2019 Alternative Finance Predictions

December 21, 2018

With 2019 approaching, AltFinanceDaily asked executives in the funding and payments industry if they had any predictions for the new year. We kept it pretty open-ended and received forecasts regarding technology, regulations, and the evolving relationship between fintech companies and banks. And yes, we also asked a few lawyers in the small business lending space for their two cents. Below is what they had to say:

“The hype around cryptocurrencies is nearly gone, and it’s time to focus on the more interesting part of it – the blockchain technology. In 2019 we expect to see first use-cases of such technology for logging and sharing data among lenders. There is a true potential for real-time data sharing which will help lenders avoid lending to clients which just took similar loans from other lenders, in a decentralized and anonymous way. This will allow the industry to overcome one of the challenges quick loan approvals bring: real time loans stacking.”

“The hype around cryptocurrencies is nearly gone, and it’s time to focus on the more interesting part of it – the blockchain technology. In 2019 we expect to see first use-cases of such technology for logging and sharing data among lenders. There is a true potential for real-time data sharing which will help lenders avoid lending to clients which just took similar loans from other lenders, in a decentralized and anonymous way. This will allow the industry to overcome one of the challenges quick loan approvals bring: real time loans stacking.”

Ido Lustig, Chief Risk Officer, BlueVine

“We look forward to big changes coming. Four years ago banks still were not sure about Fintech firms. Now the banks are approaching alternative lenders trying to figure out various partnership options. We think in 2019 we will see banks engage in various levels of mutually prosperous partnerships…We believe new products will be launched in 2019 that will continue to support small business growth. And as the Alt Lenders are able to access cheaper cost of capital, it will give more options to small business owners.”

“We look forward to big changes coming. Four years ago banks still were not sure about Fintech firms. Now the banks are approaching alternative lenders trying to figure out various partnership options. We think in 2019 we will see banks engage in various levels of mutually prosperous partnerships…We believe new products will be launched in 2019 that will continue to support small business growth. And as the Alt Lenders are able to access cheaper cost of capital, it will give more options to small business owners.”

Robert Gloer, President and COO, IOU Financial

Given the explosive growth of MCAs and the fact that MCAs have evolved from an early stage industry to a mainstream industry – MCAs have been around for decades – we expect regulation of the industry to become a reality. At 6th Avenue Capital, we believe regulation will be healthy for the industry and will reduce the industry’s bad actors, allowing those institutions that practice transparency and industry best practices to thrive.

Given the explosive growth of MCAs and the fact that MCAs have evolved from an early stage industry to a mainstream industry – MCAs have been around for decades – we expect regulation of the industry to become a reality. At 6th Avenue Capital, we believe regulation will be healthy for the industry and will reduce the industry’s bad actors, allowing those institutions that practice transparency and industry best practices to thrive.

As a former Chief Compliance Officer, I set up the company with regulation in mind. In fact, we are the only firm to be a member of both ILPA and SBFA, both organizations that are active participants working with regulators to help create a regulatory environment beneficial to both SMBs and SMB funders. The need for alternative credit, and access to fast capital, continues to grow and the industry is not going away with regulations. The winners in the MCA space will be those that adopt sound practices early.

Christine Chang, CEO, 6th Avenue Capital

“We will likely continue to see state efforts to enact disclosures in MCA and small business lending transactions. We will also likely see efforts at the state level to ban practices viewed as aggressive by elected officials. These efforts will lead to a weeding out of the weaker players in the space and will strengthen the companies dedicated to compliance and customer service.

“We will likely continue to see state efforts to enact disclosures in MCA and small business lending transactions. We will also likely see efforts at the state level to ban practices viewed as aggressive by elected officials. These efforts will lead to a weeding out of the weaker players in the space and will strengthen the companies dedicated to compliance and customer service.

Catherine Brennan, Partner, Hudson Cook

“A business slowdown (possible but hard to predict, at least by me) will test the effectiveness of algorithm-based credit granting. I am not optimistic. Mid-market banks might start to purchase MCA-type technology and try their hand at selling it, albeit at a lower cost.”

“A business slowdown (possible but hard to predict, at least by me) will test the effectiveness of algorithm-based credit granting. I am not optimistic. Mid-market banks might start to purchase MCA-type technology and try their hand at selling it, albeit at a lower cost.”

Robert Zadek, Of Counsel, Buchalter

“Older, more traditional SMBs will broaden their lending horizons. In 2017, 30% of business owners looked for a small business loan online. The 70% who didn’t are predominantly older, and more traditional in their approach to seeking financing. In 2019, we will see a more aggressive push by SMB lenders to tap into a more mainstream audience of business owners who have not been looking online for financing options. This will be driven in part by increased competition between the SMB lenders, and a larger push by those lenders to market themselves to a broader audience of SMBs.”

Charles Amadon, VP of Business Development & Strategic Partnerships, BlueVine

“In 2019, we’ll see more and more retailers offer flexible, pay-over-time financing options and promotional 0% tools to drive sales and make gifting more affordable for customers. As customers continue to look for online pay-over-time options, we can expect to see savvy [merchants] taking advantage of these trends to both improve performance and meet the expectations of the modern shopper.”

Kate Levin, Vice President of Merchant Success, Bread

“Large corporations, from card payment organizations right through to banks, are making significant investments in reinventing themselves. I think some of them will be very successful in doing this…like Marcus by Goldman Sachs and also First Data’s Clover product. These both demonstrate that long-established companies are starting to really get it right when it comes to being innovative with fintech. I believe in the next five years, we’ll see other huge companies begin to get it right with fintech.”

Simon Black, CEO, PPRO

MCA Participations and Securities Law: Recognizing and Managing a Looming Threat

December 11, 2018Authors: Gregory J. Nowak and Mark T. Dabertin

Due to the high volume of relevant judicial decisions issued by New York courts over the past two years, the risk that enforceability of a merchant cash advance (MCA) contract1 might be successfully challenged as a disguised usurious loan has received ample attention in law firm white papers and published legal articles, including articles by Pepper Hamilton attorneys.2 Avoiding this risk of “loan re-characterization” is essential if the MCA industry is to achieve wider acceptance as a source of small business financing. But another risk—which we believe is largely unrecognized—could significantly throttle further expansion of MCA financing. This risk is that the funding structures MCA providers rely on to generate funding from third-party investors could be found to involve the issuance of unregistered securities. Unless an exception is available, that would be unlawful and could result in fines, penalties, defense costs and even rescission of the entire transaction, with the “issuer” being required to return investor capital.

Many MCA providers raise new funding by offering “participation interests” in their MCA contracts to third-party investors. These are usually structured in one of two ways. Under a “true participation,” the participant acquires the right to receive payments, and a resulting return on the participant’s investment, exclusively from the MCA provider. To this end, the participant receives no rights to enforce, nor any direct interest in, the underlying MCA contracts. Alternatively, the participation agreement may be structured so as to make each investor a pro rata “co-funder” of the underlying MCA contracts in an agreed-upon percentage (the “participation share”). Under this structure, the MCA provider’s contract with the merchant typically acknowledges the possible existence of “co-funders” in general terms, and does not require the merchant to ratify and accept named co-funders as they come into being. This add-on is usually accomplished through a novation to the MCA contract.

Under either of the above-described participation structures, the nature of the participant’s investment is purely passive, with no possibility for active involvement in the underlying MCA relationships. In fact, the participation agreement likely expressly prohibits such interference. The passive nature of a participant’s investment matters, because the presence of passivity, and the resulting reliance on the efforts of another party (i.e., the party offering the investment) to realize a profitable return, is a key factor for purposes of determining whether a security exists under the federal securities laws.

In SEC v. WJ Howey Co.,3> the U.S. Supreme Court established the following four-factor test for identifying the existence of a security: (1) an investment, (2) in a common enterprise, (3) with a reasonable expectation of profits, (4) to be derived from the entrepreneurial or managerial efforts of others. The facts of Howey concerned investments in an orange grove operation, where the investors were entirely dependent on the efforts of the orange grove manager/promoter to maintain the trees that the investor had invested in. In the case of an MCA participation structured as described above, all four Howey factors are arguably present. An investment is made with the expectation of realizing a profit. In addition, as discussed above, because that investment is passive in nature, its success hinges on the efforts of the MCA provider. Finally, at least one court has opined that the existence of common enterprise is inherent to any participation relationship.4

The Howey test, which seeks to identify the presence of an “investment contract,” is not the sole means for evaluating whether an investment constitutes a security. In Reves v. Ernst & Young, the U.S. Supreme Court recognized that the expansive definition of the term “security” under the Securities Act of 1933 and the Security Exchange Act of 1934 extends to other forms of “notes” besides investment contracts.5 In determining whether the “demand notes” at issue in Reves constituted a security, the court applied what is commonly known as the “close resemblance” test. Under this test, if the note in question bears a close resemblance to a type of note that has been judicially recognized as not involving a security, that note likewise will not be considered a security. For example, on its face, an MCA contract closely resembles “a short-term note secured by a lien on a small business or some of its assets.”6 However, in an MCA contract, the purchased future receivables provide the source of repayment of the advanced funds, as opposed to providing security for a lien.

This distinction is important. because in an MCA, the receivables do not yet exist, so there is nothing to lien. Rather, the MCA involves receivables to be created, presumably using the proceeds of the MCA to do so. Properly drafted MCAs sidestep all “note-like” characteristics, and make it clear that the MCA is a contract to purchase an asset (i.e., receivables) that are yet to be created. There is no sum certain for repayment – unlike a note, if the receivables turn out to be bad, the MCA provider has no recourse back to the merchant that created them. The receivables are not security for a loan; rather, the receivables are the property being forward purchased. MCAs are different in kind and extent from loans.

Notwithstanding the Howey test, and as noted above, it is possible to argue persuasively that an instrument that appears to be a security instead describes the terms of an individually negotiated contractual agreement. In this regard, in Marine Bank v. Weaver,7 the U.S. Supreme Court held that a contract between a bank and a married couple that called for the latter to pledge a certificate of deposit as security for a loan between the bank and an unrelated corporate borrower in exchange for the opportunity to share in the latter’s future profits did not involve a security. In doing so, the court distinguished the note in question from investments that fall within the “ordinary concept of a security. . . [which are offered] to a number of potential investors.”8 In contrast, the Court in Marine Bank found that the contested note created “a unique agreement [that was] negotiated one-on-one by the parties” and was therefore, “not a security.”9

In the absence of an applicable statutory exemption, the public offering of unregistered securities constitutes a criminal violation of the federal securities laws. Because securities can generally only be sold to the public by a registered broker-dealer, people who engage in selling such securities, as well as their related corporate actors, may be subject to monetary penalties for the resulting violations of law. An improperly structured MCA participation presents the risks that: (i) sales of participations made under the flawed structure could be declared void and subject to rescission; and (ii) both the MCA provider and its primary individual actors could be subject to criminal prosecution and resulting monetary penalties. In the remainder of this article, we discuss ways for effectively mitigating these risks.

Structuring the MCA participation so as to make each participant not merely a “co-funder” in name, but an actual party to each underlying MCA contract by means of a contract novation signed by the merchant and naming the individual participants, would arguably eliminate any risk that the structure might be deemed to involve the unlawful issuance of securities. Under this structure, each participant, at least in theory, could enforce the MCA contracts directly against the applicable merchants, without having to rely on the MCA provider. The main flaw with this option is that the MCA participation agreement necessarily prohibits such independent actions by the participant, because those actions could directly conflict with the economic interests of either or both the MCA provider or additional participants. Hence, any actual ability of the participant to be actively engaged in the underlying merchant relationships will be missing. As the number of participants increases to more than a handful, this structure – requiring as it does that the merchant ratify and accept every new participant as each participant is added, is unwieldy and becomes infeasible to administer.

One could also argue that including a requirement in the MCA participation agreements that the participant must evaluate independently the quality of each MCA contract before the purchase of the participation share precludes the existence of a common enterprise. However, unless each participant has its own series of MCAs, this distinction is unlikely to be of significance, because all participants are participating in the same MCA. Also, notwithstanding the obligation to conduct independent reviews, the MCA participant must still rely on the MCA provider to source qualified merchants. In addition, as noted above, the investor also must depend on the MCA provider’s success in collecting payments from merchants, which will determine whether a profitable return is achieved. Finally, where a pool of investors all share in the risks and benefits of a particular business enterprise (known in securities law as “horizontal commonality”), the resulting presumption of a common enterprise is extremely difficult to disprove.

In view of the above, we suggest that the best way to manage the risk that the participation structure might be viewed as involving the unauthorized issuance of securities is to embrace the substance, if not the precise letter, of the federal securities laws. Specifically, by structuring the participation in a manner that complies with the safe harbor from the requirement to register securities described in Section 506 of the SEC rules under the Securities Act of 1933. This entails: (i) only selling participations to accredited investors; (ii) describing the applicable risks (i.e., the risk factors) and potential conflicts of interest in an addendum to the participation agreement; (iii) making sure that all sales of participants are made on a one-to-one basis, with no general solicitation or marketing; and (iv) advising participants that the resale of their participation share may be subject to a one-year minimum holding period. (Of course, if the MCA pays off before the one year period and extinguishes the MCA, that is not an issue under this rule.)

We caution that the securities laws are both difficult to navigate and prone to divergent interpretations. The consequences of misinterpretation can be severe and could result in the rescission of existing participations and monetary penalties. Hence, this is not a DIY proposition.

Pepper Points

-

The risk that an MCA participation structure could be found by a regulator or court to constitute the unlawful issuance of securities is under appreciated, and has serious consequences that could throttle the availability and growth of MCA financing.

-

Although legal arguments can be made in support of the position that the most commonly used MCA participation structures do not involve the unlawful issuance of unregistered securities, none of those arguments is sufficiently persuasive to preclude the need for additional risk mitigation efforts.

-

Mitigation plans for managing the risk that a given MCA participation structure involves should incorporate complying with the substance, and the precise letter, of the federal securities laws.

The federal securities laws are difficult to navigate and prone to divergent interpretations. The consequences of misinterpretation are severe and could include the rescission of existing participations and assessments of monetary penalties, including against individual actors.

Endnotes

1 An MCA is a business financing option that involves the advance of funds to a merchant, typically to assist the merchant in managing its short-term cash flow needs, in exchange for the sale of a specified percentage of the merchant’s future receivables at a sizeable discount. It is a relatively new offshoot of “factoring,” which likewise involves the purchase and sale of receivables at a discount in exchange for an advance of funds to a business, with the primary difference being that the receivables in the case of MCA financing are not yet extant. An MCA contract might be deemed a disguised usurious loan for many reasons, including the inclusion of a set term within which the advance must be repaid in full to avoid default. The most critical factor in this regard is whether the MCA provider is looking to the purchased receivables for repayment, or to the merchant itself or its individual owner(s); e.g., in the form of a financial guarantee given by the owner(s).

2 For a broader discussion of MCA financing, and the risk of re-characterization as a usurious loan, see: https://www.pepperlaw.com/publications/recent-litigation-illustrates-why-merchant-cash-advances-are-not-loans-2017-04-20/.

3 328 U.S. 293 (1946).

4 Provident National Bank v. Frankfort Trust Co., 468 F. Supp. 448, 454 (E.D. Pa. 1979) (By its “very nature” any participation involves a common enterprise.).

5 494 U.S. 56, 64 (1990) (“The demand notes here may well not be ‘investment contracts,’ but that does not mean they are ‘notes.’ To hold that a ‘note’ is not a ‘security’ unless it meets a test designed for an entirely different variety of instrument ‘would make the Acts’ enumeration of many types of instruments superfluous’ Landreth Timber, 471 U.S. at 692, and would be inconsistent with Congress’ intent to regulate the entire body of instruments sold as investments, see supra at 60-62”.).

6 Id. at 65.

7 455 U.S. 551 (1982).

8 Id. at 552.

9 Id.at 560. In Vorrius v. Harvey, 570 F. Supp. 537, 541 (S.D.N.Y. 1983), the court followed Marine Bank in finding that a contested loan participation agreement involved an individually negotiated contract versus a security. A key factor in that case, however, was the existence of a comprehensive federal regulatory scheme apart from the federal securities laws in the form of banking laws and regulations, which made application of the former unnecessary for purposes of protecting the interest of investors. No such alternative regulatory scheme exists in the case of the MCA industry, which is generally unregulated.

The material in this publication was created as of the date set forth above and is based on laws, court decisions, administrative rulings and congressional materials that existed at that time, and should not be construed as legal advice or legal opinions on specific facts. The information in this publication is not intended to create, and the transmission and receipt of it does not constitute, a lawyer-client relationship.

OnDeck Expands Canadian Business with Merger

December 5, 2018 OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

“The combination of OnDeck’s Canadian operations with Evolocity will create a leading online platform for small business financing throughout Canada and represents a significant investment in the Canadian market,” said Noah Breslow, Chairman and CEO of OnDeck. “There is an enormous need among underserved Canadian small businesses to access capital quickly and easily online.“

According to the announcement, “the transaction will combine the direct sales, operations, and local underwriting expertise of the Evolocity team with the marketing and business development capabilities of the OnDeck team.”

As part of the merger, Neil Wechsler, who is the CEO of Evolocity, will become the CEO of OnDeck Canada. And the management team will include Evolocity co-founders David Souaid as Chief Revenue Officer and Harley Greenspoon as Chief Operating Officer. OnDeck Canada will be governed by a Board of Directors chaired by Breslow and composed of existing OnDeck and Evolocity management.

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. AltFinanceDaily inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. AltFinanceDaily inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Investment in online small business lending in Canada is growing. IOU Financial, a Montreal-based small business funder that primarily funds American small businesses, told AltFinanceDaily last month that they made a concerted marketing effort in the third quarter to reach Canadian small business owners. Meanwhile, Thinking Capital, a Canadian online small business funder, announced in July the launch of BillMarket, a service that provides Canadian small businesses with a credit grade (A through E), making it easier for them to get funded.

“BillMarket represents a cash flow revolution for the Canadian small business market,” said Jeff Mitelman, CEO of Thinking Capital, which has roughly 200 employees between its Toronto and Montreal offices.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

Evan Marmott, founder of Canadian small business funder, Canacap, told AltFinanceDaily earlier this year that unlike the saturated small business market in the U.S., the Canadian small business market is still ripe for growth. Not only this, he said that while the market is smaller in Canada, the default rates are generally lower and he found that Canadian merchants do less shopping around. He also said he has seen less fraud in Canada than in the U.S.

“For brokers, while commissions are lower, you could actually speak to business owners who are not being bombarded with calls [as they are in the U.S.] and have a much higher closing rate,” Marmott said.

Evolocity has 70 full-time employees and offices in Montreal, Vancouver and Marham, in the Toronto area. OnDeck has funded over $10 billion to small businesses and became a public company (NYSE: ONDK) in 2014. OnDeck is headquartered in New York.

“We are excited to join forces with OnDeck…to enhance our best in class digital financing solutions to small businesses across Canada,” said Wechsler, Evolocity CEO. “Additionally, this transaction will augment our data science and analytics capabilities to help deliver an unparalleled merchant experience.”

BFS Capital Announces New CEO

November 28, 2018 BFS Capital announced today that it has appointed Mark Ruddock as CEO, effective immediately. Co-founder Marc Glazer, who has served as interim CEO since the departure of Michael Marrache earlier this year, will be Chairman.

BFS Capital announced today that it has appointed Mark Ruddock as CEO, effective immediately. Co-founder Marc Glazer, who has served as interim CEO since the departure of Michael Marrache earlier this year, will be Chairman.

“I sense there is tremendous potential in this firm,” Ruddock told AltFinanceDaily. “It has in its DNA an innate understanding of the needs of small business and I think the opportunity for it is to leverage significant increases in data science and technology to help scale and deliver on this potential.”

Most recently, Ruddock served as interim CEO for nearly two years at 4finance, one of the largest European consumer focused online lenders, with more than 3,000 employees and customers across 17 countries. Ruddock said that at 4finance, every day they would issue more than 16,500 loans and make about 22,500 risk decisions. And the entire process was automated.

“There is an opportunity to achieve real scale [in small business lending] through the use of leading edge technology,” Ruddock said, and that is what he intends to do at BFS Capital. Ruddock is relocating to Florida from Berlin, Germany.

Glazer will remain a key part of the operations at BFS Capital.

“One of the biggest assets this company has is Marc Glazer,” Ruddock said. “The two of us see this very much as a joint endeavor moving forward…and I’m going to hold him to remaining actively involved here.”

Their offices are right beside each other, Ruddock said.

“[Ruddock] has an outstanding track record of transforming financial services and technology companies by accelerating their innovation and business growth,” Glazer said. “His diversity of experience, from founder to growth stage executive, across a wide variety of industries and geographies makes him an exceptional choice for BFS Capital at such a pivotal stage in our evolution.”

Ruddock was the founder and CEO of INEA Corporation, an enterprise software firm focused on the financial services industry that was acquired in 2005. Following INEA, he became CEO of mobile software company Viigo, whose flagship app became one of BlackBerry’s most downloaded apps of all time by the time the company was acquired by RIM (Blackberry) in 2010. He held a number of other positions before becoming interim CEO at 4finance in 2017.

Headquartered in Coral Springs, FL, BFS Capital funds American and Canadian small businesses with merchant cash advances and business loans. Through its affiliate, Boost Capital, the company also provides funding to small businesses in the UK. Since 2002, BFS Capital has funded more than $1.9 billion. The company also has offices in New York, California and the UK.

Dan DeMeo is Back in Action… at Lendr

November 15, 2018 Daniel DeMeo has been hired as Chief Revenue Officer by the Chicago-based funder, Lendr.

Daniel DeMeo has been hired as Chief Revenue Officer by the Chicago-based funder, Lendr.

DeMeo has been working as an independent consultant for the last two years, according to LinkedIn. Prior to that he was the CEO of CAN Capital, a company he had dedicated himself to for nearly seven years until an internal account performance issue led to several senior executives taking an immediate leave of absence.

Under DeMeo, CAN enjoyed success as one of the nation’s largest non-bank small business financiers, partially attributed to the company’s major head start in pioneering merchant cash advance products when the company was founded in 1998. DeMeo even landed on the cover of AltFinanceDaily’s November/December 2015 issue, around the time when the company was widely believed to be planning an IPO.

It never happened.

The systems issue that toppled CAN’s top execs including DeMeo, brought the company to its knees, putting all new funding on hold for six months until it was saved by a capital infusion from Varadero Capital in July 2017. CAN Capital survived while DeMeo has notably since then kept a low public profile.

Now he’s back in action at Lendr, an ambitious funding company that offers MCAs, small business loans, equipment financing, and just recently, factoring.

“Dan is a highly strategic and thoughtful leader with broad perspective of the industry that enables him to understand specific challenges we face as a growing company,” said Tim Roach, CEO of Lendr. “Dan’s experience is a perfect addition to the team as we accelerate our growth plans, raise Lendr’s brand recognition, and further increase our market share.”

“I’m thrilled to be joining such a dynamic and progressive company,” said DeMeo. “Lendr has emerged as one of the leaders in the financial solutions space and we are poised to build strategic partnerships and alliances with those who share the same zeal in helping small- and medium-sized businesses grow.”

Lendr is setting its sights high. “We’ll be north of $100 million in our first year of factoring,” Lendr co-founder and CEO Tim Roach told AltFinanceDaily in September.

The company has also been showing off its technological and fundraising prowess as of late. This past March, they closed on a $25 million credit facility that’s expandable up to $50 million. That news was followed by the announcement of a new funding option made possible through virtual and physical debit cards.

Lendr has offices in Chicago and New York and employs over 45 people.

IOU Continues to Post Positive Earnings

November 14, 2018

Loan originations for IOU Financial’s third quarter were $36.1 million, an 85% increase over last year’s Q3 originations of $19.6 million. This is also IOU’s fourth consecutive quarter with positive earnings.

“IOU continued to deliver strong loan origination growth and earnings performance during the third quarter of 2018 and we have successfully managed loan defaults as a result of measures implemented last year,” said IOU Financial CEO Phil Marleau.

The measures implemented last year refer, in part, to changes in collection efforts, such as using a more aggressive litigation strategy against businesses that default on their loan obligations, Marleau told AltFinanceDaily. Provisions for loan losses in Q3 were $1.2 million, a decrease of 51% compared to last year at this time.

Most of IOU’s revenue comes from making loans of up to $300,000 to American small businesses. Marleau said the average IOU loan is for $100,000 with a 12 month term, although they do offer terms up to 18 months. A significant percentage of IOU’s merchants use the business loans to purchase equipment. Other loans are used for business expansion and temporary cash flow. To date, IOU has originated nearly $600 million in loans.

Despite the fact that the lender mostly services the American market, with its headquarters in Montreal and its stock listed on the Toronto Stock Exchange, IOU made a marketing push this quarter to expand its service in Canada.

“We’ve been getting the word out to brokers that we’re looking to serve Canadian merchants,” Marleau said.

Ironically, in many cases, that has meant telling American ISOs who market to Canada that IOU is open for business in its own country.

Marleau, who is Canadian, met cofounder and IOU President Robert Gloer at a fintech conference in San Francisco, and the company’s first loan was made in 2009. Gloer had ties to Atlanta, which is why IOU’s U.S. office is located there. While the company’s headquarters is in Montreal, the Atlanta office is larger and is where the company’s sales operations take place. The company has about 40 employees, but only about ten work at the Montreal headquarters.

Clearbanc Swaps VC Investing for MCA

November 13, 2018 The business model for many startups is that the business won’t even be close to profitable for years until it gets enough clients or users. But this isn’t the case for all startups. Some of them actually generate considerable revenue after just months. For companies like these, that also need capital for marketing or expansion, Clearbanc is interested to work with them.

The business model for many startups is that the business won’t even be close to profitable for years until it gets enough clients or users. But this isn’t the case for all startups. Some of them actually generate considerable revenue after just months. For companies like these, that also need capital for marketing or expansion, Clearbanc is interested to work with them.

Founded as a venture capital firm by serial entrepreneurs Andrew D’Souza and Michele Romanow, among others, the company now primarily offers merchant cash advances. Instead of analyzing the company’s founders, they are looking at tangibles like revenue and percentage growth.

“We pay a lot of attention to our underwriting and decision-making process because if we make a mistake, we can lose a lot of money,” D’Souza, who is CEO, told Techcrunch yesterday. “Unlike a VC, we don’t expect the majority of our companies to fail and have the winners make up for the losses.”

Clearbanc offers cash advances to new businesses in the U.S. and Canada, from $5,000 to $10 million. At this point, Clearbanc only funds eCommerce and Consumer SaaS (software as a service) companies. Also, eligible companies must be incorporated, have a monthly average revenue of at least $10,000 and have at least six months of consistent revenue history.

So far, Clearbanc has funded $100 million to 500 companies in 2018. Founded in 2015, the company is based in Toronto, Canada.

Is Small Business Lending Stuck in the Friend Zone?

October 23, 2018 Small-business owners have lots of places to go for capital, and the alternative small-business funding industry doesn’t exactly top the list, recent research shows. In fact, entrepreneurs claim they’re more than four times as likely to receive funding from a friend or family member than from an online or non-bank source.

Small-business owners have lots of places to go for capital, and the alternative small-business funding industry doesn’t exactly top the list, recent research shows. In fact, entrepreneurs claim they’re more than four times as likely to receive funding from a friend or family member than from an online or non-bank source.

That bit of intelligence comes from the National Small Business Association‘s 2017 Year End Economic Report, the most recent from the Washington-based trade group. Thirteen percent of the entrepreneurs who responded to the survey received loans from family or friends in the preceding 12 months, while 3 percent obtained funding from online or non-bank lenders, the report says.

But some variables come into play. Shopkeepers and restaurateurs are more likely to rely on friends and family for financing during their first five years in business, says Molly Brogan Day, the NSBA’s vice president of public affairs and a 15-year veteran of the survey. The association’s members, who account for many – but not all – of the respondents tend to have been in business longer than non-members so the actual percentage of all owners receiving funds from family or friends could well be higher than the survey indicates, she notes.

In fact, the average NSBA member started his or her business 11 years ago – a fairly long time for the sector, Day says. The association attracts well-established merchants partly because the trade group concentrates on advocacy and lobbying in the nation’s capital, Day notes. “There’s not a lot of networking, there’s not a ton of resources or educational offerings,” she says of the association. In other words, the organization’s emphasis tends to attract prospective members who have been in business long enough to see the results of laws and regulation instead of newcomers still struggling daily to establish themselves, she observes.

Anyway, it’s also worth noting that small-business owners appear nearly as likely to approach family or friends for cash as to petition large banks for funding, Day says, noting that 13 percent turn to friends and family, while 15 percent manage to obtain loans from large banks. To her, that indicates that banks just aren’t lending to small businesses as frequently as they should – a notion that should sound familiar to anyone in the alternative small-business funding industry.

Unsurprisingly, the association’s research indicates bank lending declined as the Great Recession made itself felt in 2007 and 2008. Before that, nearly 50 percent of merchants responding to the survey reported they had recently qualified for loans from big banks, small banks or credit unions, the research shows. “Now it’s pretty consistently a percentage in the low 30’s,” Day says. “People really need these loans.”

Lending by banks hit another snag in 2012 when new regulation and legislation, including the Dodd-Frank Wall Street Reform and Consumer Protection Act, made itself felt. “There was such a massive overcorrection in the banking industry that it’s still really difficult for small businesses to get loans,” Day says.

Moreover, banks were granting fewer “character-based” loans even before the double whammy or recession and regulation, Day observes. Instead of employing the older practice of assessing the intangible virtues of a business owner well-known in the community, bankers began applying a more formulaic approach to evaluating loan applications based on credit scores and other quantifiable variables, she says.

That switch to numbers-oriented decisions proved detrimental for many entrepreneurs. “A lot of small business owners don’t look great on paper,” Day admits. Even a great business plan might not convince bankers to loosen their purse strings these days, she notes.

That’s where the alternative small-business funding industry comes into the picture. NSBA researchers began including the category of online and non-bank lenders in their surveys in 2013 and have seen the percentage of respondents using them grow each year to its current level of 3 percent.

“It’s not huge growth, but it’s notable,” Day says. Notable enough to achieve importance, she continues. “It’s an important opportunity for your readers to fill that void,” she says of the shortfall of adequate small business funding. “They’ve been doing a pretty good job of doing it.”

In fact, the NSBA research indicates that alternative funding and other sources have tended to take up the slack created by the banking industry’s decision to exercise extreme caution when evaluating small business loans. Some 73 percent of small business owners are obtaining enough financing these days, according to the survey.

Yet hiccups have occurred, like the decline to only 59 percent finding adequate funding in 2010, Day points out. And the fact that two-thirds to three fourths are generally securing adequate funding means that a fourth to a third aren’t, she notes, adding that she urges focusing on the latter group. “It’s concerning,” she says.

Inadequate funding can prove especially challenging for newer businesses that don’t have a track record, haven’t stockpiled proceeds from past operations, don’t own stock to leverage and aren’t savvy enough to finesse placement of debt, Day maintains. More-established businesses have greater access to those resources or have honed those skills, she notes.

And much is at stake. Lack of funds not only hurts that significant portion of small-business owner but also prevents hiring workers, stymies economic growth and hinders community development, Day maintains. She points to research that shows the nearly direct correlation between availability of capital and increases in hiring. (See Chart A.)

And much is at stake. Lack of funds not only hurts that significant portion of small-business owner but also prevents hiring workers, stymies economic growth and hinders community development, Day maintains. She points to research that shows the nearly direct correlation between availability of capital and increases in hiring. (See Chart A.)

Other NSBA findings include the fact that in July of 2017 merchants reported having debt that averaged $496,000. Some 73 percent of those reported had at least some debt. Some 40 percent of survey respondents, the largest category have debt of $50,000 or less. (See Chart B.)

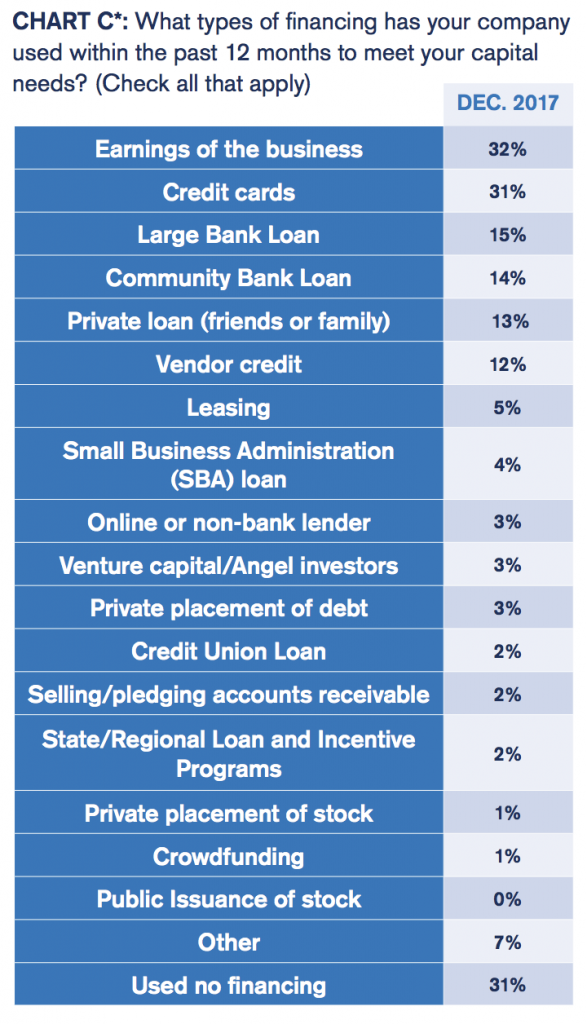

Financing most often comes from funds the business has earned, the trade group says. Some 32 percent of merchants cite that source. Yet simply pulling out a credit card remains a common way to make ends meet, with 31 percent saying they did that to meet capital needs in the last 12 months. (See Chart C.)

While most (57 percent) say that lack of capital hasn’t hurt their enterprises recently, 31 percent say a dearth of capital prevented them from expanding their operations, 14 percent report they weren’t able to expand their sales because they lacked funding, and 13 percent admit they laid off employees because it was difficult to find the cash to meet the payroll. (See Chart. D)

While most (57 percent) say that lack of capital hasn’t hurt their enterprises recently, 31 percent say a dearth of capital prevented them from expanding their operations, 14 percent report they weren’t able to expand their sales because they lacked funding, and 13 percent admit they laid off employees because it was difficult to find the cash to meet the payroll. (See Chart. D)

The availability of credit hadn’t changed much in the year leading up to the survey, the association says. About 77 percent reported no change in their lines of credit or credit cards, while 18 percent saw their perceived creditworthiness increase and 5 percent saw it decline.

Those results come with a bit of history. The NSBA has been surveying small-business owners since 1993. At first, the trade group hired polling companies to perform the task and cooperated on the report with the Arthur Andersen accounting firm. Computerization enabled the association to take the project in house beginning in 2007. It works on the survey with ZipRecruiter, an online employment marketplace.

Some 1,633 small-business owners participated in the research for the 2017 Year End Economic Report by answering 42 questions online in December 2017 and January 2018. Many of the survey questions have remained the same over the years to facilitate comparisons and tracking.

Some 1,633 small-business owners participated in the research for the 2017 Year End Economic Report by answering 42 questions online in December 2017 and January 2018. Many of the survey questions have remained the same over the years to facilitate comparisons and tracking.

Small businesses on the list of members and the list of non-members receive two email messages alerting them to the survey and providing an online link to the questions. The surveys take place twice a year.

As mentioned earlier, some survey respondents belong to the association and some don’t, but Day was unable to pinpoint the percentages. In response to a question from AltFinanceDaily, she said she may begin tallying how many respondents are members and non-members because non-members tend to have been in business for a shorter time than members. Non-members also tend to differ from members because political engagement often brings the former to the association’s attention.

Participating merchants come from every industry and every state, Day says. Manufacturing and professional services are very slightly overrepresented, while mining is the only category that’s scarcely represented, she admits. Not many small businesses operate in the mining sector, she adds.