

Leo Kanell, a funder from Utah, runs the 7 Day Funding CEO Challenge, a seven-day marathon video livestream of inspirational and educational funding content.

“So how [the challenge works] is basically, we’re looking for communities, and we’re building a community,” Kanell said. “Our focus is how can we help existing loan brokers, and then how can we help people who are looking for an additional stream of income that they can do from home obviously with the pandemic.”

All the action happens in a livestream on Facebook.

“Everybody kept asking ‘we need some training,’ so we built out a custom website for them so that they can build their funding empire from home,” Kanell said.

Many of the brand new market entrants are sales-minded individuals that are interested in working from home. Kanell has a sales mind and a small business funding background. He grew up in a family of nine from a small town in Utah with a population of only 3,000. He knew he would be a salesman when he turned a summer painting business internship into a $60,000 operation. After college, he tried his hand at real estate, but after 2008 he started looking for another industry.

“I started and went ‘Well, I’m gonna need money for that business,'” Kanell said. “I started looking at the different options to get financing for that next business venture, and it was very difficult, especially for a new business, especially if you’re a pre-revenue business or you don’t have a lot of sales and or collateral.”

He realized SMB funding was the business he should be getting into so he jumped in with both feet. From there he veered into a business education program alongside products like business credit cards.

He soon said that he was doing well, but he heard the funding industry calling his name. “Everything pulled me back into funding,” Kanell said and he decided to combine his education system toward loan broker training programs. He said many brokers don’t realize startups and pre-revenue bushiness can qualify for 0% for up to 15 months.

Now, Kanell hosts an industry podcast that features financial industry guests, and alongside funding, he looks forward to building a community of broker and funder education services.

“We’re going to not only get you the best funding guaranteed, but we’re going to educate you and empower you along the way,” Kanell said. “They can work as direct funders and keep 100% of the commission, and that if they want us to do the work you know, we can do splits.”

Senators Marco Rubio, Sherrod Brown Renew Campaign to Ban COJs Nationwide

April 15, 2021 The Small Business Lending Fairness Act is back. Senators Marco Rubio and Sherrod Brown reintroduced a bill this week that failed to advance the two previous times it was introduced.

The Small Business Lending Fairness Act is back. Senators Marco Rubio and Sherrod Brown reintroduced a bill this week that failed to advance the two previous times it was introduced.

One of cornerstone objectives is to outlaw confessions of judgment from being used in business loan transactions nationwide.

“With this bill, we are taking another step toward protecting America’s small businesses—the foundation of our economy—by preserving the right of a business to be heard in a court of law before a potential credit default,” Rubio said. “I remain committed to protecting our small businesses from predatory, out-of-state lenders, and I urge my colleagues to join me in this effort.”

“When we let financial predators harm hardworking Americans through scams like confessions of judgment, we undermine the dignity of work,” Brown said. “This bipartisan bill would protect consumers and small business owners from predatory lenders that use legal tricks to strip away their hard earned money.”

This is not the first swipe at COJs. In 2019, New York passed a law that made it illegal to file a confession of judgment against a non-New York debtor in the New York state court system. However, this does not prevent a party from using another state’s COJ and filing the COJ in that respective state.

The federal bill was previously introduced in 2018 and 2019 and failed to advance both times. The text of the bill can be found here.

Gregory J. Nowak, Partner at Troutman Pepper, Has Passed Away

April 13, 2021 Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

The firm’s website introduced Nowak as a veteran attorney that was “sought after for advice on complex securities law matters, particularly on issues arising out of the Investment Company Act of 1940; the Investment Advisers Act of 1940; federal and state securities laws and regulations; broker dealer, FINRA, CFTC and NFA regulatory matters; and corporate and M&A transactions.”

That perfectly sums up the context in which I first encountered Nowak in 2017 when he spoke at a small event put on by the Alternative Finance Bar Association where I was the only non-lawyer in the entire audience. One might expect a presentation on the finer minutiae of securities law of which he gave, to be a mundane, easily forgotten experience for a financial journalist such as myself, but his energetic delivery and fluid command of the subject matter translated complex securities questions into a folksy debate wherein one could feel confident in resolving the Howey Test over the dinner table just as easily as they could in the courtroom.

In fact, I approached him afterwards to thank him on his presentation and even followed up later over email, asking if I might have the honor to list him as a recommended securities attorney on the AltFinanceDaily website. That was four years ago and as fate would have it, he remained the only recommended attorney that AltFinanceDaily formally listed under the securities category, despite my coming to know very many accomplished and competent attorneys in the same field of law.

Nowak was one of the earliest public voices in the world of merchant cash advance participations and syndication where the securities question was a consideration some weren’t even sure applied as the industry created new products and investing structures at a furious pace.

He spoke at AltFinanceDaily’s first major conference in 2018 on the subject of “Syndication and Raising Capital,” and he continued to generate recognition of the need for securities legal support in the burgeoning industry.

He was a co-author of an article published with a colleague at Pepper Hamilton LLP (now Troutman Pepper) that he had given permission to be reprinted on AltFinanceDaily in December 2018, titled MCA Participations and Securities Law: Recognizing and Managing a Looming Threat. It was read by more than 1,500 people on the AltFinanceDaily website that first day alone.

Nowak was highly sought out on merchant cash advance issues. “Most judges want to see consistency of treatment and that includes your vocabulary,” Nowak said in an interview with AltFinanceDaily in April 2019. “The word ‘loan’ should be banned from their email and Word files.”

Although our relationship was one of professional acquaintances, I often told those seeking advice about MCA syndication that they should “probably call Greg Nowak about that.”

In “Does Your Merchant Cash Advance Company Pass The Scrutiny Test?“, Nowak explained that funders that decide for business purposes to solicit money from investors, have to be careful not to run afoul of SEC rules. He said that he recommended funders treat these fundraising efforts as if they are issuing securities and follow the rules accordingly. Otherwise they risk being the subject of an enforcement action where the SEC alleges they are raising money using unregulated securities.

“You need to be very careful here because these rules are unforgiving. You can’t ignore them,” Nowak said.

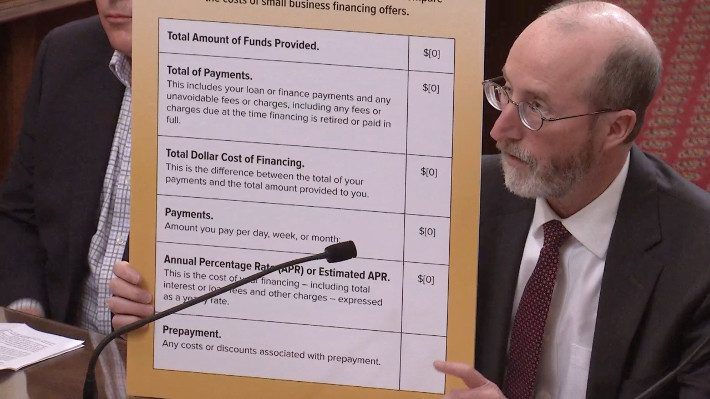

California’s Business Loan & MCA Disclosure Law Is Nearing Finality

April 13, 2021 Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

The 52-page document is the result of years of negotiations between various parties that all have a stake in its implementation. Among the finer details are the characteristics of the fonts permitted in the disclosures, what column a certain disclosure can be placed in, and the aspect ratio of the columns themselves.

But that’s the easy part. Here’s the hard part, according to a brief published in Manatt’s newsletter yesterday.

“The modified regulations continue to require use of the annual percentage rate (APR) metric, rather than annualized cost of capital (ACC), to disclose the total cost of financing as an annualized rate. This appears to be a final decision, which will make it difficult if not impossible for many commercial finance companies to comply given the significant challenges of calculating APR on products with substantial variance in the amounts and timing of payments or remittances.”

Manatt highlights other issues, including that all the necessary disclosures be provided “whenever a payment amount, rate, or price is quoted based on information provided by the proposed recipient of financing…”

This requirement, the firm says, is not even required under Federal Regulation Z for consumer loans.

“Many companies will not be able to comply with this requirement absent radical changes to their California application and underwriting procedures, as it is common today for companies to have preliminary discussions with applicants about potentially available financing terms before full underwriting has been completed.”

Manatt’s newsletter on the issue can be found here.

Any interested person may submit written comments regarding SB 1235’s modifications by written communication addressed as follows:

Commissioner of Financial Protection and Innovation

Attn: Sandra Sandoval, Regulations Coordinator

300 South Spring Street, 15th Floor

Los Angeles, CA 90013

Written comments may also be sent by electronic mail to regulations@dfpi.ca.gov with a copy to jesse.mattson@dfpi.ca.gov and charles.carriere@dfpi.ca.gov.

The last day to submit comments is April 26, 2021