Investing in the Industry: Break Out of Your Bubble

June 29, 2015 Even if you’re already working in alternative lending and know a lot about your particular area, the industry is growing by leaps and bounds and you might be feeling a little overwhelmed by the multitude of investment opportunities. Amid all the options, finding the right place to invest your money can feel as challenging as picking out the proverbial needle in a haystack.

Even if you’re already working in alternative lending and know a lot about your particular area, the industry is growing by leaps and bounds and you might be feeling a little overwhelmed by the multitude of investment opportunities. Amid all the options, finding the right place to invest your money can feel as challenging as picking out the proverbial needle in a haystack.

“Most people don’t know everything that’s out there. There are huge opportunities,” says Peter Renton, an investor and analyst who founded Lend Academy LLC of Denver, Colorado, a popular resource for the online lending industry.

Indeed, there are a growing number of online alternative lending sites that theoretically allow a person to invest in all shapes and sizes of loans. There are sites like Lending Club and Prosper that allow smaller investors to tap into the burgeoning P2P market. There are also a plethora of platforms that cater only to wealthier, more sophisticated investors in a host of areas like small business, real estate, student loans and consumer loans.

Even though there is a surplus of options, prudent investing is not quite as simple as depositing ample funds in an account and clicking the “go” button. Before you get started, you need to carefully consider factors such as your own finances and risk tolerance. You should also have a good handle on the specifics about the online platform—how it works, its history and track record, the types of investments it offers, the platform’s management team, technology and your ability to diversify based on available investment opportunities.

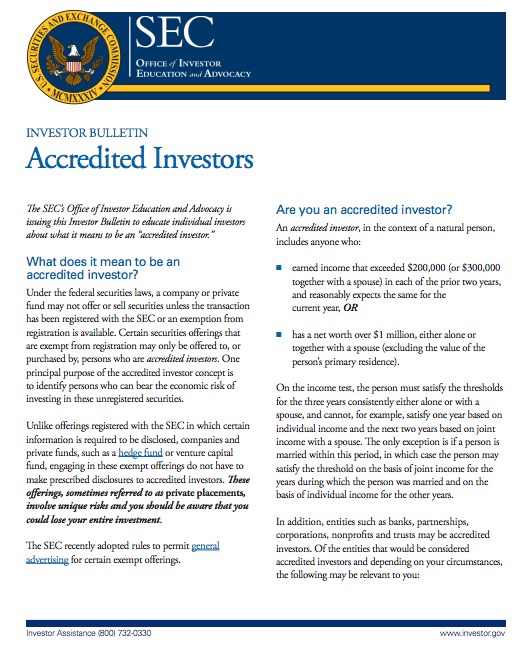

One of the first things you’ll have to think about as a potential investor is whether you have the financial wherewithal to be considered accredited by the SEC. If the answer’s yes, you’ll have a lot more choices of online marketplaces to choose from as well as types of investments. Basically, to meet the SEC’s threshold, you’ll need to have earned income that exceeded $200,000 (or $300,000 together with a spouse) in each of the prior two years, and reasonably expect to earn the same for the current year. Alternatively, you need to have a net worth over $1 million, either alone or together with a spouse (excluding the value of your home). (Check out the SEC’s website for more detailed info.)

If you don’t fit the definition of accredited investor, it’ll be more difficult for you to find out about all the investment possibilities that are on the market today. That’s because the platforms that cater to accredited investors aren’t allowed by SEC rules to solicit, so many online marketplaces are hesitant to say much of anything for fear their words will be misconstrued by regulators as an attempt to drum up new business. With limited exceptions, you won’t be able to get more than very basic information from and about these platforms’ unless you are accredited.

If you don’t fit the definition of accredited investor, it’ll be more difficult for you to find out about all the investment possibilities that are on the market today. That’s because the platforms that cater to accredited investors aren’t allowed by SEC rules to solicit, so many online marketplaces are hesitant to say much of anything for fear their words will be misconstrued by regulators as an attempt to drum up new business. With limited exceptions, you won’t be able to get more than very basic information from and about these platforms’ unless you are accredited.

But smaller investors do have options. Two San Francisco-based online lending platforms, Lending Club and Prosper, cater to individual investors, and you can still make a pretty penny plunking down money with these venues. You’ll also find a wealth of information about investing with them by perusing their websites as well as by reading the blog posts of media-savvy financiers.

“Right now, Lending Club and Prosper provide a great entry point for people who want to get involved in investing in alternative lending,” says Renton of Lend Academy.

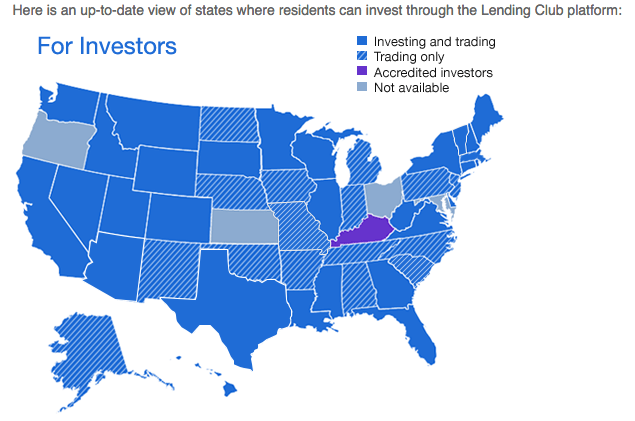

The caveat is that these platforms aren’t yet open to investors in every state, so if yours isn’t on the list you’re out of luck for now. However, with each marketplace you’ve got more than a 50 percent chance your state is on the approved list, so it’s worth digging deeper.

Assuming you meet their respective suitability requirements, you can choose to invest on one platform or both. To be sure, they are alike in many ways. Both allow you to invest with as little as $25 and fund one loan, however they recommend you buy at least 100 loans to be properly diversified, which you can do for as little as $2,500. You can manually choose which loans to buy, or enter your investment criteria so loan picking is automated. You can also invest retirement money in an IRA through Lending Club or Prosper.

There’s no fee to get started investing on either platform. For Lending Club, investors pay a service fee equal to 1 percent of the amount of payments received within 15 days of the payment due date. Prosper charges investors 1% per year on the outstanding balance of the loan. As the loan gets smaller, the servicing fee, which is charged monthly, gets smaller too.

To invest in Lending Club, in most cases you’ll need either $70,000 in income and a net worth of at least $70,000, or a net worth of at least $250,000. There may be other financial suitability requirements that vary slightly depending on the state you live in. For Prosper, individual investors must be United States residents who are 18 years of age or older and have a valid Social Security number.

At any given time, Lending Club has more than 1,000 loans visible on the platform and new ones get added every day, according to Scott Sanborn, chief operating officer and chief marketing officer. Prosper, meanwhile, on average has more than 200 loans for people to invest in, says Ron Suber, president.

Returns tend to be favorable compared with other fixed income investments—a major reason investing in online loans is becoming more desirable. Of course, actual returns will depend on what loans you invest in and the level of risk you take—typically the more risk you take on, the greater your potential return will be. At Lending Club, for instance, Grade-A loans have an adjusted net annualized return of 4.89%, compared with 9.11% for Grade-E loans, according to the company’s website.

Returns tend to be favorable compared with other fixed income investments—a major reason investing in online loans is becoming more desirable. Of course, actual returns will depend on what loans you invest in and the level of risk you take—typically the more risk you take on, the greater your potential return will be. At Lending Club, for instance, Grade-A loans have an adjusted net annualized return of 4.89%, compared with 9.11% for Grade-E loans, according to the company’s website.

To encourage more people to start investing, some savvy investors have started to self-publish online the quarterly returns they accumulate through the Lending Club and Prosper platforms. Renton, of Lend Academy, reported a balance of $476,769 on Dec. 31, 2014 and a real-world return for the trailing 12 months of 11.11 percent. Another well-known P2P investor and blogger, Simon Cunningham—the founder of LendingMemo Media in Seattle—reported a 12-month trailing return of 12.0 percent over the same time period, with a published account value of $41,496. Both investors say they expect returns to drop back somewhat over time, however, as the online marketplaces continue to lower interest rates to attract more borrowers.

Of course, if you’re an accredited investor, you will have access to even more online marketplaces. For instance, there’s SoFi of San Francisco for student loans, Realty Mogul of Los Angeles for real estate loans and Upstart of Palo Alto, California, that focuses on loans to people with thin or no credit history. The list of possibilities goes on and on.

Generally speaking, the more money you have to invest, the more options you have. “In this country today, you’ve got well over a hundred options if you’re willing to put seven figures in,” Renton says.

The minimums at venues that focus on accredited investors tend to be more than you’d find at Lending Club or Prosper. At SoFi, accredited investors need at least $10,000 to begin investing in the company’s unsecured corporate debt. SoFi’s been in the lending business for several years now and currently focuses on student loans, mortgages, personal loans and MBA loans. Investors, however, can’t currently invest in these loans, says Christina Kramlich, co-head of marketplace investments and investor relations at SoFi. The company plans to eventually offer investment opportunities in the areas of mortgages and personal loans, she says.

At Funding Circle USA in San Francisco, accredited investors can buy into a limited partnership fund for at least $250,000. Or they can buy pieces of small business loans for a minimum of $1,000 each, though the recommended minimum is $50,000, explains Albert Periu, head of capital markets. There may also be upper limits on your investment, based on your financials. If you’re part of the pick-and-choose marketplace, you’ll pay an annual servicing fee of 1%. With the fund, you’ll also pay an administration fee of 1%. Trailing 12-month net returns for investors are north of 10%, Periu says.

At Funding Circle USA in San Francisco, accredited investors can buy into a limited partnership fund for at least $250,000. Or they can buy pieces of small business loans for a minimum of $1,000 each, though the recommended minimum is $50,000, explains Albert Periu, head of capital markets. There may also be upper limits on your investment, based on your financials. If you’re part of the pick-and-choose marketplace, you’ll pay an annual servicing fee of 1%. With the fund, you’ll also pay an administration fee of 1%. Trailing 12-month net returns for investors are north of 10%, Periu says.

Because it’s still so new, it can be hard for investors to know how to compare marketplaces. For starters, consider the platform’s historical performance. There are a lot of new marketplaces popping up, but it takes time to develop a proven track record. This isn’t to say you shouldn’t dabble with the newer platforms, but if you do, you’ll want above-average returns to balance out the higher risk, says Sanborn of Lending Club. “About three years in, we started to build a track record. At five years in, it was very solid,” he says. “You need time to see how a basic batch of loans is going to perform.”

Before investing, you’ll want to get a sense of how committed senior management is to the company and try and get a sense of whether the company seems to have enough capital for the business to run well. Try to find out about the cash position of the company, how the loans are going to be serviced, what entity is doing the underwriting and how and where your cash will be held.

“It’s not just assessing the risk of the asset and the investment, it’s assessing the risk of the enterprise that is making it available to you,” Sanborn says.

It’s also important to ask questions about the loans themselves. Where do they come from and is the volume sustainable? Ideally, a platform should offer a variety of loans so investors can properly diversify, or you might need to consider investing with multiple platforms to achieve your desired balance.

Before you get started, you’ll also want to ask about the company’s compliance procedures and controls and how you can recover your money if you no longer want to invest. Data security is another area to explore. Not every company is as protective of customer data as perhaps they should be.

Before you get started, you’ll also want to ask about the company’s compliance procedures and controls and how you can recover your money if you no longer want to invest. Data security is another area to explore. Not every company is as protective of customer data as perhaps they should be.

When you’re asking all these questions, try to get a sense of how receptive the platform is to the feelers you’re putting out. Investors should only work with companies that are willing to be open about how they are investing your money, their historical returns and other important data. “I can’t stress transparency enough,” says Periu of Funding Circle.

The technology the platform uses is another key element. Is the technology easy to use, or does the platform create stumbling blocks for investors? Are there ways to automate lending, or do you have to log on every day and manually invest in loans?

Suber of Prosper says investors should also consider whether platforms work with a back-up servicer in case there’s a disruption and whether they run regular tests to make sure everything works as expected. “It’s just like a backup generator and you have to test it every once in a while and make sure it goes on.”

Certainly it pays to do your homework before you invest your hard-earned cash with an online platform. Ask around, attend industry conferences and absorb all you can from publicly available data. The good news is that there will probably be even more information for you to tap into as the industry continues to grow.

“Two years ago [marketplace lending] was very esoteric. A year ago it was still esoteric,” says Funding Circle’s Periu. Now, more and more investors are hearing about marketplace lending and want to make it part of their broader fixed income bucket. Even so, more has to happen for it to become a mainstream investment. “Awareness and education need to continue,” he says.

Once more people understand the extent of what’s out there, Suber of Prosper expects investing in online marketplaces will take off even more than it already has. “A lot of people still don’t know this as an investment opportunity,” he says.

Small Business Lending is King to Institutional Investors

June 2, 2015

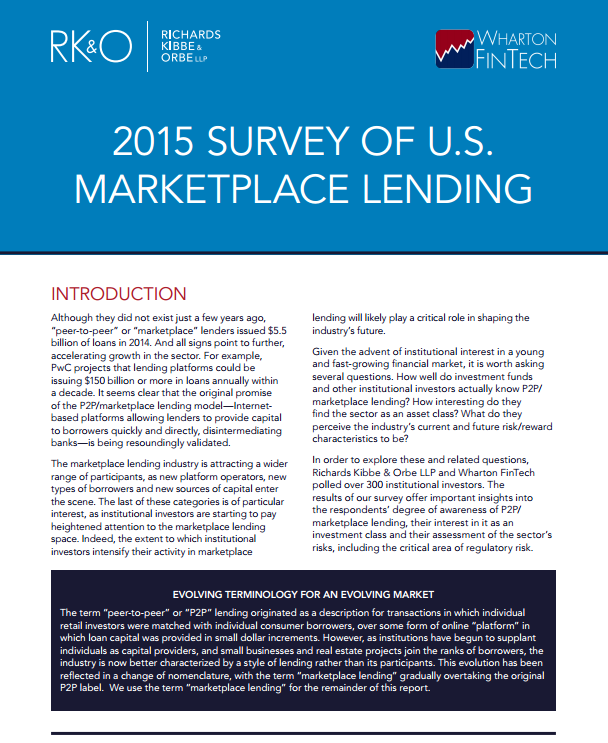

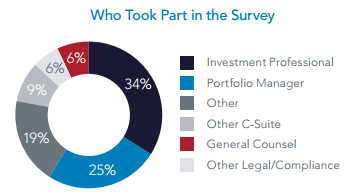

Richards Kibbe & Orbe LLP and Wharton FinTech polled more than 300 institutional investors to gauge their thoughts on marketplace lending. They published their findings in a recently released report.

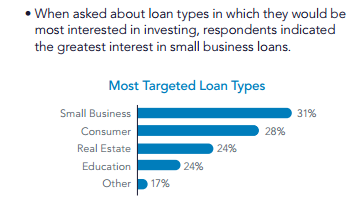

The surveyors seemed surprised that institutional investors indicated their interest in small business loans was greater than that of consumer, real estate, education, and everything else.

Securitizations ranked lowest on the list of investments worth pursuing and buying whole loans was second only to “multiple strategies.”

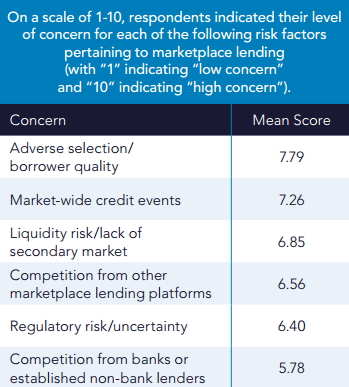

Regulatory risk and uncertainty was low on the list of concerns while borrower quality was the most concerning factor. Curiously, competition was the least concerning of all.

Speaking to the liquidity issues of the assets, institutional investors indicated that the development of a mature secondary trading market was more likely than anything else to lessen their concerns about marketplace lending.

Do any of these results surprise you?

Download the Key Findings report

Letter From the Editor – May/June 2015

May 1, 2015 Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

New financial products can be just as intimidating to the professionals working within the wider industry as they are to the customers they’re being offered to. I’ve blogged often of my experience investing in Lending Club and Prosper notes, something I assumed everyone in the business finance world could relate to. Alas, I find that usually raises more questions with readers than it does answers.

Are you just nodding your head and smiling when your peers talk about their alternative lending portfolios? There’s no better way to understand today’s loan marketplaces than being an investor in them, even if it’s just a small amount. Whether it’s merchant cash advances, real estate loans, student loans, or credit card debt, there are plenty of opportunities and worlds to explore. You should conduct research, diversify, and be smart of course. You don’t want to be trapped in a bubble.

Outside the knowledge bubbles, we have regional enclaves. There are entire city neighborhoods being overrun by small business financing startups. In New York City, it had long been Midtown, but some shops started moving south and before anyone realized what was happening, Wall Street had been overrun by a new breed of broker. The culture in lower Manhattan is different than you might find in Midtown or in the next two largest industry hubs, Miami and San Francisco.

In this issue, we’ll begin to explore the industry’s bubbles, both geographically and structurally.

–Sean Murray

When Merchant Cash Advance isn’t the Right Fit

August 12, 2013 “I know you do a million in gross sales monthly but since you process only $5,000 in credit cards, we can only approve you for $7,000.”

“I know you do a million in gross sales monthly but since you process only $5,000 in credit cards, we can only approve you for $7,000.”

Before ACH repayment became mainstream, the MCA industry was incredibly restrained in its ability to help businesses. A merchant seeking a half million dollars with the cash flow and size to back that request up was being told that the absolute best they could get would be maybe $10,000, and that’s with a 100% holdback in place instead of the industry standard max of 30-35%. It was an awkward sale for both parties.

To pitch a business owner generating $12 million a year in sales a paltry $10,000 is like telling your boss that the only thing you did at work this month is forward a single e-mail. To the business owner, they’re probably left wondering if lending really has dried up that much or perhaps they’re wondering if they’re just talking to the wrong people. Some of these mismatched situations actually turn into closed deals. I can personally remember one where a semi-serious request for $2 million became a $6,000 signed contract. I think they waited only 24 hours before applying for a renewal. The majority of these sales calls go nowhere though because what’s being offered is not a fit for what is needed.

It’s okay to have mismatches in life. As a salesman, your product is not the right solution for EVERY problem, no matter what your rebuttal script says. If a man is wheeled into an emergency room with 7 deep stab wounds, Johnson & Johnson is going to have to pass up the opportunity to offer him Band-Aids as the answer. A million Band-Aids might work, but they’re not the right solution.

In 2013, I am hearing a wider call to diversify product offerings to stay competitive. Yes, offering a fixed daily repayment loan based off of gross sales is a nice way to compliment the purchase of future credit card sales, but that’s not really diversity anymore, that’s a necessity to stay alive. By really diversifying, I’m talking about financial products beyond daily repayment loans and advances. Almost everyone agrees that being able to service more deals is a good thing but when it comes right down to it, they may see it as a distraction from their main focus.

We’ve all seen a friend or two bite off more than they can chew by trying to broker an SBA loan or commercial real estate deal. There’s no shortage of financial companies sitting on the periphery of the MCA industry waving a flag that says “if a deal isn’t compatible for you, then send it our way.” They don’t really speak the MCA language though and they expect you to do a lot of the closing and negotiating on your own. Some of these deals take months to process and if the lender believes the deal is only a one-time thing, they might not even pay you for it. Ugh! Looking at it from this perspective, perhaps it’s better to just stick with MCA and let every other type of deal fall by the wayside, that is until you look at your marketing expenses again and wonder…

An inbound lead is one that you’ve already paid for, so if they’re not a candidate for a daily repayment loan or advance, then what is the most efficient way to monetize and service them? Who can you really depend on to make servicing it a reality and how long will it take? How easy will it be? I searched beyond the industry for answers but began to find them inward. It seems New York City based Strategic Funding Source has recognized the need for product diversification and is eager to assist account reps in servicing more clients and closing more deals. Your marketing dollars are already spent, so now it’s time to monetize what they’re bringing in. There is a universe beyond daily repayment deals and if you hope to stay ahead of the curve, I recommend you become intimately familiar with programs like invoice factoring and accounts receivable factoring. You can and should be doing deals of this nature every month, not once in a blue moon.

While I like to consider myself knowledgeable on a wide range of financial topics, Lenny Leff, who heads Strategic Plus, a new division of Strategic Funding Source, has offered to write his own regular column on Merchant Processing Resource.

I spoke to David Sederholt, Strategic Funding Source’s COO, about this first in regards to Lenny’s role at the company:

“Through this new division of Strategic Funding Source, led by Lenny, we can say ‘yes’ to more businesses seeking capital to grow and are not limited to cash advance and loan products. We take a human approach to financing and know that the needs of small business owners are as diverse as the businesses themselves. With more product offerings, we are able to continue to be true partners to the small businesses we finance.”

– David Sederholt, Strategic Funding Source COO

Lenny’s posts will provide guidance and information about opportunities outside of MCA. After a few in-person meetings, I think he is uniquely positioned to discuss this topic, especially considering his prior experience in the MCA industry. I asked if Lenny would introduce himself in this post and he added the following:

“I am happy to be joining Strategic and look forward to sharing my 15+ years experience in factoring and asset based lending. The blog will give business owners and ISOs the opportunity to learn more about the different solutions and alternatives available when they go to someone offering a one-stop shop; Purchase Order Financing, Invoice Factoring, Equipment Leasing, Healthcare Lending to Business Loans and MCA. Our goal is to expand the knowledge within our community and help our partners find customized financing for their clients. We are thrilled and excited to share our insights with Sean and the Merchant Processing Resource site.”

– Lenny Leff, Strategic Plus

When the deal doesn’t fit, will you try to sell it anyway? Will you throw it out? Or will you try to monetize the lead you’ve already paid for? I don’t like the first two options… and I’m sure many of you don’t either.

Learn more about Strategic Plus at http://www.sfscapital.com/news/view/3596

Contributors

David Sederholt

Lenny Leff

Discuss factoring on DailyFunder

http://dailyfunder.com/showthread.php/353-PO-Financing-Factoring/page2

The Other 93%

July 13, 2012The SEO war rages on for Merchant Cash Advance providers, ISOs, micro lenders, and other financing firms, but just how much real estate is everyone really fighting over? According to data recently provided in The Green Sheet by First Annapolis Consulting, only 7% of all merchant account leads are generated via the Internet. So if your business plan’s success hinges on getting to page 1 of Google search, you might be shutting yourself out from nearly the entire marketplace. Don’t get us wrong, there’s a lot of money to be made and business to be acquired via the Internet, but even the big firms get roughed up from time to time by competition, new algorithms, and SEO companies that promise the world but deliver few results.

So if not the Internet, then what else is there besides cold calling? That’s a question that tons of small ISOs ask themselves when they realize that competing online isn’t easy. It just so happens that the “what else” comprises of 85% of all generated leads in the payments industry. More than 50% are derived from bank referrals and associations alone.

Has anyone ever wondered why companies like AdvanceMe (Capital Access Network) are still number one in the Merchant Cash Advance arena? They’ve managed to defy Darwin’s theory of evolution. In every industry, there is a pioneer that leads the way, gets too comfortable, stops innovating, and is systematically made irrelevant by fresh thinking competition. There was MySpace until there was Facebook. There was Yahoo until there was Google. There was AOL until…there was just everything else.

So one would expect that in 2012, the mere mention of AdvanceMe would be part of a requiem for the founding fathers of the Merchant Cash Advance industry. That isn’t the case and is quite the opposite considering they are on pace to fund at least $700 million this year. So they must be #1 on Google, right? Nope. For all of the main keywords that people are fighting over, they rarely if ever, even show up on the first page of the results.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

All the sales pitches in the world about lower rates and free POS systems aren’t going to compete with a merchant who has just been given a referral by a company they already have a relationship with. Hell, even you have probably enlisted an insurance company, wedding vendor, or mortgage broker because someone you trusted said they were great.

This isn’t another lecture about how referrals are crazy good and that cold calling is wicked bad, especially since we don’t even necessarily feel that way. The point is really to highlight just how much more potential there is out there for small funders and ISOs. You can actually be successful with a sucky website and no SEO if you can just solidify some key relationships.

If you want to be around 14 years later, you can’t ignore the other 93% of the market. The volume of Internet leads will probably increase in the future as more computer savvy people become small business owners. But it’s way too easy to set up a website, hire an SEO guy, and throw money at Pay-Per-Click. Anyone can do it and everyone is doing it. That means most companies are losing the battle and tons of you are saying “what else is there?” Fortunately, the lead generation pie chart offers unlimited hope. You just need to think bigger and try harder.

If the other categories seem too ambitious, well then you’ll never make it in this biz kid…

Media, Market Duped Again in Fintech Fake News

September 13, 2021 Multiple media outlets fell victim to a major hoax Monday morning, after GlobeNewsWire claimed that Walmart was beginning to accept Litecoin as tender for purchases in its stores. The wire seemed legit — a formally structured release from a credible source that was packed with quotes form Walmart’s CEO Doug McMillon about the company’s apparent move.

Multiple media outlets fell victim to a major hoax Monday morning, after GlobeNewsWire claimed that Walmart was beginning to accept Litecoin as tender for purchases in its stores. The wire seemed legit — a formally structured release from a credible source that was packed with quotes form Walmart’s CEO Doug McMillon about the company’s apparent move.

With a bad link on the release alongside silence of the supposed partnership on Walmart’s end, skeptics quickly realized that no move was ever in the works. After denying the validity of the release, tons of major outlets began scurrying to announce the hoax.

The motive may have been to artificially inflate Litecoin, as it shot up 35% minutes after outlets ran with the story.

This is eerily like one of the industry’s most infamous hoaxes, when the news service known as Internet Wire made headlines for the wrong reasons back in 2000. Then 23-year old Mark Jakob was out almost $100,000 after shorting stock for the Emulex Corporation, which he attempted to recoup by writing a fake press release stating that the company was going to restate quarterly earnings as losses, and their CEO was quitting the company. Jakob was a former employee of Internet Wire and a community college student at the time.

His faux release resulted in Emulex losing over $2 billion in market cap, while Jakob netted almost a quarter of a million dollars to cover his shorts and then some.

Jakob later pled guilty to creating the fake release in order to cover his shorts. He earned himself over 40 months behind bars, forfeited all of his earnings, and was handed a 6-figure penalty for his actions.

Then there was PRWeb’s publishing of a press release that falsely stated that Google had made a $400 million deal to purchase a Rhode Island- based wireless hotspot provider in 2012, which made the provider’s shares jump dramatically. Many major media outlets took PRWeb at their word and ran with the story. It was later discovered that the release was completely bogus and had come from a Gmail account that had originated in Aruba.

Reporting with one hundred percent accuracy is difficult. Information updates, numbers fluctuate, and deadlines loom. Vetting sources is an integral part of being a quality journalist, but even the best can get fooled, turning perceived truth into a manipulated consensus of reality.

In fintech news however, these hoaxes aren’t just blurring facts and changing narratives, they could result in the moving of billions of dollars around the market before the deception is revealed.

Notorious Tampa Bay Loan Broker Likely Headed Back to Jail

July 27, 2018 Tampa Bay loan broker Victor Clavizzao pleaded guilty this week to one count of wire fraud, which could land him in prison for up to 20 years. This would not be his first time behind bars. In 2009, a federal judge sentenced him to five years for conspiring to fraudulently obtain nearly $6 million in mortgage loans.

Tampa Bay loan broker Victor Clavizzao pleaded guilty this week to one count of wire fraud, which could land him in prison for up to 20 years. This would not be his first time behind bars. In 2009, a federal judge sentenced him to five years for conspiring to fraudulently obtain nearly $6 million in mortgage loans.

This time, Clavizzao, 55, cheated a church congregation out of $16,350 that they had set aside to build a new church. According to a Tampa Bay Times story, shortly after leaving prison in 2014, Clavizzao was still on probation when he created Key Business Loans. Around the same time, he met husband and wife, Sam and Minnie Wright. Minnie Wright is the pastor of the Tampa Bay-area New Testament Outreach Holiness Church #2, and she asked Clavizzao if his company would be able to make a loan to their church.

According to the Tampa Bay Times story, Clavizzao said “Absolutely.”

Clavizzao, who used the named Victor Thomas, ingratiated himself with the Wrights and other church congregants and told them that not only could he help them obtain a $650,000 loan, he could also handle the purchase of the plot of land along with other details. The church gave Clavizzao a series of initial payments – for an architect and for an environment inspection of the land – and when the Wrights started getting suspicious, Clavizzao disappeared.

Last year, suspected of defrauding the Wrights and others, Clavizzao told Tampa Bay Times in a phone interview that his business, Key Business Loans, was completely legitimate.

“Knock yourself out, I’m not doing anything wrong,” he said, acknowledging that he discloses his criminal history to prospective borrowers. “Any person who has a problem about my past can choose to do business with me or not do business.”

In July of 2014, Clavizzao presented the Wrights with a “Proposal Letter for Guaranteed Business Purchase Loan” from Key Capital Commercial Funding, a New York City-based company he said he had ties with. The proposal outlined the terms of a 15-year, $650,000 loan at 5.1 percent interest. The Wrights signed it. However, what the Wrights did not know at the time was that there was no Key Capital Commercial Funding in New York City, or anywhere else.

In part because of persistent reporting on Clavizzao from Susan Taylor Martin at Tampa Bay Times, the Wrights were able to learn more about Clavizzao’s criminal past and the FBI got involved.

After Clavizzao’s recent guilty plea, he is currently out on bond pending his sentencing. A date has not been set.

Introducing LendingRobot Series: One-Stop Investing in Alternative Lending

January 26, 2017January 26, 2017 – Seattle, WA – LendingRobot, the first robo-advisor for Alternative Lending built for individual investors, announced today the launch of robo-fund LendingRobot Series. Designed as an alternative to traditional fixed income investments, LendingRobot Series is a one-stop solution that combines cloud-based investment automation, fully transparent fund secured by Blockchain technology and sophisticated machine learning algorithms to provide superior, predictable returns uncorrelated to stock market performance.

LendingRobot Series is a unique combination of a robo-advisor and an investment fund, created as one-stop solution for accredited investors looking for a way to easily invest in consumer, small business or real-estate loans diversified across multiple ‘peer lending’ origination platforms.

“Alternative lending proved to return excellent performance and with new origination platforms growing quickly comes the opportunity to diversify further. But fragmentation makes investing even more complex for individual investors” said Emmanuel Marot, CEO of LendingRobot.

Unlike a traditional fund, LendingRobot Series improves liquidity, is flexible with regards to loan selection, and 100% transparent. Investors decide what kind of risk and time horizon they want, and LendingRobot automatically manages their investments.

Hedge Funds typically charge management fees of 2% plus 20% of performance, plus obscure or unlimited fund expenses, which makes their expense ratio disproportionate to fixed income returns. In contrast with traditional investment firms, LendingRobot Series only charges 1.00% of assets under management, and caps fund expenses at 0.59%.

“Turmoil within the past twelve months among some of the largest origination platforms showed that ‘platform risk’ is real, and left many clients increasingly worried about investing only in unsecured consumer loans despite the fact that the returns have remained steady,” continued Mr. Marot. “All investors would be well served by diversifying into multiple marketplaces, but that process is tedious, complicated, and requires a high degree of domain expertise to accomplish correctly. That’s why we’ve created LendingRobot Series: to provide investors that understand the value of investing in Alternative Lending with the confidence that comes from intelligent automation, easy liquidity, and complete transparency.”

LendingRobot manages investments across four different Series, with target maturity going from 20 to 36 months, and net returns up to 9.66%. Investor’s money is converted in Units of ownership in these Series, that are issued on a weekly basis. By default, loans payments keep being re-invested and the Units value increases. LendingRobot publishes every week a detailed ledger of its holdings, down to the value and individual payments made by each note.

A ‘Hash code’ signature of the ledger is integrated in the subsequent versions as well as notarized in Ethereum’s Blockchain to ensure the data is tamper-proof.

To ensure maximum safety, assets are hold in a bankruptcy protection vehicle, with no other liabilities than its investors.

Investors willing to cash simply flip a switch on the LendingRobot website to start redeeming their Units on a weekly basis. Between 33% and 100% of loan payments are distributed in priority for redemption, which means that under normal circumstances investors should be able to cash out entirely in less than 3 weeks.

Investors interested in learning more about LendingRobot Series can visit www.lendingrobot.com/series.

About LendingRobot:

LendingRobot is a fully automated investment service for alternative lending platforms including Lending Club, Prosper and Funding Circle. After signing up for a LendingRobot account, investors select their risk tolerance and enable LendingRobot to instantly make investments on their behalf. Based in Seattle, Washington, LendingRobot serves 6,500 clients totaling over $120M in assets.