To Niche or Not to Niche, That Is the Fintech Question

October 1, 2019 A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

In the past decade, the fintech industry has followed this model to a tee. Whether it was B2B or B2C, fintech startups broke the banking business into narrower segments, offering singular niche services for various finance needs, e.g. credit card refinancing, small business loans, student loans, P2P payments, mortgages and more. From this model, big banks became the TGI Fridays of financial offerings (where you go to experience a full spread of financial services), and fintech platforms became the speciality grilled cheese shops (where you go to get the one thing you really crave).

Fintech Niches Fill Big Gaps

Many startups went niche not only because it was a business model that worked, but because the legacy banking industry model was out of date and there was room for true disruption. With these opportunities, niche fintechs could hone in on services that fulfilled singular needs, and they could do it with a focus, passion and dedicated customer service that most general banks couldn’t provide—and the results of this have been mostly positive. Globally, financial inclusion of unbanked people has improved. According to The World Bank, 69 percent of adults or 3.8 billion people now have an account at a bank or mobile money provider. In the U.S., niche fintechs made it easier for small businesses to get a loan post-recession. A host of online lenders stepped in to fill the gap, understanding that without access to relevant capital, small businesses struggle, which ultimately affects economic growth, jobs and inflation.

Can Fintechs Stand up to Tech Giants?

Tech giants thrive when users treat their platforms/offerings as a one-stop shop, something that is already commonplace in China, where millions of people use Tencent’s WeChat app to do almost everything—pay bills, book medical appointments, chat, play games, read news and pay for meals. Although this is not at the same level of activity in the U.S., it is a trend likely to continue.

The winds have been shifting as fintech companies question whether it makes sense to stay true to their niche or offer additional services as a path to scalability and profitability. By taking the latter path, former niche startups are now either a) building out and offering more financial services or b) partnering with more established companies/banks. Some recent examples include eBay and Square Capital, Venmo and Uber and KeyBank and HelloWallet. These partnerships seem to be a win-win—for the niche companies hoping to solve for scale and revenue stream issues, and for the established companies looking to offer complimentary services their core customers already use—but they also have fintech startups standing at a crossroads. Will working a niche be sustainable in 2020 and beyond, or is becoming a jack of all trades the only means of survival?

Beware of Diluting the Brand

For starters, the only means of survival for any fintech company is to solidly define what the company brand is and what it stands for. For example, many small business lenders are deeply passionate about fueling the American dream through helping business owners unlock their financial potential. Supporting small business is key to our country’s economic fabric. Dynamism and the ability to recover from an economic downturn are both dependent on startups’ ability to grow quickly, and in most cases, the only way for them to do so is through access to capital. For a fintech lender to become a trusted brand to small business owners, it must remain devoted to them as a company that has the financial wellbeing and vitality of small businesses in mind. This means facilitating the right loan for them, right when they need it.

The key for fintech companies is to be careful about diluting the brand. When companies stray too far from what they are passionate about, their core audiences suffer. Tech giants enter new spaces every day, whether from R&D or acquisitions. A strong brand (and the loyalty its customers have to it) will not only insulate a fintech company from the tech giant threat, but make its mission and voice stronger by comparison. Think about this the next time you are eating at In-N-Out Burger (sorry, East Coasters!). The humble hamburger shop became a cultural phenomenon through its razor-sharp focus on simplicity, quality and consistency.

Always Consider the Human Factor

Innovation and automation are both critical to survival in the fintech space. But how much tech can a fintech leverage in its solutions to avoid becoming too niche? The answer lies in understanding the core customers’ needs and how much technology can be used to fulfill those needs. For an e-wallet app, the key needs of customers are frictionless payments and transfers happening in real time; it is not a solution (when it’s working) that needs a lot of human interaction. A fintech company such as this can use technology and machine learning to automate most of its services.

Conversely, the human factor is still a huge part of the equation in some fintech services. For example, a person’s livelihood is at stake when a small business takes on a loan or another capital solution for its growth needs. This is a very personal and consequential decision for a business owner. In fact, in the majority of cases, they don’t want to rely solely on a technology-powered platform to deliver the most appropriate loan options for their needs, not to mention address their specific concerns and questions. A fintech lender can leverage technology at every touchpoint to optimize the application and loan approval process; but ultimately, many business owners will desire interaction with a live representative, not a chatbot. The human factor is crucial in business lending, and something that could become lost as a result of brand dilution. While scalability is important, customer service is equally so.

In the end, the decision to offer niche services or to go wide will depend on what’s at the core of a fintech company. Indeed, the pressures to scale, grow and earn returns for investors are huge for any business, but decision-makers must keep their perspective on the market they serve and the problems they solve best. If expanded offerings and partnerships with other service providers enhance your brand and what it stands for, then this approach makes sense for growth and customer satisfaction. If not, then serving up the best grilled cheese sandwiches around, to the folks who really crave them, may well be the best path.

Stripe Ventures Into Merchant Cash Advance Financing

September 6, 2019 Stripe, a payments firm lauded as the world’s most valuable private fintech company (at $22.5B), has officially launched a merchant cash advance product.

Stripe, a payments firm lauded as the world’s most valuable private fintech company (at $22.5B), has officially launched a merchant cash advance product.

Dozens of news outlets have announced that the company is providing loans, but that’s not all, AltFinanceDaily has learned. Both loans and merchant cash advances are available.

The company’s FAQ page originally explained the “Capital” product as a merchant cash advance but it’s since been updated to reflect that they offer access to both merchant cash advances and loans. An official Stripe spokesperson also clarified that an offer could be an MCA or a loan. The updated FAQ says that funding terms would be available in the customer dashboard, in the funding contract, and that which one a customer qualifies for depends on the specifics of their business.

Stripe merchant account customers can find out if they’re eligible for funding in their dashboard. If they’re not, they can still send Stripe a note through the dashboard to signal that they’re interested, say how much they’re looking for, and select what they plan to do with the funds. Stripe says they will not review your credit report and that all offers are based solely on Stripe transaction history.

The new product will not disrupt the separate integration with Funding Circle, according to a statement provided to Digital Transactions. Stripe customers can still apply to Funding Circle by connecting their Stripe account. Funding Circle offers term loans that range from six months to five years.

Stripe’s MCA product is currently only available in the US, but the company’s founders, Patrick and John Collison, brothers, hail from an unlikely place, rural Ireland. The company handles tens of billions of dollars in payments a year across 34 countries.

Like other recent entrants into the small business funding space, Stripe’s advantage is its ability to tap into its existing customer base. Other payments companies such as PayPal and Square, for example, were among the top four largest originators (for which public data is available) of alternative small business funding in 2018.

Note: This article has been updated to reflect the changes made on Stripe’s website as well as an additional clarification from the company.

The 2019 Top Small Business Funders By Revenue

August 14, 2019The below chart ranks several companies in the non-bank small business financing space by revenue over the last 5 years. The data is primarily drawn from reports submitted to the Inc. 5000 list, public earnings statements, or published media reports. It is not comprehensive. Companies for which no data is publicly available are excluded. Want to add your figures? Email Sean@debanked.com

| Company | 2018 | 2017 | 2016 | 2015 | 2014 |

| Square | $3,298,177,000 | $2,214,253,000 | $1,708,721,000 | $1,267,118,000 | $850,192,000 |

| OnDeck | $398,376,000 | $350,950,000 | $291,300,000 | $254,700,000 | $158,100,000 |

| Kabbage | $200,000,000+* | $171,784,000 | $97,461,712 | $40,193,000 | |

| Global Lending Services | $232,200,000 | $125,700,000 | |||

| Bankers Healthcare Group | $220,300,000 | $160,300,000 | $93,825,129 | ||

| National Funding | $121,300,000 | $94,500,000 | $75,693,096 | $59,075,878 | $39,048,959 |

| Forward Financing | $75,500,000 | $42,100,000 | $28,305,078 | ||

| ApplePie Capital | $69,700,000 | ||||

| Fora Financial | $68,600,000 | $50,800,000 | $41,590,720 | $33,974,000 | $26,932,581 |

| Reliant Funding | $64,800,000 | $55,400,000 | $51,946,000 | $11,294,044 | $9,723,924 |

| Envision Capital Group | $32,700,000 | ||||

| Expansion Capital Group | $31,300,300 | $23,400,000 | |||

| SmartBiz Loans | $23,600,000 | ||||

| 1 Global Capital | bankruptcy | $22,600,000 | |||

| IOU Financial | $19,200,000 | $17,415,096 | $17,400,527 | $11,971,148 | $6,160,017 |

| Quicksilver Capital | $16,500,000 | ||||

| Channel Partners Capital | $23,000,000 | $14,500,000 | $2,207,927 | $4,013,608 | |

| Lendr | $16,500,000 | $11,800,000 | |||

| Lighter Capital | $16,000,000 | $11,900,000 | $6,364,417 | $4,364,907 | |

| United Capital Source | $9,735,350 | $8,465,260 | $3,917,193 | ||

| Fundera | $15,600,000 | $8,800,000 | |||

| US Business Funding | $14,800,000 | $9,100,000 | $5,794,936 | ||

| Wellen Capital | $12,200,000 | $13,200,000 | $15,984,688 | ||

| PIRS Capital | $11,900,000 | ||||

| Nav | $10,300,000 | $5,900,000 | $2,663,344 | ||

| P2Binvestor | $10,000,000 | ||||

| Seek Business Capital | $8,800,000 | ||||

| Fund&Grow | $7,500,000 | $5,700,000 | $4,082,130 | ||

| Funding Merchant Source | $7,500,000 | ||||

| Shore Funding Solutions | $5,000,000 | $4,300,000 | |||

| StreetShares | $4,967,426 | $3,701,210 | $647,119 | $239,593 | |

| FitSmallBusiness.com | $3,000,000 | ||||

| Eagle Business Credit | $3,600,000 | $2,600,000 | |||

| Everlasting Capital | $2,500,000 | $2,100,000 | |||

| Swift Capital | acquired by PayPal | $88,600,000 | $51,400,000 | $27,540,900 | |

| Blue Bridge Financial | $6,569,714 | $5,470,564 | |||

| Fast Capital 360 | $6,264,924 | ||||

| Cashbloom | $5,404,123 | $4,804,112 | $3,941,819 | ||

| Priority Funding Solutions | $2,599,931 |

Funding Circle Originated $377M of US Loans in First Two Quarters of 2019

August 8, 2019Funding Circle originated $377M of loans in the US in the first six months of 2019, according to their latest public report. The company said that “growth was proactively controlled” and that they tightened higher risk band lending and increased prices. They’ve now loaned more than $2B cumulatively in the US since inception and their growth is being led by “new borrowers” that are being lured away from traditional lenders.

Funding Circle still lags behind PayPal, OnDeck, Kabbage, Square Capital, and Amazon in the US in loan origination volume, according to the AltFinanceDaily small business finance rankings. Its closest competitors by volume are BlueVine, National Funding, and Kapitus.

Import/Export SMBs Introduced to Fintech Lending Options

August 2, 2019 Early this week TangoTrade announced its partnership with the online lender Fundation. TangoTrade, which deals primarily in payment assurances for US small business importers and exporters, will now offer alternative financing to SMBs with the help of Fundation.

Early this week TangoTrade announced its partnership with the online lender Fundation. TangoTrade, which deals primarily in payment assurances for US small business importers and exporters, will now offer alternative financing to SMBs with the help of Fundation.

The development is a reaction to the struggles faced by small businesses who engage in global trade. Sam Hayes, Co-founder and President of TangoTrade, said that “If you’re an SMB and a transaction goes south, it causes major problems for cash flow. There’s very little recourse you can have as a small business.”

Explaining that about one-third of all US imports and exports originate from small businesses (roughly 200,000 small businesses import and 300,000 export), Hayes notes that this is a large portion of the American economy that is potentially at risk. Especially when they are being left out to hang by banks whose debit and credit facilities come attached with lengthy approval wait times and complex application processes that are often too inconvenient for SMB owners.

The partnership with Fundation, which is backed by both Goldman-Sachs and SunTrust Bank, will enable TangoTrade to fund SMBs up to $1 million. As mentioned, TangoTrade also offers payment assurance for importers and exporters, which reduces payment risks by managing the entire payment process for both parties involved and offering imbursement via 130 currencies. As well as this, the option to wire funds globally is available through TangoTrade’s partnership with TempusFX.

These services have been centralized by TangoTrade, being made accessible through the business’s site, a decision that is key to the company’s vision of offering services through a platform, Hayes told AltFinanceDaily. “We’ve seen innovations in cross-border payments and global sourcing, but not a whole lot in this particular area,” which is why TangoTrade is pushing to incorporate fintech in their dealings.

And this impetus has attracted attention. With a diverse set of investors ranging from Hard Yaka, which has ties to Square, Ripple, and Twitter; to Village Global, a venture capital network that is backed by Bill Gates, Jeff Bezos, and Mark Zuckerberg, TangoTrade has links to large names. Such diverse connections are mirrored in the company itself, with their team bringing together experience from MasterCard, Payoneer, NASDAQ, and Oracle.

A cabal of tech heads to be sure, Fundation CEO Sam Graziano says that this approach will “enable small businesses to access low-cost capital through an integrated user-friendly digital experience on their platform.”

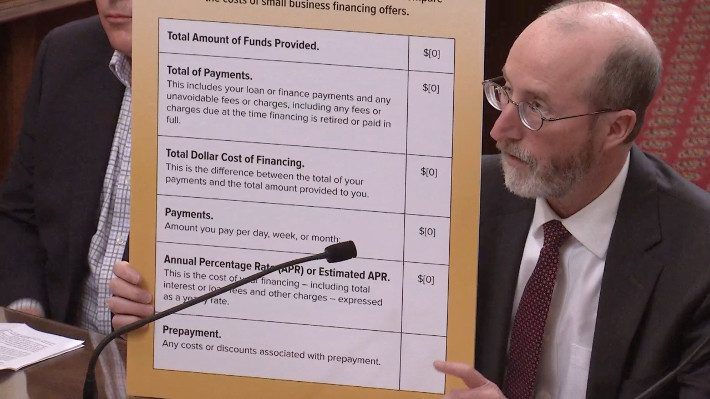

California DBO Making Progress On Finalizing Rules Required By The New Disclosure Law

July 29, 2019 Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

The DBO then issued a public invitation to comment on how that format should work. They got 34 responses. Among them were Affirm, ApplePie Capital, Electronic Transactions Association, Commercial Finance Coalition, Fora Financial, Equipment Leasing and Finance Association, Innovative Lending Platform Association, International Factoring Association, Kapitus, OnDeck, PayPal, Rapid Finance, Small Business Finance Association, and Square Capital.

On Friday, the DBO published a draft of its rules along with a public invitation to comment further. The 32-page draft can be downloaded here. The opportunity to comment on this version of the rules ends on Sept 9th.

You can review the comments that companies submitted previously here.

PayPal Begins Offering Business Loans in Canada

July 28, 2019 PayPal has extended its popular working capital business loan program to Canada, according to company CEO Dan Schulman.

PayPal has extended its popular working capital business loan program to Canada, according to company CEO Dan Schulman.

“This quarter, we began offering our PayPal business loan product to PayPal merchants in Canada, allowing them to access financing to build and sustain their businesses,” he said during the Q2 conference call. “This follows the expansion of our business financing solutions to Germany in Q4 2018 and in Mexico earlier this year in partnership with Mexican lending platform Konfio.”

AltFinanceDaily ranked PayPal as the leading alternative small business finance company by originations in 2018. They are followed by OnDeck, Kabbage, Square, and Amazon.

Are The Bankers Taking Over Fintech?

June 27, 2019

For Rochelle Gorey, the chief executive and co-founder of SpringFour, a “social impact” fintech company, mingling with industry movers and shakers at this year’s LendIt Fintech Conference was just what the doctor ordered. “I went mainly for the networking opportunities,” Gorey told AltFinanceDaily.

SpringFour, which is headquartered in Chicago, works with banks and financial institutions in the 50 states to get distressed borrowers back on track with their debt payments. It does this by digitally linking debtors with governmental and nonprofit agencies that promote “financial wellness.

The indebted parties—more than a million of whom had referrals that were arranged by Gorey’s tech-savvy company last year—constitute not only household consumers but also commercial borrowers. “Small businesses face the same issues of cash flow as consumers, and their business and personal income are often combined,” she says. “If their financial situation is precarious, it’s super-hard to get credit, a line of credit, or a business loan.”

Although Gorey felt “overwhelmed” at first by the throng of 4,000 conference-goers at Moscone Center West in San Francisco—roughly the same number as attended last year, conference organizers assert— her trepidation was short-lived. It wasn’t too long before she was in circulation and having chance encounters and serendipitous interactions, she says, with “all the right people at the workshops and at the tables in the Expo Hall.”

Although Gorey felt “overwhelmed” at first by the throng of 4,000 conference-goers at Moscone Center West in San Francisco—roughly the same number as attended last year, conference organizers assert— her trepidation was short-lived. It wasn’t too long before she was in circulation and having chance encounters and serendipitous interactions, she says, with “all the right people at the workshops and at the tables in the Expo Hall.”

Armed, moreover, with a “networking app” on her mobile phone, Gorey was able to arrange targeted meetings, scoring roughly a dozen, 15-minute tete-a-tetes during the two-day breakout sessions. These included audiences with community bankers, financial technology companies, and “small-dollar” lenders. “And it went both ways,” she says. “I had people reaching out to me”—just about everyone, it seemed, appeared receptive to “finding ways to boost their customers’ financial health.”

Gorey’s success at networking was precisely the experience that the event’s planners had envisioned, says Peter Renton, chairman and co-founder of the LendIt Fintech Conference. Organizers took pains to make schmoozing one of the key features of this year’s gathering. Not only did LendIt provide attendees with a bespoke networking app, but planners scheduled extra time for meet-ups. “We had around 10,000 meetings set up by the app,” Renton says, “about double the number of last year.”

AltFinanceDaily did not attend the LendIt USA conference on the West Coast this year. But the publication sought out more than a half-dozen attendees—including several financial technology executives, a leading venture capitalist, a regulatory law expert, and the conference’s top administrators—to gather their impressions. While informal and manifestly unscientific, their responses nonetheless yielded up several salient themes.

The popularity—and effectiveness—of networking was a key takeaway. Most seized the opportunity to rub elbows with influential industry players, learn about the hottest startups, compare notes, and catch up on the state of the industry. Most importantly, the event presented a golden opportunity to make the introductions and connections that could generate dealmaking.

“My goal this year was to strike more partnerships with lenders and fintech companies,” says Levi King, chief executive and co-founder at Utah-based Nav, an online, credit-data aggregator and financial matchmaker for small businesses. “We had great meetings with Fiserv, Amazon, Clover Network (a division of First Data), and MasterCard,” he reports, rattling off the names of prominent financial services companies and fintech platforms.

James Garvey, co-founder and chief executive at Self Lender, an Austin-based fintech that builds creditworthiness for “thin file” consumers who have little or no credit history, said his goal at the conference was both to serve on a panel and “meet as many people as I could.”

Self Lender is in its growth stage following a $10 million, series B round of financing in late 2018 from Altos Ventures and Silverton Partners. Garvey reports having meetings with Bank of America and venture capitalist FTV Capital “over coffee” as well as F-Prime Capital, another venture capitalist. “It’s just about building a relationship,” he said of making connections, “so that at some point, if I’m raising money or want to partner, I can make a deal.”

There was a concerted effort to recognize women, as evidenced by a packed “Women in Fintech” (WIF) luncheon that drew roughly 250 persons, 95% of whom were women. (“Many men are big supporters of women in fintech and we didn’t want to exclude them,” Renton says). The luncheon was preceded by a novel event—a 30-minute, ladies-only “speed-networking” session—which attracted 160 participants, reports Joy Schwartz, president of LendIt Fintech and manager of the women’s programs.

At the luncheon, SpringFour’s Gorey says, “it was empowering just to see lot of women who are senior leaders working in financial services, banks and fintechs.” The keynote speech by Valerie Kay, chief capital officer at Lending Club, was another highlight. “She (Kay) talked about taking risks and going to a fintech startup after 23 years at Morgan Stanley,” Gorey reports, adding: “It was inspiring.”

The women’s luncheon also marked the launch of LendIt’s Women In Fintech mentor program, and presentation of a “Fintech Woman of the Year” award. The recipient was Luvleen Sidhu, president, co-founder and chief strategy officer at BankMobile, a digital division of Customers Bank, based near Philadelphia, which employs 250 persons and boasts two million checking account customers.

I am honored to be the 2019 Fintech Women of the Year and thrilled that @BankMobile won Most Innovative Bank. It’s very exciting to be recognized by @LendIt Fintech with this prestigious award and I congratulate the finalists in all the categories. https://t.co/qjADuKEMrB pic.twitter.com/hFJVFw1fLS

— Luvleen Sidhu (@LuvleenSidhu) April 11, 2019

BankMobile, which also won LendIt’s “Most Innovative Bank” award, has an alliance with Upstart to do consumer lending and a partnership with telecommunications company T-Mobile. Known as T-Mobile Money, the latter service provides T-Mobile customers with access to checking accounts with no minimum balance, no monthly or overdraft fees, and access to 55,000 automated teller machines, also with no fees. (At its website, T-Mobile Money describes itself as a bank and uses the slogan: “Not another bank, a better one.”)

The impressive salute to women notwithstanding, their ranks remained fairly thin: just 733 attendees identified themselves as “female” on their registration forms, LendIt’s Schwartz says, a little more than 18% of total participants. Seventy-five of the 350 total speakers and panelists—or 21%—were female. (Schwartz also reports that another 157 registrants selected “prefer not to say” as their sexual orientation, while 22 checked the box describing themselves as “non-conforming.”)

In LendIt’s defense, AltFinanceDaily, who caters to a similar audience, regularly reviews its readership demographics using several tools. They have consistently indicated that women make up 18% – 23% of the total, in line with what LendIt experienced at its most recent event.

By all accounts, many panels were informative, jampacked and attendees were engaged. King, who moderated a panel on regulatory changes in small business lending, which dealt with such topics as California’s commercial “truth-in-lending” law and controversial “confessions of judgment” laws, says: “They didn’t have to lock the door but the room was pretty full and people seemed to be paying attention. I didn’t see people studying their cellphones.”

The Expo Hall was teeming with budding fintech entrepreneurs, financial services companies and multiple vendors hawking their wares. But as numerous fintechs were angling to forge lucrative symbiotic relationships with banks, some participants—even those who were hailing the conference for its networking and deal-making opportunities—lamented the heavy presence of the establishment.

The banks’ ubiquitousness especially vexed Matthew Burton, a partner at QED Investors, an Arlington, (Va.)-based, venture capital firm and a veteran fintech entrepreneur. Before signing on with QED last year, Burton had been the co-founder of Orchard Platform, an online technology and analytics vendor for fintech and financial services companies which was purchased by fintech lender Kabbage.

Not only did bankers seem to playing a more prominent role at the LendIt conference, Burton notes, but “big four” accounting firm Deloitte had signed on as a major sponsor. “The energy level seemed a bit lower than in past years,” Burton told AltFinanceDaily. “It’s not like people were depressed but it wasn’t bubbling with excitement. A couple of years ago we thought all these new fintechs would replace the banks,” he explains. “Now the discussion is over how to partner and collaborate with banks. It’s not as exciting as when everyone thought banks were dinosaurs.

“I couldn’t really tell if there were more bankers attending this year,” Burton adds, “but it sure felt like it.”

King, the Nav executive, told AltFinanceDaily: “It was a little bit subdued. I don’t know if it was nervousness about the economy or politics, but the subject of risk came up more often in side conversations with venture-backed businesses and banks and alternative fintech lenders. One large bank we deal with,” he adds, “told me it’s spending most of its time working on risk.”

Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute who participated in a standing-room-only session on state and federal fintech regulation, declares: “I’ve been to three of their conferences, including one in New York, and I would say that this one did not have as much pizzazz. It may be that the industry is maturing.”

For his part—when asked whether there was a palpable absence of passion this year—LendIt’s Renton told AltFinanceDaily: “I would say that it felt more businesslike. Fintech has had a lot of hype and we have had conferences that were ridiculously over-hyped in 2015 and 2016. And in 2017 (the mood) was much more somber. This one felt optimistic and businesslike.”

There were 750 bankers in attendance, almost one in five participants. “The number of bankers was not up significantly” over last year, Renton says, “but the seniority of the bankers was higher. We worked very hard to get senior bankers to attend this year.”

Renton was bullish on the closer ties developing between nonbank online lenders and banks. That was reflected as well in the several panels exploring ways to develop partnerships between the two sides. He noted that a session called “How Banks are Matching Fintechs on Speed of Funding and User Experience” drew a heavy crowd. “It brought more bankers than we’ve ever had before,” Renton says.

Moderated by Brock Blake, founder and chief executive at the fintech Lendio, the panel was composed of three bankers: Ben Oltman, the Philadelphia-area head of digital lending and partnerships at Citizens Bank; Gina Taylor Cotter, a senior vice-president at American Express (the highest-ranking woman at the company); and Thomas Ferro, a senior marketing manager at Bank of America. “The banks came to LendIt not just to learn but to decide whom they’re going to partner with,” Renton says. “Fintechs need banks and banks need fintechs. That is the narrative you hear on both sides.”

(Asked whether any banks sponsored this year’s conference, Renton replied: “They are not sponsoring yet in any number but we are working on that.”)

OnDeck, a top-tier fintech lender to small-businesses in the U.S., which has been making forays abroad to Australian and Canadian markets, is an enthusiastic champion of the fintech-bank union. So much so that it claimed LendIt’s “Most Promising Partnership” award for the cooperative relationship it struck with Pittsburgh-based PNC Bank, which uses OnDeck’s platform to make small business loans. (Among the partnerships that OnDeck-PNC beat out: Gorey’s SpringFour, which was named a finalist in the competition for its association with BMO Harris Bank.)

“We were the first fintech lender to strike a true platform relationship with a bank,” Jim Larkin, head of corporate communications at OnDeck says, noting that the PNC deal follows on the New York-based fintech’s similar, innovative arrangement with J.P. Morgan Chase. “Others may do referrals,” he explains. “What we do is actually provide the underlying platform to accelerate a bank’s online lending capabilities. We deliver the software and expertise to construct the right type of online lending engine.”

Meanwhile, there was avid interest about the stock performance of publicly traded fintechs—for example, Square and GreenSky—both of which had seen their share prices tumble and then recover.

Burton noted that, among venture-backed firms, the most excitement seemed to be coming from Latin America. “Everyone was very bullish on a Mexican company, Credijusto, an alternative small business lender that was written up the in the Wall Street Journal,” he says. “It’s not going public yet but it had a large debt-and-equity raise of $100 million from Goldman Sachs. And SoftBank Group announced a $5 billion Latin American tech fund.

“There was a lot of talk,” he adds, “about how money was flowing into Mexico and Brazil.”