The Top 10 Alternative Small Business Funders

April 12, 2016At Lendit yesterday, I learned the 2015 origination volume of two additional small business funders that I was not able to ascertain previously. They are CA-based National Funding and GA-based Kabbage. Below is a list of the original top 8 funders that has been amended to form the top 10.

RANKINGS

| Company Name | 2015 Funding Volume | 2014 Funding Volume |

| OnDeck | $1,900,000,000 | $1,200,000,000 |

| CAN Capital | $1,500,000,000 | $1,000,000,000 |

| Funding Circle | $1,200,000,000 | $600,000,000 |

| Kabbage | $1,000,000,000 | $400,000,000 |

| PayPal Working Capital | $900,000,000 | $250,000,000 |

| Bizfi | $480,000,000 | $277,000,000 |

| Fundry (Yellowstone Capital) | $422,000,000 | $290,000,000 |

| Square Capital | $400,000,000 | $100,000,000 |

| Strategic Funding Source | $375,000,000 | $280,000,000 |

| National Funding | $293,000,000 |

An even larger list exists in the current issue of our magazine. To subscribe to future issues for free, click here.

Collude, not collide: Why Online Lenders Want to Work with Banks

April 8, 2016 Don’t look now but online lenders are in cahoots with the banks they want to disrupt.

Don’t look now but online lenders are in cahoots with the banks they want to disrupt.

Last week (April 4th), Spanish banking giant Santander shut down 450 branches and partnered with Atlanta-based Kabbage to speed up the underwriting process to provide same day loans.

Today, online consumer lender Avant announced a similar deal with Birmingham, Alabama-based Regions Bank to offer loans anywhere between $1,000 to $35,000. Regions will use Avant’s platform on its website to sell unsecured loans where borrowers get an immediate credit decision and are approved or rejected immediately, with funds being available the very next day.

“Working with Avant, we will be able to offer a better online experience, while maintaining our commitment to responsible lending — something that benefits customers, the community and our shareholders,” said Logan Pichel, executive vice president and head of Consumer Lending for Regions Bank. That said, Regions does not typically approve borrowers with a credit score below 700 while Avant’s customers average a 650 credit score.

So why are lenders befriending the banks they wanted to fight? And what’s in it for banks? Access to a bigger customer banks and quick loan approvals. Banks want to tap into the lean and loose loan processing model that online lenders have become popular for, throwing open a hitherto market of risky borrowers.

Last year, JP Morgan Chase partnered with OnDeck to speed up small business loans for some of the bank’s 4 million customers. As banks tend to lean towards working with alt lenders rather than building competitive products in-house, the industry will only see more such partnerships. As for Avant, the company has more such deals in the pipeline, Adam Hughes, Avant chief operating officer said.

Any bets on who might be next?

Q1 Update: Here are Five Partnership Deals Lenders Struck

April 6, 2016

It’s the end of Q1 and it’s time for that scorecard and see what lenders were up to. The year has been favorable for marketplace and online lenders so far. The Fed kept rates unchanged, small business borrowing peaked in February and many of these companies made impressive hires. As companies prepare for the second quarter, here are some of the key partnerships made by online lenders so far this year.

Opus-OnDeck

The year started with a bang for alt lending posterboy OnDeck Capital with a referral arrangement with California-based Opus Bank. OnDeck will finance Opus’ small business clients requiring up to $500,000 through lines of credit, flexible term loans and quicker processing.

Prosper-HomeAdvisor

Home improvement loans have been a cash cow for San Francisco-based Prosper Loans. Last month, (March 14th), marketplace HomeAdvisor entered into an exclusive multi-year contract with Prosper to provide home improvement loans after the company quietly terminated a similar contract with Lending Club.

As of 2014, approximately 8 percent of Prosper borrowers said their loan was for home improvement. Orchard, in its analysis states that these loans may in part be a substitute for traditional home equity lines of credit, which used to be easier to obtain prior to the housing crash.

Bizfi-West Coast Banking Group,

Small business lender Bizfi struck a deal with Western Independent Bankers, a trade association of community banks in the west coast to be the exclusive alternative finance lender for small businesses that are members of the association.

The New York-based alternative lender also signed on the New York State Restaurant Association to provide equipment financing, invoice financing and lines of credit for 2,000 restaurants that are members.

Avant-Loandepot

Consumer lending company loandepot and marketplace lender Avant launched a borrower referral program. Under the mutual borrower program, the two companies will have access to each other’s customer base to “expand credit options to responsible borrowers.”

Kabbage-NFIB, Santander

Atlanta-based Kabbage landed itself a sweet deal with the National Federation of Independent Business, throwing open a potential market of 325,000 small businesses where members can access lines of credit of up to $100,000 and flexible term loans.

Kabbage also debuted in the UK with Santander Bank which will use Kabbage’s technology to underwrite quick loans up to 100,000 pounds the same day for loans that typically take 2-12 weeks to process.

Why OnDeck Wants Small Biz Owners to be Financially Literate

April 5, 2016 OnDeck is preparing a market it can serve.

OnDeck is preparing a market it can serve.

The New York-based lender partnered with SCORE, a non profit mentoring small businesses to offer training workshops to its mentors.

OnDeck’s training aims to raise awareness for alternative forms of lending such as crowdfunding, invoice financing among small businesses who typically borrow from banks. OnDeck will also screen entrepreneurs and small businesses for financing options they may qualify for.

Outreach and borrower referral programs have become far too common and a back door entry for marketplace lenders as they gradually march forth on banks’ turf. Last week, (March 31st) The National Federation of Independent Business (NFIB) joined hands with Atlanta-based Kabbage Capital throwing open a potential customer base of 325,000 businesses. Thanks to alt lenders or not, small business borrowing is growing. Reuters data showed that borrowing was up 17 percent in February, edging up from a two year low in January.

So maybe it’s working?

Bizfi Partners With West Coast Banking Group

March 17, 2016Bizfi will be the exclusive alternative finance solutions provider for small businesses that are members of the Western Independent Bankers, a trade association of community banks in the west coast.

Small businesses in the midwest and west coast in states including Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada New Mexico, Oregon, Utah, Washington and Wyoming can benefit from this partnership. Bizfi’s marketplace partners with lenders like OnDeck, Funding Circle and Kabbage.

“WIB member banks are the leading funders of America’s small businesses,” said Michael Delucchi, President and Chief Executive Officer of WIB and WIB Service Corporation. “With Bizfi as a WIB Premier Solutions Provider we are able to offer their expertise in alternative financing and superior technology to our member banks and deliver a complete solution for small business funding.”

Earlier this month, Bizfi partnered with The New York State Restaurant Association to provide business financing for its 2,000 small businesses in the restaurant space.

Google Culls Online Lenders – Pay or Else?

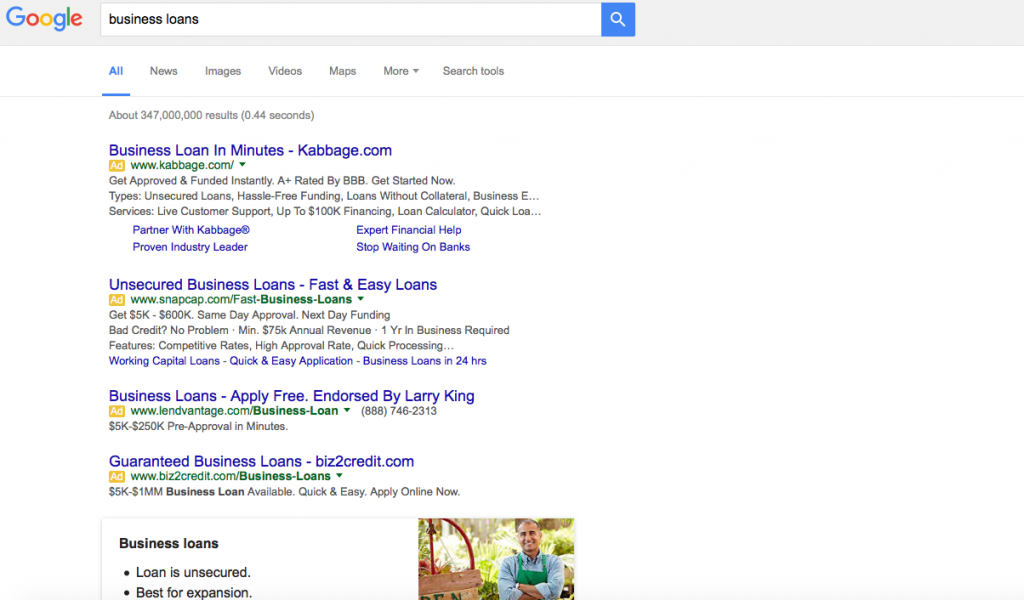

March 15, 2016Can you become one of the biggest or most successful online lenders without Google? A search layout update may be inadvertently culling the herd.

In late February, Google eliminated ads from the right side of the page while adding another layer to the top and bottom. When factoring in features like site links, the effects on organic search has been devastating. Non-paid links are now entirely below the fold for many commercial keywords, which means users may limit their selections entirely to ads. Here’s an example of a full screen browser window on a Macbook Air when searching for Business Loans:

Brad Geddes, a Google Adwords marketing author, expert and consultant, has said the Click-through rate (CTR) on this new 4th ad placement is skyrocketing. “Depending on the keyword, position 4 is going to have a 400%-1000% CTR increase,” he said on Webmaster world. And while side links and bottom links were never a huge factor anyway (less than 15% of click-throughs), Geddes believes a consequence of this change is that fewer ad slots means higher cost bids to rank on the 1st page. “Companies with thin margins are going to have a lot of words fall to page 2,” he wrote.

In summary: Fewer ad placements, higher costs per click, decreased likelihood of organic click-throughs.

And the online lending industry is already feeling the burn. Several funders and ISOs on the commercial side have told AltFinanceDaily in confidence that the online lead gen battle has been lost or that they have been temporarily sidelined by the increase in costs. At least one funder is refocusing their efforts entirely on the ISO channel after a horrible experience with Pay-Per-Click.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

On one industry forum, ISOs have reported that the cost of acquiring a merchant cash advance or business loan deal from Pay-Per-Click is ranging from $700 to $1,200. “PPC for premium keywords as high as $40 at times. Ugly. Real ugly,” one user wrote. Another user wrote, “It’s not just Adwords that is saturated. The whole market is saturated. Lenders and the onslaught of new brokers are making it tough. Lenders with programs like Funding Circle and Kabbage, and with all the advertising money in the world to burn and get direct traffic.” And still another believes that online ads are simply inviting the lowest hanging fruit. “Internet leads have the highest level of fraud,” said one sales manager.

Notably, many of the top 8 funders are only competing for a limited number of competitive keywords or may not even be running Adwords at all. PayPal and Square for example, focus only on their existing payment processing customers despite being “online lenders.”

It’s too early to tell what effects Google’s ad changes will have on the online lending industry, though a couple of companies who were paying just enough to extract clicks from side ads have indicated the change is for the worse and they have suspended their campaigns.

The natural alternative to paid search, organic search, is seldom discussed anymore as a realistic strategy these days, in part because the rankings might be rigged anyway.

One irony that’s pervasive in the online lending industry is that borrowers are being targeted offline where it’s potentially more affordable. In a discussion thread that garnered 76 posts last fall, ISOs and funders suggested that direct mail, referrals, UCCs, cold calling, radio and even going out and shaking hands, were pegged as “what’s next” for marketing. Pay-Per-Click was only mentioned once and only in the context of it being something that had long ago been made too expensive for small and mid-size companies.

The cost of making these things work might be why so many funders are hoping that brokers can figure it out. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” said Nulook Capital’s Jordan Feinstein in an interview with AltFinanceDaily last month.

With Google becoming even more competitive now though, perhaps United Capital Source’s Jared Weitz summed it up best. “Marketing is getting more expensive and only the ones who can afford to pay can play,” Weitz said.

Bizfi Woos Restaurants With Lending Products

March 3, 2016The New York State Restaurant Association signed Bizfi to provide business financing for its 2,000 members.

The New York-based financial platform will be the designated funder of equipment financing, invoice financing, lines of credit, medium term financing, short-term financing, franchise financing and long-term loans from more than 45 partners.

“Restaurants have unique funding needs and owners often do not have time to spare in order to complete the long application process at traditional lenders,” said Stephen Sheinbaum, founder of Bizfi.

Bizfi’s lending partners include all the major lenders in the industry including OnDeck, Funding Circle, Kabbage, IMCA Capital, Bluevine, and SmartBiz and the company has funded over $1.4 to over 27,000 small businesses since 2005.

![]()

No, Social Media isn’t the New Credit Score

February 25, 2016 The “social media is the new FICO score” crowd suffered a blow on Wednesday when a Wall Street Journal article reported that it ain’t working too good.

The “social media is the new FICO score” crowd suffered a blow on Wednesday when a Wall Street Journal article reported that it ain’t working too good.

Almost 3 years ago, Kabbage co-founder Marc Gorlin told CNN that small businesses who link up their facebook and twitter accounts up with their system, were 20% less likely to be delinquent on their loans. Around that time, Hong Kong-based Lenddo was heralding other positive claims about the value of social media. In the loans they made in Colombia and the Philippines for example, Slate reported that “they scrutinized the applicants’ connections on Facebook and Twitter and that the key to getting a successful loan from Lenddo was having a handful of highly trusted individuals in your social networks.”

For a time, non-bank lenders were saying that social media was the future of credit. That is until it wasn’t.

The WSJ recently reported that lenders are backing away from social media data because it’s becoming harder to tap into and because of the potential regulatory consequences under fair credit laws. Just last month for example, the FTC published a report titled, Big Data, A Tool for Inclusion or Exclusion? In it, the FTC warned that “if a company targets services to consumers who communicate through an application or social media, they may be neglecting populations that are not as tech-savvy.” The implication is that there is potential for unconscious and unintended discrimination of certain minority groups. “Systemic disparate treatment occurs when an entity engages in a pattern or practice of differential treatment on a prohibited basis. In some cases, the unlawful differential treatment could be based on big data analytics.”

But even then, companies like Kabbage have seemingly softened their stance on the value of social media anyway. “Who your social circle is, or whether you play ‘Mafia Wars’—we haven’t seen that as very valuable,” Kabbage CEO Rob Frohwein said to the WSJ.

Facebook is restricting the depth of data available to third parties now anyway. As a result, dozens of startups (not just lenders) that had been using Facebook data have shut down, according to the WSJ.

Lenders like OnDeck might not be surprised by the industry’s sudden realization. Two years ago at LendIt 2014, company CEO Noah Breslow said you have to be careful with the noise of social media as there can be a lot of false signals. And RapidAdvance COO Joe Looney was already telling CNBC three years ago that his company was “not going to make a decision based solely on a string of online comments on a social-media site” even though they would consider the mere presence of an active social-media footprint to be a “good sign.”

It looks like the future of credit scoring isn’t likely to be social media any time soon. All hail the fundamentals.