i2B Capital Provides $4 Million Revolving Line of Credit to CFG Merchant Solutions

November 8, 2016NEW YORK–(BUSINESS WIRE)–i2B Capital (www.i2bcap.com), a provider of direct financing to niche-market financial entrepreneurs, is pleased to announce the closing of a $4 million asset-based revolving line of credit with an accordion to $6 million with CFG Merchant Solutions (CFGMS). CFGMS is a privately owned and operated specialty finance company focused on providing working capital to small and mid-sized businesses (Merchants) in the U.S. that are historically underserved by traditional financial institutions.

Said Mr. Larry L. Curran II, CEO of i2B Capital, “CFGMS gave us the perfect opportunity to apply asset-based lending principals to non-traditional receivable assets in an early stage specialty finance company. CFGMS is a new division of an established finance business with traditional bank financing; however, these receivable assets were excluded from the existing borrowing base. The CFGMS management team is seasoned, backed by private equity, and enabled with technology—exactly what we look for in our target customer. Additionally, they have grown their financed receivables more than 500% since beginning the process.”

Barbara Anderson, Chief Operating Officer at i2B Capital commented, “Our goal over the initial 18-month funding commitment is to prepare CFGMS for more traditional institutional financing in the future. To accomplish that we will provide the growth capital along with our commercial lending expertise to help them prepare for the disciplined reporting requirements and credit processes at the next level.”

William Gallagher, President of CFGMS said, “Obtaining an asset-based loan against our non-traditional asset class within our first year of operation is instrumental in allowing us to execute on our growth strategy, and achieve some very aggressive portfolio and revenue targets. We had to work through several considerations with i2B due to the age and size of the portfolio, but through mutual collaboration we were able to put in place a facility that will enable us to take our business to the next level.”

CFGMS is a subsidiary of CapFlow Funding Group, a commercial finance company that offers an array of products such as factoring, purchase order finance, and asset-based loans. Both companies are headquartered in Rutherford, New Jersey. CFGMS with additional offices in New York City is a direct funder providing working capital to small businesses. They are entrepreneurs who understand first-hand the challenges of acquiring flexible and timely financing. CFGMS combines proprietary analytics and technology, with common sense underwriting to provide fast and efficient access to capital. Programs include Small Business Advance, Merchant Cash Advance, and Invoice Factoring. For more information about CFGMS contact William Gallagher at wgallagher@cfgms.com or visit www.cfgmerchantsolutions.com.

i2B Capital is headquartered in Fort Collins, Colorado with offices in Herndon, Virginia. The company provides senior debt and direct asset investments for growth capital to qualifying entrepreneurs and equity-backed emerging specialty finance companies throughout the United States. For more information about i2B Capital contact Barbara Anderson at 703-871-3993 or banderson@i2bcap.com, or visit www.i2bcap.com.

Contacts

i2B Capital

Barbara Anderson, 703-871-3993

banderson@i2bcap.com

Everlasting Capital Appoints Director of Equipment Finance & Leasing

October 24, 2016 New Hampshire, October 21, 2016 – Everlasting Capital (www.Everlastingcapital.com) announced today that Dan Marquette has joined the team to further develop their growing portfolio of national equipment vendor and direct client accounts. Dan Marquette comes with a wealth of experience within the industry, having spent the last 5 years in the Equipment Finance & Leasing industry where Dan was instrumental in acquiring numerous strategic vendor relationships, along with numerous Investor relationships. Joining in advance of the expected growth of Everlasting Capital’s Equipment Finance & Leasing product, Dan can continue in his success.

New Hampshire, October 21, 2016 – Everlasting Capital (www.Everlastingcapital.com) announced today that Dan Marquette has joined the team to further develop their growing portfolio of national equipment vendor and direct client accounts. Dan Marquette comes with a wealth of experience within the industry, having spent the last 5 years in the Equipment Finance & Leasing industry where Dan was instrumental in acquiring numerous strategic vendor relationships, along with numerous Investor relationships. Joining in advance of the expected growth of Everlasting Capital’s Equipment Finance & Leasing product, Dan can continue in his success.

Dan joins Everlasting Capital as Director of Equipment Finance & Leasing to continue Everlasting Capitals continued success capturing larger market share providing business financing options to the national SMB market. Dan Comments “My goal as Commercial Equipment Director with Everlasting is to levy the outstanding talent within the organization’s equipment vertical, to increase our strategic partnerships throughout the Vendor, Franchise and Broker space. Ultimately, working in conjunction with our CEO to improve process, product diversification and day-to-day production efficiencies. I couldn’t be more excited about being a part of such a dynamic commercial finance organization.”

Josh Feinberg, President/CEO said “Dan’s wealth of experience and industry knowledge has already made him a key addition to the Everlasting Capital family. We view his appointment as a sign of our commitment to being the leading company is our industry. Our new innovations and the increasing demand from our customer led us to look for an addition to our team who will fit in with our ethos of innovation and exceptional service, and it is very fortunate that we could find someone of Dan’s Caliber to fulfill this role. I’m confident that Dan will play a key role in providing and implementing high quality solutions for our clients”

About Everlasting Capital

Everlasting Capital is a national business finance solutions provider(www.everlastingcapital.com), redefining lending and financing by consistently providing outstanding customer experiences and innovative, world- class services with creative financing options.

Contact

Everlasting Capital

Dan Marquette

603-471-3282 Dmarquette@everlastingcapital.com

A Glimpse into Square Capital’s Marketing

October 20, 2016As a merchant, Square has marketed their Square Capital program to me before. But this is the first time I’ve received direct mail marketing from them. Here’s a snapshot of what that looks like:

To view the potential offers, merchants are directed to log in to their Square accounts where they will see multiple terms. Even though their particular product is a loan made possible through Celtic Bank, all of the proposed loan offers are presented using the Total Cost of Capital method. That means cost is disclosed as a precise dollar amount so that potential borrowers will know exactly how much they will have to pay. Several studies have indicated that this is the easiest to understand, though it has been subject to some debate.

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

One of the defining features that makes Square Capital’s loan product different from a merchant cash advance or a purchase of future sales, is that Square enforces a fixed 18 month term. “If the loan hasn’t been repaid in full at the end of 18 months, the remaining loan balance will be due in full,” they state. That is completely unlike a purchase transaction in which there is no deadline or term. Even MCA purchase transactions that stipulate fixed daily payments do not actually have fixed terms. That’s usually because if a merchant’s sales activity rises or falls, they have the contractual right to request an adjustment to those payments to effectuate the basis of the agreement, that future sales be delivered in accordance with the unpredictable ebb and flow of business. That makes the date in which delivery will be satisfied in full unknowable. It’s that unknowable that can cause MCA transactions to be more expensive than their loan counterparts, though that is absolutely not always the case.

For Square, unknowable contract satisfaction dates likely made it difficult to bundle these deals up to sell off to institutional investors. Square Capital head Jackie Reses articulated this challenge during her appearance on an April 2016 LendIt stage. “From an investor side, that’s really where the savings are between the form of an MCA and the form of a loan, in that there’s an actual repayment date,” she said.

Even institutional investors recognize and understand that MCA purchase agreements do not have fixed terms.

Merchant Cash Advance Misinformation Abounds – What’s A Broker To Think?

October 10, 2016

Last week, at least two panelists at the major commercial loan broker conference critiqued merchant cash advances, even going so far as to assign an arbitrary cost to them. Craig McGrain, President of factoring company Durham Funding, said they cost about 75%. Bob Coleman, owner of The Coleman Report, an SBA loan journal, said that merchant cash advance contracts should stipulate that prices are basically equivalent to 100% APR. Neither accurately describes a merchant cash advance if for no other reason than because a merchant cash advance is merely a methodology or a mechanism, not a price. The term itself is derived from the process of making a merchant an advance on their future projected sales. With hundreds of companies employing that concept, some are able to do it at a low cost and others at a high cost.

And it’s obviously the high cost ones to which their disdain was directed. But even then, when MCAs are properly structured as a purchase of future sales, there is no calculable APR because there is no assigned time frame, predetermined payments, or interest rate. This doesn’t mean an MCA product can’t be expensive, because surely they can be, but assigning randomly high percentages to scare people only compounds the misinformation that has persisted for years.

On a panel I participated in with Bob Coleman, Coleman said that these purchases were really just loans. The New York Supreme Court, however, repeatedly disagrees with him. In Platinum Rapid Funding Group Ltd v. VIP Limousine Services, Inc. and Charles Cotton, the court affirmed a purchase of future receivables for an upfront payment, adding that the request for the Court to convert the Agreement to a loan and assign an interest rate to it would require unwarranted speculation, and would contradict the explicit terms of the sale of future receivables in accordance with the Merchant Agreement.

In Merchant Cash & Capital, LLC v G&E Asian Am. Enter., Inc., the court reached the same conclusion.

With regard to McGrain of Durham Funding, he said that 70%-80% of companies that apply for his company’s factoring services have already used an MCA. This kind of competitive pressure is probably a leading reason why a factor would mischaracterize MCAs. In fact, the factoring industry has felt so threatened by MCAs, that two years ago the International Factoring Association voted to ban all MCA companies from their organization.

This isn’t to suggest that factoring is an inferior product and that MCA is the newer better thing. On the contrary, factoring is an excellent loan alternative and to McGrain’s credit he said that he believed the free market would work everything out. To facilitate that, more MCA brokers need to be educated on factoring and SBA lending. And in return commercial finance brokers need to understand the true nuts and bolts of MCA. That process gets sullied when misinformation abounds. Merchants will get the best help when the brokers fully understand all of the market’s options.

My panel with SBA lending expert Bob Coleman and equipment leasing veteran Kit Menkin at the NACLB conference last week highlighted some differences of opinions across these closely related industries but also demonstrated areas in which we all agree. Small businesses have different needs and it’s up to the brokers to prescribe the most appropriate solution. Whether it’s short-term or long-term, cheap or expensive, proactive or reactive, there’s capital out there. Hopefully the kind of cooperative engagement the NACLB conference provided this year will continue to be fostered for years to come.

Square Capital Revs Up, Funds $189M to Small Biz in Q2

August 4, 2016

Square is proving that the business loan sector is still hot, especially since their payment processing ecosystem requires nearly no marketing budget to advertise Square Capital. With $189 million funded in Q2, a growth of 123% year-over-year, their shift from merchant cash advances to loans seems to have had the desired effect since they have attracted even more investors willing to buy them.

“We sell a majority of our loans to third-party investors for an upfront fee and a small ongoing servicing fee. In addition, we continue to have a strong continued pipeline of interested investors,” the company said in its earnings report.

The average loan size remains small, only $6,000, but ranges from $1,000 to $100,000. Square CFO Sarah Friar, said during the earnings call that their data shows an overall increase in the gross payment volume of merchants who use their loans, which indicates that borrowers are indeed using the funds to grow their businesses.

A typical Square Capital loan is close to 10% of a seller’s annual processing sales and the average repayment term is 9 months. Loss rates remained steady at 4%.

Friar also said that PayPal Working Capital and American Express Working Capital were not really competition since they are working directly with their own existing user base.

The company made about 34,000 loans in Q2.

Square Capital Has No Borrower Acquisition Costs, Hints at Making Loans to Non-Square Users

May 8, 2016

As the marketplace lending industry frets over acquisition costs, one lender is sitting pretty, Square. That’s because they source their borrowers from their existing payment processing ecosystem. Square CFO Sarah Friar said on their earnings call last week that it was one of the big advantages they had with investors looking to buy loans. “We’re not having to go out and it’s not costing us more to do customer acquisition because it doesn’t cost us anything. We’ve already acquired them,” she said. Compare that to OnDeck who spent $16.5 million in Q1 to acquire borrowers through sales and marketing.

Also on the call, Friar did reveal one benefit of having switched from a merchant cash advance product to a loan product that didn’t have anything to do with investors, and that’s being able to handle clients who want to satisfy the balance in full or obtain additional funds. Since no interest accrues with traditional merchant cash advances, there are no presumed discounts if you want to repurchase your sold receivables. Early repayments were apparently the number one request they received from their clients.

It’s not clear exactly what Square did previously when merchants wanted to “repay early,” but there are other merchant cash advance companies that will allow clients to repurchase back their sold receivables at a slightly discounted price if it’s relatively soon after the original transaction occurred. Either way, Friar said that the shift from MCA to loan hadn’t changed the level of demand.

Notably, while not even directly asked, Friar also said that they are also continuing to look into making loans to non-Square users, perhaps through other card processors.

Online Lending APR ‘SMART Box’ To Apply To Loans, Not Merchant Cash Advances

May 5, 2016

OnDeck, Kabbage and CAN Capital have launched an initiative to make online loan shopping easier. Dubbed the SMART (Straightforward Metrics Around Rate and Total Cost) Box, these lenders plan to present small businesses “with a chart of standardized pricing comparison tools and explanations, including various total dollar cost and annual percentage rate metrics that enable a comprehensive pricing comparison of loans of equivalent duration.”

The Box, clearly meant to increase transparency, was explained in an ironically confusing way, particularly where it said it would include annual percentage rate metrics. An Annual Percentage Rate (APR) is indeed a representation of several metrics and thus it wasn’t clear if the Box would just include some of these individual metrics and conveniently leave out the APR itself.

OnDeck CEO Noah Breslow for example told Forbes only six months ago that annual terms don’t make sense. “The APR overstates the actual cost of the loan to the borrower,” he said. He was not alone in thinking that way. Several studies have concluded too that merchants don’t always even know what APR represents. Lendio for example, found that two-thirds of small businesses selected the total dollar cost of a loan as the easiest to understand. Only 17.4% said the APR was the easiest.

And there’s another thing, the fact that CAN doesn’t just do loans, they also do a significant amount of merchant cash advances. What role could an APR have there? While the Box’s final system won’t be decided until after the conclusion of a 90-day national engagement period that begins next month, one can only imagine that it might have a Schumer Boxer feel to it.

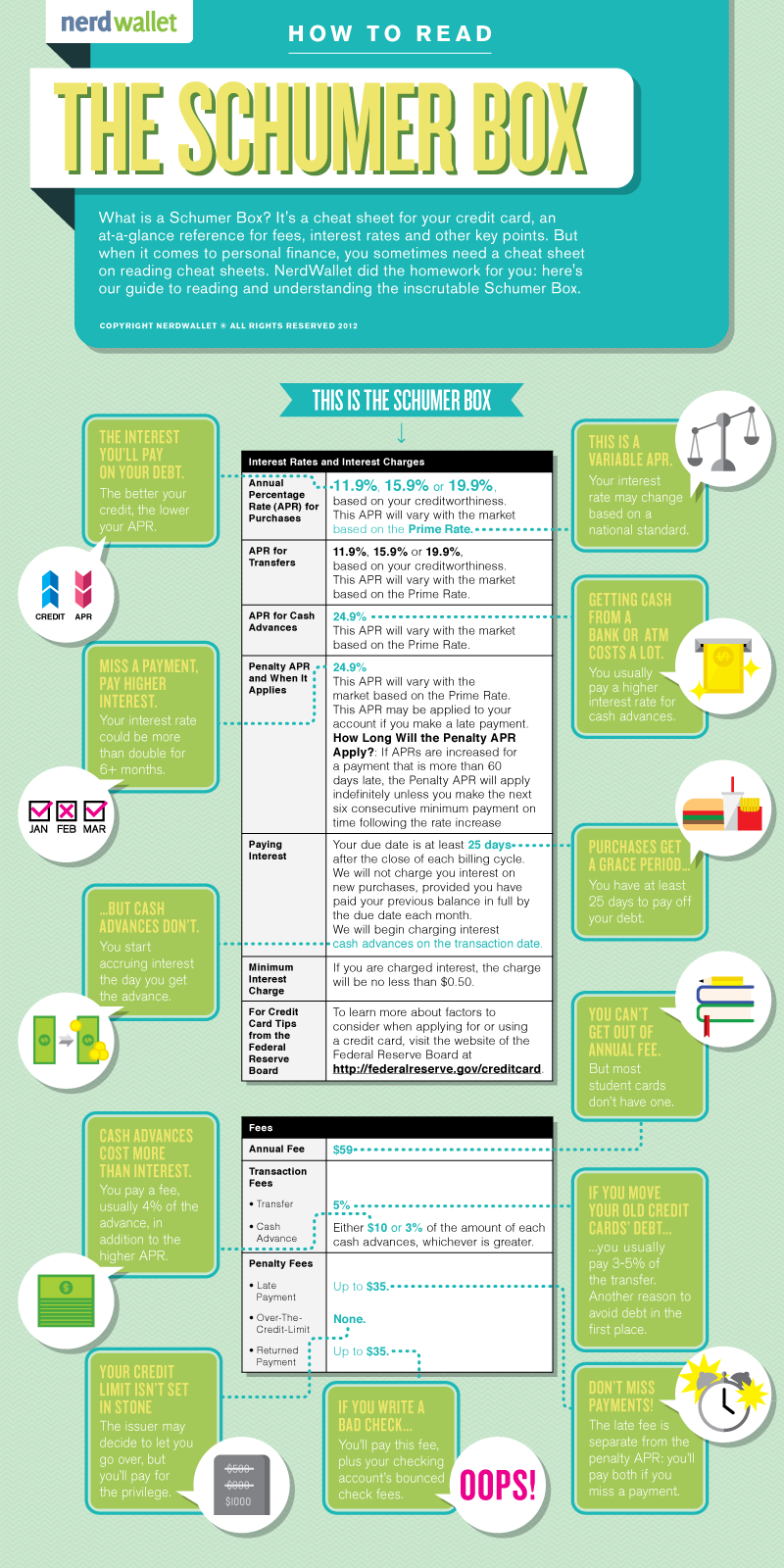

A Schumer Box explained:

Via: NerdWallet

The syntactic ambiguity in the announcement however was unintentional. A spokesperson for the group (Known as the Innovative Lending Platform Association) said that the SMART Box will indeed include Annual Percentage Rates.

But that’s where loans are concerned…

When AltFinanceDaily asked about merchant cash advances, Daniel Gorfine, vice president and associate general counsel of OnDeck; Parris Sanz, Chief Legal Officer of CAN Capital and Azba Habib, assistant general counsel of Kabbage, submitted the following joint response:

“As part of the SMART Box initiative, we are interested in engaging with providers of MCA products. Based on consistent assumptions about a small business’s future sales volumes and its ability to deliver the contracted amount of receivables within the period of time estimated during underwriting, the SMART Box could apply to MCA products.”

So long as SMART Box disclosure is voluntary, an MCA company could perhaps employ their own version of it. It just might come sans APR given the product’s history with state regulations. The Association is emphatic however that this concept could be used by MCA companies and others in the small business financing space. After all, the initiative is rooted in transparency for the small business owner, they say.

In September, the Association “will encourage those interested in promoting the responsible development of the small business lending industry to voluntarily adopt or support the model disclosure.”

Given the level of influence these companies have on the industry, the voluntary nature of the SMART Box has the potential to spark an industry-wide box revolution. MCA companies however would need to structure transparent disclosure around their contractual frameworks. But even that could be a good thing. One commercial financing broker for example, posted a redacted service fee agreement to the DailyFunder forum earlier this week that purported to show another broker trying to charge a merchant a 26% premium (26% of the funding amount) for their work. Despite this unusually high cost, the charge itself was hard to find, hidden among fine print on an otherwise benign looking page. Naturally, others in the industry did not respond kindly to it. Even other brokers referred to it as “outrageous,” “nonsense,” or “bs.”

Their reactions make clear that there is a desire for transparency even among the group most often blamed for the lack thereof. Some of the industry’s forward thinkers have told AltFinanceDaily that a system like a SMART Box is the future of the industry whether one agrees with it or not. And if not for the sake of small businesses and regulators, then for the sake of being able to compete fairly against companies that may be relying on truly hidden fees.

SMART Box. All aboard the transparency train?

Square Capital’s Default Rate is 4%

May 5, 2016

Square revealed today that its Square Capital division had extended $153 million through more than 23,000 advances and loans in the first quarter. The company is still transitioning from merchant cash advances to loans to appease institutional investors. This was not only said at LendIt by Jackie Reses but also reiterated in their Q1 earnings report. “We believe that the transition to a loan product further increases our ability to attract new Square Capital investors,” it said.

Their default rate continued to hover at 4%.

That number is shockingly low considering that under a pure merchant cash advance model they did not conduct credit checks, nor did even they review bank statements or tax returns. Rather the company relied almost entirely on a merchant’s sales history with Square.

This process may have made funding easy but was potentially a hard sell to regulators. As part of their transition to a lending model, all applicants are now subject to a credit approval and have to supply identifying documents. Square also bought an analytics startup less than two months ago to help them make more informed underwriting decisions. This can only mean that if their default rate was 4% with no underwriting, their prowess as a lender will likely increase considerably.